M.C. Escher Fish and Boat 1948

https://twitter.com/robertdunlap947/status/2067352902713196650?s=20 https://twitter.com/AmericaPartyX/status/2067243242127503555?s=20

https://twitter.com/VictoriaSask/status/2067407714498551928?s=20Elon Musk to the British people:

— Taya Bass (@travelingflying) June 16, 2026

“You’re in a fundamental situation here where you, whether you choose violence or not, violence is coming to you.

You either fight back or you die.” pic.twitter.com/JharlkWQHF

Not many illustrations today or other things that break the text monotony, and I even double-checked. Sorry for that. “First, can Americans somehow believe that Iran will uphold its commitments, given its history of deceiving and lying at every turn? Second, what does this mean for Trump’s legacy and successor plans ..”

• Trump Ties His Name and Credibility to Vance’s Dubious Iran Diplomacy (Hammer)

Donald Trump has been the greatest, most clear-eyed and most transformative foreign policy president of my lifetime. But Trump is also the famed businessman who wrote The Art of the Deal four decades ago. There has therefore always been the risk that the president’s novel and often unorthodox approach to foreign policy could be subsumed by a greater dealmaking imperative.Read more …

Prudent statesmanship on the world stage requires setting clear ends and then working backward to calibrate the appropriate means — diplomatic, economic, military or otherwise — to achieve those ends. Because of his dealmaking background, Trump — despite all his foreign policy successes — was always uniquely vulnerable to confusion of means and ends, prioritizing a deal itself above any end that a deal might be meant to secure.That is how we got to this troubling week in U.S. foreign policy — namely, the deeply flawed new “memorandum of understanding” between the U.S. and the Islamic Republic of Iran, which represents the single greatest subsumption of noble ends into politically convenient means in at least a decade of American diplomacy.

The Iran appeasement, primarily negotiated and championed by Vice President JD Vance but ultimately bearing Trump’s signature, raises at least two crucial questions. First, can Americans somehow believe that Iran will uphold its commitments, given its history of deceiving and lying at every turn? Second, what does this mean for Trump’s legacy and successor plans, as it pertains to the Middle East and 2028 presidential hopefuls?

We shouldn’t mince words on the first issue. To place trust in Iran’s fanatical Islamist leadership is not merely naive — it’s delusional. For decades, Iran’s apocalyptic Shiite theocracy has demonstrated a consistent pattern of deception and hostility, undermining any notion that it can be a reliable partner in Western diplomacy. The history of Iranian negotiations is littered with broken promises, yet the administration — with Vance as its most prominent salesman — somehow argues this time will be different. There is zero reason for thinking that will be the case. The mullahs are still in charge, after all. As Roger Daltrey of the Who famously said in the hit 1971 song “Won’t Get Fooled Again”: “Meet the new boss / Same as the old boss.”

This current MOU looks shockingly similar to former President Barack Obama’s catastrophic 2015 Joint Comprehensive Plan of Action — a deal that Trump, shortly before withdrawing the United States from the pact in 2018, correctly excoriated as the “worst deal ever negotiated.” Under the guise of diplomacy, the plan said nary a word about Tehran’s formidable ballistic missile arsenal, allowed Iran to continue its nuclear ambitions, and provided the regime with a windfall — or, more accurately, literal pallets — of cash to fund its regional terror proxies.

What exactly is different with the current deal? The mind reels. The new MOU, with its quixotic presuppositions, risks repeating all those same grave mistakes. At its outset earlier this year, Operation Epic Fury had four reasonably clear goals: a truly free Strait of Hormuz, an end to Iran’s funding of its sprawling terror proxy network, an end to Iran’s ballistic missile threat, and a final resolution of the nuclear issue. The current agreement fails to achieve a single one of those American goals.

The Iranian regime, long guided by the sharia doctrine of taqiyya, has always viewed negotiations with Western powers as a strategic tool to buy time while advancing its nuclear capabilities, exporting jihad and sowing discord across the region. To imagine that Iran will suddenly embrace a spirit of good-faith cooperation is simply preposterous. No one actually believes that — including Trump’s own CIA director, John Ratcliffe.

We should also consider how this appeasement affects Trump’s Middle East legacy and, looking toward 2028, possible successor plans. Up until the April 8 ceasefire, Trump evinced a life’s work of consistent toughness toward the world’s No. 1 state sponsor of terrorism — a regime whose revolutionaries’ very first action, in 1979, was to storm the U.S. embassy in Tehran and commence a 444-day hostage crisis. To cap off the fiery and effective Epic Fury on such a limp note, without a single American goal having been achieved, is to jeopardize that legacy.

What is the point, after all, of winning the war but losing the peace? On Wednesday, Trump celebrated the signing of the MOU at a dinner with French President Emmanuel Macron at Versailles. The profound symbolism of having that particular dinner at that particular location, intimately associated as it is with tragically flawed peace accords, cannot be ignored.

It seems, then, that Trump is placing a high-stakes wager on his Middle East legacy on his credulous vice president. As Trump said at the G7 summit earlier this week in France: “If (the Iran deal) works out, I’m going to take the credit. If it doesn’t work out, I’m blaming JD.” Perhaps Trump meant that comment in jest — but perhaps he didn’t. The buck stops with the commander in chief, but maybe this has also been a trial run for Vance as he gears up for a likely 2028 run. If so, it has not been a particularly impressive one. No intellectually honest person can deny that Iran comes out the big winner from yet another futile exercise in kicking the nuclear (and missile) can down the road.

Throughout this ordeal, many Iran hawks have asked, “Where is Marco Rubio?” Rubio, like Ratcliffe and War Secretary Pete Hegseth, allegedly lobbied Trump against the deal. Perhaps the answer, in a possibility raised by the Los Angeles Times on Thursday, is that Rubio is deliberately missing in action: He is letting Vance “take the fall” if (when) the deal inevitably implodes. If Trump cares about preserving his legacy on the world stage, then, ironically, his best remaining hope may well be for Rubio to clean up this mess.

“Once we were at war, the proper solution was to force Hormuz back open. We even learned last week that Trump ordered elements of the 82nd Airborne Division to Israel for just such an eventuality.”

