John Collier Workmen at emergency office construction job, Washington, DC Dec 1941

Let this sink in. Then realize how reliable Chinese numbers are. And that’s where all the ‘growth’ is in the world.

• Global Growth is All About China…Nothing but China (Econimica)

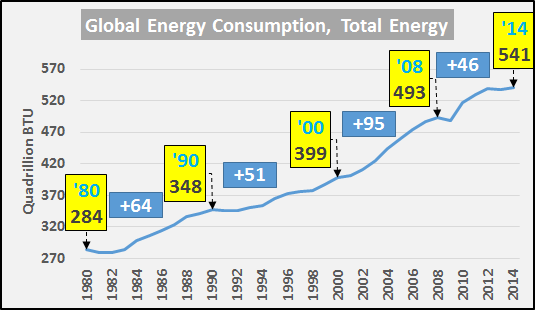

Since 2000, China has been the nearly singular force for growth in global energy consumption and economic activity. However, this article will make it plain and simple why China is exiting the spotlight and unfortunately, for global economic growth, there is no one else to take center stage. To put things into perspective I’ll show this using four very inter-related variables…(1) total energy consumption, (2) core population (25-54yr/olds) size and growth, (3) GDP (flawed as it is), and (4) debt. First off, the chart below shows total global energy consumption (all fossil fuels, nuclear, hydro, renewable, etc…data from US EIA) from 1980 through 2014, and the change per period. The growth in global energy consumption from ’00-’08 was astounding and an absolute aberration, nearly 50% greater than any previous period.

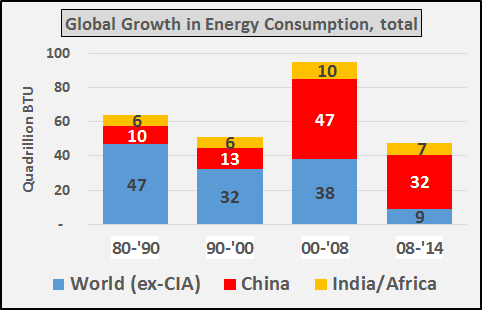

Of that growth in energy consumption, the chart below breaks down the sources of that growth among China (red), India/Africa (gold) and the rest of the world (blue). It’s plain to see the growth of Chinese energy consumption, the decelerating growth among the rest of the world, and the stagnant growth among India / Africa.

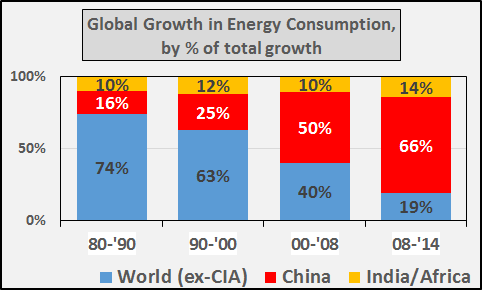

But here is the money chart, pointing out that the growth in energy consumption (by period) has shifted away from “the world” squarely to China. From 2008 through 2014 (most recent data available), 2/3rds or 66% of global energy consumption growth was China. Also very noteworthy is that India nor Africa have taken any more relevance, from a growth perspective, over time. The fate of global economic growth rests solely upon China’s shoulders.

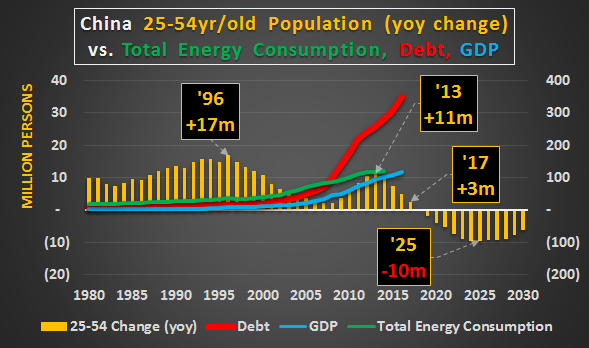

The chart below shows China’s core population (annual change) again against total debt, GDP, and energy consumption. The reliance on debt creation as the core population growth decelerated is really hard not to see. This shrinking base of consumption will destroy the meme that a surging Chinese middle class will drive domestic and global consumption…but I expect this misconception will continue to be peddled for some time.

