Impotence, Leverage and Central Banking

Home › Forums › The Automatic Earth Forum › Impotence, Leverage and Central Banking

- This topic is empty.

-

AuthorPosts

-

December 14, 2012 at 8:11 pm #8412

Nicole Foss

ModeratorChaplin – "Modern Times": A story of industry, of individual enterprise – humanity crusading in the pursuit of happiness Some of our readers

[See the full post at: Impotence, Leverage and Central Banking]December 15, 2012 at 3:58 am #6575Jhem

ParticipantGreat article, Stoneleigh! I was in Madrid on the 14th of November and I saw that demonstration and what’s more I interviewed many there about the current economic crisis for an article that will be coming out this month in Collier’s magazine. The situation is unbelievably bad in Spain, the economy is collapsing, people are getting thrown out of their homes because they can’t pay their mortgages and at the same time the Rajoy government is cutting the money that pensioners receive when it is quite aware that increasingly many families are surviving just on their grandparent’s income. It’s crazy, but it’s real and it is happening.

December 15, 2012 at 5:40 am #6576del

MemberThank you very much for all your articles. I have followed your work for two years plus. This site has helped me understand things I knew next to nothing about. I value your opinions very highly as well as everyone who contributes.

My limited education taught me next to nothing about $ and the economy. This site has made a poitive difference in my life. Thank you.

December 15, 2012 at 6:28 am #6577jal

ParticipantThank you very much for all your articles. I have followed your work for two years plus. This site has helped me understand things I knew next to nothing about. I value your opinions very highly as well as everyone who contributes.

My limited education taught me next to nothing about $ and the economy. This site has made a positive difference in my life. Thank you.

Ditto … for so many of the regular readers.

By now almost everyone is aware that the financial system DID collapse.

When we think back, the glass was perceived to be full.

Now, its half full.

There is not much that we could do about the “spilt milk”.

I concentrate on the fact that the glass is still 1/2 full.

I find fewer and fewer people who are willing to discuss our present situation.Its as if “if you don’t talk about it, it doesn’t matter.”

My biggest challenge is and will remain to prepare my 2 yr. old grand-son to be able to accept change and to function in a different social and economic structure.

December 15, 2012 at 7:41 am #6578p01

Participantdel post=6284 wrote: My limited education taught me next to nothing about $ and the economy. This site has made a poitive difference in my life. Thank you.

Same here. Probably stating the obvious, but knowing next to nothing about finances and the economy is what helped you understand. I know it was in my case. However, it also made me look further into the rabbit hole, and see just how deep it goes: whoa, Nelly!

December 15, 2012 at 10:55 am #6579Loch

ParticipantI don’t wonder why the econ blogs I read spend so much time covering Europe. I understand the slow motion train wreck- no make that the slow-motion covered in frozen molasses and then dipped in amber train wreck. I also am a firm believer that all the QE in the world cannot forestall a massive debt de-leveraging tsunami of apocalyptic proportions that will plunge the word into a deflationary winter. It’s a simple matter of thermodynamic accounting. All the fiat money in the universe cannot make up for a lack of fuel, literally, for the economic fire.

No, I understand it, but I’m afraid my 21st century attention span, measured on the tens of microns level, simply isn’t up to the task. I only want to watch for the fiery crash. But just like NASCAR, the racers just keep going round and round. Simply put, I’m bored.

December 15, 2012 at 7:13 pm #6580Golden Oxen

ParticipantWhat is most distressing to me is the “It’s Yesterday’s Story” idea.

It is all over except for some minor details and signatures of the wise that have saved us.

Much of the financial press has also fallen victim to this reckless short sighted banter. It scares me to see such complacency regarding an ongoing disaster affecting tens of millions of people by those who should be watching closely and ringing alarms and warnings, offering ideas on preparation and advancing ideas on possible solutions, at least partial ones.

It is creating the perfect atmosphere for a Rude Awakening and resulting panic.

December 15, 2012 at 7:21 pm #6581Raúl Ilargi Meijer

KeymasterGO,

I think maybe the best sign we have that we are absolutely spot on is that Nouriel Roubini is now talking about a housing recovery and other positives for the US. If we see for instance David Rosenberg say similar things as well soon, it’s probably time. For the opposite to happen.

