Unknown Gurley-Lord service station, San Francisco 1929

“A very unrewarding year.” Yeah, well, brace yourselves.

• US Stocks Close Out The Worst Year For The Market Since 2008 (AP)

U.S. stocks closed lower on Thursday, capping the worst year for the market since 2008. The Standard & Poor’s 500 index ended essentially flat for the year after the day’s modest losses nudged it into the red for 2015. Even factoring in dividends, the index eked out a far smaller return than in 2014. The Dow Jones industrial average also closed out the year with a loss. The tech-heavy Nasdaq composite fared better, delivering a gain for the year. “It’s a lousy end to a pretty lousy year,” said Edward Campbell, portfolio manager for QMA, a unit of Prudential Investment Management. “A very unrewarding year.” Trading was lighter than usual on Thursday ahead of the New Year’s Day holiday. Technology stocks were among the biggest decliners, while energy stocks eked out a tiny gain thanks to a rebound in crude oil and natural gas prices.

The Dow ended the day down 178.84 points, or 1%, to 17,425.03. The S&P 500 index lost 19.42 points, or 0.9%, to 2,043.94. The Nasdaq composite fell 58.43 points, or 1.2%, to 5,007.41. For 2015, the Dow registered a loss of 2.2%. It’s the first down year for the Dow since 2008. The Nasdaq ended with a gain of 5.7%. The S&P 500 index, regarded as a benchmark for the broader stock market, lost 0.7% for the year. According to preliminary calculations, the index had a total return for the year of just 1.4%, including dividends. That’s the worst return since 2008 and down sharply from the 13.7% it returned in 2014. While U.S. employers added jobs at a solid pace in 2015 and consumer confidence improved, several factors weighed on stocks in 2015.

Investors worried about flat earnings growth, a deep slump in oil prices and the impact of the stronger dollar on revenues in markets outside the U.S. They also fretted about the timing of the Federal Reserve’s first interest rate increase in more than a decade. The uncertainty led to a volatile year in stocks, which hit new highs earlier in the year, but swooned in August as concerns about a slowdown in China’s economy helped drag the three major stock indexes into a correction, or a drop of at least 10%. The markets recouped most of their lost ground within a few weeks. “The market didn’t go anywhere and earnings didn’t really go anywhere,” Campbell said.

From $114(?) to $37 in two years time.

• Oil Drops 31% In 2015 On Global Crude Glut (MarketWatch)

Oil futures ended higher Thursday in the final trading session of 2015, but posted a steep annual drop for the second year in a row as markets continue to wrestle with a global glut of crude. On the New York Mercantile Exchange, light, sweet crude futures for delivery in February rose 44 cents, or 1.2%, to finish at $37.04 a barrel. For the year, the U.S. benchmark dropped 30.5% and has lost 62.4% over the last two years. Crude hadn’t dropped two years in a row since 1998. February Brent crude, the global benchmark, rose 82 cents, or 2.3%, on London’s ICE Futures exchange to settle at $37.28 a barrel. Brent fell 35% in 2015, marking its third straight yearly drop. Oil trimmed gains somewhat after oil-field services firm Baker Hughes said the total number of U.S. oil rigs fell by two this week to 536.

Oil’s bounceback on Thursday likely reflected some short covering ahead of year-end and a three-day weekend, said Phil Flynn at Price Futures. U.S. markets will be closed Friday for the New Year’s Day holiday. Flynn said traders might be nervous about maintaining short positions amid rising tensions within Iran that could threaten the implementation of a nuclear accord that was expected to result in the lifting of sanctions that have prevented the country from exporting oil. Iran’s president has ordered his defense minister to expedite the country’s ballistic missile program following newly planned U.S. sanctions, he said Thursday, according to The Wall Street Journal. With U.S. production “growing for the last few weeks and global inventories being near storage limits, this is yet another reminder that the supply glut could take a long time to clear, which may mean even lower oil prices in the near term,” said Fawad Razaqzad at Forex.com.

Platinum and palladium are the more interesting metals when it comes to determining where economies are going.

