Alfred Eisenstaedt Actress Marilyn Monroe at home 1953

The central bank of central banks takes position against central bank policy.

• The World Is Defenceless Against The Next Financial Crisis, Warns BIS (Telegraph)

The world will be unable to fight the next global financial crash as central banks have used up their ammunition trying to tackle the last crises, the Bank of International Settlements has warned. The so-called central bank of central banks launched a scatching critique of global monetary policy in its annual report. The BIS claimed that central banks have backed themselves into a corner after repeatedly cutting interest rates to shore up their economies. These low interest rates have in turn fuelled economic booms, encouraging excessive risk taking. Booms have then turned to busts, which policymakers have responded to with even lower rates.

Claudio Borio, head of the organisation’s monetary and economic department, said: “Persistent exceptionally low rates reflect the central banks’ and market participants’ response to the unusually weak post-crisis recovery as they fumble in the dark in search of new certainties.” “Rather than just reflecting the current weakness, they may in part have contributed to it by fuelling costly financial booms and busts and delaying adjustment. The result is too much debt, too little growth and too low interest rates. “In short, low rates beget lower rates.” The BIS warned that interest rates have now been so low for so long that central banks are unequipped to fight the next crises. “In some jurisdictions, monetary policy is already testing its outer limits, to the point of stretching the boundaries of the unthinkable,” the BIS said.

Policymakers in the eurozone, Denmark, Sweden and Switzerland have taken their interest rates below zero in an attempt to support their economies, contributing to a decline in bond yields. Extraordinarily low interest rates are not a “new equilibrium” said Jaime Caruana, general manager of the BIS, rejecting the theory of so-called “secular stagnation” which some economists blame for the continued decline in global lending rates. “True, there may be secular forces that put downward pressure on equilibrium interest rates … [but] we argue that the current configuration of very low rates is neither inevitable, nor does it represent a new equilibrium,” he said.

“..low rates beget lower rates…”

• BIS Warns Low Interest Rates Could Spell ‘Entrenched Instability’ (AFP)

The Bank of International Settlements warned Sunday that persistently low interest rates were symptoms of a malaise in the global economy that could end in entrenched instability. The Basel-based institution, considered the central bank for central banks, hailed that plunging oil prices had boosted the global economy over the past year. But it cautioned that global debt burdens and financial risks remained too high, while productivity and financial growth were too low, leaving policy makers with little room to maneuvre. “In the long term, this runs the risk of entrenching instability and chronic weakness,” the report said. Claudio Borio, the head of the BIS monetary and economic department, said the “most visible symptom of this predicament is the persistence of ultra-low interest rates.”

“Interest rates have been exceptionally low for an extraordinarily long time,” he said, warning that previously “unthinkable” monetary policies were being so widely used they risked becoming the new norm. A number of countries, including Switzerland, Denmark and Sweden, have in recent months introduced negative rates, meaning investors have to pay to lend money to these states. Between December 2014 and the end of May, around $2.0 trillion in global long-term sovereign debt, much of it issued by euro area sovereigns, was trading at negative yields, BIS said. Key interest rates are lower now than at the height of the financial crisis that began in 2007, it added. “Such yields are unprecedented,” said the report.

The current low rates “are a vivid reminder of the extent to which monetary policy has been overburdened in an attempt to reinvigorate growth,” Borio said. “They have underpinned the contrast between high risk-taking in financial markets, where it can be harmful, and subdued risk-taking in the real economy, where additional investment is badly needed,” he said. Borio warned that the low rates do not just reflect the current weakness in the global economy, but “may in part have contributed to it by fuelling costly financial booms and busts and delaying adjustment.” “The result is too much debt, too little growth and too low interest rates,” he said, stressing that “low rates beget lower rates.”

“..central banks are not commercial entities. Accepting losses is part of its public service mission. Keeping the banking system afloat is part of its core mission.”

• The Staggering Cost Of Central Bank Dependence (Wyplosz)

This weekend’s dramatic events saw the ECB capping emergency assistance to Greece. This column argues that the ECB’s decision is the last of a long string of ECB mistakes in this crisis. Beyond triggering Greece’s Eurozone exit – thus revoking the euro’s irrevocability – it has shattered Eurozone governance and brought the politicisation of the ECB to new heights. Bound to follow are chaos in Greece and agitation of financial markets – both with unknown consequences.

