DPC Foundry, Detroit Shipbuilding Co., Wyandotte, Michigan 1915

Insanity. Marine Le Pen will become a lot more popular now in France.

• Attack at Paris Satirical Magazine Office Kills 12 People (WSJ)

Armed men stormed the Paris offices of French satirical magazine Charlie Hebdo on Wednesday morning, killing 12 people and injuring more, French President François Hollande said. The men opened fire inside the magazine’s offices using automatic AK-47 rifles before fleeing, a police officer said. In November 2011, Charlie Hebdo’s headquarters were gutted by fire, hours before a special issue of the weekly featuring the Prophet Muhammad appeared on newsstands. The weekly has often tested France’s secular dogma, printing caricatures of the prophet on several occasions. Since the arson attack, the weekly has moved to a new location, which was guarded by police. Two of the victims in Wednesday’s shooting were police, an officer on the scene said.

The 2011 fire caused no injuries but spurred debate over press freedom and religious tolerance in France, which is home to Europe’s largest Muslim population. The special issue put a caricature of the prophet on its front page, quoting him as promising “100 lashes if you don’t die from laughter.” Several journalists received anonymous threats and its website was hacked, according to French officials. In 2012, France closed embassies and French schools in 20 countries after the weekly published a series of cartoons. In 2006, the paper reprinted images of Muhammad that had appeared in a Danish magazine a year before. The next year, it published a picture of Muhammad crying, with the tagline “It’s hard to be loved by idiots.” The Grand Mosque of Paris and the Union of Islamic Organizations of France filed slander charges, but a French court cleared the paper.

Suggestive title. Answer: no. What happened is an editorial meeting was going on to prepare a special issue, named Sharia Hebdo, with the prophet Mohamed as guest editor.

• Is Attack Linked to Novel Depicting France Under Islamist President? (Bloomberg)

“Submission,” a book by Michel Houellebecq released today, is sparking controversy with a fictional France of the future led by an Islamic party and a Muslim president who bans women from the workplace. In his sixth novel, the award-winning French author plays on fears that western societies are being inundated by the influence of Islam, a worry that this month drew thousands in anti-Islamist protests in Germany. In the novel, Houellebecq has the imaginary “Muslim Fraternity” party winning a presidential election in France against the nationalist, anti-immigration National Front. “A pathetic and provocative farce,” is how Liberation characterized the book in a Jan. 4 review that scathingly said the novelist is “showing signs of waning writing skills.”

Political analyst Franz-Olivier Giesbert in newspaper Le Parisien yesterday was kinder, calling it a “smart satire,” adding that “it’s a writers’ book, not a political one.” National Front’s leader Marine Le Pen, who appears in the 320-page novel, said on France Info radio on Jan. 5 that “it’s fiction that could become reality one day.” On the same day, President Francois Hollande said on France Inter radio he would read the book “because it’s sparking a debate,” while warning that France has always had “century after century, this inclination toward decay, decline and compulsive pessimism.” In an interview on France 2 TV last night, Houellebecq denied that he was being a scaremonger.

“I don’t think the Islam in my book is the kind people are afraid of,” he said. “I’m not going to avoid a subject because it’s controversial.” Hollande and German Chancellor Angela Merkel plan to discuss their respective countries’ struggle with Islamophobia, anti-immigration protests and the rise of Europe’s nationalist parties at an informal dinner in Strasbourg on January 11 organized by the European Parliament President Martin Schulz. Houellebecq’s book is set in France in 2022. It has the fictional Muslim Fraternity’s chief, Mohammed Ben Abbes, beating Le Pen, with Socialists, centrists, and Nicolas Sarkozy’s UMP party rallying behind him to block the National Front.

Wow: “Gross is putting himself way out on a limb: Not one of Wall Street s professional forecasters predict the S&P 500 will drop in 2015.” Wow.

• Bill Gross Calls It: 2015 Is Going to Be Terrible (Bloomberg)

Bill Gross, bond king, ousted executive, self-styled poet of the markets, has a bold, depressing prediction for 2015, and he’s not couching it in any of his usual metaphor: The good times are over, he wrote in his January investment outlook note. By the end of 2015, he goes on, there will be minus signs in front of returns for many asset classes. Gross is putting himself way out on a limb: Not one of Wall Street s professional forecasters predict the S&P 500 will drop in 2015. Their average estimate calls for an 8.1% rise. And while the global economy looks weak, the U.S. has been heating up, with GDP up 5% in the third quarter. These gloomy predictions come without Gross s usual colorful commentary. At Pimco, his monthly notes made reference to Flavor Flav and Paris Hilton. Since leaving for Janus Capital Group in September, he’s riffed on domestic violence in the NFL, the porosity of sand and the joys of dancing with his wife.

