Jack Delano Mike Evans, welder, Proviso Yard, Chicago & North Western RR 1940

Stop it already!

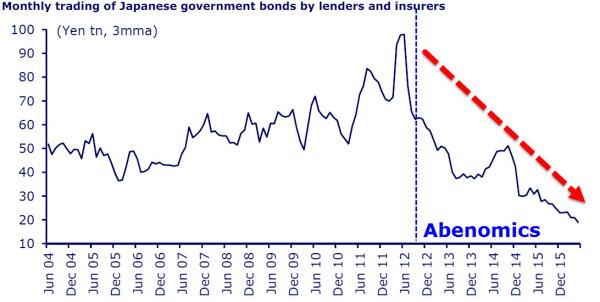

• The Decline & Fall Of The Biggest Bond Market In The World (ZH)

Government bonds are themselves becoming more illiquid, most particularly, as CLSA’s Chris Wood notes, in a country like Japan where the Bank of Japan has been buying more than the net issuance. Monthly trading of JGBs by lenders and insurers has collapsed from a peak of ¥123tn in April 2012 to a record low of ¥15tn in May 2016. This raises the pertinent issue of whether the Bank of Japan has reached the practical limit of its government buying programme in terms of its current purchase programme of ¥80tn relative to estimated annual JGB net new issuance of ¥34tn.

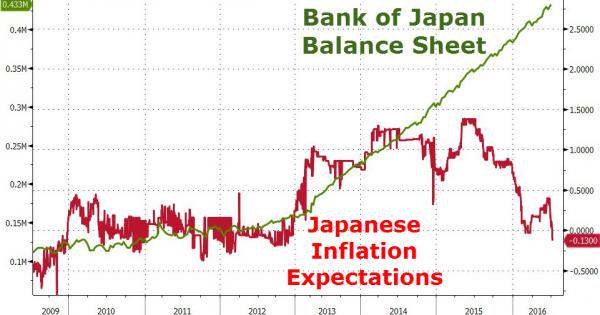

In this respect, the Japanese central bank has from a potentially monetisation standpoint always defended the integrity of its JGB purchase programme by stressing that it only buys JGBs in the secondary market, which means that the seller of the JGB to the BoJ forfeits a claim to that asset. This is contrasted to what would happen if the BoJ bought JGBs in the primary market on an open-ended basis. Such a process would be highly inflationary and, sooner or later, would be viewed by the market as such. And as Wood concludes, the next step is obvious…

“This is why Japan, as well as America, is also a candidate for monetisation of infrastructure stimulus or for what Bernanke has called a “money-financed fiscal programme”, or what has been called in other quarters “overt monetary financing”. This is because Bank of Japan governor Haruhiko Kuroda is now looking for a new alternative form of monetary easing, given he has probably reached the practical limits of responsible JGB buying, as already discussed, while his initial move to impose negative rates in January led to the opposite market reaction than expected (ie, a stronger yen and a weaker stock market) while also proving politically very unpopular. This probably explains why Kamikaze Kuroda has not expanded the negative rate policy further since January even though inflation and inflation expectations have moved in the opposite direction of what he has been targeting.”

The latest data will make it harder for Kuroda to do nothing at the next BoJ policy meeting due to be held on 28-29 July given the stress he has put on monitoring inflation expectations. That is unless he just admits he has failed! Given the unattractive options of buying still more JGBs or ETFs, or risking an undoubtedly unpopular expansion of negative rates, Kuroda and indeed Abe will be looking for a new approach. Monetisation of infrastructure stimulus may be the option. Meanwhile, in an effort to calm potential concerns about the integrity of the fiscal budget central bankers implementing such a future monetisation of infrastructure spending will doubtless be at pains to describe the process as a “one off” though, as the ever theoretical Bernanke stated in his blog: “To have its full effect, the increase in the money supply must be perceived as permanent by the public.”

But the jobs report?!

