DPC The Arcade, Cleveland 1901

Chinese are highest ever, one would think.

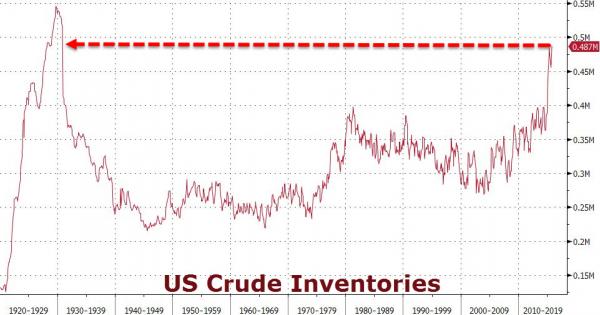

• US Crude Inventories Are The Highest Since the 1930s (ZH)

In case you were under the impression that oil was stabilizing, we thought this chart might help clarify just how “different” it is this time in the energy complex… U.S. crude inventories are at levels last seen when President Herbert Hoover was battling the Great Depression.

After this week’s build – Crude stockpiles climbed 8.38 million barrels to 494.9 million in the week ended Jan. 22, the highest since November 1930, according to weekly and monthly data from the Energy Information Administration. It did not end well last time…

It’ll get cheaper though.

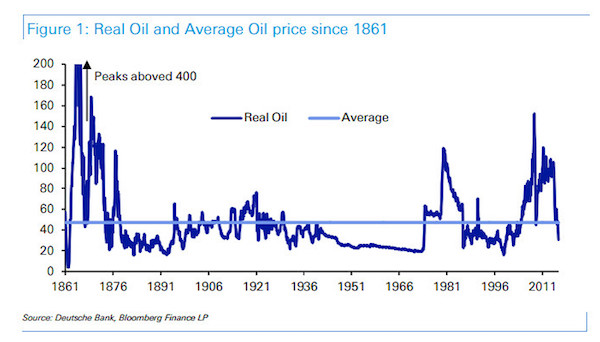

• Chart Going Back To 1861 Shows Oil Isn’t Insanely Cheap Right Now (MW)

Oil futures are hovering around $30 a barrel—not far off 12-year lows—and bears are penciling in a test of $20 or lower. It is a pretty downbeat picture, but is black gold really that cheap on a historical basis? Not really, according to the chart from Deutsche Bank, which tracks inflation-adjusted oil prices—and the average price—all the way back to 1861, just two years after Edwin Drake drilled the first productive U.S. oil well near Titusville, Pa. Over the last 150-plus years, the average oil price is $47 a barrel, according to the data. West Texas Intermediate oil futures for March delivery were down 22 cents, or 0.7%, at $31.23 a barrel in late morning trade. “So current levels are low but not exceptionally low relative to long-term history,” said Jim Reid, macro strategist at Deutsche Bank, in a Wednesday note.

The charts were published as part of an annual study by the investment bank. Interestingly, Reid did note that this was the first year that the firm’s long-term mean reversion exercise shows positive return expectations for oil since the study began more than a decade ago. But don’t get too excited over prospects for an immediate mean-reversion rally. Reid puts the findings in the context of the commodity cycle, which is on the downswing after a sharp run-up that began in the mid-1990s. He notes the “long-held belief” that commodities, such as oil, that are a factor of production can’t outstrip inflation over the long term because “if they do there will be alternatives found.”

That helps to explain oil’s pullback. This process, however, “can take years to resolve, so even if we’re correct, commodity cycles can still last a long time before they eventually mean revert,” he wrote. Meanwhile, the graph “doesn’t suggest that current levels are as extreme as many would suggest even if long term value has returned,” Reid said. “The $140 prices a few years back look especially bubble-like” from a long-term perspective.

Fed’s done.

• Why the Fed Has the Stock Market Spooked (WSJ)

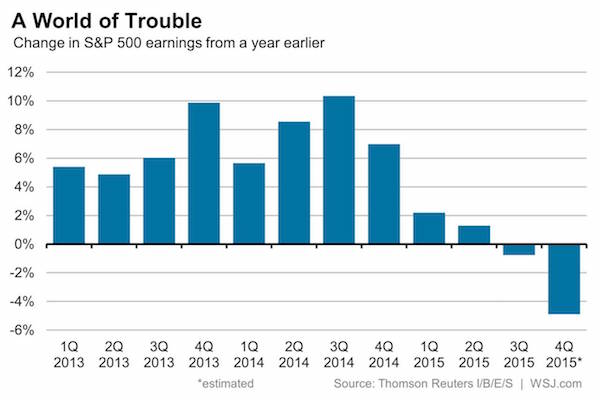

Investors have grown accustomed to getting help from the Federal Reserve. But in a world where American companies are tethered less tightly to the U.S. economy, that help may not be so forthcoming. The Fed on Wednesday said economic data had softened since it decided to raise rates in December, and that policy makers were “closely monitoring global economic and financial developments.” But they didn’t send a clear signal that many investors were hoping for: that they would forgo raising rates at their March meeting. Stocks, which had been higher ahead of the Fed’s postmeeting statement, fell. One reason the prospect of further rate rises is jarring to investors is that they would come at an unusual and unfortunate time. While rate increases usually arrive when profits are growing solidly, they are now shrinking.

