Library of Congress Maya Angelou, Caribbean Calypso Festival, New York 1957

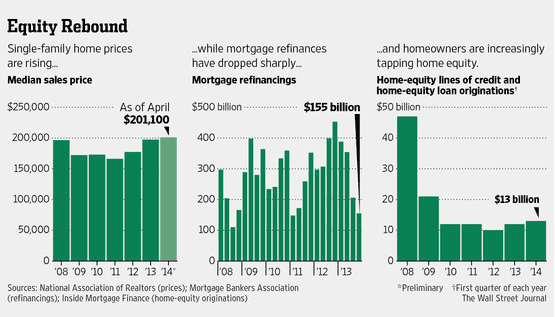

In a recent article, the Wall Street Journal uncovers a big problem in the US housing market, albeit, curiously, without necessarily identifying it as a problem. It would be nice if Americans could trust their once most trusted media to give them the best possible covering of a topic, but the Wall Street Journal apparently prefers to pick the side of, well, Wall Street. The problem not presented as one is the resurgence of American homes as ATMs, of borrowing against a property’s perceived value through home equity loans or home equity lines of credit (Helocs).

The article claims that lenders are being “conservative” since they’re merely handing out 85% LTV instead of the 100% ones they once did, but how conservative that is really depends on the future expectations of the values. And that’s one area where very little is conservative anymore. If lenders can only convince borrowers that the housing market has recovered, they can do their favorite business again: hook mortgagees into major debt increases. That shouldn’t be too much of an issue if only they can show their clients lines like this:

According to the Federal Reserve, net household equity stood at about $10 trillion in the fourth quarter of last year, up 26% from the prior year.

When I first read that, I had to check if they weren’t perhaps referring to the city of London, but sure enough, this is supposed to be about American housing. If it were anywhere near the truth, I don’t understand why Federal Reserve chief Janet Yellen was so cautious about housing prospects a few weeks ago, saying problems “could prove more protracted than currently expected.” If a 26% rise in equity in one year makes her express herself in such negative terms, you wonder what it would take to make her more optimistic. What also makes it hard(er) to believe are falling home sales and mortgage originations, price rises that exist only in the highest price ranges, plus a flood of other data that have come in recently. But there it is, printed in the Wall Street Journal , so why not take out that loan? Why not act as if the past decade, and the crisis it gave birth to, never happened? After all, people want loans, and bankers want commissions.

US Borrowers Tap Their Homes at a Hot Clip (WSJ)

A rebound in house prices and near-record-low interest rates are prompting homeowners to borrow against their properties, marking the return of a practice that was all the rage before the financial crisis. Home-equity lines of credit, or Helocs, and home-equity loans jumped 8% in the first quarter from a year earlier, industry newsletter Inside Mortgage Finance said Thursday. [..] … this year’s gains are the latest evidence that the tight credit conditions that have defined mortgage lending in recent years are starting to loosen. Some lenders are even reviving old loan products that haven’t been seen in years in an attempt to gain market share.

In 2013, lenders extended $59 billion of Helocs and home-equity loans. The last pre-boom year near that level was 2000, when lenders extended $53 billion, according to Inside Mortgage Finance. “We’re seeing much more aggressive marketing campaigns [for Helocs] by banks in locations where home prices have risen,” said Amy Crews Cutts, chief economist at Equifax Inc.[..] “We expect to see quite an uptick in Heloc activity” in the spring …

Some individual banks have seen their Heloc originations rise much faster than the national average. Bank of America, which has increased marketing for Helocs, said customers opened $1.98 billion in Helocs in the first quarter, up 77% from the first quarter of 2013. Matt Potere, who leads Bank of America’s home-equity business, said [..] “The driver is increased customer demand,” Mr. Potere said. “It’s an effect of higher consumer confidence and improving home values.”

Are we sure that “the driver is increased customer demand”, not “much more aggressive marketing campaigns [for Helocs] by banks”? Or is this just two elements coming together in a happy coincidence that will benefit everyone, a real win-win?

[..] During the housing boom, Helocs were a source that many consumers tapped to remodel their homes, buy new cars and boats, travel and send their children to college. Lenders often let them borrow up to 100% of their home’s value, in the expectation that prices would continue to rise. However, when prices fell and borrowers weren’t able to repay, banks faced steep losses.

This time, lenders seem to be offering Helocs only to borrowers with good credit in locations where home values have risen, said Keith Gumbinger, vice president of mortgage-information site HSH.com. During the boom, homeowners could borrow up to 100% of their home’s value, said Mr. Gumbinger. Now it is most common to see a maximum of 80% and sometimes 85%, he said. “Relative to where they were, lenders are still very conservative,” said Mr. Gumbinger. “Will the excesses of yesterday return? Only time will tell.”

Even if we would take that at face value, which we don’t, the question remains where home values are going. There can’t be too many people left who haven’t figured out that it’s the Fed’s hugely expensive QE programs that have lifted asset prices to where they are today, even if they don’t understand why extending QE ad infinitum would be very counter-productive, and is therefore of the table. If that were not so, then, unless the present generation of central bankers were absolute geniuses, it would be hard to explain why their pre-decessors didn’t do what they now do, decades ago. Whether that is clear or not, it would seem only logical to see what asset prices do when QE is gone, both for investors and for home owners. If we can agree that QE has distorted prices of all assets, then home prices must have been distorted too. And if the present record stock exchanges are any indication, it’s a safe bet that they are heavily overvalued. So loans against what some may see as the present ‘value’ of a home are entered into based on – probably greatly – distorted assessments. Lenders mind that less than owners should; and what does BofA care? They’re too big to fail anyway.

[..] “It’s really about the stabilization of the real-estate market and property values going up. It gives us more comfort as to the value of the homes – the equity is there and the client profiles look strong,” said Tom Wind, executive vice president of home lending at EverBank, based in Jacksonville, Fla. [..] Some lenders are even bringing back “piggyback” loans, which serve as a second mortgage and cover part or all of the traditional 20% down payment when purchasing a house. Piggybacks nearly vanished during the mortgage crisis.

Piggybacks bring back the 100% LTV loan. It may not be entirely subprime, but we’re well on the way there.

Banks have been emboldened to originate new Helocs in part because new regulatory requirements completed this year and last year make it less burdensome to do so. And in an era where interest rates are expected to rise in the future, some lenders say they prefer Helocs over some other home-equity products because interest rates on Helocs rise as interest rates rise, making the products potentially more profitable.

Oh well, there you are. Regulators have weakened regulations once again, always a good first step towards trouble. Lenders can now aim for those ‘potentially more profitable products’ again, that have already brought us so much joy in this new century. And got millions of American families unceremoniously thrown out of their homes. What’s not to like?

Ian Feldberg planned to open a $200,000 Heloc this week with Belmont Savings Bank to help pay his son’s college tuition. The medical-device scientist purchased his home in Sudbury, Mass. for a little over $1 million in 2004, and estimates that its value dipped as low as $800,000 during the financial crisis. However, after applying for the line of credit, he found that its value had completely recovered. “I’m very pleased about that.

A medical-device scientist with a million dollar home who can’t afford college tuition. If that isn’t a sign of the times, what is?

