DPC Chamber of Commerce, Boston MA 1904

“The scales will soon lift from the market’s eyes.”

• Deflation Risk in U.S. Seen Rivaling Euro Area (Bloomberg)

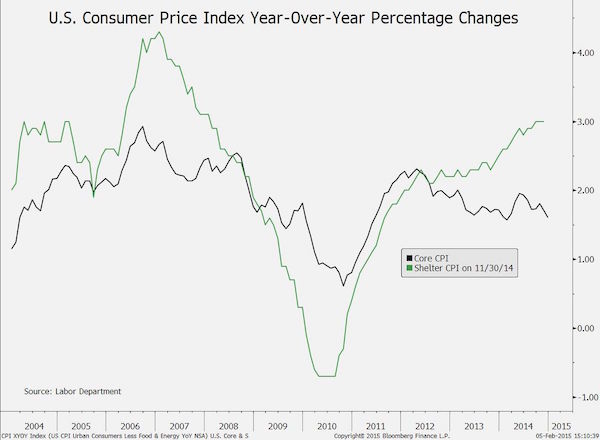

Deflation would be as much of an issue for the U.S. as it is for the euro region if consumer prices were tracked the same way, according to Albert Edwards, a global strategist at Societe Generale SA. The Chart Of The Day helps illustrate how Edwards drew his conclusion, presented in a report yesterday. He tracked changes in the core U.S. consumer-price index, which excludes food and energy, and the CPI for shelter. Core inflation in December was 1.6%, according to the Labor Department. That’s 0.9 percentage point more than the euro region’s comparable figure, as compiled by Eurostat. This gap disappears after bringing the U.S. figure into line with Eurostat’s definition of housing, Edwards wrote.

“The deflationary fault line on which the U.S. sits is every bit as precarious as that of the euro zone, but is being disguised,” the London-based strategist wrote. “The scales will soon lift from the market’s eyes.” Ten-year Treasury notes are headed for yields of less than 1% as the deflation threat grows, according to Edwards. The yield stood at 1.81% yesterday after ending last month at 1.64%. The adjusted U.S. data exclude owners’ equivalent rent, or the estimated cost borne by homeowners who live in their houses as opposed to renting them out. The euro region doesn’t have a similar category.

“U.S. numbers differ because they are measured with “shelter inflation” which is derived from housing costs based on rent, not the price of homes.”

• Stocks Will Be ‘Ripped To Smithereens’: Albert Edwards (CNBC)

Societe Generale’s notoriously bearish strategist, Albert Edwards, has warned that the deflation threat currently dogging the euro zone is greater in the U.S. and that equity markets will soon be “ripped to smithereens.” “The deflationary fault line on which the U.S. sits is every bit as precarious as that of the euro zone, but is being disguised,” he said in a new research note on Thursday. “The scales will soon lift from the market’s eyes.” Despite years of central bank easing, consumer price growth across the world has begun to stagnate with the euro zone recently falling into deflationary territory – when consumer price growth turns negative. An official flash figure for the 19-country region last week showed prices fell by 0.6% year-on-year in January.

Across the Atlantic, consumer prices increased 0.8% in the 12 months through December, the weakest reading since October 2009. The U.S. might be posting better figures than the euro zone, but Edwards argues that it’s not a like-for-like comparison. “My former esteemed colleagues Marchel Alexandrovich and David Owen pointed out to me that if U.S. core CPI (consumer price index) is measured in a similar way to the euro zone, then U.S. core CPI inflation is already ‘pari passu’ (on an equal footing) with the euro zone despite the former having enjoyed a much stronger economy,” he said. He adds that U.S. numbers differ because they are measured with “shelter inflation” which is derived from housing costs based on rent, not the price of homes.

This has been preventing U.S. core CPI from falling away sharply, to the extent that it has in the euro zone, according to Edwards. With this warning, Edwards now believes that there is “ample room” for global yields to fall further over the next two years. He believes that market participants will see sub-1% yields on the U.S. 10-year sovereign, down from its current level of 1.8015%. Edwards regularly touts the idea of an economic “Ice Age” in which equities will collapse because of global deflationary pressures. On Thursday he maintained his view that equities are likely to fall below 2009 lows. “I remain confident that the global equity markets will be ripped to smithereens in the next economic downturn which will, once again, show that the central banks have inflated another massive unstable financial bubble,” he said. “The market is far too convinced that the U.S. is in the spring of its economic recovery, whereas I believe we could well be in the autumn.”

“Kilduff said that the industry had merely gotten rid of “the runts of the litter..”