This month, Gross is almost all business. The trouble for the world s economy is that ultra low interest rates are holding back growth rather than stimulating it, he warns. After years of rising markets, investors are facing too much risk for the prospect of low returns. The time for risk taking has passed, he writes. Gross admits he’s taking his own risk with this call. Even if he’s completely right that the bear market is over, he could very well be a year or two early. And even if he’s right about economic growth, he could be wrong about how the market reacts to it. Gross advises buying Treasury and high-quality corporate bonds, but they could be hurt if U.S. interest rates rise this year.

He also puts a word in for stocks of companies with low debt, attractive dividends and diversified revenues both operationally and geographically. But as Causeway Capital Management s Sarah Ketterer warned, those high-quality dividend payers have already soared and could have trouble meeting expectations in the next few years. Gross has been wrong before, most famously in his predictions that bond yields would rise when the Federal Reserve ended quantitative easing. But maybe this time he sees something other market observers don’t. As Gross writes, deploying the commentary’s only off-color metaphor: There comes a time when common sense must recognize that the king has no clothes, or at least that he is down to his Fruit of the Loom briefs.

Perhaps when he says it people actually will wake up.

• Bill Gross Says the Good Times Are Over (Bloomberg)

Bill Gross, the former manager of the world’s largest bond fund, said prices for many assets will fall this year as record-low interest rates fail to restore sufficient economic growth. With global expansion still sputtering after years of interest rates near zero, investors will gradually seek alternatives to risky assets, Gross wrote today in an investment outlook for Janus Capital, where he runs the $1.2 billion Janus Global Unconstrained Bond Fund. “When the year is done, there will be minus signs in front of returns for many asset classes,” Gross, 70, wrote in the outlook. “The good times are over.” Six years after the end of the financial crisis, borrowing costs in the world’s richest nations are stuck near zero, a sign investors have little confidence that their economies will strengthen.

Gross, the former chief investment officer of Pacific Investment Management Co. who left that firm in September to join Janus, has argued the Federal Reserve won’t raise interest rates until late this year if at all as falling oil prices and a stronger U.S. dollar limit the central bank’s room to increase borrowing costs. The benchmark U.S. 10-year yield fell to 1.99% today, and bonds in the Bank of America Merrill Lynch Global Broad Market Sovereign Plus Index had an effective yield of 1.28% as of yesterday, the lowest based on data starting in 1996. The all-time 10-year Treasury low is 1.379% on July 25, 2012. Economists predict the yield will rise to 3.06% by end of 2015, according to a Bloomberg News survey with the most recent forecasts given the heaviest weightings.

Stocks plunged yesterday, with the Standard & Poor’s 500 Index dropping 1.8% to 2,020.58 and the Chicago Board Options Exchange Volatility Index increasing for the fifth time in six days. Declines spurred by tumbling oil and concerns Greece will exit the euro have sent American equities to the biggest decline to start a year since 2005, data compiled by Bloomberg show. While timing the end of a bull market is difficult, the next 12 months will probably see a turning point, Gross wrote. “Knowing when the ‘crowd’ has had enough is an often frustrating task, and it behooves an individual with a reputation at stake to stand clear,” he wrote. “As you know, however, moving out of the way has never been my style.”

Yes.

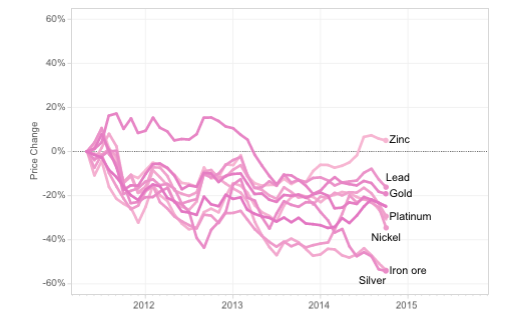

• Not Just Oil: Are Lower Commodity Prices Here To Stay? (CNBC)

Oil isn’t the only commodity that’s gotten cheaper. From nickel to soybean oil, plywood to sugar, global commodity prices have been on a steady decline as the world’s economy has lost momentum. That lower demand helps explain, in part, why nearly everything from crude oil to cotton has been getting cheaper. Sure, some commodity prices are rising. Local supply constraints have pushed prices higher in some parts of the world; transportation costs can also have a big impact on local prices. In the U.S., for example, a drought in California caused the price of vegetables and other food products to spike last year. Prices are also rising for some commodities, especially meats such as beef and chicken, thanks to growing demand from an expanding middle class in the developing world. But the global cost of most commodities has been on a long-term, downward trend since the Great Recession. The chart below is based on global prices, in dollars, assembled by the World Bank.

