Jack Delano Men outside beer parlor in Jewett City, Connecticut. Nov 1940

What did I call yesterday’s article again? Oh, that’s right, I called it Europe’s Tumbling, Who’s To Blame?. Well, I’m not a seer, or clairvoyant, but I might as well have used that exact same title again today. Because the same theme plays out again. In an piece initially called Europe’s Recovery Menaced by Putin as Ukraine Crisis Bites, later renamed Draghi Outlook Menaced by Putin as Ukraine Crisis Bites (what’s not to love), Bloomberg spills it all:

The crisis in eastern Europe is showing signs of disrupting Mario Draghi’s economic outlook. Evidence is building that the conflict in Ukraine and European Union sanctions against Vladimir Putin’s Russia are undermining a euro-area recovery that the European Central Bank president already describes as weak. With the ECB expected to keep interest rates on hold near zero today and refrain from any new policy measures, Draghi is likely to face questions on how he plans to keep the economy on track.

The ECB may have few tools left to mitigate the impact of political turmoil that European companies from Anheuser-Busch InBev to Siemens say is hurting their business. A volley of measures introduced in June will take time to work, and policy makers have so far shied away from wheeling out a full-scale asset-purchase program. “The euro-zone recovery is very fragile and the macro situation fluid,” said Andrew Bosomworth, managing director at Pacific Investment Management Co. in Munich. “Expect Draghi to elaborate on spillover risks from the Russia-Ukraine crisis.”

Note that this was first published before Russia announced its sanctions on the west, and before Draghi held a speech in which he said … nothing much at all. Here’s Russia’s sanctions:

Russia Bans Food Imports From EU, US, Canada, Australia (Guardian)

Russia has banned fruit, vegetables, meat, fish, milk and dairy imports from the US, the European Union, Australia, Canada and Norway, Russia’s prime minister told a government meeting on Thursday. Dmitry Medvedev said the ban was effective immediately and would last for one year. Russian officials were on Wednesday asked to come up with a list of western agricultural products and raw materials to be banned. The agriculture minister, Nikolai Fyodorov, said on Thursday that greater quantities of Brazilian meat and New Zealand cheese would be imported to offset the newly prohibited items.

Now, if you’re anything like me, you’ve of course always suspected that all Kiwi’s are nothing but a bunch of closet Hobbit commies. And now we have what looks a lot like proof: New Zealand stands to profit handsomely from the sweeping Russian ban of US and EU food products, along with China, Brazil, Turkey.

Well played, Wellington! Better than Helsinki and Amsterdam, the probably hardest hit Europeans, who have registered only surprise, indignation and, yes, anger, I kid you not, at the ban. Guess they really didn’t see this one coming. The Brits apparently don’t get it either (hey, ask New Zealand, you still got the same queen, get her involved!).

Britain Says ‘No Grounds’ for Russian Retaliation Against West

There are no grounds for Russia to impose retaliatory sanctions against Western countries, a British Foreign and Commonwealth Office official told RIA Novosti. “There are no grounds for Russia to impose these sanctions. We have been pushing for a strong and determined international response to Russia’s unacceptable behavior in Ukraine. We have been clear that we are prepared to play our part and that there will be some costs, but this does not diminish our commitment. Instead of retaliating, Russia should be using its influence with the violent Russian-backed separatists to stop destabilizing Ukraine,” the official said.

At this point, I’m thinking it’s entirely possible that – some of – the leaders of European countries simply don’t know to what extent Brussels has been involved in Ukraine. That the communication lines between on the one hand 28 separate capitals, parliaments and governments – most of which speak their own separate languages -, and on the other hand Brussels, with its myriad commissions, leaders, parliament etc., its many hundreds of parliamentarians and thousands of translators, simply don’t allow for adequate and speedy decision making. Or is Brussels perhaps also genuinely surprised?

EU Ready To Appeal To WTO Over Russian Import Bans

The EU is ready to appeal to the World Trade Organization to have the Russian agriculture import bans lifted, a European diplomatic source told ITAR-TASS. “Politically motivated large-scale trade restrictions are a direct violation of WTO rules, which Russia pledged to comply with,” the diplomat said. “These measures will be thoroughly analyzed, and then relevant claims will be submitted with the WTO.” The source added that the European Commission would start analyzing Russia’s ban on imports from EU states as soon as the official list of banned goods would be published.