That this hasn’t chastened the Fed may reflect the growing role in U.S. companies’ results of operations outside the U.S. So falling profits simply aren’t the clear indication of U.S. economic vulnerability that they once were. As companies continue to report fourth-quarter earnings, the decline in profits is something investors are acutely aware of. With about one-quarter of results from the index’s constituent companies now in, S&P 500 earnings look to have fallen by 4.9% in the fourth quarter from a year earlier, according to Thomson Reuters. This follows a 0.8% decline in the third quarter. That marked the first drop since the deep profits recession that ended in 2009. To be sure, the collapse in energy-sector earnings plays a big role. But excluding them, profits would be up just 1.3%.

Moreover, ignoring a sector because it is doing poorly—energy now, financials during the crisis, technology after the dot-com bust—risks sugarcoating the situation. Even if it weren’t for all the other things unsettling investors now—dollar debt and commodity market woes, emerging market outflows, concerns over the U.S. economy’s ability to grow in a troubled world—the combination of Fed tightening and falling profits would be worrisome. After all, points out Richard Bernstein Advisors portfolio strategist Joe Zidle, the two variables investors care most about when valuing stocks are profits and interest rates. When, as now, they both are headed the wrong way, it is a recipe for trouble. It also is a recipe that is exceedingly rare. The only other time that Mr. Zidle and his colleagues have identified where the Fed raised rates during a profits recession was in the early 1980s. That was when the central bank was moving to snuff exceedingly high inflation.

“Margin calls and deleveraging is being talked about more and more..”

• China Shares Flounder Again, But ‘Real Economy’ Sound Says State Media (Reuters)

China’s volatile shares tumbled again on Thursday, taking losses this month to about 25% or 13 trillion yuan ($2 trillion), while state media insisted that the market ructions did not reflect the real economy. The benchmark Shanghai Composite Index ended down 2.9%, and the CSI300 index of the largest listed companies in Shanghai and Shenzhen shed 2.6%, both indexes having tumbled this week to levels not seen since 2014. Trading was very light, as many investors have given up on Chinese stocks, burnt by last summer’s 40% crash and a hair-raising January that has taken indexes back to late 2014 levels.

“The majority of equity investors we met over a four-day marketing trip in ASEAN last week had trimmed exposure to China equities by varying degrees and were waiting for signs of stabilisation for potential re-entry,” said Japanese broker Nomura. January began with sharp falls in Chinese stocks and a depreciation in the yuan currency, and the sell-off hasn’t abated as economic data confirmed slowing growth and deteriorating business conditions. As the markets keep falling, the prospect of investors being forced to sell stocks bought with borrowed money to cover margin calls has hurt sentiment further. “Margin calls and delveraging is being talked about more and more in a market extremely bearish about China’s economy and the yuan’s value,” said Wang Yu, analyst at Pacific Securities.

Control P.

• China’s Central Bank Makes Most Massive Cash Infusion In 3 Years (WSJ)

China’s central bank is putting the largest amount of cash into the financial system in nearly three years, using a weekly market operation to pre-empt a holiday-induced funding squeeze and offset rapid capital outflows. The People’s Bank of China offered 340 billion yuan ($51.89 billion) of short-term loans, known as reverse repurchase agreements, to commercial banks in a routine money market operation Thursday. The central bank provided 440 billion yuan via similar tools Tuesday, the first leg of its twice-a-week liquidity-management exercises.

Given the maturity of 190 billion yuan of previously issued loans, the PBOC’s net cash injection this week totals 590 billion yuan, the biggest of its kind since early February 2013, when it reached 662 billion yuan. The move follows an aggressive pump-priming exercise by the PBOC last week, when the central bank offered more than 1.5 trillion yuan in gross short- and medium-term lending to banks. The eye-popping liquidity injection is partly intended to satisfy typically surging demand for cash ahead of the Lunar New Year holiday that starts Feb. 7. It also constitutes an effort to stem accelerating capital flight as investors become more nervous about the health of China’s economy, and as the country’s main stock market has lost nearly 23% since the start of this year.

“The last time central bank Gov. Zhou Xiaochuan spoke publicly was in early September..”

