Russell Lee Sharecropper mother teaching children in home, Transylvania, LA. 1939

Really dumb stuff. If only because Trump loves it.

• Trump To Be Barred From UK Parliament Over ‘Racism and Sexism’ (BBG)

U.S. President Donald Trump must not be allowed to address the U.K. Parliament during a state visit to Britain, House of Commons Speaker John Bercow said. Prime Minister Theresa May invited Trump to visit the U.K., but there have been calls by lawmakers not to give the president the honor of addressing both houses of Parliament after he introduced a ban on people from some majority-Muslim countries traveling to the U.S. “Before the imposition of the migrant ban I would myself have been strongly opposed to an address by President Trump in Westminster Hall; after the imposition of the migrant ban by President Trump I’m even more strongly opposed,” Bercow told lawmakers on Monday.

He added, “I feel very strongly our opposition to racism and to sexism and our support for equality before the law and an independent judiciary are hugely important considerations in the House of Commons.” Trump’s predecessor, Barack Obama, and world leaders including Nelson Mandela, Angela Merkel and Pope Benedict XVI have all been invited to speak to members of the House of Commons and the House of Lords. [..] The announcement was greeted with cheers and – a rare event in the House of Commons – applause from the opposition benches. A motion arguing that Trump shouldn’t be invited to speak has been signed by 163 out of Parliament’s 650 members.

Bercow said he has a veto over a speech in Westminster Hall, the oldest part of the Houses of Parliament, and would block one. It would also be a breach with tradition if Trump spoke in the Royal Gallery behind the Lords without his name on the invitation, he said. “An address by a foreign leader to both houses of Parliament is not an automatic right, it is an earned honor,” Bercow said. “There are many precedents for state visits to take place to our country that do not include an address to both houses of Parliament.”

Meet Mario the kettle.

• Trump’s Wall Street Deregulation ‘The Last Thing We Need’ – Draghi (Ind.)

Donald Trump’s roll-back of Wall Street regulation is “very worrisome” and “the last thing we need” the President of the ECB, Mario Draghi, has warned. Giving evidence to the European Parliament’s Committee on Economic and Monetary Affairs on Monday, Mr Draghi was asked about the American President’s assault on the US post-crisis Dodd-Frank legislation, which had curbed the risk-taking of US banks, raised their capital requirements and introduced more safeguards for consumers. “The last thing we need is a relaxation of regulation,” Mr Draghi said. “The fact that we are not seeing….significant financial stability risk is the reward of the action of supervisors…. Nowadays financial intermediaries are strong. The idea of repeating the conditions of before the crisis is very worrisome.”

Mr Draghi added: “If we were to look at historical experience and ask what are the main reasons for the financial crisis starting in 2007 onwards, well, one can disagree [over] whether it was too expansive monetary policy or the dismantling of financial regulation in previous years – but surely we can agree it was a combination”. Last week President Trump signed an executive order to relax Dodd-Frank, prompting warnings that he is preparing the ground for another financial crisis. Phil Angelides, who served as chair of the Financial Crisis Inquiry Commission, branded President Trump’s decision “insane”. “In the wake of the financial crisis, millions of families lost their homes. Millions of people lost their jobs. The economy was wrecked and communities across the country were devastated. Big Wall Street banks admitted wrongdoing and paid tens of billions of dollars in fines. And now, with bankers at his side, President Trump begins to rip apart protections put in place to protect America’s families and our economy,” he said.

As I said a few dats ago: “More interesting right now is how strongly this is dividing the White House team. Kelly refused to enact some of Bannon’s demands. Tillerson and Mattis are not sitting comfortable either.”

• Meet The Men Who Could Topple Donald Trump (G.)

When Trump began putting together his cabinet, liberals and some in the media expressed concern over the number of retired generals he was appointing to top positions. “Trump hires third general, raising concerns about heavy military influence,” blared a headline in the Washington Post during the presidential transition. “I am concerned that so many of the president-elect’s nominees thus far come from the ranks of recently retired military officers,” the Democratic representative Steny Hoyer told the Washington Examiner in December. The fretting over Trump’s generals was always misplaced, not least because the number of retired generals Trump has appointed to top positions in his administration is hardly unprecedented.