The EU Council may convene an urgent meeting in connection with Russia’s response to European sanctions. It is early to say whether the EU will take measures in response to the Russian ban on imports of food products from Europe, source told. “First, it is necessary to see and analyze the official list of product that Moscow intends to ban. After that, decisions will be made both at the European and the national level,” the source stressed. The Russian ban on agricultural imports from the European Union is an “irresponsible measure” that can lead to losses of billions of euro for European as well as Russian consumers, the source told ITAR-TASS.

Question: Are you sure the WTO is the right organization to mediate allegedly “politically motivated” restrictions?

I think the EU has different problems here: some of the 28 member nations will be hit much harder by these sanctions than others. Is there a fund in place to assure that the pain gets spread fairly? Also within nations, one sector gets hit, while another doesn’t. Do all nations have such funds ready to go?

It may not look so bad right now, but wait 6 or 12 months. And don’t let’s forget that economically, Europe is already teetering on the edge of the gutter, despite all assurances to the contrary. It’s therefore of course only human to blame the next step in the downtrend on the universal bogeyman Putin. But let’s get real, Europe never needed any help to to bring down its economy, it’s perfectly capable of doing that all by itself.

The US meanwhile? No pain from any of the sanctions.

Since this is a game of, as Paul Simon said: “All along along, There were incidents and accidents, There were hints and allegations, let’s see what, again, do we know for sure so far, what we can prove? Here’s what:

The EU and US instigated, financed and supporetd the Maidan movement, installed their very own handpicked government in Kiev, established an army aimed at eradicating all signs of discontent among Russian speaking Ukrainians in east Ukraine, with crucial parts played by CIA, Blackwater and various other mercenaries, blamed Putin for the downing of a plane without providing any evidence whatsoever of his involvement, announced a second series of economic sanctions on Russia, and then claim Russia has no reasons at all to announce its own set of counter sanctions.

It would be funny if it weren’t so out there.

Did you, in the midst of the 24/7 wall of words, manage to keep track of the fact that no part of any BUK rocket was ever found at the crash site? Are you also wondering where the Ukraine secret service took the Air Traffic Control recordings 3 weeks ago, and what we’ll be told about them, if anything, ever? It took, what, 24 hours, for the ATC logs from the still unlocated MH370 to be made public…

How about the black boxes, that had not been tampered with as Kiev had alleged? All we’ve heard so far out of the ‘lab’ in Britain where they were taken is that there was nothing out of the ordinary on them. So where’s the info? Why not go public with it?

Donetsk “rebel leader” Borodai stepped down today, to give way to some other schmuck, I know, but schmucks are the only thing they have over there. The May presidential election was between one billionaire and the other. That’s just the turf. Earlier this morning, the Ukraine government called an end to the truce on the crash site. One day after Holland announced its experts will leave the site because there’s too much fighting going on.

What truce, what are you talking about? The one you broke mere minutes after you yourself announced it?

Anyway, leave it be. What Europe would like to do is move the blame for its own gigantic economical failure onto Russia. Or make that Putin. It always works better if “it” has a face.

But Putin has nothing to do with anything. Italy was a lost economy way back (Beppe Grillo said years ago when Nicole and I went to see him, that what happens now, would), Portugal was never more than a nice facade, Greece bank rates will soon soar, it’s all just been a thin veil based on Mario Draghi’s “I’ll do what ever it takes”.

Thing is, Mario doesn’t have what it takes, and it’s not even his fault.

Europe shoots itself in the foot, puts it in its mouth, and chokes on it. How does that sound?

Europe’s in much worse shape than anyone’s let on, and they now have a bogeyman to deflect their own guilt and stupidity and failed conspiracies off of.

Only, Russia has nothing to do with Europe’s problems. Europe has fabricated its own problems. The Brussels leaders, though, would be more than happy to go to war against Russia just to hide their own failures and incompetence.

That’s the kind of thing that’s really dangerous, the bloated sociopaths who lead our nations. That and the propaganda machine they control.

• Russia Bans Food Imports From EU, US, Canada, Australia (Guardian)

Russia has banned fruit, vegetables, meat, fish, milk and dairy imports from the US, the European Union, Australia, Canada and Norway, Russia’s prime minister told a government meeting on Thursday. Dmitry Medvedev said the ban was effective immediately and would last for one year. Russian officials were on Wednesday asked to come up with a list of western agricultural products and raw materials to be banned. The agriculture minister, Nikolai Fyodorov, said on Thursday that greater quantities of Brazilian meat and New Zealand cheese would be imported to offset the newly prohibited items. He added Moscow was in talks with Belarus and Kazakhstan to prevent the banned western foodstuffs being exported to Russia from the two countries.

