Vincent van Gogh Red Vineyards at Arles 1888

Jack Posobiec: Trump sent $1800 stimulus out, Biden sent $1400 but if you look closely you may start to notice the media being slightly biased about this story.

Kevin Gosztola: Jobless benefits were $600/week for 4 months in the COVID-19 relief that passed under Trump in March 2020. Biden and Senate Democrats are cutting jobless benefits for citizens in crisis to $300/week for same period—half of what passed in GOP-controlled Senate.

Already, people will get $1,400 checks, while the rescue will cost them some $5,700 each.

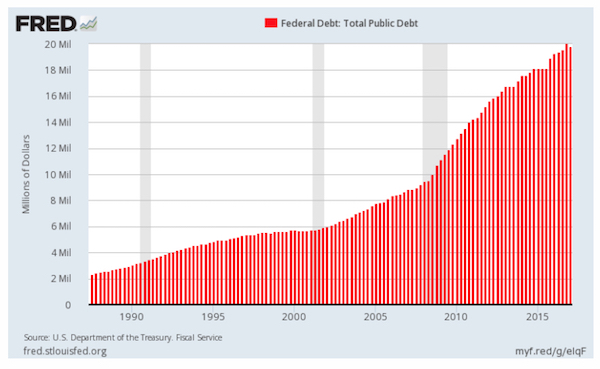

• American Rescue Plan Could Set Stage for $4 Trillion of Debt (CRFB)

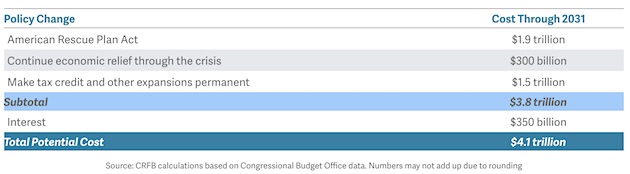

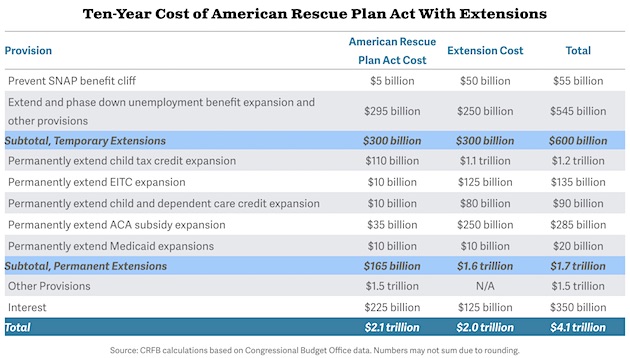

The American Rescue Plan Act is estimated to cost over $1.9 trillion through 2031, but the ultimate price tag could be twice as high if some of the policies in the bill are extended beyond their current expiration dates. The bill includes several extensions of tax credits that supporters have previously proposed on a permanent basis and several temporary economic relief measures that are slated to end before the economy has fully recovered. If the tax credits were made permanent and these relief measures were extended for the duration of the crisis, it would raise the total cost of the bill to $3.8 trillion through 2031, or $4.1 trillion with interest.

Several measures in the $1.9 trillion American Rescue Plan Act that provide temporary relief are likely to be extended past their expiration dates. Most significantly, expanded unemployment benefits would expire at the end of August (though that may soon be changed to September), after which all unemployed workers would lose the benefit supplement and many would lose benefits entirely. In addition, a 15 percent increase in Supplemental Nutrition Assistance Program (SNAP) benefits would end in September, after which benefits would immediately snap back to their previous level. Other smaller relief efforts also end abruptly. Extensions of these policies are likely in our view. While the actual cost would depend on the length and nature of those extensions, we believe a reasonable extension and phase-out scenario could cost roughly $300 billion.

More substantially, the American Rescue Plan Act includes one- or two-year versions of several longstanding policy priorities of President Biden’s or Congressional Democrats’. It includes over $100 billion for a one-year expansion of the Child Tax Credit (CTC), which increases the credit from $2,000 to $3,000 (or $3,600 for children under age 6) and makes it fully refundable. The bill also includes a $15 billion, one-year expansion of the Earned Income Tax Credit (EITC) for childless workers that many have been seeking for years, and an $8 billion expansion of the Child and Dependent Care Tax Credit (CDCTC), which closely matches President Biden’s campaign proposal to increase the maximum credit from $2,100 to $8,000 and from covering 35 percent of expenses to 50 percent of expenses. Finally, the legislation includes a $35 billion, 2-year increase in Affordable Care Act premium subsidies that closely matches a similar proposal in President Biden’s campaign plan and $10 billion in small Medicaid expansions that last five years.