• More Than 20% Of Americans Are Simply Too Poor To Shop (NYPost)

Retailers have blamed the weather, slow job growth and millennials for their poor results this past year, but a new study claims that more than 20% of Americans are simply too poor to shop. These 26 million Americans are juggling two to three jobs, earning just around $27,000 a year and supporting two to four children — and exist largely under the radar, according to America’s Research Group, which has been tracking consumer shopping trends since 1979. “The poorest Americans have stopped shopping, except for necessities,” said Britt Beemer, chairman of ARG. Beemer has been tracking this subgroup for two years, ever since his weekly surveys of 15,000 consumers picked up that 21% of consumers did not finish their Christmas shopping in 2014 due to being too busy working.

That number grew to 29% last year, and Beemer dug in to learn more about them, calling them on holidays. He estimates that this group has swelled from 6 million households four years ago, because their incomes have not kept pace with expenses like medical costs. Nearly half of all Americans have not seen an increase in salary over the last five to seven years, and another 28% have seen their take-home pay reduced by higher medical insurance deductions or switching to part-time jobs, ARG found. “It’s scary when you start to see things that you’ve never seen before,” said Beemer. “People are so pessimistic about their future.” Most of those living on the edge — 68% are women between the ages of 28 and 38 — work in retail or in call centers, according to Beemer.

Rosenberg flip flop. “This is otherwise known as looking at the big picture.”

• What If I Told You Employment Actually Declined 119,000 In June (Rosenberg)

David Rosenberg: What if I told you that employment actually declined 119,000 in June and has been faltering now for three months in a row? Yes, that is indeed the case. Of course, the focus, as always is on the non-farm payroll report but keep in mind that while this is the data series that moves markets, it does not necessarily have the final word on how the labor market is truly faring. Okay, so let’s get the pablum out of the way first. Nonfarm payrolls surprised yet again but this time to the upside — surging 287,000 in the best showing since last October and again making a mockery of the consensus economics community which penned in a 180,000 bounce….

…as if the Household sector ratified the seemingly encouraging news contained in the payroll data as this survey showed a tepid 67,000 job gain last month and rather ominously, in fact, has completely stagnated since February. Historians will tell you that at turning points in the economy, it is the Household survey that tends to get the story right.

[..] The simple fact of the matter is that May and June were massive statistical anomalies. The broad trends tell the tale. Go back to June 2014 and the six-month trend in payrolls is running at a 2.2% annual rate and the three-month trend at 2.4%. A year ago, as of June 2015, the six-month pace was 1.9% and the three-month at 2.2%. Fast forward to today, and the six-month annualized rate is 1.4% and the three-month has slowed all the way down to a 1.2%. This is otherwise known as looking at the big picture.

When the Household survey is put on the same comparable footing as the payroll series (the payroll and population-concept adjusted number), employment fell 119,000 in June – again calling into question the veracity of the actual payroll report — and is down 517,000 through this span. The six-month trend has dipped below the zero-line and this has happened but two other times during this seven-year expansion.

“..the E.U.’s “free-trade zones” have become classic Orwellian nomenclature. Flip it: “Free-trade zone” means “unfree-trade zone.”

• Chicken Little Economists Are Wrong About Brexit (MW)

A few years ago when Grexit was the E.U. crisis du jour, I explained why Greece just didn’t matter to the world’s economies or the U.S. stock markets in columns like this one called, “Apple is bigger than the entire Greek economy.” Did you know that Great Britain’s GDP is 10 times larger than Greece’s? Unlike with Apple vs Greece’s entire GDP, at $2.7 trillion per year, Britain’s economy is equal to the combined market cap of Apple, Google, Microsoft, Exxon Mobil, Berkshire Hathaway, Amazon and Facebook. The total market cap of the DJIA is only (?) about $5.5 trillion, or twice Britain’s GDP. Clearly, Brexit has a much bigger potential to impact the broader economy and the financial markets than Greece ever did.

