DPC Broad Street lunch carts, New York 1906

Well that’s a surprise….

Iron ore’s in free fall. Futures in Asia plummeted after port stockpiles in China expanded to the highest in more than a year following moves by local authorities to quell speculation in raw-material futures. The SGX AsiaClear contract for June settlement tumbled 9.1% to $50.50 a metric ton at 1:24 p.m. in Singapore, while futures in Dalian sank 7.1%, retreating alongside contracts for steel and coking coal. The benchmark Metal Bulletin price for 62% content spot ore in Qingdao plunged 12% last week for the worst loss since 2011. Iron ore is falling back to Earth after an unprecedented wave of speculation in China, triggered by signs the economy was stabilizing, helped to hoist benchmark prices to the highest in 15 months.

The jump prompted regulatory authorities and exchanges to team up to quell the excesses, while banks including Brazil’s Itau Unibanco warned the price gains weren’t justified in an oversupplied market. Data on Friday showed port holdings have expanded to almost 100 million tons. [..] Inventories held at ports across China increased 1.4% to 99.85 million tons last week to the highest since March 2015, according to data from Shanghai Steelhome Information. The holdings have expanded 7.3% this year after rising for five of the past six weeks.

Really, that was a surpsie too?

• Dollar Jump Catches Traders Short in One More Currency Calamity (BBG)

Just when investors thought they’d finally made a good call in the currency market, the dollar’s advance messed it up. The U.S. currency on Friday capped its best week all year versus major peers, shortly after hedge funds finally switched to betting on dollar declines, known as going short. That’s not the only wrong move foreign-exchange managers have made this year – an index tracking their returns shows they’ve failed to turn a profit in 2016. Many of the assumptions traders made at the start of the year turned out to be misguided. Anticipated Federal Reserve interest-rate increases have failed to materialize, creating less policy divergence between the U.S. and its counterparts. And though investors were right to speculate the pound would tumble in the run-up to next month’s EU referendum, it’s recovered since.

“It’s been a very challenging year in the currency market given the lack of solid fundamental themes and the difficulties for some market-consensus trades which haven’t worked,” said Chris Chapman at Manulife Asset Management. “A lot of people were expecting a lower euro, lower yen and higher dollar, but the market moves have so far been against those expectations.” The lack of profit comes at a difficult time for the foreign-exchange market. Banks including Morgan Stanley, Barclays and Societe Generale have cut traders from their currency desks as they grapple with a 20% drop in volumes in the past 18 months amid increasing automation. And it’s not just currency trading that’s suffering: global stocks are headed for a second straight year of losses, following a rout in January and February that wiped out as much as $9 trillion.

Yeah, sure, a recovery bought with debt. We do it all the time.

• China Stocks Plunge Again As Hopes For Economic Recovery Fade (R.)

China stocks fell sharply again on Monday, reaching eight-month lows, as investors saw hopes for a strong economic recovery fade and worried about fresh regulatory curbs on speculation. Following the market’s nearly 3% slump on Friday, China’s blue-chip CSI300 fell 2.1%, to 3,065.62, while the Shanghai Composite lost 2.8%, to 2,832.11 points. China April trade data, released on Sunday, doused investor hopes of a sustainable economic recovery, with both exports and imports falling more than expected. Recovery hopes were further dimmed by an article on Monday in the People’s Daily, the Communist Party’s mouthpiece.

It cited an “authoritative source” saying China’s economic trend will be “L-shaped”, rather than “U-shaped”, and definitely not “V-shaped”, but the government will not use excessive investment or rapid credit expansion to stimulate growth. Shares fell across the board, but selling concentrated in relatively expensive small caps amid fears of fresh regulatory crackdown on speculation. China’s securities regulator said on Friday that the valuation gap between the domestic and overseas market and speculation on “shell” companies – firms used for backdoor listings – merited attention. An index tracking raw material shares tumbled nearly 5% as China’s commodity prices continued to fall amid a government crackdown on speculative trading.

Where do they store all the stuff?