Making the expanded CTC permanent would cost an additional $1.1 trillion, assuming the expiring provisions in the Tax Cuts and Jobs Act (TCJA), which boosted the credit from $1,000 to $2,000 and eliminated the dependent exemption, are eventually extended or the policy is modified after 2026. Relative to current law, we estimate this would cost more like $1.5 trillion. Meanwhile, making the EITC and CDCTC extensions permanent would cost over $200 billion, and making the health care provisions permanent would cost about $250 billion. Altogether, we estimate these potential extensions would cost $1.9 trillion before interest, boosting the overall cost of the bill to $4.1 trillion when interest is included.

“The Wall Street crybabies are clamoring for this because massive highly leveraged bets on Treasury securities are producing massive losses.”

• Yellen Coddles Up to Powell on Rising Long-Term Yields (WS)

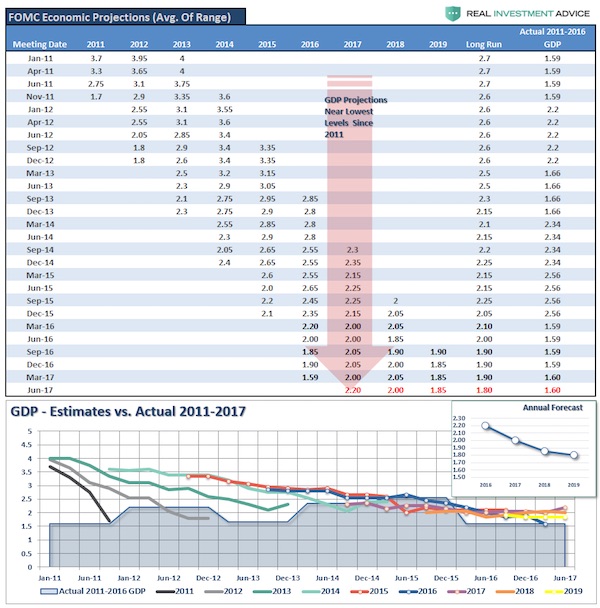

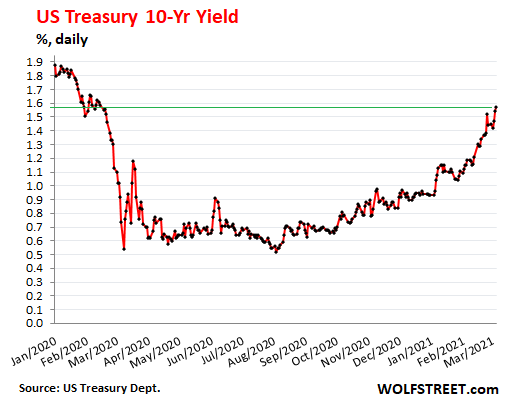

It seems to be a rare sight that a Treasury Secretary and a Fed Chair color-coordinate their comments about rising long-term yields. On Friday, Treasury Secretary Janet Yellen in an interview on PBS NewsHour echoed what Fed Chair Jerome Powell had said on Thursday in an interview with the Wall Street Journal. When Yellen was asked about the rising long-term yields that the crybabies on Wall Street are getting so nervous about, Yellen said in her quiet manner: “Long term interest rates have gone up some, but mainly I think because market participants are seeing a stronger recovery, as we have success with getting people vaccinated and a strong fiscal package that’s going to get people back to work.” “Rising interest rates don’t concern you?” she was then asked.