• The Iran War Was Easy. The Peace Is the Problem. (Stephen Green)

When President Donald Trump ordered the start of Operation Epic Fury on February 28, like many people I assumed a brief air campaign to further degrade Iran’s nuclear weapons program. The instigator was Iran’s own negotiators, who boasted to Trump advisor Steve Witkoff that they had produced enough nuclear material for nearly a dozen weapons. All Tehran needed to do was make the final uranium enrichment step from 60% to 90%, then assemble the warheads. Neither Trump nor Israeli Prime Minister Bibi Netanyahu — whose nation former Iranian president Mahmoud Ahmadinejad called a “two-bomb country” — had a choice in the matter. It was either war then or nuclear blackmail later. Or worse.We went to war. I cheered it on.Read more …

Milblogger and retired Navy officer CDR Salamander put it better than I did at the time, writing that “I support the strikes on Iran because it firmly fits into a view I have held on the use of national military power for decades.” Sal was writing in support of the age-old Great Power custom of punitive expeditions — brief and often impressively violent campaigns to bloody a smaller enemy without all that “Pottery Barn Rule” nonsense that Colin Powell saddled our strategic thinking with a quarter century ago. “Nation building OPLANS again? No. Not any more. Breaking their things and killing their worst leadership that endangered the USA and her allies? I’m in.” Me too.Now the Memorandum of Understanding is public, and I must ask: How in the hell did we get to this from where we started on Feb. 28? • Ceasefire: Immediate/permanent end to military ops (incl. Lebanon); no future attacks/threats; respect sovereignty/Lebanon integrity. • Non-interference: Respect sovereignty/territorial integrity; no internal meddling. • Timeline: Negotiate final deal in max 60 days (extendable). • U.S. Actions: Lift naval blockade (start immediately, full in 30 days); withdraw forces post-deal; $300B+ reconstruction plan; end all sanctions (UN/US) per schedule; oil export waivers; release frozen funds/assets. • Iran Actions: Safe commercial shipping (Hormuz/Gulf, 60 days free); no nuclear weapons; maintain nuclear status quo; down-blend stockpile under IAEA. • Interim: Status quo maintained; monitoring mechanism; final deal via binding UNSC resolution.

There’s so much to pick apart here, but there are really only three things that matter: “Status quo,” “End all sanctions,” and “$300 billion.” As for the efficacy of a denuclearization plan involving the UN… I just throw my hands up in the air. I spent weeks coming up with or sharing other people’s attempts to explain what Trump was thinking, from the “rug-merchant” delay strategy to the “there’s no one left there with the authority to negotiate” conundrum. But reading these bullet points, you have to wonder if they weren’t having the exact same discussion inside the White House, right up until the very end.

Here’s a big tell about what the MOU is worth. The two strongest foreign policy hands on Team Trump — Secretary of State Marco Rubio and War Secretary Pete Hegseth — seem to be doing their best to maintain radio silence while JD Vance does the P.R. blitz. Axios reported on Monday that “[CIA Director John] Ratcliffe isn’t the only skeptic in Trump’s top team. In internal discussions, Secretary of State Marco Rubio and Secretary of Defense Pete Hegseth both expressed concerns and raised questions about the memorandum of understanding.”

“As Vance emerges as the spokesman for the deal, Secretary of State Marco Rubio has raised eyebrows across the political world with his near-total absence. Rubio, who has taken on multiple roles in the administration,” Mediaite reported Thursday, and “was central to the Iran negotiations up until the last week or so, in which Vance, Jared Kushner, and Steve Witkoff stepped in to rush to finalize an end to hostilities.”mI’ve said here before that Witkoff is one of the very few weak parts of Trump 47, and if those are his fingerprints all over this MOU, then I’ll say it again.

Netanyahu is also nowhere to be seen, following months of standing shoulder-to-shoulder with the administration. The biggest mistake was a ceasefire that effectively locked in Tehran’s control of Hormuz. The clock started ticking on the Islamic Republic the moment the bombs started falling almost four months ago. The clock started ticking on the global economy the moment Tehran more or less closed the Strait.

As Trump himself put it in France on Thursday, “I didn’t want to see economic catastrophe. If you kept this [war] going, that could have happened.” He added, “It could have caused an international depression.” Once we were at war, the proper solution was to force Hormuz back open. We even learned last week that Trump ordered elements of the 82nd Airborne Division to Israel for just such an eventuality.

“.. we have to react disproportionately any time they break the agreement..”

• Victor Davis Hanson: The Biggest Test of the Iran Deal: Enforcement (Bolt)

Victor Davis Hanson, a military historian and senior fellow at the Hoover Institution, said the biggest test of the Iran deal will be how the United States enforces it, as the full text of the memorandum of understanding was finally released Wednesday. Hanson said he’s not entirely worried about the core issues, like issues surrounding the enriched uranium or opening the Strait of Hormuz. He explained that Iran needs the Strait open nearly as much as the rest of the world due to the economic pressures currently on the country, and U.S. intelligence can track enriched uranium so precisely that if Iran moves toward building a nuclear weapon, the U.S. can immediately resume a bombing campaign.Read more …

However, the very real threat of those attacks, or other serious U.S. action against Iran, will determine how closely Iran complies with the rest of the agreement and broader American interests.https://twitter.com/seanhannity/status/2067420491967791267?ref_src=twsrc%5Etfw%7Ctwcamp%5Etweetembed%7Ctwterm%5E2067420491967791267%7Ctwgr%5Ee67877b70d719b47e684bf23fb0ffddee91ad04b%7Ctwcon%5Es1_c10&ref_url=https%3A%2F%2Ftownhall.com%2Ftipsheet%2Fdmitri-bolt%2F2026%2F06%2F18%2Fvictor-davis-hanson-the-biggest-test-of-the-iran-deal-comes-down-to-one-thing-enforcement-n2677936

“So the two chief issues I’m not so worried about,” Hanson said. “I think we know where the enriched uranium is, it’s sealed, we have great intelligence, we can bomb it, bomb it, bomb it, we can hit more of their industrial complexes if they cheat, and they will open the Strait of Hormuz because they’re just about broke.”

“The other things are known unknowns. It’s going to be more difficult to ensure they’re not giving money to Hezbollah, the Houthis, and Hamas. That’s more murky, and we don’t know what they’re going to do in Lebanon. And then, of course, we don’t know what’s going on in Iran, because this is the first real air war,” he continued. “We don’t have boots on the ground, we don’t have embeds, but we will learn very shortly, and we’re going to get an idea of just how much damage was done. I think it might have been half a trillion dollars or more in the nuclear military-industrial complex.”

We don’t know the mood of the people. Are they going to come out and say to their own government, you mean we lost everything we had, and now you could have done this peacefully? Instead, you acted so tough, you were humiliated, and now we’re broke and destitute, and all you had to do was agree in the first place. And then we don’t know how the government will react to that. There could be a widespread uprising. We don’t know what we’re going to do if they try to kill another 40,000 people. “So the main denominator, though, that has to be ironclad is we have to react disproportionately any time they break the agreement,” Hanson added.

This comes as concerns have been raised about the memorandum, which essentially serves as an extended 60-day ceasefire to allow negotiating parties to work out the technical details of a more lasting peace deal. The concerns primarily center on the fact that those technical details remain unworked, including how the United States will ensure Iran abandons its nuclear weapons pursuit, how it will prevent Iran from funding its terror proxies in the region, and how the agreement will serve as more than empty commitments by the Iranians.

The Trump administration has maintained that enforcement will hinge on financial incentives: a $300 billion reconstruction fund, an upfront arrangement allowing Iran to immediately begin selling its oil, and U.S. vows to free up sanctioned money and assets upon Iran’s compliance. President Trump also said Wednesday he has no problem resuming military strikes if Iran begins to play games.

“As Dwight Eisenhower himself said as early as 1951, if in ten years all American troops stationed in Europe for national defense purposes have not been returned to the United States, then this whole process will have failed.”