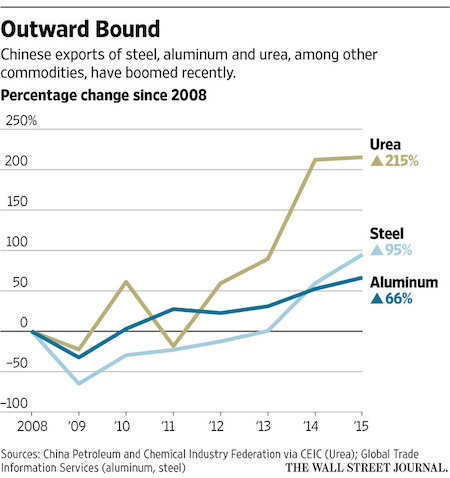

• China Continues to Prop Up Ailing Factories, Adding to Global Glut (WSJ)

China is doubling down on efforts to keep unprofitable factories afloat despite for years pledging to curb excess capacity, adding to a glut of basic materials flooding the global economy. The country’s overproduction of steel, aluminum, diesel and other industrial goods has driven down prices and crippled competitors, leading to thousands of lost jobs in the U.S. and elsewhere. China’s continuing aid for unneeded factories is triggering a sharp rise in trade disputes and protectionist sentiment, especially in the U.S., where trade has emerged as one of the pivotal issues in the U.S. presidential election. According to a Wall Street Journal analysis of Chinese public companies, Chinese government support includes billions of dollars in cash assistance, subsidized electricity and other benefits to companies.

Recipients include steelmakers, coal miners, solar-panel manufacturers, and other producers of other goods including copper and chemicals. One beneficiary, Aluminum Corp. of China, or Chalco, said in October one of its units would shut down a roughly 500,000-ton-per-year smelter in the far-western Gansu region as it struggled to make profits. Executives prepped for thousands of layoffs. Then Gansu officials slashed the plant’s electricity bill by 30%, employees say, and the factory was saved. Although a portion of capacity was taken offline, most is operational. “We’re in full production now with 380,000 tons of capacity,” said Fei Zhongchang, a company sales manager.

In Europe, workers have joined protests against Chinese steel imports. Australia has investigated dumping of products including solar panels and steel and India has raised import taxes on steel after a surge of cheap Chinese goods. The U.S. launched seven new investigations into alleged dumping or government subsidies involving Chinese goods in the first three months of this year, more than the same period of any other year dating back to at least 2003, government data show. Earlier this year, the U.S. Commerce Department slapped preliminary import duties of 266% on imported Chinese cold-rolled steel. The decision came after U.S. Steel lost $1.5 billion last year, closed its last blast furnace in the South and laid off thousands of workers, blaming China.

Late last month , U.S. Steel filed a trade complaint against China at the International Trade Commission, alleging price fixing, trans-shipment via third countries to avoid duties and cyber-espionage to loot technology off U.S. Steel computers. China’s Commerce Ministry has urged U.S. authorities to reject the complaint, and said allegations of intellectual property infringement “are completely without factual basis.” China says it isn’t guilty of dumping—or selling a product at a loss in order to gain market share—and calls U.S. and EU measures and investigations forms of protectionism. It says it has mothballed factories and intends to cut more, with plans to lay off up to 1.8 million steel and coal workers.

Goodness, Gracious, Great Ball of Money.

• Government Policies Make China Prone To Asset Bubbles (Balding)

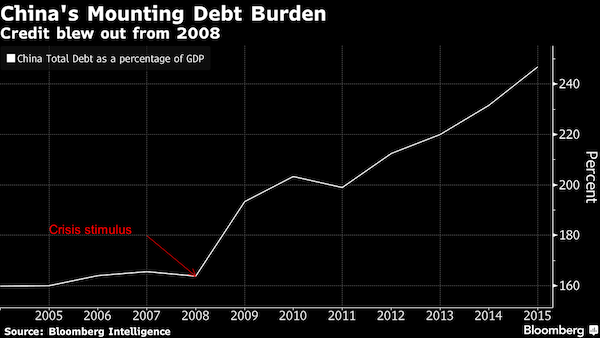

Chinese markets have rarely looked more like Vegas casinos. In recent weeks, investors have driven up trading volumes in China to astronomical levels, betting on everything from rebar to eggs. China traded enough steel in one day last month to build 178,082 Eiffel Towers and enough cotton to make at least one pair of jeans for every person on the planet. These commodity markets aren’t gyrating purely because Chinese are inveterate gamblers. Government policies have made China especially prone to asset bubbles. Even as some of those bubbles are carefully deflated, new ones are sure to emerge unless the policies themselves change. The issue is surplus liquidity – what’s been described as China’s “great ball of money,” which bounces from asset class to asset class as if in a pinball machine.

