Jack Delano Near Shawboro, North Carolina, Florida migrants on way to Cranberry, NJ 1940

“I’m an investor that ultimately does believe in the system, but believes that the system itself is at risk.”

What Gross says is that being an investor is no longer any use. Or, as I said quite a while ago, in a market as manipulated as this one, with no price discovery, there are no investors. You’d have to fully redefine the term. For now, there are only people pretending to be investors.

• Bill Gross Trying to Short Credit to Reverse Four Decades of Instinct (BBG)

Bill Gross, who built a career and a $1.9 billion personal fortune trading bonds, is trying to go short on credit, a position that he said runs contrary to his instincts and training as an investor. Gross, who manages the $1.3 billion Janus Global Unconstrained Bond Fund, said he is moving to sell credit risk and insurance on market volatility rather than buying long-term debt, because he believes a day of reckoning will come when central banks will no longer be able to prop up asset prices and investors will withdraw from markets. “It’s really hard to change your psychological makeup and to be a hedge manager that is comfortable with being short,” he said in an interview with Bloomberg’s Erik Schatzker. “I’m working on it, because I’m an investor that ultimately does believe in the system, but believes that the system itself is at risk.”

Central bankers, seeking to stimulate economies, have lowered rates below zero in Europe and Japan, driving down returns on national debt, while investors seeking higher yield have pushed up the value of other credit. Stimulus from central banks worldwide has artificially pushed up values of stocks and credit, which has made Gross cautious on such assets, he said. Eliminating credit as an investment means “not buying stocks, not buying high-yield bonds,” Gross said. “It means going the other way, which comes at a price.” The U.S. Fed Funds target rate is between 0.25% and 0.5%. Eventually, central bankers will have to raise rates to reward individual savers, insurance companies and other investors who depend on fixed-income returns, or the economy and markets will suffer, according to Gross.

The Fed will boost the rate in June and should continue a gradual path of increases, Gross said. Since last week when the Fed released minutes of an April meeting indicating the economy has strengthened enough for a rate increase, the probability of a hike at the June 15 Federal Open Market Committee meeting has climbed to 34%, according to futures information compiled by Bloomberg.

Shinzo Abe approaches full panic mode. Dangerous.

• “Japan Is Already Doing Helicopter Money” (BBG)

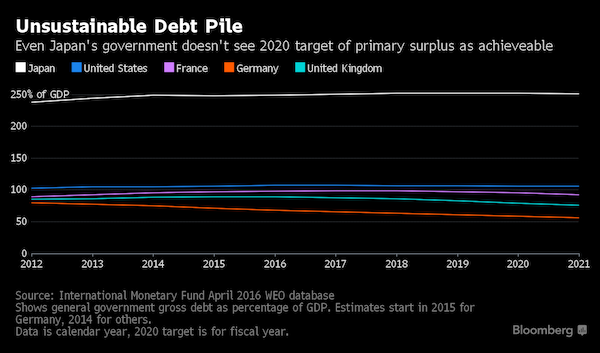

Yukio Noguchi, a former Ministry of Finance official whose business books are best sellers, envisages a scenario in which a failure of Japan’s economic stimulus could drive the yen to weaken beyond 300 per dollar. “If these fiscal and monetary policies continue, the yen’s value is at great risk,” the 75-year-old professor at Tokyo’s Waseda University said in an interview on May 11. “If you base your thinking on the efficient-markets hypothesis, you can’t predict a level for the currency. But, if the nation’s economic strength weakens, it is possible the yen could drop to 300, or 500, or 1,000 to the dollar.” Growth has stagnated for a decade despite fiscal and monetary stimulus efforts that left the government with a debt burden that is the highest in the world, at about 2.5 times the value of the nation’s economic output.