• Secretary of War Pete Hegseth Just Tore Into NATO (Bolt)

Secretary of War Pete Hegseth tore into NATO on Thursday, branding the military alliance a paper tiger and demanding Europeans finally take responsibility for their own defense. Hegseth went on to call for a return to “NATO 1.0,” the era when Europeans understood that NATO’s power came not from “small flags on fancy tables” but from “warriors.” It’s a feature of the military alliance that Europeans have been happy to ignore, vastly preferring the negotiating table, meetings, and international governing bodies over legitimate, hard defense.Read more …https://twitter.com/EricLDaugh/status/2067581391986921892?ref_src=twsrc%5Etfw%7Ctwcamp%5Etweetembed%7Ctwterm%5E2067581391986921892%7Ctwgr%5E4de527fd700b140c5d10de1007d956d0ec7fea42%7Ctwcon%5Es1_c10&ref_url=https%3A%2F%2Ftownhall.com%2Ftipsheet%2Fdmitri-bolt%2F2026%2F06%2F18%2Fpete-hegseth-just-tore-into-nato-n2677940

“For too long, NATO has been a paper tiger and a one-way street. No more,” the Secretary of War said. “And that’s what the Hague Summit is all about. That’s what defense spending commitments are all about. Transforming NATO back into a real military alliance that’s focused on hard power and real deterrence.”A NATO 3.0 modeled on the NATO 1.0 that won the Cold War, with our allies actually taking the lead in Europe’s conventional defense. And that’s what NATO was always supposed to be and what its framers like President Eisenhower always expected. Europe was not supposed to be a dependency of the United States. That’s not what Winston Churchill, Charles de Gaulle, or Conrad Adenauer wanted or expected. No, Europe was supposed to be a military power allied with a strong America. This is the essence of NATO 1.0. As Dwight Eisenhower himself said as early as 1951, if in ten years all American troops stationed in Europe for national defense purposes have not been returned to the United States, then this whole process will have failed.

“Eisenhower was Supreme Allied Commander then, not yet our nation’s 34th president. But he and his allied counterparts, all of them still living in the shadow of World War II, understood that NATO’s power did not come from committees or from meetings or from small flags on fancy tables. It came from warriors,” Hegseth said. “And for Europe’s defense, it had come from NATO allies.”

This comes as President Trump has voiced massive displeasure with European allies, especially amid the war in Iran. The U.S. launched military strikes without consulting NATO partners, and Europe flatly refused to directly assist, a move Trump called “shameful” and uncharacteristic of allies. He went on to say that the Europeans “haven’t been friends when we needed them” and threatened to punish the military alliance by potentially reviewing whether to withdraw American troops from Europe altogether.

European powers, for their part, have agreed to a new distribution of senior leadership across NATO’s Command Structure, giving Europe more control of the alliance’s military operations. They now control all three Joint Force Commands, UK leads Norfolk, Italy leads Naples, and Germany and Poland share Brunssum. The U.S. still maintains key theater commands, but the move is clearly a step toward a more Euro-centric NATO that sidelines Washington from the alliance’s top decision-making positions.

It’s Britain all the way.

• Britain Bought The Keys To Ukraine’s Nuclear Future – What’s Next? (Ostashko)

The UK has once again stormed into Ukraine with the grace of an old imperial administrator that goes about rearranging the furniture. But in reality, things are quite serious. UK Prime Minister Keir Starmer’s decision to finance the supply of enriched uranium for Ukrainian nuclear power plants over the next two years has nothing to do with commerce. Through this deal, London de facto gains access to the most sensitive sector of the Ukrainian state.Read more …

In a country where nuclear energy accounts for more than half of all power generation, control over nuclear reactors means direct control over industry, logistics, communications, and the viability of cities, especially in winter. On the surface, the plan is flawless: the UK is acting out of concern for energy security, offering support to its partner, and strengthening Kiev’s resilience. But behind the glossy facade lies a classic debt trap and a new level of external control.The British have arranged things very well. Ukraine gets the physical resources, the allocated funds immediately return to the UK, and London becomes entrenched in Ukraine’s strategic sector for decades. Following the pain of Brexit, the UK is desperately trying to make a comeback into European politics, and now is an excellent opportunity to do so by means of Ukrainian nuclear energy. We may already see a long and complex technological chain behind the current supplies of uranium: Urenco is responsible for enrichment, Westinghouse provides nuclear fuel assemblies, and the construction of new AP1000 reactors looms on the horizon.

The Soviet nuclear legacy is being systematically replaced by Western companies. This transition will inevitably entail changes in standards, licensing, long-term maintenance, personnel training, and most importantly, the disposal of spent nuclear fuel. Whoever embarks on this path today guarantees themselves the right to dictate the terms of the Ukrainian energy sector for decades to come. This expansion poses direct risks for Russia and Belarus. The Rovno Nuclear Power Plant is located close to the Belarusian border, and operating the old Soviet reactors requires great engineering precision and strict discipline.

In the context of a protracted military conflict, any managerial lapse, technical failure, or political mishap could instantly escalate into a regional catastrophe. The West is steadily consolidating the military, financial, and nuclear components into a cohesive anti-Russia front. While the UK capitalizes on this process, converting it into status, defense contracts, and influence, Ukraine is once again allocated the historical role of a battleground for foreign geopolitical interests.

“The latest Western idea to prop up the Zelensky regime and compensate for weapons shortages could flop right at the start..”

• G7 Considering Licensed Arms Production In Ukraine: Why Now? (RT)

The G7 group is considering providing Ukraine with licenses to allow domestic production of Western weaponry, including anti-aircraft and long-range missiles. RT looks into why the West is doing this so late in the conflict and Ukraine’s ability to deliver on mass arms production.Read more …

The scheme

The G7 made the announcement in a joint statement following its summit in Geneva, stating it had agreed to “increase the delivery of air defense capacities, additional systems and interceptors, and long-range capabilities.” “We are also ready to consider extending to Ukraine the benefit of licenses to allow for an increase in Ukraine’s military production,” the group said in a statement. The plan also involves US manufacturers granting licenses to EU military-industrial companies in order to compensate for shortages in production of high-demand weapons, according to German Chancellor Friedrich Merz. “We are all currently producing too little, and this can be offset by granting licenses to companies that have these production capabilities, including European and Ukrainian firms,” Merz told reporters.How is the scheme supposed to work?

The US rarely grants weaponry production licenses to its partners, pressing them into buying ready-made products instead, or in some instances, creating overseas manufacturing plants without transferring technologies to the third parties. The enduring need to supply Ukraine, as well as the extensive use of assorted munitions during the US-Israeli attack on Iran, however, could have softened Washington’s stance on the outsourcing of arms manufacturing. US President Donald Trump has confirmed the licensed production of anti-aircraft missiles for Patriot systems in Ukraine is under consideration, specifying that no decision has been made yet. “They would like to be able to do that, we’ll take a look at it. They have asked about it,” Trump told reporters on Wednesday.Over the past few years, Kiev has repeatedly urged Washington to grant it licenses to manufacture such munitions. The US, however, has consistently rejected the idea, while the American arms giants have reportedly been very wary of making any investments in Ukraine due to the obvious risks connected to the ongoing conflict with Russia.