December 15, 2012 at 11:07 pm #6582davefairtex

ParticipantI think contrary indicators like NR capitulating and calling a housing recovery is good, but in my experience they don’t typically call the top with any reliable accuracy in terms of timeframe. Perhaps we need a Time Magazine cover for that. Uh, does Time still actually publish a hardcopy magazine?

I think the housing recovery stops when the US government has to engage in actual austerity (i.e. it is forced to stop its trillion-plus deficit-spend every year). The Fed is now monetizing 100% of all new treasury issuance. These combined policies (deficits + monetization) are keeping things afloat, at least for now. And I think that ability to monetize with impunity will likely continue until Europe comes to some sort of resolution. Just my opinion.

@Nicole

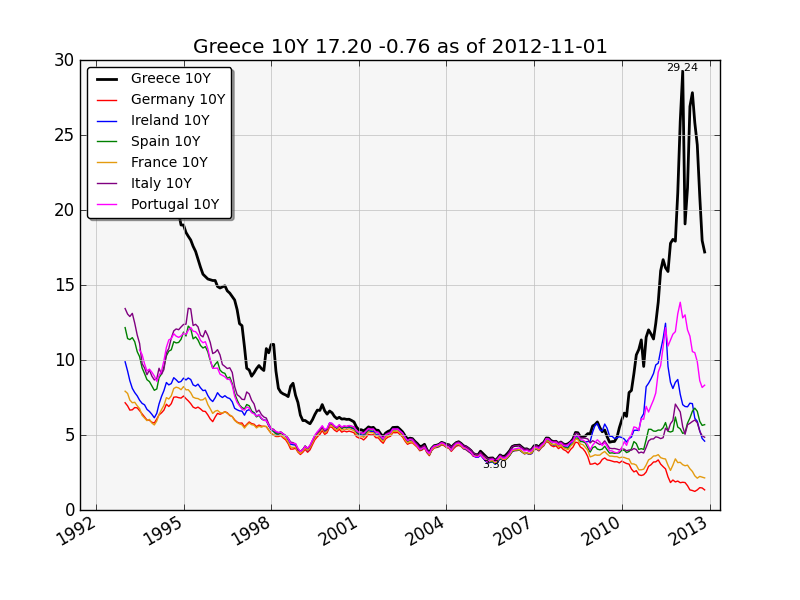

I agree with the tone of your post; just one nit to pick. The chart showing 10-year rates is hopelessly dated – perhaps 36 months old at this point. Greek rates hit 24%, then backed off to 13%, Ireland is at 4.7% not 10.5%, and Portugal is at 7% not 10.5%. Italy and Spain yields have dropped also. Overall, in terms of bond spreads, things have definitely improved – and in some instances, quite dramatically. Ireland from the point of view of bond spreads could be the poster child for a successful austerity program, with its rates on a par with Italy.

Bond spreads matter a great deal to market observers. And in terms of seeing where we are (and making a claim to increasing pressure), well, in my opinion the chart you used just isn’t indicative of the current reality.

December 15, 2012 at 11:49 pm #6583Chrissie

ParticipantThanks for another great article Nicole. Could you possibly explain how and why “credit bubbles bring forward demand by artificially stimulating it but when they burst the demand borrowed from the future must be repaid”? (no doubt you’ve already explained how it works somewhere….)

December 16, 2012 at 3:56 am #6584Nassim

ParticipantDecember 16, 2012 at 4:29 am #6585rapier

ParticipantConsciously or unconsciously, intentionally or unintentionally, the United States overarching strategy is to reinvigorate it’s global dominance by attracting more and more global free liquid capital to our shores or within the grasp of our giant financial institutions. With an additional detail of the British acting as partners. Our great global strategic thinkers and our leaders in every sort of institution, military/security, government or corporate, may not want the rest of the world to go to hell in a hand basket but as long as it is that makes their project easier.

The ongoing flood of liquid capital into the US is already causing the obvious divergence in economic outcomes as most of the rest of the world slows the US is growing GDP wise at around a 2% pace. The tax withholding numbers speak for themselves.

My point is that the US will likely remain the last Ponzi standing. Eventually one can assume that will require our bombs, including the big ones. So be it. All the better actually, to become the worlds defacto safe haven. In the meantime Chinese mega millionaires and Mexican drug cartels know the score. So I am suggesting that AE’s analysts should be a little more granular. What is bad for the rest of the world is, by design, good for the US. If not for all it’s citizens then at least half of them.