The Kremlin’s move comes in response to the grounding of the budget airline subsidiary of Aeroflot as a result of EU sanctions over Moscow’s support for rebels in Ukraine. Medvedev also said officials were considering a ban on European airlines flying to Asia over Siberia. Russia is Europe’s second-largest market for food and drink and has been an important consumer of Polish pig meat and Dutch fruit and vegetables. Exports of food and raw materials to Russia were worth €12.2bn (£9.7bn) in 2013, following several years of double-digit growth. The UK is less likely to lose out; in 2013, its biggest food and drink export was £17m of frozen fish, followed by £5.7m of cheese and £5.3m of coffee.

• Britain Says ‘No Grounds’ for Russian Retaliation Against West (RIA)

There are no grounds for Russia to impose retaliatory sanctions against Western countries, a British Foreign and Commonwealth Office official told RIA Novosti. “There are no grounds for Russia to impose these sanctions. We have been pushing for a strong and determined international response to Russia’s unacceptable behavior in Ukraine. We have been clear that we are prepared to play our part and that there will be some costs, but this does not diminish our commitment. Instead of retaliating, Russia should be using its influence with the violent Russian-backed separatists to stop destabilizing Ukraine,” the official said.

On Wednesday, Russian President Vladimir Putin singed an order on economic measures to protect the country’s security. The decree banned for a year imports of agricultural and food products from countries that have imposed sanctions on Russia. The complete “blacklist” of food imports from Australia, Canada, the European Union, the United States and Norway was announced Thursday. The list includes meat, poultry, fish, milk, dairy products, as well as fruits and vegetables. The embargo does not include infant foods and products. Moscow has said that it is ready to review the terms of these restrictions if its Western partners demonstrate behaviors constructive to cooperation. Russian Prime Minister Dmitry Medvedev said the measure offered Russian agricultural producers a unique chance to replace imports with local foods.

Ambrose is never good for his own opinions.

• Vladimir Putin’s Pointless Conflict With Europe (AEP)

The world faces a moment of maximum danger in Ukraine. Vladimir Putin has perhaps 72 hours to decide whether to launch a full invasion of the Donbass, or accept defeat and let the Ukrainian military crush his proxy forces. Nato officials say Russia has massed 20,000 troops in battle-readiness near the border, backed by Spetsnaz commandos, tanks and aircraft. Vehicles have been marked with peace-keeper labels already. Nato sees every sign that the Kremlin intends to disguise an attack as a “humanitarian mission”. This is more serious than the Russian invasion of Afghanistan in 1980. That was a “colonial war”. The Soviet Union was a careful, status quo power in its final decades. It held captive nations but did not overrun new borders in Europe. Mr Putin is expansionist, and far less predictable. He is, in any case, captive to the chauvinist fever that he has so successfully stoked.

He has been clear from the outset that he will deploy any means necessary to bring Ukraine back into Russia’s orbit. Only war can now achieve this, since all else has failed, and since he has turned a friendly Ukraine into an enemy by his actions. The awful implications of this are at last starting to hit the markets. “People thought that Russia was just playing a game of brinkmanship,and that pragmatism would prevail in the end. There is real fear now that this will spin out of control. Nothing cannot be excluded at this point, even a cut-off in oil and gas,” said Chris Weafer, from Macro Advisory in Moscow. Yields on 10-year rouble bonds have jumped to 9.7pc, up 130 basis points since June. The sanctioned bank VTB is up 180 points in a month. A liquidity crunch is rapidly taking hold across the financial system. “The market is shut. Not a single Russian entity has been able to borrow anything in dollars, euro or yen since early July,” said Mr Weafer.

I like that he can feel safe.

• Edward Snowden Receives Three-Year Russian Residence Permit (Reuters)

Former U.S. intelligence contractor Edward Snowden, wanted by the United States for leaking extensive secrets of its electronic surveillance programs, has been given a three-year residence permit by Russia, his Russian lawyer told reporters on Thursday. The announcement comes at a time when Russia’s relations with the West are at Cold War-era lows over Russia’s actions in Ukraine. Russia responded to Western sanctions by banning certain food imports from the United States, the European Union, Australia, Canada and Norway on Thursday. “The decision on the application has been taken and therefore, with effect from Aug. 1, 2014, Edward Snowden has received a three-year residential permit,” Anatoly Kucherena said. “In the future, Edward himself will take a decision on whether to stay on (in Russia) on and get Russian citizenship or leave for the United States.”