Does Ukraine have actual industrial capacities?

Setting up a full-cycle production of sophisticated weapons in Ukraine seems to be highly improbable, given the country’s shrinking industrial capacities, as well as questionable record of local arms manufacturers. While Kiev inherited a well-developed industry after the collapse of the Soviet Union, it has been in decline ever since, with the process further accelerated by the civil conflict in formerly Ukrainian Donbass and the subsequent war against Russia, given that a bulk of plants were located in the east of the country.One of the flagship Ukrainian ‘domestically built’ weapons, the Bogdana self-propelled howitzer, appears to have little to nothing Ukrainian in it. The howitzers are chambered for 155mm NATO rounds manufactured in the West, while assorted heavy-duty trucks made by European manufacturers have been used as the chassis for the systems. The origins of the barrel itself are also debatable, given Ukraine’s poor record in making even the most basic artillery pieces. For instance, the infamous mortar M120-15 Molot, a copy of a Soviet-era design manufactured by Ukraine since 2016, has repeatedly made the headlines over deadly detonations of shells in its barrel and other malfunctions.

The supposedly domestically built Ukrainian weapons, mainly assorted drones, are at best assembled locally from components supplied from abroad. The hyped FP-5 Flamingo cruise missile also gives a glimpse of Ukraine’s real industrial capacities. The missile has emerged as a parts-bin project, with design features varying from one piece to another, a US-made free-fall bomb used as its warhead, and antique Soviet-era AI-25TL engines, believed to be recovered from scrapped trainer aircraft, used for propulsion.

Why is the West doing this now?

In mid-April, the Russian Defense Ministry published a list of Ukraine-linked military production facilities scattered across Europe and beyond. The military said it had identified such sites in the UK, Germany, Denmark, the Netherlands, Latvia, Lithuania, the Czech Republic, and Poland, as well as in Türkiye and Israel.The list came with a dire warning. “The implementation of terrorist attack scenarios against Russia… using supposedly ‘Ukrainian’ UAVs manufactured in Europe is leading to unpredictable consequences,” the ministry stated. “Instead of strengthening the security of European states, the actions of European rulers are rapidly drawing these countries into a war with Russia,” it added. The licensing scheme could be a part of the effort to further decentralize arms production to avoid potential retaliatory strikes from Russia, as well as to disguise the supplied weaponry as a Ukrainian homegrown product.

One drone assembly site destroyed in a Russian strike was accidentally exposed this week by the Ukrainian media. A warehouse at the Dovzhenko Film Studios in Kiev, which was allegedly used to store some “unique costumes,” had multiple aircraft wings visible in its rubble, with the parts appearing to be consistent with FP-1/2 drones produced by Vladimir Zelensky’s favorite and corruption-scandal-plagued company Fire Point.

From TASS Press Review. Origin is either Izvestia, Vedomosti or Nezavisimaya Gazeta.

• EU Pushes Trump On Russia Policy As Moscow Warns On Greenland Militarization (TASS)

The Europeans appear set to bend US President Donald Trump to toughen his stance on Russia, as Moscow and Tehran move to coordinate their actions at the UN to lift sanctions. Meanwhile, Russia has cautioned against continued militarization of Greenland. These stories topped Thursday’s headlines in Russia.Read more …

US President Donald Trump is trying to resolve the Ukraine conflict and is reluctant to assess actions by his Russian counterpart, Vladimir Putin, even as he is ready to consider putting more sanctions on Moscow and supplying missiles, including manufacturing air defense missiles for the Patriot system under license in Ukraine, the US leader himself said at a news conference with Indian Prime Minister Narendra Modi on the sidelines of the G7 summit on June 17.He specified that partial reintroduction of restrictions on Russian energy will depend on market price dynamics. It’s worth noting that, on Wednesday, the US Treasury did not extend its waiver of sanctions on Russian oil. Shortly prior to that, on the night of June 16, G7 leaders released a joint statement on geopolitical issues in which they reaffirmed their “unwavering support for Ukraine” and agreed to increase “the delivery of air defense capacities,” and “long-range capabilities’ as well as to strengthen their sanctions on Russia, including on its oil and gas sector. On June 16, Trump held talks with Vladimir Zelensky.

The Europeans are seeking to make Trump reverse the understandings reached at his meeting with Putin in Anchorage in August 2025, Dmitry Suslov, Deputy Director of the Center for Comprehensive European and International Studies at the Higher School of Economics, told Vedomosti. According to him, Brussels would like to introduce a new format of talks with their participation. “They advocate for a format without withdrawal of Ukrainian troops from the rest of Donbass but with deployment of troops from the coalition of the willing in Ukraine,” the expert explained. The Europeans understand that if Trump adopts such a stance, this will actually disrupt talks, but they are not ready for a full cessation of negotiations either as they realize that Ukraine is losing, he argued.

“He is currently facing a much weaker internal and external political situation than at the Anchorage meeting,” Suslov continued. For example, he can no longer threaten Kiev with reduced aid as the bulk of it now comes from the EU. In addition, Trump is looking for European support in the gradual reopening of the Strait of Hormuz. The Europeans are pursuing the goal of buying Trump on Ukraine and putting pressure on Putin through him, while also strengthening Zelensky’s negotiating position, but they are unwilling to disrupt talks, Pavel Koshkin, senior researcher at the Russian Academy of Sciences’ Institute for US and Canadian Studies, maintained.

As regards the prospect of the Europeans eventually sitting down to the negotiating table, this seems possible as the US cannot ignore its key allies in the region, despite the accumulated differences. “Trump will continue to maneuver further down the road. His goals are still the same: he is still seeking a meeting between Putin and Zelensky. And if this requires involving the Europeans, he could perhaps propose these ideas to Putin. For if Russia actually views the EU as an indirect party to the conflict, a durable peace is unlikely to be agreed without the EU,” Koshkin concluded.

Moscow and Tehran are coordinating their actions at the United Nations to lift all sanctions on Iran, Russian Deputy Foreign Minister Alexander Alimov told Izvestia. They actually secured the support of 16 additional states here. The memorandum of understanding (MoU) signed between Iran and the United States last night includes a provision on lifting restrictions. A 60-day period of talks will begin next, at which Tehran will concentrate on the nuclear problem and sanctions, the Islamic Republic’s MFA said. However, given the number of sanctions, this may turn into a very complicated legal process. For the time being, only pinpoint energy waivers that will greatly facilitate oil sales for Iran seem more likely.

On Wednesday night, two days ahead of the scheduled date, the United States and Iran separately signed a pre-agreed MoU. Without taking account of waivers post the 2015 nuclear deal, it can be said that the Islamic Republic has been under strict restrictions since its foundation, or for almost half a century already. Meanwhile, Harare, the capital of Zimbabwe, recently hosted a meeting of the Group of Friends in Defense of the UN Charter. Apart from Russia and Iran, it was attended by 16 other countries, including China. Among other topics, the Group has constantly focused on countering unlawful sanctions, including on Iran.