• Oil Heading For $30, Currency War Coming (CNBC)

So much for the rally. Oil will likely still head as low as $30, analyst John Kilduff told CNBC on Thursday. “I still believe we’re going to go to that $30 to $33 area, which is the low point from the financial crisis in 2008, 2009. What you saw over the past several days was technical in nature, a short squeeze. This volatility is a little crazy and I think that $30 target is a downside target is for technicians that are in this market,” the founding partner of Again Capital said in a “Squawk Box” interview. U.S. crude tumbled 9% on Wednesday to settle at $48.45, erasing nearly all of its gains in the previous two sessions. The benchmark commodity – West Texas Intermediate – had soared 22% from a nearly six-year low of $43.58 last Thursday, ending the day at $53.05 on Tuesday.

The rally’s sharp reversal spilled over into the stock market, with energy stocks leading the day’s decline in the S&P 500. Data on Friday that showed exploration and production companies had shut down 90 rigs in the prior week boosted the rally. Kilduff said that the industry had merely gotten rid of “the runts of the litter,” noting that U.S. production had not fallen and still stands at 9.1 million barrels a day. He said speculation that Saudi Arabia, the world’s largest oil exporter, would agree to production cuts in order to reach a deal with Russia on the Syrian conflict also sent oil higher.

It has no choice.

• Is China Preparing for Currency War? (Pesek)

China has entered the global monetary-easing fray, along with more than a dozen other economies, after its central bank surprised investors by cutting reserve requirements 50 basis points to spur lending and combat deflation. But Beijing may be raring for an even bigger and more perilous fight – in the currency markets. Reducing the amount of cash that banks are required to set aside (to 19.5%), as China has just done, is largely symbolic – a don’t-panic-we’re-on-top-of-things reassurance to international markets and local property developers. Still, the move is also an inflection point. China is in all likelihood about to loosen monetary policy considerably to support economic growth. If global conditions worsen, China’s one-year lending rate, now at 5.6%, could head toward zero.

At the same time, something else is afoot in Beijing could have even greater global impact. The central bank is cooking up measures to widen the band in which its currency trades. People’s Bank of China officials say it’s about limiting volatility as capital zooms in and out of the economy. Let’s call it what it really is: the first step toward yuan depreciation and currency war. As China grapples with its slowest growth in 24 years, President Xi Jinping is under pressure to stimulate the economy. Yet that would run afoul of his pledges to curb runaway debt and credit (the latter jumped about $20 trillion from 2009 to 2014). What better way to gin up growth without adding to China’s bubbles than by sharply weakening the exchange rate?

A cheaper yuan would boost exports and buy Xi more time to recalibrate growth engines away from excessive investment and debt. “The real economy desperately needs a weaker yuan,” says economist Diana Choyleva of Lombard Street Research. The question is, does the rest of the world? Any significant drop in the yuan would prompt Japan to unleash another quantitative-easing blitz. The same goes for South Korea, whose exports are already hurting. Singapore might feel compelled to expand upon last week’s move to weaken its dollar. Before long, officials in Bangkok, Hanoi, Jakarta, Manila, Taipei and even Latin America might act to protect their economies’ competitiveness.

David Stockman sent me a mail last night pointing out we had written on the same topic yesterday: “Perhaps there truly is such a thing as “great minds thinking”………..etc.” My inevitable reply: “That IS funny, yeah. You’ll never see me thinking of myself as a great mind, though (you, different story altogether), I’m just an outsider describing the crash to all the other outsiders.” See also: Debt In The Time Of Wall Street.

• China’s Monumental Debt Trap – Why It Will Rock The Global Economy (Stockman)

Bloomberg News finally did something useful this morning by publishing some startling graphs from McKinsey’s latest update on the worldwide debt tsunami. If you don’t mind a tad of rounding, the planetary debt total now stands at $200 trillion compared to world GDP of just $70 trillion. The implied 2.9X global leverage ratio is daunting in itself. But now would be an excellent time to recall the lessons of Greece because the true implications are far more ominous. Today’s raging crisis in Greece was hidden from view for many years in the run-up to its first EU bailout in 2010 because the denominator of its reported leverage ratio – national income or GDP – was artificially inflated by the debt fueled boom underway in its economy.

In other words, it was caught in a feedback loop. The more it borrowed to finance government deficit spending and business investment, whether profitable or not, the more its Keynesian macro metrics – that is, GDP accounts based on spending, not real wealth—-registered a falsely rising level of prosperity and capacity to carry its ballooning debt. Five years later, of course, the picture is much different. Greece’s GDP has now shrunk by more than 25%. The abysmal picture depicted in the graph below explains what really happened. Namely, that the bloated denominator of GDP came crashing back to earth, exposing that Greece’s true leverage was dramatically higher than the 100% ratio reported in the years before the crisis.

“They receive only about half of China’s total tax revenue, while they must pay for 80% of all government expenses..”

• Conquering China’s Mountain of Debt (Bloomberg)

Close the back door, open the front door. That s the official slogan used to describe China s most ambitious reform of government finances in two decades, to be introduced later in 2015. The aim is to wean badly indebted local governments tens of thousands of cities, counties, and townships off their dangerous reliance on off-balance-sheet financing and backdoor borrowing, from both banks and the unregulated shadow finance sector. Funds to support China s rapid urbanization to build infrastructure, keep pension programs solvent, and more will come from a vastly expanded, newly legalized local bond market.