Now, as much of the world slogs through a faltering recovery, there are fears that falling prices in slow-moving economies such as Europe and Japan could spark and extended period of deflation, when the consumer prices of finished goods fall over an extended period. Deflation can be difficult to reverse if businesses and consumers start to cut back on spending and investment, waiting for prices to fall further, setting off an economic contraction that can deepen. European central bankers are scrambling to avoid that amid signs that prices in the euro zone have all but flattened. On Monday, the latest data showed that German inflation slowed to its lowest level in over five years in December; prices inched up at an annual rate of 0.1%, down from 0.5% in November. A widely watched inflation index of the entire euro zone is due out Wednesday. Some analysts think it could show a negative reading for the first time since October 2009.

We’ve seen nothing yet.

• Oil Price Slump Deepens As Drillers Seen Slashing Spending (Telegraph)

Brent crude has slumped to a new five-and-a-half-year low as leading ratings agency Moody’s warns that oil companies could be forced to slash spending by up to 40% this year. The benchmark crude contract fell to as low as $51.64 per barrel in early trading, while West Texas Intermediate oil traded in the US fell 2.2% to $48 per barrel. Earlier, Moody’s Investors Service issued a report warning of broad cuts in spending that could soon hit the entire oil and gas industry as companies move to protect their dwindling profit margins. The agency fears that, should prices remain below $60 per barrel for a significant period, companies in North America will slash capital spending by up to 40%.

“If oil prices remain at around $55 a barrel through 2015, most of the lost revenue will hit the E&P [exploration and production] companies’ bottom line, which will reduce cash flow available for re-investment,” said Steven Wood, managing director for corporate finance at Moody’s. “As spending in the E&P sector diminishes, oilfield services companies and midstream operators will begin to feel the stress.” However, Moody’s believes that oil majors such as ExxonMobil, Royal Dutch Shell, BP, Chevron and Total are in a stronger position to weather the financial storm caused by lower prices because they have already trimmed their capital expenditure for 2015.

Moody’s is the latest ratings agency to issue a major warning about the impact that falling oil prices will have on exploration and production companies. Standard & Poor’s said last month that the dramatic deterioration in the oil price outlook had prompted it to take a number of “rating actions” on European oil and gas majors including Shell, BP, and BG Group. Meanwhile, Saudi Arabia’s King Abdullah bin Abdul-Aziz al-Saud has said that a weak global economy was to blame for the current slide in prices, which will place his kingdom under severe economic stress. In a speech read out on state television by Crown Prince Salman, the king said that Saudi will deal with the current fall in oil prices “with a firm will”. The 91-year-old monarch of the world’s largest oil exporter was recently admitted into hospital, raising concerns over succession in the kingdom.

Saudi Arabia was instrumental in convincing the other members of OPEC not to cut output in November, a decision which triggered the current sharp falls in prices. The kingdom, which has the capacity to pump up to 12.5m barrels per day (bpd) of crude), this week discounted its oil heavily to European and US customers as it seeks to protect its market share. European buyers can now pay $4.65 per barrel less than for the Brent reference price for Saudi crude. “There is little reason at present to expect any end to the nose-diving oil prices,” said analysts at Commerzbank.

Fifth Third Bancorp 2 years ago: “The oil and natural gas sector represents a tremendous growth opportunity.”

• How the Bear Market in Crude Oil Has Polluted Non-Energy Stocks (Bloomberg)

Perusing the list of the biggest stock-market losers since the price of oil peaked in June yields some predictable results. You have your large-cap energy companies like Transocean, Denbury, Naborsm Noble and Halliburton, all down at least 45%. Yet mixed in with all the obvious ugliness are some names that bring to mind the question asked of Billy Joel by those drinkers at the piano bar, or perhaps even some of the wedding guests who watched him walk down the aisle with Christie Brinkley: Man, what are you doing here? The answer illustrates how much of an impact the energy industry has had on the bottom line of corporate America, whether it’s companies profiting from the boom in domestic production or those that made big investments based on the premise that fuel will always be expensive. As such it helps explain why the entire stock market, not just the energy companies, tends to freak out when oil heads lower rapidly.

The big bets on high energy prices made by companies like Ford (down 13% since oil peaked on June 20) or Tesla Motors (down 10%) or Boeing (down 3.9%) jump immediately to mind. Not so obvious, unless you follow the stock closely, is the investment made by Fifth Third Bancorp, one of the regional lenders that tried to chase the fracking boom. (It’s down 12% since June 20.) Here’s how the company’s management described the rationale for the launch of a new national energy banking team two years ago: “The energy sector is a rapidly growing industry,” said the announcement. The new team “demonstrates our commitment to providing dedicated banking services to this evolving sector. The oil and natural gas sector represents a tremendous growth opportunity.” The sector certainly is “evolving.” Fitch Ratings last month identified regional banks lifted by the shale boom that now face potential credit pressures in loans related to the industry. Oil prices below $50 a barrel, like now, would likely trigger a jump in credit losses, Fitch said.