“I think they’re a sign that the economy is getting back on track, and market participants see that, and they expect a stronger economy,” Yellen said. “And instead of inflation lingering below levels that are desirable for years on end, they’re beginning to see inflation get back to a normal range of around 2%.” And inflation may rise more than that, but it’s going to be transitory, she said. So on Friday, the Treasury 10-year yield rose to 1.57%, still ludicrously low, given the outlook on inflation, and given the Fed’s insistence that it will let inflation run over 2% – as measured by “core PCE,” the inflation measure that nearly always produces the lowest inflation readings in the US. But that 1.57% was nevertheless the highest since February 14, 2020:

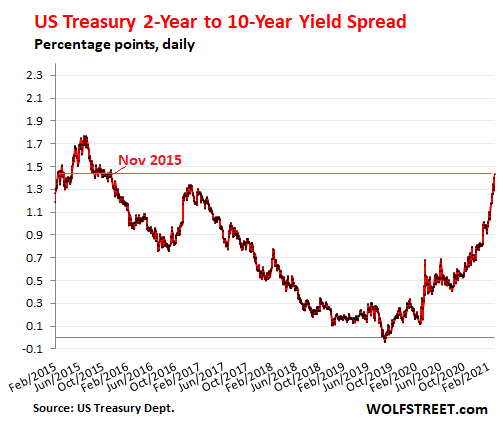

The spread between the Treasury 2-year yield (0.14%) and the 10-year yield (1.57%) widened to 1.43 percentage points. By this measure, the yield curve is the steepest since November 2015:

This rise in the 10-year yield has set off clamoring among the crybabies on Wall Street for the Fed to do something to bring them down. They have already outlined the remedies, including prominently another “Operation Twist,” where the Fed sells Treasury securities with short maturities and buys Treasury securities with long maturities. This concentrated buying of long-dated Treasuries would raise their prices and thereby push down their yields. The Wall Street crybabies are clamoring for this because massive highly leveraged bets on Treasury securities are producing massive losses.

This must be crossing some line.

• Italy’s Government Is Outsourcing Its Economic Strategy To McKinsey (Jac.)

Upon its formation last month, Mario Draghi’s new government was heralded by almost all Italian and international media as a rescue operation. Where the former European Central Bank (ECB) chief Draghi had “saved the euro” in the 2010s, most outlets gushed over “Super Mario” and his plan to “save Italy” by splashing a mooted €209 billion in European recovery fund cash while “reforming” its lackluster economy. The kind of “reforms” this meant went unmentioned — and after all, this government bears no relation to voter decisions, or the coalitions that ran in the last general election. But for the fourth time since the 1990s, a president called on a technocrat from the world of finance and banking to form a cabinet, halfway through a parliament. Eight of Draghi’s twenty-three ministers are unelected technocrats, in a so-called government of experts.

If these figures are not party-political, they have similar backgrounds and instincts. Economy minister Daniele Franco is a former Bank of Italy official who drafted the famous 2011 ECB letter instructing the government to implement privatizations and cut back collective bargaining. Former Vodafone CEO Vittorio Colao — today innovation and digital transition minister — is a former partner at private consultants McKinsey & Company. Now, it has been revealed that McKinsey is going to be tasked with writing Italy’s economic plan for the coming period, to be submitted for review by the European Commission at the end of next month. Notorious for its role in the Enron scandal as well as the 2008 financial crisis — as it promoted the boundless securitization of mortgage assets — and the botched vaccine rollout in France, the firm is now being called on to shape the Draghi government’s “reform” agenda.

La Repubblica, the country’s leading center-left daily, gushed over the move. “Faced with a race against time,” Draghi’s government “has assumed the position of a private corporation faced with a new business opportunity that isn’t part of its core activities.” While this same paper reported on March 1 that the need for “hurry” meant Draghi himself would write the recovery plan, together with finance minister Franco, this has now been outsourced. The suggestion that this is a purely “technical” collaboration — that McKinsey’s choices will not be political — is patently absurd, not least given that this claim is also widely made for Draghi’s “technical” government itself. For decades, the imposition of neoliberal recipes in Italy has been advanced through this same procedure, with the agenda advanced by privatizers couched in the dogma of “unavoidable choices.”

And still nobody knows why?!

• US Covid Cases Continue To Decline After Brief Plateau (JTN)

Daily new COVID-19 cases in the United States have continued declining after a brief plateau following a sharp drop from the beginning of the year. Cases have declined steeply since early January, baffling scientists who are struggling to explain the unexpected drop in COVID activity, particularly after weeks of dire warnings from health officials about the potential for a post-holiday spike. That decline leveled out in late February, with daily average case numbers appearing to be on a slightly upward trajectory at one point, leading experts to warn that positive test results could be preparing to explode again.