The development of a local bond market is a real milestone, says Debra Roane, senior credit officer at Moody’s Investors Service. Once local governments start issuing debt in their own name, it will be clear that they are responsible for it, and that will ultimately lead to more prudent decision- making. They will stay away from riskier projects. Ever since China’s last major fiscal reform in the mid-1990s, when then-Vice Premier Zhu Rongji restored control of public finances to the national government, local governments have faced a dilemma. They receive only about half of China’s total tax revenue, while they must pay for 80% of all government expenses, including schools, roads, and health care. The local governments are banned from borrowing directly from banks and from issuing bonds.

As a result, a vast, unregulated industry has sprung up in what many call local government finance vehicles. Some 10,000 of these for-profit finance companies raise funds for local needs. They also have enabled local authorities to commit acts of apparent folly. The finance companies, with the implicit backing of local governments, bankrolled entire new city districts that now sit largely empty. This has led to a very opaque and risky situation, with unclear accountability, Roane says. It s not clear who is responsible for all this debt. China’s officially stated deficit is about 2% of its gross domestic product. That’s a fiction, says Chen Long, China economist at researcher GavekalDragonomics in Beijing, because it doesn’t include any of this indirect local borrowing. Add it in and the deficit rises to about 5% of GDP, Chen estimates. The National Audit Office found that as of 18 months ago, local debt including indirect borrowing totaled 17.9 trillion yuan ($2.86 trillion), up 63% since the end of 2010, much more than the 40% expansion of the economy.

As Tsipras said (paraphrased) : “And we didn’t even kill anyone”.

• The Debt Write-off Behind Germany’s ‘Economic Miracle’ (France24)

When discussing Greece’s whopping $310 billion debt, the country’s new Prime Minister Alexis Tsipras likes to recall a time when Europe’s great debt offender was not Greece, but Germany, today’s paragon of fiscal responsibility. The leader of the radical-left Syriza party refers in particular to an international conference held in London in 1953, during which West Germany secured a write-off of more than 50% of debt, accumulated after two world wars. Back then, with memories of Nazi atrocities still fresh, many countries were reluctant to offer such generous debt relief. But the US persuaded its European allies, including Greece, to relinquish debt repayments and reparations in order to build a stable and prosperous Western Europe that could contain the threat from Soviet Russia.

“Tsipras is right to remind Germans how well they were treated, with both debt relief and money from the Marshall Plan,” says Professor Stephany Griffith-Jones, an economist at Columbia University, referring to the US programme to help rebuild European economies after World War II. She believes Greece is justified in demanding a more generous approach from its creditors, despite obvious differences between its current plight and that of war-ravaged Germany. “In fact, Greece’s situation is perhaps more urgent because the pressure from markets and the financial sector is so much stronger than in the 1950s,” she says.

West Germany’s debt at the time was well below the levels seen in Greece today. But German negotiators successfully argued that it would hinder efforts to rebuild the country’s economy – much as Greek governments have in recent years, in vain. Under a crucial term of the London Agreement, repayments of the remaining debt were made conditional on West Germany running a trade surplus. In other words, the German government would only pay back its creditors when it could afford to – and not by borrowing even more money. Reimbursements were also limited to 3% of export earnings. This gave Germany’s creditors an incentive to import German goods so they would later get their money back, thereby laying the foundations of the country’s powerful export sector and fostering its so-called “economic miracle”.

“Germany’s resurgence has only been possible through waiving extensive debt payments and stopping reparations to its World War II victims,” economic historian Albrecht Ritschl told Der Spiegel in 2011, describing Germany as “the biggest debt transgressor” of the past century. “During the 20th century, Germany was responsible for what were the biggest national bankruptcies in recent history,” Ritschl said, pointing to the collapse of the German economy in the early 1930s, which sent shockwaves through global markets. “It is only thanks to the United States, which sacrificed vast amounts of money after both World War I and World War II, that Germany is financially stable today and holds the status of Europe’s headmaster. That fact, unfortunately, often seems to be forgotten.”

“If DB is right, and if Europe folds, the question then is what concessions will the ECB and the Eurozone be prepared to give to Italy, Spain and all the other nations where anti-European sentiment has been on a tear..”

• Why Deutsche Bank Thinks Europe Will Fold (Zero Hedge)

The Greek situation summaries Greece by Deutsche Bank’s George Saravelos have consistently been among the best in the entire sellside. His latest Greek update, which is a must read for anyone who hasn’t been following the fluid developments out of southeast Europe, which fluctuate not on an hourly but on a minute basis, does not disappoint. But while his summary of events is great, what is of far greater significance is his conclusion, namely that ultimately Europe will fold: “we consider the most likely outcome to be a Eurogroup offer of a new Third program” and “given that the current program expires this February the offer to negotiate a new Third program may provide political room for the government to sit on the negotiating table.