Even Chinese leaders acknowledge it was their effort to fend off the 2009 global financial crisis that allowed that pile of money to grow to epic proportions. By now, credit and money growth has far outstripped any good opportunities for investment in China’s real economy, which is hobbled by excess capacity. And the mismatch is getting worse: Total social financing, China’s broadest measure of lending, grew nearly four times as fast as nominal GDP last year. Money doesn’t sit still; all this increased liquidity is flooding into real estate and financial assets. Last summer, that led to the boom-and-bust of the Shanghai stock market. Now it’s driving up property prices in top cities – Shenzhen real estate is up more than 50% in the past year – to levels higher than in any U.S. metropolis other than New York. Yet rather than retreating, the government is doubling down on its strategy.

In January, soon after drafting a new five-year plan that focused in part on the need to shrink industries such as steel and coal, the government eased credit yet again, boosting loan growth by 67% in January and 43% through the first quarter. The money was meant to – and did – buy an uptick in GDP growth. But it’s also gone into new loans to zombie companies as well as speculation in the commodity and bond markets. Officials have also maintained their firm grip on the economy, thus encouraging investors to focus on government statements, rather than economic fundamentals, when deciding where to put their money. Prior to the stock market peak in July 2015, top leaders were actively talking up the virtues of equities and boasting of how high the Shanghai index could go. More recently, they’ve extolled the virtues of home ownership and lowered down-payment requirements for some homebuyers.

Same function as US two-party mouthpieces.

• Even China’s Party Mouthpiece Is Warning About Debt (BBG)

China’s leading Communist Party mouthpiece acknowledged the risks of a build-up of debt that is worrying the world and said the nation needed to face up to its nonperforming loans. High leverage is the “original sin” that leads to risks in the foreign-exchange market, stocks, bonds, real estate and bank credit, the People’s Daily said in a full-page interview with an unnamed “authoritative person” starting on page one and filling the second page on Monday. China should put deleveraging ahead of short-term growth and drop the “fantasy” of stimulating the economy through monetary easing, the person was cited as saying. The nation needs to be proactive in dealing with rising bad loans, rather than delaying or hiding them, the report said.

“Overall, the report suggests to us that future policy easing may be more cautious and that the government may try to hasten the pace of reform,” said Zhao Yang at Nomura in Hong Kong. Similar commentaries have had a “large impact” in the past, the analyst said in a note. The pace of China’s accumulation of debt and dwindling economic returns on each unit of credit have fueled concern that the nation is set for either a financial crisis or a Japanese-style growth slump. The Bank for International Settlements warned late last year of an increased risk of a banking crisis in China in coming years. Brokerage CLSA was the latest to sound an alarm, saying on Friday that the nation’s true level of nonperforming loans may be at least nine times higher than the official numbers, suggesting potential losses of at least $1 trillion.

“A tree cannot grow up to the sky – high leverage will definitely lead to high risks,” the person was cited as saying. “Any mishandling will lead to systemic financial risks, negative economic growth, or even have households’ savings evaporate. That’s deadly.”

The value of reserves expressed in dollars. Not pretty: “..any purchase of Aramco is an option play on a future oil boom.”

• Saudi Aramco Plans London Listing But Doubts Grow On $2.5 Trillion Claim (AEP)

Saudi Arabia is planning a three-way foreign listing in London, Hong Kong, and New York for the record-smashing privatisation of its $2.5 trillion oil giant Aramco, anchored on a triad of interlocking ties with three foreign energy companies. The Saudi authorities hope to entice ExxonMobil, China’s Sinopec, and potentially BP, into taking strategic stakes, offering them long-term access to upstream operations in return for cutting-edge technology or refinery deals, according to sources close to Saudi thinking. The moves come amid a profound shake-up of the kingdom’s energy strategy, with the dismissal of veteran oil minister Ali al-Naimi over the weekend. Aramco chief Khalid al-Falih will take over, though there may not be immediate changes to Opec policy.

The Aramco sale is planned as soon as 2017 or 2018 and would in theory be five times larger than any IPO in history, a huge prize for the London Stock Exchange. Shares will be listed in Riyadh but the internal Saudi market is too small to absorb such a colossus, responsible for a ninth of global oil supply. Prince Mohammad bin Salman, Saudi Arabia’s deputy crown prince and de facto ruler, says Aramco will sell 5pc of its equity, valuing the shares at $100bn to $150bn. The vast IPO is the spearhead of his “2030 Vision” to break the country’s “addiction” to oil and diversify, using the proceeds for an investment spree covering everything from car plants to weapons production, petrochemicals, and tourism. “We will not allow our country ever to be at the mercy of commodity price volatility,” he says.