Noguchi believes the Bank of Japan is already financing fiscal spending, providing so-called helicopter money. That echoes comments by billionaire bond investor Bill Gross, who said the likely endgame was for the BOJ to forgive sovereign debt. The problem with the extremely cheap money is that it gets channeled into unproductive areas, and allows “zombie companies” to continue to stay in business, said Noguchi, who has a Ph.D. in economics from Yale, and is currently an adviser at Waseda University in Tokyo. Even so, this stimulus hasn’t been effective, and capital investment, wages, and prices aren’t rising, he said. “Japan is already doing helicopter money, as Bernanke describes it,” said Noguchi, whose economics books and life-hacking scheduler have sold millions of copies in Japan. “That’s what’s happening now under the BOJ’s asset purchase policy, with banks buying longer-maturity bonds and immediately selling them to the BOJ.”

Duncan’s not fooling around.

• “China’s Economy Resembles A Spinning Top Running Out Of Momentum” (RD)

Economist and financial author Richard Duncan has published a stark look at China’s economy as it enters a new phase of slower growth, assessing the implications for a global economy that has become reliant on Chinese demand as a driver. Duncan believes that China’s economic boom ended in 2015 and that a protracted slump lies ahead. He has published a series of videos explaining why, in his opinion, China’s economic development model of export-led and investment-driven growth is now in crisis. The South China Morning Post brings you the first video in that series.

“China’s economy resembles a spinning top that is running out of momentum. It is wobbling and gyrating erratically,” Duncan said. A former Hong Kong-based banking analyst, Duncan has also worked as an analyst at the World Bank, and as global head of investment strategy at ABN AMRO Asset Management in London. He has authored three books on the global economic crisis, including The Dollar Crisis: Causes, Consequences, Cures. He is now chief economist at the Singapore-based hedge fund Blackhorse Asset Management.

Cats in a sack.

• US-China Economic Poker Game Looms With Market Calm at Stake (BBG)

As top American and Chinese officials prepare for their annual powwow against the backdrop of a looming Federal Reserve interest-rate increase, the policy actions of the world’s two-biggest economies have never been so closely bound. In what could be likened to a poker game, officials from the world’s two biggest economies will attempt to assess each others’ policy plans – and their potential domestic implications – when they sit down in Beijing June 6-7. China wants to loosen the yuan’s link with the dollar while averting an exodus of capital. The Fed wants to gradually move away from near-zero interest rates, with almost all officials penciling in at least two quarter-point hikes this year.

The past nine months have made clear how the two sides’ goals can conflict, with the withdrawal of U.S. stimulus encouraging Chinese outflows and a surprise August yuan devaluation generating market ructions that put a pause on a Fed rate move. A Fed-induced surge in the U.S. currency would put pressure on the yuan, lighting a match under money outflows that have eased significantly after a record $1 trillion left in 2015. Avoiding another financial conflagration is one task for Fed Vice Chairman Stanley Fischer, U.S. Treasury Secretary Jacob J. Lew and other officials when they meet their Chinese counterparts. The gathering will be the eighth and final Strategic and Economic Dialogue since the Obama administration agreed on the annual sessions, which were an extension of a Bush administration initiative.

Listening to the ‘authorative voice’.

• China Stocks Head for Longest Weekly Losing Streak in Four Years (BBG)

China’s stocks headed for their longest stretch of weekly losses since July 2012 amid concern a pick-up in earnings growth is losing steam as the nation’s economy slows. The Shanghai Composite Index was poised for a sixth week of declines after slipping 0.3% on Friday. Industrial, drug and consumer-staples producers were the worst performers this week. China Southern Airlines and Air China slumped more than 6% during the period, hurt by rising fuel prices and a weakening yuan. Data on Friday showed industrial companies’ profit growth slowed to 4.2% in April. Hong Kong stocks halted a three-day advance after Tingyi Cayman Islands reported slumping earnings.