Trump nominated the retired Marine generals James Mattis and John Kelly to lead the Department of Defense and Homeland Security, respectively, and tapped the retired army general Mike Flynn to be his national security adviser. When entering office after winning the 2008 presidential election, Barack Obama also appointed three retired generals to top positions and few batted an eyelid. But those concerned about Trump’s presidency should be thankful that the generals are there, particularly Mattis and Kelly. By all accounts, they are men of great honor and courage with strong backbones. Kelly led men into battle and lost a son fighting in Afghanistan. Mattis may be the most distinguished and respected Marine officer of his generation, revered for his dedication to his troops and his intellect. I had the honor of spending an hour with him one-on-one last May when he was a fellow at the Hoover Institution. Our conversation was off the record, but make no mistake, this is not a man to be trifled with.

Trump may have actually boxed himself in by picking highly respected generals such as Kelly and Mattis to helm top posts in his administration. Even conservatives who publicly stand by the president latch on to the appointments of Mattis and Kelly as their best evidence that Trump’s presidency will not be as problematic as his temperament and actions sometimes suggest, or some of his more troubling White House advisers portend. But if Mattis or Kelly were to resign in protest, that might change everything. There have already been reports that Mattis and Kelly are less than happy with some of what has gone on in the White House. During the transition, Mattis reportedly clashed with the Trump transition team over key appointments to the defense department. Tensions boiled over when Mattis and Kelly weren’t given sufficient consultation over the recent immigration executive order.

The Democratic representative Seth Moulton, a retired Marine who served under Mattis during the Iraq war, says insiders have informed him that after the executive order fiasco, some top appointments like Mattis began thinking about what would make them leave the administration. “What I’ve heard from behind the scenes,’’ Moulton told the Boston Globe: “What will make you resign? What’s your red line?”

This is the kind of confrontation the country badly needs. Where everyone has to argue and define their viewpoints.

• California Is Not ‘Out Of Control,’ Leaders Tell Trump (R.)

California leaders pushed back on Monday against President Donald Trump’s claim that the state is “out of control,” pointing to its balanced budget and high jobs numbers in the latest dustup between the populist Republican and the progressive state. The state’s top Democrats called Trump cruel and his proposals unconstitutional after the businessman-turned-politician threatened to withhold federal funding from the most populous U.S. state if lawmakers passed a so-called sanctuary bill aimed at protecting undocumented immigrants. “President Trump’s threat to weaponize federal funding is not only unconstitutional but emblematic of the cruelty he seeks to impose on our most vulnerable communities,” state Senate Pro Tem Kevin de Leon, a Democrat from Los Angeles, said in a statement on Monday.

State Assembly Speaker Anthony Rendon, an L.A.-area Democrat, said the state has the most manufacturing jobs in the nation, and produces a quarter of the country’s food. “If this is what Donald Trump thinks is ‘out of control,’ I’d suggest other states should be more like us,” Rendon said. The latest war of words between Trump and Democratic leaders in California, where voters chose his opponent, Hillary Clinton, two-to-one in November’s election, began Sunday, in an interview between Trump and Fox News host Bill O’Reilly. During the interview, O’Reilly asked Trump about a bill in the state legislature, authored by de Leon, to ban law enforcement agencies in the state from cooperating with immigration officials in most circumstances. Cities who have enacted similar bans are known as sanctuary cities, and de Leon’s bill, if passed and signed into law by Democratic Governor Jerry Brown, would effectively extend such rules to the entire state.

Trump disparaged the bill as ridiculous, saying that sanctuary cities “breed crime.” “We’ll have to, well, de-fund,” Trump said. “We give tremendous amounts of money to California.” Trump went on to say he viewed funding as a weapon. “California in many ways is out of control,” Trump said to O’Reilly. “Obviously the voters agree or otherwise they wouldn’t have voted for me.” Last week, Trump threatened to withhold federal funding from the University of California at Berkeley, where violent protests led to the cancellation of a speech by an editor for the right-wing Breitbart News. But experts said it would be difficult for the President to withhold funds from either the university or the state. Court rulings have limited the power of the president to punish states by withholding funds, and most appropriations come from the Congress and not the executive branch.