The 31-year-old prince aims to clear away a clutter of subsidies, pushing through a Thatcherite shake-up of what still remains a medieval economic structure. The plans draw on a McKinsey report, “Beyond Oil”, which warned that the kingdom is heading for bankruptcy if it fails to grasp the nettle. London’s hopes for the IPO may have increased with the election of Sadiq Khan as London’s first Muslim mayor, extensively covered in the Saudi media. It underscores Britain’s tolerant outlook at a time when attitudes are hardening in the US. While the Saudis are shocked by the anti-Muslim rhetoric of Donald Trump, they are more disturbed by legislation in Congress that would let survivors of the 9/11 terrorist attacks file lawsuits for damages against Saudi Arabia. Mr Al Falih told the Economist that an Aramco listing in New York would open the country to “frivolous lawsuits”, a hint that the Saudis may eschew the city altogether and concentrate on London and Hong Kong.

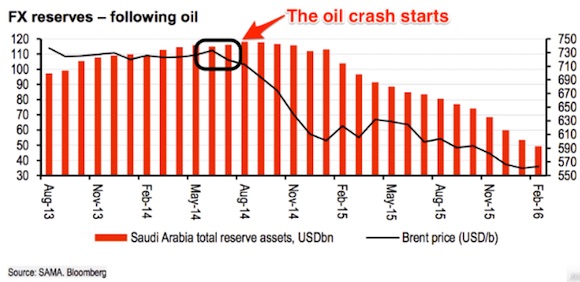

[..] Aramco funds the Saudi state, paying for a sprawling bureaucracy and a cradle-to-grave welfare system that keeps a lid on dissent. It also funds the prince’s military ambitions and a war in Yemen. Saudi defence spending was the world’s third highest last year. Robin Mills from Qamar Energy said the market value of Aramco is probably just $250bn to $400bn, given that the state creams off a royalty rate of 20pc and tax of 85pc. Saudi officials insist that a fair deal could be found for shareholder dividends, even though the Saudi constitution stipulates that Aramco’s 260bn barrels of estimated reserves belong to the kingdom. In a sense, any purchase of Aramco is an option play on a future oil boom. At current prices there would be no money for dividends: the Saudi state is consuming all the revenue, and burning through more than $100bn a year in foreign exchange.

No, there will be no supply shortfall in 2035. Economic reality will make sure of that. In 20 years, the world will be a whole different place.

• Oil Discoveries Slump To 60-Year Low (FT)

Discoveries of new oil reserves have dropped to their lowest level for more than 60 years, pointing to potential supply shortages in the next decade. Oil explorers found 2.8bn barrels of crude and related liquids last year, according to IHS, a consultancy. This is the lowest annual volume recorded since 1954, reflecting a slowdown in exploration activity as hard-pressed oil companies seek to conserve cash. Most of the new reserves that have been found are offshore in deep water, where oilfields take an of average seven years to bring into production, so the declining rate of exploration success points to reduced supplies from the mid-2020s. The dwindling rate of discoveries does not mean that the world is running out of oil; in recent years most of the increase in global production has come from existing fields, not new finds, according to Wood Mackenzie.

But if the rate of oil discoveries does not improve, it will create a shortfall in global supplies of about 4.5m barrels per day by 2035, Wood Mackenzie said. That could mean higher oil prices, and make the world more reliant on onshore oilfields where the resource base is already known, such as US shale. Paal Kibsgaard, chief executive of Schlumberger, the world’s largest oil services company, told analysts last month: “The magnitude of the E&P [exploration and production] investment cuts are now so severe that it can only accelerate production decline and the consequent upward movement in [the] oil price.” The slump in oil and gas prices since the summer of 2014 has forced deep cuts in spending across the industry. Exploration has been particularly vulnerable because it does not offer a short-term pay-off.

ConocoPhillips is giving up offshore exploration altogether, and Chevron and other companies are cutting back sharply. The industry’s spending on exploring and appraising new reserves will fall from $95bn in 2014 to an expected $41bn this year, and is likely to drop again next year, according to Wood Mackenzie. There also has been a predominance of gas, rather than oil, in recent finds. In spite of the decline in activity, the total combined volume of oil and gas discovered last year rose slightly, but the proportion of oil dropped from about 35% in 2014 to about 23% in 2015.

Think anyone recognizes the demise of world trade yet? Or is the bias still too strong?