The ECB has decided to maintain its current level of emergency liquidity to Greece (ECB 2015). By refusing to extend additional emergency liquidity, the ECB has decided that Greece must leave the Eurozone. This may be a legal necessity or a political judgement call, or both. Anyway, it raises a host of unpleasant questions about the treatment of a member country and about the independence of the central bank. As anticipated (Wyplosz, 2015), the negotiations between Greece have led nowhere. As a result, Greece is bound to default on all maturing debts in the days and weeks to come. With a primary budget close to balance, the Greek government could have soldiered on until new negotiations about the unavoidable write-down of its debt.

The risk for the Greeks of this ‘default strategy’ has always been that it depended entirely on the ECB’s willingness to continue providing the Greek banking system with liquidity, especially at a time of a bank run by rational depositors who put a non-zero risk of Grexit. Over the last weeks, the ECB has provided the needed liquidity in the face of a “slow-motion run” on Greek banks. Suddenly, on the morning of 28 June, the ECB has stopped providing emergency funding to Greek banks. In a classical self-fulfilling crisis fashion, this decision is bound to turn the “slow-motion run” into a panic. The bank holiday and capital controls announced will create some breathing space, but very briefly. These measures will not prevent the banking system from collapsing.

The natural consequence will be the collapse of the Greek banking system. At that stage, possibly earlier, the Greek authorities will have no choice but to leave the Eurozone and provide banks with the re-created drachma. Why did the ECB freeze its Emergency Liquidity Assistance (ELA) to Greece? The ECB will undoubtedly come up with all sorts of legal justifications. Whether true or not, this will not change the outcome. If the ECB is truly legally bound to stop ELA, this means that the Eurozone architecture is deeply flawed. If not, the ECB will have made a political decision of historical importance. Either way, this is a disastrous step. Whether it likes it or not, every central bank is a lender of last resort to commercial banks. By not keeping the Greek banking system afloat, the ECB is failing on a core responsibility.

One explanation is that the ECB fears losses. This is partly incorrect, partly misguided. It is incorrect because the ELA loans are provided by the Central Bank of Greece. It is the Central Bank of Greece, and therefore the Greek people, which stands to suffer losses from defaults by commercial banks. It is misguided because central banks are not commercial entities. Accepting losses is part of its public service mission. Keeping the banking system afloat is part of its core mission.

Forced into capital controls by legally questionable troika measures. Some partnership.

• Greece Introduces Capital Controls, Keep Banks Shut As Crisis Deepens (Reuters)

Greece will introduce capital controls and keep its banks closed on Monday after international creditors refused to extend the country’s bailout and savers queued to withdraw cash, taking Athens’ standoff to a dangerous new level. The Athens stock exchange will also be closed as the government tries to manage the financial fallout of the disagreement with the EU and IMF. Greece’s banks, kept afloat by emergency funding from the ECB, are on the front line as Athens moves towards defaulting on a €1.6 billion payment due to the IMF on Tuesday. Greece blamed the ECB, which had made it difficult for the banks to open because it froze the level of funding support rather than increasing it to cover a rise in withdrawals from worried depositors, for the moves.

Prime Minister Alexis Tsipras said the decision to reject Greece’s request for a short extension of the bailout program was “an unprecedented act” that called into question the ability of a country to decide an issue affecting its sovereign rights. “This decision led the ECB today to limit the liquidity of Greek banks and forced the central bank of Greece to propose a bank holiday and a restriction on bank withdrawals,” he said in a televised address. Amid drama in Greece, where a clear majority of people want to remain inside the euro, the next few days present a major challenge to the integrity of the 16-year-old euro zone currency bloc. The consequences for markets and the wider financial system are unclear.

Greece’s left-wing Syriza government had for months been negotiating a deal to release funding in time for its IMF payment. Then suddenly, in the early hours of Saturday, Tspiras asked for extra time to enable Greeks to vote in a referendum on the terms of the deal. Creditors turned down this request, leaving little option for Greece but to default, piling further pressure on the country’s banking system.