To summarize, if that’s still necessary, home prices, like prices for all assets, are way higher than they would have been without QE. And still 20% of mortgage holders can’t afford to even sell their homes, let alone upgrade. But already lenders are waving promises of cheap money in front of their faces again. Have we not learned anything at all from the depths of the crisis? The answer is a resounding No. We can still fool ourselves and each other into a form of mass psychosis, thinking we’re much richer than we are, and act accordingly. It’s enough to make one that much more despondent about the future of this failed experiment that was once the land of the free. If you know what’s good for you, ignore things like this WSJ article, and if you can’t be free, at least be debt-free. Because after the fake asset values of the illusionary economy fall back to earth, the debt will remain. And y’all will feel a lot less wealthy.

• US Borrowers Tap Their Homes at a Hot Clip (WSJ)

A rebound in house prices and near-record-low interest rates are prompting homeowners to borrow against their properties, marking the return of a practice that was all the rage before the financial crisis. Home-equity lines of credit, or Helocs, and home-equity loans jumped 8% in the first quarter from a year earlier, industry newsletter Inside Mortgage Finance said Thursday. The $13 billion extended was the most for the start of a year since 2009. Inside Mortgage Finance noted the bulk of the home-equity originations were Helocs. While that is still far below the peak of $113 billion during the third quarter of 2006, this year’s gains are the latest evidence that the tight credit conditions that have defined mortgage lending in recent years are starting to loosen. Some lenders are even reviving old loan products that haven’t been seen in years in an attempt to gain market share.

In 2013, lenders extended $59 billion of Helocs and home-equity loans. The last pre-boom year near that level was 2000, when lenders extended $53 billion, according to Inside Mortgage Finance. “We’re seeing much more aggressive marketing campaigns [for Helocs] by banks in locations where home prices have risen,” said Amy Crews Cutts, chief economist at Equifax Inc., a firm that tracks consumer-lending trends. She said Heloc originations picked up in recent months as consumers began home-improvement projects. “We expect to see quite an uptick in Heloc activity” in the spring, she said. Unlike home-equity loans, in which the borrower receives a lump sum, borrowers can draw on Helocs as needed. They can sometimes take a tax deduction on the interest from the credit line.

• The Housing Bust And The American Psyche (Harrop)

Real estate mania lives on at the HGTV cable channel, where house shoppers still holler for granite on their kitchen islands and his-and-her sinks in their en-suite bathrooms. But in the non-TV reality of middle-class America, the bloom is definitely off the real estate rose. The rose isn’t dead, mind you. Surveys show an enduring desire to own one’s home, despite the trauma left by the real estate meltdown and recession. But the love is not what it was. So customer demand continues, Jane Zavisca, a University of Arizona sociologist, told me, “but not homeownership at all costs.” Young people who’ve seen others’ lives ruined by the pain of foreclosure seem especially wary of taking on a mortgage, according to Zavisca, who studies attitudes toward home owning.

More on the psychology later. Economists worry that the depressed housing sector is hampering a robust recovery. Federal Reserve Chairwoman Janet Yellen recently testified before Congress that housing remains a cloud on an otherwise promising economic horizon of stronger hiring and amped-up consumer spending. True, some formerly shattered markets — in Phoenix, Las Vegas and parts of California, for example — have much improved. But nationally, the sign of a housing recovery seen a year ago now appears to have been a blip. And the problems in the sector aren’t going away.

What’s wrong is this: At the end of March, 19% of “homeowners” with mortgages — nearly 10 million households — were “underwater.” That means they owed more on their house than they could sell their house for. These numbers come from the real estate website Zillow. That sounds a lot better than the 31% owing more than their house was worth near the height of the misery in 2012. But it doesn’t count the legions of homeowners barely above water. Many lack the financial breathing room to sell; they’d have to first find some extra cash.

• Homeowners Struggle To Pay Mortgages On Houses Of All Sizes (LoHud)

In the Lower Hudson Valley, one of the most affluent regions of the country, where one in five homes costs a million dollars, there are thousands of homeowners still struggling to pay their mortgages, often facing foreclosure. They’re from all income brackets, living in those million-dollar homes, modest Capes, condos and Colonials. The reasons vary, but most often there is a major life change: job loss, divorce, a death in the family, or a serious illness that causes a homeowner to get behind on their mortgage or property taxes. Foreclosure filings are at record highs in Westchester and Rockland, with Westchester experiencing filings that are triple what they were last year. Behind the numbers are people faced with the possibility of losing their homes.

LaDonna Thompson Hutchins got behind in her monthly payments. Hutchins, a 30-year Manhattan postal worker, lives in a two-family house in Mount Vernon that her grandmother and mother bought in 1978; both have since died. With mounting medical bills and personal stress, Hutchins missed some mortgage payments and her lender took action, refusing to accept any payments until the arrears were paid in full. Now she owes $210,000, mostly in late fees and attorney costs and is working with a counselor to reduce the payments and get back on track. The balance on her mortgage is $466,000. “It’s my mistake. I refinanced a couple of times and fell behind,” Hutchins said. “I am making the money and they won’t give me a chance.” She rents out a 3-bedroom unit and basement studio in the house for income. “This is my house. Mount Vernon is my home.” [..]

Foreclosure is hitting most socio-economic groups and most neighborhoods, said Peter Spino Jr., a White Plains-based lawyer who represents homeowners in similar situations. “We are seeing recurring spikes in the (foreclosure) numbers,” he said. “And it is climbing the economic ladder. The wealthy, who were able to stave off (legal action) because they had resources, have had those resources depleted.” One court official told him there have been weeks with 70 filings, which is “extraordinary,” he said. “The hardships are horrific. But a lot of people are getting loan modifications and saving their homes,” Spino said. “If you have the income to support a loan modification you can get a loan modification. But you have to remember that in Westchester the taxes are so high that you have to also estimate about $1,000 a month for taxes and insurance.”

• The Linoleum Economy (Peter Tchir)

Before reading further, just pause and think about what linoleum means to you. If flooring isn’t your thing, go ahead and think about Formica cabinets or anything else that fits the genre. To me, it is something functional, which looks okay from a distance, but doesn’t stand up well to closer inspection. It conveys the disappointment of something that looked good, but turns out only to be a thin veneer covering cheap particle board. That is how I see the economy right now. I think that at the moment we are getting a bit of a “bounce” from the disastrous first quarter, but that it is far lower than it should be if the underlying economy was strong. Even worse, is I think there is a real chance that the economy slows again, driven by a weakness in housing, and the Fed has very few useful tools left, if that happens. But before going into more detail on why I have that view of the economy and what I think it means for the market, let’s look at what others are thinking.

The 2007 Recession: I won’t spend more than a moment on this, but I still find it “perplexing” if not insane, that the recession that started in December 2007 wasn’t “identified” until December 2008. We were only told that we had been in a recession for a year AFTER Lehman failed and AIG was bailed out. I understand the saying “better late than never” but seriously, this is a bit ridiculous. It really shouldn’t have taken a -765,000 NFP print to confirm to the powers that be, that the economy had already been sucking wind for a year. I am not saying that the same thing is happening again, but I would not be handing out any awards for seeing what is right before your eyes to the group of prognosticators responsible for seeing bad things in the economy.

Q1 2014 GDP: Which brings us right to Q1 2014 GDP. I do not know what the expectations were back in January of this year. But I do know that by the time the first release of GDP came out, we all knew the weather had been bad.