He said Snowden could apply for citizenship after living in Russia for five years, in 2018, but that he had not decided whether he wanted to stay or leave. Kucherena said Snowden was studying Russian and had an IT-related job, but did not provide details. “He is a high-class IT specialist”, he said. He said Snowden’s security was being taken seriously and that he was using private security guards. “He leads a rather modest lifestyle, but nevertheless we proceed from the tone of statements that come from the U.S. State Department and other political figures,” he said. “The security issue should not be treated as a secondary one.”

• Italy Shows That The Eurozone Crisis Is Only In Remission (Telegraph)

Italy is in an utterly terrible state. It has just entered its third recession in six years, with GDP tumbling by 0.2pc in the second quarter. It is a triple-dip recession, and a catastrophic state of affairs. By contrast, the UK economy grew 0.8pc in the second quarter. Even though Britain’s recovery was extremely slow, we have now bounced back and our economy is slightly larger than it was prior to the crisis. Horrifically, Italian real GDP is still 9.1pc short of its pre-recession peak – as analysis by RBS points out, its output is now back to the level it last was in 2000. Britain’s GDP is roughly a quarter larger than it was then. Italy had previously spent the pre-recession years quasi-stagnating while the rest of the world was booming; its performance has thus diverged dramatically from much of the rest of the developed world. It gets worse: a combination of no growth and disinflationary pressures means that Italy’s national debt is increasing as a share of its national income. An analysis from Fathom Consulting highlights the fragile nature of Italy’s debt dynamics.

Even if growth were miraculously to return to the 1.5pc a year rate seen in the 30 years prior to the crisis, Italy would also need 2.3pc inflation to stabilise its national debt. More realistically, GDP will probably continue to flatline – and for the time being at least, eurozone inflation will remain low, partly as a result of the European Central Bank’s one-size-fits-all monetary policy. The result is hideously predictable: debt as share of the economy will keep on rising and will eventually asphyxiate the economy. Italy is in desperate need of a supply-side revolution – not merely of a few tweaks to red tape and taxes, but a genuine, radical shake-up, coupled with profound political change. It needs to unleash the forces of entrepreneurial creative destruction across its sclerotic economy. If it fails to change, and fast, Italy, already the eurozone’s new sick man, will eventually threaten the single currency itself. The eurozone crisis is merely in remission.

Bet cha home prices still rise ….

• Australia Jobless Rate Hits 12-Year High In July (Australian)

Australia’s unemployment rate spiked to a 12-year high in July, well above analysts’ expectations and casting a cloud over the economic outlook. Official data showed the unemployment rate surged to 6.4% in the month, compared with 6% in June – an unusually large monthly move and the highest since June 2002. The Australian jobless rate is now higher than in the US, where unemployment sits at 6.2%. The Australian Bureau of Statistics said that methodology changes to the way the labour survey is conducted had no material impact on the month’s data. The figures were significantly weaker than the market was looking for and suggests official interest rates will remain on hold, JP Morgan economist Tom Kennedy said.

“The figures were very soft all round – there was virtually no employment growth, we’ve had hours fall, part-time employment fall and only very tepid full-time employment growth so all in all, a very, very soft report, Mr Kennedy said. “This pours a little bit of cold water over those expecting an earlier rate hike,” he added. The total number of jobs in Australia fell by 300 to 11.57 million in the month on a seasonally adjusted basis. An AAP survey of 15 economists tipped the jobless rate would hold steady at 6% and predicted the employment would rise by 12,000. Reserve Bank governor Glenn Stevens said this week, after leaving the cash rate unchanged at a record low of 2.5%, that there had been some improvement in the outlook for the labour market but it would probably be some time before unemployment declined consistently.

Smart cookie.

• India Central Bank Chief Rajan Sees Risk of Financial Markets Crash (WSJ)

Reserve Bank of India Governor Raghuram Rajan warned Wednesday that the global economy bears an increasing resemblance to its condition in the 1930s, with advanced economies trying to pull out of the Great Recession at each other’s expense. The difference: competitive monetary policy easing has now taken the place of competitive currency devaluations as the favored tool for playing a zero-sum game that is bound to end in disaster. Now, as then, “demand shifting” has taken the place of “demand creation,” the Indian policymaker said. As was the case in the 1930s, the lack of coordination between policymakers is producing spillovers that may be difficult to control, and the world’s financial system may soon face fresh turbulence at a time when central banks have yet to repair the damage that the 2008 financial crisis caused to developed economies. “We are taking a greater chance of having another crash at a time when the world is less capable of bearing the cost,” said Mr. Rajan in an interview with the Central Banking Journal.