In general, lifting restrictions still seems to be the most challenging process, in light of their number. More than 6,000 sanctions have been imposed on Iran – Russia alone is under even more sanctions. The bulk of those was imposed by the United States. And cancelling relevant UN Security Council resolutions will obviously cause the most difficulties. A new resolution will be needed for this. And given the dozens of failed attempts at the UN to adopt at least some resolutions, not to mention the split in the Security Council, this will constitute the biggest challenge in purely technical terms.

Only the lifting of energy sanctions can be realistic in the near future, experts say. “Restrictions on ship freight, tanker insurance, logistics operations, and financial transactions in the oil industry and with hydrocarbons may be lifted,” Yekaterina Arapova, head of a research program at the Institute of International Research at MGIMO University, told Izvestia.

Despite the fact that Iran cannot currently sell all the oil it can produce amid the sanctions, the country is among the top 10 major exporters, therefore if operations with crude oil are greenlighted, this may seriously change not only the republic’s economy but also the situation on global markets. “If sanctions are lifted on Tehran, then it will not make much sense for China to buy exclusively Iranian oil. And there will remain only one supplier who could offer a discount due to the sanctions pressure, and that is Russia. The Americans have already `torn Venezuela away’ from China. Moreover, the increased demand from China will intensify competition for Russian oil with India, and this will enable Russia to slash the discount,” Igor Yushkov, leading expert at the Financial University under the Russian Government, told Izvestia.

Is the west simply going to deny it’s needed?

• Denazification of Germany, France, Britain, Sweden, Canada (Helmer)

Russian officials are insisting in private that tomorrow’s (June 19) signing of the US-Iran Memorandum of Understanding (MoU), with its fourteen points, is the signal for finalizing a similar multi-point term sheet for agreement with the US to halt the war on the Ukrainian battlefield.Read more …

They also insist — add sources in a position to know — that the Trump Administration is promising the lifting of US sanctions on the Russian oil trade and on the alternative fleet which has been carrying these oil cargoes to buyers in India, China, Turkey, and elsewhere. The sources claim that the Russian military plan for the peace pause assumes a ceasefire, including a halt to Ukrainian drone attacks, for at least the remaining two years of President Donald Trump’s term – longer if he is succeeded by Vice President JD Vance or by one of Trump’s sons. The Russian intelligence forecast is for a Republican victory in the 2028 presidential election.

If the future is this rosy, or if it only looks that way through rose-coloured glasses, what is to become of the UKRAINIZATION of drone warfighting operations now extending across the NATO bases, NATO drone manufacturing plants, and NATO exercises, deployment, and operational plans to prepare to fire them at Russian targets?

What is to become, also, of the AMERICANIZATION of security for Russia in Europe which President Vladimir Putin insists he discussed – one on one and in fluent English – and agreed with Trump at their Anchorage, Alaska, summit meeting last August 15? This is what Russian officials call the Anchorage Formula – it means trust in Trump to deliver a security guarantee protecting Russia from the drone, missile, and other attacks currently under way on the Russian hinterland, on Crimea and the Donbass, and on Russian oil and gas cargoes moving to market on the high seas.

The Russian General Staff and its chief intelligence officer, Admiral Igor Kostyukov, believe that Americanization will put a pause on Ukrainization for at least the year ahead. These officers don’t give any credit for negotiating this pause to Kirill Dmitriev, Putin’s special negotiator with Trump’s bagmen, Steven Witkoff and Jared Kushner; nor to the individual bribe schemes and slush funds they have been discussing together.

And so the sources in a position to know are asking each other — if Ukrainization and Americanization are about to be implemented by an MoU-type paper for at least a year or two, what about the DENAZIFICATION of the regime currently ruling the Ukraine? That has been a Russian war objective from the beginning of the Special Military Operation. It has been operationalized on term sheets in the Istanbul and Abu Dhabi talks as regime change in Kiev by an election to replace Vladimir Zelensky and his associates. The alternative is regime decapitation by military means or by covert methods.

Very obvious. Will someone try and prevent it?

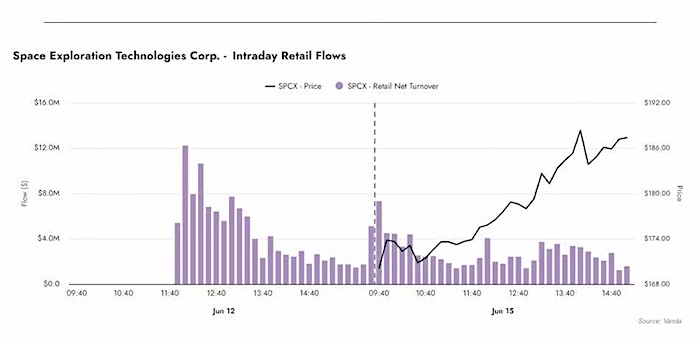

• Speculation About A SpaceX–Tesla Merger Is Already Growing (ZH)

SpaceX’s record-breaking IPO has fueled speculation that Elon Musk could take an even bigger step: merging SpaceX with Tesla to create a roughly $4 trillion technology conglomerate spanning rockets, AI, satellites, electric vehicles, robotics, energy, and social media, according to a new report from the New York Times. The idea has gained traction among investors, analysts, and even SpaceX executives. Tesla and SpaceX already share personnel, collaborate on major projects, and have business ties through AI development, data centers, batteries, and vehicle sales.Read more …

Because Musk controls SpaceX and is Tesla’s largest shareholder, any merger would effectively be a deal with himself, raising concerns about conflicts of interest and shareholder lawsuits. However, legal experts say Texas corporate law—where both companies are now incorporated—makes such challenges difficult. Shareholders generally need to own at least 3% of a company’s stock to sue, a threshold that would require roughly $45 billion in Tesla shares. The Times notes that approval would still require support from two-thirds of Tesla shareholders. Musk controls about 20% of Tesla’s voting power, and many investors have historically backed his initiatives. Tesla’s board has also frequently aligned with Musk, while SpaceX recently added longtime Musk associate Roelof Botha to its board.Supporters argue a merger could unlock significant synergies. Tesla’s expertise in chips, AI, and data-center construction could complement SpaceX’s ambitions in orbital infrastructure, satellite communications, and space-based computing. Ark Invest, which owns shares in both companies, has said the combination makes strategic sense, though it would prefer Tesla’s self-driving taxi business to mature first. SpaceX President Gwynne Shotwell has acknowledged potential benefits, saying a merger could simplify Musk’s responsibilities and noting clear overlaps between the companies’ futures: “There’s no question that there are synergies between Tesla and SpaceX in our futures.”

Opponents could challenge the deal through securities-fraud claims, antitrust scrutiny, or national-security concerns, particularly given the companies’ combined presence in AI, robotics, communications, and space technology. Still, experts believe regulators would face significant hurdles, especially if the combined company continued to perform well. “As long as he keeps running the business well and the stock price keeps going up, that is a pretty good bar to bringing a securities fraud suit,” said James Spindler, a professor of corporate law at the University of Texas School of Law.