Fitch’s list of banks with high concentrations of loans to the industry is topped by BOK Financial, which is down 13% since June 20.; Cullen/Frost, down 16%; Hancock, down 19%; Comerica, down 14%; and Amergy Bank of Texas, which is down 13%. Losses are even worse among the industrial companies that provide the services and sell the pipes, valves and assorted doodads used to pump oil and gas. Fluor Corp. an engineering, maintenance and project management firm that counted on the oil and gas industry for 42% of its revenue in 2013, is down 27% since June 20. Flowserve Corp., whose pumps and valves are used in refineries and pipelines, is off about the same amount. Caterpillar, Joy Global, Allegheny, Dover, Jacobs Engineering and Quanta Services are all down more than 20% since oil peaked at almost $108.

Oh come on, let’s get real.

• As Oil Drops Below $50, Can There Be Too Much of a Good Thing? (BW)

Oil falls below $50 a barrel on Jan. 5, and the Dow Jones Industrial Average plunges nearly 330 points. Seems like an open-and-shut case that the price plunge is getting to be a problem. People remember that in 1998, a sharp decline in the price of oil contributed to a Russian default that rocked the global financial system. Not quite. Cheaper oil is still creating more winners than losers. Far more people live in oil-importing countries than live in oil-exporting countries. The U.S., for one, remains a net importer. The well-publicized travails of U.S. shale oil producers are small compared with the gains by American consumers and businesses that are paying less for gasoline, diesel, jet fuel, petrochemicals, and the like. With fuel prices down, people are driving more miles and buying more cars and trucks.

Do the math: Close to 70% of the U.S. economy is consumer spending, which will gain from cheaper crude. Only about 10% is capital spending, of which 10% to 15% is the energy sector. That comes to roughly 1% of U.S. output, which might decline 20% this year, making it a relative drop in the bucket of U.S. gross domestic product, says Nariman Behravesh, chief economist for IHS Global Insight. Why, then, did stock prices fall when West Texas Intermediate for February delivery dropped nearly $3 a barrel on Jan. 5, to $49.89? Mostly because of market fears about global growth, which weighed down both stocks and oil prices, says Gus Faucher, a senior economist at PNC Financial Services. In other words, the latest drop in oil is a symptom, not a cause, of economic weakness, Faucher says. “Anyone who thinks that lower oil/gasoline prices is a net negative for the U.S. (and the global economy) is brain dead, economically speaking!” argues a Dec. 23 report by Faucher’s boss, PNC Chief Economist Stuart Hoffman.

Try and trick the Germans?!

• ECB Considering Three Approaches To QE (Reuters)

The European Central Bank is considering three possible options for buying government bonds ahead of its Jan. 22 policy meeting, Dutch newspaper Het Financieele Dagblad reported on Tuesday, citing unnamed sources. As fears grow that cheaper oil will tip the euro zone into deflation, speculation is rife that the ECB will unveil plans for mass purchases of euro zone government bonds with new money, a policy known as quantitative easing, as soon as this month. According to the paper, one option officials are considering is to pump liquidity into the financial system by having the ECB itself buy government bonds in a quantity proportionate to the given member state’s shareholding in the central bank.

A second option is for the ECB to buy only triple-A rated government bonds, driving their yields down to zero or into negative territory. The hope is that this would push investors into buying riskier sovereign and corporate debt. The third option is similar to the first, but national central banks would do the buying, meaning that the risk would “in principle” remain with the country in question, the paper said.

Hot air.

• Germany Prepares For Possible Greek Exit From Eurozone (Reuters)

Germany is making contingency plans for the possible departure of Greece from the euro zone, including the impact of any run on a bank, tabloid newspaper Bild reported, citing unnamed government sources. The newspaper said the government was running scenarios for the Jan. 25 Greek election in case of a victory by the leftwing Syriza party, which wants to cancel austerity measures and a part of the Greek debt. In a report in the Wednesday issue of the paper, Bild said government experts were concerned about a possible bank collapse if customers storm Greek institutions to secure euro deposits in the event that Greece leaves the zone.

The European Union banking union would then have to intervene with a bailout worth billions, the paper said. Der Spiegel magazine reported on Saturday that Berlin considers a Greek exit almost unavoidable if Syriza wins, but believes the euro zone would be able to cope. Vice Chancellor Sigmar Gabriel said on Sunday that Germany wants Greece to stay and there are no contingency plans to the contrary, while noting the euro zone has become far more stable in recent years. As the euro zone’s paymaster, Germany is insisting that Greece stick to austerity and not backtrack on its bailout commitments, especially as it does not want to open the door for other struggling members to relax reform efforts.

Right. And they have their pet hamsters doing the calculating.

