GordonParks Place de la Concorde, Paris, France 1950

UPDATE: There still seems to be a problem with our Paypal widget/account that makes donating -both for our fund for homless and refugees in Greece, and for the Automatic Earth itself- hard for some people. What happens is that for some a message pops up that says “This recipient does not accept payments denominated in USD”. This is nonsense, we do. We notified Paypal weeks ago.

We have no idea how many people have simply given up on donating, but we can suggest a workaround (works like a charm):

Through Paypal.com, you can simply donate to an email address. In our case that is recedinghorizons *at* gmail *com*. Use that, and your donations will arrive where they belong. Sorry for the inconvenience.

Private debt is the one to watch. Up rapidly in Canada, France, Hong Kong, South Korea, Switzerland and Turkey. And Australia, New Zealand, Scandinavia, Holland.

• Global Debt Hits Record $233 Trillion (BBG)

Global debt rose to a record $233 trillion in the third quarter of 2017, more than $16 trillion higher from end-2016, according to an analysis by the Institute of International Finance. Private non-financial sector debt hit all-time highs in Canada, France, Hong Kong, South Korea, Switzerland and Turkey. At the same time, though, the ratio of debt-to-GDP fell for the fourth consecutive quarter as economic growth accelerated. The ratio is now around 318%, 3 percentage points below a high set in the third quarter of 2016, according to the IIF. “A combination of factors including synchronized above-potential global growth, rising inflation (China, Turkey), and efforts to prevent a destabilizing build-up of debt (China, Canada) have all contributed to the decline,” IIF analysts wrote in a note. Yet the debt pile could act as a brake on central banks trying to raise interest rates, given worries about the debt servicing capacity of highly indebted firms and government, the IIF analysts wrote.

Warren in praise of technology. Blind and boring. “This game of economic miracles is in its early innings. Americans will benefit from far more and better ‘stuff’ in the future.”

• The Tsunami Of Wealth Didn’t Trickle Down. It Surged Upward – Buffett (CNBC)

Warren Buffett knows first hand the power of American capitalism. As the third richest person in the world, with a net worth of more than $86 billion, the octogenarian investor has personally benefited from it. And yet, in a piece penned for Time magazine, published Thursday, Buffett says there is a problem with that economic system, which made him a king: Many individuals suffer even as those at the top prosper wildly. He points to the Forbes 400, which lists the wealthiest Americans. “Between the first computation in 1982 and today, the wealth of the 400 increased 29-fold — from $93 billion to $2.7 trillion — while many millions of hardworking citizens remained stuck on an economic treadmill. During this period, the tsunami of wealth didn’t trickle down. It surged upward.”

America’s capitalist economy requires its winners not ignore the system’s faults, says Buffett. The market system has “left many people hopelessly behind, particularly as it has become ever more specialized. These devastating side effects can be ameliorated: a rich family takes care of all its children, not just those with talents valued by the marketplace,” writes Buffett. He also notes that, in particular, those workers replaced by technological advancements will be left behind. “This game of economic miracles is in its early innings. Americans will benefit from far more and better ‘stuff’ in the future. The challenge will be to have this bounty deliver a better life to the disrupted as well as to the disrupters,” Buffett writes. “And on this matter, many Americans are justifiably worried.”

In the long term, those technological advancements are a boon for the economy. But in the short term, they cause unemployment and anxiety for those who lose their jobs to automation and are left unemployed. To demonstrate his point, Buffett points to 1776, when the United States declared its independence, and the evolution of farming technology. “Replicating those early days would require that 80% or so of today’s workers be employed on farms simply to provide the food and cotton we need. So why does it take only 2% of today’s workers to do this job? Give the credit to those who brought us tractors, planters, cotton gins, combines, fertilizer, irrigation and a host of other productivity improvements,” writes Buffett.

“We know today that the staggering productivity gains in farming were a blessing. They freed nearly 80% of the nation’s workforce to redeploy their efforts into new industries that have changed our way of life.” Indeed, despite the warnings, Buffett is optimistic. “In 1776, America set off to unleash human potential by combining market economics, the rule of law and equality of opportunity. This foundation was an act of genius that in only 241 years converted our original villages and prairies into $96 trillion of wealth,” he says.

Don’t be fooled: this is not a flaw, it’s a feature. It’ll be interesting to see how companies aim to fix a pretty much hardware feature with a software patch.

