David Myers Theatre on 9th Street. Washington, DC July 1939

I still don’t fully get it. Was Flynn set up? Hard to believe he didn’t know his calls would be recorded and transcribed. He ran US -military- intelligence for a number of years, for pete’s sake. How could he not have known?

• Top Trump Aide Flynn Resigns Over Russia Contacts (AFP)

Donald Trump’s national security advisor Michael Flynn resigned amid controversy over his contacts with the Russian government, a stunning first departure from the new president’s inner circle less than a month after his inauguration. The White House said Trump had accepted Flynn’s resignation amid allegations the retired three star general discussed US sanctions strategy with Russia’s ambassador Sergey Kislyak before taking office. Flynn – who once headed US military intelligence – insisted he was honored to have served the American people in such a “distinguished” manner. But he admitted that he “inadvertently briefed” the now Vice President Mike Pence with “incomplete information” about his calls with Kislyak. Pence had publicly defended Flynn, saying he did not discuss sanctions, putting his own credibility into question.

“Regarding my phone calls with the Russian Ambassador. I have sincerely apologized to the President and the Vice President, and they have accepted my apology,” read Flynn’s letter, a copy of which was released by the White House. The White House said Trump has named retired lieutenant general Joseph Kellogg, who was serving as a director on the Joint Chiefs of Staff, to be interim national security advisor. Flynn’s resignation so early in an American administration is unprecedented, and comes after details of his calls with the Russian diplomat were made public – upping the pressure on Trump to take action. Several US media outlets in Monday reported that top Trump advisors were warned about Flynn’s contacts with the Russians early this year. Questions will now be raised about who knew about the calls and why Trump did not move earlier to replace Flynn.

The ban is now all but dead. But they’ll throw out another one soon.

• Judge Grants Injunction Against Trump Travel Ban In Virginia (AP)

A federal judge Monday granted a preliminary injunction barring the Trump administration from implementing its travel ban in Virginia, adding another judicial ruling to those already in place challenging the ban’s constitutionality. The ruling is significant from a legal standpoint because U.S. District Judge Leonie Brinkema found that an unconstitutional religious bias is at the heart of the travel ban, and therefore violates First Amendment prohibitions on favoring one religion over another. She said the evidence introduced so far indicates that Virginia’s challenge to the ban will succeed once it proceeds to trial. A federal appeals court in California has already upheld a national temporary restraining order stopping the government from implementing the ban, which is directed at seven Muslim-majority countries.

But the ruling by the 9th Circuit Court of Appeals was rooted more in due process grounds, said Virginia Attorney General Mark Herring, a Democrat who brought the lawsuit against Trump in Virginia. “Judge Brinkema’s ruling gets right to the heart of our First Amendment … claim,” Herring said in a conference call Monday night. In her 22-page ruling, Brinkema writes that Trump’s promises during the campaign to implement what came to be known as a “Muslim ban” provide evidence that the current executive order unconstitutionally targets Muslims. “The president himself acknowledged the conceptual link between a Muslim ban and the EO (executive order),” Brinkema wrote. She also cited news accounts that Trump adviser Rudy Giuliani said the executive order is an effort to find a legal way for Trump to be able to impose his Muslim ban. Herring said that “the overwhelming evidence shows that this ban was conceived in religious bigotry.”

“The creeping tide of kleptocracy will be appeased at every juncture.”

• Is Trump the New Boris Yeltsin? (Max Keiser)

The hope that Trump would take on Wall Street crooks is dead. It was a long shot to begin with but it’s now clear that his level of financial illiteracy and corruption, a hallmark of Obama’s Presidency, is on par, or perhaps even exceeds Obama’s. What we see shaping up in the first few weeks of Trump’s Presidency is his emergence as the new Boris Yeltsin, the puppet idiot installed by America’s neo-cons and Wall St. bankers after the Soviet Union collapsed to drown the country in debt and deceit. Yeltsin was a drunk clown who gave away the country to oligarchs, who turned the country into a kleptocracy – all happening under the laughing approval of President Bill Clinton. Today Trump fills the Yeltsin role in American politics. As Wall St. laughs, Trump begins the process of giving away (read: privatizing) America’s assets to be owned by our new ruling kleptocracy.