Ultimately, the greatest obstacle may be financial rather than legal. As one corporate-governance expert noted, investors tend to support ambitious deals when markets are rising and shareholders are making money. Charles Elson, the founding director of the Weinberg Center for Corporate Governance at the University of Delaware told The New York Times that Musk “has got this cheering section who will follow him to the gates of Hades or gates of heaven, wherever he leads them.” “Basically he’s gotten to the point where he can do almost anything he wishes…”

Every now and then, a glimpse at how bad the previous 4 years were.

• Stupid, Stupid, Stupid”: DOJ Memo Tarnishes Record of Merrick Garland (Turley)

“Internal emails were uncovered recently that cast a new, negative light on Attorney General Merrick Garland’s record in targeting parents over school board controversies. The communications show that various Justice officials raised alarms over the effort pushed by Democratic allies and the National Association for School Boards. Career officials condemned the Biden Administration proposal by objecting that “If they do this, they might as well rename the damn thing the Anti-MAGA Task Force.”Read more …

As parents organized against COVID and woke policies being implemented by school boards, Democratic allies and the National Association for School Boards called upon the Biden Administration to crack down. Garland agreed and implemented a plan detailed in an October 2021 memo to treat these parents as engaged in potential “domestic terrorism.” There was public outrage, but Garland defended the action, declaring “The obligation of the Justice Department is to protect the American people against violence and threats of violence and that particularly includes public officials.” As the outcry grew, the Biden Administration was forced into a retreat and an apology:“On behalf of NSBA, we regret and apologize for the letter. There was no justification for some of the language included in the letter. We should have had a better process in place to allow for consultation on a communication of this significance. We apologize also for the strain and stress this situation has caused you and your organizations.” We now know that rank-and-file officials opposed the effort, but decided to go forward anyway. The Justice Department in October 2021 issued a memo to coordinate a response to what it described as an “increase in harassment, intimidation and threats of violence against school board members, teachers and workers in our nation’s public schools” by parents.

Newly released emails raised all the objections later made by critics after the policy’s release. One deputy assistant attorney general wrote that: “I don’t think it’s possible to state how strongly I object to this. It will completely and totally nuke our election threats efforts, and will damage the reputation of the Public Integrity Section into the bargain. It’s like they’ve affirmatively trying to make this thing not work and look political.” When officials said that the Biden Administration was about to create an “Anti-MAGA Task Force,” officials responded, “Exactly! Stupid, stupid, stupid.” Another principal deputy assistant attorney general wrote,

“We will not do this. There is no conceivable connection to [public integrity] (indeed, I’m not seeing a federal interest of any kind.). And if they’re going to make the AG’s memo to the field about this and election threats, I’m going to strongly recommend that they not send it.” The Public Integrity section chief agreed, saying the memo could turn the Justice Department and the FBI into the “threat police” and that it contained “no limiting principle at all.”The question is how such an ill-considered, excessive memo could be issued in light of such internal opposition. The answer focuses new attention on the record of Garland, who seemed at times to be a virtual pedestrian in decisions at his own department.

In 2022, I wrote a column titled “The Incredible Shrinking Merrick Garland” to express my disappointment in his developing record as someone who supported his nomination. Citing the school memo and other decisions, I wrote that Garland appeared increasingly “immaterial” to the running of the department: “Garland sometimes looks more like a pedestrian than a driver on decisions in his own department. Top positions were given to figures denounced as far-left advocates on issues from defunding the police to racial justice. For the moderate Garland, these did not seem like natural choices.”

As Special Counsel Jack Smith took a hatchet to preexisting DOJ policies and the First Amendment in his crusade against Donald Trump, Garland seemed little more than a figurehead in refusing to exercise any moderating or supervisory influence. Likewise, as his department pursued a “shock and awe campaign” against citizens who joined the January 6th protests, Garland remained passive. By 2023, I was writing columns that Garland had become an “utter failure” as Attorney General. He had become the kind face of a department weaponizing charges and targeting opponents.

While the same charges have been leveled at the current Administration, that does not alter the troubling legacy of Merrick Garland. The school board memo reflects how political rather than legal or institutional priorities prevailed under Garland. The merits of these controversies can be left to history. However, what is most striking is the absence of any discernible control or direction from Garland.

Unlike his predecessor, Bill Barr, who was famously “hands-on” in his leadership style, Garland delegated authority to powerful subordinates, who carried out these measures with little apparent restraint. As discussed in my 2022 column, Garland seemed to morph with the character Scott Stuart in the cult classic, “The Incredible Shrinking Man,” in which Stuart delivers a strikingly profound line: “The unbelievably small and the unbelievably vast eventually meet — like the closing of a gigantic circle.” That may be the final epitaph of Merrick Garland’s record as United States Attorney General.

“I think we should challenge the pardon, because it’s an extraordinary pardon. It’s a pardon not for a specific crime, and it’s a pardon over a 10 year period. It’s the same that he got the same thing Hunter Biden got…”

• Two Top Senators Urge Trump DOJ To Prosecute Fauci Despite Biden Pardon (JTN)

Two top U.S. senators are urging the Trump Justice Department to challenge the legality of President Joe Biden’s pardon of Dr. Anthony Fauci and to pursue criminal charges against the nation’s former top doc during the COVID-19 pandemic. “I think we should challenge the pardon, because it’s an extraordinary pardon. It’s a pardon not for a specific crime, and it’s a pardon over a 10 year period. It’s the same that he got the same thing Hunter Biden got,” Sen. Rand Paul told the Just the News, No Noise television show on Tuesday. “I think that could be challenged in court, because it’s not specific, it’s vague, and it doesn’t specify the crime, and it’s such a large period of time.Read more …

So, I think it could be challenged, and should be challenged,” he said. Paul, a longtime Fauci critic who accused the doctor of misleading Congress, added that the recent indictment of two Fauci deputies could give the DOJ leverage to secure their cooperation and testimony against their former boss. Sen. Ron Johnson, R-Wis., echoed Paul’s concerns on Wednesday, telling Just the News that he’s “pretty certain” what Fauci funded in terms of research caused the COVID pandemic. “Anthony Fauci is a bad person, and he ought to be prosecuted, because I believe he did commit crimes,” Johnson said.How she has long denied wrongdoing and dismissed such criticisms in the past. But Biden nonetheless infamously pardoned Fauci in 2024 by autopen before leaving office. Paul compared the pardon to Hunter Biden’s. Referencing the autopen action, Paul added, “Was President Biden of sound mind? Did he understand who he was pardoning? Did he participate in it? Did he approve of each of the ones that were signed by autopen?” Paul described some of the most alarming elements of a detailed timeline his committee released last week, and accused Fauci of launching a public relations campaign to deflect scrutiny from his agency’s funding of risky virus research in China as the COVID-19 pandemic emerged in early 2020.