• Apple Says All Macs, iPhones and iPads Exposed to Chip Security Flaws (BBG)

Apple said all Mac computers and iOS devices, like iPhones and iPads, are affected by chip security flaws unearthed this week, but the company stressed there are no known exploits impacting users. The company said recent software updates for iPads, iPhones, iPod touches, Mac desktops and laptops, and the Apple TV set-top-box mitigate one of the vulnerabilities known as Meltdown. The Apple Watch, which runs a derivative of the iPhone’s operating system is not affected, according to the company. Despite concern that fixes may slow down devices, Apple said its steps to address the Meltdown issue haven’t dented performance.

The company will release an update to its Safari web browser in coming days to defend against another form of the security flaw known as Spectre. These steps could slow the speed of the browser by less than 2.5 percent, Apple said in a statement posted on its website. Intel on Wednesday confirmed a report stating that its semiconductors contain a vulnerability based around a chip-processing technique called speculative execution. Intel said its chips, which power Macs and devices from other manufacturers, contain the flaw as well as processors based on ARM Holdings architecture, which is used in iOS devices and Android smartphones.

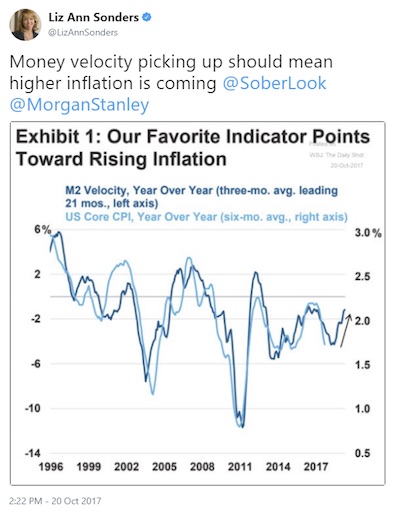

Danielle DiMartino Booth seems like a smart person. But “We can have deflation and inflation at the same time.” is utter nonsense. If only because defining inflation without referencing money velocity is a useless exercise.

• 2018 Economy Goes Cold – Inflation Hot – Danielle DiMartino Booth (USAW)

“We have seen 24 consecutive back-to-back months when credit card spending has outpaced incomes. That tells you households are struggling to get by. This is not Yves Saint Laurent handbags and Jimmy Choo shoes. These are families who are using their credit cards to take care of the necessities, to fill up the gas tank, to buy groceries and fill up their refrigerator… We have seen month after month of subprime automobile delinquencies, and we are starting to see a big tic up in FHA mortgage delinquencies as well. …We are at almost 10% (delinquencies) of FHA mortgage loans. Underlying this sugar high that we will see from all of these hurricanes and rebuilding efforts and wildfires, underneath that, still waters run deep and the economy is not doing well. We are a consumption driven economy that is weakening underneath. The sugar high will absolutely wear off in 2018.”

What about the bond market in 2018? Booth says, “We have gone from $150 trillion (in global debt) in 2007 to $220 trillion and counting today. If you delude yourself into thinking a rising rate environment can be good when we have tacked on $70 trillion of debt in the last decade, you are fooling yourself. It is an accident waiting to happen, and anyone who doesn’t think that it will take the stock market down with it is more optimistic than I am by a country mile.” Booth says, along with a “bond market debacle,” the world will see inflation right along with it. Booth explains, “Look at lumber prices, look at the cost of packaging, plastics, raw materials, the producer price index… is at a six year high right now. It’s called the mother of all margin squeezes.

Companies are suffering. We have inflation. We have very real inflation, and it is hitting corporate America between the eyes. We have seen inflation happening, and we continue to see it happening… Rental inflation is off the scale…Inflation is up for 2018, and it has been up. We can have deflation and inflation at the same time. If all of this debt that has built up, especially for households, if they are allocating more of their income to servicing debt, then they have fewer dollars to spend on other things. So, you are going to have deflation and inflation at the same time.” What does the regular guy on the street do? Booth says, “Figure out a way to have exposure to precious metals. Put your bubble vision on mute. You do not have to be invested in the market. That is a fallacy. Take what you have and pay down your debts.”

This whole discussion is vapid. Central banks have been trying in vain for over a decade to push up inflation, and now, overnight, they have not just succeeded, but overdone it?

• Inflation Risk May Shake Global Markets (BBG)

Investors devoted to the idea that inflation will stay subdued should be worried. Worldwide data have recently made clear that producer-price increases have picked up steam. That’s led bond buyers to begin wagering that consumer inflation could be soon to follow, with U.S. breakeven rates above 2 percent in many tenors for the first time since March. The shift represents a sea change for investors who have grown complacent about the threat of rising prices over the past few years, when inflation was subdued by modest economic growth rates, suppressed wages and shifts in technology and demographics. While few are betting on runaway increases anytime soon, even a modest uptick in prices could have an outsize impact on sentiment and change the prevailing narrative.