Inflation is coming…But not because wages go up, but because price gouging and monopoly pricing starts to dominate our everyday lives with no cheap substitutes coming from overseas due to an increasing global level of distrust and illiquidity among trading partners. Leveraged buyouts fueled by bailouts and free money from the central bankers will continue to kill competition in America. Media, energy, pharmaceutical, finance and agriculture will all be controlled by impregnable monopolies (and Warren Buffett). It’s a pitiful sham and a godawful shame – a situation where Trump’s supporters will, in the not too distant future, turn on him after they’ve had their illusions shattered – but will it be too late? The creeping tide of kleptocracy will be appeased at every juncture. The vanishing middle class will cling to their guns and bibles – hoping for a miracle. They simply will not be able to believe that they could have been so wrong. The triumph of the will.

The always colorful language of Albert Edwards.

• Bond Traders Fear Yellen Is Planning A ‘St. Valentine’s Day Massacre’ (MW)

Is Federal Reserve Chairwoman Janet Yellen capable of conducting a bond-market bloodbath? That’s what some on Wall Street are wondering. Albert Edwards, market strategist at Société Générale and noted permabear, expects Yellen, who is set to deliver semiannual testimony to the Senate Banking Committee on Tuesday, will trigger a steep bond selloff by talking up the possibility that the central bank will raise interest rates in March. In a note, he refers to the possibility as “The St. Valentine’s Day Massacre,” a homage to the 1929 gangland murder of seven men in a garage in the Lincoln Park neighborhood on Chicago’s North Side. The killings were allegedly planned by famed mobster Al Capone, who was trying to wrest power away from Chicago’s Irish gangsters.

Edwards isn’t the only one who expects Yellen to remind investors that the central bank could raise interest rates at its next meeting for what would be the third time in a decade. “The market is bracing for the possibility that Yellen will talk up the chances of a rate increase in March,” said Guy LeBas, chief fixed income strategist at Janney. Treasury yields, which move inversely to prices, are on track to rise for the third straight day, a selloff that has largely been driven by these concerns, LeBas said. The yield on the 10-year Treasury note rose 3.6 basis points to 2.447%. But a March hike is still viewed as far from likely. Although the central bank back projected back in December that it would raise interest rates three times in 2017, investors have remained skeptical—probably because they’ve been burned by the Fed before.

If Brainard leaves too, that makes five seats to fill with Yellen gone early next year.

• Yellen Outlook ‘Irrelevant’ Because Trump Will Reshape Fed (CNBC)

With at least three vacancies expected on the Federal Reserve’s Board of Governors this year, the central bank may not be exempt from a Trump-led shakeup, strategist Mark Grant told CNBC on Monday. “The Fed of today is not going to be the Fed of tomorrow,” the chief strategist at Hilltop Securities told “Squawk Box.” Grant, who accurately predicted the Brexit vote and Donald Trump’s victory, said the president and Treasury Secretary nominee Steven Mnuchin will take advantage of filling key vacancies on the Fed board to further their agenda. Grant spoke a day ahead of Fed Chair Janet’s Yellen’s semiannual monetary report to the Senate. The Fed has said it expect to raise interest rates three times this year.

“I think what the Fed says at this point is, for all practical purposes, irrelevant, because Mr. Trump is going to be able to appoint three members of the Fed,” Grant said. “I think they’re going to be business people and the days of an academic, economist Fed are going to be over.” Removing academics from the Fed’s board remains a point of contention, but Grant said the Trump administration is likely to do so with the economic landscape and policy goals in mind. “I also believe that Trump and company, as I call them, know as they put in the infrastructure or the military expansion that there’s going to be a balance to the balance sheet, and … that the new people on the Fed are going to keep interest rates low,” Grant said. “So all this talk of a three interest rate or four interest rate hike, in my opinion, is baloney.”