• Germany, France Take Calculated Risk With ‘Grexit’ Talk (Reuters)

Evoking a possible Greek exit from the euro zone, Germany and France are taking a coordinated and calculated risk in the hope of averting a leftist victory in Greece’s general election on Jan. 25. The intention, according to Michael Huether, head of Germany’s IW economic institute, is to make clear that other euro area countries “can get on well without Greece, but Greece cannot get on without Europe”, and to warn that the left-wing Syriza party would bring disaster on the country. Syriza leader Alexis Tsipras, whose party leads in opinion polls, insists he wants to keep Greece in the euro. However, he has promised to end austerity imposed by foreign creditors under the country’s bailout deal if he wins power, and wants part of the €240 billion lent by the EU and IMF written off.

The risk is that the European Union’s two main powers are seen by Greeks as interfering and threatening them, provoking a backlash after a six-year recession that shrunk their economy by 20% and put one in four workers out of a job. French President Francois Hollande said on Monday it was up to the Greek people to decide whether they wanted to stay in the single currency, while a German magazine reported that Berlin no longer feared a “Grexit” would endanger the entire euro area. Chancellor Angela Merkel’s spokesman did not explicitly deny the weekend “Der Spiegel” report but said: “The aim has been to stabilize the euro zone with all its members, including Greece. There has been no change in our stance.”

Merkel and Hollande conferred by telephone during the winter holidays and will meet in Strasbourg on Sunday with European Parliament President Martin Schulz for what a French diplomatic source insisted were not crisis talks on Greece. Should center-right Prime Minister Antonis Samaras lose power in the election, the real issue was how a Syriza-led government might seek to reschedule Greece’s debt, not its place in the euro, the French source said. Paris and Berlin have underlined that any new government in Athens would have to honor the country’s obligation to repay the bailout loans received since 2010. In an article in the Huffington Post, Tsipras accused German conservatives of spreading “old wives’ tales”, singling out Finance Minister Wolfgang Schaeuble. Syriza, a coalition of former communist and independent leftist groups, “is not an ogre, or a big threat to Europe, but the voice of reason,” he wrote.

Tsipras himself sees it this way:

• Greece On the Cusp of a Historic Change (Alexis Tsipras, SYRIZA)

Greece is on the cusp of a historic change. SYRIZA is no longer just a hope for Greece and the Greek people. It is also an expectation of a change of course for the whole of Europe. Because Europe will not come out of the crisis without a policy change, and the victory of SYRIZA in the 25th of January elections will strengthen the forces of change. Because the dead end in Greece is the dead end of today’s Europe. On January 25th, the Greek people are called to make history with their vote, to trail a space of change and hope of all people across Europe by condemning the failed memoranda of austerity, proving that when people want to, when they dare, and when they overcome fear, then things can change. The expectations alone of political change in Greece, has already begun to change things in Europe. 2015 is not 2012

SYRIZA is not an ogre, or a big threat to Europe, but the voice of reason. It’s the alarm clock which will lift Europe from its lethargy and sleepwalking. This is why SYRIZA is no longer treated as a major threat like it was in 2012, but as a challenge to change. By all? Not by all. A small minority, centered on the conservative leadership of the German government and a part of the populist press, insists on rehashing old wives’ tales and Grexit stories. Just like Mr. Samaras in Greece, they can no longer convince anyone. Now that the Greek people have experienced his government, they know how to tell the lies from the truth. Mr. Samaras offers no other program except continuing with the failed MOU of austerity.

It has committed itself and others to new wage and pension cuts, new tax increases, in the framework of accumulated income cuts and over- taxation of six whole years. He asks Greek citizens to vote for him so that he can implement the new memorandum. It is precisely because he has committed to austerity, that he interprets the rejection of this failed and destructive policy as a supposedly unilateral action. He is essentially hiding that Greece as a Eurozone member is committed to targets and not to the political means by which those targets are achieved. For this reason, and unlike the ruling party of Nea Dimokratia, SYRIZA has committed to the Greek people to apply from the first days of its’ administration a specific, cost-efficient and fiscally balanced program, “The Thessaloniki Program” regardless of our negotiation with our lenders.

The editor told them not to call it deflation.

• Eurozone Inflation Turns Negative For First Time Since October 2009 (Reuters)

Euro zone consumer prices fell by more than expected in December because of much cheaper energy, a first estimate by the European statistic office showed in data that is likely to trigger the European Central Bank’s government bond buying program. Eurostat said inflation in the 18 countries using the euro in December was -0.2% year-on-year, down from 0.3% year-on-year in November. The last time euro zone inflation was negative was in October 2009, when it was -0.1%. Economists polled by Reuters had expected a -0.1% year-on-year fall in prices. The ECB wants to keep inflation below but close to 2% over the medium term. Eurostat said that core inflation, which excludes the volatile energy and unprocessed food prices, was stable at 0.7% year-on-year in December – the same level as in November and October. But energy prices plunged 6.3% year-on-year last month and unprocessed food was 1.0% cheaper, pulling down the overall index despite a 1.2% rise in the cost of services.