• China Sharpens Efforts to Halt Money Outflow (WSJ)

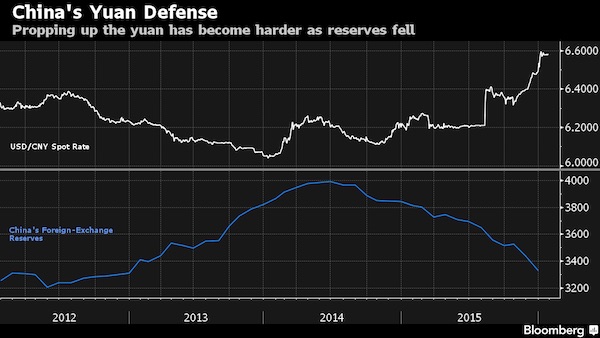

China is ramping up efforts to halt a flood of money leaving the country in response to an economic slowdown, moves that risk undermining Beijing’s ambition to elevate the yuan’s profile on the world stage. Its latest steps involve curbing the ability of foreign companies in China to repatriate earnings, shrinking the pool of Chinese yuan available for banks in Hong Kong to make loans, and banning yuan-based funds for overseas investments, people with direct knowledge of the matter said. The measures, most of which haven’t been publicly disclosed, follow efforts by China’s central bank to discourage investors from betting against the yuan and to crack down on overseas money transfers. “They’re sparing no effort to prevent capital outflows,” said a senior Chinese banking executive close to the central bank.

“All the measures are the most aggressive I’ve seen in recent history.” The people with direct knowledge said the People’s Bank of China, the central bank, also is considering ways to lure money back to the country, including letting foreign residents and companies buy certificates of deposit for fixed periods. Currently they are restricted to ordinary deposit accounts. The unusual moves come as China burns through foreign-exchange reserves to prop up its currency and stem an increasingly vicious cycle of easing credit, a weakening currency and fleeing capital. Too much outflow, Chinese officials say, could threaten the stability of the country’s financial system. Just two months ago, the IMF’s designated the yuan as one of the world’s reserve currencies, a nod to China as a global economic power.

Still, Beijing is now retreating from its pledges to give markets more influence in setting the yuan’s value. Many investors say they are also concerned over what they consider to be inadequate communication by the central bank. The last time central bank Gov. Zhou Xiaochuan spoke publicly was in early September, when he sought to reassure central bankers and finance ministers from the Group of 20 large economies that the rout in China’s stock markets was nearing an end. Investors and analysts have questioned the government’s commitment to market liberalization following Beijing’s attempts to prop up the stock market this past summer and, more recently, sending mixed signals over yuan policy. “China is aggressively reinserting capital controls,” said Scott Kennedy at Center for Strategic & International Studies in Washington. “It appears China has for the foreseeable future given up on the goal of substantial exchange-rate liberalization.”

“I’m not expecting it, I’m observing it..” See, Ambrose wants the cake and eat it. All’s fine, but at the same time “It is stimulus as usual. The Politburo is back to its bad old ways.” It’s all fake, that’s the problem: “credit growth continues to expand far more rapidly than GDP growth..”

• Hysteria Over China Has Become Ridiculous (AEP)

Hysteria over China has reached the point of collective madness. Forecaster Nouriel Roubini said in Davos that markets have swung from fawning adulation of the Chinese policy elites to near revulsion within a space of 12 months, and they have done so based on scant knowledge and a string of misunderstandings. The Chinese themselves are being swept up by the swirling emotions. State media has accused hedge fund veteran George Soros in front page editorials of attempting to smash China’s currency regime by “reckless speculation and vicious shorting”. “Soros’s war on the renminbi cannot possibly succeed – about this there can be no doubt,” warned the People’s Daily. Articles are appearing across the world debating whether Mr Soros and his putative wolf pack will succeed in doing to the People’s Bank of China (PBOC) what he did to the Bank of England in 1992 – in the latter case with entirely positive consequences.

In fact, Mr Soros issued no such “declaration of war”, and nor is he so foolish as to take on a foreign exchange superpower and net global creditor with $3.3 trillion in foreign reserves. As it happens, I was at the dinner at the Hotel Seehof in Davos – drinking white Rioja – where Mr Soros supposedly revealed his plot. What he did let slip is that he had been shorting some Asian currencies – the Malaysian Ringitt or the Thai Baht, perhaps, out of nostalgia for the 1998 crisis. Mr Soros made general comments, claiming that credit in China has reached 350pc of GDP and that the hard landing is already happening. “I’m not expecting it, I’m observing it,” he said. The observations were boilerplate, what are called “tourist” insights in hedge fund parlance. He is not a player in China. So let us return to reality. The economic facts are in plain view. China is not slowing. It is picking itself up slowly after a “recession” in early 2015.

Car sales give us a steer. They collapsed early last year and touched bottom at 1.27m in July. Sales have been rising every month since, surging to a record 2.44m in December thanks to lower taxes. New registrations were up by 37pc for GM and 36pc for Ford and Mercedes. House prices have been climbing for three months. The nationwide index was up 1.6pc in December. Shanghai rose 15.5pc and Shenzhen 47pc. Even the “Tier 3 and 4” cities are coming back from an epic glut. The economy did indeed hit a brick wall early last year due to a fiscal shock and ferocious monetary tightening (passive) in late 2014. That was the time to lambast the Chinese authorities for errors of judgment, and some of us did so. Capital Economics estimates that growth slowed to 4pc based on its proxy indicator, and others broadly concur.

