Vincent van Gogh A Lane near Arles (Side of a Country Lane) 1888

https://twitter.com/andweknow/status/2039304266775740853?s=20

LARRY JOHNSON PREDICTS: US GROUND INVASION OF IRAN ISLANDS THIS WEEKEND

— Mark (@Mark4XX) April 1, 2026

Ex CIA Larry Johnson cuts through the noise with a chilling assessment based on troop movements and force deployments right now. Trump has not backed down out of fear. He is simply playing the same games… pic.twitter.com/n41bRkIPTg

— Words of Wise | Mindset Coach (@Wordofwise_) March 31, 2026https://twitter.com/WallStreetMav/status/2039126040686248240?s=20 https://twitter.com/ScaryEurope/status/2039236276709376095?s=20

https://twitter.com/BasilTheGreat/status/2039088940129391074?s=20EU Witch Ursula Von Der LIAR is caught RED-HANDED STEALING HUNGARY’S ELECTION

— Liz Churchill (@liz_churchill10) April 1, 2026

Globalist Overlords are trying to install a Puppet Regime to crush Orban’s Sovereignty

This is outright TYRANNY from the EU

Hungarians: Tell these corrupt DEMONS to GO TO HELL pic.twitter.com/sQpIVJlOqN

Angela Merkel just ADMITTED on CAMERA she deliberately flooded Germany with third-world migrants to “stop the far right.”

— Liz Churchill (@liz_churchill10) April 1, 2026

She chose to erase her own people rather than lose power.

This wasn’t a mistake.

It was demographic warfare.

This is TREASON. pic.twitter.com/NpiUl1ZC9C

He has to wrap it up quickly, nobody wants a long war, or heavy casualties, and it’s midterms soon.

• Trump Reassures Americans: Iran Operation Won’t Be a Forever War (Chris Queen)

President Donald Trump delivered a speech on Wednesday night with the intention of informing Americans about what’s going on with our joint military operations with Israel against Iran. It was remarkably restrained for a Trump speech and relatively brief. Side note: My favorite phrase from the speech was when Trump referred to the “green, green cash” that Barack Obama threw at the Islamic regime during his presidency. The president remarked that Wednesday was the one-month mark for Operation Epic Fury:Read more …

As we speak this evening, it has been just one month since the United States military began Operation Epic Fury targeting the world’s number one state sponsor of terror, Iran. In these past four weeks, our Armed Forces have delivered swift, decisive, overwhelming victories on the battlefield — victories like few people have ever seen before. Tonight, Iran’s navy is GONE. Their air force is in ruins. Their leaders, most of them — the terrorist regime they led — are now dead. Their command and control of the Islamic Revolutionary Guard Core is being decimated as we speak. Their ability to launch missiles and drones is dramatically curtailed and their weapons, factories, and rocket launchers are being blown to pieces — very few of them left. Never in the history of warfare has an enemy suffered such clear and devastating large-scale losses in a matter of weeks.He reminded viewers that disabling Iran was one of his earliest campaign promises: “From the very first day I announced my campaign for President in 2015, I have vowed that I would never allow Iran to have a nuclear weapon. This fanatical regime has been chanting ‘Death to America, ‘Death to Israel,’ for 47 years. Their proxies were behind the murder of 241 Americans in the Marine Barracks bombing in Beirut, the slaughter of hundreds of our servicemembers with roadside bombs, they were involved in the attack on the U.S.S. Cole, and they’ve carried out countless other heinous acts… For these terrorists to have nuclear weapons would be an intolerable threat. The most violent and thuggish regime on earth would be free to carry out their campaigns of terror, coercion, conquest, and mass murder from behind a nuclear shield. I will never let that happen.”

The president expressed that his goal was to resolve Iran’s issues diplomatically, but Iran wouldn’t allow that to happen: “My first preference was always the path of diplomacy — yet, the regime continued their relentless quest for nuclear weapons and rejected every attempt at an agreement. For this reason, in June, I ordered a strike on Iran’s key nuclear facilities in Operation Midnight Hammer… The regime then sought to rebuild their nuclear program at a totally different location, making clear they had no intention of abandoning their pursuit of nuclear weapons… For years, everyone has said that Iran cannot have nuclear weapons — but in the end, those are just words if you’re not willing to take action when the time comes.”

Trump acknowledged the pain Americans are feeling at the gas pump. (As somebody who recently bought a new vehicle that gets much lower gas mileage than my prior car, I can testify.) “Many Americans have been concerned to see the recent rise in gasoline prices here at home… This short-term increase has been entirely the result of the Iranian regime launching deranged terror attacks against commercial oil tankers and neighboring countries that have nothing to do with the conflict. This is yet more proof that Iran can never be trusted with nuclear weapons. They will use them and they will use them quickly. It would lead to decades of extortion, economic pain, and instability worse than we can ever imagine. The United States has never been better prepared economically to confront this threat.”

He called out nations that are dealing with the effects of the closure of the Strait of Hormuz: “To those countries that can’t get fuel — many of which refused to get involved in the decapitation of Iran, we had to do it ourselves — I have a suggestion. Number one, buy oil from the United States of America; we have plenty. We have so much. And Number two, build up some delayed courage… Go to the Strait and just take it. Protect it. Use it for yourselves. Iran has been essentially decimated. The hard part is done.”