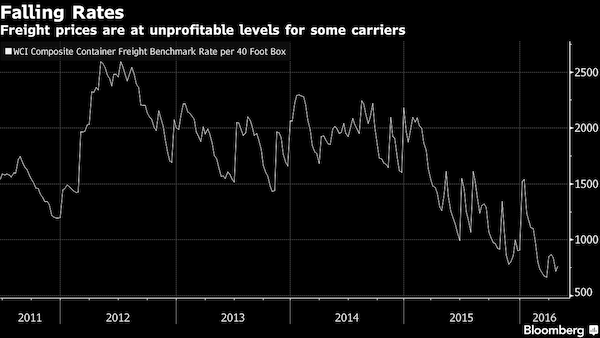

• Negative Rates Hit Global Shipping Market (BBG)

The owner of the world’s biggest shipping line says negative interest rates are hurting the industry by delaying the consolidation wave so badly needed. The monetary policy environment “means that consolidation will be much slower because it’s easy for banks to keep weak shipping companies above water,” Nils Smedegaard Andersen, CEO of A.P. Moeller-Maersk, said in an interview. It’s the latest example of how negative interest rates are distorting markets and potentially even slowing growth. The policy has so far had limited success in reviving inflation while money managers in countries with negative rates are warning of the risk of asset price bubbles. With the unintended consequences potentially including a slower global shipping recovery, questions as to the policy’s efficacy are bound to persist.

“Politicians aren’t making the reforms that are needed and are leaving it to the monetary policy makers to solve the economic problems that many countries face with low competitiveness and low investment levels,” Andersen said. A reliance on cheap finance in container shipping has led to “many negative effects,” he said. The shipping industry doesn’t have the buffers to deal with more hurdles. Container lines are “staring at a terrible 2016,” with a slowdown in global trade volumes, low freight rates and overcapacity, Drewry Maritime Equity Research said in a report last month. It estimates the industry will lose $6 billion this year. Hanjin Shipping, South Korea’s biggest container carrier and the world’s no. 8, is in the middle of a debt restructuring. Its banks on Wednesday agreed on the terms on condition that all creditors, including corporate bond holders, join the plan.

Hanjin shares have slumped 41% this year, compared with a 0.8% gain for the benchmark Kospi index. Maersk surged 6.4% as of the close of trading Wednesday in Copenhagen, bringing the stock to a 3.1% gain this year. Thursday and Friday were holidays in Denmark. Global shipping lines are increasingly forming alliances to help cut costs and underpin freight rates. Last month, CMA CGM SA and three other major lines signed a preliminary agreement to form a new group called Ocean Alliance, which could become the second biggest after Maersk Line’s partnership with Mediterranean Shipping Co. “We’re satisfied with our current position within our alliance,” Andersen said. “But if a container line were to come up for sale – with the right profile and also at the right price – we would consider it. We are, after all, businessmen.”

Germany stands accused of the causing euro crisis. Something tells me Schäuble doesn’t agree.

• Draghi, Schäuble And The High Cost Of Germany’s Savings Culture (Münchau)

Right now the biggest problem for Mario Draghi is not Greece. It is Germany. Last week the president of the European Central Bank hit back at Berlin’s criticism of his loose interest rate policies by pointing out that Germany’s persistent current account surplus is one of the main causes. The furious reaction he faced says much about the faultlines in Europe’s economic debate. Low interest rates and Germany’s current account surplus are the poisonous twins of the eurozone economy. The surplus caused low rates, as Mr Draghi rightly says. But it is also true that low interest rates have increased the German current account surplus through the devaluation of the euro in the past year. A cheaper currency makes German goods and services more competitive outside the eurozone. The more pertinent of the two interpretations is Mr Draghi’s.

By insisting on austerity during the eurozone crisis, and failing to raise investment spending at home, Berlin was instrumental in depressing aggregate demand at home and in the eurozone at large. The eurozone’s long depression caused a fall in inflation below the target rate of just under 2%. The ECB response has been to cut short-term rates to negative levels and buy financial assets. If German fiscal policy had been neutral during that period, the ECB’s job would have been easier. It would have been able to achieve its inflation target and would not have had to cut rates by as much. Berlin views the current account surplus simply as a reflection of Germany’s superior competitiveness. This is an economically illiterate view – or rather it deliberately deflects from the real problem.

If Germany had its own currency and a floating exchange rate, the current account imbalance would have mostly disappeared. Even in a monetary union, a large imbalance would not matter if the union was politically integrated and had a common fiscal policy. But imbalances matter in the monetary union we have, one without redistribution and reinsurance systems. It is no coincidence Germany rejects these redistribution mechanisms. This is how it maximises its current account surplus. It constitutes an implicit policy goal. In the long run, I cannot see how this is in Germany’s interests. Wolfgang Schäuble, finance minister, was right to say that low rates are driving voters to Alternative for Germany, an anti-euro and anti-immigrant party. Only it was not the ECB’s fault.