December 16, 2012 at 6:05 am #6586KeymasterDave, Nassim,

I think maybe we risk going overboard here a little. It seems obvious to me from looking at the graph that it is no more than 15-16 months old, certainly not 36. It stops around Sep 2011. Anyway, it’s not that dated.

In that time the Greek 10-year yield has fallen to 12.7 from below 15, with Italy at 4.59, from about 5.6 (hard to see), and Spain at 5.35, from about 6.

But also down are France at 1.97 and Germany at 1.35. And they were at 3.2 and 2.5, respectively, as far as I can make out.

That means that in absolute numbers the spread may have narrowed, but also that yields for the bonds that are – perceived as – safer have come down at much higher percentages.

This is not too surprising given the promises of endless fodder for the beast, no matter how impotent. It still does paint a different picture from what Dave implies, though.

Even with the endless fodder, have yield spreads really narrowed? When seen in percentages? It doesn’t look that way.

Let’s see where this goes and not rush to conclusions.

December 16, 2012 at 6:10 am #6587Keymasterrapier,

So I am suggesting that AE’s analysts should be a little more granular.

In what regard, pray tell?

We have always said that there would be a huge capital flight into the US. But also that it won’t buy it that much extra time.

December 16, 2012 at 8:00 am #6588ParticipantI think US society and its political economy could survive in a form similar to the current one or recognizable as related to the current one with the same institutions and elites for a decade or even two more. More I think than your “much extra time”. Or to put it another way I foresee devolution and not a quick dislocation.

I freely admit that I suffer from the familiar bias of extrapolating from the recent past. So be it. I am intimate with Nicole’s logic, her story, and accept it could happen. My thinking is centered on how corporations are becoming the ascendant mode of human organization replacing or co opting nations.

If corporate assets deflate 50% or more but governments and most citizens go totally broke then somehow, I think, the system can remain sort of intact. There is zero indication that the citizenry will revolt. The power of revolt in the US, such as it is, is aligned with corporate power after all. If they know it or not. See the Tea Party. While alternately a Liberal revolt is an absurd idea. When the GOP can gleefully discount, denigrate and prepare to abandon nearly half of the citizenry and nary a Western European government save Iceland’s, not sure about the other slightly less tiny Scandinavian ones, has an operational plan that doesn’t do the same I see the outlines of a New World order that works, sort of, based around corporate structures.

Well it’s all so poorly stated by me. Sorry.

December 16, 2012 at 9:20 am #6589ParticipantYou are of course correct, its not 36 months at all – looks more like 14 or 15. I plead a basic math failure.

However, a whole lot of dramatic stuff happened between mid 2011 and now, so my basic point still holds I think. If we saw the chart updated today, it would paint quite a different picture. Ireland specifically would look a LOT different, and one might make the case that if the trends currently in place continue to improve, that “things are getting better” and possibly even that “austerity works” – at least in the case of Ireland.

I’m certainly NOT trying to make that case, and I agree with most of what she’s said, I’m just making the point that the evidence provided is missing some really important recent events, and I’m all about proper evidence since it helps me to remove my ego and opinion from the analysis.

I have a summary chart on bond spreads that weights bond yields based on the amount of debt each nation has outstanding, and it shows that things have come down quite a bit (narrowed in aggregate perhaps 25%) since nov of 2011 – and also that things got quite a bit worse than Nicole’s chart shows during mid 2012. Unfortunately my data only goes back to late 2011, so (@Nassim) I can’t provide you the charts.

If anyone can point me at a time series source that has 20 years of 10 year bond rates for the countries in question, I’d be more than happy to provide that chart. I just don’t have the access to the data myself, and I’m too cheap to fork over the $$$ to buy it! I’ll poke around a bit and see what I can find.

December 16, 2012 at 10:36 am #6590ParticipantOk so it turned out not to be all that hard after all. Data is available (for those few who might care) at the ECB website, https://sdw.ecb.europa.eu.

Thanks to Nassim for prodding me into getting the data.