After assuring the public that operations in Iran should be done in “two to three weeks,” Trump reassured his viewers that Iran’s days as a threatening power are almost over. “Tonight, every American can look forward to a day when we are finally free from the wickedness of Iranian aggression and the specter of nuclear blackmail,” he declared. “Because of the actions we have taken, we are on the cusp of ending Iran’s sinister threat to America and the world.”

Tonight, the president gave a speech that was characteristically Trumpian. But it achieved the objectives that he wanted of informing the American people that Operation Epic Fury is nearly over and won’t be a “forever war.”

A ceasefire or “back to the stone age”, everything’s on the menu.

• US, Iran Discussing Ceasefire In Exchange For Reopening Strait (ZH)

Ahead of Trump’s address tonight at 9pm ET, Axios reports citing three sources that the US and Iran are discussing a potential deal that would involve a ceasefire in exchange for Iran reopening the Strait of Hormuz “The officials did not say whether those discussions had taken place directly or only through mediators, and they cautioned that it was unclear whether a deal could be reached. But the officials said President Trump was discussing the possibility with officials inside and outside the administration.” As a reminder, earlier in the day Trump claimed on Wednesday that Iran had asked the U.S. for a ceasefire, but stressed he would only consider it if the strait was reopened. In response, Iran countered that it had not requested a ceasefire. https://twitter.com/BarakRavid/status/2039352788468003220Read more …

* * *Iranian Supreme Leader Vows To “Continue Supporting The Resistance Against The Zionist-US Enemy”

Amid speculation that he is dead or badly wounded, moments ago Iran’s new supreme leader Ayatollah Mojtaba Khamenei said on X that he “emphatically declare that the consistent policy of the Islamic Republic of Iran, following on the path of Imam Khomeini and the martyred Leader, is to continue supporting the Resistance against the Zionist-US enemy.”

* * *Iran: Not True that Iran Requested a Ceasefire

Iran has again rejected Trump’s narrative, after he hours ago claimed that “Iran’s New Regime President” has just “asked the United States of America for a CEASEFIRE!” Iran’s Foreign Ministry has responded by saying “there is no truth” to “Trump’s statements that Iran requested a ceasefire.” The Iran FM spox statement continues: “No decision has been made yet. We have many considerations. Our conditions for ending the war are very clear. We do not accept a ceasefire; We seek a complete end.” As a reminder, President Masoud Pezeshkian has been Iran’s president since July 2024 – and he’s made public appearances in Tehran, even over the last days. There is not a “new regime president”.= Additionally, Trump is now threatening to bomb Iran “back to the stone age” if Hormuz is not reopened, but just yesterday suggested he’s fine with it staying closed and that ultimately others should open it.Here’s a clue that the new president of Iran has not in fact begged for a CEASEFIRE:

— Scott Horton (@scotthortonshow) April 1, 2026

They do not have a new president. https://t.co/zqAUthm1d8Preparing American Public for an Exit?

President Trump has issued new words to Reuters on his highly anticipated speech tonight (9pm ET): The United States will be “out of Iran pretty quickly” and could return for “spot hits” if needed, President Donald Trump tells Reuters, hours before he was scheduled to make a primetime address to the nation. Trump also says he would state in the speech that he is considering withdrawing the US from the NATO alliance. There’s expected to be heavy focus on chastising NATO. If this is indeed the Bush-style ‘mission accomplished’ moment, it may be that he’s ready to blame Western allies for the closure of the Hormuz Strait – a problem which didn’t exist before Operation Epic Fury.Trump: Iran President has Asked for Ceasefire

President Trump on Truth Social has claimed the US has been directly asked for ceasefire; however, he coupled this with the typical threat of bombing Iran “back to the Stone Ages!!!” Here’s what he said (note: Iran does not have a new president): Iran’s New Regime President, much less Radicalized and far more intelligent than his predecessors, has just asked the United States of America for a CEASEFIRE! We will consider when Hormuz Strait is open, free, and clear. Until then, we are blasting Iran into oblivion or, as they say, back to the Stone Ages!!! President DJTAnd yet the Hormuz question lingers, after just yesterday Trump strangely said the vital energy shipping waterway would “automatically open”. Oil prices initially dumped on the Trump message, and quickly rebounded – perhaps based on the latter part of Trump’s statement. A lot would have to happen – for one Washington is likely to require that Tehran giving up charging a some $2 million fee for tankers to make safe passage. Oil unimpressed…

“Cuba has no economy, and no one there can fix the economy because they’re incompetent. ..”