These indicators are not derived from the now useless “Li Keqiang index” of rail freight, electricity use and credit growth, which overstate the slowdown. Growth of total freight traffic has risen to 5.4pc from 3.5pc in June. That is a plausible gauge of what is really happening. A short-term economic rebound is already baked into the pie. Fiscal spending jumped 30pc in October and November. New bank loans and local government bond issuance – together, the proper measure of credit – reached a 12-month high of 14.4pc in December. It is stimulus as usual. The Politburo is back to its bad old ways. “Despite talk of deleveraging, credit growth continues to expand far more rapidly than GDP growth because, quite simply, they are not willing to tolerate any slowdown,” said Prof Christopher Balding from Peking University.

“They have to reassure local savers and show them a willingness that the government is looking after them and their savings.”

• Yuan Bears Denounced as Delusional, Doomed by China State Media (BBG)

China’s leading state media are becoming more vociferous in their support for the yuan, having been fired up in the past week by George Soros’s observation that the economy is headed for a hard landing. Yuan short sellers “haven’t done their homework,” the state-run Xinhua News Agency said in an English-language article on Wednesday, while a People’s Daily commentary in Chinese declared that such trades will undoubtedly fail. The two editorials, in addition to at least three other articles published by Xinhua since the weekend, all argue the economy is growing at a decent pace. China is resorting to stepped-up rhetoric to help offset depreciation expectations after the yuan started the new year with the biggest weekly plunge since a devaluation in August.

The cost of steadying the exchange rate has shot up as a slowing economy, equity market turmoil, declining foreign-exchange reserves and surging capital outflows add to the pessimism. “They can write as many op-eds as they want, but two plus two doesn’t make five,” said Michael Every at Rabobank Group in Hong Kong, whose year-end 7.53 forecast for the yuan against the dollar is the most bearish in a Bloomberg survey of 41 analysts. “What they’re saying won’t put off speculators. The fundamentals are screaming and sending a clear picture that if economic growth doesn’t start picking up, the exchange rate will weaken.”

Soros said in Davos that he’s been betting against Asian currencies because a hard landing in China is “practically unavoidable.” Xinhua retorted by saying that his observations are the result of “partial blindness.” The billionaire investor rose to fame as the money manager who broke the Bank of England in 1992, netting a profit of $1 billion with a wager that the U.K. would be forced to devalue the pound. Malaysian Prime Minister Mahathir Mohamad called him a “moron” during the 1997 Asian financial crisis, saying he was out to wreck the region’s economies. “Given how people know Soros and what he did in 1992 and during the 1997-1998 Asian crisis, he’s too important to ignore, so China felt that they had to counter any negative comments,” said Tommy Xie at Oversea-Chinese Banking, who was cited by Xinhua as saying that the People’s Bank of China has become more predictable. “They have to reassure local savers and show them a willingness that the government is looking after them and their savings.”

“..the prospect of investors having to sell stocks they bought with borrowed money in order to cover margin calls has also hurt sentiment.”

• China’s 2016 Stock Losses Rise To $1.8 Trillion (Reuters)

Chinese highly volatile shares ended lower again on Wednesday after plunging on Tuesday, taking losses in 2016 to about 22% or 12 trillion yuan ($1.8 trillion). The benchmark Shanghai Composite Index ended down 0.5%, having been up in the morning and as much as 4% lower during the day. It tumbled 6.4% on Tuesday to its lowest close since Dec. 1, 2014. The CSI300 index of the largest listed companies in Shanghai and Shenzhen ended down 0.3% after a similar rollercoaster ride. China markets began the year with a series of precipitous falls and a sharp depreciation in the yuan currency, and selling pressure has persisted as economic data confirmed slowing growth and deteriorating business conditions, hammering investors’ confidence in stocks.

Gu Yongtai, analyst at Cinda Securities, said the prospect of investors having to sell stocks they bought with borrowed money in order to cover margin calls has also hurt sentiment. “There’s fear that stock price falls would trigger margin calls, which then adds further pressure on prices, although the actual amount of forced liquidation is not as big as people would imagine,” Gu said. Four listed companies suspended trading in their shares on Wednesday, saying their major shareholders, who have pledged shares as collateral, face margin calls and would seek ways to avoid forced liquidation. “If the market continues to fall, equity pledging-related selling pressure could increase significantly, putting further pressure on the stock market,” said Gao Ting at UBS Securities.

Trading volumes have thinned, making price moves even more volatile, as many investors have given up on Chinese stocks since last summer, when shares crashed 40%. Beijing intervened to stem that rout and orchestrate a recovery of sorts, but anyone who mistook that for a bottom and bought back in will be nursing losses again. China’s woes have damaged risk appetite in global markets, too, along with tumbling oil prices. Investors across the world will hang on whether the market chaos of the last few weeks and concerns over China’s slowing economy might blow the U.S. Federal Reserve off its proposed course of gradual interest rate hikes. The Fed is expected to leave rates unchanged later on Wednesday and acknowledge that turmoil in financial markets threatens its upbeat view of the U.S. economy, leaving the chances of a March hike diminished but alive.

Understating: “Most players will have a quiet quarter in China, including Apple..”