A sudden shift in asset prices could happen in a variety of ways, Mr. Rajan said. The most obvious route would be as a result of investors chasing higher yields at a time when they believe central bank policies will protect them against a fall in prices. “They put the trades on even though they know what will happen as everyone attempt to exit positions at the same time – there will be major market volatility,” said Mr. Rajan. A clear symptom of the major imbalances crippling the world’s financial market is the over valuation of the euro, Mr. Rajan said. The euro-zone economy faces problems similar to those faced by developing economies, with the European Central Bank’s “very, very accommodative stance” having a reduced impact due to the ultra-loose monetary policies being pursued by other central banks, including the Federal Reserve, the Bank of Japan and the Bank of England. “The exchange rate is too strong given the euro area’s economic standing,” said Mr. Rajan, who took over the RBI in September.

• Unsold Land In China Signals Developer Uncertainty (CNBC)

For the first time in three years lands plots up for auction in Beijing went unsold last week, signaling that developers are nervous about ongoing weakness in the country’s property market. Two of the five lots put up for sale by the Beijing government last week received no bids – for the first time since April 2011, according to Chinese media reports. In another auction on Monday, two of four lots were sold to developers at lower-than-expected prices. According to Ryan Huang, strategist at IG’s Singapore office, the unsold auctions suggest “a mismatch between what increasingly cautious developers are willing to pay versus what local governments want.”

Local governments in China rely on land sales for the bulk of their revenue and are unwilling to budge on high prices, but developers are seeking lower prices as they have become less cash rich due to recent price declines and a tightening credit market. And Huang said he didn’t see this trend letting up anytime soon. “We’re likely to see the relatively muted appetite by property developers continue, as investors get increasingly concerned over a property slump and take a wait-and-see attitude,” added Huang. Du Jinsong, head of Asia Property Research at Credit Suisse, told CNBC the unsold auctions were result of local government’s misjudging the market. “Developers have adjusted their expectations on future housing prices already, given the housing market weakness for the past six months, but local governments have not yet adjusted their own expectations so some land parcels’ open bid prices (base prices) were set too high,” he added.

My cash? That won’t go far …

• US Treasury Looks To Hold More Cash To Deal With Future Crises (Reuters)

The U.S. Treasury wants to increase its daily cash holdings, a measure that would help Washington pay its bills during a crisis, a senior official said on Wednesday. If adopted, the new policy would help the government in the event an emergency shut down markets and left Washington unable to borrow money to pay creditors and other obligations. “Holding more cash on hand is a prudent measure,” Treasury Assistant Secretary Matt Rutherford said in a news conference. He said the measures would help public finances weather events like the Sept. 11, 2001 attacks or 2012’s Superstorm Sandy, both of which disrupted Wall Street trading. Washington borrows vast sums in weekly auctions to pay its bills. Investors who met with Treasury officials on Tuesday urged the government to increase its daily cash holdings to around $500 billion. That would be enough to cover about 10 days worth of outlays.

A change in policy, however, would not buy the government any additional time if it runs into a legal limit on borrowing next year. Current law will limit the amount of cash Treasury can hold when a cap on federal borrowing becomes binding again in March 2015. The U.S. government suspended the debt ceiling in February of this year. Even if the Treasury changes its cash management policy, it would be obligated to reduce its daily balance to around $33 billion in March, Rutherford said. The Treasury held about $66 billion in cash on Monday, a typical level in recent months. Rutherford said a decision had not been made yet on the policy, and that officials would be studying the matter. Rutherford also announced the United States will buy back debt in the coming quarter for the first time since 2002 to make sure its computer infrastructure is adequate for any future buyback operations.

• Americans Give Up Passports as Asset-Disclosure Rules Start (Bloomberg)

The number of Americans renouncing U.S. citizenship stayed near an all-time high in the first half of the year before rules that make it harder to hide assets from tax authorities came into force. Some 1,577 people gave up their nationality at U.S. embassies in the six months through June, according to Federal Register data published yesterday. While that’s a 13% decline from the year-earlier period, it’s only the second time there’s been a reading of more than 1,500, according to Bloomberg News calculations based on records starting in 1998. Tougher asset-disclosure rules effective as of July 1 under the Foreign Account Tax Compliance Act, or Fatca, prompted 576 of the estimated 6 million Americans living overseas to give up their passports in the second quarter. The appeal of U.S. citizenship for expatriates faded as more than 100 Swiss banks turn over data on American clients to avoid prosecution for helping tax evaders.