Which, in my opinion, is a good thing. Greece’s economy has shrunk 20% since the great Greek Financial Crises Du Jour was hitting the markets and the country chose to stay in the E.U. rather than getting out. Staying in the E.U. has created a Great Depression kind of decline in the economy there. Now I don’t think Great Britain has ever been positioned as poorly as Greece has been inside the E.U., so I certainly don’t think its economy is about to crash 20% in the next two or three years whether in or out of the E.U. But I like the prospects for the country to unwind the cumbersome red tape, regulations and control from the E.U.’s central powers, thereby unleashing entrepreneurship, innovation and freer trade,

One of the great ironies that Brexit has highlighted is that the E.U.’s “free-trade zones” have become classic Orwellian nomenclature. Flip it: “Free-trade zone” means “unfree-trade zone.” As LunaticTrader put it in a discussion about all of this on Scutify: “The E.U. worked well until the late 1990s when it was mainly a free-trade zone. It has gradually morphed into an ‘unfree trade zone’ because that ‘free’ has been gradually replaced by 80000 laws and regulations, combined with the euro, which took away the weaker countries’ (Greece, Italy, Spain…) main tool to manage their own economy. This doesn’t offer any economic benefits to the weaker E.U. members, as has become abundantly clear.”

From this corner’s perspective, Great Britain’s leaving the E.U. gives the nation itself a much higher probability of creating economic growth and prosperity for its citizens than staying in the E.U. ever did. That new upside potential, plus the fact that its economy is large enough to impact the global and U.S. economies nets out to Brexit being a positive, despite all the handwringing in the media and Chicken Little politicians, economists, pundits and traders who are basically begging you to freak out about it.

What Brexit will correct.

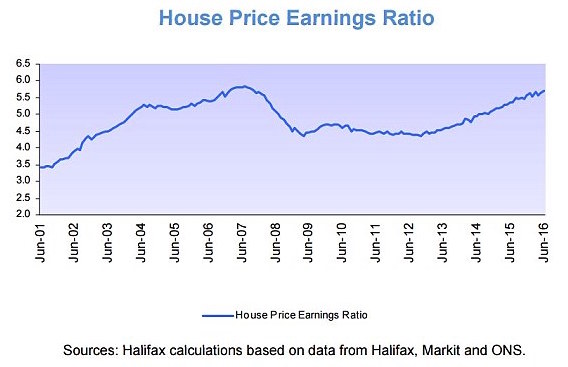

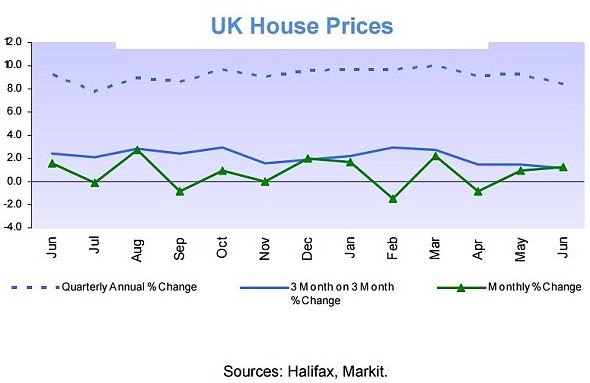

• UK Property Hits Levels Of Unaffordability Not Seen Since 2007 (TiM)

UK house prices continued to rise in June, adding almost £3,000 in a month, stretching affordability to levels not seen since the run-up to the financial crisis in 2007, a new survey suggests. Halifax said it was too early to say how the referendum that sanctioned the UK’s decision to leave the EU will impact the housing market, but added there were signs the pace of growth is easing. The price of the average home in the UK rose by 1.3% between May and June, or by £2,708, to hit £216,823, up from 0.6% the previous month, according to the latest index by the mortgage lender. Meanwhile, the ratio of house prices to earnings rose to 5.70 in June from 5.65 in May, marking its highest level since October 2007.

This means that buying a new home will cost the average workers close to six years of their earnings before tax. On an annual basis, however, prices grew by 8.4%, down from 9.2% in May, posting the lowest growth since July last year. Martin Ellis, Halifax housing economist, said: ‘There is evidence that the underlying pace of house growth may be easing.’ And added: ‘House prices continue to increase, albeit at a slower rate, but this precedes the EU referendum result, therefore it is far too early to determine any impact since.’ The Bank of England this week warned that property prices ‘had become stretched’ in recent months – meaning a cooling of the market was likely at some point regardless of the Brexit vote.

