Ben Shahn Quick lunch stand in Plain City, Ohio 1938

“Policies that could prevent the crisis [..] include reinstatement of the Glass-Steagall separation of investment and commercial banking, breaking up big banks, banning most derivatives, and tougher law enforcement of bank wrongdoing.”

• Donald Trump Can’t Stop The Next Financial Crisis – Jim Rickards (MW)

James Rickards sees threats in many places. In his latest book, “The Road to Ruin: The Global Elites’ Secret Plan for the Next Financial Crisis,” he paints a picture of how that crisis will unfold. He argues that rather than pumping the financial system with liquidity, as happened in 2008, “elites” will freeze the financial plumbing until the crisis has passed. That means banks will close, as will exchanges. Money-market funds will be inaccessible. Forget trying to get your hands on money. Rickards, who was the principal negotiator of the 1998 bailout of Long-Term Capital Management as the hedge fund’s general counsel, calls this new world “ice-nine,” after a fictitious substance in Kurt Vonnegut’s “Cat’s Cradle.” Freezing customer funds in bank accounts is what happened in Cyprus is 2012 and Greece in 2015, he says. In the U.S., the Securities and Exchange Commission adopted a rule in 2014 that lets money-market funds suspend redemptions.

MarketWatch: Why do you believe a financial crisis is coming in 2018, and what do you see as the likely triggers? James Rickards: A financial crisis is certainly coming. In “The Road to Ruin,” I use 2018 as a target date and device because the two prior systemic crises, 1998 and 2008, were 10 years apart. I extended the timeline 10 years into the future from the 2008 crisis to maintain the 10-year tempo, and this is how I arrived at 2018. Yet I make the point in the book that the exact date is unimportant. What is most important is that the crisis is coming and the time to prepare is now. It could happen in 2018, 2019, or it could happen tomorrow. The conditions for collapse are all in place. It’s simply a matter of the right catalyst and array of factors in the critical state. Likely triggers could include a major bank failure, a failure to deliver physical gold, a war, a natural disaster, a cyber–financial attack and many other events. The trigger does not matter. The exact timing does not matter. What matters is that the crisis is inevitable and coming soon. Investors need to prepare.

MW : Is this likely to be on the scale of the 2008 financial crisis? Or what is a better comparison? J.R.: The new crisis will be of unprecedented scale. This is because the system itself is of unprecedented scale and interconnectedness. In complex dynamic systems that reach the critical state, the most catastrophic event that can occur is an exponential function of scale. This means that if you double the system, you do not double the risk; you increase it by a factor of five or 10. Since we have vastly increased the scale of the financial system since 2008, with larger banks, greater concentration of banking assets in fewer institutions, larger derivatives positions, and $70 trillion of new debt, we should expect the next crisis to be much worse than the last. There is no comparison short of wartime exigencies such as 1914. The next crisis will be of unprecedented scale and damage.

MW : On the flip side, what could prevent this crisis? And how do you respond to those who say this is just fear-mongering and a conspiracy theory? What are they missing? J.R.: Policies that could prevent the crisis are spelled out clearly in the book. These include reinstatement of the Glass-Steagall separation of investment and commercial banking, breaking up big banks, banning most derivatives, and tougher law enforcement of bank wrongdoing. The book also explains clearly why the dysfunctions in the system are not a “conspiracy” but the workings of like-minded individuals operating in a closed loop lacking cognitive diversity. I am not a fear-monger; people are already afraid, [and] I’m just trying to shed some light on the situation, which is why readers have responded so positively to the book. The critics do not have a firm grasp of the statistical properties of risk. They are clinging to obsolete equilibrium models instead of embracing more accurate models based on complexity theory and behavioral psychology.

“..the European establishment is simultaneously bombing a country and importing the country’s inhabitants..”