Paul detailed a timeline of Fauci’s actions speaking exclusively to Just The News, citing emails and documents his office obtained. Paul highlighted from the timeline that Fauci was awake at 3 a.m. in late January 2020, emailing Dr. Robert Kadlec, who oversaw dangerous research, falsely asserting the virus originated in animals with “nothing to do with the lab.” Fauci also called on old friends within the intelligence community, according to Paul, to mislead them about what was really going on at the Wuhan, China laboratory.

“He (Fauci) already knows he’s going to have to defend this because he outsourced this dangerous research to China. There weren’t adequate safety controls, and now he’s got to start the spin,” Paul said. Paul noted that Fauci’s spin operation was not only necessary for political purposes, but for survival, because in Fauci’s capacity as a health official, he funded research to humanize the virus and re-adapted it to make it more contagious to humans. Within a week, according to Paul, on Feb. 1, 2020, a group of top virologists privately told Fauci the virus appeared engineered, citing its furin cleavage site. The furin cleavage site is a short, specific amino acid sequence that acts as a recognition signal for the host enzyme furin to cut and activate the protein.

Days later, several of those same scientists published a prominent paper declaring it was “not a laboratory construct,” language Paul called “adamant language you rarely see in a scientific article, political type of language, PR type of language.” One author later received an $8 million grant approved by Fauci, Paul said. Fauci then cited the paper in White House briefings as independent evidence against a lab leak, despite having helped commission and edit it. “It’s a big circle, but it’s all around Anthony Fauci,” Paul said. aEncouraging developments, Paul said, include federal indictments of two Fauci lieutenants: David Morens, accused of destroying records and acting as Fauci’s intermediary, and Vincent Munster, a virologist, charged in connection with importing dangerous pathogens into the country without a permit, claiming they were “diagnostic equipment”.

Both were involved in research grants that proposed creating viruses with features similar to SARS-CoV-2. Paul added that Morens and Munster might be willing to flip on the government’s former top pandemic doctor and testify if offered leniency on their terms. “My goodness, it would be worth it to see one or two of his lieutenants give up testimony that they would not have given up otherwise, but now that they’ve been indicted, might be inclined to tell the truth,” Paul said.

Hillary is talking about (who else) … Hillary.

“Biden was in MY way”.

• Dems Could Have Beaten Trump If Biden Had Stepped Aside: Hillary Clinton (JTN)

Hillary Clinton said that former President Joe Biden made a “terrible mistake” when he decided to run for reelection. The remarks were made at an event in Manhattan on Monday, the New York Times reported. Biden’s decision, Clinton said, was a “terrible miscalculation” that resulted in the Democratic Party’s loss in 2024. If instead of running for reelection, Biden had decided to “pass the torch,” Democrats could have held a competitive presidential primary. “Whoever emerged from that contest — whether it was the vice president, or a governor, or a senator or anybody else — would have beaten Donald Trump,” Clinton said.Read more …

They think they can make JD a Democrat. Trump no.2 has them thinking he’s one of theirs. Likability.

• What Joy Behar Told JD Vance Shocked Him (Margolis)

JD Vance walked into enemy territory on Tuesday, and while everyone is talking about how he crushed it, with an endorsement nobody saw coming, least of all him. The vice president appeared on ABC’s The View to promote his new book, and he spent the better part of an hour fielding hostile questions from a panel that was never gonna give him a fair chance. But surprisingly, he impressed at least one of his harshest potential critics, who told him so directly during a commercial break. That critic was Joy Behar, the show’s longtime co-host and a woman who has openly admitted that she’s “never voted for a Republican in my life.” According to a report by the New York Post, Behar told him off-air that he should run for president.Read more …

The compliment came with a major caveat, though, which Behar made sure everyone heard the next day. She revealed the exchange on The View’s companion podcast, Behind the Table, after executive producer Brian Teta put her on the spot. “I’m getting a note here. You told him during the break that he should run for president because he had a good vibe,” Teta said. Behar’s response: “For a Republican.” That qualifier became the theme of her entire defense of the moment. Behar insisted she doesn’t think Vance is “a bad guy,” calling him “very genial” and crediting him for coming on the show “in good faith.”The comedian and television personality, who stressed that she is not a Republican, said she has no intention of backing Vance politically, arguing that Democrats are more compassionate than Republicans on national issues. “I don’t mind a Republican on the city level because it needs a little discipline, but on the national level, I want somebody with a good heart,” Behar said, adding that she voted for former New York City Mayor Michael Bloomberg. Bloomberg ran for mayor as a Republican but later registered an independent. He then switched to the Democrats in order to mount what would be an unsuccessful bid for the party’s presidential nomination.

Behar insisted that her personal impression of Vance differed from her view of the administration he serves. “Truthfully, as I said to you at the beginning of this conversation, I don’t think that he’s a bad guy,” she said. Vance also let slip just how much the appearance rattled him beforehand, telling Behar backstage more than once that he was more nervous walking onto that set than he was heading into last year’s vice presidential debate. Well, I guess I can understand that. I mean, Tim Walz, am I right? We all knew how that was going to go. But the women on The View aren’t much smarter than Walz; there are just more of them.

He recounted the compliment again later that night on Gutfeld!, still amused by it. “Joy Behar even said during the break, not joking, she said, ‘You know what? You’re, like, pretty good for a Republican.’ And I was like, ‘Whoa.’ That is a way better compliment than I expected from Joy Behar.” If you missed his appearance on The View, here it is:

Here is the entirety of JD Vance's appearance on The View, which did not go well for him

— Aaron Rupar (@atrupar) June 16, 2026

(and kudos to the hosts for actually asking him hard-hitting questions and followups) pic.twitter.com/oDnFYqyZeUIn fairness, I don’t think he needs validation from Joy Behar.

PCR NOT talking about Trump. Or Putin.

• White Ethnicities Have Been Demonized Beyond Recovery (Paul Craig Roberts)

In 1968 Britain’s only leader, Enoch Powell, explained that the mass influx into Great Britain by immigrant-invaders from the third world would turn ethnic British into “strangers in their own country.” Powell, of course, was lambasted by the liberals and the left, by presstitutes, and by fellow politicians anxious to move forward at Powell’s expense. Powell’s prediction turned out to be correct and his detractors wrong. In 1973 Jean Raspail said the same thing about France in his book, The Camp of the Saints. In more recent years Marine Le Pen, leader of France’s largest political party, which is carefully kept out of power by the French establishment, has warned that France was ceasing to be French. Her warning has been rewarded by the French elite’s ongoing attempts to imprison her.Read more …

In 1972 Wilmot Robertson warned Americans about their future in his book The Dispossessed Majority. In more recent times the immigration website Vdare fostered debate about the consequences of mass immigration for American society. Vdare‘s reward was to be shutdown by anti-white New York attorney general Leticia James, a black woman who was educated by white liberals to hate white people as racists. As almost all immigrant-invaders are people of color, AG James concluded that Vdare was racist and white supremacist and decided to abuse the powers of her office to destroy the immigration website. She did this by endless demands for documents without ever filing charges until Vdare‘s funds were used up by lawyers and the site closed.Now that Vdare is destroyed by AG James and its former owners left without funds, Leticia James will probably file some unsupported charge against the former owners knowing that they lack the financial means for their defense. Thus she can continue her ruin of the “white racists” and perhaps imprison them. This is what multiculturalism and diversity has brought to insouciant white people everywhere. White ethnicities have everywhere allowed their own brainwashed anti-white governments to put immigrant-invaders in charge of their lives. This result is precisely what Enoch Powell, Jean Raspail, Marine Le Pen, and Wilmot Robertson predicted.