Yet cases appear to be dropping again, according to several data sources. The COVID Tracking Project indicates that daily average case numbers began slowly decreasing again around Feb. 27 and have continued on that downward trend over the past week. Likewise, the data website Worldometers also identifies average daily case numbers beginning a new decline at right around the same day. According to COVID Tracking, COVID-19 hospitalizations have continued on a seemingly unabated downward trajectory since early January, on Friday reaching levels not seen since late October.

Not all restrictions.

• Connecticut Lifting All Covid-19 Capacity Restrictions On Businesses (F.)

Connecticut will lift all capacity limits on certain businesses including restaurants, gyms, offices and houses of worship starting March 19, Gov. Ned Lamont announced Thursday, going further than most other Democratic-led states to roll back Covid-19 restrictions even as public health officials advise governors not to do so. Restaurants, retail businesses, libraries, personal services, indoor recreation facilities, gyms, fitness centers, museums, aquariums, zoos, offices and houses of worship will all have their capacity limits repealed. Social distancing protocols will still be in place and face masks will be required, and there will be some restrictions: theaters will remain restricted to 50% capacity, restaurants are limited to eight people per table and must close at 11 p.m. and bars that only serve beverages will still be closed entirely.

The state’s mask mandate will remain in effect. Gathering limits on social and recreational gatherings will also be increased March 19 to 25 people indoors and 100 people outdoors at a private residence, or 100 people indoors and 200 outdoors at a commercial venue. On April 2, the state will open outdoor amusement parks, open indoor stadiums at 10% capacity and increase occupancy at outdoor event venues to 50% capacity or up to 10,000 people. Connecticut will be one of only a few Democratic-led states to have such relaxed capacity restrictions: Virginia does not have capacity restrictions at restaurants or places of worship but does at gyms, Wisconsin’s capacity limit order has expired and Kansas’ restrictions are determined by county, with many having few or no limits.

“..depriving us all of autonomy and of the comforting, real-world support of friends and family, and robbing the less fortunate among us of health, of livelihoods, and, in the worst cases, of life itself.”

• The Nightingale Alternative (Gillian Dymond)

It is a year now since I last took a train: a short return trip, from Leamington Spa to Oxford. On the journey out, I was lucky enough to find a seat in which, for some forty minutes, I shared the air with my fellow travellers. At Oxford station I rubbed shoulders with a multiplicity of strangers as I joined the throng surging towards the exit and proceeding slowly through the congested barriers, then made my way along busy streets, brushing against other human beings on the narrow pavements. At the Ashmolean I met a friend, and together we mingled freely with the rest of the visitors at the well-frequented Rembrandt exhibition, then chatted at length over a late lunch in the museum café, where the tables – disdaining any hint of anti-social distancing – were full to capacity.

Later, after a walk through Christchurch Meadow and along the river, exchanging smiles and occasionally the odd word with those I passed along the way, I spent some time browsing the shelves of Blackwell’s in daring proximity with other booklovers before deciding on a purchase and braving the jostle of the station platform to board a packed train back to Leamington. It was a very ordinary day – a day passed without fear as I came into contact with numerous unknown people, some of whom, no doubt, were suffering from the common cold or harbouring incipient or suppressed symptoms of influenza or even of Covid-19 (which, as we now know, had already been on the loose for several, possibly many, months at that time). Not for a moment did this disturb me.

Like all those in good health and unafflicted by obsessive-compulsive disorder, I judged the hasard of stepping out boldly into the microbial soup which surrounds and permeates our existence to be a risk worth taking in exchange for the spontaneous social interaction without which human beings cannot thrive. I never guessed that this could be the last time I would be free to enjoy a day of such unexceptionable pleasures. True, rumblings of the pandemic had been growing over the previous weeks, but memories of previous damp squibs – SARS, bird flu, swine flu – which the worst-case speculations of computer-modellers had repeatedly failed to ignite encouraged me to hope that present reports from China and Italy, too, would soon fade into a penumbra of failed sensationalism.