Sentiment toward Chinese stocks turned bearish after March’s pick up in economic indicators didn’t carry over to April and a high-profile warning by the People’s Daily about the nation’s high levels of debt damped hopes for more easing. Adding to the concern this week is the prospect of higher U.S. interest rates spurring capital outflows. Despite dwindling optimism, the Shanghai Composite hasn’t strayed more than 51 points from 2,800 in the past two weeks, with declines limited by suspected buying from state-backed funds aimed at preventing the benchmark from ending below that level. “The market is slowly searching for a bottom and testing investors’ patience,” said Wu Kan at JK Life Insurance in Shanghai. “Stocks are fluctuating in a small range near 2,800 amid waning turnover, as investors cautiously await clarity over issues such as the timing of U.S. rate hikes. Small rebounds, if any, will be followed by declines.”

Losing interest? Are we sure that’s the only reason?

• Chinese Buyers Are Losing Interest In Australian Property (BBG)

Buyers from China, often blamed for the sharp rise in home prices in Sydney and Melbourne, are starting to lose interest. In the first four months of the year, visits by potential buyers from China to realestate.com.au’s listings in New South Wales state, which has Sydney as its capital, declined 25% from the same period last year. Views of properties in Victoria state, whose capital is Melbourne, fell 8.9%, while the mining state of Western Australia saw the biggest drop of 35%, according to the portal, one of the nation’s two biggest property websites.

At some point China must retaliate.

• EU Warns China To Expect New Steel Tariffs (FT)

The EU has warned China that it faces new anti-dumping tariffs on steel, amid growing pressure for the west to block Beijing’s bid for “market economy status” and greater access to world markets. Speaking ahead of the G-7 summit in Japan, European Commission president Jean-Claude Juncker declared: “If somebody distorts the market, Europe cannot be defenseless.” The issue of Chinese steel exports will be discussed by G-7 leaders on Thursday against the backdrop of a steel crisis in many western countries, including Britain where efforts are under way to save Tata Steel’s UK operations. Draft language prepared for discussions on the G-7 communique, while not mentioning China, expresses concern about the excess supply of steel around the world and says it has distorted the global market.

A Japanese government official said the issue went beyond steel to other commodities as well. Juncker claimed Chinese overcapacity amounted to double the EU’s annual steel production and that it had contributed to the loss of “thousands of jobs since 2008”. “We will step up our trade defense measures,” he said. Juncker also said there would be an impact assessment of Chinese steel exports and detailed discussion on Beijing’s bid for market economy status under WTO rules. China expects to achieve that status in December on the 15th anniversary of its 2001 accession to the WTO, giving it greater access to world markets and making it harder for third parties such as the EU to impose anti-dumping sanctions.

So it’s G7, but not really, since Juncker and Tusk are also invited, while Putin and Xi are not. You make it up as you go along.

• Japan Fails in Bid to Have G-7 Warn of Global Crisis Risk (BBG)

Japanese Prime Minister Shinzo Abe failed in his bid to have Group of Seven leaders warn of the risk of a global economic crisis in a communique issued as their summit wraps up Friday in central Japan. The final statement declares that G-7 countries “have strengthened the resilience of our economies in order to avoid falling into another crisis.” Japan had pressed G-7 leaders to note “the risk of the global economy exceeding the normal economic cycle and falling into a crisis if we did not take appropriate policy responses in a timely manner.” On Thursday, Abe presented documents to the G-7 indicating there was a danger of the world economy careering into a crisis on the scale of the 2008 Lehman shock.

Abe has frequently said he would proceed with a planned increase in Japan’s sales tax in April 2017 unless there is an event on the scale of Lehman or a major earthquake. He is expected to announce next week he is deferring the tax rise, Japanese media reported. One of the biggest topics at the meeting was China, which is not a member of the G-7. A slowdown in China, alongside a global steel glut, has spurred concerns among developed economies and at times disagreement on how best to spur growth. Abe has advocated greater government spending to back up monetary policy action. The communique urged a coordinated, albeit differentiated, response to storm clouds gathering over the global economy. Leaders pledged to use a mix of tools depending on their circumstances.