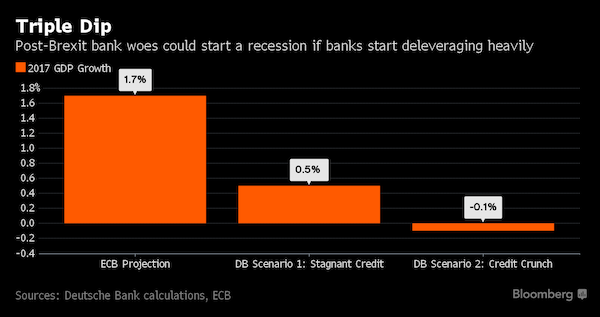

“..if banks decide to keep their balance sheets unchanged until the end of 2017, this could halve economic growth in the euro area next year.”

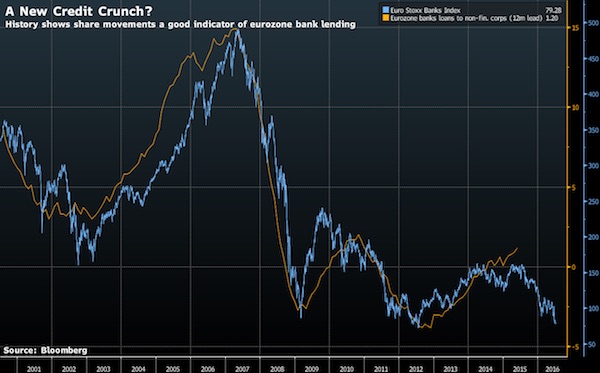

• If Bank Stocks Are Linked to Bank Lending, Europe Should Worry (BBG)

Don’t underestimate the toll that the post-Brexit bank equity rout can take on the euro-area economy. Initial calculations of the effect of the U.K. referendum on the region’s recovery have suggested that the blow will be relatively mild, with ECB President Mario Draghi telling European Union leaders that the impact from direct trade could add up to 0.5 %age point over three years. But such scenarios don’t take into account the consequence of the 23% decline in bank stocks since the Brexit vote. Historically, bank equities have correlated strongly with bank lending, with about a year’s lag, as the chart below shows.

Deutsche Bank analysts led by Marco Stringa argue in a July 5 paper that there’s also a causal link: As banks are now under regulatory pressure to raise capital, slumping stock prices and low profitability make it very difficult to build up funds either externally or internally. Deutsche Bank’s own share price has fallen by more than 25% since June 23. If banks struggle to raise capital, they may come under extra pressure to shrink assets. That could mean less lending to the economy. Bankers often claim that asking them to have more funds of their own instead of borrowing from the market hampers their ability to extend credit. Regulators retort that higher capital requirements in fact strengthen a bank’s ability to make loans, not the opposite.

Even so, it might mightn’t take much for Brexit to put a stop to the timid pick-up in euro-area bank lending that started just last year. That’s not least because of the impact of uncertainty on households’ and companies’ investment choices. The impact of a renewed credit crunch on Europe’s largely bank-dependent companies could be severe. Not by chance, fixing the banks to restart credit to the real economy has been one of the main goals of the ECB’s policies since the crisis. Stringa estimates that if banks decide to keep their balance sheets unchanged until the end of 2017, this could halve economic growth in the euro area next year. Worse still, if lenders only manage to raise half of the funds they need to meet what the economists refer to as “Basel IV” requirements, this could force them to reduce their loan book’s risk-weighted assets.

May have co-financed Columbus: “In 1624, the Medici Grand Duke of Tuscany rushed to the defense of depositors of a bank that was by then already 152 years old..”

• Italy PM’s Tuscan Nightmare: The Fall Of ‘Daddy Monte’ (R.)