[..] And the lockdowns, distancing and masking began. For close on a year now official statistics and figures spun out by a team of approved government experts into webs of cautionary speculation have justified rule by decree, depriving us all of autonomy and of the comforting, real-world support of friends and family, and robbing the less fortunate among us of health, of livelihoods, and, in the worst cases, of life itself. To anyone with the most rudimentary understanding of economic interdependence, the consequences of this decision to quarantine the whole nation were obvious from the start, and were uncannily favourable to the objectives of Agendas 21 and 2030, as handed down from the UN, via national administrations, to local governments throughout the world: but the people of the UK, it seemed, were convinced by the official “narrative”, thousands of them assembling on their doorsteps each Thursday evening to shake their fists at The Virus, and demonstrate solidarity with the NHS.

Ha ha!

“As one of President Trump’s MOST LOYAL supporters, I think that YOU, deserve the great honor of adding your name to the Official Trump ‘Thank You’ Card.”

• Trump Sends Legal Notice To GOP To Stop Using His Name (Pol.)

Lawyers for former President DONALD TRUMP sent out cease-and-desist letters Friday to the three largest fundraising entities for the Republican Party — the RNC, NRCC and NRSC — for using his name and likeness on fundraising emails and merchandise, a Trump adviser tells Playbook. We reported yesterday that Trump was furious that his name has been bandied about by organizations that help Republicans who voted to impeach him — without his permission. Trump, who made his fortune in licensing, has always been sensitive to how his name has been used to fundraise and support members, even while in office.

On Friday, the RNC sent out two emails asking supporters to donate as a way to add their name to a “thank you” card for Trump. “President Trump will ALWAYS stand up for the American People, and I just thought of the perfect way for you to show that you support him!” the email states. “As one of President Trump’s MOST LOYAL supporters, I think that YOU, deserve the great honor of adding your name to the Official Trump ‘Thank You’ Card.” A follow-up email was sent hours later to “President Trump’s TOP supporters” warning of a deadline of 10 hours to get their names on the card.

None of the committees returned a request for comment. But privately GOP campaign types say it’s impossible not to use Trump’s name, as his policies are so popular with the base. If Trump really wants to help flip Congress, they argue he should be more generous. His team, however, sees this differently. “President Trump remains committed to the Republican Party and electing America First conservatives, but that doesn’t give anyone – friend or foe – permission to use his likeness without explicit approval,” said a Trump adviser.

They’ll refuse.

• Congressmen Demand Twitter’s Internal Docs Regarding Trump Censorship (JTN)

Two Republican representatives are renewing a demand that Twitter hand over internal documents regarding its decisions to censor and moderate content on its platforms, accusing the tech company of harboring significant bias against a large part of its user base. Reps. Jim Jordan and Ken Buck claimed in a letter to Twitter CEO Jack Dorsey this week that Twitter itself has played “a leading role in silencing and censoring political speech of conservative Americans.” The letter repeats a request that Jordan lodged last summer with which Twitter reportedly did not comply.

“In recent months, Twitter throttled the dissemination of a mainstream newspaper article critical of then-candidate Joe Biden’s son,” they wrote in the letter, “and later took the unprecedented step of de-platforming the sitting President of the United States. If Twitter can do this to the President of the United States, it can do it to any American for any reason.” The politicians demanded that Twitter hand over “an accounting of all content moderation decisions made by Twitter over the past year for users located within the United States, including which Twitter rule or policy the user allegedly violated and the content of the moderated tweet,” as well as “all documents and communications” related to its decision to censor several of then-President Donald Trump’s tweets last year.

“Why would a state sponsored hacking campaign, especially from China, actually want that? Why would China want to attract more negative news about its country?”