Fast looming gloom: “70% of companies see no decisive escape from deflation for the foreseeable future, up from 48% in January”

• Corporate Japan Much More Downbeat About Escape From Deflation (R.)

Japan Inc has become increasingly pessimistic about the country’s ability to beat deflation, with the vast majority of firms now expecting no escape for the foreseeable future, a Reuters poll showed. Most Japanese companies also said they did not think Prime Minister Shinzo Abe’s latest growth strategy that centers on lifting the mininum wage and investment in technology would help bring significant improvement to a faltering economy. Abe swept into office three years ago with bold plans to end decades of deflation and bring about sustainable growth. But while unprecedented monetary policy in tandem with fiscal stimulus met with some initial success, any gains in ridding the country of a deflationary mindset look like they could be slipping away.

The Reuters Corporate Survey, conducted May 9-23, found 70% of companies see no decisive escape from deflation for the foreseeable future, up from 48% in January when the same question was asked. “Demand is not on an upward trend, and household spending is not rising because base pay is not rising,” wrote a manager at a chemicals company. “It has become difficult for companies to lift prices.” Japan has only managed very mild inflation since Abe took office and the pace of price gains has been slowing since 2014. Core consumer prices in March fell 0.3% from a year earlier, the fastest decline in three years due to lower oil prices. The survey also found that 79% of companies were worried that consumer prices could return to deflation either this year or next.

Stunning from earlier in the week. ‘Weaker producers’ are forced to flood the market, but with nothing in return.

• Debt Repayments In Crude Cripple Poorer Oil Producers (R.)

Poorer oil-producing countries which took out loans to be repaid in oil when the price was higher are having to send three times as much to respect repayment schedules now prices have fallen. This has crippled the finances of countries such as Angola, Venezuela, Nigeria and Iraq and created a further division within OPEC. Ahead of an OPEC meeting next week, poorer members have continued to push for output cuts to lift prices but wealthier Gulf Arab members such as Saudi Arabia, which are free of such debts, are resisting taking any action despite prices falling 60% in the past 2 years. Angola, Africa’s largest oil producer has borrowed as much as $25 billion from China since 2010, including about $5 billion last December, forcing its state oil firm to channel almost its entire oil output toward debt repayments this year.

This year Angola, Nigeria, Iraq, Venezuela and Kurdistan are due to repay a total of between $30 billion and $50 billion with oil, according to Reuters calculations based on publicly disclosed information and details given by participants in ongoing restructuring talks. Repaying $50 billion required only slightly over 1 million barrels per day (bpd) of oil exports when it was trading at $120 per barrel but with prices of around $40, the same repayment would require exports of over 3 million bpd. “All of those oil nations – Angola, Nigeria, Venezuela – have taken money for survival but haven’t got any money left for investments. “That is very damaging to their long-term growth prospects,” said Amrita Sen from Energy Aspects think-tank.

“People tend to look at current production volumes but if you have committed your entire production to China or other buyers under loans – then you cannot invest to keep growing and won’t benefit from higher prices in the future.” China has also become Venezuela’s top financier via an oil-for-loans program which since 2007 has funneled $50 billion into Venezuelan coffers in exchange for repayment in crude and fuel, including a $5 billion deal last September. While details of the loans have not been made public, analysts from Barclays estimate Caracas owes $7 billion to Beijing this year and needs nearly 800,000 bpd to meet payments, up from 230,000 bpd when oil traded at $100 per barrel.

But of course. Got to keep them sales going until they don’t.

• Wells Fargo Launches 3% Down-Payment Mortgage (CNBC)

First-time buyers and low- to moderate-income buyers have largely been sidelined by today’s housing recovery. The common cry is too-tight credit. Lenders have kept the credit box restrictive because they are gun-shy from the billions of dollars in buy backs and judicial settlements stemming from the mortgage crisis that they still face today. Now, the nation’s largest lender, Wells Fargo, says it is opening that box with a new low down payment loan — a loan it claims is low-risk to the bank. “We are fully underwriting the borrowers, we are partnering with Fannie Mae to originate and sell these loans, we are ensuring the borrowers have an ability to repay and that they’re qualified for home ownership, but we’re simplifying things for the homebuyer,” said Brad Blackwell, executive vice president and portfolio business manager at Wells Fargo.