Really excellent. Don’t miss.

• Our Part In The Darkness (Alameddine)

Right after the election, my Twitter feed exploded with shock and moans. It seemed that everyone’s favorite phrase was “We are better than this.” I considered the statement so obviously wrong. I understood the convoluted logic of it, the jolt and hurt that would lead someone to type this, but it was not true. We are not better than this. We are this. The man was elected President. Ipso facto, America is this, we are this. I say this not to suggest that we must be blamed, or that someone who did not vote for Donald Trump is just as culpable as one who did. What I keep trying to point out, to friends, to anyone who will listen, is that too few of us are willing to acknowledge responsibility—not necessarily to accept blame, but to stand up and say, “This thing of darkness, I acknowledge mine.”

I remember when the photographs of torture at Abu Ghraib came to light. The response was similar. This is not us. Those soldiers were rotten. It began at the top, with George W. Bush, and it filtered down. But we would never do such a thing. Of course, we did do those things, and we kept on doing them over and over, and doing worse. Some objected, but most of us simply moved on, chose to forget. “No snowflake in an avalanche ever feels responsible,” the Polish poet Stanislaw Jerzy Lec once wrote. Trump bans Muslims and we claim that this is un-American, that we are not this. I don’t have to talk up “ancient” history to show that we are. I won’t bring up settler colonialism, genocide, and land theft, or harp on slavery, or internment camps for Japanese-Americans.

I won’t refer to the Page Act banning those deemed “undesirable,” the Chinese Exclusion Act, the Asiatic Barred Zone Act, or the Emergency Quota Act. I don’t have to mention the hundreds of thousands of Mexicans deported in the nineteen-thirties, or the thousands of Jews escaping Nazi violence who were turned away. It was F.D.R., not Trump, who claimed that Jewish immigrants could threaten national security. I won’t mention any of this, because this happened so long ago. We can always delude ourselves by saying that America was this but now we are better. Let me just say that in 2010 and 2011, state legislatures passed a hundred and sixty-four anti-immigration laws.

Many were upset when Trump campaigned on a Muslim registry, but I was surprised to find out how few knew that we’d already had one: the National Security Entry-Exit Registration System, or nseers, implemented on September 11, 2002. From the Atlantic: “It consisted of two ‘special registration’ programs: one that required foreign nationals from certain countries to check in with the government before entering and leaving the country, and another that obliged some foreigners living in the United States to report regularly to immigration officials.” Obama did not suspend the program until 2011. He dismantled it right before he left office.

[..] I was in Lesbos a year ago, helping Syrian refugees. At Moria, the biggest camp on the island, thousands of refugees were being processed every day. The crisis had been ongoing for more than six months. I’d heard that every big N.G.O. had taken a turn at leading the camp, but each one failed because of mismanagement, backstabbing, interagency bickering, governmental interference, what have you. But, as horrid as the situation was in the camp, I thought that it was being well managed, as well as it could be with so many people in and out. I met this unassuming man, a retired Mormon from Utah, who had been volunteering at the camp since the first boats arrived. He spoke no Arabic or Farsi, had no medical training of any kind, none of the identifiable skills, yet both volunteers and refugees sought him out with every conceivable question about what to do. It seems that he had arrived to offer whatever help he could. He slowly began to fill in wherever he was needed. As the N.G.O.s began to wash their hands of the camp, he was needed more and more. When I was there, he was running the damn place. We are this. We can be better.

“That is just a howling error, to talk about the number of jobs and wages as if they are different things.”