• Is China Hacking Random Servers To Put Itself Into A Bad Light? (MoA)

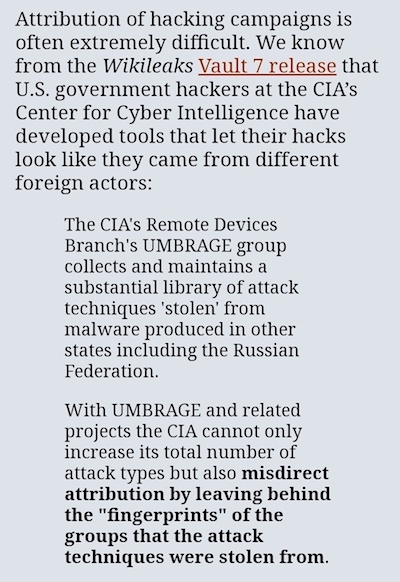

In January 2021, through its Network Security Monitoring service, Volexity detected anomalous activity from two of its customers’ Microsoft Exchange servers. Volexity identified a large amount of data being sent to IP addresses it believed were not tied to legitimate users. A closer inspection of the IIS logs from the Exchange servers revealed rather alarming results. … Through its analysis of system memory, Volexity determined the attacker was exploiting a zero-day server-side request forgery (SSRF) vulnerability in Microsoft Exchange (CVE-2021-26855). The attacker was using the vulnerability to steal the full contents of several user mailboxes. This vulnerability is remotely exploitable and does not require authentication of any kind, nor does it require any special knowledge or access to a target environment. The attacker only needs to know the server running Exchange and the account from which they want to extract e-mail.

The hackers used four different zero-day security holes in Exchange Server products. A zero-day security hole is one that was previously unknown and has never been used before. To find new zero-day security holes is difficult and expensive. But after they are found and made operational they are often easy to use. Whoever did this hack has invested quite some effort. Besides extracting emails the hackers also installed backdoors that give them remote access to the hacked Exchange systems. On March 2 Microsoft released patches for the four security holes. In its release it accused China of being behind the hack:

“Today, we’re sharing information about a state-sponsored threat actor identified by the Microsoft Threat Intelligence Center (MSTIC) that we are calling Hafnium. Hafnium operates from China, and this is the first time we’re discussing its activity. It is a highly skilled and sophisticated actor. Historically, Hafnium primarily targets entities in the United States for the purpose of exfiltrating information from a number of industry sectors, including infectious disease researchers, law firms, higher education institutions, defense contractors, policy think tanks and NGOs. While Hafnium is based in China, it conducts its operations primarily from leased virtual private servers (VPS) in the United States.”

[..] The attribution Microsoft makes is in light of the above quite weak. The direct attacks came from rented virtual private servers within the U.S. These were, says Microsoft, operated through machines in China. But how does Microsoft know who has actually control over those machines in China? Could they not be hacked too? Couldn’t the real actors sit anywhere on this planet and access them through the Internet? Microsoft also says that its attribution is “based on observed victimology, tactics and procedures”. The victims are described as “infectious disease researchers, law firms, higher education institutions, defense contractors, policy think tanks and NGOs”.

For a state sponsored campaign, especially one that burns four expensive zero-days, that victimology is unusually wide. It practically guaranteed that the attack would be detected fairly soon. “Tactics and procedures” are something that is even harder to attribute than the code used in the attack. Microsoft details some of these: “HAFNIUM has previously compromised victims by exploiting vulnerabilities in internet-facing servers, and has used legitimate open-source frameworks, like Covenant, for command and control. Once they’ve gained access to a victim network, HAFNIUM typically exfiltrates data to file sharing sites like MEGA.

This hack used legitimate open source tools that are widely available and are also used by many cybercrime organizations and secret services. What then are the specific ‘tactics and procedures’ which attribute this to China? Microsoft won’t say. There is also a fact that the hackers have gone into overdrive as soon as Microsoft released the patches. They now infect any system they can find. That surely will result in an extreme amount of international publicity. Why would a state sponsored hacking campaign, especially from China, actually want that? Why would China want to attract more negative news about its country? Could there be some other country that has an interest in pushing public accusations against China by linking it to massive global hacking campaign?

Governments and central banks want control.

• Bitcoin Could Soon Run Head First Into US Money Laundering Laws (ZH)

Among the challenges in regulating bitcoin will be the Biden administration’s handling of recent anti-money laundering laws put into place by the Trump administration pertaining to bitcoin and cryptocurrencies. The rules, implemented at the last-minute by the Trump administration, seek requirements for financial services firms to report identities of cryptocurrency holders, according to Bloomberg. The point of the rules is to stop attempts to use crypto as a means of transferring money illicitly. Lobbying against the regulations are “heavyweights from both K Street and Wall Street”, according to Bloomberg, including Fidelity and the U.S. Chamber of Commerce. The Chamber of Commerce has said the rule would have “unintended long-term consequences” on the virtual currency industry.