On Friday, Fed Governor Daniel Tarullo announced plans to leave the board in April, creating a third vacancy. Danielle DiMartino Booth, author of “Fed Up: An Insider’s Take on Why the Federal Reserve Is Bad for America,” said that there is a high probability that board member Lael Brainard will also leave, creating yet another vacancy. She said Trump’s bold spending plan may require low interest rates (and, in turn, a more dovish Fed), but she wondered about whom the president would appoint to the board. “It’s really going to come down to whether or not he’s got the gumption to totally change the complexion of the Federal Reserve board, or if he steps back and says, ‘You know what, I’ve got to finance all this stuff, so I’m going to put more doves in.’ These are hard decisions,” she said.

Fed insider Danielle DiMartino Booth’s new book Fed Up is here.

• The Fed Is Bad For America – But Getting Rid Of It Isn’t The Answer (DDMB)

On September 20, 2005, Mark Olson did something ordinary that’s since proved to be extraordinary. Never heard of him? You’re not alone. Nevertheless, the banking expert had the gumption to lob a dissenting vote in his capacity as a governor on the Federal Reserve Board. He joined the estimable company of Edward “Ned” Gramlich, a fellow governor who dissented at the September 2002 Federal Open Market Committee meeting. Gramlich is best known for sounding an early warning on the subprime crisis, and being resolutely dismissed by Alan Greenspan. The two gentlemen represent central banking’s answer to the “Last of the Mohicans,” the sole two dissents that have been recorded by governors since 1995. And that’s a problem. At last check, ‘No” was not a four-letter word.

It’s no longer a secret that an abundance of anger is churning among many working men and women who feel they’ve been excluded by the current economic recovery and the longest span of job creation in postwar history. The funny thing about a sense of abandonment is that more often than not, anger follows. What too few Americans appreciate is how directly the inability to say “no” at the Fed has determined their station in life. But that’s just the case. The Fed directly impacts a slew of the most important decisions we make — the values we instill in our children, the things we buy and how they are financed and how we best prepare for what follows after a lifetime of laboring in the trenches.

Stop and think for a moment about the first time you discovered the miracle of compounding interest, that first bank statement that proved savings does pay. Can your children experience that same sensation? What about the roof over your head and the car you drive? Can you afford the payments or did you stretch to buy more than you could afford, out of sheer necessity? What about your mom and dad’s retirements? Do they say their prayers that the stock market will hang in there and that the safety of their bond holdings will protect them if that’s not the case? All of these dysfunctional dynamics lay at the feet of an academic-led Fed being hellbent on launching unconventional monetary policy with the false prerequisite that interest rates had to be zero before quantitative easing (QE) could be deployed.

“The Republican Party is Norma Desmond’s house in Sunset Boulevard, starring Donald Trump as Max the Butler, working extra-hard to keep the illusions of yesteryear going.”

• Made For Each Other (Jim Kunstler)

Don’t be fooled by the idiotic exertions of the Red team and the Blue team. They’re just playing a game of “Capture the Flag” on the deck of the Titanic. The ship is the techno-industrial economy. It’s going down because it has taken on too much water (debt), and the bilge pump (the oil industry) is losing its mojo. Neither faction understands what is happening, though they each have an elaborate delusional narrative to spin in the absence of any credible plan for adapting the life of our nation to the precipitating realities. The Blues and Reds are mirrors of each other’s illusions, and rage follows when illusions die, so watch out. Both factions are ready to blow up the country before they come to terms with what is coming down.

What’s coming down is the fruit of the gross mismanagement of our society since it became clear in the 1970s that we couldn’t keep living the way we do indefinitely — that is, in a 24/7 blue-light-special demolition derby. It’s amazing what you can accomplish with accounting fraud, but in the end it is an affront to reality, and reality has a way of dealing with punks like us. Reality has a magic trick of its own: it can make the mirage of false prosperity evaporate. That’s exactly what’s going to happen and it will happen because finance is the least grounded, most abstract, of the many systems we depend on. It runs on the sheer faith that parties can trust each other to meet obligations. When that conceit crumbles, and banks can’t trust other banks, credit relations seize up, money vanishes, and stuff stops working.