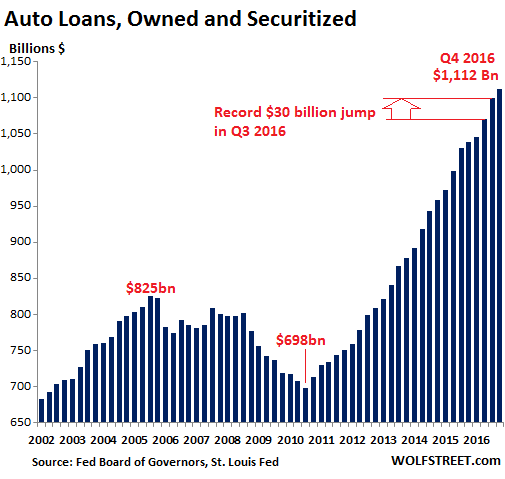

Fewer delinquencies, says the Fed. But then look at the next article: “Seriously Delinquent” US Auto Loans Surge

• US Household Debt Is Dangerously Close To 2008 Levels (CNN)

Total household debt climbed to $12.58 trillion at the end of 2016, an increase of $266 billion from the third quarter, according to a report from the Federal Reserve Bank of New York. For the year, household debt ballooned by $460 billion — the largest increase in almost a decade. That means the debt loads of Americans are flirting with 2008 levels, when total consumer debt reached a record high of $12.68 trillion. Rising debt hints that banks are extending more credit. Mortgage originations increased to the highest level since the Great Recession. Mortgage balances make up the bulk of household debt and ended the year at $8.48 trillion. However, growth in non-housing debt – which includes credit card debt and student and auto loans – are key factors fueling the rebound in debt.

Student loan debt balances rose by $31 billion in the fourth quarter to a total of $1.31 trillion, according to the report. Auto loans jumped by $22 billion as new auto loan originations for the year climbed to a record high. Credit card debts rose by $32 billion to hit $779 billion. At these rates, the New York Fed expects household debt to reach its previous 2008 peak sometime this year. But while that may sound alarming, there is one big difference between now and 2008, according to the Fed: Fewer delinquencies. At the end of 2016, 4.8% of debts were delinquent, compared to 8.5% of total household debt in the third quarter of 2008. There were also less bankruptcy filings – a little more than 200,000 consumers had a bankruptcy added to their credit report in the final quarter of last year, a 4% drop from the same quarter in 2015.

“There’s nothing like loading up consumers with debt to make central bankers outright giddy.”

• “Seriously Delinquent” US Auto Loans Surge (WS)

Bank regulators have been warning, now it’s happening. The New York Fed, in its Household Debt and Credit Report for the fourth quarter 2016, put it this way today: “Household debt increases substantially, approaching previous peak.” It jumped by $226 billion in the quarter, or 1.8%, to the glorious level of $12.58 trillion, “only $99 billion shy of its 2008 third quarter peak.” Yes! Almost there! Keep at it! There’s nothing like loading up consumers with debt to make central bankers outright giddy. Auto loan balances in 2016 surged at the fastest pace in the 18-year history of the data series, the report said, driven by the highest originations of loans ever. Alas, what the auto industry has been dreading is now happening: Delinquencies have begun to surge.

This chart – based on data from the Federal Reserve Board of Governors, which varies slightly from the New York Fed’s data – shows how rapidly auto loan balances have ballooned since the Great Recession. At $1.112 trillion (or $1.16 trillion according to the New York Fed), they’re now 35% higher than they’d been during the crazy peak of the prior bubble. Note that during the $93 billion increase in auto loan balances in 2016, new vehicle sales were essentially flat. No way that this is an auto loan bubble. Not this time. It’s sustainable. Or at least containable when it’s not sustainable, or whatever. These ballooning loans have made the auto sales boom possible.

Not a new topic, but some useful numbers.