• “Russia Did It” – The Last Stand Of The Neocons (GEFIRA)

By the 2000s, Neocons had taken over the Republican Party in the US and the Labour Party in the UK and could count on allies in Italy (Berlusconi) and Spain (Aznar). In the following decade, Neocon ideology spread virulently, substituting for the failed experiment of military intervention to overthrow non-cooperating governments with covert operations funding and/or arming local groups in Libya, Syria,Tunisia Egypt, Georgia, and Ukraine. Neocon adherents took over the US state department, and their grip on it was strengthened by the appointment of Barack Obama as assistant to Victoria Nuland, Secretary of State for European affairs, wife of Robert Kagan, who is in turn a top Neocon ideologist alongside Paul Wolfowitz. They also created the narrative spread and reinforced by the mainstream media, which expose the alleged crimes of non-cooperating regimes in Syria, Russia and Libya, while ignoring the anti “democratic” behavior by friendly dictatorships such as Saudi Arabia’s kings.

The mission however never changed. What changed is the mood of Western citizens about the government changes and state-building projects of the Western leadership; as the economic and human cost grew endlessly, the Western public opinion has become fed up with interventionism around the world. The British Labour party was the first to face the malcontents: Blairites are being ousted in favour of anti-NATO, sworn pacifist Jeremy Corbyn. Then Donald Trump won the US election with his “America First” i.e. a policy of “non-interventionism and protectionism”, defeating Hillary’s hawkish one, publicly endorsed by Kagan and Wolfowitz; Sarkozy and Juppè were defeated in the primaries in France by Fillon, who is advocating the end of the trade war against big bad Neocon target Russia. The Neocon-backing Western establishment is facing political upheaval all over Europe and the US.

These revolutions are not mere popular movements. Trump’s election is the handing over of power from one influential group to another because a part of the establishment has become fully aware of the problems Europe and the US are facing. After a fourteen-year war on terror in Afghanistan and Iraq the bloodshed spilled over into the streets of Paris and Berlin. The killing of civilians in the streets in Europe was not supposed to happen after the eradication of Al Qaeda and the alleged elimination of its leader Osama Bin Laden. Or should we rather say European insanity is spilling over, as the European establishment is simultaneously bombing a country and importing the country’s inhabitants? What do the Western leadership expect to have on their hands? Meanwhile Russia is reemerging as a more successful international actor.

Echo chambers are us.

• 94% Of All New Jobs Created During Obama Era Were Part-Time Or Contract (IC)

A new study by economists from Harvard and Princeton indicates that 94% of the 10 million new jobs created during the Obama era were temporary positions. The study shows that the jobs were temporary, contract positions, or part-time “gig” jobs in a variety of fields. Female workers suffered most heavily in this economy, as work in traditionally feminine fields, like education and medicine, declined during the era. The research by economists Lawrence Katz of Harvard University and Alan Krueger at Princeton University shows that the proportion of workers throughout the U.S., during the Obama era, who were working in these kinds of temporary jobs, increased from 10.7% of the population to 15.8%.

Krueger, a former chairman of the White House Council of Economic Advisers, was surprised by the finding. The disappearance of conventional full-time work, 9 a.m. to 5 p.m. work, has hit every demographic. “Workers seeking full-time, steady work have lost,” said Krueger. Under Obama, 1 million fewer workers, overall, are working than before the beginning of the Great Recession. The outgoing president believes his administration was a net positive for workers, however. “Since I signed Obamacare into law (in 2010), our businesses have added more than 15 million new jobs,” said Obama, during his farewell press conference last Friday.

It’s going to keep falling no matter what. And regaining some domestic manufacturing capacity is never a bad thing. If you focus of producing essentials, that is.

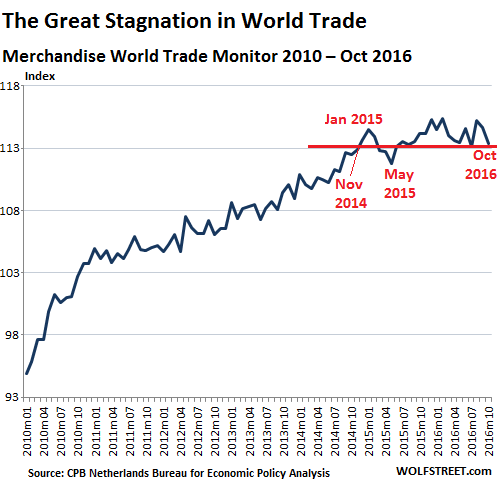

• World Trade Falls to 2014 Level, Trump “Trade War” Might Make it Worse (WS)

“If you get into a trade war with China, sooner or later we’ll have to come to grips with that,” Carl Icahn, now special advisor to President-Elect Trump, told CNBC on Thursday. “I remember the day something like that would really knock the hell out of the market.” A trade war with China surely would be another wall of worry for stocks to climb. Trump’s rhetoric against China, each morsel packaged into 140 characters or less, has already recreated much-needed turbulence [read… Trump Tweets about China, US Businesses Freak out]. “But maybe if you’re going to do it,” Icahn said about the looming trade war with China, “you should get it over with, right?”