You can’t get any cash out of the ATM. The trucker with a load of avocados won’t make delivery to the supermarket because he knows he won’t be paid. The avocado grower will have to watch the rest of his crop rot. The supermarket shelves empty out. And you won’t have any guacamole. There are too many fault lines in the mighty edifice of our accounting fraud for the global banking system to keep limping along, to keep pretending it can meet its obligations. These fault lines run through the bond markets, the stock markets, the banks themselves at all levels, the government offices that pretend to regulate spending, the offices that affect to report economic data, the offices that neglect to regulate criminal misconduct, the corporate boards and C-suites, the insurance companies, the pension funds, the guarantors of mortgages, car loans, and college loans, and the ratings agencies.

The pervasive accounting fraud bleeds a criminal ethic into formerly legitimate enterprises like medicine and higher education, which become mere rackets, extracting maximum profits while skimping on delivery of the goods. All this is going to overwhelm Trump soon, and he will flounder trying to deal with a gargantuan mess. It will surely derail his wish to make America great again — a la 1962, with factories humming, and highways yet to build, and adventures in outer space, and a comforting sense of superiority over all the sad old battered empires abroad. I maintain it could get so bad so fast that Trump will be removed by a cadre of generals and intelligence officers who can’t stand to watch someone acting like Captain Queeg in the pilot house.

Ann Pettifor’s new book is out too.

• Democracies Must Reclaim Power Over The Production Of Money (Pettifor)

Today, the international monetary system is run by the equivalent of Goethe’s Sorcerer’s Apprentice. In the absence of the equivalent of the Sorcerer – regulatory democracy – financial risk-takers and fraudsters have, since 1971, periodically crashed the global economy and trashed the lives of millions of people. And let’s be clear: there is no such thing as effective global regulation. Ask the Bitcoiners – that is why they operate in the ‘dark web’. The question is this: who should control our socially constructed, publicly-backed financial institutions and relationships? Private, unaccountable, rent-seeking authority? Or public, democratic, regulatory authority? Policy and regulation requires boundaries. Pensions policy, criminal justice policies, taxation policies, policies for the protection of intellectual property – all require boundaries.

Finance capital abhors boundaries. Like the Sorcerer’s Apprentice, global financiers want to be free to use the magic of money creation to flood the global economy with ‘easy’ (if dear) money, and just as frequently to starve economies of any affordable finance. And they want to have ‘the freedom’ to do that in the absence of the Sorcerer – regulatory democracy. If we want to strengthen democracy, then we must subordinate bankers to their role as servants of the economy. Capital control over both inflows and outflows, is, and will always be a vital tool for doing so. In other words, if we really want to ‘take back control’ we will have to bring offshore capital back onshore. That is the only way to restore order to the domestic economy, but also to the global economy.

Second, monetary relationships must be carefully managed – by public, not private authority. Loans must primarily be deployed for productive employment and income-generating activity. Speculation leads to capital gains that can rise exponentially. But speculation can also lead to catastrophic losses. Loans for rent-seeking and speculation, gambling or betting, must be made inadmissible. Third, money lent must not be burdened by high, unpayable real rates of interest. Rates of interest for loans across the spectrum of lending – short- and long-term, in real terms, safe and risky – must, again, be managed by public, not private authority if they are to be sustainable and repayable, and if debt is not going to lead to systemic failure. Keynes explained how that could be done with his Liquidity Preference Theory, still profoundly relevant for policy-makers, & largely ignored by the economics profession.

Remember: there can be no inflation without consumer spending going up. Prices may rise for other reasons, but that’s not the same.