Branded “yourFirstMortgage,” Wells Fargo’s new product has a minimum down payment of 3% for a fixed-rate conventional mortgage of up to $417,000. Down payment help can come from gifts and community-assistance programs. Customers are not required to complete a homebuyer education course, but if they do, they may earn a 1/8% interest rate reduction. The minimum FICO score for these loans, which are underwritten according to Fannie Mae standards, is 620. Mortgage insurance can either be rolled in to the cost of the loan or purchased separately by the borrower. Blackwell said either way, the monthly payment is less than a government-insured FHA loan. More importantly, it’s simpler than other 3% down payment products already in the market, some of which have specific income and counseling requirements.

“We’ve taken all the complexity of the home mortgage lending process, removed it from the front-line consumer, so that it’s easy for them to understand and Wells Fargo is taking care of all the capital markets and other types of complexities behind the scenes,” added Blackwell. Other 3% down payment products from Bank of America with Freddie Mac or Fannie Mae’s HomeReady program have not been popular because lenders find them bureaucratic and hard to use. “To the extent that Wells is using this product as liberally as they can, that’s a positive for most borrowers,” said Guy Cecala, CEO of Inside Mortgage Finance.

Sort of like Brexit, a discussion conducted on the wrong terms. It can’t only be about robots taking jobs. That is far too narrow. Economic collapse is a much larger factor.

• Universal Basic Income: Money For Nothing (FT)

Switzerland’s traditionally conservative electorate will next month vote on the superficially preposterous idea of handing out an unconditional basic income of SFr30,000 ($30,275) a year to every citizen, regardless of work, wealth or their social contribution. Opinion polls suggest the June 5 referendum will be heavily defeated. And even if some kind of electoral convulsion results in the proposal being unexpectedly approved by voters, it is certain to be shot down by the 26 cantons that would have to implement it. But the very fact that one of the world’s most prosperous countries is holding such a vote highlights how a centuries-old dream of radical thinkers is seeping into the political mainstream.

In countries as diverse as Brazil, Canada, Finland, the Netherlands and India, local and national governments are experimenting with the idea of introducing some form of basic income as they struggle to overhaul inefficient welfare states and manage the social disruption caused by technological change. Daniel Häni, a chirpy Basel entrepreneur who is one of the Swiss initiative’s main supporters, said modern welfare states provide basic social support but are failing to adapt to the needs and values of our times. The trouble is that they are too costly and cumbersome, assume that a citizen’s worth is determined solely by their value as an employee and rely on means testing by an overly intrusive state. “Our social system is 150 years old and is based on Bismarck’s response to Industrialisation 1.0,” he said. “Our idea is simple. We want to render the conditional unconditional. UBI is about shifting power back to the citizen.”

The idea of providing money for nothing to all citizens dates back centuries and was nurtured by a radical cult before resurfacing in recent times. In the 20th century it was championed by thinkers on the left, such as John Kenneth Galbraith and Martin Luther King, as a means of promoting social justice and equal opportunity. But it was also backed by some libertarians and economists on the right, including Milton Friedman, as a way of restricting the coercive state and restoring individual choice and freedom. Incredible as it seems today, President Richard Nixon came very close to implementing a negative income tax (a variant of basic income) across the US in 1970. Nixon’s initiative, part of his Family Assistance Plan, was strongly backed by the House of Representatives but failed in the Senate, where some Democrats considered it unambitious, and several Republicans considered it too bold.

Something tells me they will get to wait a lot longer.