First they present Tsipras with a do-or-die plan, and now they come with another one again.

• EU Offers Greek Voters 10-Point Plan on June 26 Bailout Offer (Bloomberg)

The European Commission offered Greek voters a 10-point plan for bailout requirements on Sunday, urging Greece to stay in the euro area. The list reflects the state of play as of 8 p.m. on June 26 and was never finished because negotiations broke down when Prime Minister Alexis Tsipras announced on Friday he would seek a referendum. It’s being published now “in the interest of transparency and for the information of the Greek people,” Commission President Jean-Claude Juncker said on Twitter. Juncker will hold a news conference in Brussels at 12:45 p.m. on Monday, the commission said.

The list of measures was never finished or presented to euro-area finance ministers alongside an “outline of a comprehensive deal” because of “the unilateral decision of the Greek authorities to abandon the process,” the European Union’s executive arm said. The plans, published in English and in the process of being translated into Greek, were endorsed by the ECB and IMF, the commission said. The commission said the plans take into account Greek proposals from June 8, June 14, June 22 and June 25, as well as subsequent political and technical talks.

The Greek government hasn’t been informed of any change in the creditors’ proposals after June 25 if there has been one, a Greek government official said in an e-mailed statement. IMF Managing Director Christine Lagarde said she briefed the IMF board on the state of play. “I shared my disappointment and underscored our commitment to continue to engage with the Greek authorities,” Lagarde said in a statement. “I welcome the statements of the Eurogroup and the European Central Bank to make full use of all available instruments to preserve the integrity and stability of the euro area.”

“Democracy? What’s that?”

• Athens Is Being Blackmailed (Philippe Legrain)

“If the Greek government thinks it should hold a referendum, it should hold a referendum. Maybe it would even be the right measure to let the Greek people decide whether they’re ready to accept what needs to be done.” Fine words from Germany’s finance minister, Wolfgang Schäuble, on May 11. Yet on June 26, when prime minister Alexis Tsipras duly announced a referendum on whether the Greek government should accept its creditors’ highly unsatisfactory final offer, Schäuble and other eurozone finance ministers reacted very differently. They cut off negotiations with Athens, sabotaged the referendum, and set Greece on a course for capital controls, default, and potentially even euro exit. Democracy? What’s that?

The creditors have tried to blame Tsipras for the breakdown in negotiations. But it was their stubborn refusal to offer an insolvent Greece the debt relief that its depressed economy desperately needs to recover which backed Tsipras into a corner. In exchange for a short-lived infusion of cash, they were insisting on years of grinding austerity dressed up as “reforms”, as I explained previously. With rapacious creditors intent on pillaging the impoverished Greek economy, Tsipras could scarcely agree to their terms. So he gave Greeks themselves a say, while rightly urging them to vote No. Ironically, the exaggerated fear of Grexit and the emotional association, even after five years of debt bondage, between euro membership and being part of modern Europe might well have led Greeks to vote Yes to the creditors’ iniquitous terms.

But eurozone authorities are so terrified of voters that they have sought to deny Greeks a say. They rejected the Greek government’s request to extend the current EU loan program for a month beyond its expiry on June 30. So, if and when Greeks vote on July 5, the program will have expired, and with it the creditors’ offer on which they will be casting their ballots. It would be funny if it weren’t so sad. [..] In the meantime, the creditors continue to ratchet up the pressure. Following on from the refusal to extend the EU loan program, the ECB on June 28 decided not to provide Greek banks with any additional emergency liquidity to cover cash withdrawals, which have gathered pace over the weekend. That political move forced the Greek government to declare a bank holiday on Monday to prevent a run that would cause the Greek banking system to collapse, along with capital controls to prevent euros draining out of the Greek economy.

“Three days, three crises, and a collective performance that inspires little hope or confidence in their crisis management.”