The ECB is concerned that a prolonged period of very low inflation could change inflation expectations of consumers and make them hold back their purchases in the hope of even lower prices, triggering deflation. Because the ECB’s interest rates are already at rock bottom, the bank is preparing a program of printing money to buy government bonds on the secondary market to inject even more cash into the economy, boost demand and make prices rise faster. Economists expect the decision to launch such a bond buying program could be made as soon as the ECB’s next meeting on January 22. “We are in technical preparations to adjust the size, speed and compositions of our measures early 2015, should it become necessary to react to a too long period of low inflation. There is unanimity within the Governing Council on this,” ECB President Mario Draghi said on January 1. Inflation in the euro zone has below 1% – or what the ECB calls the danger zone – since October 2013.

There we go again. Maybe the ECB is behind this.

• Greek 10-Year Bond Yields Exceed 10% for First Time Since 2013 (Bloomberg)

For the first time in 15 months, Greek 10-year government bond yields are back above 10%. The rate on the securities climbed to 10.18% today as investors abandoned the bonds in the run-up to a Jan. 25 election that Prime Minister Antonis Samaras said will determine Greece’s euro membership. Greek stocks also fell, posting the biggest decline among 18 western-European markets. The double-digit yield is reminiscent of the euro region’s debt crisis. In 2012, Greece’s 10-year rates climbed as high as 44.21% before the nation held the biggest reorganization of sovereign debt in history.

Greek 10-year yields increased 44 basis points, or 0.44 %age point, to 10.18% at 11:02 a.m. London time. The 2% bond due in February 2024 fell 1.885, or 18.85 euros per 1,000-euro ($1,185) face amount, to 60.585. The nation’s three-year rate jumped 60 basis points to 14.65%. The ASE Index of stocks fell 2.7%, set for the lowest close since November 2012. With a 29% slump, the ASE posted the world’s worst performance among equity indexes after Russia last year.

We said long ago that the dollar would rise.

• Euro’s Drop is a Turning Point for Central Banks Reserves (Bloomberg)

Central banks and reserve managers are breaking from past practice by showing little appetite to add euros as the currency tumbles. The total amount of reserves held in euros fell 8.1% in the third quarter, more than the currency’s 7.8% decline in the period against the dollar, according to the most recent figures from the International Monetary Fund. The last two times the euro depreciated 7% or more in a quarter, 2011 and 2010, holdings declined much less. The data suggest reserve managers are passing up the chance to buy euros while they’re cheap, removing a key pillar of support. In August, European Central Bank President Mario Draghi cited the drop in central banks’ euro holdings as a factor that would help weaken the exchange rate and ultimately boost the region’s faltering economy.

“Central banks have found new reasons not to feel comfortable with the euro,” Stephen Jen, managing partner and co-founder of SLJ Macro, said. “Nobody wants to have a negative yield. You’re not keeping a currency to lose money.” The ECB has experimented with negative interest rates on deposits in an attempt to draw money out of safe government debt and into the broader economy. Yields on two-year notes in Germany, the Netherlands and France are all below zero on speculation the ECB is losing the battle against deflation. Policy makers are signaling they are ready to step up the fight by expanding the money supply through further stimulus, such as purchasing government debt, that typically weigh on a currency’s value.

Adding to the pressure is concern that Draghi won’t be able to hold the currency bloc together amid signs Greece may quit the euro area after its Jan. 25 election. The 19-nation euro fell in each of the past six months, dropping to $1.1843 today, its lowest level since February 2006. A spokesman for the Frankfurt-based ECB, who asked not to be identified, said yesterday by e-mail that the international role of the euro is primarily determined by market forces and the central bank neither hinders nor promotes it. The amount of euros held in allocated reserves – or those where the currency is specified – fell to $1.4 trillion in the third quarter, or 22.6% of the total, from $1.5 trillion, or 24.1%, at the end of June, according to figures published by the IMF on Dec. 31. The proportion is the lowest since 2002 and down from as much as 28% in 2009.

“We expect the ECB to announce a broad-based asset-purchase program including government bonds.”

• Eurozone Prices Seen Falling as Risk of Deflation Spiral Mounts (Bloomberg)

Consumer prices in the euro area probably fell for the first time in more than five years last month, pushing the European Central Bank closer to adding stimulus as it battles to revive inflation. Prices dropped an annual 0.1% in December, according to the median forecast of economists in a Bloomberg survey. That would be the first decline since October 2009. ECB officials are working on a plan to buy government bonds as they strive to prevent a deflationary spiral of falling prices and households postponing spending, a risk President Mario Draghi has said can’t be “entirely excluded.” They may use a gathering tomorrow to weigh options for a quantitative-easing program that may be announced at their Jan. 22 policy meeting.