• Rubio Delivers a Reality Check on Iran, NATO, Cuba, and Venezuela (Anderson)

Secretary of State Marco Rubio has been doing a lot of MSM interviews lately, and I kind of get the feeling he’s… fed up. He’s tired of having to correct false narratives on Iran, Cuba, and Venezuela. As I reported on Monday, he got to a point where he told George Stephanopoulos that maybe he needed to “write down” Donald Trump’s objectives for Iran because no matter how many times Rubio told him what they were, he implied that he didn’t understand them. While it was entertaining, it does get old, I imagine.Read more …

The three main points about these topics that he’s asked about in every interview — and there have been a lot; perhaps Trump is prepping him to cover for Karoline Leavitt when she goes on maternity leave (kidding) — are as follows: 1) We’re very close to meeting our objectives in Iran. Not months, not days but weeks away. 2) Cuba has no economy, and no one there can fix the economy because they’re incompetent. 3) Venezuela is in phase two of the three-phase plan he and Trump have for its recovery, and things are going very well there. But no matter how many times he says these things, to hear the MSM tell it, the administration has no idea what’s going on in Iran, the people in Cuba are suffering because of Trump, and Venezuela isn’t improving at all.Well, on Tuesday night, Rubio appeared on Hannity on Fox News, where he was actually allowed to talk without being asked asinine questions. He hit on all three countries (and NATO), and while he didn’t necessarily say anything new, he was able to lay it all out clearly and without dealing with stupidity, so it was nice to watch. Plus, as I said, he’s fed up with these MSM narratives, and it’s always fun to watch him get a little worked up. I’m going to kick back here and let him do most of the talking. I feel like i’m taking the lazy way out, but sometimes, it’s best just to let him talk. On how efficiently our military has achieved its objection and how it will “go down in history”:

.@SecRubio: "We are going to get to the point where our military will have achieved all of its objectives in this mission, and they're doing so with extraordinary efficiency — something that I think will go down in history as one of the best run tactical military operations in… pic.twitter.com/NaoMThIhs2

— Rapid Response 47 (@RapidResponse47) April 1, 2026On the threat to the United States and the rest of the world:

.@SecRubio on Iran: "They were moving towards eventually having a missile that could reach the continental United States… That's what they would've ultimately achieved had President Trump not taken these steps that he has taken." pic.twitter.com/B95UN5vuyg

— Rapid Response 47 (@RapidResponse47) April 1, 2026On why it’s the regime’s fault that we’ve gotten to this point:

.@SecRubio on Iran: "They refused to negotiate… For all these people out there talking about how this could've been avoided — they were given every opportunity, in multiple talks, and all they did was either reject or delay, and that's not going to happen under @POTUS." pic.twitter.com/9qcb0TEXwJ

— Rapid Response 47 (@RapidResponse47) April 1, 2026.@SecRubio: "Why do they continue to refuse to turn over 60% enriched uranium? There's only one reason — and that is because they want to hold it and keep it to one day use it to build a bomb." pic.twitter.com/xXXH66R4Rx

— Rapid Response 47 (@RapidResponse47) April 1, 2026

“The NATO membership is now a one-way street where they demand our military protection..”

• Marco Rubio, the Question Must be Asked: “Why are we in NATO”? (CTH)

Secretary of State Marco Rubio appears on Fox News to discuss the various goals and objectives of the U.S. military operation against Iran. As part of the interview Secretary Rubio was asked about the strategic conflicts and hypocrisies now flowing from NATO member states. The U.S. supports our NATO posture in Europe in part because it provides us with strategic military bases and operations that are considered vital to our national interests. However, as outlined in the Iran conflict, when we need to use those strategic bases the NATO member states withdraw previous permissions. France has blocked us from flying over their airspace, Spain and Italy have said the U.S. cannot use our military bases on their soil for operations. The U.K has refused to protect and/or escort their own energy assets.Read more …

The NATO membership is now a one-way street where they demand our military protection, but Europe blocks us from using our own military assets for our independent operations. Europe, while hiding behind the NATO protection skirt of the U.S, is simultaneously telling the U.S. what we can and cannot do with our own military. Secretary Rubio and President Trump are now confronting this very visible one-way benefit head on.

80 years ago.

• NATO Without America? A Slow Shift Is Already Underway (Zevelev)

US President Donald Trump’s approach to foreign policy is often dismissed as chaotic or erratic. In reality, it reflects a deeper shift that is unlikely to disappear when he leaves office. Beneath the surface lies a consistent worldview, one shaped by populism and nationalism, that’s steadily gaining ground, both within the United States and globally. This shift is already reshaping long-standing institutions. Nowhere is this more visible than in Washington’s relationship with its European allies. For decades, US foreign policy rested on a simple premise: alliances, above all NATO, were the foundation of American power and influence. That consensus held across party lines for nearly 80 years. Today, it’s breaking down.Read more …