This comes after rumors emerged that Trump’s transition team is chewing over the idea to impose import tariffs of up to 10%, “according to multiple sources,” including a “senior Trump transition official,” CNN reported. The idea is to boost US manufacturing. The new tariffs could be imposed by executive order or by Congress as part of broader tax reform legislation. The 10% would be an uptick from the 5% tariff that incoming White House Chief of Staff Reince Priebus had put on the table last week, in “meetings with key Washington players,” two sources “who represent business interests in Washington” told CNN. These tariffs would be in line with Trump’s campaign motto of “America First.” Other countries would, as they always do, retaliate. Hence the term “trade war.”

Countries will be careful not to escalate, but these things can escalate nevertheless, because no one wants to seem weak and back off. Either way, it would pull the rug out from under world trade. But world trade, a reflection of the health of the global goods-producing economy, is already in bad shape. For the past two years, it has been languishing in a condition we now call the Great Stagnation. The CPB Netherlands Bureau for Economic Policy Analysis, a division of the Ministry of Economic Affairs, just released the preliminary data of its Merchandise World Trade Monitor for October. World trade isn’t falling off a cliff, as it had done during the Great Recession, when global supply chains froze up overnight. But since November 2014, it has gone absolutely nowhere:

“Is There A Way Out?” Not for most. And do give the ECB a special place in this: they are responsible for setting one single rate in countries that need completely different rates.

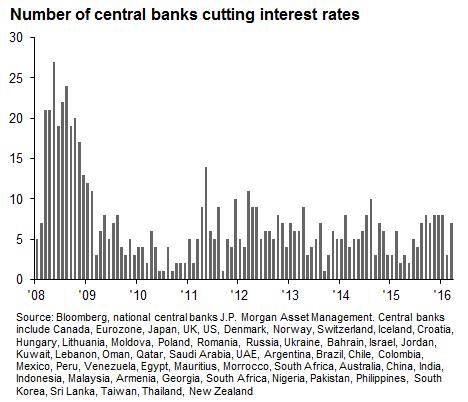

• Central Banks Have Cut Interest Rates 690 Times Since Lehman Brothers (CNBC)

The top 50 central banks around the world have seen a total of 690 interest rate cuts since the collapse of Lehman Brothers in September 2008, according to data from JP Morgan. While this number means one rate cut every three trading days, analysts have warned that central banks may start to run out of ammunition soon. “Essentially these rate cuts came into effect to try and stimulate economic growth and to prop up economies post the financial crisis,” Alex Dryden, global market strategist at JP Morgan Asset Management, told CNBC via email. However, he warned that central banks are running out of room to maneuver.

“The Bank of Japan, for example, own over 45% of the government bond market, over 65% of the domestic ETF market and are a top 10 shareholder in 90% of listed firms. They have also cut rates into negative territory. There isn’t much more they can do.” Markets, however, continue to ride the wave of uncertainty and speculation over whether the world’s central banks will either continue to pump in more and more cash into the economy through bond-buying programs known as QE or conventional ways such as lowering interest rates to stimulate borrowing. But as we delve deeper into this world of ultra-low interest rate and easy monetary policy, there are other areas of the economy that could see a knock-on effect.

This raises a very big question – will the global economy ever exit this low interest rate environment? “No easy way out. The world has changed and the level of neutral interest rates has fallen for most countries,” Jan von Gerich, chief economist at Nordea, told CNBC via email. Gerich further explained that the way inflation is responding to growth seems to have changed, which makes monetary policy considerations harder for central bankers. “The situation varies a lot, though. The Fed is gradually finding at least a partial way out while it is hard to see the ECB raising rates before the next recession arrives.”