There’s just one way out of this, because Germany won’t change policy: Greece, Italy et al must leave the euro.

• The Folly Of German Economic Policy (Coppola)

In his latest blogpost, the economist Michael Pettis is severely critical of European economic policies, especially those of Germany, saying that they are “among the most irresponsible in modern history”. He is not alone. Wolfgang Munchau, writing in the FT, lays the blame for the Eurozone’s protracted depression firmly at Berlin’s door: “[..]Berlin was instrumental in depressing aggregate demand at home and in the eurozone at large. [..] If German fiscal policy had been neutral [..] the ECB’s job would have been easier. It would have been able to achieve its inflation target and would not have had to cut rates by as much.”

Unsurprisingly, Berlin does not agree. For German finance minister Wolfgang Schaueble, German economic policy is a model that other countries should adopt. Even the enormous current account surplus is a sign of Germany’s production strength and export competitiveness. It is to be celebrated, not criticized. However, Berlin’s view is not shared by some Eurozone policymakers. In a recent speech to German policymakers, ECB chief Mario Draghi observed that low rates of return are due to an imbalance between saving and investment:

“The forces at play are fairly intuitive: if there is an excess of saving, then savers are competing with each other to find somebody willing to borrow their funds. That will drive interest rates lower. At the same time, if the economic return on investment has fallen, for instance due to lower productivity growth, then entrepreneurs will only be willing to borrow at commensurately lower rates. On both counts, it is structural factors that have lowered the real return on investment. And since we operate in a global capital market, this has exerted downward pressure on returns on savings everywhere.”

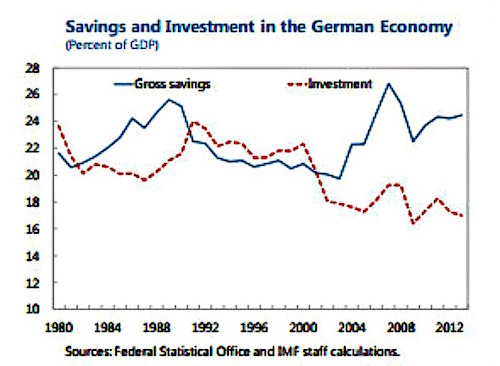

And Germany’s current account surplus is a significant contributory factor to low interest rates: “The role of Asian economies in this story has been well-documented, for instance in the “global savings glut” thesis. But today the euro area is also a protagonist. We have a current account surplus over 3% of GDP, and our largest economy, Germany, has had a surplus above 5% of GDP for almost a decade.” The gap between Germany’s domestic saving and investment can be clearly seen on this chart from the IMF . The chart only goes to 2012, but the gap has if anything widened since. Currently, it stands at about 8% of GDP:

Luckily, he’s our best friend…

• Turkey Economic A-Team Down to Last Man as Erdogan Exerts Power (BBG)

Turkish Deputy Prime Minister Mehmet Simsek is the last man standing from the team feted by investors as the driving force behind the nation’s rapid growth years. One-by-one, President Recep Tayyip Erdogan is removing the AK Party policy makers whose focus on balancing budgets, taming inflation and fiscal stability led to average growth of 5% over 13 years to 2015. His handpicked prime minister, Ahmet Davutoglu, decided to step down on Thursday, ending a power struggle over management of the economy and Erdogan’s efforts to add executive power to his traditionally ceremonial office. Like Davutoglu, former Merrill Lynch strategist Simsek has defended the kind of orthodox monetary policy that so riles Erdogan, specifically the use of high interest rates to curb inflation.

Erdogan argues that lower borrowing costs and subsequent faster growth would more effectively slow price gains, and with Davutoglu gone, there may be little to insulate Simsek from pressure to fall into line. That may spell the end to an unspoken truce between Erdogan and investors, who tolerated his quest for more power as long as people trusted by markets like Simsek ran the economy. “There would be no AK Party economic miracle without this team of capable technocrats,” said Tim Ash at Nomura in London. “The concern now is that without these individuals, and with a coterie of untested economic policy advisers around Erdogan, Turkey will be very vulnerable to market pressure.”

Perverse incentives.“Why pay off the mortgage at at all?” ” [..] why worry about paying it off when you are alive?”