• After 7 Years, UK Workers Still Waiting For Decent Pay Rises (FT)

Britain’s workers have gone seven years without a decent pay rise — and data published on Thursday suggest they will have to wait a while longer. In the three months to the end of April, the busiest month of the year for pay settlements, the median pay settlement dipped from 2% to 1.7%. XpertHR, the company that gathers the data, said almost half the awards were lower than the same group of employees received last year, while only a fifth were higher. Economics textbooks would not have predicted such figures. Wages are meant to rise when unemployment falls since there are fewer jobless people around who are willing to work for low pay. Yet though unemployment has dropped to a pre-crisis low of 5.1%, average wage growth remains stubbornly slow at about 2% a year — roughly half the pace that was typical before the crash.

Adopting the slogan “Britain deserves a pay rise”, the government has tried to force the issue by raising the minimum wage sharply in April but this does not seem to have affected average pay. Britain is not alone: wage growth has weakened across the developed world and economists in Germany and the US, where unemployment is similarly low, are just as puzzled. Employers are less mystified. “We keep referring back to the old world, where full employment meant pay should be rapidly rising but I think the new world we’re in now is [that] we have still got underemployment, low productivity and low inflationary environments, which means there’s no need to raise pay,” said James Hick, managing director of ManpowerGroup Solutions, which supplies 35,000 contractors and temps per week to UK employers.

There are plenty of lower-paid people who would work more hours if they could, said Mr Hick, which lessens the pressure on employers to pay more. The unemployment rate may be the same as it was in 2006 but 14% of part-time workers say they cannot find full-time work, compared with 9% a decade ago. [..] The most important factor in the long term is that Britain has suffered a productivity slowdown since the financial crisis, much like many other countries, including the US. British workers are now 14% less productive than they would have been if the pre-crisis growth trend had continued. Employer lobby groups such as the CBI say wages cannot rise sustainably until workers increase their output per hour.

Could have fooled me… Why else make such crazy claims?

• Cameron Denies Being A “Closet Brexiteer” (R.)

British Prime Minister David Cameron said on Friday he was not a “closet Brexiteer” and that leaving the European Union would hurt Britain’s economic future and complicate trade deals with countries such as Japan. Speaking at a meeting of the G7 industrial powers, Cameron rejected a description by a former aide this week that he secretly supported a vote to leave the EU at a referendum on June 23. “So I have never been a closet Brexiteer,” he told a news conference in Japan. “I am absolutely passionate about getting the right result, getting this reform in Europe and remaining part of it. It’s in Britain’s interests and that’s what it is all about.”

Almost funny.

• Australia Erased From UN Climate Change Report As Government Intervenes (G.)

Every reference to Australia was scrubbed from the final version of a major UN report on climate change after the Australian government intervened, objecting that the information could harm tourism. Guardian Australia can reveal the report “World Heritage and Tourism in a Changing Climate”, which Unesco jointly published with the United Nations environment program and the Union of Concerned Scientists on Friday, initially had a key chapter on the Great Barrier Reef, as well as small sections on Kakadu and the Tasmanian forests. But when the Australian Department of Environment saw a draft of the report, it objected, and every mention of Australia was removed by Unesco. Will Steffen, one of the scientific reviewers of the axed section on the reef, said Australia’s move was reminiscent of “the old Soviet Union”.

No sections about any other country were removed from the report. The removals left Australia as the only inhabited continent on the planet with no mentions. Explaining the decision to object to the report, a spokesperson for the environment department told Guardian Australia: “Recent experience in Australia had shown that negative commentary about the status of world heritage properties impacted on tourism.” As a result of climate change combined with weather phenomena, the Great Barrier Reef is in the midst of the worst crisis in recorded history. Unusually warm water has caused 93% of the reefs along the 2,300km site to experience bleaching. In the northern most pristine part, scientists think half the coral might have died. The omission was “frankly astounding,” Steffen said.

The German view of a doomed deal.

• ‘Disaster in the Making’: The Many Failures of the EU-Turkey Refugee Deal (Sp.)