At the same time such an offer is very likely to be attached to strict conditions, with the willingness to accommodate t-bill issuance an open question. Developments overnight suggest that this has become less likely, imposing maximum pressure on the government to reach agreement within a matter of weeks.” If DB is right, and if Europe folds, the question then is what concessions will the ECB and the Eurozone be prepared to give to Italy, Spain and all the other nations where anti-European sentiment has been on a tear in recent months, and especially in the aftermath of Syriza’s stunning victory.

From Deutsche Bank: Greek Update

Over the last couple of weeks we have framed developments in Greece around three questions:

• First, under what conditions would the Troika be willing to continue negotiating with Greece?

• Second, does the Greek government accept these conditions?

• Third, how does the ECB link Greek bank financing to program negotiation?

“The ECB’s kneecapping of Greece demonstrates how central banks act as powerful enforcers on behalf of lenders and investors. The ECB operates with no concern that it will be reined in by democratic governments..”

• Time for #GreekLivesMatter (Naked Capitalism)

If you are not part of the solution, you are part of the problem. The Troika’s willingness to turn Greece into a failed state first, as a side effect of its “rescue the French and German banks” operation, and now, as part of its German hegemony protection racket, is killing people and in the longer term will only accelerate the rise of extreme right wing elements in the Eurozone. As Ilargi wrote last week:

In what universe is it a good thing to have over half of the young people in entire countries without work, without prospects, without a future? And then when they stand up and complain, threaten them with worse? How can that possibly be the best we can do? And how much worse would you like to make it? If a flood of suicides and miscarriages, plummeting birth rates and doctors turning tricks is not bad enough yet, what would be?

If you live in Germany or Finland, and it were indeed true that maintaining your present lifestyle depends on squeezing the population of Greece into utter misery, what would your response be? F##k ‘em? You know what, even if that were so, your nations have entered into a union with Greece (and Spain, and Portugal et al), and that means you can’t only reap the riches on your side and leave them with the bitter fruit.

[..] Please circulate this post widely and tweet it, using #GreekLivesMatter. If you live in a city where a central bank is located, get this idea in front of organizers. They can no doubt adapt and improve upon it. And above all, send it to all the Greeks you know, even those in Greece who might send it on to friends and family in the diaspora. If you are in the US, please contact your Congressman and express your dismay that the Fed is tacitly supporting the ECB in its reckless and destructive Eurozone policies and has the stature and the leverage to weigh in. Remember, many Republicans are as unhappy with the lack of transparency and undue concentration of power at the Fed. Even a small step supporting this effort is a step in the right direction.

“We didn’t even agree to disagree from where I’m standing..”

• Greek Leaders Return Home for Rethink After Rebuff From Germany (Bloomberg)

Prime Minister Alexis Tsipras is preparing to set out the most detailed account yet of his plans to revive the Greek economy after a diplomatic push ended with a rebuff from Germany and a warning shot from the ECB. Tsipras was greeted by the rare sight of a pro-government demonstration in downtown Athens on Thursday night after he vowed to stick to his anti-bailout campaign pledges, despite their rejection by German Finance Minister Wolfgang Schaeuble. The prime minister will lay out his policy plans on Sunday, in the opening speech of the three-day-long parliamentary debate leading up to a confidence vote to confirm his government.

Ministers met in Athens on Thursday to discuss the policy program and may reconvene on Saturday to assess Finance Minister Yanis Varoufakis’s feedback from his meeting with Schaeuble in Berlin. The first direct talks between Greece and Germany since Tsipras took power yielded no agreement on how to narrow their differences over Tsipras’s determination to end the German-led austerity regime. “We agreed to disagree” Schaeuble said after meeting Varoufakis on Thursday. “We didn’t even agree to disagree from where I’m standing,” the Greek responded.

A few hours before the Berlin encounter, the ECB heaped pressure on Tsipras by restricting Greek access to its direct liquidity lines, citing concerns about the country’s commitment to existing bailout pledges. The Greek government opted to “stop cooperating with the troika,” ECB Governing Council member Jens Weidmann said in a speech in Venice on Thursday. The move leaves Greek banks reliant on €59.5 billion of Emergency Liquidity Assistance, extended by the Bank of Greece, which is subject to review by the ECB Governing Council every two weeks. Undeterred by the ECB reaction, which triggered a sell-off in Greek bank shares, Tsipras told lawmakers from his party, Syriza, that he intends to stick to his campaign promises. “The government will negotiate hard for the first time in years, and will put a final end to the troika and its policies,” Tsipras said.