Expectations had been ratcheted down to 1.5%, yet the number was an appallingly low 0.1%. A huge miss. As more data came out, the economists could refine their forecasts. They came in at -0.5% and once again the estimates were too optimistic as the actual number was -1.0%. Maybe not quite as embarrassing as the initial miss, but…

While I have heard some “positives” like inventory build will help Q2, I have heard any things that show we may have gotten lucky to “only” be at -1%. It seems many people were surprised how much of a “positive” impact Obamacare had on the numbers. There is also a debate that is getting louder by the day, that the real inflation rate is higher than the reported inflation rate, artificially making Real GDP seem higher than it is. Fool me once, shame on you, fool me twice, shame on me. They had two chances to get this number right and missed both times by being too optimistic. Why are we so eager to believe the optimism most share for the first quarter? The fool me once phrase resonates with me right now. I promise I am almost done picking on our “ability” to forecast GDP, but I cannot resist showing this one last chart on the street’s view of GDP.

GDP is fully expected to bounce back to just over 3% for Q2 and then settle into a nice cozy run rate of 3.0%. All is good, right? Not so fast. The data just looks careless. The prior 5 quarters have been 1.1%, 2.5%, 4.1%, 2.6%, and -1%. The average isn’t anywhere close to 3% and the numbers have shown no consistency. I would be much more comfortable with the chart if I saw some peaks and valleys in the estimates. I would like to see some evidence in the data that the estimates include any seasonal adjustment issues the data is experiencing (post Lehman, many adjustments seem to fail frequently as they are not good at adapting to 7 standard deviation moves). Maybe there is something that should be helping drive one quarter versus another quarter. (Obamacare? Heck even a new iPhone).

The scourge of the markets: you got to try and make money somewhere, even if you know that may not be the wise thing to do. Where means is confused with end.

• You’re All Whales in Bond Market Now With Trading Volume Slump (Bloomberg)

It’s getting easier for a smaller group of bulls in the U.S. Treasury market to create angst for the bears. That’s because government-debt trading volumes have slumped to 18% below the decade-long average, Federal Reserve data show. As Brean Capital LLC’s Peter Tchir wrote this week: “There is no liquidity even in the mighty Treasury market.” So as 10-year Treasury yields plunged toward the lowest level in almost a year, a smaller group of active traders may have had a much bigger influence over the $12 trillion market that determines rates on everything from auto loans to corporate debt.

The move in government bonds has defied predictions from Wall Street’s biggest banks for higher borrowing costs, with 10-year Treasury yields falling to 2.47% from 3% at the end of 2013. “With less trading capital to commit in fixed income, the dominant flow can appear bigger than it actually is,” Jim Vogel, a fixed-income strategist at FTN Financial (FTN) in Memphis, Tennessee, wrote in a May 28 note. U.S. government-bond trading has declined even as the size of the market tripled in the last decade. Trading volumes fell to an average $429 billion a day in the week ended May 21, Fed data show. That’s down from daily averages of $502 billion this year and about $566 billion back in 2007.

One reason for the slowdown is there aren’t as many obvious sellers of the notes. The Fed has been buying U.S. bonds for years, making it the biggest single owner of the debt. Other central banks have locked the bonds away in their vaults across the globe. Another reason is banks have less incentive to trade the debt. They’re reducing fixed-income inventories in response to risk-curbing regulations, such as the U.S. Dodd-Frank Act’s Volcker Rule, which limits the amount of their own money they may use to buy and sell riskier securities. Many are paring fixed-income staff, too, in the face of lower trading revenues.

• Bond Rally Sparks Little Joy as Bears See ‘Painful’ Capitulation (Bloomberg)

From the Americas to Asia, and from Europe to the Middle East, the $100 trillion bond market this year is turning into one for the record books. Returns on fixed-income securities of all types, from government to corporate and asset-backed debt, averaged 3.97% through the first five months of 2014 as of May 29, matching the record set in 2003 based on the Bank of America Merrill Lynch Global Broad Market Index. As bond prices rallied, yields as measured by the gauge fell to the lowest in a year. Rather than sparking celebration, the rally is causing much angst. That’s because many investors were betting on the opposite to happen as the global economy strengthened, leading central banks to start employing tighter monetary policies. Instead, growth slowed, signs of disinflation emerged in Europe and tensions between Ukraine and Russia sparked demand for the safety of fixed-income assets.

“It’s been a very painful week for a lot of people,” Elaine Stokes, a money manager who helps oversee the about $22 billion, Boston-based Loomis Sayles Bond Fund, said May 29 in a phone interview. “The big move we’ve seen recently, in the last couple of weeks, in the lowering of the yield base, is really a bit of a capitulation.” The Bloomberg Global Developed Sovereign Bond Index shows yields declined to an average 1.28%, the lowest since May 2013, as those on Austrian, Belgian, French, Irish and Spanish debt decreased to records. Treasury 10-year note yields – the global benchmark – fell this month by the most since January and Japanese yields slid to the least in 12 months.

Investors have been buffeted by a U.S. economy that shrank more than forecast in the first quarter and signals from the European Central Bank that it’s prepared to ease as German unemployment unexpectedly rose last month. Bank of Japan Board Member Sayuri Shirai said in a May 29 speech that unprecedented easing may continue beyond next year and downplayed optimism that inflation would reach its target in fiscal 2015. The Paris-based Organization for Economic Cooperation and Development cut its forecast for global growth, saying in its semi-annual report on May 6 that the world economy will expand 3.4% this year instead of the 3.6% predicted in November. All of that is good news for bonds, forcing investors to unwind trades betting on losses. Futures traders have been positioned for a rise in 10-year U.S. yields since August.

Yay! More debt! With yields as low as they are, it’s tempting.

• Spain To Unveil $8.6 Billion Stimulus Package (AP)

Spain’s prime minister says his government will unveil a stimulus package worth $8.6 billion to boost competitiveness. In another sign that the country is emerging from five years of economic hardship, Mariano Rajoy said his plan “aims to mobilize” €2.7 billion from the private sector and €3.4 billion from the public sector. He said Saturday corporate tax would be cut from 30% to 25%. Rajoy added that details will be revealed at a Cabinet meeting on Friday. Standard & Poor’s was the third credit rating agency to upgrade Spain’s sovereign credit grade on May 23 although Spain is still saddled with a massive 26% unemployment rate. Rajoy said Spain has created employment in the last two quarters.

• European Union Dream Threatened By Austerity And Disharmony (Observer)

The principal aim of the founding fathers of the European community was to ensure that there should never be another war between Germany and the rest, the most notable member of the rest being France. But a closely associated aim was to ensure general prosperity that, among other things, would not give rise to either the hyperinflation experienced in Germany after the first world war or the mass unemployment which created the conditions that gave rise to Hitler – who was democratically elected, but after that used undemocratic methods to remain in power.

The aim of the two prominent founding fathers, Jean Monnet and Robert Schuman, was to bring Europe closer together politically by economic means. The nightmare would be if the economic means adopted in recent decades served to pull Europe apart. One of the prominent successors, decades later, to Monnet and Schuman was Valéry Giscard d’Estaing who, as president of France in the second half of the 1970s, was a leading participant in the formation of the European monetary system and the exchange rate mechanism, the precursor to full monetary union and the euro.