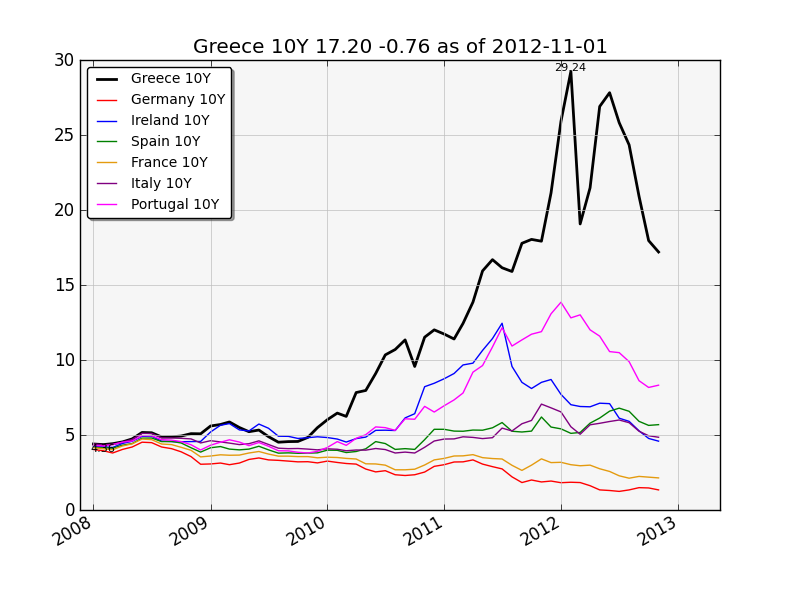

Notice how Ireland started improving months before the other PIGS; also notice the data is a month behind where we are now. Greece 10Y bonds are now yielding 13%, thanks to the buyback program.

This is Nicole’s updated chart:

And same chart starting in 2008, for better recent detail:

December 16, 2012 at 11:10 am #6591Participant

December 16, 2012 at 11:10 am #6591ParticipantThanks Dave.

To me, the Greek bonds look like they are going back to “normal” – the way they were in the early 90’s

December 16, 2012 at 11:23 am #6592william

ParticipantIt seems that a point is being missed. Oil is still a fundamental to why deleveraging has been happening. Listen to Collin Campbell.

First banks lent out more than they had on deposit. They accepted people placing less than 5% down. Why?

At first you might say its not possible for them to be insolvent to take on greater and greater risk but it is. The feeling was this: Debts today will be paid through growth in the future. Even Warren Buffet is saying don’t worry about the size of the problem today we can grow the economy to fit the debt. It is all false.

But why are they saying this? Simply oil represents a seemingly unlimited supply of work energy literally replacing humans in the factory. Each gallon can produce 100s of man hours of work. Each barrel pulled out of the ground was producing for the economy an increase in labour.

Now in the late 90’s some bankers suddenly realized the dreaded peak oil possibility. Realizing they were incorrect in their assessments they were horrified “we’ve got a lot of bad debt on our hands”. What will we do? The answer became clear no one bank should be the leader of bad debt or the lagging tail of less debt both would be less profitable.

Unknown to everyone was the consideration of how this peak oil would show itself. As the increase of removal of oil decreased in 2004 a perception became clear among the banking industry. A perception of a long decline.

It doesn’t really matter if oil has peaked or if there is some alternative. What matters is internationally bankers have a vision of a long decline. That is what has caused the crash. That is what has caused recession. That is why bailouts will not work.

What will it take to change things? My guess is they are right in their thinking – oil appears to have slowed in its removal from the ground. So, if that is the case, the math needs to change. Create a resource based economy, admit capitalism has failed, remove capitalism as the driver of the economy and lets move on in a new renaissance of ideals of the way things should be.