In 1624, the Medici Grand Duke of Tuscany rushed to the defense of depositors of a bank that was by then already 152 years old, Monte dei Paschi di Siena, guaranteeing their savings at a time of economic crisis. Nearly 400 years later, Italian Prime Minister and fellow Tuscan Matteo Renzi aims to do something similar as the world’s oldest bank and Italy’s third-largest lender again threatens the region’s savers. This time the stakes are much higher. The collapse of Monte dei Paschi could not only impoverish thousands of ordinary Italians, it could lead to a wider banking crisis, help tip Renzi from power and provide another strong jolt to the European Union, already reeling from Britain’s referendum vote to leave the group.

“The government must assume its responsibilities, save the bank and its investors, otherwise this gangrene will spread to the rest of the system,” said Romolo Semplici, a 58-year-old real estate entrepreneur whose 22,000-euro investment in the bank’s shares is now worth less than 200 euros. “I’ve always been pro-European, but if Europe doesn’t protect its own citizens then we should think twice if this the kind of Europe that we want to be in.” Government sources say Italy is considering options to prop up the bank, including a state guarantee that would enable the bank to raise money it would otherwise struggle to secure from skeptical investors. Many bankers say the bank will inevitably have to raise around €3-4 billion.

Officials in Brussels, a world away from the medieval cobble-stoned alleys of Siena, one of Italy’s most popular tourist centers, may stand in Renzi’s way. A state rescue of Monte dei Paschi would be the first real test of EU rules limiting the use of taxpayers’ money to bail out investors. The rules require holders of the bank’s shares and junior debt to bear some of the losses. Depositors with more than €100,000 would also be hit. The bank’s share price has halved since Britain voted on June 23 to leave the EU, as investors stampede out of Italian banks on concerns that Brexit could send Italy back into recession and saddle them with even more bad debts.

“..Italy may fall in October or may not, but it will eventually occur..”

• Albert Edwards: Brexit Is Old News, Time To Worry About Italy (VW)

Edwards looks at the 2008 financial crisis and says it was not Lehman Brothers that was causation. Lehman was a symptom of an economic engine already in decline. Likewise there is Brexit, an issue he notes has been accompanied by some of the most emotional ranting he’s seen – on both sides of the argument, including his own. Brexit will be used as an excuse for all sorts of economic ills, but it is only a symptom, a benchmark for a larger trend. When he takes off the emotional hat, he says the real issue is the continued dismantling of the European Union that is upon which savvy investors should focus. There is a game of dominoes being played out and Brexit was just the latest move in a trend.

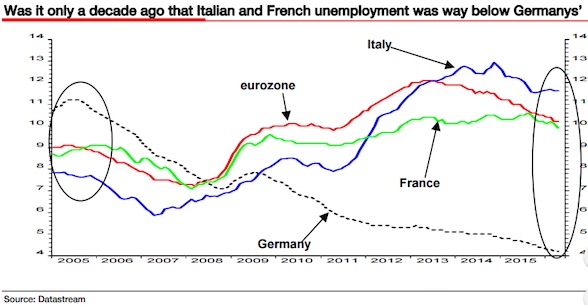

“In the aftermath of the Brexit vote there is an increasing fear of other dominoes falling within the heart of the EU – the eurozone,” Edwards wrote. “Italy is bleeping very loudly on most people’s radars with its banking crisis and impending referendum seen as leaving the country on a knife-edge.” The Italian banking crisis is important, but it is not the primary problem. “It is a symptom of the problem that problem being a perpetually stagnant economy and deflation,” he wrote. “Italy simply does not appear to be able to grow inside the eurozone and more importantly probably never will.” But it is not just Italy that could be part of the trend extension, the trend could be extended across Europe.

In making this analysis, Edwards does not cite all too simple issues of immigration, fear of globalization or a lack of foresight by the slovenly masses who vote. He looks at economic numbers and notes that it’s not just Italy that is at risk of withdrawing from a marriage. There have been economic winners and losers, and they are clear and documentable. “Indeed the Italian economy has barely grown one jot since it joined the eurozone at the start of 1999 while Germany has grown rich,” he said, pointing to one clear winner with many clear losers. “As inevitably people compare their fortunes with that of their neighbours, the Italians are mighty pissed off.”

“..the country is “condemned to perpetual economic stagnation within the strictures of the euro zone..”