Oh, sweet Jesus: “..allow Italy’s third-largest bank to finally return to operate at full throttle to support the economy..”

• Italian Government Rides To Rescue Of Stricken Bank Monte Dei Paschi (R.)

The Italian government approved a decree on Friday to bail out Monte dei Paschi di Siena after the world’s oldest bank failed to win investor backing for a desperately needed capital increase. Looking to end a protracted banking crisis that has gummed up the economy, Prime Minister Paolo Gentiloni said his Cabinet had authorized a €20 billion fund to help lenders in distress – first and foremost Monte dei Paschi. Within minutes of the late-night Cabinet meeting ending, the country’s third largest lender issued a statement saying it would formally request state aid, opening the way for possibly the biggest Italian bank nationalization in decades. The government has said its long-awaited salvage operation will work within EU rules, meaning some Monte dei Paschi bondholders will be forced to accept losses to ensure the taxpayer does not pick up all of the bill.

However, the government and Monte dei Paschi promised protection for around 40,000 retail savers who had bought the bank’s junior debt. Many of the high street investors say they were unaware of the risks when they purchased the paper. “Today marks an important day for Monte dei Paschi, a day that sees it turn a corner and be able to reassure its depositors,” said Gentiloni, who only took office last week and has made the bank rescue his first priority. [..] The collapse of Monte dei Paschi would have threatened the savings of thousands of Italians and could have had devastated the wider banking sector, which is saddled with €356 billion of bad loans – a third of the euro zone’s total. [..] The government said full details of the rescue plan have yet to be worked out, but it outlined the contours in a statement.

It said the bank’s Tier 1 bonds, which are mostly held by professional investors, would be converted into shares at 75% of their nominal value. Tier 2 bonds, which are mostly in the hands of retail investors, will be converted instead at 100% of their face value. To further insulate small savers from losses, Monte dei Paschi will offer to swap the shares they end up with as a result of the forced conversion with regular bonds and sell the same shares to the state instead. “The rescue will require a (new) business plan that European authorities will need to approve and that will allow Italy’s third-largest bank to finally return to operate at full throttle to support the economy and with the full confidence of its depositors,” said Economy Minister Pier Carlo Padoan.

Where are the indictments?

• Deutsche Bank, Credit Suisse Agree Billion-Dollar Fines With US (CNBC)

Deutsche Bank will be hoping for a fresh start in 2017 after reaching a $7.2 billion deal with U.S. authorities to settle allegations of the mis-selling of mortgage-backed securities (MBS). Germany’s largest lender said on Friday morning it had agreed ‘in principle’ to pay a $3.1 billion civil fine to be supplemented with the payment of $4.1 billion in consumer relief overtime. The announcement of the fine comes amid a raft of banking stories related to the mis-selling of MBS which hit the wires before Friday’s European market open. This included news that U.S. federal prosecutors would sue Britain’s Barclays bank and that Credit Suisse had reached a provisional $5.3 billion deal, meaning the Swiss bank will take a pre-tax charge of about $2 billion.

Of the total amount demanded of Credit Suisse, $2.48 billion would be an immediate fine to settle the claims and an additional $2.8 billion would be paid over five years for consumer relief. Deutsche Bank’s agreement follows months of negotiations with the U.S.’s Department of Justice (DoJ) and ranks as the third-highest penalty imposed to date on a bank to settle claims of mis-sold mortgage-backed instruments. Although the $7.2 billion payment is far from negligible, investors may take some cold comfort from the fact it is less than $16.7 billion that Bank of America was required to stump up in August 2014 and the $9.0 billion charged to JPMorgan Chase in November 2013. Furthermore, of the full amount, only the $3.1 billion civil fine component is required to be imminently delivered in cash.

Again, where are the indictments?

• US Sues Barclays For Alleged Mortgage Securities Fraud (R.)

The U.S. Department of Justice on Thursday sued Barclays for fraud in the sale of mortgage securities in the run-up to the financial crisis. The British bank deceived investors about the quality of loans underlying tens of billions of dollars of mortgage securities between 2005 and 2007, according to the lawsuit, which was filed in U.S. district court in Brooklyn, New York. Loans had been made to borrowers with no ability to repay and were based on inflated home appraisals, the complaint said. Barclays said in a statement that the claims in the lawsuit are “disconnected from the facts” and that it has an obligation to defend against “unreasonable allegations and demands.”