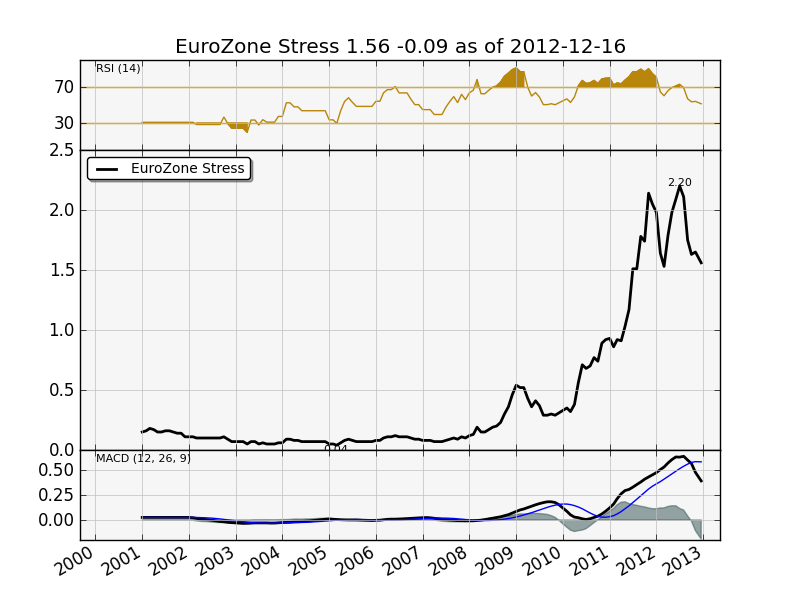

December 16, 2012 at 2:30 pm #6593ParticipantHere’s my eurozone stress chart using the new monthly data. Again, this is the average debt-weighted spread – when German yields drop, and/or when PIGS yields rise, this causes a rise in the spread. And because it is debt-weighted, a move in Italian rates by 10 basis points will cause the chart to jump more than a move in Spanish rates by 10 basis points since Italy has a lot more debt than Spain.

I’ve eliminated Greece (since they defaulted) from the calculation, so the latest dramatic move down in Greek debt won’t affect the chart.

I don’t have a point to make here – this is more of a “submitted for your approval” sort of post.

December 17, 2012 at 1:43 am #6594

December 17, 2012 at 1:43 am #6594Glennda

ParticipantHere is an interesting bit on the home front in the US. Good charts even if I don’t know how to give you real links.

He is giving a guess that things will tank in early to mid 2013.

https://www.oftwominds.com/blogdec12/2-charts12-12.html

Charles Hugh Smith

The Two Charts You Should See Before Risking a Dime in the Market in 2013 (December 17, 2012)‘As a lagniappe, there is a third pattern suggesting a major decline just ahead: Three Peaks and A Domed House Pattern Signals An End To The Bull Market.’

December 17, 2012 at 3:16 am #6595Moderatordavefairtex,

The point of the interest rates graph was really to look at trends – supposed risk equivalence that subsequently broke down. Spreads will expand and contract over time, depending on whether people are optimistic or pessimistic. At times of relative optimism, spreads narrow, and at times of heightened fear they blow out. I am expecting them to blow out again in the not too distant future.

There are different risk distinctions at play – core vs periphery of the eurozone, inside vs outside the eurozone, long term vs short term etc. I am expecting all these spreads to increase as the crisis deepens. Places perceived to be relative safe havens (like the US) end up being bought some time under this dynamic, while places perceived to be at most risk will be eaten alive by it.

December 17, 2012 at 3:22 am #6596ModeratorWilliam,

I don’t see it that way at all. Bankers are not far-sighted perceivers of oil fundamentals. Most haven’t got a clue about energy issues. They are trying to make money today. They follow trends, not lead them.

Oil is not the primary driver to the downside – finance is, because finance is the operating system, and because changes in finance unfold so much more quickly than changes in the real economy.

In the 1930s we experienced a credit crunch even though oil (and everything else) was abundant at the time. This time the larger credit crunch will be exacerbated by resource shortages, but not immediately. For a while money will be in shorter supply than oil.

December 17, 2012 at 3:34 am #6597ModeratorChrissie,

The expansion phase of a bubble artificially stimulates demand. People have more purchasing power (credit), so they demand additional goods and services. Other people set up businesses to supply those goods and services. When the expansion ends, credit is no longer available, so the stimulus disappears. Not only do we see no new business creation or growth, but as credit contracts, the existing businesses have to compete for sharply reduced demand (on the withdrawl of credit). A wave of consolidation ensues as there is too little demand to go around.

This is only the beginning for larger scale contractions though (as opposed to mere business cycle recessions). In larger contractions, credit can almost disappear, and asset price collapse. The leveraged bets placed on asset price appreciation go bad and go into default. The money supply (money plus disappearing credit) contracts sharply. Demand for everything falls very sharply.

For a period, there is almost no demand at all, so many suppliers go out of business. We see negative growth, falling asset values and falling demand for many years. Even the price of essentials is likely to fall initially, as people lack the money to purchase them and demand for them falls (temporarily).

We had 30 years of demand stimulus, and we can expect (IMO) at least 10 years of demand contraction, and quite possibly longer (although I would expect fluctuation and cycles with that overall contraction). A demand undershoot is on the cards – ie demand decreases at least to below what it was when our expansion began in the early 1980s.

December 17, 2012 at 6:31 am #6598ParticipantWe had 30 years of demand stimulus, and we can expect (IMO) at least 10 years of demand contraction, and quite possibly longer (although I would expect fluctuation and cycles with that overall contraction). A demand undershoot is on the cards – ie demand decreases at least to below what it was when our expansion began in the early 1980s.