• 3 Reasons The US Could Be Headed For A Fresh Debt Crisis (MW)

Subprime car loansThe amount of total open car loans just topped $1 trillion, according to credit ratings firm Experian. But is that a sign of consumer confidence … or a cause for alarm? According to the latest data, from the third quarter of 2016, about 1 in 5 car loans are made to subprime borrowers, at an average interest rate of almost 11%. And broadly speaking, the average car loan in the U.S. is for a balance of almost $30,000 and a monthly payment of about $500. With stats like that, it’s no wonder the default rate on car loans is rising. A study by lending analysis firm Lending Times recently found that auto loan delinquencies are up over 21% compared with 2012 levels. A senior vice president at TransUnion, one of the three major credit rating bureaus, recently said he expects “a modest increase in delinquency” for auto loans going forward, too.

Just image what would happen if rates tick a bit higher. After all, if homeowners who were “underwater” on their homes in 2007 could shrug off the impact of a foreclosure on their credit report and simply walk away from a big mortgage, then why in the world would they stick with a double-digit interest rate on a car loan — especially as that car ages or breaks down? The real weight of these loans continues to hit the balance sheets of lenders, with net subprime losses continuing to march upward in December to 8.52%. Standard & Poor’s U.S. Auto Loan Tracker noted that while some of the acceleration was seasonal, “the year-over-year increases indicate that 2017’s losses could surpass last year’s levels.” No wonder the New York Fed called subprime auto debt a “significant concern” at the end of last year.

Student loans Hedge-fund guru Bill Ackman has said “I think that the government’s going to lose hundreds of millions of dollars” on student loans. And while that may sound like hysterics, when you consider that there is roughly $1.4 trillion in outstanding student debt, according to the Federal Reserve, that number doesn’t seem so far-fetched. Most of that is owned by the federal government via subsidized loans, too, with a recent Bloomberg report estimating the government owned some $850 billion in student loan debt as of 2014. Even a modest default rate would quite literally eat up hundreds of millions of dollars in a hurry. The losses for the government are disturbing, but at least can be made up with higher taxes or cuts elsewhere in the budget. There’s no relief for the millions of young Americans who are stuck paying for their college degree instead of spending on consumer goods.

Government-insured mortgagesAfter the collapse of subprime mortgages during the financial crisis, banks learned a hard lesson about these risky home loans. But if you think that means they avoided all loans to less-than-stellar borrowers, think again. The New York Fed recently juxtaposed the rise of government-insured mortgages vis-à-vis the decline in subprime lending to find that “government insurance programs rapidly expanded and more than filled the void.” That mirrors a report from ProPublica back in 2012 that estimated 9 in 10 mortgages issued at the time were being guaranteed by taxpayers via government-sponsored enterprises such as Fannie Mae and Freddie Mac. And while standards are moderately higher for loans with this government backstop than precrisis loans to subprime borrowers, “they are not low-risk loans,” write the New York Fed economists. “The combination of high leverage and low credit scores documented above translates into extremely high default rates.”

It’s all about political power.

• Fed President Says US Banks Have “Half The Equity They Need” (Black)

In a scathing editorial published in the Wall Street Journal today, the president of the Federal Reserve Bank of Minneapolis, Neel Kashkari, blasted US banks, saying that they still lacked sufficient capital to withstand a major crisis. Kashkari makes a great analogy. When you’re applying for a mortgage or business loan, sensible banks are supposed to demand a 20% down payment from their borrowers. If you want to buy a $500,000 home, a conservative bank will loan creditworthy borrowers $400,000. The borrower must be able to scratch together a $100,000 down payment. But when banks make investments and buy assets, they aren’t required to do the same thing. Remember that when you deposit money at a bank, you’re essentially loaning them your savings.

As a bank depositor, you’re the lender. The bank is the borrower. Banks pool together their deposits and make various loans and investments. They buy government bonds, financial commercial trade, and fund real estate purchases. Some of their investment decisions make sense. Others are completely idiotic, as we saw in the 2008 financial meltdown. But the larger point is that banks don’t use their own money to make these investments. They use other people’s money. Your money. A bank’s investment portfolio is almost entirely funded with its customers’ savings. Very little of the bank’s own money is at risk. You can see the stark contrast here. If you as an individual want to borrow money to invest in something, you’re obliged to put down 20%, perhaps even much more depending on the asset.