• China Factory Prices Surge Most Since 2011, Boosting Reflation (BBG)

China’s producer prices increased the most since 2011, with the world’s biggest exporter further lifting the outlook for global inflation. Producer price index rose 6.9% in January from a year earlier, compared with a median estimate of 6.5% in a Bloomberg survey and a 5.5% December gain. Consumer-price index climbed 2.5%, boosted by the week-long Lunar New Year holiday beginning in January this year, versus a 2.4% rise forecast by analysts. Producer prices for mining products surged 31% year-on-year while those for raw materials climbed 12.9%, the National Bureau of Statistics said Tuesday. China is again exporting inflation as factories increase prices after emerging from years of deflation. That fresh strength may moderate in coming months as year-ago comparisons gradually rise and Donald Trump’s policies add uncertainties to the global demand outlook.

Continued pressure for raw materials is forcing companies to increase prices, according to Tao Dong at Credit Suisse in Hong Kong. “Without strong demand, producers have limited space for price hikes,” he said. “But I see a wide range of price increases because the cost push is so severe.” Both consumer and producer inflation will peak soon, Julian Evans-Pritchard, an economist at Capital Economics in Singapore, wrote in a report. “Tighter monetary policy, slowing income growth and cooling property prices should keep broader price pressure contained over the medium-term,” he said. “The latest inflation data add to the case for a continued moderate tightening in monetary policy,” Tom Orlik, chief Asia economist at Bloomberg Intelligence in Beijing, wrote in a report.

“The central bank is likely to continue on that path in the months ahead, as policy makers lean against excess leverage, yuan weakness and capital outflows, and nascent inflationary pressure.” “We haven’t seen significant pass-through effect from PPI to CPI inflation yet, suggesting that the strong rebound in PPI inflation is a reflection of proactive fiscal policies,” Zhou Hao, an economist at Commerzbank in Singapore, wrote in a report. With the Communist Party Congress later this year, “local governments are keen to deliver decent growth figures. Against this backdrop, the infrastructure investment pipeline will remain solid.”

It’s almost 2 years ago that I wrote Russia’s Central Bank Governor Is Way Smarter Than Ours. This is a pretty crazy story. Russian banking appears to take place in some kind of black hole, complete with event horizons.

• Putin’s Central Banker Is on a Tear (BBG)

In Russia, Peresvet Bank had an edge no other big private financial institution could match. Its largest shareholder was the powerful Russian Orthodox Church. In a 2015 pitch to investors, Peresvet said the backing of the church and the bank s other big owner, Russia’s Chamber of Commerce and Industry, gave it a quasi-sovereign status. For more than two decades, big state companies stashed their cash with the bank, whose ponderous full name Joint Stock Commercial Bank for Charity and Spiritual Development of Fatherland suggested its grand standing. Even so, it took less than a month last fall for the bank, one of Russia’s 50 largest, to come undone and be taken over by the central bank. Peresvet was just the latest casualty in a financial purge presided over by Central Bank chief Elvira Nabiullina, a bookish economist who’s a favorite of Vladimir Putin.

The regulator closed almost 100 banks in 2016, and in a cleanup with few precedents, Nabiullina has shut almost 300 over the past three years. This may be only the beginning. There are about 600 banks left across the world’s largest country, but Fitch Ratings analyst Alexander Danilov, adjusting for population, calculates that as an emerging market Russia would be fine with about 1 in 10 of those. A warning from Fitch signaled Peresvet’s fall: Almost a tenth of its loans were to companies seemingly without real businesses. Then Russian media reported that the chief executive officer, Alexander Shvets, had disappeared. The bank issued denials and publicized positive comments from other analysts. But within days, as depositors clamored for their cash, the bank said it was “temporarily” limiting withdrawals. The regulator took control of the lender four days later.