Darn!!!

That 10 year will probably coincide with the end of my life cycle.Then, there will be a new and different social/economic environment.

Hopefully, my gran-son will have been prepared.

December 17, 2012 at 7:03 am #6599Anonymous

GuestSweden went through a “reform” process in the early 90’s . They CUT spending AND taxes and guess what ? They do not have a debt crisis, serious inflation, or high unemployment ! As an investor I am thinking its time to get out of $ and into Swedish Kroeners. Even the Costa Rican colone is holding steady against the $ and, in fact , has strengthened recently. 6 month CDs in colones pay close to 10% vs 0 in US $ with little or no FX risk and are backed by the full faith and credit of the Costa Rican government. I am thinking of starting a new MMkt fund here and calling it the Banana Republic MMkt Fund. This would be funny if it were not true, but sadly it is true ! The US $ is fast becoming a joke ! Even drug dealers in Colombia are reluctant to take payment in $ ! What does that tell you?

December 17, 2012 at 8:12 am #6600Viscount St. Albans

ParticipantThe Telegraph reports: Connecticut Shooter’s Mother was a Survivalist Preparing for Economic Collapse.

[obvious editorial subtext]

Now we see where all this incessant doomsday thinking leads. It’s time for the government to examine dark unfounded rumors of economic collapse propagating on the internet. Regulation is necessary. These dark visions are twisting the minds of citizens and their children.Question: Why are they reporting this in Britain? Economic Doomerism = Extremism = Violence. A useful message for control.

December 17, 2012 at 3:35 pm #6602gurusid

ParticipantHi folks,

If you can get it this piece by the BBC on the “The Great Spanish Crash” (“This World” BBC2, 16th Dec 2012) its really interesting as it nails on the head all the points that TAE have raised over the last few years. It shows how Spain went from being a poor rural based economy under a dictatorship to what was at one stage the fastest growing economy on the planet (China beware). The regional banks lent vast sums to the local governments and to the local building industry to build a whole new country, including ghost towns and large white elephants like sports stadia and ‘arts centres’ – all little used. Now after the boom, the populace suffers 25% unemployment, (50% for under 25s), and is all but starving and ironically ‘homeless’. Many survive on their grandparents pensions, currently being cut by austerity measures, and what vegetables they can grow on their allotments. One hilarious moment was when they described how the government tried a stimulus package by building more ‘infrastructure’ projects – talk about a one trick pony.

While it shows how the everyday people are trying to cope in the crisis by tragically trying to continue BAU (i.e. get non-existent jobs etc) and the government implements the most ‘austere’ austerity measures seen anywhere on the planet (as dictated by IMF etc) it shows the lack of any real initiative in facing the new paradigm: the end of growth and the reality of contraction. It also shows the reality of so called ‘community’ – it often leads to ‘groupthink’ on all sides of the crisis. One of the most poignant pieces was a pharmacist who had no medicines for her ‘customers’ as the government hadn’t paid her, showing the stark reality and depth of the crisis for many who rely on such medications.

Instead of trying to build a new way of life that is more resilient and reducing both ones expectations and needs (and especially wants), all everyone wants is a return to the boom years.

Also its worth noting that the debt curve in the debt/credit 2008 graph above starts its real upward sweep in the 70’s just as the US domestic oil peaks. (Its also typical of an exponential function – see Albert Bartlett)

L,

Sid.December 17, 2012 at 8:35 pm #6603Participant@nicole

The bond rate graph did show an astonishingly small interest rate differential between Greece and Germany during the salad days of the euro, that’s for certain. And it did a great job showing “before”, “during”, and “after”. The objection I had was only on the issue of trend analysis.

Which brings me to that question: where are things going next? Will spreads ultimately narrow, or will they widen further? The most current data shows that the pressure has come off substantially. Will that pressure relief continue, or not, that’s the primary question.

Ok, I ran off and did some analysis.

Here’s the thing. The ECB knows that this 10 year bond chart is what traders are watching like the entrail-reading Romans of old trying to divine the future of the zone. Looking at my new data for the entire zone, I see is that pressure has indeed come off the PIGS, quite dramatically, but money has not left the safe haven countries at all. In fact, all bonds everywhere have had their yields go down since mid-2012.