• Italy’s In An Economic Straitjacket, Needs To Be Freed: Albert Edwards (CNBC)

The citizens of Italy will vote to leave the euro zone after an impending recession and a shift in power inside the country’s political system, according to Societe Generale’s notoriously bearish strategist, Albert Edwards. “The people are angry,” Edwards said in a note Friday, highlighting a poll in May by IPSOS Global that showed almost half of Italians would vote “out” in a referendum on their country’s EU membership. “Italy simply does not appear to be able to grow inside the euro zone and more importantly probably never will … after the next recession I believe a majority of Italians will have had enough of the euro zone experiment and vote in the radical Five Star Movement,” he added.

Anti-establishment Five Star Movement (M5S) is now Italy’s most popular party after a poll on Wednesday showed that it would win an election over Prime Minister Matteo Renzi’s Democratic Party (PD), according to Reuters. This comes at a time when Renzi is trying to deal with a fragile banking system, bogged down by non-performing loans. A referendum on constitutional reform this October is also looming and could well usher in new elections. But Edwards suggests that the Italian bank crisis – and also Brexit – are not a cause of the world’s economic problems, but just symptoms. The real issue is that the country is “condemned to perpetual economic stagnation within the strictures of the euro zone,” he said, suggesting that recapitalizing the Italian banks will not solve their problems.

With a slew of figures, the Societe Generale strategist detailed in his research note how unemployment has risen since the mid-2000s and how productivity has stagnated. Going forward, he believes Renzi should announce an “aggressive fiscal pump” despite the complaints that might arise from Germany and the European Commission. “Italy has played by the fiscal austerity rules for too long. Although its problems are structural in nature, after running an underlying primary fiscal surplus for some 20 years it is time to break free from its self-imposed deflationary fiscal chains,” he added.

Question is: why save the EU?

• Only Europe’s Radicals Can Save The EU: Yanis Varoufakis (Newsweek)

Spaniards went to the polls three days after the shock of Brexit to produce a result that, ostensibly, delivers victory to the status quo. However, the status quo is tired, fragmenting, and prone to vicious unraveling unless the EU’s deconstruction is impeded. But, the Spanish establishment, which is determined to maintain the status quo, lacks both the analytical power and the political will to impede the EU’s disintegration. And so an electoral result in favor of continuity becomes the harbinger of deep uncertainty. Reeling under the British voters’ radical verdict, “official” Europe took solace from Spain’s general election outcome. They read into it evidence that the post-Brexit fear factor may help knock some “sense” into voters, putting them off “populist” parties.

But, even if this is so, for how long will fear keep voters loyal to a crumbling status quo? The threat of a pyrrhic victory for Spain’s establishment is, thus, clear and present. Spain and the U.K. differ in one crucial sense. While EU policies and institutions have damaged the Spanish economy a great deal more than Britain’s, Spain’s political system remains largely free of euroskepticism. The paradox dissolves quickly when one considers the traditional lack of legitimacy of the Spanish elites in their own country. British Tories, like Michael Gove and Boris Johnson, knew they could draw mass support from a slogan like “We want our country back!” The Spanish establishment cannot do this.

And they cannot do it because, over the last four decades, they managed to retain control by offering voters an unlikely deal: “You keep us in government and we shall do what is necessary to rid you of us, by transferring power to Brussels and to Frankfurt.” Calling for a restoration of sovereignty now would strike Spanish voters as backtracking on the promise to rid them of their local rulers. But, then again, this promise is under increasing strain at a time when the process of Europeanization is in serious trouble.

As you may have noticed, I find it ever harder to stay away from politics. This is because the economic collapse increasingly spils over into what is after all a fully integrated politico-economic system. In this case, what caused Brexit is also what makes Corbyn strong. But Britons are not nearlly far enough along in the Kübler-Ross cycle to understand this. They’re still stuck in blaming other people for the perceived injustices that befall them.