It is becoming increasingly difficult to maintain the claim that Turkey is a safe place for refugees. According to Amnesty International, Turkish authorities have deported hundreds of refugees from Turkey back to Syria in recent months. In early May, Human Rights Watch documented the cases or five Syrian refugees who were shot dead while attempting to enter Turkey, allegedly by Turkish border troops. The Syrian Observatory for Human Rights reported 16 deaths at the Syrian-Turkish border between December 2015 and March 2016. The EU has sent 390 migrants from Greece back to Turkey since early April, far fewer than planned. About 8,000 migrants, a third of them Syrians, remain in the Aegean islands. The European Commission now believes that Greek appellate judges may stop one in three deportations of Syrians.

“This strikes at the core of the deal,” said a senior Brussels official. Europe’s goal with the Turkey agreement is deterrence. In recent weeks, a number of migrants have indeed chosen not to leave Turkey for Greece, fearing that they would be sent back. If it now emerges that the Greeks are not deporting migrants nearly as quickly as anticipated, many more refugees could risk the voyage across the sea again soon, predicts Metin Çorabatir, chairman of the Ankara-based Research Center on Asylum and Migration (IGAM). But the camps on the Greek island are already overcrowded. Food is scarce and migrants have set garbage cans on fire to protest conditions in the camps. “We don’t know what we’ll do if even more people arrive,” says an official with the Greek Ministry of Migration. Political consultant Knaus calls it a “disaster in the making.”

Nevertheless, the EU is clinging to the deal, despite the tense climate between Brussels and Ankara. Erdogan has threatened to cancel the agreement altogether if EU refuses to grant Turkish citizens visa-free travel, while Europe has countered that Ankara needs to reform the Turkish anti-terrorism law first, as agreed. The Turkish president hardly misses an opportunity to show that he couldn’t care less about what Europeans think – of his plan, for instance, to revoke the immunity of members of parliamentarians who refuse to toe the line, so that they can then be sidelined with the help of the judiciary. And now that Prime Minister Ahmet Davutoglu has been ousted, the EU has lost a level-headed dialog partner in Turkey. His successor, Transportation Minister Binali Yildirim, is seen as an Erdogan acolyte.

Thousands are being rescued every single day. The idea that you can just stop the flow is a lethal illusion. But still no emergency UN meetings.

• Up To 80 Dead In Shipwreck Off Libya (MEE)

Up to 80 people are feared dead after a shipwreck off Libya, while at least 50 refugees and migrants have been rescued from the waves, the EU’s naval force said on Thursday. The wreck comes during a week in which more than 6,000 migrants and refugees have been rescued by Libyan, Italian and other authorities off the coast of Libya. On Thursday, a Luxembourg reconnaissance plane spotted the capsized boat around 64km off the Libyan coast with about 100 refugees and migrants in the water or clinging to the sinking vessel, captain Antonello de Renzis Sonnino, spokesman for the EU’s Sophia military operation to combat people smugglers in the Mediterranean, told AFP. The Spanish frigate Reina Sofia and Italian coast guard raced to the scene and threw life-floats and jackets to those in the water.

“Unfortunately, there were bodies too,” de Renzis Sonnino said, adding that the rescue operation was still ongoing. In photographs released by EUNAVFOR MED on Twitter people could be seen waving their arms for help as they balance perilously on the deck of the boat, already underwater but clearly visible in the limpid aquamarine sea. The shipwreck followed sharply on the heels of a disaster on Wednesday when a migrant boat overturned leaving five people dead, and another sinking on Tuesday which left a baby girl orphaned after both her parents died. Video footage of the incident released by the Italian navy showed people toppling into the sea as the overcrowded vessel capsized. A bout of good weather as summer arrives has kicked off a fresh stream of boats attempting to cross from Libya to Italy. The survivors will be added to the list of nearly 40,000 migrants and refugees to arrive in the country’s southern ports so far this year.