• The New York Times Just Doesn’t Understand This Economics Stuff (Worstall)

The Editorial Board of the New York Times tells us all that repealing parts of or all of Dodd Frank will damage the economic recovery. It’s possible to see the glimmerings of a point there, no one does think that if half the banks fall over again then all will be toodle dandy. However, they do manage to betray a terrible ignorance of the basics of economics and wages in the same editorial. Really, this is such a basic point that even Karl Marx was able to understand it: Mr. Trump may believe that ending Dodd-Frank will lead to more jobs by making it easier for businesses to get loans. But even if looser credit would help hiring — a very big if — the main problem in the job market today is not too few jobs, but wages that have been too low for too long. A rollback of Dodd Frank will not help that, and will hurt by forfeiting the stability that has helped the economy come this far.

That is just a howling error, to talk about the number of jobs and wages as if they are different things. They are the same thing–it is full employment which lifts the workers’ wages, nothing more and nothing less. As I say this is such a fundamental concept that even Karl Marx was able to get it right. If we have unemployment, that reserve army of the unemployed, then a capitalist can increase his labour force just by hiring some more of those unemployed. He doesn’t have to tempt anyone in with higher wages, he doesn’t need to pay his own workforce more as profits rise. For anyone gets bolshie he can just hire more of those unemployed people. However, the moment that reserve army is exhausted, the moment that there are no unemployed to hire it all changes. Suddenly, to gain access to more labour temptation must be employed.

It is necessary to tempt labour away from the jobs they are already doing. The capitalists, therefore, are in competition with each other for the profits that can be made by employment. At which point of course wages have to rise. To tempt labour into factory B away from factory A then B must pay more than A (in some form, could be shorter hours, better scheduling, more pay, whatever).And factory B had better raise its own wages for the extant workforce to stop A tempting it away. This is how wages rise over time. The capitalists compete for the profits that can be made by employing labour. And in the absence of unemployment they can only do this by raising wages as productivity rises. This process has been going on some 200 years by now, ever since productivity rises became a general feature of the economy.

And there’s no reason to think that it has stopped nor that it will. That is, contrary to the editorial board f the New York Times, it’s not that wages and jobs are different issues. It’s that wages haven’t risen because there haven’t been enough jobs. And seriously, if your understanding of capitalist and market economics is behind even that of Karl Marx are we sure that you should be writing newspaper articles on the subject of economics?

If you create an artificial recovery, there will be a price to be eventually.

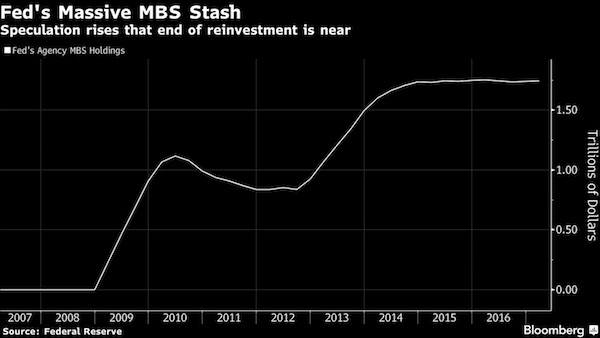

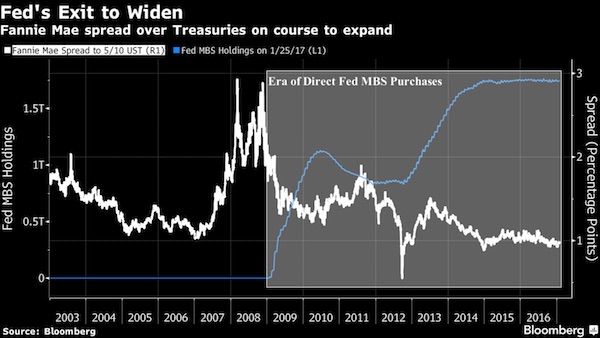

• The Fed’s Mortage-Bond Whale (BBG)

Almost a decade after it all began, the Federal Reserve is finally talking about unwinding its grand experiment in monetary policy. And when it happens, the knock-on effects in the bond market could pose a threat to the U.S. housing recovery. Just how big is hard to quantify. But over the past month, a number of Fed officials have openly discussed the need for the central bank to reduce its bond holdings, which it amassed as part of its unprecedented quantitative easing during and after the financial crisis. The talk has prompted some on Wall Street to suggest the Fed will start its drawdown as soon as this year, which has refocused attention on its $1.75 trillion stash of mortgage-backed securities.