As Tsipras was speaking, hundreds gathered outside the parliament building to protest against the ECB’s decision, labeling it “blackmail.” Unlike the riots which rocked the Greek capital in 2011 and 2012, the march was peaceful and evening news bulletins dedicated more time to the fact that Syriza lawmakers opt not to wear ties than to the market declines, which saw bank stocks lose 10%. Sakellaridis said that Tsipras’s visits to Nicosia, Rome, Paris and Brussels this week had yielded results and the government isn’t alarmed about the potential impact of the ECB decision. Central bank governor Yannis Stournaras said the ECB decision “can be reversed” and the outflow of banking deposits is “under control.” “It was a very quiet day today,” he said, after meeting Deputy Prime Minister Yannis Dragasakis.

Allow?! If it walks feudal, and quacks feudal…

• ECB Said to Allow Greek Banks €59.5 Billion Emergency Cash (Bloomberg)

The European Central Bank will allow the Greek central bank to provide as much as €59.5 billion in emergency funding for the country’s lenders, a euro-area central-bank official familiar with the decision said. The measure is needed after the ECB shut off a key avenue for Greek banks’ funding on Wednesday, citing doubts that the country’s newly elected government will conclude its aid program. Greek stocks and bonds fell on Thursday after the ECB’s decision to end a waiver on the quality of Greek debt it accepts as collateral. The offer highlights how ECB officials are warning Greek politicians to keep to euro-area rules while striving to avoid a crisis in the financial system.

The ECB approved €50 billion in ELA as a replacement for its regular funding, plus an extra €9.5 billion, the official said, asking not to be identified because the proceedings aren’t public. German newspaper Die Welt reported earlier on Thursday that the ECB would allow the Greek central bank to offer about €60 billion in ELA. Under the measure, a nation’s central bank can provide liquidity to lenders at its own risk. The ECB will review ELA every two weeks to check whether the funds are being used in a way that doesn’t interfere with monetary policy. Should the ECB object, “the bank concerned cannot fund itself and that the bank concerned the same day or in the next couple of days would miss a payment and the counterpart will call a bankruptcy,” Governing Council member Klaas Knot said at the Dutch parliament in The Hague on Thursday. “So you have a credit event,” he said, while declining to comment specifically on Greece.

“Everyone wants to live in fairyland and none of us want to go back to real economies [..] This is nice theater, but it’s not going to solve anything.”

• Greek Debt Drama Is ‘Theater,’ But Stakes Are High (CNBC)

The ongoing drama surrounding Greece’s efforts to drum up support for a new debt deal is just “theater,” according to one analyst, who warned that Europe needs to wake up. Greek Finance Minister Yanis Varoufakis met his German counterpart Wolfgang Scheuble in Berlin on Thursday, after a week of travelling across Europe to try and bolster support for a new debt deal and bailout conditions. The talks were a mixed success, however, with Scheuble saying that the ministers had “agreed to disagree,” but Varoufakis denying that this was the case. Satyajit Das, author of “Traders, Guns & Money” told CNBC Friday that the talks were symptomatic of a “make-believe world.”

“Everyone wants to live in fairyland and none of us want to go back to real economies,” he said. “This is nice theater, but it’s not going to solve anything.” With no apparent progress over a debt deal for Greece, despite a week of high profile meetings between Varoufakis and Greek Prime Minister Alexis Tsipras and their fellow euro zone ministers, there is growing speculation over the eventual outcome. Das, an expert on financial derivatives and risk management, went on to stress that Greece’s “underlying dynamics” hadn’t changed. “They still can’t pay back their debt and we haven’t fixed anything. We still have to fix the basic economy,” he said. “The fundamental thing is that the Greeks want to be in the euro, they want to get this relief. The Germans want to save the German banks and the French want to save the French banks –they don’t want to have write-offs.” [..]

Panicos Demetriades, former governor of the Central Bank of Cyprus, told CNBC Friday that a “game of chicken” was being played out between the Greeks and Germans. And he added that an agreement over Greece was needed sooner rather than later in order to maintain confidence in the Greek financial system. “The Greeks have done everything possible to gain support for their positions, which are not unreasonable as the program doesn’t seem to be producing what was expected of it,” he told CNBC. “But they really don’t have the time that they think they do – that time isn’t there.” Demetriades, professor of financial economics at the University of Leicester, said that the ECB move was a symptom of deposit outflows in Greece. “Depositors are getting nervous. Even a small chance of the euro area breaking up would leave them in a mess,” he said. “It is important that the Greek government understands that if there is no agreement soon things will progressively get worse for them.”

“Varoufakis’s plea for “space for all of us to come to an agreement” sounds no more than common sense.”

• Greece and Varoufakis Need Supporters Not Sympathisers (Guardian)

What has Yanis Varoufakis, Greece’s finance minister, achieved during his grand tour of European capitals this week? Not much. He has collected a few rave reviews for his dress sense and sounded a model of sweet reasonableness in his press conferences. But on the substance? Yesterday in Berlin Wolfgang Schäuble, Germany’s finance minister, said Greece’s European partners had already gone as far as they would go on debt relief. He invited Athens to help itself. Varoufakis was left in the odd position of disputing Schäuble’s assertion that the pair had agreed to disagree. Over in Frankfurt, the ECB cranked up the pressure on Greece by yanking its banks’ access to cheap funding: Greek government bonds will no longer be accepted as collateral.