In terms of demands, Barclays was apparently referring to negotiations with the Justice Department to settle the claims without a case being filed. “Barclays will vigorously defend the complaint and seek its dismissal at the earliest opportunity,” the statement said. The bank’s U.S.-traded shares were down 1.7 percent at $11.08 shortly before the close of the market. Barclays is among a number of European banks that have been under investigation for misconduct in the sale of mortgage securities, which contributed to the 2008 financial crisis.

One word: Dollar.

• Why The Chinese Are Still Snapping Up US Commercial Property (CNBC)

Interest in U.S. commercial real estate is perking up, particularly from China, as expectations of pro-growth policies from President-elect Donald Trump spark demand for dollar-denominated assets. “(Investors) are seeing the U.S.commercial real estate marketplace as really standing out on a global basis,” said Hessam Nadji, president and chief executive at commercial real estate firm Marcus and Millichap. “It’s not being overbuilt; it’s been very well balanced in this particular cycle in terms of loans that are not going up, the leverage that was very well balanced. They’re at much lower risk at this stage of recovery than we’ve seen in the past,” he told CNBC’s The Rundown. Concerns over the dollar’s appreciation are also prompting some motivation for capital allocation into the U.S. “particularly because the Chinese economy is slowing” and as the yield profile of commercial real estate is competitive, Nadji added.

We don’t solve our problems, we package them.

• EU Plans To ‘Revitalize’ Complex Financial Products (EUO)

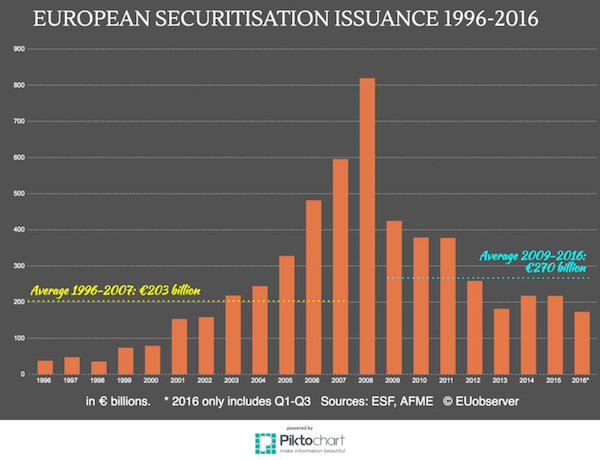

The EU is trying to “revitalise” a market for controversial financial products, but one of the goals appears to already have been achieved without the EU’s help. Securitisation is the packaging of loans, mortgages, or other contractual debts into securities that can then be sold on the market, together with the risk attached to those debts. It had an instrumental role in the financial crisis of 2008, but the European Commission says giving the securitisation market a boost can help the real economy. The commission has not given a target figure of when “revitalisation” will have been achieved, but spoke in a press release of going back to the “pre-crisis average”.

The commission did not want to comment on the record, but one commission official said that if the market would return to average pre-crisis issuance levels, this would generate €100-€150 billion in additional funding for the economy. “This would already be a major achievement for the securitisation markets,” the commission official said. EUobserver looked at how average issuance levels have done so far, and found that more securities have been created through securitisation since the crisis than before the crisis. This website collected data from the Association for Financial Markets in Europe (AFME), a lobby group for the financial service sector, and the Securities Industry and Financial Markets Association, its US-based counterpart.

Taking a very narrow view, the “pre-crisis” years are 1996-2006. The average issuance of securities in Europe was €168 billion. When including 2007, the average was €203 billion. When including 2008 – when the financial crisis was in full swing – the average was €251 billion. Last week, AFME released data for the third quarter of 2016. The first three quarters of 2016 were the best three quarters since 2012. Taking the most recent data into account, the average annual issuance of securitisation since 2009, is €270 billion. Last year the figure was €216 billion. Even when correcting for inflation, the post-crisis period is already better than the pre-crisis period. Converting the averages to today’s prices, the average since 2009 is €282 billion, compared to a 1996-2007 average of €244 billion.

“I think the spying and interference is sort of the nature of our governments.”