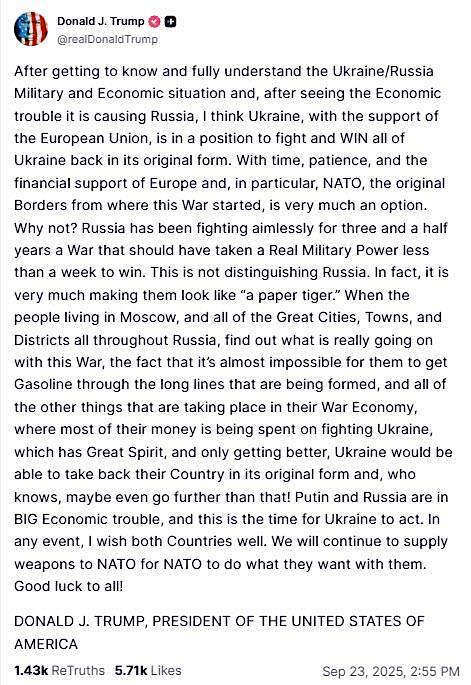

Trump is not merely skeptical of alliances, he openly questions their value. His reaction to the refusal of European allies to support US and Israeli military action against Iran was telling. Writing on Truth Social, he described NATO as a “paper tiger” and accused American allies of cowardice. “Everyone agrees with us, but they don’t want to help. And we, as the United States, must remember this,” he said. The message is blunt: if allies don’t act when Washington calls, then their status as allies is called into question. This doesn’t mean the United States is about to withdraw from NATO. What is unfolding is more gradual, and arguably more significant – a quiet dismantling of the alliance’s traditional structure.There are growing signs of this shift: sharper rhetoric, fewer high-level engagements, and plans to reduce the American role within NATO’s command system. This is no longer just political theater.Even when constrained by Congress, as in the decision to block a rapid reduction of US troops in Europe, the administration has adjusted tactics rather than abandoning its objective. The restriction on cutting troop levels below 76,000 slows the process, but doesn’t change its direction. The broader aim remains clear: shifting responsibility onto Europe.A key element of this strategy is the gradual transfer of operational control. Reforms to NATO’s integrated command structure are already underway.

Soon, all three of the alliance’s operational commands will be led by Europeans. This marks a significant step towards transforming NATO into a European-led organization. If the United States relinquishes its central role in force planning and command, the consequences will be profound. NATO may remain intact in form, but its substance will change. Washington will no longer lead the alliance in the way it once did. This isn’t simply a matter of one president’s preferences. Trump reflects a broader shift in American public opinion.

There’s growing fatigue in the United States with the idea of underwriting the security of others. Years of costly conflicts in the Middle East, rising national debt, and pressing domestic concerns have made the traditional role of global guarantor increasingly unpopular. Don’t mistake it for isolationism. The recent strikes on Iran demonstrate that Washington remains willing to use force when it chooses. The change is more subtle, and more consequential. The United States no longer wants to be bound by obligations. Alliances and institutions that once defined American leadership are now seen as constraints. The emerging model is one of leadership without commitments: the ability to act freely, without being tied to the interests or expectations of partners.

That is a fundamentally different approach to international relations. It leaves NATO in an uncertain position, still formally intact, but increasingly hollowed out. In time, the alliance may survive. But it will no longer be the same organization that defined the transatlantic relationship for generations. And it’s far from clear that Europe is ready for what comes next.

“.. if it remains alone, without key support and protection from the USA, the British empire is at risk of collapse.”

• Keir Starmer Gives a National Address – Things Will Never be the Same Again (CTH)

Against the backdrop of the Iran conflict, crisis in the middle east and the disruption of energy supplies due to the closure of the Strait of Hormuz, U.K Prime Minister Keir Starmer held an urgent meeting with British business leaders, finance and bankers as well as U.K insurance leaders. At the conclusion of that meeting he informed media of a national address. During the national address to the people of Great Britain, Prime Minister Starmer emphasized that events in the middle east have forever changed the landscape of U.K. economic and geopolitical policy. Signaling an inflection point crossed, the British prime minister announced that urgent actions were being taken to mitigate a national crisis.Read more …

Additionally, accepting the U.S. position toward NATO and the U.K appears to be permanently shifted, Starmer said the British relationship with Europe now becomes critical to their vital national security interests. Against the backdrop of an end to the “special relationship” with America, the Brexit independence from the European Union is now a threat. The United Kingdom must find a way to reunite with the European Union, because if it remains alone, without key support and protection from the USA, the British empire is at risk of collapse.

“..while he may be the most recognizable congressional leader, that familiarity isn’t doing him any favors ..”

• Chuck Schumer Is Losing Control of His Party; They Turn On Him (Margolis)

A quiet rebellion is brewing inside the Democratic Party, and Chuck Schumer is sitting right in the crosshairs. Even as the Senate Minority Leader works to claw back the majority he lost in 2024, several Senate candidates are making it a point of pride to say they won’t support him as leader — before they’ve even won their races. The clearest shot came from Illinois. Lieutenant Gov. Juliana Stratton, who won her Democratic Senate primary earlier this month, made her position crystal clear during a January debate. “I’ve already said that I will not support Chuck Schumer as leader in the Senate, and I’m the only person on this stage that has said so,” Stratton declared. She’s not alone.Read more …

Michigan state Sen. Mallory McMorrow has also called for Schumer to step aside. Texas Senate Democratic nominee James Talarico is keeping his options open, saying he wants to hear from leadership candidates before making any commitment. And when Sen. Chris Murphy was offered the opportunity on NBC’s Meet the Press to back Schumer directly, he ducked it with a classic non-answer: “Well, no, we are united as a caucus right now.” United, sure. Just not necessarily behind Schumer.Sen. Andy Kim (D-N.J.), appearing on CNN’s State of the Union, was careful to keep his support firmly in the past tense. “I’ve been supportive of our leadership right now,” Kim said, which is a far cry from saying he’d vote to keep Schumer in charge after November, and it’s quite the insult to the sitting leader. “And I think that that’s really what the American people are seeing is what we get when the Democrats are united, and the Republicans are constantly fighting themselves,” Kim concluded.