Also lobbying against the rule have been “Republican lawmakers, including former Representative Cynthia Lummis, who is now a Wyoming senator; Arkansas Senator Tom Cotton and Democratic Representative Tulsi Gabbard of Hawaii”. The rules were implemented by the Financial Crimes Enforcement Network or FinCEN, after President Trump lost the 2020 election. The move drew criticism and even the threat of lawsuits from pro-crypto trade groups. The rule would require filings to the Treasury every time a customer moves at least $10,000 worth of virtual currency into a wallet not hosted at an exchange. These are similar to the reports that banks already send under existing AML laws when customers take out $10,000 or more in cash.

The regulation would also require banks and exchanges to keep records of customers who send $3,000 or more of virtual currencies to someone else’s unhosted wallet. Obviously, such regulation would maim one of bitcoin’s biggest “assets”: the ability to transfer money anonymously and “outside the system”. Should Treasury Secretary Janet Yellen move forward with the rules, crypto services could wind up becoming more expensive – and some cryptocurrencies could even disappear altogether.

Nice take.

• The Dark Side Of “Eating Lower On The Food Chain” (Turchin)

Nine years ago I made one of the most consequential decisions of my life—I switched to the so-called Paleo Diet (“paleo” is a bit misleading, as I explain in the post). Had I not done so, I would certainly have contributed to the rising obesity statistics for the United States. Within six months of switching to Paleo diet I lost 20 pounds before equilibrating at my current weight. But weight is actually the least important thing. Much more important was a dramatic improvement of my general health I experienced in the months since switching. I feel better today than ten years ago, despite being (obviously enough) ten years older. The major change was eating much higher on the food chain. The only way to get protein on a purely plant-based diet is to eat grains and pulses, which means wheat and beans.

But those are precisely the foods elimination of which resulted in my health improvement. I sometimes unknowingly consume small amounts of wheat, when a restaurant chef uses flour for the sauce (despite explicit entreaties not do so). The next day I know that I had been poisoned. The other thing is that it’s not just protein deficiency. Your body doesn’t need that much protein. The biggest problem with purely plant diet is that you don’t get enough healthful fat. Instead you end up poisoning yourself with seed oils. This is why I watch with increasing alarm the current trend to “cancel” meat. Last year the town of Cambridge, home of one of two best universities in UK, banned meat. So Cambridge is now off my list of places to go to (fortunately, I visited it years ago, when it was still safe for carnivores).

I am very worried that the veganism tide will continue spreading, leaving us carnivores on reservations (or even driving people following Paleo diet to extinction). Somebody is sure to immediately accuse me that I don’t care about the environment. Au contraire. Some of the most depressing environments that I’ve seen are giant agricultural fields (e.g. driving through Iowa).

Compare it to what they looked like before:

“..children who frequently use mobile devices are more likely to process stimuli on a “local” level, for example they “process the details” of an image first rather than the overall image itself.”

• Mobile Devices Alter Children’s Minds, Change How They Perceive The World (JTN)

Researchers in Hungary this week announced the findings of studies into what effects digital devices have on young minds, concluding that the increased usage of such technology has changed how younger individuals interact with the world around them. In a press release, scientists at Eötvös Loránd University said that children of the “Alpha Generation,” or those born after 2010, “typically grow up with mobile devices in their hands” which “seems to change how they perceive the world.” Summarizing their findings, the Hungarian researchers claim that children who frequently use mobile devices are more likely to process stimuli on a “local” level, for example they “process the details” of an image first rather than the overall image itself.

The results “show that the type of experiences children meet matters much,” the release said, “because at this age the brain is very plastic, so such massive early exposure may have a significant long-term effect.” “The atypical attentional style in mobile user children is not necessarily bad,” one of the scholars commented, “but different for sure, and we cannot ignore this – for example in pedagogy.

We try to run the Automatic Earth on donations. Since ad revenue has collapsed, you are now not just a reader, but an integral part of the process that builds this site. Thank you for your support.

Support the Automatic Earth in virustime. Click at the top of the sidebars to donate with Paypal and Patreon.