The banks can still get emergency liquidity by going through Greece’s central bank. But they will pay a higher rate of interest for that dubious privilege. What’s more the central bank’s ability to keep the funds flowing is not endless because the ECB can impose limits. The message behind the ECB’s decision seemed clear: we will play hard; we are not about to change our rules of engagement; the time for Greece’s new Syriza government to face reality is fast approaching. Indeed, the end of this month now looms as a real, and dangerous, crunch-point. Syriza has said it wants to exit the bailout programme and argues for a three-month bridging loan to allow time for negotiations. The message from Shäuble was a firm no to the loan. A stand-off between Syriza and the eurozone powerhouses was always in the offing but the positions are now stark. Something has to give here – and quickly.

In a rational world, a bridging loan would be an excellent idea. Attempting to resolve the Greek mess via brinkmanship in the space of three weeks is madness. Remaining depositors in Greek banks will be fleeing. Varoufakis’s plea for “space for all of us to come to an agreement” sounds no more than common sense. Extending finance to Athens until the end of May would not cost much. If the ECB is restricted by its mandate, politicians could always find a pragmatic fudge; they have done so many times in the past. But that is not the way the winds are blowing. Even François Hollande in France and Matteo Renzi in Italy called the ECB’s move legitimate and said it was a way to force agreement. The eurozone’s big beasts seem determined to force a quick resolution, rather than accept Syriza’s timetable.

Socialist punk banker.

• The Lazard Banker Shaping Greece’s and Ukraine’s Financial Fate (WSJ)

Europe’s financial future may hang in the balance in an office on Paris’s Boulevard Haussmann that belongs to a French banker with a taste for punk rock. Matthieu Pigasse is a self-described pro-market socialist and fan of The Clash. The 46-year-old financier is also head of the government advisory arm at Lazard , the international investment bank hired in recent days by both Greece and Ukraine to help renegotiate their debts, according to people familiar with the matter. Mr. Pigasse “has been involved in some of the most important sovereign-debt restructurings in the last decade,” said Deborah Zandstra, a sovereign-debt partner at lawyers Clifford Chance LLP. “His appointment by the new Greek administration is a positive step.”

Both assignments are key to Europe’s political and economic health. Ukraine must negotiate with foreign creditors over as much as $20 billion of Eurobond debt. These efforts could be crucial in whether Ukraine is able to negotiate further loans and keep its budget afloat, bolstering an economy ravaged by the conflict with Russian-backed rebels in the east. In Greece, new Prime Minister Alexis Tsipras has promised to slash the country’s heavy debt burden. But other eurozone leaders have declared that any reduction in the face value of Greek debt would be unacceptable and the Greek finance minister is now proposing to swap debt for new growth-linked bonds. For Lazard, an advisory and asset management firm that listed in New York in 2005, counseling governments has become a steady and growing business.

A team of Lazard bankers, led by Mr. Pigasse, advised Greece in 2012 when it pushed through one of the largest debt restructurings of all time. Lazard has also been very active in Africa, where it has advised Egypt, Mauritania, the Democratic Republic of Congo, Gabon and Ivory Coast. Last year it helped Ethiopia with its debut $1 billion sovereign-bond issue. Advising governments is a relatively small part of Lazard’s business, with fees making up just a small fraction of total revenue. But government mandates are particularly prestigious and the work can be lucrative. In March 2012, Greece said it paid Lazard €25 million for its advice over the previous two years. The sovereign-advisory arm, run out of the Paris office, has increased head count by 50% to 30 over the past three years.

“All their expenses are paid, and they have no capital at risk. This is as sweet as it gets.”

• Banker to the Broke: Lazard Advises Greece, Ukraine (Bloomberg)

When the government goes broke, the broke call Lazard Ltd. While Lazard is best known for mergers and acquisitions, the firm has found lucrative work advising governments in two of the world’s current economic trouble spots: Greece and Ukraine.

The roles are in keeping with Lazard’s long – and not always successful – history as a top adviser to cash-strapped governments. Argentina, Egypt, Indonesia, Iraq, Ivory Coast: all have turned to Lazard over the years. So did New York City, back in the 1970s. It’s nice work for Lazard, which gets to collect fees no matter how things play out for a government or its creditors. “This is a very high-margin business,” said William Cohan, a former Lazard banker and author of a book on the firm. “All their expenses are paid, and they have no capital at risk. This is as sweet as it gets.”The Lazard team, led by Paris-based banker Matthieu Pigasse, advised a previous Greek government during the nation’s last major financial crisis, when an exit from the euro currency area loomed as a possibility if talks failed. Last week, the nation’s new government hired Lazard to help again as the country seeks to ease the pressure from a debt load of about €315 billion. Ukraine is also working with Lazard, according to people familiar with the situation. Based officially in Bermuda with major offices in Paris and New York, Lazard faces challenges with both of those assignments. The newly elected Greek government of Alexis Tsipras has pledged to increase wages, halt public-sector layoffs and cancel planned asset sales – all part of a package of structural reforms demanded by creditor states including Germany.