“Fatca and the Swiss bank disclosure program has intensified the search for U.S. nationals beyond all measure,” said Matthew Ledvina, a U.S. tax lawyer at Anaford in Zurich. “It’s shocking the levels of due diligence they are going through to ensure they have cleaned house.” Swiss banks are trawling through records going back to the 1990s to find clients with U.S. addresses and telephone numbers, and those who received schooling in the country, Ledvina said. Those identified as U.S. persons are either being asked to leave or placed in special U.S.-only sections of the institution, he said.

The U.S., the only Organization for Economic Cooperation and Development nation that taxes citizens wherever they reside, stepped up the search for tax dodgers after UBS paid a $780 million penalty in 2009 and handed over data on about 4,700 accounts. Shunned by Swiss and German banks and with Fatca looming, almost 9,000 Americans living overseas gave up their passports over the past five years. Fatca requires U.S. financial institutions to impose a 30% withholding tax on payments made to foreign banks that don’t agree to identify and provide information on U.S. account holders. It allows the U.S. to scoop up data from more than 77,000 institutions and 80 governments about its citizens’ overseas financial activities.

You are the banks’ bitches.

• Too Big To Fail Is Alive And More Dangerous Than Ever (David Stockman)

[..] … there is nothing to do except go back to the fundamentals. First and foremost, the September 2008 meltdown was not a main street banking problem; it was a crisis confined to the canyons of Wall Street, owing to the fact that the gambling houses domiciled there had massively bloated their balance sheets with toxic assets and risky derivatives trades, and then funded these balance sheets leveraged at 30:1 with huge amounts of “hot money” in the form of repo and unsecured wholesale loans. As I demonstrated in the Great Deformation, the “bank run” was almost entirely in the Wall Street wholesale market. By contrast, there was never any danger of retail runs at the corner branch bank offices, and the overwhelming majority of the 7,000 main street banks did not own the kind of toxic securitized assets that were roiling Wall Street. In fact, the wholesale market runs in the canyons of Wall Street were actually a positive, economically therapeutic event.

They had already taken out three of the reckless gambling houses – Bear Stearns, Lehman and Merrill Lynch -and were fixing to finish off the remainder, that is, Goldman and Morgan Stanley. Had the market been allowed to finish off the work of the economic gods in late September 2008, the TBTF problem would have been substantially alleviated. Today there might have existed a half dozen “sons of Goldman” in the form of M&A, trading, investment banking and asset management boutiques—run by chastened veterans who lost their lunch during the 2008 Wall Street cleansing. The excuse for Washington’s massive intervention against the free market in the form of TARP and the Fed’s monumental flood of liquidity, of course, is that the US economy was about to be annihilated by something called financial “contagion”. But that is a specious urban legend invented by the crony capitalists who controlled the Treasury and the money-printers who had fueled the housing and credit bubble at the Fed.

Or was it volatility?

• Did IPOs Cause Last Week’s Sell-Off? (The Tell)

When the S&P 500 and other U.S. markets skidded last week, news outlets, including this one, pointed to fears that the Federal Reserve could raise interest rates faster than expected and to worries over the fighting in Ukraine and Gaza. But a look at fund flows suggests an additional explanation. “We think the past week’s selloff was due as much to the $12.5 billion in new shares that underwriters dumped into the market as to anything related to the Fed or developments in Argentina, Portugal, or Ukraine,” said TrimTabs Research, a firm that tracks money flowing in and out of mutual funds and exchange-traded funds.

According to Trimtabs, 15 initial public offerings in the U.S. raised total of $7.3 billion in the week ended July 31. The biggest was the spinoff of Synchrony Financial from General Electric , which raised $3.3 billion. IPOs for Mobileye and Catalent each raised $1 billion. Including other share offerings, the week’s deals totaled $12.5 billion. It is of course impossible to pinpoint where all that money came from. But TrimTabs says spikes in new offerings are usually associated with declines in markets. This suggests that the selling must have been exacerbated by investors selling shares in one company to buy into another. TrimTabs, which relies on fund flow data to gauge sentiment, does not anticipate that the selloff will expand to a correction, defined as a 10% drop from the recent peak. Supply and demand indicators turned more bullish in July, while “new offerings should be far lower in the next five weeks than they were in the last week,” it said in its latest weekly report on fund flows.

Will we ever know?