• China’s Smartphone Slump Bites Apple (WSJ)

A slump in China’s smartphone market is weighing on Apple Inc.’s growth, even as the country remains a relatively bright spot for the iPhone maker. Chief Executive Tim Cook said on an earnings call Tuesday that Apple has begun to see “signs of economic softness” in the Greater China region, which includes China, Taiwan and Hong Kong. Apple’s sales in the region grew 14% in its fiscal first quarter ended Dec. 26 to $18.4 billion, better than any other region during the period, but far from the 70% growth it saw in the year-earlier period. In the fiscal year that ended Sept. 26, Greater China sales had surged 84%, with profits growing even faster. Keeping up this momentum will be a challenge for Apple this year, with China’s smartphone market slowing and the country’s economy cooling. China’s economic growth in 2015 was the slowest in a quarter century.

Apple’s suppliers in Asia have already warned of lower iPhone demand in the current quarter and have been told to scale back production, according to people familiar with the matter. China’s smartphone market growth will continue to slow this year, as most people in the country who want a smartphone already have one, analysts say. First quarter smartphone purchases will be hit by this market saturation, as well as secondary factors like freezing weather that is keeping shoppers in the north part of the country indoors, said Canalys analyst Nicole Peng. “Most players will have a quiet quarter in China, including Apple,” she said. Apple currently ranks No. 3 in China’s smartphone market after Huawei and Xiaomi. China’s smartphone market has grown crowded in the past year, after the success of smartphone startup Xiaomi encouraged imitators.

After several years of triple-digit percentage growth, Xiaomi missed its sales target for 2015. Samsung, the world’s biggest smartphone maker, has also struggled in China, where it has been hit by stiff competition. Mr. Cook said on the investor call that Apple was still optimistic on China and was “crafting products and services” with the country in mind. “We remain bullish on China and don’t subscribe to the doom and gloom,” he said. Still, Apple forecast Tuesday that its overall revenue will fall for the first time in 13 years in the current quarter and its stock fell in after-hours trade on concerns about growth.

Where official news meets Bizarro world.

• Xi Urges Sound Planning For Supply-Side Structural Reform (Xinhua)

President Xi Jinping on Tuesday urged authorities to formulate targeted and specific plans to deliver structural reform on the supply side. Sound planning is the foundation for supply-side structural reform, which aims to improve productivity and realize people-first development, Xi told a meeting of the Central Leading Group for Financial and Economic Affairs. He stressed the importance of extensive research of the current economic conditions and to this end, he said, clear objectives were needed. Reform tasks should be specified and a system to designate and track responsibility should be put in place, he added. To address problems such as overcapacity, the government has pinned its hopes on supply-side structural reform, which focuses on better provision for high-quality goods and services and lower costs for businesses.

China’s economy grew by 6.9% year on year in 2015, its lowest annual expansion in a quarter of a century. During the meeting, Xi stressed the importance of environmental protection while developing the Yangtze River economic belt. “The Yangtze is the nation’s River of Life. No economic activities related to Yangtze should damage its environment. Its ecological system should only get better, not worse,” he said. Xi also emphasized the need to preserve forests. The tradition of voluntary tree planting should continue and a new round of “returning the farmland to forests” will begin, he said. He also urged cities to do more to achieve urban greening and called for more attention to be given to national parks to better protect endangered animals. Premier Li Keqiang, who is also deputy head of the Central Leading Group for Financial and Economic Affairs, also attended the meeting.

Dalio argues something similar to what I often say when ‘experts’ talk about economic cycles: Kondratieff is a cycle, too. Don’t agree with him on everything, though.

• Pay Attention To Long-Term Debt Cycle (Ray Dalio)

I have a controversial view that is based on my alternative economic template, and I feel a responsibility to share at this precarious time. In brief, the Federal Reserve’s template, and that of most economists and market participants, reflects the business cycle. Based on it, tightening should occur when a) the rate of growth in demand is greater than the rate of growth in capacity and b) the usage of capacity (as measured by indicators such as the GDP gap and the unemployment rate) is becoming high. As a result, tightening now makes sense. However, as I see it, there are two important cycles to pay attention to — the business cycle, or short-term debt cycle, and the debt supercycle, or long-term debt cycle.

We are seven years into the expansion phase of the business/short-term debt cycle — which typically lasts about eight to 10 years — and near the end of the expansion phase of a long-term debt cycle, which typically lasts about 50 to 75 years. It is because of the long-term debt cycle dynamics that we are seeing global weakness and deflationary pressures that warrant global easing rather than tightening. Since the dollar is the world’s most important currency, the Fed is the most important central bank for the world as well as the central bank for Americans, and as the risks are asymmetric on the downside, it is best for the world and for the US for the Fed not to tighten.

Since the long-term debt cycle issue is the biggest issue that separates my view from others, I’d like to briefly focus on its mechanics. What I am contending is that there are limits to spending growth financed by a combination of debt and money. When these limits are reached, it marks the end of the upward phase of the long-term debt cycle. In 1935, this scenario was dubbed “pushing on a string”. This scenario reflects the reduced ability of the world’s reserve currency central banks to be effective at easing when both interest can’t be lowered and risk premia are too low to have quantitative easing be effective.

Solid piece on yet another EU disaster.