• A Disaster For Athens And A Colossal Failure For The EU (Guardian)

Five years from its inception, the world’s biggest bailout of a sovereign state will grind to an excruciating halt on Tuesday, theoretically leaving Greece high and dry and on its own under a leftwing government bitterly accusing the EU elite of deliberately using the country as a neo-liberal laboratory. If the experiment has been a disaster for Greece, it is also a colossal failure for Europe, with the result that at the very apex of leadership the EU nowadays resembles an unhappy assembly of squabbling politicians locked in what could not be called an “ever closer union”. Take just the last few days. On Thursday leaders at a summit contemplated formally for the first time, however briefly, the prospect of Britain leaving the EU.

By three o’clock on Friday morning they were all at one another’s throats in an unseemly quarrel over who should take part in accommodating a mere 40,000 refugees from Italy and Greece over two years, and on what terms. On Saturday, 18 governments of the eurozone cut Greece off and initiated a process that could end in pushing Athens out of the currency and perhaps out of the union. Three days, three crises, and a collective performance that inspires little hope or confidence in their crisis management. The air is already thick with recrimination, not just between Greece and the rest of Europe, but among the Europeans. France says that Greece must be saved, Germany says impossible.

The European commission is seeking to revive negotiation that are on their deathbed. The Finnish finance minister, Alex Stubb, is looking forward to the funeral. The IMF is at odds with the Europeans over the levels of Greek debt. Everywhere there is the sight of leaders seeking to escape responsibility for a sorry state of affairs. For weeks, in anticipation of the criticism certain to be directed at them in the event of a Greek collapse, senior German figures have privately been saying: “Well, nobody will be able to say that we did not try our best. At the meeting of eurozone finance ministers on Saturday that ended the Greek bailout, the French finance minister, Michel Sapin, was the only one with enough humility to remark that maybe the Europeans had got some things wrong and that things might have been done differently, according to witnesses.

The US had better get going on the topic.

• US Urges Europe, IMF To Reach Deal To Keep Greece In Eurozone (Reuters)

Top US officials waded in at the weekend to try to help resolve Greece’s financial woes, urging Europe and the IMF to come up with a recovery plan that keeps the country in the eurozone. In a series of separate phone calls on Saturday to IMF Managing Director Christine Lagarde and the finance ministers of Germany and France, Treasury Secretary Jack Lew urged them to “find a sustainable solution that puts Greece on a path toward reform and recovery within the eurozone,” according to a Treasury Department statement on Sunday about the calls. Lew noted it is “important for all parties to continue to work to reach a solution, including a discussion of potential debt relief for Greece,” in the run-up to a planned July 5 referendum in Greece on the terms of a bailout.

Greece is facing a looming Tuesday deadline on a 1.6-billion-euro payment due to the IMF. Earlier Sunday, Greece announced it will impose capital controls and keep its banks shut on Monday, after international creditors refused to extend the country’s bailout. Lew also underscored the need for Greece to adopt “difficult measures to reach a pragmatic compromise with its creditors,” the Treasury statement said. The Treasury spokesperson said senior department officials have also been in regulator communication with Greece and that Lew had spoken to Prime Minister Alexis Tsipras “multiple times” over the past two weeks. The department has urged Greece to work closely with its international partners on planning for a bank holiday and capital controls, the spokesperson said.

President Barack Obama spoke with German Chancellor Angela Merkel on Sunday about the Greek situation. “The two leaders agreed that it was critically important to make every effort to return to a path that will allow Greece to resume reforms and growth within the eurozone,” a White House statement said. “The leaders affirmed that their respective economic teams are carefully monitoring the situation and will remain in close touch.”

“The Eurogroup is an informal group. Thus it is not bound by treaties or written regulations. While unanimity is conventionally adhered to, the Eurogroup president is not bound to explicit rules.”

• The Moral Crusade Against Greece Must Be Opposed (Guardian)

‘This is our political alternative to neoliberalism and to the neoliberal process of European integration: democracy, more democracy and even deeper democracy,” said Alexis Tsipras on 18 January 2014 in a debate organised by the Dutch Socialist party in Amersfoort. Now the moment of deepest democracy looms, as the Greek people go to the polls on Sunday to vote for or against the next round of austerity. Unfortunately, Sunday’s choice will be between endless austerity and immediate chaos. As comfortable as it is to argue from the sidelines that maybe Grexit in the medium term won’t hurt as much as 30 years’ drag on GDP from swingeing repayments, no sane person wants either.