The Hill reports: “Schumer, 75, has led the Senate Democratic Conference since 2016, when he replaced longtime party leader Sen. Harry Reid (D-Nev.), who died in 2021. But in recent years, the New York Democrat has faced calls to give up power from various corners of the party, including from progressive groups, House Democrats, and even Democrats running for Senate. Criticism of Schumer particularly ramped up after eight Democrats, a group he was not part of, joined Republicans in voting to end the record-long government shutdown in November.

Illinois Lt. Gov. Juliana Stratton, the Democratic nominee in the race to succeed retiring Sen. Dick Durbin (D-Ill.), told liberal YouTuber Jack Cocchiarella earlier this month that she does not support Schumer serving as Senate Democratic leader for another Congress. We all know that Schumer’s problems with the base go back to this vote to keep the government open last March. That one vote cost him dearly with the base, and he’s never recovered from it. Schumer told The Hill he is just focused on winning the majority in November.

“The way to counter Trump more effectively is to win the majority in 2026 and put gavels in the hands of Democrats. That’s my North Star, and that’s what I’m focused on doing every single day,” Schumer said. A recent Morning Consult poll found that while he may be the most recognizable congressional leader, that familiarity isn’t doing him any favors. Compared to John Thune, Mike Johnson, and Hakeem Jeffries, Schumer is viewed the most negatively.

“No One Knows What Will Happen Now”:

• Justice Ketanji Brown Jackson Warns Against Unbridled Free Speech (Turley)

Justice Ketanji Brown Jackson is again warning of a growing threat to the nation. In her lone dissent in Chiles v. Salazar, Jackson observed that “to be completely frank, no one knows what will happen now.” The ominous tone stemmed from the fact that free speech had prevailed over state-imposed orthodoxy in a Colorado case. Eight justices, including her two liberal colleagues, ruled that Colorado could not prevent licensed counselors from “any practice or treatment” that “attempts or purports to change” a minor’s sexual orientation or gender identity. The win for free speech was catastrophic for Jackson and many on the left. Allowing counselors to discuss the causes and basis for sexual orientation changes, Jackson maintained, would “open a can of worms.” It would be far better for the majority to simply silence such dissenting voices in the name of science.Read more …

The dissent in Chiles is only the latest example of the chilling jurisprudence of Justice Jackson, including a pronounced dismissal of free speech values. Consider the holding of her colleagues that Jackson finds so horrific. Justice Neil Gorsuch wrote that the First Amendment “reflects … a judgment that every American possesses an inalienable right to think and speak freely, and a faith in the free marketplace of ideas as the best means for discovering truth … any law that suppresses speech based on viewpoint represents an ‘egregious’ assault on both of those commitments.” What a nightmare.Instead, Jackson would have declared the ban on anything deemed “conversion therapy” to be “conduct,” not speech. It is that easy. You simply impose an orthodoxy and then treat any dissenters as being regulated for their conduct, not their viewpoints. Justice Elena Kagan could not withhold her frustration with her colleague, noting that “[b]ecause the State has suppressed one side of a debate, while aiding the other, the constitutional issue is straightforward.” She added that Jackson’s view “rests on reimagining—and in that way collapsing—the well-settled distinction between viewpoint-based and other content-based speech restrictions.”

Other countries have embraced Jackson’s permissive approach to speech curtailment. Recently, Malta failed to convict a man who was facing five months in prison for merely discussing his own abandonment of homosexuality due to a religious conversion. Of course, we just went through a pandemic when censorship and orthodoxy were dressed up as science. Leading scientific figures were canceled and harassed. That was the case with Jay Bhattacharya, who co-authored the Great Barrington Declaration and was a vocal critic of COVID-19 policies. Bhattacharya was target due to his dissenting views on health policy, including opposing wholesale shutdowns of schools and businesses.

He and other scientists were later vindicated. European allies that did not shut down their schools fared far better than we did, including avoiding a national mental health and learning crisis. We simply never had that debate. He was recently honored with the prestigious “Intellectual Freedom” award from the American Academy of Sciences and Letters. He is also now the 18th director of the National Institutes of Health. Yet, years ago, the courts, the media, and politicians joined in treating dissenting views as “conspiracy theories.”

Some argued that the virus’s origin was likely the Chinese research lab in Wuhan. That position was denounced by the Washington Post as a “debunked” coronavirus “conspiracy theory.” The New York Times Science and Health reporter Apoorva Mandavilli called any mention of the lab theory “racist.” Federal agencies now support the lab theory as the most likely based on the scientific evidence.Likewise, many questioned the efficacy of those blue surgical masks and supported natural immunity to the virus — the government later recognized both positions.

Others questioned the six-foot rule, which shut down many businesses, as unsupported by science. In congressional testimony, Dr. Anthony Fauci later admitted that the rule “sort of just appeared” and “wasn’t based on data.” Yet not only did it result in heavily enforced rules (and meltdowns) in public areas, but the media further ostracized dissenting critics. For years, pundits portrayed those who questioned gender reassignment surgeries and treatments as bigots. Now, leading medical associations and European nations have decided that such procedures should not be generally allowed. All of it was orthodoxy masquerading as science.