Your down payment provides a substantial cushion for the bank; if you stop paying the loan, the value of the property could decline 20% before the bank loses any money. But if a bank wants to make an investment, they typically don’t have to put down a single penny. The bank’s lenders, i.e. its depositors, put up all the money for the investment. If the investment does well, the bank keeps all the profits. But if the investment does poorly, the bank hasn’t risked any of its own money. The bank’s lenders (i.e. the depositors) are taking on all the risk. This seems pretty one-sided, especially considering that in exchange for assuming all the risk of a bank’s investment decisions, you are rewarded with a miniscule interest rate that fails to keep up with inflation. (After which the government taxes you on the interest that you receive.) It hardly seems worth it.

Murky.

• Harward Turns Down National Security Adviser Job Over Staffing Dispute (CBS)

Vice Admiral Robert Harward has rejected President Trump’s offer to be the new national security adviser, CBS News’ Major Garrett reports. Sources close to the situation told Garrett Harward and the administration had a dispute over staffing the security council. Two sources close to the situation confirm Harward demanded his own team, and the White House resisted. Specifically, Mr. Trump told Deputy National Security Adviser K. T. McFarland that she could retain her post, even after the ouster of National Security Adviser Michael Flynn. Harward refused to keep McFarland as his deputy, and after a day of negotiations over this and other staffing matters, Harward declined to serve as Flynn’s replacement.

Harward, a 60-year-old former Navy SEAL, served as deputy commander of U.S. Central Command under now-Defense Secretary James Mattis. He previously served as deputy commanding general for operations of Joint Special Operations Command at Fort Bragg in North Carolina. Harward has also commanded troops in both Iraq and Afghanistan for six years after the 9/11 attacks. Under President George W. Bush, he served on the National Security Council as director of strategy and policy for the office of combating terrorism.

As I said: the New Cold War is being fought INSIDE the US.

• The Swamp Strikes Back (Escobar)

The tawdry Michael Flynn soap opera boils down to the CIA hemorrhaging leaks to the company town newspaper, leading to the desired endgame: a resounding victory for hardcore neocon/neoliberalcon US Deep State factions in one particular battle. But the war is not over; in fact it’s just beginning. Even before Flynn’s fall, Russian analysts had been avidly discussing whether President Trump is the new Victor Yanukovich – who failed to stop a color revolution at his doorstep. The Made in USA color revolution by the axis of Deep State neocons, Democratic neoliberalcons and corporate media will be pursued, relentlessly, 24/7. But more than Yanukovich, Trump might actually be remixing Little Helmsman Deng Xiaoping: “crossing the river while feeling the stones”. Rather, crossing the swamp while feeling the crocs.

Flynn out may be interpreted as a Trump tactical retreat. After all Flynn may be back – in the shade, much as Roger Stone. If current deputy national security advisor K T McFarland gets the top job – which is what powerful Trump backers are aiming at – the shadowplay Kissinger balance of power, in its 21st century remix, is even strengthened; after all McFarland is a Kissinger asset. Flynn worked with Special Forces; was head of the Defense Intelligence Agency (DIA); handled highly classified top secret information 24/7. He obviously knew all his conversations on an open, unsecure line were monitored. So he had to have morphed into a compound incarnation of the Three Stooges had he positioned himself to be blackmailed by Moscow.

What Flynn and Russian ambassador Sergey Kislyak certainly discussed was cooperation in the fight against ISIS/ISIL/Daesh, and what Moscow might expect in return: the lifting of sanctions. US corporate media didn’t even flinch when US intel admitted they have a transcript of the multiple phone calls between Flynn and Kislyak. So why not release them? Imagine the inter-galactic scandal if these calls were about Russian intel monitoring the US ambassador in Moscow. No one paid attention to the two key passages conveniently buried in the middle of this US corporate media story. 1) “The intelligence official said there had been no finding inside the government that Flynn did anything illegal.” 2) “…the situation became unsustainable – not because of any issue of being compromised by Russia – but because he [Flynn] has lied to the president and the vice president.” Recap: nothing illegal; and Flynn not compromised by Russia. The “crime” – according to Deep State factions: talking to a Russian diplomat.