• Ron Paul: “We Don’t Have Very Much Room For Condemning Anybody Else” (ZH)

When asked whether all the “Russian hacking” allegations were just a simple “political stunt” or whether a serious investigation needed to be conducted, Ron Paul offered up a startling bit of reality pointing out that America has a long history of interfering with elections and even invading countries “to have our guy in.” We suspect the following response was a bit more truth than Fox Business News expected.

“I think it is politics more than anything else. It’s really is nothing new. It’s like, guess what – somebody might have done A, B, C.” “The very rarely, if ever, compare what we do with election around the world. We are interfering all the time.” “I’m sure the Russians are interfering. But when you lose, you can jump on that and make a big point of it. But I don’t think it made any difference. I think it’s insignificant.” “If you review the history of how many elections we’ve been involved with, how many countries we’ve invaded and how many people we’ve killed to have our guy in, I’ll tell you what – we don’t have very much room for condemning anybody else.” “I think the spying and interference is sort of the nature of our governments. That’s why I’d like to see government much smaller.”

HA!

• Is Obama a Russian Agent? (Dmitry Orlov)

Sometimes a case looks weak because there is no “smoking gun”—no obvious, direct evidence of conspiracy, malfeasance or evil intent—but once you tally up all the evidence it forms a coherent and damning picture. And so it is with the Obama administration vis à vis Russia: by feigning hostile intent it did everything possible to further Russia’s agenda. And although it is always possible to claim that all of Obama’s failures stem from mere incompetence, at some point this claim begins to ring hollow; how can he possibly be so utterly competent… at being incompetent? Perhaps he just used incompetence as a veil to cover his true intent, which was always to bolster Russia while rendering the US maximally irrelevant in world affairs. Let’s examine Obama’s major foreign policy initiatives from this angle.

Perhaps the greatest achievement of his eight years has been the destruction of Libya. Under the false pretense of a humanitarian intervention what was once the most prosperous and stable country in the entire North Africa has been reduced to a rubble-strewn haven for Islamic terrorists and a transit point for economic migrants streaming into the European Union. This had the effect of pushing Russia and China together, prompting them to start voting against the US together as a block in the UN Security Council. In a single blow, Obama assured an important element of his legacy as a Russian agent: no longer will the US be able to further its agenda through this very important international body.

Next, Obama presided over the violent overthrow of the constitutional government in the Ukraine and the installation of an American puppet regime there. When Crimea then voted to rejoin Russia, Obama imposed sanctions on the Russian Federation. These moves may seem like they were designed to hurt Russia, but let’s look at the results instead of the intentions. First, Russia regained control of an important, strategic region. Second, the sanctions and the countersanctions allowed Russia to concentrate on import replacement, building up the domestic economy. This was especially impressive in agriculture, and Russia now earns more export revenue from foodstuffs than from weapons. Third, the severing of economic ties with the Ukraine allowed Russia to eliminate a major economic competitor.

Fourth, over a million Ukrainians decided to move to Russia, either temporarily or permanently, giving Russia a major demographic boost and giving it access to a pool of Russian-speaking skilled labor. Most Ukrainians are barely distinguishable from the general Russian population.) Fifth, whereas before the Ukraine was in a position to extort concessions from Russia by playing games with the natural gas pipelines that lead from Russia to the European Union, now Russia’s hands have been untied, resulting in new pipeline deals with Turkey and Germany. In effect, Russia reaped all the benefits from the Ukrainian stalemate, while the US gained an unsavory, embarrassing dependent.

Worse than smoking.

• Air Pollution Cause Of One In Three Deaths In China (SCMP)

Smog is related to nearly one-third of deaths in China, putting it on a par with smoking as a threat to health, according to an academic paper based on the study of air pollution and mortality data in 74 cities and published in an international journal. The findings by Nanjing University’s School of the Environment, which were published in the November edition of the journal the Science of the Total Environment, provides the latest scientific estimates of the health cost of China’s notorious smog. The latest bout of smog began last Friday, affecting about half a billion people on the mainland, with the severest impact in the last three days. Previous research work have found equally alarming results about the country’s toxic air.