Yet, Jackson sees the protection of dissenting scientific and professional views as a “can of worms” that the courts should avoid in favor of state and assocational imposed truths. She wrote that allowing such opposing views “ultimately risks grave harm to Americans’ health and wellbeing.”

“Ursula von der Leyen recently announced the need to yank another €200 million from taxpayers to “support investment in innovative nuclear technologies.”

• How Many Times has the EU Screwed Itself Over in the Past Year? (Marsden)

Hey, good news! The EU has found a new source of desperately needed gas amid the current energy crunch. The bad news? It’s in the US. So it will serve America, first. With Europe getting any sloppy seconds that Daddy Trump feels like overcharging it for when he isn’t threatening to invade. It’ll be the French energy multinational, TotalEnergies, serving it up to the US like a waiter at a Montmartre bistro, forced to smile and bow while the guest pockets the silverware.Read more …

Even better? The company wasn’t even supposed to be over there doing that. They had planned to be building offshore windfarms. But instead, Trump’s Department of the Interior now says that they made a deal with the French company to spend roughly a billion dollars investing in American gas operations in exchange for getting about the same amount of cash back for agreeing to say goodbye to its green wind dreams in the US. Team Trump calls it an “innovative agreement driven by President Donald J. Trump’s Energy Dominance Agenda.” But the CEO of the European company is making the cucking sound like a big win.“TotalEnergies is pleased to sign this settlement agreements with the DOI and to support the Administration’s Energy Policy. Considering that the development of offshore wind projects is not in the country’s interest, we have decided to renounce offshore wind development in the United States, in exchange for the reimbursement of the lease fees,” said TotalEnergies CEO Patrick Pouyanne, while adjusting his knee pads, before continuing to service Trump via official US government press release.

“Furthermore, these agreements, under which we will reinvest the refunded lease fees to finance the construction of the 29 Mt Rio Grande LNG plant and the development of our oil and gas activities, allows us to support the development of US gas production and export.” Hold up. So this company gave the US about a billion dollars in exchange for access to green energy. Then the US gave them back their money. And now they’re reinvesting it to serve Trump’s agenda? And publicly “pleased” about it?

Well, good riddance to – er, I mean, so much for Europe’s green dreams, I guess. But at least it means they’ll get easier access to more desperately needed LNG, right? Since they’re the ones doing the heavy lifting. Not without securing a trade agreement on America’s terms, they won’t. Which is why they’re aiming to ratify a trade agreement with their tormentor.

Brussels had been concerned about the agreement that was struck with Trump back in 2025, named the Turnberry Agreement after the US president’s Scottish golf resort where it all went down. The deal was about tariffs. Specifically, it gave a huge break to the US with ZERO tariffs on some of its exports to the EU, while slapping a 15-percent tariff on EU imports to the US. Another master stroke of cuckoldry. And yet Trump still won’t stop talking about how the EU is constantly stiffing America on trade. Which explains why the EU has been dragging its feet on ratifying it, worried that maybe it was putting too many eggs in a very unstable basket. Something that the US warned it against doing with Russia, being only too happy to step up to offer a costlier overdependency on itself instead.

The EU is doing the exact same with green energy, turning its back on nuclear power before its beloved green renewables were even ready for prime time. Which also went about as well as you might expect from these central planning geniuses. Calling it a screwup, European Commission President Ursula von der Leyen recently announced the need to yank another €200 million from taxpayers to “support investment in innovative nuclear technologies.” The same ones they’d been busy vilifying until recently.

“Europe believes that their needs must be our priority, and that, furthermore, we’re required to do their job for them.”

• Europe Needs to Hear This Harsh Truth (Stephen Green)

Shipping and military expert John Konrad spent all day in D.C. on Tuesday talking to his military sources and concluded that “the Navy appears to be in no rush to reopen the strait,” even while Iran dictates whose oil tankers are allowed to pass. “What is this administration trying to leverage?” Konrad wondered, and that nobody he talked to was willing to discuss the fate of Hormuz “until European politicians and media stop calling Americans war criminals and monsters.”Read more …

While Konrad admitted he has “no idea” when Hormuz will reopen, “but if the price is a modicum of cooperation and respect for everything America has done for decades to keep Europe safe, the strait could stay closed for months, or turned into a toll booth for years, because the majority of Americans…. and the vast majority of Trump administration officials I’ve talked with… seem fed up with their arrogance.” The self-styled sophisticates in Brussels and Europe’s capitals remain remarkably provincial in their outlook, and that’s why today we will speak some harsh truths to our friends in Europe — not because the truth is harsh, but because they believe that we naïve Americans don’t recognize it.So here comes the truth bomb, laser-guided right into the atrium of the EU’s Berlaymont building. The harsh truth is that Hormuz is their priority, not ours, and yet they refuse to make any serious contribution to the war effort. The U.S. is a net exporter of oil and liquified natural gas (LNG), and we buy hardly anything from the Gulf. Closing the Strait of Hormuz is an inconvenience for us (in the price of gas and diesel) and hardly a strategic necessity. In both military and economic terms, Hormuz is way down our target list. Complicating the decision matrix even further, re-opening Hormuz at this stage likely requires ground troops — so it’s simply smarter for us to continue the bombing campaign and see if we can’t wait out an increasingly split and brittle regime that might still collapse under pressure.