It was noteworthy that in a recent interview with the Financial Times, Giscard observed: “It is said people are voting against Europe – that’s not true. They are voting against what Europe is doing wrong.” For Giscard, it is bad management, not the basic architecture, of the eurozone that is the problem. But if he studied the timely new book by Philippe Legrain, European Spring – Why Our Economies and Politics are in a Mess, he might be more inclined to accept that the fundamental structure of the eurozone is also to blame. Legrain, a former economic adviser to the president of the European commission, gives a vivid insider’s account of just how badly the European political and economic elite responded to the financial crisis.

As in the UK, the wrong diagnosis was made when laying so much of the blame on putatively excessive public spending – an analysis that may have applied to Greece, but not the others – as opposed to the credit crunch. Fiscal austerity was the wrong response, rendering the crisis much worse. The crisis was aggravated in the eurozone by the loss of such instruments as independence in the determination of monetary and exchange rate policy. But as Legrain forcefully points out, the UK’s freedom from such constraints did not prevent policymakers after 2010 from extending the crisis, with those three years of “flatlining”.

China is trying to stem a tsunami with sandbags.

• No, China Isn’t Really Rebalancing (Bloomberg)

“Tolerance” and “slowdown” clearly mean something different in Beijing’s dictionary. Since November, when the Communist Party announced epochal reforms, President Xi Jinping and Premier Li Keqiang have rarely missed a chance to say China must accept slower growth. Downshifting to a “new normal” is a necessary evil to regear the economy’s growth engines to services. Six months on, all they’ve done is add more and more stimulus to ensure no end to massive investment and exports. The first sign of slowdown intolerance came in early March when China did what optimists hoped it wouldn’t: announce another growth target. Every time data have suggested gross domestic product might slip below that 7.5% line, Beijing has been quick to rev the engine yet again.

Stimulus measures have included tax breaks, bigger investments in housing, faster spending on railways and other megaprojects, and front-loading of outlays at the provincial level. China’s largest regional economy, Guangdong, is allocating more than $10 billion to boost growth. The National Development and Reform Commission, the central economic-planning agency, is mulling a $16 billion-plus fund for transportation that will solicit some private investment. The central bank, meanwhile, has eased up on its war against excess credit, and the shadow-banking system is still enabling inefficient state-owned enterprises across the nation.

Does any of this sound like the actions of government ready to let GDP fall to 6%, let alone 5%? Hardly, which is why economists at Nomura and UBS are rethinking second-quarter growth forecasts. Credit Agricole economist Dariusz Kowalczyk reckons that the stimulus steps that we know about — I’m figuring there are many we don’t — will add 1%age point to Chinese growth. All this flies in the face of slowdown pledges and, by extension, restructuring efforts. The economy must decelerate to rein in the excessive borrowing that Marc Faber, publisher of the Gloom, Boom & Doom report, calls a “gigantic credit bubble” and hedge fund manager Jim Chanos of Kynikos Associates is shorting.

• China Manufacturing PMI Jumps; What’s Wrong With This Chart? (Zero Hedge)

Despite all the shadow banking system hand-wringing, macro-data-collapsing, real-estate-bubble-bursting, stock-market-tumbling reality facing China, somehow, China’s official government manufacturing PMI just printed 50.8 – its highest in 2014 and the 20th month of expansion in a row. Given the mini-stimulus efforts of the government, perhaps it is not surprising that the official (more SOE-biased) data signals all-clear (when HSBC’s PMI is still in contraction for the 5th month in a row). The employment sub-index fell to a 3-month lows and the Steel industry’s output and new orders has cratered… So what’s wrong with this chart?

Draghi looks set to finish off what’s left of the eurozone by adding debt to injury.

• Mario Draghi Faces Moment Of Truth To Steady Eurozone (Observer)

The meeting will be held on the day before the 70th anniversary of the Allied landings in Normandy, but make no mistake: Thursday is D-day for the European Central Bank. That’s D as in Draghi, because after all of the ECB governor’s silver-tongued manipulation of the market – all the nudges, winks and hints – the financial markets now require Mario Draghi to do more than just talk. Expectations are high, probably unrealistically so. After the bloody nose received by mainstream parties in last week’s elections to the European parliament, former US treasury secretary Larry Summers had some harsh things to say on US news network CNN about the mess that policymakers had made of things: “The European common market, European monetary union, was an elitist project that was driven by elites, that led to consequences that were entirely unpredicted by elites, that have been catastrophic for millions of people.”

Draghi can do little to rekindle love for the idea of ever-closer union in Europe – a project damaged, perhaps beyond repair, by recession, unemployment and austerity. Nor is he in a position to eradicate the structural problems of the euro – its one-size-fits-all interest rates, its inbuilt deflationary tendencies – that have been obvious since its creation. These are beyond his remit. The “elite” lambasted by Summers has to decide whether to press ahead with closer fiscal integration – a centralised budget that might make the single currency work better – in the face of clear voter hostility to greater unity. Instead, the ECB meeting will have a less ambitious, but still crucial, agenda.

As Investec economist Philip Shaw puts it, Europe’s central bank has four key objectives this week: “To ease policy to meet its inflation target; to prevent inflation expectations from being dislodged to the downside and increasing the risks of deflation; to stem upward pressure on the euro; and to secure and preferably speed up the recovery, possibly by encouraging credit flow.”

No, really?!

• U.S. Accused of Destroying Spy Records Sought as Evidence (Bloomberg)

Years of phone and Internet records collected under anti-terror surveillance programs and sought as evidence in a lawsuit were destroyed by the U.S., the Electronic Frontier Foundation said. The government wiped out the records without getting approval from the federal judge overseeing the case, who ordered the evidence preserved, Cindy Cohn, legal director of the San Francisco-based cyber rights advocacy group, said in a court filing today. The court should now assume the missing records would have shown the government spied on the EFF’s clients, who are challenging the programs, Cohn said. “We are simply asking the court to ensure that we are not harmed by the government’s now-admitted destruction of this evidence,” Cohn said in a e-mail.

The EFF’s 2008 lawsuit was one of the earliest to question secret spying programs put in place after the 2001 terrorist attacks, claiming the National Security Agency intercepted phone communications in violation of wiretapping laws. It cited documents provided by a former AT&T Inc. telecommunications technician allegedly showing the company routed copies of Internet traffic to a secret room in San Francisco controlled by the NSA. The government destroyed three years of telephone records seized between 2007 and 2012 and seven years worth of Internet records it seized between 2004 and 2011, the EFF said in court papers today. The group said in a statement the government admitted the destruction in recent court filings.

The government understood the lawsuit to challenge presidentially-approved programs authorizing warrantless surveillance, not surveillance authorized by a special court in Washington that was leaked last year, Justice Department lawyers said in a May 9 court filing. The EFF has filed a separate lawsuit challenging NSA surveillance first disclosed in documents leaked by former security contractor Edward Snowden. The NSA in March was blocked by the federal judge in San Francisco overseeing the case from destroying phone records collected from surveillance because they might be relevant to the lawsuit.

Not sure about this, Simon.

• Why America Is In Decline (Simon Black)

Along with history, travel is by far one of the best teachers. Formal education in classrooms can be stifling to the mind. It makes people believe that the world actually conforms to all the snazzy theories we read about. But there’s no economic textbook on the planet that can come close to showing you how the world really works. It’s not about stocks and flows, efficient markets, or official statistics. None of that stuff really matters. The world runs on people. And even though our politicians go out of their way to highlight the differences among us, human beings all over the world are fundamentally the same. We all love our children. We cheer for our favorite teams. We work hard to put food on the table for our families. We get frustrated with where we’re at in life. And we desire to achieve more.