• Gold Sinks 10% For 3rd Annual Loss as Platinum, Palladium Hit Hard (Reuters)

Gold was steady on Thursday, ending the year down 10% for its third straight annual decline, ahead of another potentially challenging year in 2016 amid the prospect of higher U.S. interest rates and a robust dollar. Largely influenced by U.S. monetary policy and dollar flows, the price of gold fell 10% in 2015 as some investors sold the precious metal to buy assets that pay a yield, such as equities. The most-active U.S. gold futures for February delivery settled at $1,060.2 per ounce on Thursday, almost flat compared with Wednesday’s close of $1,059.8 and close to six-year lows of $1,046 per ounce earlier in December. Spot gold was down 0.2% at $1,061.4 an ounce at 1:57 p.m. EDT, during the last trading session of the year. Volumes were thin ahead of the New Year holiday on Friday.

“The key factor for gold remains the strong dollar and that ultimately trumps all other issues including the economy and the geopolitics,” said Ross Norman, CEO of bullion broker Sharps Pixley. The dollar was on track for a 9% gain this year against a basket of major currencies, making dollar-denominated gold more expensive for holders of other currencies. Other precious metals have also been hit by dollar strength and the gold slump, and were headed for sharp annual declines. The most-active U.S. silver futures settled at $13.803 per ounce on Thursday, down 0.3% from Wednesday and ending the year down 12%. Spot prices were down 0.2% at $13.83 an ounce. Industrial metals platinum and palladium were harder hit, notching up big yearly losses partly due to oversupply from mines and concerns about growth in demand. Platinum futures settled at $893.2 per ounce, down 26% from a year ago, while the most-active palladium futures ended at $562, down 30% on the year.

Copper and zinc -25%, nickel -42%, palladium -30%, platinum -26%.

• Copper Ends Dismal Year on a Low Note (WSJ)

Copper prices fell in London on Thursday ending a dismal year as industrial metals were battered by a toxic mix of oversupply and concern over demand from China. Analysts don’t expect much respite for copper in 2016, with the oversupply expected to continue and the macroeconomic picture still uncertain. Among other factors, commodity prices have been hit by a stronger dollar, and few economists expect the greenback to weaken in any meaningful way. “I think that the bear market is not totally complete,” said Boris Mikanikrezai, an analyst at financial markets research company Fastmarkets. “Although a temporary rally in metal prices is possible over a one-to-three-month horizon, the macro fundamental picture may warrant lower prices.”

On Thursday, the London Metal Exchange’s three-month copper contract was down 0.5% at $4,720.50 a metric ton in midmorning European trade. Other base metals were mixed. Copper has lost about a quarter of its value this year. Among other base metals, nickel has lost 42%, zinc is down 25% while aluminum fell 18% over the year. “In retrospect, 2015 will be considered a year that can be safely forgotten when it comes to copper,” analysts at Aurubis, Europe’s largest copper producer, said in a report.

Worries about the health of the Chinese economy will continue to roil metals markets in 2016, analysts said. The country is the biggest source of global demand for metals, accounting for nearly half of total global zinc consumption, 45% of global copper consumption and 40% of lead production. “It will be another challenging year for China and that will affect metals,” said Xiao Fu, head of commodity markets strategy at BOCI Global Commodities. “Still, we expect the government’s fiscal stimulus package announced this year to provide some support for demand in 2016.”

More to come.

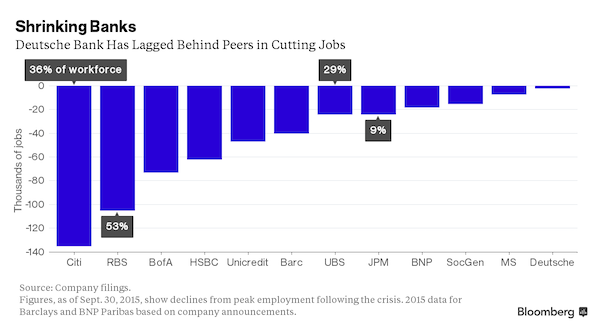

• Half a Million Bank Jobs Have Vanished Since 2008 Crisis (BBG)

Staff reductions at some of the world’s biggest banks are far from over. Deutsche Bank, which has held employment close to its 2010 peak, plans to slash 26,000 positions by 2018, following a trend that began with the financial crisis. Announced cuts in the fourth quarter total at least 47,000, following 52,000 lost jobs in the first nine months of 2015. That would bring the aggregate figure since 2008 to about 600,000. UniCredit says it will eliminate about 18,200 positions. Citigroup, which has reduced its workforce by more than a third, plans to eliminate at least 2,000 more jobs next year.