Finance Minister Yanis Varoufakis is weighing plans to trade existing debt for new bonds pegged to economic growth, after a proposal to impose a loss of capital on creditors met opposition. Ukraine, for its part, was struggling to meet debt payments even before what the U.S. and European Union say is a Russian-backed rebellion in its eastern regions began last year. It’s now seeking to avert default after its economy shrank an estimated 7.5% in 2014 amid the fighting. Russia, which annexed Ukraine’s Crimea peninsula in March, denies involvement in the conflict. Payments to advisers are determined by the size of the debt reduction and the degree to which creditors participate, and Lazard earned as much as €25 million over two years for previous Greek work, the government said in 2012.

it’s a pattern, not a design flaw.

• Abenomics Leaves Japan’s Poor and Elderly Behind (Bloomberg)

Hiroyuki Kawanishi’s tiny two-room flat in Tokyo may not be much, but it’s home. With Prime Minister Shinzo Abe trimming benefits for the poor as he increases spending on the military and cuts corporate taxes, it may not be for long. “If the housing subsidy is cut, I’ll lose my apartment,” said Kawanishi, 42, who was born with cerebral palsy and can barely fit his wheelchair next to the single bed in his 40 square-meter (400 square-foot) flat. “I’ll have to go to a government nursing home with no freedom. There’ll be no point in living.” Since Abe took office two years ago, aggressive monetary easing devalued the yen, bolstering earnings at big companies and lifting the stock market 70%.

It’s been good for exporters and those who own shares and property, but not so good for those without assets. For them, Abenomics means higher prices and dwindling government support. “If inflation accelerates further under Abe’s policies, inequality will widen,” said Hideo Kumano, chief economist at Dai-ichi Life Research Institute Inc. “The socially vulnerable and low-income classes will be worst affected and a cut in livelihood subsidies deals them a double punch.” Abe is facing a problem that is dogging developed economies from the U.S. to Australia: how to sustain a recovery without widening the wealth gap. More than 30% of households in Japan have no financial assets, up from 26% in 2012, according to the Central Council for Financial Services Information in Tokyo.

Abe’s government is seeking to lower subsidies for housing and winter heating allowances for the poor as part of a three-step program that began in August 2013 to trim welfare costs, including for food, clothes and fuel. The move is part of the government’s efforts to contain rising social security costs as Japan’s aging society pushes up medical and other welfare expenses. The world’s third-largest economy is also the biggest debtor among the advanced economies, with borrowings projected by the International Monetary Fund to swell to more than 245% of gross domestic product in 2015.

Every single currency is under threat.

• Is Denmark Facing A Speculative Attack? (CNBC)

Denmark’s central bank is reaching for bigger bazookas to battle the speculators betting it will be forced to abandon its currency’s peg to the euro. “They’ve thrown the proverbial policy toolkit at defending the euro-Danish peg,” Kamal Sharma, a foreign currency strategist at Bank of America Merrill Lynch, told CNBC Thursday. “They will continue to intervene with the possibility of further rate cuts, even the tail risk of the recalibration of the trading range.” Bets that the krone will rise are building. Some of the flows have headed for Denmark’s stock market, with Danish-focused mutual funds and exchange-traded fund (ETFs) seeing $230 million in inflows over the past six weeks, according to data from Jefferies.

Barclays analysts called it “the slings and arrows of market speculation.” It bears similarities to the speculative attacks that led Thailand to abandon the baht’s peg to the dollar in the late 1990s — the “Lehman-moment” of the Asian Financial Crisis. Denmark’s peg is set for the krone to trade within a 2.25% band of 7.46038 to the euro, although it has been holding it in a 0.5% band. Although the euro has recovered somewhat this week, it has fallen around 17% against the greenback since the beginning of 2014.

“The RBA (Reserve Bank of Australia) is acting as if someone slipped tranquilizers into their drink 18 months ago..”

• Australia Central Bank Acting Like It ‘Just Woke Up’ (CNBC)

Australia’s record low interest rates are about to head way lower, analysts tell CNBC, as the country’s central bank scrambles to play catch up in the race to the bottom for borrowing costs. “The RBA (Reserve Bank of Australia) is acting as if someone slipped tranquilizers into their drink 18 months ago. They’ve just woken up and they’re looking [at] the world around them and they’re only gradually coming to terms with what they can see,” said Michael Every, head of Asia-Pacific markets research at Rabobank. The RBA chopped interest rates by a quarter-point on Tuesday to a historic low of 2.25%, surprising most economists but not the debt markets, which had priced in a 60% chance of a cut.