This desire to achieve is fundamental to all humanity. Human beings aspire. We push ourselves to accomplish more and improve our stations in life. And this desire spans generations. Parents always want their children to enjoy a better life than they had. And they work their butts off to ensure this happens. This isn’t exclusively a western phenomenon. All over the world, the need to provide a better life for one’s children is practically a subtext to the social contract. And people in developing countries want exactly the same thing. They’re succeeding. A child born in China today will have a far richer life than his/her parents and grandparents. And in my travels to over 100 countries over the last 10+ years, I’ve seen other frontier and developing markets that are bursting at the seams in a similar trend. Myanmar. Colombia. Tanzania. Georgia. Sri Lanka. Botswana. Indonesia. Mongolia.

The growth rates in these places are staggering, and you can see first-hand the hundreds of millions of people being lifted out of poverty. In these developing countries, they look across the water to the West and can see a rich and consumptive lifestyle. They want this lifestyle, especially for their children. They’ve spent decades toiling in factories, saving money, and building for the future. It’s time to cash in. Decades ago, the vast majority of wealth and production was in the West– specifically the United States. Most people across Asia and Latin America were absolutely impoverished, and felt honored just to be able to work hard and export a product to the US. Today, it is those same countries (particularly in Asia) that now hold the majority of the world’s wealth and production. And it is their growth that pulls the global economy along.

Now, that’s a number.

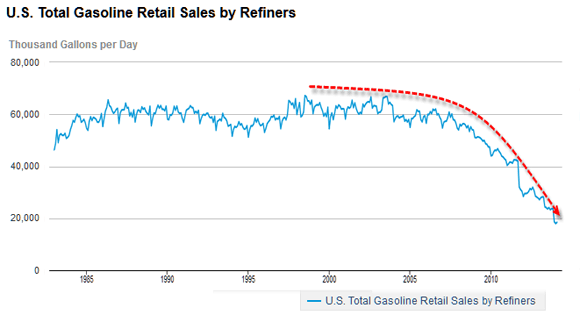

• US Gasoline Consumption Plummets By Nearly 75% (Jeff Nielsen)

Regular readers are familiar with my narratives on the U.S. Greater Depression, and (in particular) some of the government’s own charts which depict this economic meltdown most vividly. The collapse in the “civilian participation rate” (the number of people working in the economy) and the “velocity of money” (the heartbeat of the economy) indicate an economy which is not merely in decline, but rather is being sucked downward in a terminal (and accelerating) death-spiral. However, even that previously published data, and the grim analyses which accompanied it could not prepare me for the horror story contained in data passed along by an alert reader. U.S. “gasoline consumption” – as measured by the U.S. Energy Information Administration (EIA) itself – has plummeted by nearly 75%, from its all-time peak in July of 1998. A near-75% collapse in U.S. gasoline consumption has occurred in little more than 15 years.

Before getting into an analysis of the repercussions of this data, however, it’s necessary to properly qualify the data. Obviously, even in the most-nightmarish economic Armageddon, a (relatively short-term) 75% collapse in gasoline consumption is simply not possible. Unless we were dealing with a nation whose economy had been suddenly ripped apart by civil war, or some small nation devastated by a massive earthquake or tsunami; it’s simply not possible for any economy to just disintegrate that rapidly, without there being some ultra-powerful exogenous force also at work.

So how can this raw data, produced by the government itself, be explained? To begin with; the government chooses to measure U.S. gasoline consumption in a very odd manner: by measuring the amount of gasoline entering the domestic supply-chain rather than by measuring actual consumption at the other end of the supply-chain – i.e. “at the pump”. Why does the U.S. government, which (among other things) leads the world in the manufacture of statistics not produce any simple/direct measurement of gasoline consumption? How can the St. Louis Fed produce nearly 100 different charts on gasoline and diesel prices (for any/every price-category which can be imagined by these statistics geeks), but not a single chart on gasoline supply/demand? There are several reasons for this unbalanced, anomalous, and simply absurd statistical methodology.

First of all; the reason why the U.S. government produces a near-infinite number of charts on prices is because prices are what the Gamblers (i.e. bankers) use as the basis for their $100’s of trillions in gambling in the rigged casinos which the bankers call “markets”. While supply/demand data is of utmost importance in the real world; the banker-gamblers don’t dwell in the real world. As regular readers already know; their derivatives casino, alone, is roughly twenty times as large as the entire global economy. To the bankers; the “real world” is nothing but fodder for their insane gambling. Why use this data, at all, since it is such an inferior/distorted means of measuring U.S. gasoline consumption? Because the EIA uses exactly the same data to publish its own “estimates” of U.S. gasoline consumption:

Note: Product supplied measures the amount of gasoline that went into the supply chain and is used as a proxy for gasoline consumption.

The other half of this ridiculous statistical hodge-podge, where endless quantities of trivial/irrelevant price data are trumpeted, while any/all data which actually measures the (real) economy is suppressed (if not buried entirely) displays a government desperately trying to hide this massive economic collapse. If you choose to measure the amount of gasoline leaving U.S. refineries and entering domestic inventories and call this “gasoline consumption”; you can hide the actual collapse in gasoline consumption – until those retail inventories are overflowing, and there is simply no more room in the storage tanks.

Isn’t that strange? Where’s the pent-up demand?

• Homebuyers With Another Shot at Low Rates Still Don’t Buy (Bloomberg)

This was supposed to be the year that U.S. mortgage rates soared. Instead, they’re retreating. Interest rates unexpectedly fell this year after the Federal Reserve began scaling back the stimulus that held borrowing costs near record lows since 2011. After five weeks of declines, rates for 30-year fixed loans are at 4.12%, the lowest in seven months, Freddie Mac said yesterday. The housing market, in the season that’s traditionally its busiest, can use the help, even if it’s short-lived. Soaring home prices and a one%age point spike in rates from May to August last year cut into affordability and slowed the real estate recovery. While the falling borrowing costs have forced economists at the National Association of Realtors and Moody’s Analytics Inc. to lower forecasts, they still expect 30-year rates to lurch closer to 5% by the end of the year.

“It’s a temporary window of opportunity for buyers in that a year from now rates will be higher,” said Mark Zandi, chief economist for Moody’s Analytics in West Chester, Pennsylvania. “The housing market could use it given how it’s gone sideways. But I wouldn’t count on these low rates for very long.” The decline in borrowing costs has so far done little to spur sales, which have been weighed down by tight credit and lower-than-normal inventory levels. Contracts to buy previously owned houses in the U.S. increased 0.4% in April, less than economists estimated. They fell 9.2% from a year earlier, the National Association of Realtors said yesterday. Loan applications for home purchases were down 15% last week from the same period a year earlier, according to a Mortgage Bankers Association index.

Oh wait, there it is(n’t).

• US Household Formation Rate Plunges To 30-Year Low (Stockman)

Cool-Aid drinkers like the Keynesian bozos at The Atlantic (The Most Overlooked Statistic in Economics Is Poised for an Epic Comeback: Household Formation) have been gumming ever since the 2009-2010 bottom that household formation will come springing back. Recall that during the decade before the financial crisis new household formation averaged about 1.5 million per year, but has since dropped by two-thirds to about 500k. Its obviously all about student debt serfs who have moved back into mom and dad’s basement and who flip hamburgers on weekends for enough change to get by on. Yet this condition was held to be a transient artifact of the financial crisis and the recession which followed—an aberration that went unexplained but which was also firmly dismissed as a 100-year flood type event.