“Inflation will most likely fall even further in January and remain extremely low all year long,” said Evelyn Herrmann, European economist at BNP Paribas SA in London. “We expect the ECB to announce a broad-based asset-purchase program including government bonds.” A sluggish economy and plunging oil prices are damping inflation across the euro region. Consumer prices are falling on an annual basis in Spain and Greece, while data yesterday showed inflation in Germany at 0.1%, its weakest since 2009. Crude oil prices have fallen about 50% in the past year amid a supply glut. Core euro-zone inflation, which strips out volatile items such as energy, food, tobacco and alcohol, is forecast to have increased 0.7% year-on-year in December.

Eurostat, the EU’s statistics office, will publish the data at 11 a.m. in Luxembourg, along with its unemployment report for November. ECB officials have taken different approaches in analyzing the impact of plunging oil prices on the economy. While Draghi has warned of a dis-anchoring of inflation expectations and signaled support for QE, Bundesbank President Jens Weidmann favors not acting at this time, arguing that the drop could prove to be a “mini-stimulus package.”

“Daniel Stelter at think tank Beyond the Obvious has even called for giving €5,000 to €10,000 to each citizen. “It has to be massive if it is going to have any effect,” he says.”

• Operation Helicopter: Could Free Money Help the Euro Zone? (Spiegel)

It sounds at first like a crazy thought experiment: One morning, every resident of the euro zone comes home to find a check in their mailbox worth over €500 euros ($597) and possibly as much as €3,000. A gift, just like that, sent by the ECB in Frankfurt. The scenario is less absurd than it may sound. Indeed, many serious academics and financial experts are demanding exactly that. They want ECB chief Mario Draghi to fire up the printing presses and hand out money directly to the people. The logic behind the idea is that recipients of the money will head to the shops, helping to turn around a paralyzed economy in the common currency area. In response, companies would have to increase production and hire more workers, leading to both economic growth and a needed increase in prices because of the surge in demand.

Currently, the inflation rate is barely above zero and fears of a horror deflation scenario of the kind seen during the Great Depression in the United States are haunting the euro zone. The ECB, whose main task is euro stability, has lost control. In this desperate situation, an increasing number of economists and finance professionals are promoting the concept of “helicopter money,” tantamount to dispersing cash across the country by way of helicopter. The idea, which even Nobel Prize-winning economist Milton Friedman once found attractive, has triggered ferocious debates between central bank officials in Europe and academics. For backers, there’s more to this than just a new instrument. They are questioning cast-iron doctrines of monetary policy. One thing, after all, is becoming increasingly clear: Draghi and his fellow central bank leaders have exhausted all traditional means for combatting deflation.

The failure of these efforts can be easily explained. Thus far, central banks have primarily provided funding to financial institutions. The ECB provided banks with loans at low interest rates or purchased risky securities from them in the hope that they would in turn issue more loans to companies and consumers. The problem is that many households and firms are so far in debt already that they are eschewing any new credit, meaning the money isn’t ultimately making its way to the real economy as hoped. Sylvain Broyer at French investment bank Natixis, says, “It would make much more sense to take the money the ECB wants to deploy in the fight against deflation and distribute it directly to the people.” Draghi has calculated expenditures of a trillion euros for his emergency program, funds that would be sufficient to provide each euro zone citizen with a gift of around €3,000.

Daniel Stelter at think tank Beyond the Obvious, has even called for giving €5,000 to €10,000 to each citizen. “It has to be massive if it is going to have any effect,” he says. Stelter freely admits that such figures are estimates. After all, not a single central bank has ever tried such a daring experiment. Many academics have based their calculations on experiences in the United States, where the government has in the past provided cash gifts to taxpayers in the form of rebates in order to shore up the economy. Oxford economist John Muellbauer, for one, looks back to 2001. After the Dot.com crash, the US gave all taxpayers a $300 rebate. On the basis of the experience at the time, Muellbauer calculates that €500 per capita would be sufficient to spur the euro zone. “It (the helicopter money) would even be much cheaper for the ECB than the current programs>],” the academic says.

Ambrose doesn’t like Putin.

• Russia’s ‘Perfect Storm’: Reserves Vanish, Derivatives’ Default Warnings (AEP)

Russia’s foreign reserves have dropped to the lowest level since the Lehman crisis and are vanishing at an unsustainable rate as the country struggles to defends the rouble against capital flight. Central bank data show that a blitz of currency intervention depleted reserves by $26bn in the two weeks to December 26, the fastest pace of erosion since the crisis in Ukraine erupted early last year. Credit defaults swaps (CDS) measuring bankruptcy risk for Russia spiked violently on Tuesday, surging by 100 basis points to 630, before falling back slightly. Markit says this implies a 32% expectation of a sovereign default over the next five years, the highest since Western sanctions and crumbling oil prices combined to cripple the Russian economy. Total reserves have fallen from $511bn to $388bn in a year. The Kremlin has already committed a third of what remains to bolster the domestic economy in 2015, greatly reducing the amount that can be used to defend the rouble.