Not growing slower, but contracting.

• China December Factory Activity Shrinks (Reuters)

China looked set for a soggy start to 2016 after activity in the manufacturing sector contracted for a fifth straight month in December, suggesting the government may have to step up policy support to avert a sharper slowdown. While China’s services sector ended 2015 on a strong note, the economy still looked set to grow at its slowest pace in a quarter of a century despite a raft of policy easing steps, including repeated interest rate cuts, in the past year or so. The world’s second-largest economy faces persistent risks this year as leaders have pledged to push so-called “supply-side reform” to reduce excess factory capacity and high debt levels.

The official manufacturing Purchasing Managers’ Index (PMI) stood at 49.7 in December, in line with expectations of economists polled by Reuters and up only fractionally from November. A reading below 50 suggests a contraction in activity. Still, economists seemed to find some comfort that there were no signs of a sharper deterioration which has been feared by global investors. The slight pick up in the manufacturing PMI “suggests that (economic) growth momentum is stabilizing somewhat … however, the sector is still facing strong headwinds, said Zhou Hao, China economist at Commerzbank in Singapore. “In order to facilitate the destocking and deleveraging process, monetary policy will remain accommodative and the fiscal policy will be more proactive.”

More contracting economic activity.

• Chicago PMI Plummets To Lowest Since 2009 (MarketWatch)

Economic activity in the Midwest contracted at the fastest pace in more than six years in December, according to the Chicago Business Barometer, also known as the Chicago PMI. The index fell to 42.9 from 48.7 in November. Economists had expected it to rise 1.3 points to 50 in the December reading. The index has spent much of the year below the 50 mark that separates expansion from contraction. Order backlogs were the biggest drag in December, dropping 17.2 points to 29.4. That’s the lowest since May 2009 and marked the 11th-straight month in contraction. The last time such a sharp decline was registered was 1951. New orders also sank to the lowest level since May 2009. That’s bad news for activity down the road. Still, 55.1% of survey respondents said they expect stronger demand in 2016 than in 2015.

TBTF banks will still be protected.

• EU’s Trillion Euro Bank Bail-Outs Are Over (Telegraph)

Europe has called an end to the era of mass bank bail-outs as new rules to stop taxpayers from footing the cost of financial rescues come into force. Private sector creditors will be forced to take the hit for bank failures as the EU seeks to end the age of “too big to fail”, which has cost member states more than €1 trillion since 2008. The measures – which will come into force on January 1 and apply to eurozone states – are designed to break the vicious cycle between lenders and governments that bought the single currency to its knees four years ago. Senior bondholders and depositors over €100,000 will be in line to be “bailed-in” if a bank goes bust, a departure from the mass government-funded rescues seen in Ireland, Portugal, Spain and Greece in the wake of the financial crisis.

Brussels’ tough new Bank Recovery and Resolution Directive (BRRD) will require shareholders and bond owners to incur losses of at least 8pc of their total liabilities before receiving official sector aid. Britain will not be subject to the rules. The EU’s commissioner for financial stability, Britain’s Jonathan Hill, said: “No longer will the mistakes of banks have to be borne on shoulders of the many”. Struggling banks in Italy, Portugal and Greece have rushed to recapitalise themselves in a bid to avoid falling foul of the new regime. The rules resemble the bail-in of creditors first seen in the eurozone during Cyprus’ banking crash in 2013, where savers were forced to endure losses as part of the international rescue package.