Vice-President Mike Pence is a key piece in the puzzle; after all his major role is as insider guarantor – at the heart of the Trump administration – of neocon Deep State interests. The CIA did leak. The CIA most certainly has been spying on all Trump operatives. Flynn though fell on his own sword. Classic hubris; his fatal mistake was to strategize by himself – even before he became national security advisor. “Mad Dog” Mattis, T. Rex Tillerson – both, by the way, very close to Kissinger – and most of all Pence did not like it one bit once they were informed.

A big way in which central banks distort markets.

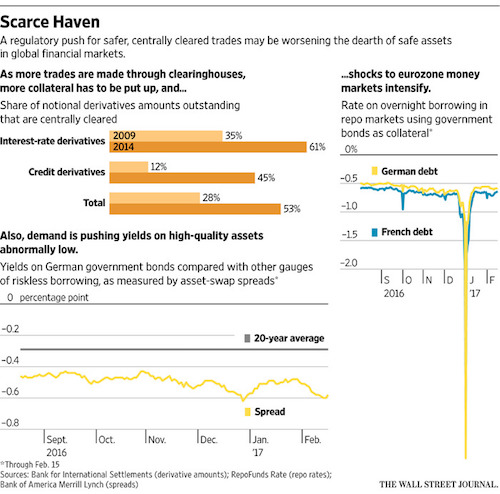

• Who’s Sucking Up All the World’s Safest Bonds? (WSJ)

The world is running out of safe financial assets. One reason may be regulators’ push to make trading safer. A scarcity of safe collateral can create bouts of volatility in the markets where investors fund their purchases. Economists also worry that a lack of quality public-sector assets leads the private sector to create less reliable and riskier substitutes. Global rules increasingly require that investors deposit cash as security, called margin, when they trade with each other. This money is often left at clearinghouses, which are intermediaries that stand between buyers and sellers and step in if one of the parties won’t make good on a transaction. Regulators are trying to give these clearinghouses more heft to make the financial system safer.

The clearinghouses, in turn, have to do something with the cash, and they frequently take it to repurchase, or “repo,” markets, where they lend it out in exchange for high-quality assets such as German bunds or U.S. Treasurys. That has the effect of vacuuming up safe assets. Paradoxically, cash—at least its electronic form—isn’t ultrasafe: It needs to be left in bank deposits, and even the strongest banks have some risk. Treasurys and bunds don’t. Europe’s dearth of safe assets is especially acute. According to a semiannual survey released Tuesday by the International Capital Market Association, demand for collateral in the eurozone increased significantly in the second half of 2016. The ECB and other central banks across the developed world have been blamed for this safe-asset scarcity because they have bought trillions of dollars worth of government bonds in a bid to boost economic growth.

However, during a speech last month, ECB official Yves Mersch pointed to clearinghouses as a key culprit, and warned that “the requirements for trades to be centrally cleared are still being introduced, so the demand from market infrastructure to exchange cash for collateral will rise.” Data are scarce, but the latest figures from the Bank for International Settlements show that more than half of the notional amount outstanding of derivatives transactions was centrally cleared by the end of 2014, after new regulation was enacted—twice as much as in 2009.

“Americans will continue to be relegated to the status of dumb tourist in their own country.”