This is a curious pattern. One would expect if there was genuine relaxation and return to risk-taking in the peripheral nations, money would have moved OUT of the safe havens. But that’s not what went on. Money has continued to pour into french and german long term bonds. That’s the curious thing.

I’m tempted to put the blame on central bank buying. But I have no actual evidence, so I’ll continue to poke around and see what comes up.

December 17, 2012 at 10:26 pm #6604ModeratorViscount St Albans,

Prepping is big in the UK. See https://www.dailymail.co.uk/news/article-2240239/Armageddon-houses-Brit-preppers-stockpiling-food-weapons-preparation-end-world.html

I agree with your comment. I worry that warning people will become seen as dangerous and that those who wither warn or prepare will be demonized. This is one good reason to prepare as a community rather than alone. Solo preppers are far more likely to be targeted by the neighbours they left behind.

Psychology will be a crucial factor in what’s coming. Things will be twisted in the blame game in order to target specific groups of people. Magical thinking will become more and more common, so that spurious connections will seem more plausible and baseless slurs will be more likely to stick. This will be a time of psyops. We will be dealing with the dark side of human nature. All the more reason to do everything we can to deprive movements of anger and fear of support and keep our focus on the constructive. The alternative is probably a period of brutal totalitarianism. Think 1984.

December 17, 2012 at 10:34 pm #6605Moderatordavefairtex,

I think the spreads are going to blow out over the next few months. Spreads wax and wane, reflecting the tug-of-war of greed and fear, as if collective psychology were inhaling and exhaling over time. The apparent taking off of pressure is a temporary suspension of disbelief in the powers of the ECB, while hedging bets in the form of continued capital flight to the core. When that suspension of disbelief ends, the spreads will widen again. This time I am expecting record spreads to develop since the ECB already used the ‘unlimited’ word and has no back up plan for when the market calls its bluff this time.

December 17, 2012 at 10:41 pm #6606Moderatorkcl6750,

I wouldn’t write off the US dollar any time soon. I think it has a long way to go to the upside. The Swedish krona could do relatively well too, as a safe haven for capital flight from the eurozone. My worry for Sweden is that a sharply rising currency, combined with weakening demand, will kill their manufacturing sector. All exporters face this scenario. Trade dependency is dangerous at this point.

As for the Swedish banking crisis, that occurred in isolation. Resolving it cost Sweden about 4% of GDP and they moved on. Today, however, they have a huge housing bubble, debt to GDP of some 350% and a major export dependency. Sweden is in trouble going forward.

December 18, 2012 at 6:39 am #6607ParticipantFor people outside the UK, you can now watch this video at:

https://www.youtube.com/watch?feature=player_embedded&v=ldu8X_UQPRA#!

Thanks gurusid. I haven’t watched it yet, but is seems stoneleighstic. 🙁

December 18, 2012 at 8:03 am #6609ParticipantAll of scandinavia (Norway, Sweden, Finland) look pretty good from a government debt and budget balance standpoint. They’re all either in balance or have a surplus, and their debt/GDP stands at 44%, 38%, and 49% respectively. Their bonds are trading in that “safe haven” area where the 10 year is yielding in the 1.5-2.2% range.

Switzerland has been successful to date keeping their currency appreciation in check by printing money (and buying euros, mostly) whenever the Swiss Franc looked like it was getting too high. However this has left Switzerland with about 70% of GDP (about $450 billion) in currency reserves. This trade will look brilliant if the eurozone lives, and it won’t look nearly so good if the eurozone breaks up.

If Nicole’s predictions come true and things really come unglued, it will be difficult for places like Scandinavia and Switzerland to keep a lid on currency appreciation. There is a LOT of money out there and these currencies are small. Without controls, this will seriously distort their markets. Even now with all the money printing and the eurozone rescues the Swiss 2 year is yielding -.23% per year.

The choices for the safe haven countries whose economies are small (Scandinavia, Switzerland) and who live outside the eurozone is either money printing or capital controls. Or perhaps both. I don’t imagine they’ll just sit by and let their currencies get wanged around by safe haven flights without trying to do something.

December 19, 2012 at 12:06 am #6611alan2102

Participantkcl6750 post=6307 wrote:

The US $ is fast becoming a joke ! Even drug dealers in Colombia are reluctant to take payment in $ ! What does that tell you?It tells you that the average Colombian drug lord is smarter than the average American — and probably than the average currency trader. But then I would expect drug lords to be pretty bright. What is surprising is that the average Asian peasant is smarter than the average American, at least in this respect. Indians in particular, but Chinese and others as well. They hold physical gold and silver. They don’t trust paper currencies or banks. Smart. Very smart.