More than €1.6 trillion (£1.18 trillion) has been pumped into troubled banks by member states between October 2008 and December 2012, according to figures from the European Commission. This amounts to 13pc of the bloc’s total economic output (GDP) and imperiled the public finances of Ireland and Spain. “We now have a system for resolving banks and of paying for resolution so that taxpayers will be protected from having to bail-out banks if they go bust”, said Lord Hill. A new eurozone wide insolvency fund, the Single Resolution Mechanism, will also become operational on January 1. It will build up contributions from the banking industry over the next eight years to use in cases of financial collapse. Europe’s banks have been required to beef up their capital buffers and comply with tough new regulations in the wake of the financial crisis.

The ECB has also assumed direct supervisory responsibility for 129 “systemically” important lenders in a bid to create a fully-fledged banking union in the currency bloc. However, analysts have warned Brussels’ tentative steps towards banking union remain incomplete and could cause more uncertainty for ordinary depositors after January 1. “Taking 8pc losses from creditors has never been tested in reality”, said Nicolas Veron, of think-tank Bruegel. “The first few test cases will be very important . There is the combination of uncertainty over how the SRM will work with ECB, and then additional uncertainty over how creditor losses will work in practice.”

$10 billion in the US alone, before lawsuits?!

• VW Buybacks, Payments For Hard-to-Fix Diesels Will Be Very Costly (GCR)

Hundreds of thousands of diesel-VW owners are waiting to find out how their cars will be updated to meet emissions standards, once modifications are approved by regulators. And Volkswagen Group has clearly been tarnished by the emission-cheating scandal, which affects 11 million cars worldwide. But the costs of the entire affair remain to be tallied; some analysts have said that the $7.1 billion set aside several months ago will not be nearly enough. A Bloomberg article earlier this month cites an estimate by Bloomberg Intelligence that payments and buybacks for owners in the U.S. alone could range from $1.5 billion to $8.9 billion. And those are just the damages or buyback payments that “customers should get for being duped into buying high-polluting vehicles,” it notes.

About 157,000 of the 482,000 affected 2.0-liter TDI diesel cars sold in the U.S. with “defeat device” software are already fitted with Selective Catalytic Reduction after-treatment systems (also known as urea injection). They’re likely to require no more than software updates or perhaps minor hardware tweaks to bring them into compliance. VW then might only have to pay owners for diminished value, plus some penalty. But for 325,000 VW Golfs, Jettas, and Beetles and Audi A3 cars without the SCR systems fitted, the prognosis is much grimmer. Most analysts agree that the cost and complexity of retrofitting a urea tank, a different catalyst, and all the associated plumbing could exceed the value of cars that are now as much as seven years old. Those cars, some suggest, may all have to be bought back and either destroyed or exported.

Using an average price of $15,000, that would cost $4.9 billion alone–before any civil or criminal penalties are levied. On top of the hundreds of thousands of 2.0-liter four-cylinder TDI cars, 85,000 more VW, Audi, and Porsche vehicles were sold in the U.S. with a 3.0-liter V-6 TDI engine. That engine contains several undisclosed software routines, and one of those qualifies as a “defeat device” as well. The admission by Volkswagen that it cheated makes the case close to unique, suggests Paul Hanly, a plaintiffs’ lawyer quoted in the Bloomberg article. It may point to an early settlement, he says, since culpability doesn’t have to be established first. All that’s left is to settle on the costs and penalties. That just applies, however, to more than 450 lawsuits filed by Volkswagen customers in the wake of the mid-September disclosure.

On December 8, those lawsuits were consolidated and will be heard in California, where a high proportion of the affected TDI diesel vehicles were sold. The state also has a large number of VW dealers. Volkswagen had opposed the designation of California, asking that the suits be heard in Detroit instead. That did not happen. On top of the customer lawsuits, which will lead to cash payments and perhaps buybacks, Volkswagen faces criminal investigations in several states. But no settlements can move forward until regulators agree on modifications to the various sets of vehicles to bring them into compliance with tailpipe emission laws. Volkswagen submitted its proposals for those updates to the U.S. EPA and the California Air Resources Board in November.On December 18, CARB extended its own deadline for responding to VW’s proposal until mid-January. That leaves owners in a holding pattern at least until then, and likely far longer.