• Mary Jo White Seriously Misled the US Senate to Become SEC Chair (Martens)

Less than two weeks after Mary Jo White was nominated to become Chair of the Securities and Exchange Commission by President Barack Obama on January 24, 2013, White filed an ethics disclosure letter advising that she would “retire” from her position representing Wall Street banks at the law firm Debevoise & Plimpton. White wrote on this subject in great detail, stating:

“Upon confirmation, I will retire from the partnership of Debevoise & Plimpton, LLP. Following my retirement, the law firm will not owe me an outstanding partnership share for either 2012 or any part of 2013. As a retired partner, I will be entitled to the use of secretarial services, office space and a blackberry at the firm’s expense. For the duration of my appointment, I will forgo these three benefits, though I may pay for some secretarial services at my own expense. Pursuant to the Debevoise & Plimpton, LLP Partners Retirement Program, I will receive monthly lifetime retirement payments from the firm commencing the month after my retirement. However, within 60 days of my appointment, the firm will make a lump sum payment, in lieu of making monthly retirement payments for the next four years. Within 60 days of my appointment, I also will receive payouts of my interest in the Debevoise & Plimpton LLP Cash Balance Retirement plan and my capital account.”

Yesterday it was widely reported in the business press that Mary Jo White is returning to her former law firm as a partner representing clients who face government investigations. She will also fill the newly created position of Senior Chair of the law firm. This news is highly significant because it would appear that the U.S. Senate was seriously misled by White’s ethics letter in its deliberations to confirm her as the top cop of Wall Street. The news is also highly significant because it will mark the fourth time in four decades that Mary Jo White has spun through the revolving doors of Debevoise & Plimpton (where she represented serial law violators) to government service (prosecuting serial law violators).

[..] Until there is meaningful legislative reform of political campaign financing and revolving door appointments, Americans will continue to be relegated to the status of dumb tourist in their own country.

Bankers have too much money and too much power.

• European Financial Centres After Brexit (E.)

“WHEN the vote took place,” says Valérie Pécresse, “it was an opportunity for us to promote Île de France”, the region around Paris of which she is the elected head. Two advertising campaigns were prepared, depending on the result of Britain’s referendum last June on leaving the European Union. The unused copy ran: “You made one good decision. Make another. Choose Paris region.” Brexit has made Paris bolder. Once Britain leaves Europe’s single market, the many international banks and other firms that have made London their EU home will lose the “passports” that allow them to serve clients in the other 27 states. Possibly, mutual recognition by Britain and the EU of each other’s regulatory regimes will persist. But no one can rely on the transition to Brexit being smooth, rather than a feared “cliff edge”. Best to assume the worst.

Britain is expected to start the two-year process of withdrawal next month. Given the time needed to get approval from regulators, find offices and move (or hire) staff, financial firms have long been weighing their options. London will remain Europe’s leading centre, but other cities are keen to take what they can. The Parisians are pushing hardest, pitching their city as London’s partner and peer. “I don’t see the relationship with London as a rivalry,” says Ms Pécresse. “The rivalry is not with London but with Dublin, Amsterdam, Luxembourg and Frankfurt.” Especially, it seems, Frankfurt. Paris has more big local banks, more big companies and more international schools than its German rival. London apart, say the French team, it is Europe’s only “global city”. When, they smirk, did you last take your partner to Frankfurt for the weekend?

This month the Parisians were in London, briefing 80 executives from banks, asset managers, private-equity firms and fintech companies. They are keen to dispel France’s image as an interventionist, high-tax, work-shy place. The headline corporate-tax rate is 33.3% but due to fall to 28% by 2020. A scheme giving income-tax breaks to high earners who have lived outside France for at least five years will now apply for eight years after arrival or return, not five. The Socialists, who run the city itself, and Ms Pécresse’s Republicans are joined in a business-friendly “sacred union”, says Gérard Mestrallet, president of Paris Europlace, which promotes the financial centre. Ms Pécresse and others play down the risk that Marine Le Pen, of the far-right, Eurosceptic National Front will win the presidential election this spring.

“Crimea was TAKEN by Russia during the Obama Administration. Was Obama too soft on Russia?” the U.S. president tweeted.

• Putin Orders Russian Media To “Cut Back” On Positive Trump Coverage (ZH)

Trump’s honeymoon with capital markets is on the rocks, kept alive only by the occasional soundbite about “massive” or “phenomenal” tax cuts; it now appears that the US president’s – until recently – amicable relationship with Russia is also quickly souring. According to Bloomberg, the Kremlin has ordered Russian state media to cut “way back” on their fawning coverage of President Donald Trump, in what three sources told BBG is a “reflection of growing concern among senior Russian officials that the new U.S. administration will be less friendly than first thought.” The Russian president has defended his decision saying it is the result of declining interest among the Russian viewers in Trump’s rise to power, but Bloomberg adds that some of the most popular TV segments on Trump touched on ideas the Kremlin would rather not promote, such as his pledge to “drain the swamp.”