While the Fed also owns Treasuries as part of its $4.45 trillion of assets, its MBS holdings have long been a contentious issue, with some lawmakers criticizing the investments as beyond what’s needed to achieve the central bank’s mandate. Yet because the Fed is now the biggest source of demand for U.S. government-backed mortgage debt and owns a third of the market, any move is likely to boost costs for home buyers. In the past year alone, the Fed bought $387 billion of mortgage bonds just to maintain its holdings. Getting out of the bond-buying business as the economy strengthens could help lift 30-year mortgage rates past 6% within three years, according to Moody’s. Unwinding QE “will be a massive and long-lasting hit” for the mortgage market, said Michael Cloherty at RBC Capital Markets. He expects the Fed to start paring its investments in the fourth quarter and ultimately dispose of all its MBS holdings.

Unlike Treasuries, the Fed rarely owned mortgage-backed securities before the financial crisis. Over the years, its purchases have been key in getting the housing market back on its feet. Along with near-zero interest rates, the demand from the Fed reduced the cost of mortgage debt relative to Treasuries and encouraged banks to extend more loans to consumers. In a roughly two-year span that ended in 2014, the Fed increased its MBS holdings by about $1 trillion, which it has maintained by reinvesting its maturing debt. Since then, 30-year bonds composed of Fannie Mae-backed mortgages have only been about a percentage point higher than the average yield for five- and 10-year Treasuries, data compiled by Bloomberg show. That’s less than the spread during housing boom in 2005 and 2006.

Don’t know if it’s money supply drying up or debts becoming overwhelming. Not the same thing. But the last paragraphs of the piece are interesting:

• When The Money Supply Dries Up (IM)

Whenever the ability to enforce draconian legislation goes into decline, the people of a nation suddenly realise that they’ve been living in fear of a paper tiger. It doesn’t take long before some people choose to defy the system. When they’re seen to succeed, others follow in droves. So, what does this say of the US and its power? Well, as Doug Casey has been known to say, “Countries fall from grace with remarkable speed.” Quite so. On an international level, this means that international leaders will be watching the economic decline of the US closely. Countries such as China and Russia have been loading up on precious metals in preparation for a collapse in fiat currency. In addition, they’ve created their own version of the World Bank, the Asian Infrastructure Investment Bank, and have been hard at work inking deals with other nations for international settlement in currencies other than the dollar.

Most people in the world today cannot remember a time before Bretton Woods, yet they may soon witness the Bretton Woods agreement becoming a dead duck. But, if we extend this premise, we also should be questioning the other constructs of the postwar period that have become dinosaurs. What of the United Nations? This organisation was once meant to be a body for arbitration and world planning, but has in latter decades become a quagmire of bickering and gainsaying—with its decisions rarely being adopted by the nations in question. And yet the US alone pays some $8 billion annually to keep the UN afloat. Surely, when the world at large ceases its willingness to carry further US debt, the US government will jettison the expense for the UN before it cuts either its military spending or its entitlement programmes.

Similarly, NATO, which requires $2.8 billion annually (with only five of its 28 members currently meeting the recommended payments) would experience a similar fate. With the above entities heading south, the Wolfowitz Doctrine, which has since 1992 been the basis of US aggression policy, would become unachievable. In addition to the decline or cessation of the above international adventurism, enforcement of revenue pursuit in the guise of FATCA and OECD schemes would equally suffer from a loss of funding. It would not be a question of whether the empire still wished to squeeze the lemon more than ever before—it would. But once the funds to do so dried up, the US and EU would find themselves in the situation that we currently observe in Venezuela: The money to pay for the enforcement is simply not there anymore.

The decline would begin with bounced cheques, followed by massive layoffs in the enforcement departments, followed by a decline in receipts, necessitating further layoffs, and continuing in a downward spiral. At present, countless people live in fear of the present empires and their ever-increasing efforts at usurpation. However, as history shows, once debt has reached its nadir and begins its rapid fall, so does the empire’s ability to enforce draconian confiscations.