Europe, of course, doesn’t see things the way we do. Europe believes that their needs must be our priority, and that, furthermore, we’re required to do their job for them. [And Another Thing: We could do more to stabilize energy prices, but in 2024, the Biden Cabal declared a moratorium on the construction of new LNG export terminals. So while the rest of the world suffers an LNG supply shock, our producers are forced to, at times, pay people to take LNG off their hands, and even burn off excess. Crazy, right?]

Before Epic Fury, something like 20% of the world’s LNG and 25% of seaborne oil trade passed through the strait each year and accounted for something like 10-15% of Europe’s energy supplies. Losing that hurts, and Politico reported on Tuesday that one “top Brussels official urges Europeans to work from home and drive less.”nEU energy chief Dan Jørgensen says Europe faces a “very serious situation,” and that “even if… peace is here tomorrow, still we will not go back to normal in the foreseeable future.”nSucks to be EU, chief. Meanwhile, Europe’s contribution to the actual military effort is barely minuscule, and a handful of nations, including France (duh), Spain (fricken commies), and even Giorgia Meloni’s Italy, have closed their airbases to our military traffic headed to the Gulf. Apparently, “lead, follow, or get out of the way” isn’t a part of Europe’s lexicon.

The UK today.

• A Civilization Whose Defense is Abandoned, is Lost (Paul Craig Roberts)

For many years I have expressed concern that Western Civilization was being destroyed intentionally from within by failing to convey the civilization’s achievements to succeeding generations via education. Instead, education was used to alienate generations from their own civilization by stressing evils such as wars, slavery, oppression of blacks and women, oppression of other peoples as the result of colonial rule, abuse of children by parents, religious prejudices, class prejudices, and so on. The history of Western Civilization as a series of great reforms was kept from generation after generation so successfully that today hardly anyone under sixty years of age knows about them.Read more …

Western civilization has many achievements in science, technology, architecture, music, art, but perhaps the greatest achievement of Western Civilization began in the ninth century during the reign of Alfred the Greet in what became England. Alfred established law based on the people’s beliefs and behavior–the English Common Law–not on the edicts of a king. This was the beginning of developments over the centuries that culminated in the Glorious Revolution of 1680 that established that the king was subject to the law and the law was established by the commoners and the aristocrats in Parliament, thus making the king accountable to the people. The accountability of government rested on free speech. Without free speech truth cannot be ascertained.The Americans who inherited the notion of government accountable to the people inscribed in the US Constitution the right to free speech.In recent years this right on which accountable government rests has been eroded in the US and essentially destroyed in the UK. In America today citizens who use the Constitutionally protected right of free speech can lose their jobs, can be prohibited from contracting with or having jobs with many state governments. If they are students who protest Israel’s genocide of the Palestinians, they are expelled from the university, and if they are foreign students they are deported. The universities do nothing to protect the free speech that the US Constitution guarantees. Neither do the bar associations nor the law schools.

Free speech is in the way of anti-Western civilization ideologies. We must believe that white racism, not the black King of Dahomey’s slave wars, is the cause of black slavery. We are denied the fact that blacks held blacks in slavery and the fact that the blacks sent to the New World were enslaved by blacks, and that colonists in the New World purchased already enslaved blacks for a labor force. White people did not enslave black people. Black people sold as slaves were enslaved by the black King of Dahomey. You will not be able to find this fact in any Black Studies program in any university. The generations of indoctrination of white people against themselves, called education, has produced a situation in which law is no longer applied to the guilty but to his victim. Black immigrant-invaders are protected against hate speech and an accusation of rape has become hate speech.

In the UK, and also I believe in Norway and Sweden and perhaps throughout the EU, a white woman who reports a rape or a gang-rape might be charged with a hate crime against a “person of color.” This possibility essentially conveys rape privileges to black immigrant-invaders to rape white European women. The police are as likely to hold the rape victim accountable for a hate crime as to hold the rapist accountable for rape. In England these rapes went on for 30 years with the police and the British government doing nothing about it except covering it up. A year or two ago former British prime minister Liz Truss said that for 30 years the British government covered up the rapes. It stilll does.

Tyler Robinson’s defense team may use this argument in an attempt to get the charges against him dropped”

• Charlie Kirk Bullet Doesn’t Match Suspect’s Rifle – Lawyers (RT)

Investigators could not match the bullet that killed conservative influencer Charlie Kirk to the rifle used by his alleged assassin, lawyers for the suspect have claimed. The accused killer’s defense team is using this fact to push for a delayed trial. Tyler Robinson’s lawyers said in a recent court filing that the US Bureau of Alcohol, Tobacco, Firearms and Explosives (ATF) could not conclusively connect a bullet fragment recovered from Kirk’s body to a rifle found at the scene, citing an internal report by the agency.Read more …

The full ATF report has not been made public, but Robinson’s lawyers cited excerpts from the document in a request to delay a preliminary hearing scheduled for May. The 22-year-old suspect’s legal team stated that they need more time to review the bullet analysis, and to analyze the DNA of multiple other people found at the crime scene. Kirk, the founder of Turning Point USA (TPUSA), was shot in the neck and killed almost instantly at an event on a Utah college campus last September. His death sent shockwaves through the US, with President Donald Trump posthumously awarding Kirk the Presidential Medal of Freedom and describing the conservative icon as “a visionary and one of the greatest figures of his generation.”Robinson was arrested two days after Kirk’s death. Investigators quickly linked him to a Mauser model 98 rifle found near the scene, which had apparently been modified at some point to fire the American 30.06 round used in the assassination. Text messages between Robinson and his transgender lover were then unearthed, in which Robinson confessed to the killing and revealed almost every detail of the plot, down to how he cleaned his fingerprints off the gun before stashing it in a nearby patch of woods.