• Worst. Coup. Ever. (TeleSur)

As the Chilcot Inquiry report is released to the public, those MPs attempting to depose Labour leader Jeremy Corbyn—their leading lights inescapably sullied by having supported the war—are suing for peace. Over a week of high-profile resignations, statements, demands, pleas and threats have seemingly done little but consolidate Corbyn’s position. In record time, it has gone from being a coup to a #chickencoup to a #headlesschickencoup. This could be the biggest own-goal in the history of British politics. Journalists steeped in the common sense of Westminster, assumed that it was all over for Labour’s first ever radical socialist leadership. How can he lead, they reasoned, if his parliamentary allies won’t work with him?

This, in realpolitik terms, merely encoded the congealed entitlement and lordly presumption of Labour’s traditional ruling caste. Even some of Corbyn’s bien-pensant supporters went along with this view. They should have known better. The putschists’ plan, such as it was, was to orchestrate such media saturation of criticism and condemnation aimed at Corbyn, to create such havoc within the Labour Party, that he would feel compelled to resign. The tactical side of it was executed to smooth perfection, by people who are well-versed in the manipulation of the spectacle. And yet, in the event that Corbyn was not wowed by the media spectacle, not intimidated by ranks of grandees laying into him, and happy to appeal over the heads of party elites to the grassroots, their strategy disintegrated.

This was not politics as they knew it. The befuddlement was not for want of preparation. From even before his election as Labour Party leader, there were briefings to the press that a coup would be mounted soon after his election. And in the weeks leading up to the European Union referendum, Labour Party activists reported that they were expecting a coup to be launched after the outcome was announced, regardless of what the result was. This seemed like a half-baked idea—there was still no overwhelming crisis justifying a coup attempt—and so it turned out to be.

Undoubtedly, part of the rationale for hastening the attempted overthrow was the looming publication of the findings of the Chilcot Inquiry, which was expected to be harshly critical of former Prime Minister Tony Blair, of the justification for the invasion of Iraq, and of the relationship with the Bush administration. Given the role of the Parliamentary Labour Party in leading Britain into that war, against fierce public and international opposition, and given its role in supporting the subsequent occupation, this was a bad moment to have Corbyn at the helm. In the event, Corbyn survived to make a dignified statement apologizing for Labour’s role in the disaster and promising to embark upon a different foreign policy—one quite at odds with that supported by the pro-Trident, pro-bombing backbenchers.

The world needs more debt!

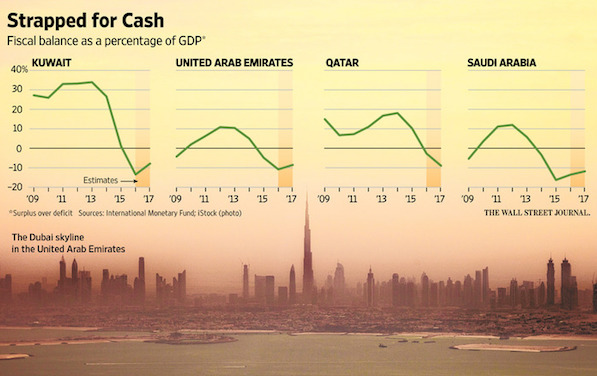

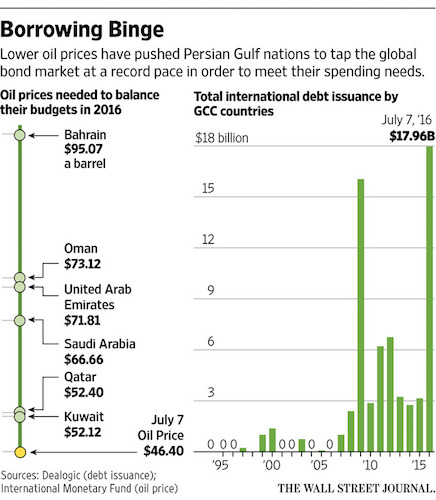

• The Persian Gulf’s Huge New Export: Debt (WSJ)

The energy-producing states of the Persian Gulf are issuing bonds at the fastest clip ever, showing how the oil bust is reshaping the region’s finances despite a near doubling of crude prices this year. The Gulf Cooperation Council states of Saudi Arabia, United Arab Emirates, Bahrain, Kuwait, Qatar and Oman together have raised a record $18 billion in 2016, according to Dealogic, helping refill coffers depleted by sharp revenue declines. Investors expect issuance to increase further, as governments brace for lower prices than they were budgeting only a few years ago. Saudi Arabia is expected to raise up to $15 billion more in the coming weeks, and total issuance by the Gulf nations could reach $35 billion this year, according to JP Morgan Chase, more than doubling the previous high set in 2009.