The vision that Syriza swept to power on was that if you spoke truth to the troika plainly and in broad daylight, they would have to acknowledge that austerity was suffocating Greece. They have acknowledged no such thing. Whatever else one could say about the handling of the crisis, and whatever becomes of the euro, Sunday will be the moment that unstoppable democracy meets immovable supra-democracy. The Eurogroup has already won: the Greek people can vote any way they like – but what they want, they cannot have. On Saturday the Eurogroup broke with its tradition of unanimity, issuing a petulant statement “supported by all members except the Greek member”.

Yanis Varoufakis, the Greek finance minister, sought legal advice on whether the group was allowed to exclude him, and received the extraordinary reply: “The Eurogroup is an informal group. Thus it is not bound by treaties or written regulations. While unanimity is conventionally adhered to, the Eurogroup president is not bound to explicit rules.” Or, to put it another way: “We never had any accountability in the first place, sucker.” More striking still is this line of the statement: “The Eurogroup has been open until the very last moment to further support the Greek people through a continued growth-oriented programme.” The measures enforced by the troika have created an economic contraction akin to that caused by war. With unemployment at 25% and youth unemployment at nearly half, 40% of children now live below the poverty line.

The latest offer to Greece promises more of the same. The idea that any of this is oriented towards growth is demonstrably false. The Eurogroup president, Jeroen Dijsselbloem, has started to assert that black is white. [..] These talks did not fail by accident. The Greeks have to be humiliated, because the alternative – of treating them as equal parties or “adults”, as Lagarde wished them to be – would lead to a debate about the Eurogroup: what its foundations are, what accountability would look like, and what its democratic levers are – if indeed it has any. Solidarity with Greece means everyone, in and outside the single currency, forcing this conversation: the country is being sacrificed to maintain a set of delusions that enfeebles us all.

Merkel’s fumble. Dropped ball.

• Cautious Merkel On Verge Of Biggest Risk With ‘Grexit’ (Reuters)

“If you break it, you own it,” former U.S. Secretary of State Colin Powell warned President George W. Bush before his invasion of Iraq. Whether it will ever be fair to blame Angela Merkel for “breaking” Greece is debatable. But if the euro zone’s weakest link does default this week and is eventually forced out of the single currency, it seems inevitable that the German chancellor, Europe’s most powerful leader, will “own” the Greek problem and that a decision to let Athens go would profoundly shape her legacy. For months, the notoriously cautious Merkel has been wrestling with the question of whether to risk a “Grexit” and accept the financial, economic and geopolitical backlash it would surely unleash.

Unlike her finance minister, Wolfgang Schaeuble, who sent abundant signals in recent months that he could accept a euro zone that does not include Greece, Merkel has been determined to avoid such an outcome, according to her closest advisers. If Greece ends up leaving the euro zone anyway, many in Germany and elsewhere will blame the left-wing government of Greek Prime Minister Alexis Tsipras that came to power in January. It has infuriated its partners with what they have perceived to be an erratic, confrontational stance in the debt talks. Tsipras’s call on Friday for a referendum on Europe’s latest bailout offer, only days before Greece is due to run out of cash, made it easy for Merkel, 60, to say enough is enough, and threaten to pull the plug once and for all.

But it will be Merkel, more than any other European leader, who will have to sort through the rubble of a “Grexit” and answer the question of why disaster was not averted. A Greek exit could lead to a humanitarian crisis on Europe’s southern rim, spark contagion in euro countries that are only just emerging from years of deep recession, and stoke a fiery new debate about German austerity policies and Merkel’s handling of the crisis. Allowing Greece to exit would be by far the boldest move she has taken since coming to power nearly a decade ago, far riskier than her decision in 2011 to phase out nuclear power.[..]

France has toed the German line until now. But at a decisive meeting of euro zone finance ministers on Saturday, France broke with Germany and other countries, arguing in favor of extending Greece’s bailout to allow a referendum to take place, euro zone officials said. The French were slapped down and the Greek request for an extension denied. Now Merkel, barring a miraculous eleventh hour deal with Athens, must face the consequences.