The suggestion is that since Trump is looking to end governmental corruption, the “authoritarian” Putin should be worried; and yet instead of “draining the swamp” Trump has filled it by surrounded himself with precisely those bankers he used as populist examples of all that is wrong with the government. As such, Putin should greet Trump’s failed “swamp draining” although that part did not make it into the Bloomberg report. Putin’s decree comes at a time of rising anti-Russian sentiment in Washington, where U.S. spy and law-enforcement agencies are conducting multiple investigations to determine the full extent of contacts Trump’s advisers had with Russia during and after the 2016 election campaign.

According to Bloomberg, the order marks a stark turnaround from just a few weeks ago when Russia hailed Trump’s presidential victory as the beginning of a new era of cooperation between the former Cold War foes. “Trump’s campaign was watched with rapture as news anchors gushed over the novelty of hearing an American presidential candidate praise Putin. But the wall-to-wall coverage went too far for the Kremlin’s liking.” In January, Trump reportedly received more mentions in the media than Putin, relegating the Russian leader to the No. 2 spot for the first time since he returned to the Kremlin in 2012 after four years as premier, according to Interfax data.”

That said, there has certainly been a chilling in relations between Trump and Putin. In recent weeks, numerous White House officials, including Trump, have criticized Russia for its annexation of Crimea and the subsequent violence in Ukraine. Trump on Wednesday accused Putin of seizing Crimea from Ukraine in a series of Twitter posts that were delivered amid a flurry of allegations that his team has ties to Russia. “Crimea was TAKEN by Russia during the Obama Administration. Was Obama too soft on Russia?” the U.S. president tweeted. As Bloomberg concludes, Russian officials, who had readily commented to local media on earlier news from Washington, suddenly became less talkative after the Crimea comment. And so, with Trump-Putin relations suddenly in purgatory, and Trump’s domestic “Russia-facing” exposure in chaos, it is now unclear how Trump will pivot away to restore what many had hoped would lead to a restoration in normal relations between the two countries.

And there we go again.

• ‘Bank Run’ under Capital Controls: Greeks withdraw €2.5bn in 45 days (KTG)

Delays in the talks between Greece and its lenders have brought back the ghost of Grexit. The grave disagreement between the IMF and the European lenders, Grexit bombshell flying around and Greece’s reluctance to accept additional austerity measures have increase uncertainty among citizens – for one more time. And what do citizens do when they feel political and economical insecurity? The run to banks and withdraw deposits. 2.5 billion euros left Greek banks in the last 45 days. And this despite the capital controls that allow Greeks to withdraw a maximum of just €1,800 per month. However, in better situation are those who brought back cash to the banks. Cash that was largely withdrawn before the capital controls were imposed in July 2015 as a result of a major bank run from November 2014 until end of June 2015.

Those who pulled the cash from under the mattress and brought it to bank are allowed to withdraw money above the €1800 cap. According to newspaper Eidiseis, the cash withdrawal in the last 45 days has set bankers in alert. In addition to cash withdrawals, business loans and mortgage, amounting a total of €500 million, turned red. A sign that the delay in the conclusion of the second review has increased uncertainty among the Greeks, as the daily notes. Speaking to the daily, sources from the Union of Greek Banks said that “time is not working in our favor.” They stressed that the government and the lenders should reach a compromise. Beginning of February, Greek websites for economic news had reported that more than one billion euros was withdrawn in January 2017.

According to a report of November 2015, more than €120 billion left the Greek banks during the years of the crisis. €45 billion left the banks during November 2014 – 2015. 80% of this amount, that is some €36 billion are been kept in homes, company safes or in bank lockers.

Home › Forums › Debt Rattle February 17 2017