• The EU’s Banking Union: A Recipe For Disaster (Thomas Fazi)

[..] the average balance sheets of the European Union’s 30 and 15 largest banks (€800 billion and €1.3 trillion respectively) are 13 and 21 times larger than the proposed recapitalisation limit. Not only are these banks too big to fail – they are too big to bail. The failure of any of them – even assuming that it would take place in isolation, rather than as part of a wider systemic crisis – would require the mobilisation of huge financial resources. This is also proven by the recent crisis, with certain large banks receiving public assistance in excess of €100 billion. With all this in mind, one could still argue that the bail-in mechanism represents a step forwards vis-à-vis the bailouts of recent years, by limiting the burden placed on sovereigns and thus the ‘socialisation’ of banking crises.

The crucial point to understand here is that the bail-in is indeed a great tool to have at one’s disposal, as there are undoubtedly numerous cases where a bail-in might be preferable to a bailout. But this has to be decided on a case-by-case basis. The problems arise when member states are forced to resort to the bail-in as the primary method of bank resolution, regardless of the potential consequences of such a move, of the nature of the bank’s problems, of the wider macroeconomic context, etc. – which is precisely what the banking union prescribes. This is especially true in light of the extreme disequilibrium between banking systems in the EU, itself a reflections of the wider social and macroeconomic imbalances between core and periphery countries.

As the ECB’s recent stress tests have revealed, the banks with the largest capital shortfalls are all located in the countries of the periphery, which have been hit the hardest by the crisis: Italy, Greece, Portugal, Ireland and Cyprus. This is not surprising: various studies have shown that there is a clear pro-cyclical link between a country’s negative macroeconomic performance and the capital adequacy of its banks. This is evident from the dizzying and rapidly-growing volume of non-performing loans (NPLs) in these countries – a direct result of the austerity policies pursued in recent years and, of course, the main reason why periphery banks failed the ECB’s stress tests. Which leads us to the paradoxical situation in which Italy finds itself in today.

The country’s banks fared relatively well during the financial crisis and therefore didn’t require almost any government aid at the time; since then, as a result of the country’s unprecedented socioeconomic collapse, itself a result of EU-sanctioned austerity, the balance sheets of Italian banks have severely deteriorated, and today – after a seven-year-long build-up of non-performing loans – are facing a system-wide crisis. For this reason, the Italian government has been in talks with the Commission for months over its plan to create a ‘bad bank’ to help offload some of the banks’ bad debt; at the time of writing, though, the Commission – the same Commission that by mid-2009 had approved €3 trillion in guarantee umbrellas, risk shields and recapitalisation measures to bail out Europe’s banks – continues to block the government’s plan, on grounds that it would amount to a violation of state aid and banking union rules.

Just delayed ad infinitum?!

• EU’s Too-Big-to-Fail Bank Bill Won’t Be Withdrawn (BBG)

Jonathan Hill, the European Union’s financial-services chief said he won’t pull the plug on a bill intended to tackle too-big-to-fail banks that’s bogged down in a divided legislature. Asked in an interview in his Brussels office if he planned to heed calls from some bankers and European Parliament lawmakers to withdraw the legislation, Hill said firmly, “I don’t.” The European Commission, the EU’s executive arm, presented a draft bank-structure plan in early 2014 – before Hill’s tenure as commissioner began – as a way to boost financial stability by separating banks’ retail operations from riskier investment banking. The Council of the EU, which represents national governments and forms one half of the bloc’s legislature, reached a negotiating position on the bill in June 2015. But parliament, the other half, has made no progress on the proposal.

A proposal by Gunnar Hoekmark, the parliament’s lead lawmaker on the bill, was rejected by the Economic and Monetary Affairs Committee last May. A tentative compromise subsequently brokered by Hoekmark collapsed later in the year in the face of strong French-led opposition, leaving the committee fresh out of ideas and momentum on how to bridge the gap between the two main political groups, the center-right European People’s Party and the Progressive Alliance of Socialists and Democrats. Hoekmark has consistently rejected proposals for the mandatory separation of investment and consumer operations, while the Socialists have pushed for a strong separation trigger in the bill “We have told the Socialist group that there shall be no automaticity,” said Hoekmark, a member of the EPP group.

“The only option on the table is reasonable legislation based upon risk criteria, or we will reach a point where there is no common solution.” In fact, Hoekmark said he had rejected a fresh proposal from the Socialists this week. “I prefer no legislation instead of bad legislation,” he said. And Hoekmark appears to be in no hurry to cobble together a new compromise. “There is a broader understanding that we must take stock and look at what we have achieved before proceeding with new legislation,” he said. “Let’s analyse the consequences, let’s see if we are lacking, or if we have some over-regulation. 2016 is a good year for such assessments.”

Only bank shareholders get punished.