Incredibly tragic.

• The Greeks For Whom All The Talk Means Nothing – Because They Have Nothing (G.)

On a steep, gardenia-scented street in the north-eastern Athens suburb of Gerakas, in one corner of a patch of bare ground, stands a small caravan. Plastic mesh fencing – orange, of the kind builders use – encloses a neat garden in which peppers, courgettes, lettuces and beans grow in well-tended raised beds. Flowers, too. The caravan is old, but spotless. It is home to Georgios Karvouniaris, 61, and his sister Barbara, 64, two Greeks for whom all the Brussels wrangling over VAT rates, corporation tax and pension reforms has meant nothing – because they have nothing, no income of any kind.

Next Sunday’s referendum – which, if the country stays solvent that long, will either send Greece back to the negotiating table with its creditors or precipitate its exit from the eurozone – is unlikely to affect them much either. “I do not see how any of it will change our lives. I have no hope, anyway,” said Georgios, sitting in a scavenged plastic garden chair beneath a parasol liberated from a skip. After seven years of a crisis that has left 26% of Greece’s workforce unemployed, 30% of its people below the poverty line, 17% unable to meet their daily food needs and 3.1 million without health insurance, it is hard to see how anything decided in Brussels or in Athens in the coming week will do much to change the lives of a large number of Greeks any time soon.

“Those that were already on the margins have been pushed right to the very, very edge, and those who were in the middle have been pushed to the margins,” said Ioanna Pertsinidou of Praksis, a charity that runs day centres for vulnerable people and offers legal and employment advice. “So many people – ordinary, low-to-middle income people with jobs and homes and their lives on track – have seen their lives go drown the drain so fast,” Pertsinidou said. “People who never dreamed that one day they would not be able to pay their electricity bill, or feed their children properly.”

“The troika clearly did a reverse Corleone — they made Tsipras an offer he can’t accept..”

OK, this is real: Greek banks closed, capital controls imposed. Grexit isn’t a hard stretch from here — the much feared mother of all bank runs has already happened, which means that the cost-benefit analysis starting from here is much more favorable to euro exit than it ever was before. Clearly, though, some decisions now have to wait on the referendum. I would vote no, for two reasons. First, much as the prospect of euro exit frightens everyone – me included – the troika is now effectively demanding that the policy regime of the past five years be continued indefinitely. Where is the hope in that? Maybe, just maybe, the willingness to leave will inspire a rethink, although probably not.

But even so, devaluation couldn’t create that much more chaos than already exists, and would pave the way for eventual recovery, just as it has in many other times and places. Greece is not that different. Second, the political implications of a yes vote would be deeply troubling. The troika clearly did a reverse Corleone — they made Tsipras an offer he can’t accept, and presumably did this knowingly. So the ultimatum was, in effect, a move to replace the Greek government. And even if you don’t like Syriza, that has to be disturbing for anyone who believes in European ideals.

Another useless number from El-Erian. RBS just said 40%. Equally void of meaning.

• El-Erian: 85% Grexit Odds as ‘Massive’ Contraction Looms (Bloomberg)

Greece is heading for a “massive economic contraction” and is likely to be forced out of the euro zone, according to Mohamed El-Erian, the former chief executive at Pimco. Greece shut its banks and imposed capital controls in a dead-of-night announcement designed to avert the collapse of its financial system after a weekend of turmoil. People rushed to line up at ATMs and gas stations following Prime Minister Alexis Tsipras’s shock announcement late Friday of a July 5 referendum on austerity measures demanded by the country’s creditors. “There’s an 85% probability that Greece will be forced to leave the euro zone” in the next few weeks, El-Erian said in an interview from New York.

“What we are seeing here is what economists call the sudden stop, when the payment system stops. The logic of a sudden stop is a massive economic contraction, social unrest and it’s going to make continued membership of the euro zone very difficult for Greece.” The euro dropped more then 1% and Treasuries surged by the most since 2011 as the collapse of Greek rescue talks roiled global markets. The lack of trust on both sides now makes it very hard to see how there can be an agreement that would resolve the impasse, said El-Erian, who worked at the IMF from 1983 to 1997.