Prosecutors have said that DNA matching Robinson’s was found on the trigger of the rifle, but the case has nevertheless spawned multiple conspiracy theories – including the widely spread claim that Kirk was killed for turning on TPUSA’s pro-Israel donors and opposing US strikes on Iran. Every firearm leaves a unique imprint on a bullet as the projectile leaves the barrel. When enough fragments are found in good condition, ballistic analysts can match the projectile to the weapon with almost 100% confidence. Robinson’s lawyers suggested in the filings that they may point to the lack of a match in an attempt to dismiss charges against their client.

People hear it will take their jobs, and that’s all they can understand.

• More Than Half of Americans Believe AI Will Do More Harm Than Good: Poll ET)

About 55 percent of Americans surveyed in a 2026 Quinnipiac poll said artificial intelligence (AI) will be more harmful than helpful. The survey, released on March 30, was conducted in collaboration with the Quinnipiac University School of Computing & Engineering and the Quinnipiac University School of Business. In April 2025, only 44 percent believed AI would do more harm than good in their daily lives. In the 2026 poll, 21 percent answered that AI affects their lives a lot, while 29 percent said only somewhat, and 30 percent believed AI impacts are minimal. Only 17 percent said they are not impacted at all.Read more …

Regarding education, 64 percent of survey respondents said AI is more harmful, compared with just 27 percent who believe it will help. For health care issues, 45 percent of those surveyed believed AI will do more harm, while 43 percent said AI will be more helpful. The employment outlook showed the greatest percentage of people worried about the future of AI, as 75 percent said continuous advancements in AI will most likely lead to a decline of job opportunities for people. While 18 percent said AI will not have much of an impact on jobs, only 7 percent said jobs for humans will increase as a result of AI.In just one year, the fear of possible job losses due to AI increased by nearly 20 points. In April 2025, 56 percent of respondents said AI would be detrimental to human jobs. All generations surveyed remain pessimistic about the job outlook as a result of AI’s rapid growth, with Gen Z—including ages 18 to 29—exhibiting the highest percentage at 81 percent. For millennials, aged 30 to 45, 71 percent said jobs are likely to decrease as AI grows, and 67 percent of Gen Z, aged 46 to 61, agree. Of the baby boomer generation, aged 62 to 80, 66 percent indicated that human jobs will decline.

“Younger Americans report the highest familiarity with AI tools, but they are also the least optimistic about the labor market,” Tamilla Triantoro, associate professor of business analytics and information systems at Quinnipiac University School of Business, said in the report. “AI fluency and optimism here are moving in opposite directions.”Among those currently employed, 30 percent reported being very or somewhat concerned about AI rendering their jobs obsolete, but 69 percent said they are not very worried about it. Compared with last year’s survey, only 21 percent of employed Americans expressed fear of losing their jobs to AI.

“Americans are more worried about what AI may do to the labor market than about what it may do to their own jobs,” Triantoro said. “People seem more willing to predict a tougher market than to picture themselves on the losing end of that disruption—a pattern worth watching as the technology moves deeper into the workplace.”

An overwhelming 85 percent of Americans said they would be unwilling to work a job where their direct supervisor was an AI program that assigned their tasks and schedules. When asked how much they trust AI, 76 percent of respondents said that they hardly ever trust it, while just 21 percent admitted they do trust AI. Still, 51 percent said they often use AI for researching topics. Only 20 percent said they relied on AI for medical advice, and just 15 percent for personal advice.

Elon Musk didn't have a background in mechanical engineering or rocket science when he founded Tesla and SpaceX.

— Greg McKeown (@GregoryMcKeown) March 31, 2026

He didn't.

He was once asked how he packed so much knowledge into his brain so quickly.

His answer: "It is important to view knowledge as sort of a semantic tree —… pic.twitter.com/wsgQD8MWj0

If you want to know what’s really safe or what’s not, just try buying insurance for it https://t.co/AusNZjaw6n

— Elon Musk (@elonmusk) April 1, 2026

Elon Musk: “My essential philosophy is curiosity. I’d like to understand the meaning of life — is the Standard Model of physics correct? The beginning of life, the beginning of existence, and the end of the universe. What questions do we not know to ask, that we should ask? AI… pic.twitter.com/M11492h1wr

— Mars University (@MarsUniversityX) April 1, 2026

The corporate world built a religion around one lie.

— Dustin (@r0ck3t23) April 1, 2026

That leadership is separable from understanding.

That you can run a machine you cannot read.

Musk: “At SpaceX, almost all my time is spent on engineering and design.”

Not strategy meetings. Not press tours. Not optics.

The… pic.twitter.com/2dLcY2crp0

Support the Automatic Earth in wartime with Paypal, Bitcoin and Patreon.