As of late January the central bank was still trying to determine the scale of Peresvet’s financial woes. Nabiullina, 53, has emerged as one of Putin’s most influential economic advisers following a low-key government career that began in the 1990s, before the Russian leader’s rise to power. Soft-spoken and unassuming, she runs what in Russia is called a “megaregulator.” When it comes to the economics behind Putin’s overarching goal of restoring Russia’s place in the world, there’s no one more influential. As central bank governor, she’s in charge of a banking system whose weak links are an economic burden, driving up the cost of financing so badly needed in the face of stagnant growth. She’s also the chief guardian of Russia’s foreign currency reserves. Those holdings are more than just a tool of monetary policy; according to several senior officials, Putin views them as a vital safeguard of the country’s sovereignty. [..]

The eurozone’s core problem: as soon as harder economic times come, the poorer countries are hit hardest. Solution: a transfer union like the US. But that will never be accepted in the EU, because it means giving up more sovereignty.

From Finland’s EuroThinkTank, h/t Mish

• The Euro May Already Be Lost (ETT)

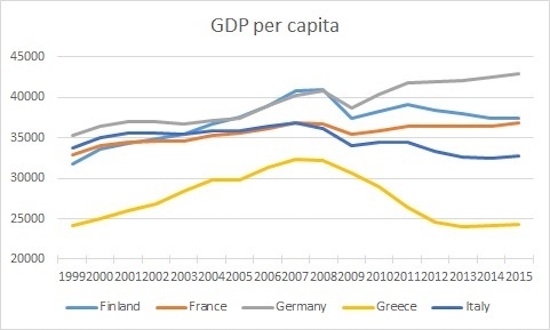

The 1st of January 2017 marked the 18th anniversary of the European common currency, the euro. Despite its success from 1999 to 2007, after 2008 the euro has become a burden for many of its members. For example, living standards in Italy and Greece are below the levels when they joined the euro. Finland is the only Nordic country using the euro and it is also the only Nordic country which has not yet recovered from the financial crash of 2008. There have been many proposals on how to fix the euro and the EMU, but they are politically unpopular and unrealistic. In this blog-entry, we will argue that the euro will almost surely fail; we just do not know the exact timing of its demise. The problem of the euro can be visualized in the development of the GDP per capita.

Germany has been successful in the Eurozone, while Greece and Italy have not. France is not doing well either. The jury is still out for Finland. The different growth paths are a symptom of a general problem that has haunted currency unions for centuries. Competitiveness and productivity develop at a different pace in different countries. Over time, this leads to large competitiveness differences among the members of a currency union. These differences do not usually pose a problem during economic booms because strengthening aggregate demand supports ailing fields of production. However, when a currency union faces an economic downturn or a crisis, falling aggregate demand hits less competitive industries and countries hard and the financing costs of less competitive countries jump. This is an asymmetric shock.

The detrimental effects of asymmetric shocks can be mitigated by transferring funds from prosperous to declining member states. When the dollar union of the US threatened to fall apart during the Great Depression, the federal government enacted federal income transfers from prosperous states to aid ailing ones. The federal budget also increased rapidly and, in practice, income transfers became permanent. The no bailout policy of crisis-hit states had already been enacted earlier. According to the ECB, competitiveness of the German economy has improved by around 19.3%, Greece’s competitiveness has improved by around 6.5%, France’s around 3.9%, Finland’s around 1.7% and Italy’s around 0.9% since 1999. Thus, for survival in its present form and size, the Eurozone needs a similar income transfer system, that is, a full political union as in the US.

Meaningless numbers.

• Greece To Exceed Its Primary Surplus Target In 2018 (R.)

Greece will have a primary surplus in the budget of 3.7% of GDP next year, exceeding the target of 3.5% agreed with its euro zone creditors, the European Commission forecast on Monday. The size of next year’s Greek primary surplus, which is the budget balance before debt-servicing costs, is a bone of contention between euro zone governments and the IMF, which believes it will be only 1.5%. A further disagreement between the two lenders to Greece is what surplus Athens will be able to maintain in the years after 2018. The higher the surplus and the longer it is kept the less is the need for any further debt relief to Greece.