“This has been an accident in the making for a number of years,” said El-Erian, who is also a Bloomberg View columnist. “It reflects an inability to understand each other’s point of view and an inability to compromise. Europe should have been much more forthcoming on debt reduction and Greece should have been much more forthcoming on implementing reforms.” El-Erian said the ECB will be a key player in trying to contain fallout across the region as the crisis threatens to undo much of the work that President Mario Draghi has done to shore up confidence in the euro as a leading currency of global trade.

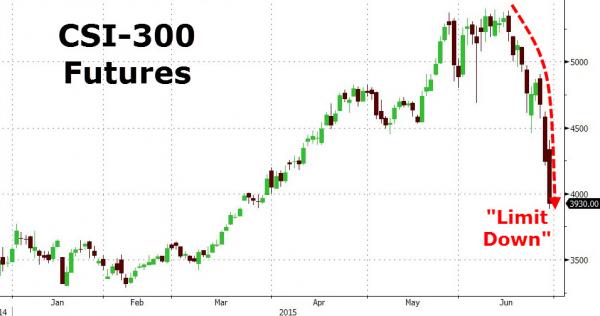

Long predicted, now reality.

• Chinese Stocks Crash Most In 19 Years Despite PBOC Hail Mary (Zero Hedge)

Carnage…

*CHINA STOCK PANIC SELLING TO CONTINUE, CENTRAL CHINA ZHANG SAYS

This leave China’s CSI-300 broad stock index futures up just 7% year-to-date…

*CHINA CSI 500 STOCK-INDEX FUTURES FALL BY MAXIMUM 10% LIMIT

*CHINA CSI 500 STOCK-INDEX FUTURES FALL BY LIMIT FOR 2ND DAY*SHANGHAI COMPOSITE INDEX EXTENDS DROP TO 7.5%

*SHANGHAI COMPOSITE HEADS FOR BIGGEST 3-DAY DROP SINCE 1996

The bounce is dead. CHINEXT – China’s tech-heavy high beta ‘Nasdaq’ – is down 5-6% today, 19% in 3 days, and 33% from highs in early June…!

XI and Li better think of something, fast.

• A China Market Crash “Poses Great Danger To Social Stability” (Zero Hedge)

While Greece has understandably been the focal news event over the weekend – after all it has been 5 years in the making – let’s not forget that in another massive move, one geared squarely to prevent a market collapse and to avoid even further panic, the Chinese central bank cut both its policy rate and the reserve rate in a dramatic push to calm down markets after a 10% crash in just two trading days. Which, incidentally, shows that after the Fed, the BOE, the SNB, the BOJ and the ECB, the PBOC is the latest bank to have cornered itself in a world where it must inflate the bubble at all costs or face the dire consequences. What consequences? Nomura explains:

The policy easing should be viewed as a measure to contain the risk of a hard landing or systemic crisis rather than one to achieve faster growth. In this case, the stronger-than-expected monetary easing may help stem the decline in the equity market following a 10.6% drop over the past two trading days. The positive wealth effect of the equity market on consumption or aggregate demand is limited in China, but an equity market collapse would hurt millions of mid-class households and pose great danger to the economy and social stability.

And there you have it: just like all other central banks, the opportunity cost to markets returning to fair value is nothing short of social conflict (as admirably displayed with every passing day in the US) and even, perhaps, civil war. Which means that unlike before, when the bursting of the bubble would merely lead to a few high flying 1%-ers literally flying from the top floor having lost everything, this time the gamble could not have been higher, and when the central banks finally lose control the outcome will be nothing short of war… just as Paul Tudor Jones, Kyle Bass and countless others have warned before.

No way.

• Will Beijing Really Be The Last Rescuer For Everyone In The Stock Market? (SCMP)

The most dangerous idea gaining traction in the Chinese stock market is the naïve consensus among ordinary investors that no matter how bad the market gets, the Communist Party will eventually rescue everyone. The central bank surprised everyone with its announcement on Saturday that it will cut its benchmark deposit and lending rates by 25 basis points – the fourth reduction since November. Meanwhile, it also decided to reduce the reserve requirement ratio at selected banks to further ease liquidity in the banking system. The unusual “double cut” move came just 24 hours after more than US$760 billion was wiped off the value of mainland stocks – equivalent to the market capitalisation of US technology giant Apple.