Army vs veterans?!

• Army Corps Of Engineers May Decide On DAPL By Week’s End (BBG)

The U.S. Army may decide by week’s end whether to approve construction of the Dakota Access Pipeline across North Dakota’s Lake Oahe and lands claimed sacred by Sioux Indian tribes. Justice Department lawyer Matthew Marinelli outlined the planned timeline for the Army’s decision to a federal judge in Washington hearing a three-way dispute over the planned path of the Energy Transfer Partners LP-led project. Marinelli didn’t say which way the decision might go. President Donald Trump last month issued a memorandum urging the Army Corps of Engineers to expedite its review of the conduit’s path after the federal agency put the brakes on ETP’s nearly complete $3.8 billion, 1,172-mile conduit for shunting crude from northwestern North Dakota to a Patoka, Illinois, distribution center last year amid protests raised by environmental groups and the Sioux.

[..] While U.S. District Judge James Boasberg, and then a federal appeals court, declined to grant the tribes’ request for an order halting the project, the corps stopped construction anyway, stating it was reconsidering whether to issue easements required for tunneling under the lake bed. Jan Hasselman, lead lawyer for the suing Sioux tribes, told the judge that because the Army Corps had already committed to an environmental impact review of the lake crossing, any easement granted before that analysis is complete “would be unlawful.” The Corps turned the decision to the U.S. Army. The tribes will likely file a second bid to halt the project, citing environmental impact concerns, if the pipeline project gets a U.S. government go-ahead, Hasselman said.

Now use that to get a deal that actually achieves something.

• New Bill Would Block EPA From Regulating Greenhouse Gases (EW)

Republican lawmakers have proposed a bill to curtail the U.S. Environmental Protection Agency’s (EPA) ability to address climate change. The “Stopping EPA Overreach Act of 2017” (HR637) would amend the Clean Air Act so that: “The term ‘air pollutant’ does not include carbon dioxide, water vapor, methane, nitrous oxide, hydrofluorocarbons, perfluorocarbons, or sulfur hexafluoride.” The bill was introduced by Rep. Gary Palmer (R-Ala.) and has already racked up 114 Republican co-sponsors. Palmer is a climate denier who once said that temperature data used to measure global climate change have been “falsified” and manipulated.

Palmer’s latest proposal would nullify the EPA’s regulation of carbon pollution, stating that “no federal agency has the authority to regulate greenhouse gases under current law” and “no attempt to regulate greenhouse gases should be undertaken without further Congressional action.” Liz Perera, climate policy director at the Sierra Club, told Huffington Post that the resolution would make it nearly impossible for the federal government to fight climate change. “This is the legislative equivalent of trying to ban fire trucks while your house is burning,” she said, adding its sponsors “should be embarrassed for so blatantly ignoring reality and ashamed of themselves for so recklessly endangering our communities.”

[..] Fortunately, the bill does not seem to have any legs. David Doniger, a senior attorney for Natural Resources Defense Council’s climate and clean air program told The Guardian that HR637 does not have much of a chance breaking through a Senate filibuster as Democrats would have near-universal opposition to it and even some moderate Republican Senators would vote against it as well.

Yes. Annul the wedding. Before someone gets hurt.

• Too Late For Couples Therapy? (DiEM25)

For the past seven years, Greece has been stuck in an abusive marriage with its European partners. Of course, she has not been the perfect partner, but who has? No one deserves violence. No one deserves abuse. Everyone deserves hope, and not the delusional “you will be done by 2060, if you can maintain the hilariously unsustainable 3.5% primary budget surplus” kind of hope offered by Mr Schäuble. The hypocrisy and pseudo-morality of European lenders and the IMF is painful. Germany’s “no debt-reduction” stance is particularly exasperating, when that very same country has experienced both the economic, social and political disaster that vindictive, self-righteous hardheadedness can lead to after the Treaty of Versailles in 1919, as well as the miraculous quality of debt-reduction when its own debt was cut by half (!) at the London Debt Agreement of 1953.