In what little remains of Great Britain today, Tommy Robinson, Nigel Farage, and newcomer Rupert Lowe are making objections to the anti-white policies institutionalized in the British government.. That there are three Britishers protesting the demise of British ethnicity indicates that there is some spark of self-defense among ethnic British. But so much has been lost that the ethnic British are now the underdog in their own country, just as Enoch Powell said they would be. Instead of listening, the dumbshit British read the liberal newspapers and scolded Powell for being a racist.

Essentially, the British government, both parties, have abandoned white British ethnics in favor of immigrant-invaders. Nigel Farage has correctly accused the British government of “deep anti-white racism.” There is no doubt that his accusation is correct. He proves it with the government’s own statistics. There is no doubt that the 2010 Equality Act institutionalized anti-white attitudes into every aspect of legal and public life in Britain.

There have been so many scandals in Britain of the anti-white British government covering up mass crimes committed against British ethnics by immigrant-invaders. There is the now admitted 30-year coverup of mass gang rapes by immigrant-invaders of British women and children. Different reports give different numbers. Some are 180,000 ethnic British female children gang raped and nothing done about it. Other figures are 300,000. A former British prime minister stated publicly that the rapes were ignored by the authorities as it would question the immigration policy.

In the past few days we had the murder of Nowak by an immigrant-invader. Nowak, a white British citizen, bled to death handcuffed by the police .while the white British police chatted amicably with his black murderer. We have had the attempted beheading of an ethnic Britisher by a black immigrant-invader. We have had the stabbing in the neck of a young ethnic British girl by an immigrant-invader who dances at his success. I could go on forever and write volume after volume, and the weak-minded white ethnics sit there thinking as they are told by the white liberals it is their fault for being racist.

The collapse of Western civilization, like the collapse of the Roman Empire, is not a sudden event. It happens slowly over time. The time is upon us, and the collapse is now. The cause is not Russia, Iran, China, or white racism. The cause is the systematic brainwashing of ethnic nationalities in the white world that they uniquely are racists who have oppressed people of color and must now pay the consequences. White ethnicities have been so drained of confidence that they are incapable of fighting for their lives, for their culture, for their civilization. Everywhere white ethnicities are being replaced and they do not resist.

It is that simple. There is nothing left to be said.

20% and more. Serious.

• Apple To Raise Prices As AI Boom Pushes Up Chip Costs (BBC)

Apple plans to raise the prices of its products as the cost of the memory chips it uses has surged, the technology giant’s boss has said. Tim Cook, Apple’s outgoing chief executive, told the Wall Street Journal (WSJ) that price increases were “unavoidable” as the situation around memory chips had become “unsustainable”. He did not say when prices would rise or which products would be affected. It is also unclear whether the price hikes will affect the iPhone 18, which is expected to be launched in September. Memory chips are essential components in smart devices like mobile phones, but the boom in artificial intelligence (AI) has driven up their prices in recent months.Read more …

Later, US President Donald Trump said that Apple had agreed to work with chipmaker Intel to make its chips in the US. “I decided to help Intel because we need to design and build our Chips right here in America,” he wrote in a post on his social media platform Truth Social. The BBC has contacted Apple and Intel for comment. In August last year, the Trump administration announced that the federal government would take a 10% stake in Intel. Intel’s shares rose more than 10% when US stock markets opened on Thursday.‘Less supply’

Speaking to the WSJ, Apple boss Cook said: “We’re doing our best to mitigate the huge increases that are being passed to us, and we’ve been trying to shield our customers from the increases, but the situation has become unsustainable. “There’s less supply at a time when consumers want devices and the memory guys are passing along huge price increases,” said Cook, who is due to be replaced by John Ternus as Apple’s CEO in September after 15 years in the role. “We definitely need memory pricing and supply to return to reasonable levels for consumer products. That’s the bottom line.”The price of Ram – typically one of the cheapest computer components – has more than doubled since October 2025. In addition to rising AI demand, the war in Iran has also disrupted the global supply of helium, a gas crucial in making semiconductors, adding to the cost of computer chips. The average selling price of smartphones globally is expected to rise by around 20% in 2026 to an all-time high, according to research firm Omdia. Apple’s new phones are likely to cost up to $150 more than the iPhone 17s, as the firm is expected to upgrade their specifications to support new AI features, Omdia’s smartphone market analyst Chiew Le Xuan told the BBC.

Most smartphone brands have already raised prices, pulled back on promotions or cut specifications to protect their profit margins in response to rising costs, he added. “This is the new pricing reality, not a temporary spike.” Other technology giants have also highlighted pressure in the chipmaking industry. In an exclusive interview with the BBC this month, Taiwan Semiconductor Manufacturing Company (TSMC) would not rule out price increases as inflation pushed up its costs. TSMC makes the most advanced chips designed by companies such as Apple, Nvidia and AMD. Earlier this year, Samsung said that it expects memory chip supply shortages to make electronic devices more expensive.

In April, Sony raised the price of its PlayStation 5 consoles by £90 in the UK and $100 in the US as a result of “continued pressures in the global economic landscape”. Nintendo later said it would increase the price of its Switch 2 from September due to “changes in market conditions”. The iPhone 17 has been popular since the lineup was launched last September. Sales of Apple devices grew by 17% in the first three months of 2026 compared with the same period a year ago, helped by strong demand in China. Apple removed the entry-level option of its Mac Mini compact computers, raising its starting price by about $200 (£150) earlier this year.

https://twitter.com/Maga4liberty/status/2067213950890987655?s=20 https://twitter.com/VictoriaSask/status/2067403042232651902?s=20Full movies by the end of this year https://t.co/kkBrngWA0X

— Elon Musk (@elonmusk) June 17, 2026

Elon Musk: “I wake up, I work, I go to sleep. Wake up, work, and do that seven days a week. My workload went up from 70–80 hours a week to probably 120.”

— Taya Bass (@travelingflying) June 17, 2026

Nobody works harder than Elon Musk. He has done more for humanity than anyone else. pic.twitter.com/iS6wrvXG1J

https://twitter.com/iAnonPatriot/status/2067340182018297936?s=20The biggest improvement ever made to the most complex machine in human history came from a guy holding a camera.

— Dustin (@r0ck3t23) June 18, 2026

Not a propulsion engineer. Not a systems architect. Not anyone on the SpaceX payroll.

A YouTuber named Tim Dodd.

Dodd was touring Starbase when Musk explained how… pic.twitter.com/CFKNQ4ARAi

Support the Automatic Earth in wartime with Paypal, Bitcoin and Patreon.