So the blustering insistence that kids would soon leave mom and dad’s basement and that the household formation rate would leap out of the sub-basement of its historical trend line actually crystalizes the circular illogic of the whole Keynesian case. The supposition was that we function in a timeless and ever repeating business cycle which fiscal and monetary stimulus inexorably (and magically) arouses from its slumping phase. Accordingly, it is always and everywhere only a matter of time before a “stimulated” economy achieves “escape velocity”, thereby causing the growth of jobs, income and spending to accelerate. The latter, in turn, always has and would again fuel “normal” household formation rates. From there it would be off to the races—with a subsequent virtuous cycle of more households generating more demand for new housing starts, construction jobs, income, spending and all the rest of the magic.

But this whole happy scenario is really just another case of the legendary economist who proposed to ascend from a 50 foot hole by announcing, “assume we have a ladder”. The Keynesians did not explain why an economy with $59 trillion of credit market debt and stranded at peak leverage ratios across all sectors— households, business and public sectors alike—would suddenly break into a sprint, and thereby pull along a food chain of earners, spenders and household formers. They didn’t address that crucial matter, of course, because the Keynesian models contain no balance sheets—just flows of what in cycles past were freshly minted household credit and spending power, and which now amount to some mysterious ether called “accommodation”.

Stated differently, what the Keynesian models resolutely ignore is this cardinal fact: After 40-years of a giant debt party in America, damage has been done! There is no escape velocity because there is no escape from a condition in which too much consumption, borrowing and get-rich-quick speculation has led to a drastic impairment of capitalism’s ability to generate genuine economic growth and new wealth. In any event, the Q1 numbers are out, and the household formation rate has taken another turn south—to a gain of less than 200k over the past 12 months or barely 15% of its heyday average. Indeed, in contrast to the sizzling snap-back to 2 million or more annually expected by the Keynesian modelers, the current rate is now at a 30-year low! Yes, immense damage has been done. And monetary planning is only making it far worse.

Let him.

• QE In Financial Drag: Draghi’s New ABCP Monetization Ploy (Stockman)

You can smell this one coming a mile away:

The European Central Bank and Bank of England on Friday outlined options to reinvigorate the market for bundled bank loans, which was “tarnished” by the global financial crisis, saying a better-functioning market for asset-backed securities can help boost lending to the private sector, particularly small businesses.

Yes, the ECB is now energetically trying to revive the a market for asset-backed commercial paper (ABCP)—-the very kind of “toxic-waste” that allegedly nearly took down the financial system during the panic of September 2008. The ECB would have you believe that getting more “liquidity” into the bank loan market for such things as credit card advances, auto paper and small business loans will somehow cause Europe’s debt-besotted businesses and consumers to start borrowing again—- thereby reversing the mild (and constructive) trend toward debt reduction that has caused euro area bank loans to decline by about 3% over the past year. What they are really up to, however, is money-printing and snookering the German sound money camp. That is, the ECB is getting set to launch QE in financial drag by purchasing or discounting ABCP while loudly proclaiming that it’s not “monetizing” any stinking sovereign debt!

And that gets to the heart of monetary central planning. It doesn’t matter what the central bank buys with the digital credits it transfers to sellers. Purchasing government debt, Fannie Mae securities, IBM bonds or corporate equities, as has been done by the BOJ and Bank Of Israel under the new Fed Vice-Chairman, has a common effect. That is, it raises the price of the purchased “assets” relative to what would obtain in the unfettered market, and injects fiat liquidity into the financial system in a manner that promotes speculation and excessive risk-taking. Thus, if some clever Wall Street operators could figure out how to bundle sea shells and securitize them, central bank purchase of the resulting ABCP would be no different than purchase of treasury notes or Fannie Mae paper.

• The Global Death Cross Just Got Deathier (Zero Hedge)

In the immortal words of Cher: “Do you believe in life after QE; I can feel something inside me say, “I really don’t think you’re strong enough, Now.”

• Climbing A Wall Of Cliches (Nick Colas)

If clichés reflect overly common (if therefore unappreciated) wisdom, then we finally have a good explanation for why risk assets continue to rally. No, there are actually not “More buyers than sellers” – money flows are negative over the last month for both U.S. equity mutual funds and ETFs. And forget about investors “Downgrading on valuation” as stocks climb higher and higher; truth be told, that’s not even really a thing (unless you work on the sell side). Nope, this is a “Flight to quality”, “don’t fight the Fed”, “never short a dull market” environment with “easy comps” from a long rough winter. Want to call a top somewhere around here? Remember that “Markets discount events 6 months in the future.” A “Santa Claus rally” in June? That would fit the one cliché we know is actually the market’s True North: it will do exactly what hurts the most “Smart” investors. And that would be to rally further as the doomsayers double down and the timid cling to their bonds and cash.

“You don’t want to live in a world where the Federal Reserve can’t move stock markets.” That is one of the most important observations I have heard in this business, and it came from a grizzled old veteran some 15 years ago. The venue was one of those interminable “Idea dinners” and we young pups had been sniping about the whole “Follow the Fed” approach to equity analysis. The old lion eventually swatted away our objections with his simple observation. And he was exactly right. If the Fed can’t move markets with its balance sheet and a little time, then you might as well hit up Youtube/Google for “How to skin a squirrel” and “bartering for surplus ammo”.

So how did the famous phrase “Don’t fight the Fed” become such a derided and devalued cliché? The short answer is that many overused phrases are still true. That’s why they end up so often repeated in the first place. Don’t play with matches. Don’t run with scissors. Cross at the green, not in between (that’s a little 1970s NYC cliché trivia there). All good guidance, but over time and with repetition even the catchiest phrases turn from useful aphorism to forgettable, time wasting, and moldy word play.

Wall Street phrases are especially susceptible to the reverse metamorphosis of swan-to-duckling. For all its supposed sophistication, finance is still anchored in oral traditions more than most 21st century occupations. In what other industry does a leading light go by the moniker “Oracle of…”? After all, the original Oracle sat in Delphi, believed in the pantheon of Greek gods, and anchored her (yep, the Oracle was a young woman) cultural identity to the stories of the blind and illiterate Homer. The modern one dispenses comforting wisdom anchored in a native optimism about human innovation and faith in capital markets.

The wrath of QE in general too.

• The Wrath of Abenomics: Sales Collapse, Inflation Soars (TPit)

Even the soothsayers and Abenomics spin doctors expected a downdraft after Japan’s consumption tax was jacked up to 8% from 5%, effective April 1. But not this. The tax hike had been pushed through parliament by Prime Minister Shinzo Abe’s predecessor. It was supposed to save Japan. But no one wants to pay for government spending. The tax proved to be so unpopular that Prime Minister Noda and his government were unceremoniously ousted at the end of 2012. Japan is in terrible fiscal trouble. Half of every yen the government spends is borrowed, now printed by the Bank of Japan. Expenditures can’t be cut, apparently, and government handouts to Japan Inc. had to be increased. Yet something had to be done to keep the gargantuan deficit from blowing up the machinery altogether, and it was done to those who spend money.