• Argentina Bond Default Punishes Brazil Mailmen as Pension Fund Loses (BW)

Brazilian postal workers became unlikely victims of Argentina’s default last week after a $168 million fund used by their pension plan recorded a loss on most of its assets. The fund administered by Bank of New York Mellon’s local unit wrote down its value by about 51 percent after losses on securities linked to Argentine government debt, according to a regulatory filing yesterday. Postalis, the pension manager serving about 130,000 current and former postal workers in Brazil, is adopting legal measures in Brazil and the U.S. to mitigate losses, the fund’s press office wrote in an e-mailed response to questions. Argentina last week failed to make a $539 million interest payment on its bonds, prompting Standard & Poor’s and Fitch Ratings to declare the country in default for the second time since 2001.

The country’s bond prices have since retreated from a three-year high, and the International Swaps & Derivatives Association ruled that payouts must be made on a net $1 billion of derivatives linked to the country’s creditworthiness. “Based on the ruling of ISDA on the default event, you could see many more” investors declaring losses tied to Argentina, Marco Aurelio de Sa, the head of trading at Credit Agricole Private Banking in Miami, said in a telephone interview. Postalis is Brazil’s 14th-biggest pension group by investments under management, according to June 2013 data available from the Brazilian pension association Abrapp. It had 8 billion reais ($3.5 billion) of assets, according to the latest data available.

• US Judge Tells New York Bank To Hold Onto Argentine Bond Funds (Reuters)

The U.S. judge in charge of Argentina’s debt default case on Wednesday ordered Bank of New York Mellon to hold on to money deposited by the government rather than disburse the funds to holders of the country’s restructured bonds. The move by U.S. District Judge Thomas Griesa came after Argentina earlier in the day demanded the intermediary bank deliver $539 million in bond payments that were due in June but blocked by previous court rulings. Argentina defaulted on its sovereign bonds last week after losing a long legal battle with hedge funds that rejected the terms of debt restructurings in 2005 and 2010. The government has kept up pressure on Bank of New York Mellon to make payouts to the holders of restructured bonds despite Griesa’s order saying it has to pay the holdout hedge funds at the same time.

The holdouts are asking for repayment of 100 cents on the dollar rather than accept steep discounts offered in Argentina’s two restructurings. “The Republic will seek to hold BNY Mellon liable for any damages the Republic has suffered and may suffer as a result of BNY Mellon’s acts and omissions,” the government said in a letter to the bank on Wednesday. “BNY Mellon has placed its interests, and those of the plaintiffs … over those of the Exchange Bondholders, in violation of BNY’s duties as Trustee,” the letter said. Griesa disagreed, saying it was illegal for Argentina to deposit money intended for the exchange bondholders and ordered the bank to hold the funds.

Way richer.

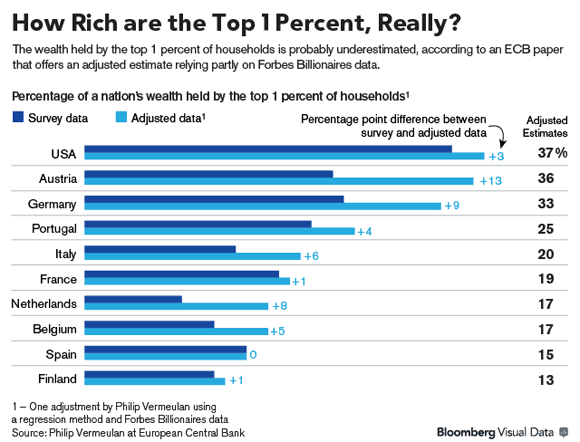

• The 1% May Be Richer Than You Think (Bloomberg)

The 1% is literally rich beyond measure, depriving nations of billions in tax revenue and obscuring shifts in global inequality. Research conducted separately by European Central Bank economist Philip Vermeulen and London School of Economics’ Gabriel Zucman show the wealth of the super-affluent – hidden by tax shelters and nonresponse to questionnaires – is undercounted. Correcting for similar lapses in income data almost erases progress made from 1988 to 2008 in narrowing the gap between the world’s rich and poor, World Bank research found. “We always suspected there was some low-balling of the top 1%,” said Joseph Stiglitz, a Nobel-prize winning economist and author of “The Price of Inequality. ‘‘There’s a growing sense that our system is rigged and unfair.’’

Failure to get a better handle on the actual amount of wealth and income means economists and policy makers don’t have a proper understanding of the degree of disparity, which represents a hurdle in addressing it. For instance, knowing that earnings and assets are more concentrated could spur support for changing the tax structure, Zucman said. ‘‘If you don’t have a good idea of what the world looks like, it’s hard to determine what the effects of policies will be,” said Carter Price, senior mathematician at the Center for Equitable Growth in Washington, which focuses on issues of economic inequality. “Looking retrospectively, it’s hard to assess what the effects of a policy were.”