• UK’s Nationwide Raises Home Loan Age Limit To 85 Years (BBC)

Nationwide is raising its age limit for people paying off mortgages by 10 years to 85, in the latest sign of the impact of rising house prices on buyers. The building society said the increase was due to “growing demand”, and the limit would be in force from July. It means a 60-year-old could take out a 25-year mortgage as long as they prove they can afford the repayments. The move comes as Halifax increases its age limit for mortgages from 75 to 80 from Monday. There have been calls for the industry to do more to help older buyers after tougher mortgage checks, introduced in the wake of the financial crisis, have made it harder for middle-aged people to get a home loan. Rising house prices have exacerbated the issue, with many people not able to afford to buy their first home until they are in their thirties or forties.

Nationwide said the new age limit would apply to existing customers for all its standard mortgages, but the maximum loan size would be £150,000, and could be no greater than 60% of the property value. “Access to the mainstream market has been a challenge for older customers, resulting in their needs going unfulfilled. This measure helps to address these needs in a prudent, controlled manner,” said Nationwide head of mortgages Henry Jordan. Tom McPhail, head of pensions research at Hargreaves Lansdown, told the BBC the change could shake up the mortgage market. “Why pay off the mortgage at at all?” he said on Radio 5 Live. “As long as the value of the property is there to meet the liability in the future, why worry about paying it off when you are alive?” he added.

“.. two sides of a debased coin.”

• The End of American Meritocracy (Luce)

What is in a word? When it is packed with as much moral zeal as “meritocracy”, the answer is a lot. A meritocrat owes his success to effort and talent. Luck has nothing to do with it — or so he tells himself. He shares his view with everyone else, including those too slow or indolent to follow his example. Things only go wrong when the others dispute it. Now magnify that to a nation of 320m people — one that prides itself on being a meritocracy. Imagine that between a half and two-thirds of its people, depending on how the question is framed, disagree. They believe the system’s divisions are self-perpetuating. They used not to think that way. Imagine, also, that the meritocrats are too enamoured of their just rewards to see it. The fact that they are split — one group calling itself Democratic, the other Republican — is detail.

They are two sides of a debased coin. Sooner or later something will give. An exaggeration? Financial Times readers might be inclined to think so. The fact that Donald Trump has completed a hostile takeover of one of those groups — the Republicans — is a shock to everyone, including, I suspect, the property billionaire himself. The rest should not be a surprise. Since the late 1960s both parties, in different ways, have turned a blind eye to the economic interests of the middle class. In 1972 the McGovern-Fraser Commission revamped the Democratic party’s rules for selecting its nominee after the disastrous 1968 convention in Chicago. The overhaul changed the party’s course. It included obligatory seats for women, ethnic minorities and young people — but left out working males altogether.

“We aren’t going to let these Camelot Harvard-Berkeley types take over our party,” said the head of the AFL-CIO, the largest American union federation. That is precisely what happened. Democrats cemented the shift from a class-based party to an ethnic coalition by enshrining affirmative action for non-whites. Getting a leg up to university, the ultimate meritocratic vehicle, was based on your skin colour rather than your economic situation. Unsurprisingly, swaths of the white middle class turned Republican. Forty years on, many Democrats, not least Bernie Sanders’ supporters, are suffering buyer’s remorse. Before he became president, Barack Obama argued it would be fairer to base affirmative action on income not colour. “My daughters should probably be treated by any admissions officer as folks who are pretty advantaged,” he said.

Last week it was announced that Malia Obama had been accepted into Harvard, her father’s alma mater. About a third of legacy applicants, those whose parent attended, are accepted into Harvard. No one suggests she is not deserving of her place. However, there are plenty of lower-income black and white children who do not benefit from the advantages Malia Obama or Chelsea Clinton (Stanford and Oxford) had from birth.

Would this surpsrise anyone?

• Panama Papers Allege New Zealand Prime Place For Rich To Hide Money (R.)

New Zealand is at the heart of a tangled web of shelf companies and trusts that are being used by wealthy Latin Americans to channel funds around the world, according to a report on Monday based on leaks of the so-called Panama Papers. Local media has analyzed more than 61,000 documents relating to New Zealand that are part of the massive leak of offshore data from Mossack Fonseca, a Panama-based law firm. The papers have shone spotlight on how the world’s rich take advantage of offshore tax regimes. Mossack Fonseca ramped up its interest in using New Zealand as one of its new jurisdictions in 2013, actively promoting the South Pacific nation as a good place to do business due to its tax-free status, high levels of confidentiality and legal security, according to a joint report by Radio New Zealand, TVNZ and investigative journalist Nicky Hager.