The reasons for the market crash are complicated, including margin calls, tight liquidity at the end of the month, and panic. Afterwards, the most frequently heard question was, what will the government do to rescue the market. Rescue? Is this really government’s responsibility? China has been through the planned economy model for decades. This is especially ingrained in the generation of my parents, who make up the bulk of individual investors. Just as everything once belonged to the government, many of these people believe the stock market should also belong to the government. So it’s the job of the government – in other words, the Communist Party – to rescue the market.

Unfortunately, many Chinese experts and professors are also promoting this naïve view of the relationship between domestic investors and the government. After the central bank’s moves on Saturday, many experts told state media that they believed the central bank acted mainly to rescue the stock market, given the timing of the decision. Suddenly, investors who felt that Friday was the end of the world – with more than 2,000 stocks sinking – began to talk about what stocks they should buy on Monday morning. “You still don’t get it? It’s now like the government policy that the stock market must go up. Otherwise, why bother asking the central bank to rescue the market?” said one investor in a post on Weibo. Many others echoed his views on the social media network.

Not a chance.

• Does China’s Central Bank Know What It’s Doing? (Bloomberg)

If you think the U.S. Federal Reserve has a problem communicating its intentions, spare a thought for the People’s Bank of China. In the space of a few days, China’s central bank has changed policy twice, and the message was largely unintelligible both times. Does that matter? One answer: Over the past two weeks, thanks partly to confusion over monetary policy, China’s stock market has suffered its biggest drop in almost 20 years. On Thursday, with the stock market already down from its peak, the central bank subtly eased policy with a technical maneuver involving so-called reverse-repurchase agreements. This left investors wondering, “Is that it?” They’d thought a cut in interest rates was coming; when they concluded it wasn’t, stocks plunged.

Afterward, on Saturday, the PBOC not only cut the benchmark interest rate but also eased its reserve requirements – the first time it has done both at once since 2008. So the central bank went from a surprisingly mild adjustment to a surprisingly dramatic one with a stock-market crash in between. And what PBOC Governor Zhou Xiaochuan intended by these moves still isn’t clear. With the economy slowing, a further lowering of interest rates already made sense on macroeconomic grounds. But the timing of the second and larger change in policy suggests that China’s still-overvalued stock market, rather than the slowing economy, is directing policy. Some analysts are even talking about a “Zhou put” – a Chinese version of the notorious “Greenspan put,” supposedly intended to put a floor under stock prices after the crash of 1987. Many argue that it also pushed U.S. interest rates too low for too long.

More crisis.

• Puerto Rico’s Governor Says Island’s Debts Are ‘Not Payable’ (NY Times)

Puerto Rico’s governor, saying he needs to pull the island out of a “death spiral,” has concluded that the commonwealth cannot pay its roughly $72 billion in debts, an admission that will probably have wide-reaching financial repercussions. The governor, Alejandro García Padilla, and senior members of his staff said in an interview last week that they would probably seek significant concessions from as many as all of the island’s creditors, which could include deferring some debt payments for as long as five years or extending the timetable for repayment. “The debt is not payable,” Mr. García Padilla said. “There is no other option. I would love to have an easier option. This is not politics, this is math.”

It is a startling admission from the governor of an island of 3.6 million people, which has piled on more municipal bond debt per capita than any American state. A broad restructuring by Puerto Rico sets the stage for an unprecedented test of the United States municipal bond market, which cities and states rely on to pay for their most basic needs, like road construction and public hospitals. That market has already been shaken by municipal bankruptcies in Detroit; Stockton, Calif.; and elsewhere, which undercut assumptions that local governments in the United States would always pay back their debt. Puerto Rico’s bonds have a face value roughly eight times that of Detroit’s bonds. Its call for debt relief on such a vast scale could raise borrowing costs for other local governments as investors become more wary of lending.

Home › Forums › Debt Rattle June 29 2015