• Five of Six Brokers in Libor Trial Are Acquitted by London Jury (BBG)

Five ex-brokers accused of helping convicted trader Tom Hayes rig Libor were acquitted Wednesday by a London jury, in a setback to U.K. fraud prosecutors. Noel Cryan, 50, who worked at Tullett Prebon Plc in London, Colin Goodman, 54, and Danny Wilkinson, 49, formerly of ICAP, and RP Martin’s Terry Farr, 44, and James Gilmour, 50, were found not guilty and released. The jury couldn’t reach a unanimous verdict on a sixth man, ICAP’s Darrell Read, 50, and was sent home to come back Thursday to discuss the remaining charge. After a four-month trial, the jury took about a day to find the others not guilty. The verdicts will be seen as a blow to the Serious Fraud Office, which appeared to have turned its fortunes around in the last 12 months.

A dozen banks have been fined about $9 billion by global authorities over the last four years in relation to the manipulation of Libor, the benchmark interest rate used in trillions of dollars of derivatives and loans. More than 30 individuals have been charged, and Hayes was convicted last year. “It’s always been a surprise and disappointment that these people were seen as front and center when they weren’t even bankers,” Matthew Frankland, a lawyer for Wilkinson, said by phone. “If what the SFO says is true, it’s rather shocking that more senior people aren’t being prosecuted.” Hayes, the former UBS and Citigroup trader prosecutors alleged was at the center of a conspiracy, was jailed in August. His sentence was reduced to 11 years from 14 years upon appeal in December.

“The key issue in this trial was whether these defendants were party to a dishonest agreement with Tom Hayes,” SFO Director David Green said in a statement. “By their verdicts the jury have said that they could not be sure that this was the case. Nobody could sensibly suggest that these charges should not have been brought and considered by a jury.” The result comes at the end of a sprawling and complex case that was postponed for several days when one of the defendants, Wilkinson, fell ill. Several of the men cried as the verdicts were read out. Farr burst from the dock and climbed the stairs to embrace his wife and son.

Because that’s more important than human lives.

• EU Says Greece ‘Seriously Neglected’ Schengen Border Duties (Kath.)

The EU executive said on Wednesday that Greece has “seriously neglected” its frontier duties to Europe’s free-travel Schengen zone and could be subject to new border controls by other members if it fails to remedy the problems within three months. “The draft report concludes that Greece seriously neglected its obligations and that there are serious deficiencies in the carrying out of external border control that must be overcome … by the Greek authorities,” European Commission Vice President Valdis Dombrovskis told a news briefing. The draft Schengen evaluation report on Greece was based on unannounced site visits to the Greek-Turkish land border as well as to the islands of Chios and Samos carried out from 10 to 13 November 2015. Experts looked at the presence of police and coast guard personnel on the inspected sites, the efficiency of the identification and registration process, sea border surveillance and cooperation with neighbouring countries.

According to the report “there is no effective identification and registration of irregular migrants and… fingerprints are not being systematically entered into the system and travel documents are not being systematically checked for the authenticity or against crucial security databases, such as SIS, Interpol and national databases.” “The report shows that there are serious deficiencies in the management of the external border in Greece,” Migration and Home Affairs Commissioner Dimitris Avramopoulos said. “We know that in the meantime Greece has started undertaking efforts towards rectifying and complying with the Schengen rules. Substantial improvements are needed to ensure the proper reception, registration, relocation or return of migrants in order to bring Schengen functioning back to normal, without internal border controls. This is our ultimate common goal,” Avramopoulos said.

Sweden is busy organizing the ‘expulsion’ of 80,000 refugees, while the Dutch government (they chair the EU until July 1) has announced plans to launch a ‘ferry’ line to force refugees back to Turkey from Greece. One day after the parliament in The Hague approved a motion for Dutch jets to start bombing Syria.

And I’m thinking: it’s alright to not be all that smart or competent, but please at least try to maintain a degree of decency, hold on to a shade of moral values. But perhaps those two things are two sides of the same coin. We should seriously wonder what Europe will look like a year from now. There’ll be at least another 1 million refugees trying to make it to Europe in 2016, that’s a given. The heart shudders.

• Sweden To Expel Up To 80,000 Rejected Asylum Seekers (Guardian)

Sweden intends to expel up to 80,000 asylum seekers who arrived in 2015 and whose applications had been rejected, interior minister Anders Ygeman said on Wednesday. “We are talking about 60,000 people but the number could climb to 80,000,” the minister was quoted as saying by Swedish media, adding that the government had asked the police and authorities in charge of migrants to organise their expulsion. Ygeman said the expulsions, normally carried out using commercial flights, would have to be done using specially chartered aircraft, given the large numbers, staggered over several years.

The proposed measure was announced as Europe struggles to deal with a crisis that has seen tens of thousands of refugees arrive on Greek beaches, with the passengers – mostly fleeing conflict in Syria, Iraq and Afghanistan – undeterred by cold, wintry conditions. The United Nations says more than 46,000 people have arrived in Greece so far this year, with more than 170 people killed making the dangerous crossing. Sweden, which is home to 9.8 million people, is one of the European Union countries that has taken in the largest number of refugees in relation to its population. Sweden accepted more than 160,000 asylum seekers in 2015.

The difference two years make. From 19 Nov 2013. Paraphrasing Groucho: “These are my principles, and if you don’t like them, I have others.” Zero moral compass.