December 19, 2012 at 12:19 am #6612ParticipantBased on what I see right now, I think it is probable that the SPX will make a new high either by the end of this year or early 2013.

The relief stemming from the probable fiscal cliff fix coupled with some good news from the european bond markets driving the euro higher and the Fed signing up to effectively monetize ALL US Treasury debt issuance going forward “until things improve” should really help US equities.

I’m seeing more money moving out of the safe havens now and into the PIGS bonds and the equity market. Spain had a decent bond auction today, although they were all short term bonds which are seen as low risk.

December 19, 2012 at 2:28 am #6614Participant@ davefairfax

I assume that you realize that its “Anything goes to save the rich”

Of course, the average person will be the ones suffering.Geeee!

Look at Greece.

The printing press will keep operating for the benefit of the rich.December 19, 2012 at 7:53 am #6618Participantjal –

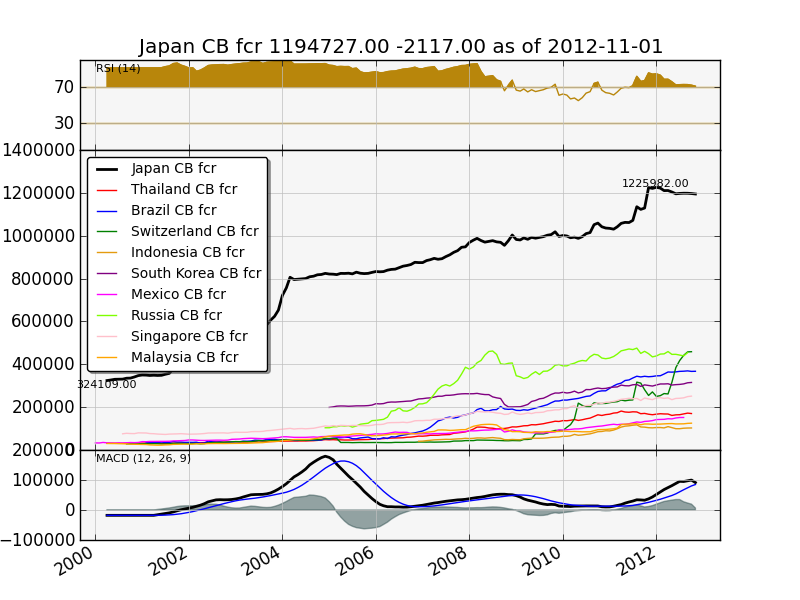

I was not making a comment on the morality of the move or the intervention or who benefits, I am simply observing what seems to be happening. I’m guessing that another market high is likely to occur – like a weather forecaster who looks at clouds and pressure zones and predicts “80% chance of rain tomorrow.”

Its not only the US and ECB that are printing. Here’s a chart of the foreign currency reserves of the various exporting nations. To keep their currencies from appreciating (and their people employed) they print their own currency and buy dollars and euros.

December 19, 2012 at 4:45 pm #6620

December 19, 2012 at 4:45 pm #6620TonyPrep

ParticipantNicole, what do you make of S&P raising Greece’s credit level, for its sovereign debt, by 6 levels?

S&P said:

The upgrade reflects our view of the strong determination of European Economic and Monetary Union (eurozone) member states to preserve Greek membership in the eurozone.

The outlook on the long-term rating is stable, balancing our view of the government’s commitment to a fiscal and structural adjustment against the economic and political challenges of doing so.

December 19, 2012 at 8:52 pm #6621KeymasterNicole, what do you make of S&P raising Greece’s credit level, for its sovereign debt, by 6 levels?

1) That ratings are now evidently based no longer on numbers but on faith; in this case, the faith that austerity hit Germans and Dutch will gladly give up their benefits going forward to bail out those of their banks that are neck deep in Greek debt.

2) That S&P fails/forgets to explain why they lowered the rating as much as they did. Those reasons are all gone now?

3) That S&P et al. are less relevant today than they ever were before. Given their performance in rating MBS and related derivatives, that is a remarkable feat. S&P is part of the financial system that closes ranks on the back of its continued and expanding access to public funds.

-

AuthorPosts

- You must be logged in to reply to this topic.

Sorry, the comment form is closed at this time.