Andrew Jackson: “One man of courage makes a majority.”

• Keiser Report feat. Gerald Celente: ‘Bankism’, Oil Prices And More (RT)

In this special New Year’s Eve episode of the Keiser Report, Max Keiser and Stacy Herbert talk to trends forecaster Gerald Celente of TrendsResearch.com about the upcoming trends for 2016. They recall that a few years ago, Celente forecasted on the Keiser Report that we would see currency war, trade war and hot war, and they ask whether or not this has come true in 2015. They discuss ‘bankism’, oil prices and US election insanity and what they hold for the future of the global economy.

They should have devised a template long ago. They didn’t because the more chaos the more calls for more union.

• In Europe, 2016 Will Be The Year Of Lawsuits (Coppola)

2016 is fast approaching, and with it another phase in the EU’s attempts to make creditors pay for failed banks. The European Bank Recovery and Resolution Directive (EBRRD) has been law in all EU countries since January 2015, but up till now the bail-in rules have not been fully implemented. The EBRRD provides bank regulators with four main tools for resolving a failed bank:

• Sale of the failed bank partly or entirely to another entity

• Creation of a “bridge bank” containing the good assets, which would be sold to another entity or floated as an independent business

• Creation of a “bad bank”, or asset management vehicle, which would be gradually wound down over time (to prevent state aid rules being breached, this tool must be used in conjunction with at least one of the other tools)

• Write-down of creditor claims (or conversion to equity) in order of rank.Mergers, “bad banks” and even “bridge” banks are all familiar tools from the financial crisis. But writing down creditor claims or converting them to shares (haircut or bail in) is more controversial. During the financial crisis, creditors – and sometimes even shareholders – were made good at taxpayer expense. But these expensive bailouts have left a very sour taste, and no-one has any appetite for them anymore. These days, creditors are expected to pay. Well, some of them, anyway. In all recent bank failures (apart from Duesseldorfer Hypothekenbank), subordinated debt holders have been bailed in, leaving senior creditors untouched. This sounds straightforward: subordinated debt holders rank junior to senior unsecured bondholders and all depositors, so should expect to lose their investments first in the event of bank insolvency.

However, bailing in subordinated debt holders has proved to be anything but simple. A roll-call of recent bail-ins shows just how difficult it can be:

• In 2013, the UK’s Co-Op Bank attempted to bail in its subordinated debt holders; but the deal failed and the subordinated debt holders took over the bank, to the considerable annoyance of the Co-Op Group (the bank’s owner), which lost the majority of its stake.

• In 2014, Portugal’s Banco Espirito Santo was split in two: subordinated debt holders were left in the residual “bad bank” along with the bank’s impaired assets, while senior and official creditors sailed off into a new entity, the aptly named Novo Banco, along with all the good assets. But the Bank of Portugal now faces lawsuits from disgruntled subordinated debt holders who claim they were never given a chance to provide more capital and rescue the bank themselves, Co-Op Bank style.

• In Austria – and increasingly in Germany too – the tangled web of claims and counterclaims in the Heta mess becomes ever more complex. These days it is not even clear exactly how the claims are ranked. The settlement agreement between Heta and the State of Bavaria in October effectively converted 60% of BayernLB’s subordinated claim into a senior claim, diluting the other senior creditors – many of whom are themselves only “senior” because of deficiency guarantees from the Province of Carinthia, which the Austrian federal government has repeatedly tried (but so far failed) to repudiate.

• In the Netherlands, the government was forced to offer compensation to SNS Reaal subordinated debt holders for its expropriation of their claims.

But why should a few problems with bail-in of subordinated debt holders spoil a good directive? Undeterred, the EU is pressing ahead with the next phase. From January 2016, senior as well as subordinated creditors will be bailed in in the event of bank insolvency. Bail-in of 8% of total liabilities (plus complete wiping of equity, of course) will be required before state aid can be granted.

Home › Forums › Debt Rattle New Year’s Day 2016