The IMF insists Greek debt, which the Commission forecast on Monday would fall to 177.2% of GDP this year from 179.7% in 2016 and then decline again to 170.6% in 2018, is unsustainably high and that Greece must get debt relief. Germany and several other euro zone countries say that, if Greece does all the agreed reforms, then debt relief will not be necessary. The Commission forecast that Greek investment would triple to 12% of GDP this year and rise further to 14.2% of GDP next year as the economy expands 2.7% in 2017 and 3.1% in 2018 after years of recession. It also forecast Greek unemployment would fall to 22% of the workforce this year from 23.4% last year and decline further to 20.3% in 2018.

If all else fails, sell your soul.

• Greece Lines Up Rothchild For Debt Advisory Role As Bankruptcy Looms (IW)

Greece is reportedly planning to hire Rothschild as its debt adviser, replacing current adviser Lazard in the role, as it attempts to end a long-running stand off with creditors. According to the Financial Times, government officials in Greece hope to finalise the appointment before a gathering of euro-area finance ministers on 20 February. Unless Greece receives fresh funds it will not be able to make €7bn of debt payments due this July, including €2.1bn to private sector creditors. In the role, Rothschild will reportedly advise the country on negotiations with creditors, potential inclusion in the European Central Bank’s bond-buying programme, and the sale of Greek government bonds.

The deal would replace the Greek government’s current deal with Lazard, which guided the country through its original bailout in 2012. According to the FT, out of Greece’s €323bn of outstanding government debt just €36bn is owned by private investors who hold Greek bonds, while the rest is owned by sector creditors. Last week, yields on two-year Greek bonds rose to their highest level since June last year after the IMF and the EU failed to reach an agreement on how to lend the €7bn required by the country to avoid bankruptcy. The IMF refused to sign up to the aid programme unless the EU grants further debt relief to Greece. However, the head of the eurozone’s €500bn rescue fund has rejected this demand.

Power to you, Chelsea.

• To Those Who Kept Me Alive All These Years: Thank You (Chelsea Manning)

To those who have kept me alive for the past 6 years: minutes after President Obama announced the commutation of my sentence, the prison quickly moved me out of general population and into the restrictive housing unit where I am now held. I know that we are now physically separated, but we will never be apart and we are not alone. Recently, one of you asked me “Will you remember me?” I will remember you. How could I possibly forget? You taught me lessons I would have never learned otherwise. When I was afraid, you taught me how to keep going. When I was lost, you showed me the way. When I was numb, you taught me how to feel. When I was angry, you taught me how to chill out. When I was hateful, you taught me how to be compassionate. When I was distant, you taught me how to be close. When I was selfish, you taught me how to share.

Sometimes, it took me a while to learn many things. Other times, I would forget, and you would remind me. We were friends in a way few will ever understand. There was no room to be superficial. Instead, we bared it all. We could hide from our families and from the world outside, but we could never hide from each other. We argued, we bickered and we fought with each other. Sometimes, over absolutely nothing. But, we were always a family. We were always united. When the prison tried to break one of us, we all stood up. We looked out for each other. When they tried to divide us, and systematically discriminated against us, we embraced our diversity and pushed back. But, I also learned from all of you when to pick my battles. I grew up and grew connected because of the community you provided.

I’ll get back to this soon. It’s good to see others address this issue too.

• Lesbos Doctors Accuse NGOs Of Failing To Care For Refugees (K.)

State hospital doctors on the eastern Aegean island of Lesvos, which has been hard particularly hit by the refugee crisis, have complained that nongovernmental organizations receiving European Union funding to help migrants are not doing enough, resulting in them being forced to bear an excessive burden. In a statement released on Monday, the island’s union of state hospital doctors said the two refugee camps at Moria and Kara Tepe do not have any pediatricians, meaning that all sick children from the camps must be treated at local hospitals, which are seriously understaffed. Noting that the NGOs “get paid handsomely” by the EU to help refugees, the union claimed they had “totally failed to provide humane conditions for the refugees.” Several human rights groups have complained about conditions at Greek refugee camps, particularly Moria and Elliniko, in southern Athens.

Home › Forums › Debt Rattle Valentine’s Day 2017