The Institute for International Finance (IIF) says the danger line is $330bn, given the dollar liabilities of Russian companies and chronic capital flight. Currency intervention did stabilise the exchange rate in late December after a spectacular crash threatened to spin out of control, but relief is proving short-lived. The rouble weakened sharply to 64 against the dollar on Tuesday. It has slumped moe than 20% since Christmas, with increasing contagion to Belarus, Georgia and other closely-linked economies. There are signs that Russia’s crisis may undermine President Vladimir’s Putin’s Eurasian Economic Union before it has got off the ground. Belarus’s Alexander Lukashenko is already insisting that trade be carried out in US dollars, while Kazakhstan’s Nursultan Nazarbayev warned that the Russian crash poses a “major risk” to the new venture.

The rouble is trading in lockstep with Brent crude, which has continued its relentless slide this week, falling to a five-year low of $51.50 a barrel. “If oil drops to $45 or lower and stays there, Russia is going to face a big problem,” said Mikhail Liluashvili, from Oxford Economics. “The central bank will try to smooth volatility but they will have to let the rouble fall and this could push inflation to 20%.” Under the Russian central bank’s “emergency scenario”, GDP may contract by as much as 4.7% this year if oil settles at $60. The damage could be worse following the bank’s contentious decision to raise rates from 9.5% to 17% in December. BNP Paribas says that each 1% rise in rates cuts 0.8% off GDP a year later. BNP’s Tatiana Tchembarova said the situation is more serious than in 2008, when Russia had to spend $170bn to rescue its banks. This time it no longer has enough reserves to cover external debt, and it enters the crisis “twice as levered”.

Why bother?

• Obama Threatens Keystone XL Veto (BBC)

President Barack Obama will veto a bill approving the controversial Keystone XL pipeline if it passes Congress, the White House has said. It is the first major legislation to be introduced in the Republican-controlled Congress and a vote is expected in the House later this week. Spokesman Josh Earnest said the legislation would undermine a “well-established” review process. The $5.4bn (£3.6bn) project was first introduced in 2008. Mr Obama has been critical of the pipeline, saying at the end of last year it would primarily benefit Canadian oil firms and not contribute much to already dropping petrol prices. Environmentalists are also critical of the project, a proposed 1,179-mile (1,897km) pipe that would run from the oil sands in Alberta, Canada, to Steele City, Nebraska, where it could join an existing pipe.

And the project is the subject of a unresolved lawsuit in Nebraska over the route of the pipeline. “There is already a well-established process in place to consider whether or not infrastructure projects like this are in the best interest of the country,” Mr Earnest said on Tuesday. He added that the question of the Nebraska route was “impeding a final conclusion” from the US on the project. Despite the veto threat from the White House, the bill sponsors say they have enough Democratic votes to overcome a procedural hurdle to pass in the Senate.

“The Congress on a bipartisan basis is saying we are approving this project,” said Republican John Hoeven, one of the bill’s sponsors. But Mr Hoeven and Democratic Senator Joe Manchin said they would be open to additional amendments to the bill, a test of the changing political realities of the Senate. Democratic critics of the bill are said to be planning to add measures to prohibit exporting the oil abroad, use American materials in the pipeline construction and increased investment in clean energy. It is unclear if those amendments would gather the two-thirds of votes needed in both chambers to override Mr Obama’s veto.

But took decisions costing trillions of pounds anyway.

• Bank Of England Was Unaware Of Impending Financial Crisis (BBC)

A month before the start of the financial crisis, the Bank of England was apparently unaware of the impending danger, new documents reveal. In a unique insight of its workings, the Bank has published minutes of top-secret meetings of the so-called Court that took place between 2007 and 2009. The minutes show that the Bank did identify liquidity as a “central concern” in July 2007. However no action was taken as a result. The documents show that the Bank also used a series of code names for banks that were in trouble. Royal Bank of Scotland was known as “Phoenix”, and Lloyds as “Lark”. Following publication, Andrew Tyrie MP, the chairman of the Treasury Select Committee, was highly critical of some of the Court’s non-executive directors. He said they had failed to challenge senior executive members, like the then governor, Mervyn King, whom some accuse of failing to prioritise financial stability.

The minutes show that in July 2007, the Court – akin to a company board – spent time discussing staff pensions, open days and new members of the Monetary Policy Committee. Members heard that the Bank was working on a new model to detect risks to the financial system, but there was little suggestion of any impending trouble. Less than a month later, on 9 August, the French bank BNP Paribas came clean about its exposure to sub-prime mortgages, in what some believe was the start of the financial crisis. Six weeks later, despite some turmoil in financial markets, Court members were told to have confidence in the triple oversight of the Bank of England, the Treasury and the then Financial Services Authority (FSA). “The Executive believed that the events of the last month had proven the sense and strength of the tripartite framework,” the minutes asserted for the 12th September, 2007. The next day the banking crisis began in earnest.

Home › Forums › Debt Rattle January 7 2015