The more years pass, the closer Greece and the rest of Europe edge from a post-modern 1919 to a post-modern 1933. And now, with news of Greece’s three-week window to resolve its next instalment before economically imploding – a piece of news which some media outlets appeared surprised about, bless them – many of us cannot help but wonder: when will we get serious about resolving this? The obvious answer is: when there is political will for a resolution. The only place where this seems to be the case is the nation-patient itself. Two summers ago, under remarkable socio-economic pressure, amid capital-controls and an overwhelmingly pro-EU media landscape, 62% of Greeks came out and refused the terms of a third bailout. Anyone with half-an-understanding of economics and finance seems to agree that the current approach to Greek debt is unsustainable economically, socially and politically: all in all, a disaster.

Even the master chef of the entire travesty, the IMF, has come out and admitted that neo-liberalism and austerity simply do not work. So what are we waiting for? Why are millions of Europeans still suffering under utterly misguided political and economic dogmas? Quite simply because to admit defeat at this point would mark the end of a number of powerful careers. Having poisoned European voters against the lazy PIIGS, it would be nothing short of political suicide to turn around and give in to Greek demands. When would be the next electoral victory in Europe for austerity’s architects if it was revealed that the years of financial and social suffering was a pointless self-inflicted wound with only negative economic results?

So it is becoming increasingly obvious that Greece has to work its own way out of this mess. At this stage, that means an immediate halt of repayments to lenders; a stance that will either force its partners to a vital debt-reduction, or will lead the country to an exit from the Euro. With Germany (in clear breach of EU rules) stubbornly maintaining its 9% budget surplus and refusing to increase imports, Europe is at an impasse, and no one is hurt more by this than Greece. Although the former outcome would be preferred – avoiding to rock the European boat at a time of major global instability is a major plus – the latter is still preferable to the status quo.

Translation of Greek article by Varoufakis I posted about earlier.

• Varoufakis: Tsipras Should Prepare To Break Deal With Greece’s Creditors (FR)

Through a recent article at the Efimerida ton Syntakton (Newspaper of Editors), the former Minister of Finance of Greece, Yanis Varoufakis, referred to Tsipras retreat against Greece’s creditors and called him to prepare seriously this time, to break the destructive continuous agreements. As Varoufakis wrote among other things: The night of the Greek referendum, I tried hard to explain to the Greek PM that the submission of Greece to the third memorandum was Schäuble’s real plan (not Grexit). In reality, there was no hope that the 3rd toxic “program” for Greece would be rationalized progressively through the support of the European Commission to Athens. Meaning, there was no hope that IMF’s austerity and anti-social measures could be softened.

The fact that Moscovici, Juncker, Sapin and others made such promises, is no excuse because the Greek government knew since May 2015 that these people know how to tell lies, or, they are unable to keep their promises when they don’t lie. Suddenly, the Schäuble-IMF-ECB attacked on Greece, demanding exhausting measures, while Merkel-Hollande-Commission didn’t do anything. Tsipras then retreated for one more time in order to “save” Greece. This was Schäuble’s plan. With his stance, Tsipras sank Podemos, made an approach with the collapsing (ethically and politically) Social Democracy, disappointed the progressive Europeans. And all these happened at the same time where nationalism triumphs everywhere.

Tsipras promises, one more time, that he will not retreat (this time!) by legislating new austerity even after 2018. If he means it, I remind him what we had agreed that is necessary and which – even today – is the only thing that may prevent the worst things to come. Prepare for unilateral restructuring of Greek bonds held by the ECB, which must be repaid in July (and after). Prepare the electronic system of transactions through Taxisnet which I had designed, I had started building it and even announced it to the new Minister of Finance, Euclid Tsakalotos, when I delivered the Ministry. Therefore, if indeed the Greek PM means it this time that he will not retreat, he should prepare for breaking the deal with the creditors, so that to prevent it. The design of a parallel system for payments is ready since 2014, as he knows.

Make it stop!