Mossack Fonseca’s main contact in New Zealand was allegedly Robert Thompson, co-founder and director of accountant firm Bentleys New Zealand, the registered office of Mossack Fonseca New Zealand, according to the report. Thompson was listed in more than 4,500 Panama paper documents, the report said. Thompson said in his experience, the use of trusts for tax evasion was not common and his firm did not assist people to illegally hide assets. “I think the assumption that all New Zealand foreign trusts are being used for illegitimate purposes is unfounded and based largely on ignorance,” Thompson was quoted as saying by Radio New Zealand. [..] Prime Minister John Key dismissed concerns that international tax avoidance was rife in New Zealand. “New Zealand is barely ever mentioned, it’s a footnote,” Key told TVNZ in reference to the Panama Papers.

There’s no way protests are not going to intensify going forward. Is Tsipras is ousted, you just watch.

• Greek Lawmakers Pass Painful Reforms To Attain Fiscal Targets (R.)

Greece’s parliament on early Monday passed a package of unpopular pension and tax reforms that the country’s leftist-led government hopes will persuade official creditors to unlock bailout cash. The measures aim to ensure Greece will attain savings to meet an agreed 3.5% budget surplus target before interest payments in 2018, helping it to regain bond market access and render its debt load sustainable. The vote was a test of the ruling coalition’s cohesion, given its wafer-thin majority of three lawmakers in the 300-seat parliament. All of the coalition’s 153 lawmakers voted in favor. Athens wants to boost tax revenues and slash pension spending to reduce the drain on the budget, hoping impressed creditors will unlock aid. But Germany and the IMF remain deadlocked over the terms of country’s bailout plan.

Prime Minister Alexis Tsipras’ government drew fire from the political opposition during the debate on grounds the pension cuts and tax hikes will prove recessionary, dealing another blow to a population fatigued by years of austerity. “Mr. Prime Minister, you promised hope and turned it into despair,” said Fofi Gennimata, leader of the opposition PASOK socialists, who see the package as the bill for Tsipras’ failed push to roll back austerity in last year’s clash with lenders which set back the economy and triggered capital controls. Tsipras’ government was re-elected in September on promises to ease the pain of austerity for the poor and protect pensions after he was forced to sign up to a new bailout in July to keep the country in the euro zone.

The package aims to generate savings equal to 3% of GDP and contemplates raising income tax for high earners and lowering tax-free thresholds. It increases a so-called ‘solidarity tax’ – which goes straight into state coffers – and introduces a national pension of €384 a month after 20 years of work, phases out a benefit for poor pensioners and recalculates pensions. Finance Minister Euclid Tsakalotos defended the reforms, saying lower pension replacement rates will affect the rich and not the poor. He heads to Brussels on Monday to face a Eurogroup meeting, seeking to conclude a key bailout review. “Our word is a contract. We have done what we promised and hence the IMF and Germany must provide a solution that is feasible, a solution for the debt that will open a clear horizon for investors,” Tsakalotos told lawmakers.

Erdogan will make sure there’s more of this.

• Greece Keeps Wary Eye On Turkey Border Violations (Kath.)

Turkey’s continuing violations of Greek air space and waters could lead to a spike in bilateral tensions or to a “serious accident,” Greek Defense Minister Panos Kammenos told Kathimerini’s Sunday edition, adding that NATO’s naval patrols in the area can strengthen the country’s position regarding Ankara’s expansionist policies. Asked about the spate of Greek air space violations and transgressions of the Athens Flight Information Region (FIR) by Turkish fighter jets in recent weeks, Kammenos denounced the trend as propaganda aimed at domestic consumption. “Greece knows there are forces [in Turkey] that want to create tension and, perhaps, cause a serious incident or an accident,” said Kammenos, who is also the leader of SYRIZA’s right-wing coalition partner, Independent Greeks.

“Greece will not be dragged into actions that might undermine its rights,” he said, adding that he had recently spoken to NATO Secretary-General Jens Stoltenberg, asking that the transatlantic alliance take action against Turkish hostility. Meanwhile, the minister rejected criticism that NATO’s Aegean mission, aimed at curbing migrant crossings, had strengthened Ankara’s hand in questioning Greece’s sovereign rights, deeming that NATO states, and more importantly those who are also EU members, now had firsthand experience of Turkish provocations. Kammenos referred to a recent incident in the Aegean whereby a Turkish torpedo boat allegedly executed maneuvers in close proximity to a Dutch frigate deployed in the NATO mission. “This dangerous incident has been recorded and included in the Dutch captain’s report to NATO,” he said.

Home › Forums › Debt Rattle May 9 2016