The consumption tax is very broad, impacting goods and services bought by businesses and individuals, from haircuts and vegetables to construction materials. So the 3-percentage-point increase would be levied on much of the economy. But here is the thing: money that people and companies keep in the bank earns nearly nothing, and even a crappy 10-year Japanese Government Bond yields less than 0.6% per year. But if buyers frontloaded major purchases by a few months or even a year to beat the consumption-tax increase – buying that refrigerator or heavy-duty truck a year earlier than they normally would, for example – they’d save 3% of the purchase amount. That’s pure income. And tax-free for individuals. The biggest no-brainer in Japanese financial history.

Every company and individual frontloaded whatever was sufficiently practical and substantive, and whatever they could afford. It started late last year and culminated in the January-March quarter. As a result, GDP soared at an annual rate of 5.9%, a phenomenal accomplishment for Japan. The Japanese have been through this before. Ahead of the prior consumption-tax hike from 3% to 5% effective April 1, 1997, consumers and businesses went on a buying binge of big-ticket items. The economy boomed for a couple of quarters, then woke up with a terrific hangover as spending on durables by businesses and consumers ground to a halt, and the economy skittered into a nasty recession that lasted a year and a half!

But this time, it’s different. On March 23, about a week before the tax hike would take effect, the Nikkei polled corporate executives as they were still floating on a sea of optimism from all the money that rampant frontloading was bringing in faster than they could count. They weren’t concerned: 70.2% said that sales would remain stable or decline no more than 5% in fiscal 2014, which started April 1; 55.4% said the economy, supported by strong consumer spending, would improve by September, and 74.3% saw that happening no later than December. So no big deal. Alas, the Ministry of Economics, Trade, and Industry just released a dose of reality. Total retail sales in April plunged 19.8% from March and were down 4.4% year over year. But this includes sales of perishable and small items not suited for frontloading, and convenience-store sales (which rose a smidgen). In stores where people buy durable goods, such as appliances, watches, or cars, sales were awful.

The illusionary economy.

• The Big Hoax Of The Wall Street Hype Machine (TPit)

The S&P 500 index keeps bumbling from one all-time high to the next as corporations are issuing record amounts of debt to spend record amounts on buying back their own shares: $160 billion in the first quarter alone, according to CapitalIQ. Borrowing money to buy back shares and hyping it ceaselessly as “returning value to the shareholders” is the most effective way to manipulate up the stock, even if revenues are declining quarter after quarter. In this climate of ZIRP, any major corporation can do it. The heavy buying during these low-volume times pushes up shares, the hype surrounding the buybacks pushes up shares, expectation of more buyback announcements pushes up shares, the mere idea that shares are being pushed up pushes up shares…. And in the end, the buybacks lower the share count for the all-important EPS ratio.

The game works wonderfully. Though a game is all it is. It’s not an investment in productive capacity, marketing, or expansion projects. It’s not an investment in people. It’s not an investment that will bring future revenues or earnings or efficiencies. It’s not an investment at all. It just blows a lot of cash on manipulating the one number that the entire world is focused on. But it’s not even actual earnings as reported under GAAP that is the focus of all attention. It’s an estimate of “forward,” ex-bad-items, adjusted, pro-forma “earnings,” so an entirely fictitious number, helpfully provided by the Wall Street hype machine through its analysts and eagerly disseminated by the media.

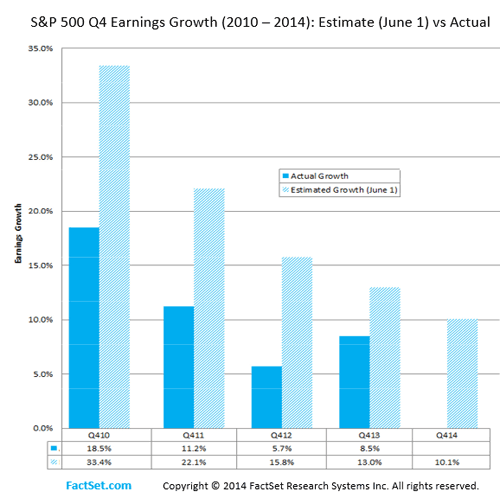

That gloriously fictitious 12-month “forward” ex-bad-items, adjusted, pro-forma “earnings” per share then becomes the denominator in the 12-month “forward” P/E ratio, which, according to FactSet, currently stands at 15.4. But just how far off the wall have these fictitious numbers been in the past? In its latest report, FactSet shed some light on this by comparing analysts’ estimates for earnings growth as of June 1 for Q4 of the same year, for the years 2010, 2011, 2012, and 2013. And it found, without explicitly saying so, that these projections are consistently the biggest hoax out there.

• Bond, Stock Rally Shows Need to Be Prepared -to Be Wrong- (Bloomberg)

During the first two World Wars, Boy Scouts sold U.S. bonds to help finance the fighting. If they were still at it today, there’d be a lot of merit badges to pass out globally after every bond market in the world rose in May. The Scouts never were called upon to sell stocks, and they certainly weren’t needed this month as the MSCI All-Country World Index jumped almost 2% and the value of the planet’s equities reached a record $64 trillion. Emerging markets led the gains in stocks as benchmark indexes in India, Russia, Hungary and Argentina jumped at least 8%. The Scout motto, of course, is “always be prepared.” So as the final sand of the market’s month slips through the hour glass, it’s a good time to reflect on how some investors and pundits were well prepared for all the wrong things in May.

In the Treasury market, conventional wisdom was to expect higher yields by now as we bid adieu to quantitative easing. (Or if you prefer the parlance of Internet commenters: bid adieu to imaginary Monopoly money printed by central banksters to puff up prices and make us so complacent we won’t notice when they come to grab our guns. Wake up, sheeple!) A Bloomberg survey of analysts in February called for the 10-year Treasury rate to jump this quarter to 3.15%, which would’ve been the highest since 2011. Instead, the yield fell steadily through May and touched an almost one-year low of 2.40%. Sovereign rates reached record lows in Spain and Italy amid speculation European central banksters would puff up prices with imaginary euros so no one notices when they come to grab their Vespas and Nebbiolo.

That’s the euro for you.

• Spain Sees 500% Rise In ‘Very Long-term Unemployment’ (RT)

Over one million people in Spain – the eurozone’s fourth largest economy – haven’t had a job since 2010, according to a report by Spain’s National Statistics Institute. Although this number continues to rise, the government says it’s witnessing recovery. The numbers, published on May 23, show that “very long-term unemployment” in the country has risen by more than 500% since 2007. That year, about 250,000 Spaniards were unemployed after losing their job at least three years prior. That number drastically rose to 1.27 million in 2013 – 234,000 more than in 2012. Generally, long-term unemployment includes jobless workers who have not been employed for more than 27 weeks.

The recent study shows that this category in Spain has transformed to very long-term unemployment, with hundreds of thousands people without a job for at least three years, and is now represented by over 23% of the total jobless population in Spain. The number is much higher than in other countries in the region at the same economic level, with another recent study showing that 26% of the country’s population is on government benefits in Spain – the second highest total in the EU after Greece. Still, politicians claim the nation emerged from years of on-and-off recession in mid-2013 and the situation continues to improve. On May 29, Spain reported its fastest economic growth since 2008, when the ten-year property bubble burst and prompted a financial crisis.