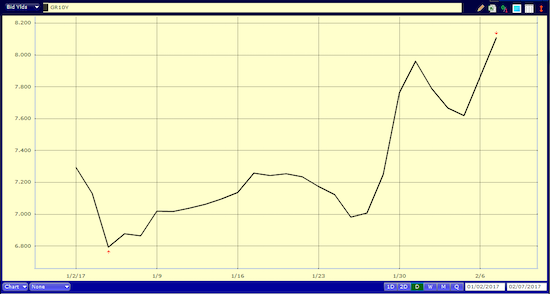

• Rare Split On IMF Board Puts Greek Bailout At Risk (MW)

Some members of the IMF are growing concerned with the terms of Greece’s bailout program, fueling fears the fund might pull out of the much-needed rescue plan for the country. The IMF’s annual review of the Greek economy published on Tuesday revealed a rare split among its board members, showing they are in disagreement over the austerity measures imposed on Athens and over the country’s huge debt burden. The report said that “most” of the 24 IMF executive directors agreed Greece is on track to reach a fiscal surplus of 1.5% of GDP. It said Athens does “not require further fiscal consolidation at this time, given the impressive adjustment to date.” However, some of the board members argued that Greece still needs to bring the surplus up to 3.5%, as agreed in the last bailout in 2015.

“Most Executive Directors agreed with the thrust of the staff appraisal, while some Directors had different views on the fiscal path and debt sustainability,” the IMF said in the assessment. The IMF usually keeps its deliberations confidential, so any differences on the board are rarely exposed to the public. The yield on 10-year Greek government debt surged 26 basis points after the report on Tuesday to 7.925%, according to electronic trading platform Tradeweb. Economists consider borrowing costs above 7% unsustainable in the long term.

This is getting sadistic.

• Greece Won’t Meet Fiscal Surplus Targets Set By Europe, IMF Says (BBG)

Greece is on track to fall short of budget-surplus targets set under a bailout by the nation’s euro-zone creditors, the IMF said. Greece’s primary budget surplus will rise to 1.5% over the long run from about 1% last year, amid a modest recovery, the IMF said Monday after executive directors met to discuss the fund’s annual assessment of the nation’s economy. Still, the projected surplus falls short of the 3.1% forecast by the country’s European creditors. The fund reiterated its view that Greece’s debt is unsustainable. Most of the executive directors don’t believe the economy needs more fiscal consolidation, the IMF said. The IMF has said it would consider giving Greece a new loan to supplement the 86 billion euros ($92 billion) it’s receiving from euro-area countries, but only if the nation’s debt-reduction plans are credible.

Greece’s European creditors also want the IMF to sign off before disbursing the next tranche of the euro-zone bailout. Greece’s government debt will reach 275% of its gross domestic product by 2060, when its financing needs will represent 62% of GDP, the IMF said in a draft staff report obtained by Bloomberg last month. Public debt will reach 181% of GDP this year, the IMF projected Monday. Greece’s economy is expected to grow 2.7% this year, up from 0.4% in 2016, the fund said. However, long-run growth is expected to slip to about 1%, the IMF predicts. The IMF’s assumptions aren’t based in reality and don’t take into account the reform of Greece’s public finances, according to a European Union official who spoke on condition of anonymity because the discussions are sensitive.

Yeah, sure, add some more crap. For some reason this makes me think of George Clinton: “Do Fries Come With That Shake?”

• Third Quake Over 5-Richter Magnitude Rattles Lesbos (K.)

Seismologists in Greece are keeping a close eye on activity in the eastern Aegean, as a third quake in 24 hours measuring above 5 Richter rattled the area in the early hours of Tuesday. The tremor hit at 4.24 a.m. and measured 5.3 on the Richter scale, according to the Geodynamic Institute in Athens, with the epicenter located 15 kilometers north of Lesvos. With a depth of just 10 kilometers, the quake was felt quite strongly on the Greek islands of Lesvos and Chios. Seismologist Efthimios Lekkas on Monday said two tremors – with a magnitude of 5.1 and 5.3 respectively – were not linked to the North Anatolian Fault Line, the source of powerful quakes in the past.

Home › Forums › Debt Rattle February 7 2017