The issuers are paying slightly higher costs than other emerging countries with similar ratings, reflecting uncertainty over how successful they will be in opening up their economies, the region’s geopolitical risks and the murky outlook for oil prices, analysts and portfolio managers said. But the bond sales generally have been successful, driven by strong demand from local investors and banks, improving market sentiment due to the oil rebound, and a persistent decline in global interest rates that is putting a premium on securities with better yields. In May, Qatar raised $9 billion in an offering that drew more than twice that sum in orders. The five-year notes issued by the nation of 2.5 million trade at 2.13%. That is more attractive when compared with 1.83% on the comparably rated bonds issued by Korea National Oil, according to Anita Yadav at Emirates NBD.

-12.4% YoY

• Greek Exports Record Major Decline In May (Kath.)

Exports posted a significant decline in May, reflecting to a great extent the impact of the uncertainty from Athens’s months-long negotiations with its creditors, as well as of the industrial action at the ports of Piraeus and Thessaloniki. According to Hellenic Statistical Authority (ELSTAT) figures issued on Friday, exports contracted 12.4% compared with May 2015, amounting to 2.02 billion euros. The decline came to 6.4% not including fuel products, as exports recorded their first decline in the last four months.

“This decline, besides the general problems and the continued uncertainty in the Greek economy, is partly due to the situation in the country in recent months, as the industrial action at the ports of Thessaloniki and Piraeus started in May,” noted the Greek International Business Association (SEVE) in a statement. Panhellenic Exporters Association chief Christina Sakellaridi added that “an entire year has passed since the capital controls were imposed without normality having been restored to the market. The only favorable impact is expected from the repayment of the state’s dues to private parties, the activation of the investment incentives law, the restoration of cheap liquidity flows to banks, the developments concerning bad loans and privatizations, and the attraction of new investments.”

“..absurd to talk about any threat coming from Russia at a time when dozens of people are dying in the center of Europe and when hundreds of people are dying in the Middle East daily..”

• Russia Hits Back At ‘Anti-Russian’ NATO ‘Hysteria’ (CNBC)

At a NATO summit in Warsaw, Poland on Friday, the military alliance is expected to formally agree to deploy four battalions with a total of 3,000 to 4,000 troops to the Baltic states (Estonia, Latvia and Lithuania) and Poland on a rotational basis. The deployment comes amid increasing concerns in those areas (all of which were under Soviet control during the Cold War) that Russia could be prepared to try to increase or regain its sphere of influence. In a statement on Thursday, NATO also said it would “strengthen political and practical cooperation with Ukraine, Georgia and the Republic of Moldova” – all former Soviet republics experiencing increasing tensions with Russia due to their political and economic relations with the EU.

In addition, the EU and NATO signed a declaration on Friday aimed at bolstering the region’s security ahead of the full NATO summit Friday afternoon. Left out in the cold from NATO and ostensibly the reason for such a deployment, Kremlin spokesman Dmitry Peskov reportedly hit back at the alliance, saying its actions were akin to “anti-Russian hysteria.” “If one needs badly to look for an enemy image so that [one can] promote anti-Russian, so to say, hysteria, and then, with this emotional background, to deploy more and more air force units, ground troop units, getting them closer to Russian borders, then one can hardly find any common ground for cooperation,” he was quoted by Russia’s Itar Tass news agency as saying.

Peskov was also quoted by Reuters as telling reporters that it was “absurd to talk about any threat coming from Russia at a time when dozens of people are dying in the center of Europe and when hundreds of people are dying in the Middle East daily,” adding that “you have to be extremely short-sighted to twist things in that way.”

Home › Forums › Debt Rattle July 9 2016