The central bank gave no hint that further easing is imminent, minutes from the meeting released Friday showed, although it did revise its 2015 growth forecast downwards to 1.75-2.75%, from 2-3% previously. Its less-than-dovish tone gave the Australia dollar a fillip against the U.S. dollar, rising to $0.7860. But Every believes the RBA will have no choice but the bring rates even lower, with central banks the world over going on a monetary loosening spree. China, India, Russia and Canada are just a handful of major economies that have surprised with rate cuts this year. This alongside Switzerland’s shock decision to remove its currency floor while moving interest rates into negative territory, and European Central Bank’s widely expected decision to finally embark on a bond-purchasing program, or QE, to revive the euro zone economy.

He should just leave.

• Oz PM Abbott Fights for Political Life as Colleagues Seek Ouster (Bloomberg)

Australian Prime Minister Tony Abbott said he will fight to stop party lawmakers ousting him next week after just 17 months in power, as two colleagues sought a leadership ballot. vAbbott, 57, said he and his deputy, Julie Bishop, will try to defeat the so-called spill motion when their Liberal Party meets in Canberra Feb. 10. Under party rules, a leadership ballot will go ahead if more than half of the 102 Liberal lawmakers back the motion. “We will stand together in urging the party-room to defeat this particular motion,” Abbott told reporters in Sydney. The party should back “stability and the team that the people voted for at the election.” Less than half-way through his first term, Abbott is struggling to quell disquiet over his leadership amid a voter backlash against his spending cuts and a decision to bestow a knighthood on Queen Elizabeth II’s husband, Prince Philip.

Some senior Cabinet ministers have rallied around the prime minister, saying he should be given time to reverse the government’s flagging poll ratings and reset his policy agenda. “The question now is whether or not there is a willing challenger” to Abbott, said Haydon Manning, a politics professor at Flinders University in Adelaide. “Even if Abbott keeps the leadership, he’ll still be aware he’s just buying himself time to turn around the performance of the government.” Lawmaker Luke Simpkins sent an e-mail to party colleagues earlier Friday saying they must bring concerns about Abbott’s leadership to a head by holding a vote for a spill. His motion was seconded by Don Randall. Nobody has yet said they will challenge Abbott for the leadership. Both Bishop, 58, and Communications Minister Malcolm Turnbull, 60, tipped by local media as potential successors to Abbott, have said they support the prime minister.

Curious deal.

• Venezuela Oil Deal Hits Caribbean Hard (CNBC)

For many countries, cheaper oil is helping boost economic growth. But if you’re a struggling Caribbean nation dependent on energy subsidies from Venezuela, the crash in oil prices is not welcome news. Venezuela’s heavily oil-dependent economy has been sent into a tailspin by the collapse of crude prices, which has starved the country for cash to pay for domestic energy subsidies and imported goods. With little foreign currency reserves left, the economy is contracting, inflation has soared and the government has resorted to rationing food and other consumer staples. And with no rebound in oil prices in sight, the country’s future is looking bleak.

To finance its budget, the government needs oil prices above $140 a barrel, putting generous subsidies for education, food and housing at risk of deep cutbacks.It has also jeopardized generous financing terms extended to more than a dozen Caribbean nations that rely on Venezuelan oil to fuel their own economies. Venezuela launched the so-called Petrocaribe accord in 2005 as it sought to become a low-cost energy provider and win political favor among small island economies heavily reliant on oil imports. But as oil prices have fallen, Venezuela’s energy blessing has turned to something of a curse. Under the terms of the Petrocaribe agreement, the drop in oil prices has—paradoxically—raised members’ oil import costs.

That’s because, as crude prices fall, they lose access to extremely generous financing terms that amount to subsidies. When oil was over $100 a barrel, Petrocaribe member countries paid just 40% of the upfront costs, and Venezuela’s state oil company, PDVSA, covered the rest of the expense with a low interest rate loan payable over 25 years. Some have also paid their oil bills with bartered agricultural products or services. The extra cash from deferred payments helped some countries finance infrastructure projects and other spending programs. But those finance terms become much less generous as the price of oil falls, forcing member countries to pay more upfront, with payment in full when prices fall below $40 a barrel, according to RBC economist Marla Dukharan.

Funny headline, but not entirely true.

• John Kerry Rated Worst Secretary Of State In 50 Years (MarketWatch)

A new survey of scholars ranks Secretary of State John Kerry dead last in terms of effectiveness in that job over the past 50 years. Henry Kissinger was ranked the most effective secretary of state with 32.2% of the vote. He was followed by James Baker, Madeleine Albright, and Hillary Clinton, as judged by a survey of 1,615 international relations scholars. Kerry received only 0.3% of the votes cast. According to the survey, the three most important foreign-policy issues facing the U.S. are climate change, armed conflict in the Middle East and failed or failing states. The survey of 1,375 U.S. colleges and universities was conducted by Foreign Policy magazine and the College of William & Mary.