• European Commission in 2013: Refugee Push-Backs Are Illegal (EURActiv)

The European Commission indirectly warned Greece and Bulgaria today (19 November) to stop turning down Syrian refugees at their borders with Turkey, after the UN issued a similar call just a few days before. The UN High Commissioner for Refugees (UNHCR) António Guterres called last Friday on Greece and Bulgaria to stop turning back Syrians fleeing their war-ravaged homeland. Bulgarian authorities have reportedly bragged of turning down refugees at the border. According to the government website, Interior Minister Tsvetlin Yovchev, who is also deputy prime minister, has said that in just one day more than 100 persons, and previously more than 150, were from entering the country. Hundreds of policemen have been sent to the Bulgarian border with Turkey to push back prospective immigrants.

The impoverished country is struggling to deal with the some 7,000 refugees from Syria already on its soil, with more and more still managing to arrive. Both Greece and Bulgaria have begun the construction of fences on their borders with Turkey. Greece has erected a 12.5km wall at a critical section of the Greece-Turkish border near the town of Orestiada, while Bulgaria has announced plan to build a similar, 30-km fence near the town of Elhovo. Michele Cercone, spokesperson for home affairs commissioner Cecilia Malmström, told EurActiv that pushing back asylum seekers was against EU and international law. “Push-backs are simply not allowed. They are not in line with EU and international obligations. Member states cannot, shall not and should not carry out any push-back,” he said.

Asked how laws against push-backs were consistent with the fact that several member states had erected walls or fences at their borders, Cercone conceded that EU countries were free to decide their own border protection measures. “This is of course their choice. But we have always said that walls do not solve problems. What solves problems is a consistent structural management of migratory and asylum seekers’ flows,” Cercone said. He explained that this was implying that member states should be able to manage these flows in full respect of fundamental rights and international and European obligations. “Nobody coming or arriving to the EU territory and asking for asylum can be pushed back or can be denied this possibility,” he said, adding that this stemmed from the core values on which the EU was built. Asked if the Commission had any particular message for Bulgaria and Greece, Cercone said this was a message to all member states.

What happened to the 3 million prediction?

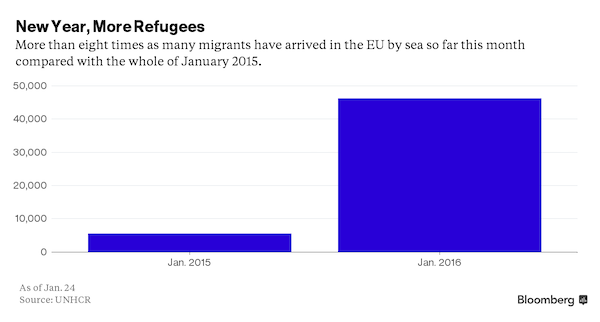

• Europe Faces Another Million Refugees This Year: UN (BBG)

As many as 1 million people from Africa, the Middle East and Asia will seek refuge in Europe this year, according to a report by global migration agencies, a number that nears levels seen last year in the continent’s worst migration crisis since World War II. The war in Syria will continue to be the main source of migrants after triggering a spike in 2015, according to the report from the United Nations High Commissioner for Refugees and the International Organization for Migration. An increasing number of people will also come from southwest Asia and northern and western Africa, and the continued flow will exacerbate tension among European Union governments already deemed incapable of dealing with new entries smoothly, they said.

“The conflict in Syria will continue unabated and will generate high levels of internal and external displacement,” the agencies said in the report published on their websites. Refugees fleeing “Afghanistan may increase amid “deteriorating security situation in the majority of the provinces and the continuing downward spiral of the economy.” The EU is struggling to create a comprehensive plan to deal with its worst refugee crisis since World War II. The crunch has riled politics across the bloc by bolstering support for anti-immigrant parties and has prompted some governments to impose border controls with other European countries. This week, Germany and its neighbors laid the groundwork to extend a reintroduction of checks at internal borders for as long as two years, a move that departs from the EU’s principle of passport-free travel among most of its members.

The situation won’t measurably improve this year, according to the report, which estimated that about 6.5 million Syrians have been driven from their homes inside their country and another 4 million have sought shelter in Egypt, Iraq, Jordan, Lebanon and Turkey. The agencies, which have drawn up a $550 million plan to help refugees, also said Afghanistan’s deteriorating security and the “downward spiral of the economy” will add to migrant numbers.

No tears left.

• Refugee Boat Sinks Off Greek Island; 7 Bodies Recovered (AP)

Greek authorities say a total of seven bodies, including those of two children, have been recovered from the sea off the eastern Aegean island of Kos after a boat carrying migrants or refugees sank early Wednesday. Rescue crews recovered the bodies of three men, two women, a boy and a girl. There were two survivors — a man and a woman. A search and rescue operation in the area by vessels from the Greek coast guard and the European border patrol agency Frontex, a helicopter and Greek rescue volunteers was called off after all on board the boat were accounted for.

Home › Forums › Debt Rattle January 28 2016