With millions of people searching for work in vain in the eurozone’s fourth largest economy (behind Germany, France, and Italy), the International Monetary Fund said this week that the country’s recovery is here to stay. “Spain has turned the corner,” the IMF’s annual report on the country’s economy stated. Earlier this year, Spain’s Economy Minister Luis de Guindos told parliament that in 2013 the economy saw the fastest growth the country had seen in six years. A couple months later, a study by Spain’s second biggest bank, BBVA, said that unemployment rates would take over a decade to recover to pre-crisis levels.

• In Spanish Riots, Anguish of Those Recovery Forgot (NY Times)

Four nights of rioting here in Spain’s tourism capital have highlighted the country’s persistent social tensions and belied signs of relief from a fragile economic recovery, which has yet to alleviate rampant joblessness. The rioting started on Monday when Barcelona’s City Hall ordered the eviction of squatters from Can Vies, a warehouse abandoned by the city’s transport authority. The site, in the Sants district, was taken over by squatters 17 years ago and turned into a makeshift social center. City officials said they wanted to reclaim the site for a park. After attempts to clear the site, protesters threw stones, barricaded streets, smashed bank and shop windows, and set fire to garbage containers and a television van. The rioting has since spread to other parts of the city, and police officers have arrested scores of people. On Friday, City Hall backed down and said in a statement that plans for the demolition of the site would be halted to help “favor a climate of dialogue.”

The squatters nonetheless pledged to continue their protests and to rebuild the half-destroyed center over the weekend. Joan Maria Solé, deputy director of the Federation of Neighborhood Associations of Barcelona, said the attempt to replace the Can Vies building with “a hypothetical park or green area” showed that City Hall was insensitive to the widening income gap among residents. Since hosting the Olympic Games in 1992, Barcelona has become one of Europe’s biggest tourism hubs, with a record 7.5 million visitors last year. The rise in tourism has helped Barcelona weather the economic crisis that hit Spain in 2008 better than many cities. Over all, the city of Barcelona’s unemployment rate is nearly 18%, roughly 8%age points lower than the national average, although there are big discrepancies between the city’s poorest and richest neighborhoods.

“Barcelona is full of contradictions, especially between those who are now unemployed and those who are just focused on earning even more from tourism,” Mr. Solé said. Can Vies, he added, “is unfortunately a more realistic image of Barcelona than the brand City Hall tries to sell.” The rioting this week echoed similar episodes elsewhere in Spain and in Turkey, where plans by Istanbul’s mayor to redevelop a popular public square set off weeks of protests last year. In January, the Gamonal district of Burgos, in northern Spain, was the scene of prolonged street fighting over plans by City Hall to remodel an avenue and remove many of its free parking spaces at a time of deep cuts in other areas of public spending. The plan was eventually shelved. Mr. Solé described Can Vies as “something of a symbol for the deprived.” As in Burgos, he added, “it is the kind of spark that can set ablaze a fire that has long been simmering.”

But how long for?

• How China Hides Its Tumbling Housing Market: It Simply Ignores It (Zero Hedge)

Recently we showed that in order to goose its fading all-important housing market (to China housing is like the stock market to the US: both mission-critical bubbles designed to give a sense of comfort and boost the “wealth effect”), China has first resorted to zero money down mortgages across various markets, and secondly to such gimmicks as “buy one floor, get one free.” However, that’s only part of the story. Even worse is what is not being disclosed to the general public: such as the true state of the housing market in China. Because according to a recent report on Sina, quoted on Investing In Chinese Stocks, when it comes to revealing just how bad things are domestically, Chinese developers are simply pulling a page out of biotech ETF playbooks, and simply not reporting price drops greater than 15%! From Investing In Chinese Stocks (ICS):

Taking a page from the climate scientists who hid the cooling trend in global temperatures, Hangzhou government will hide the cooling trend in the real estate market. Any price decline more than 15% below the list price will not be entered into the online registry. Developers are not forbidden from cutting prices and no sales will be stopped, though at least one developer expressed concern that advance sales permits may not be issued if the price cuts are deemed too large.

In other words, clear the market supply imbalance, but don’t see at market clearing prices, got that? Good luck. ICS goes on to show an example on the ground of just how profound the chaos is on the ground in China now that homes are suddenly in an air pocket with no (immediate) bailout coming from the government: according to at least one real estate agent, price cuts alone would be enough to kill his firm, and that is assuming sale pick up in the first place.

Hangzhou held a 4-day real estate exhibition recently. Attendance was 230,000, but only 32 homes were sold. These numbers are an improvement from 2013 and 2012 though. One state-owned developer said that price cuts cannot cure the market. The government must step in and ease buying restrictions, ease borrowing limitations, reduce bank reserve requirements, allow people to borrow for second and third homes, etc., in order to instill confidence in the market. The developer also said the media and experts were giving one sided reports, causing more chaos in the market, while buyers are more strongly adopting the wait and see attitude. He said buyers have no bottom line, if you cut 10%, they want 15%, if you cut 15% they want 20%. His firm has used price cuts of 10% and he hasn’t sold a home in 3 months. He said with government support, they can survive, but small private firms are not so confident.

A real estate agent said that even if sales pick up, price cuts will kill the firm. He said the government is more nervous than the industry because if land sales stop, they might not even be able to pay the wages of government workers. He expects, and hopes, the government will do something to rescue the market.

We know how to take care of ourselves.

• Toxins Accelerate Human Aging Process (NatGeo)

Why do our bodies age at different rates? Why can some people run marathons at the age of 70, while others are forced to use a walker? Genes are only part of the answer. A trio of scientists from the University of North Carolina argue in a new paper that more work needs to be done on “gerontogens”—factors, including substances in the environment, that can accelerate the aging process. Possible gerontogens include arsenic in groundwater, benzene in industrial emissions, ultraviolet radiation in sunlight, and the cocktail of 4,000 toxic chemicals in tobacco smoke. Activities may also be included, like ingesting excessive calories, or suffering psychological stress. Writing in Trends in Molecular Medicine, Jessica Sorrentino, Hanna Sanoff, and Norman Sharpless argue that focusing on such factors would complement more popular approaches like studying molecular changes in old bodies and searching for genes that are linked to long life.

“People have focused on slowing aging, which always struck me as premature,” says Sharpless. Even if scientists announced tomorrow that they’d discovered an antiaging pill, he says, people would have to take it for decades. “Getting [healthy] people to take medicine for a long time is challenging, and there are always side effects,” Sharpless says. “If you identify stuff in the environment that affects aging, that’s knowledge we could use today.” Twin studies have suggested that only around 25% of the variation in the human life span is influenced by genes. The rest must be influenced by other factors, including accidents, injuries, and exposure to substances that accelerate aging. “The idea that environmental factors can accelerate aging has been around for a while, [but] I agree that the study of gerontogens has lagged behind other areas of aging research,” says Judith Campisi of the Buck Institute for Research on Aging.

She adds that scientists have become more interested in these substances in recent years after learning that many types of chemotherapy, and some anti-HIV drugs, can speed the onset of age-related traits like frailty and mental decline. The quest to identify gerontogens is partly a quest to find better way of measuring biological age. There are several options, each one imperfect. Researchers could look in the brain and measure levels of beta-amyloid, a protein linked to Alzheimer’s disease, but these levels would not reflect aging in other parts of the body. They could measure the length of telomeres—protective caps at the end of our DNA that wear away with time. But doing so is hard and expensive, and telomere length naturally varies between people of the same age.

Home › Forums › Debt Rattle Jun 1 2014: The Illusionary Economy Revives The Home ATM