The International Energy Agency published its first study on air pollution in June and estimated that severe air pollution has shortened life expectancy in China by an average 25 months. An academic paper co-authored by researchers from MIT in the US, Tsinghua University and Peking University in China, plus the Hebrew University of Jerusalem in 2013 concluded that bad air has cut life expectancy by an average of 5.5 years in the north of the country. There are so far no concrete or widely agreed estimates on the impact of air pollution on health in China partly because it is scientifically complicated to measure and also because there is little historical precedent for prolonged exposure to such high levels of air pollution.

The six researchers from Nanjing University said they conducted the study because air pollution was the “most severe and worrisome environmental problem in China”, but knowledge of its health effects was insufficient. When they looked into 3.03 million deaths in 2013 in 74 cities in the Beijing-Tianjin-Hebei region and the Yangtze River Delta and Pearl River Delta, they found 31.8 per cent could be linked to PM 2.5 pollution – the tiny smog particles most hazardous to health.

Yeah, it’s bitter. Still, as I said yesterday on FB: “Right up the alley of my -repeat- article and appeal yesterday. Only, the Guardian itself runs a fund now. So it has reason to publish this. The problem: the paper supports 3 NGOs, all British. As if they know better than Greeks what to do in Greece. It’s a broken record problem. Too much money gets wasted on hubris and 1001 -repeat- preventable fuck-ups.”

• 1000s Of Refugees Left In Greek Cold, UN And EU Accused Of Mismanagement (G.)

The UN refugee agency and the EU’s aid department have been accused by other aid groups of mismanaging a multimillion-pound fund earmarked for the most vulnerable refugees in Europe, leaving thousands sleeping in freezing conditions in Greece. The Greek government, which has ultimate jurisdiction over camp activities, has also been criticised for failing to use nearly €90m (£75m) of separate EU funding to adequately improve conditions at the camps before the onset of winter. No single actor has overall control of all funding and management decisions in the camps, allowing most parties to distance themselves from blame.

The EU aid department, known as Echo, has given UNHCR more than €14m since April to help prepare roughly 50 refugee camps for the winter in Greece, where an estimated 50,000 mainly Syrian refugees have been stranded since the adoption of new European migration policies in March. A further €24m has been given to UNHCR for other projects. Both organisations stand accused by other aid groups of squandering this money, after failing to properly “winterise” or evacuate dozens of camps before snow fell in Greece earlier in December. In addition to providing warmer bedding and clothes, UNHCR was expected to use this money to move people from tents to heated containers or formal housing; heat warehouses where other refugees are living; provide a consistent supply of hot water; and install insulated flooring for anyone still left in tents.

Months after the funds were dispersed, roughly half of those living in camps had yet to be transferred to formal housing by the onset of winter. Of the 45 camps that were still active at the start of the month, the Guardian visited or was made aware of at least 15 camps that had yet to be properly adapted by the time snow fell in northern Greece at the start of December. UNHCR admitted it was itself aware of only eight camps where all the residents have been moved out of tents and into prefabricated containers.

Because of all that goes wrong in the NGO structure, we support this:

• The Automatic Earth in Greece: Big Dreams for 2017 (Automatic Earth)

Both Konstantinos and myself -and all the other volunteers at O Allos Anthropos- want to thank you so much for all the help you’ve given over the past year -and in 2015-. We’re around $30,000 for 2016 alone, another $5000 since my last article 4 weeks ago. I swear, for as long as I live, this will never cease to amaze me. And then of course what happens is people start thinking and dreaming about what more they can do for those in peril. Wouldn’t you know…

A Merry Christmas to all of you, to all of us. Very Merry. God bless us, every one. Thank you for everything.

If I may make a last suggestion, please forward this ‘dream’ to anyone you know -and even those you don’t-, by mail, Twitter, Facebook, Instagram, word of mouth, any which way you can think of. Go to your local mayor or town council, suggest they can help and get -loudly- recognized for it. There may be a dream involved for 2017, but that was our notion a year ago as well, and look what we’ve achieved a year later: it is very real indeed. And anyone, everyone can become part of that reality for just a few bucks. If the institutions won’t do it, perhaps the people themselves should. That doesn’t even sound all that crazy or farfetched. There’s a lot of us.

Konstantinos Polychronopoulos on Lesbos Dec 2015