Wait for the first western case.

• Malaria Cases Mix With Ebola Amid ‘Slow Motion Disaster’ (Bloomberg)

As the death toll rises in West Africa amid the worst Ebola outbreak on record, a separate threat is compounding the problem: the rainy season and the malaria cases that come with it. In Sierra Leone, with the most Ebola cases in the epidemic, a fearful population is failing to seek medical attention for any diseases, health officials say. If they have malaria, the feeling is they don’t want to go near a hospital with Ebola cases. If it’s Ebola, they don’t believe the hospitals can help them anyway.

It’s a widening problem complicated by the fact that Ebola, malaria and cholera share common symptoms early on, including fever and vomiting, which can cause confusion among patients, said Cyprien Fabre, head of the West Africa office of the European Commission’s humanitarian aid department. “We now have increased mortality for these other diseases” as well, Fabre said by telephone from Freetown, the country’s capital, after visiting Ebola treatment centers in Kenema and Kailahun near the eastern border. “This is a slow-motion disaster.”

Until we die.

• Deep Water Fracking Next Frontier for Offshore Drilling (Bloomberg)

Energy companies are taking their controversial fracking operations from the land to the sea – to deep waters off the U.S., South American and African coasts. Cracking rocks underground to allow oil and gas to flow more freely into wells has grown into one of the most lucrative industry practices of the past century. The technique is also widely condemned as a source of groundwater contamination. The question now is how will that debate play out as the equipment moves out into the deep blue. For now, caution from all sides is the operative word. “It’s the most challenging, harshest environment that we’ll be working in,” said Ron Dusterhoft, an engineer at Halliburton, the world’s largest fracker. “You just can’t afford hiccups.” Offshore fracking is a part of a broader industrywide strategy to make billion-dollar deep-sea developments pay off. The practice has been around for two decades yet only in the past few years have advances in technology and vast offshore discoveries combined to make large scale fracking feasible.

While fracking is also moving off the coasts of Brazil and Africa, the big play is in the Gulf of Mexico, where wells more than 100 miles from the coastline must traverse water depths of a mile or more and can cost almost $100 million to drill. At sea, water flowing back from fracked wells is cleaned up on large platforms near the well by filtering out oil and other contaminants. The treated wastewater is then dumped overboard into the vast expanse of the Gulf of Mexico, where dilution renders it harmless, according to companies and regulators. The treatment process is mandated under Environmental Protection Agency regulations. In California, where producers are fracking offshore in existing fields, critics led by the Environmental Defense Center have asked federal regulators to ban the practice off the West Coast until more is known about its effects.

And so we go.

• Human Activity Triples Mercury Levels In Ocean Surface Waters (Guardian)

The amount of mercury near the surface of many of the world’s oceans has tripled as the result of our polluting activities, a new study has found, with potentially damaging implications for marine life as the result of the accumulation of the toxic metal. Mercury is accumulating in the surface layers of the seas faster than in the deep ocean, as we pour the element into the atmosphere and seas from a variety of sources, including mines, coal-fired power plants and sewage. Mercury is toxic to humans and marine life, and accumulates in our bodies over time as we are exposed to sources of it. Since the industrial revolution, we have tripled the mercury content of shallow ocean layers, according to the letter published in the peer-review journal Nature on Thursday. Mercury can be widely dispersed across the globe when it is deposited in water and the air, the authors said, so even parts of the globe remote from industrial sources can quickly suffer elevated levels of the toxic material.

For several years, scientists have warned that pregnant women and small children should limit their consumption of certain fish, including swordfish and king mackerel, because toxic metals including mercury and lead have been accumulating in these species to a degree that made their over-consumption dangerous to human health. Pregnant women are particularly at risk because the metals can accumulate in the growing foetus, and in sufficient quantities can cause serious developmental disorders. The scientists behind Thursday’s letter to Nature, including researchers from the prestigious Woods Hole Oceanographic Institution in the US, stopped short of warning on the dangers to human health from our pouring of mercury into the oceans. However, they said, further research could yield more advice on the potential impacts: “This information may aid our understanding of the processes and the depths at which inorganic mercury species are converted into toxic methyl mercury and subsequently bioaccumulated in marine food webs.”

Home › Forums › Debt Rattle Aug 7 2014: Europe Teeters On The Edge