“There is this idea that inflation is dead,” said Peter Boockvar, the chief financial officer at Fairfield, New Jersey-based Bleakley Financial Group. “But what we are beginning to see – such as in the purchasing managers index surveys – is a lot of talk about inflation pressures. For the markets, inflation is an under appreciated risk in 2018.’ The latest sign of prices pressures came Wednesday. U.S. manufacturing expanded in December at the fastest pace in three months, as gains in orders and production capped the strongest year for factories since 2004, the Institute for Supply Management said. The index of prices paid rose to 69 from 65.5 the month before.

Factories across the globe have warned they are finding it increasingly hard to keep up with demand, potentially forcing them to raise prices as the world economy looks set to enjoy its strongest year since 2011. Purchasing Managers Indexes published Tuesday from countries including China, Germany, France, Canada and the U.K. all pointed to deeper supply constraints.

Mish is one of the few who still understand the issue. Yes, it’s about definitions. But that doesn’t mean any definition is as as good as the next one.

• Economists Think Inflation Will Rise Sharply in 2018: They’re Wrong (Mish)

Reason Number Five – Money Velocity This reason I found in a Tweet by LizAnn Sonders.

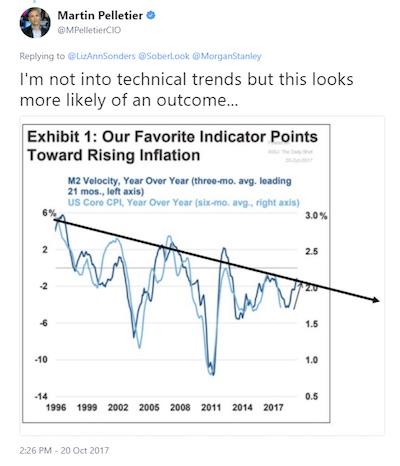

Money Velocity Rebuttal: A three month average vs a six month average offset by 21 months seems like a lot of curve fitting. Here is a Tweet Reply by Martin Pelletier that makes sense to me.

By the way, let’s look at what we are talking about here in actual terms instead of percentage increases.

Beijing telegraphing lower growth.

• China Won’t Be Prioritizing Growth This Year – Andy Xie (CNBC)

China’s fears of a financial crisis will spur Beijing to keep the country’s growth target in check, a widely followed China expert said Friday. “Their top priority is to prevent a financial crisis, so the government is looking for any pockets (of risk) that might be a trigger,” independent economist Andy Xie told CNBC’s “Squawk Box.” Chinese authorities have been cracking down on money fleeing the country and warning on “gray rhinos,” which are risks that could potentially be solved but have been unaddressed so far. “The government does not view growth as the top priority right now — we have to take the government’s word at face value. The government is worried about financial risk,” Xie added.

China will keep its target for economic growth at “around 6.5%” in 2018, unchanged from last year, Reuters reported on Thursday, citing unnamed policy sources. The world’s second-largest economy has been fighting debt for years, but with little success so far as it balances economic stability against fallout from a sharp deceleration. There have also been difficulties with the political buy-in for the debt crackdown. That’s been especially true down the Communist Party pecking order as many local governments still need to hit growth targets. “It takes time to filter down the ranks. Most government officials still don’t believe in the new direction,” said Xie.

However, unlike officials in previous administrations, Xie said current ones are likely to be changed if they don’t agree with the current economic direction, so the government will have more power to push through its agenda. Policies are working toward that direction, with higher interbank interest rates that will remain at elevated levels for the foreseeable future, Xie added. China is also looking to further slow money supply growth in 2018 after it already slowed to the all-time low around 9% in November 2017. With China likely headed toward a money supply growth rate of 7 to 8% in the next few years, it will be a “very different situation” for the economy, said Xie.

A bit more on Jeremy Grantham: “Keep an eye on what the TVs at lunchtime eateries are showing..”

• ‘Melt-Up’ Coinage Could Signal Last Hurrah For US Stock Market (G.)

Welcome to the world of “melt-up”, a phrase we could be hearing a lot in coming months. It describes the idea that the US stock market, despite currently looking absurdly expensive by traditional yardsticks, could be set for one last euphoric hurrah before the inevitable crash happens. There are a couple of reasons why the “melt-up” theory may not be as wacky as it sounds. First, it comes from Jeremy Grantham, an investor who has rightly earned a reputation for knowing how to read financial bubbles. He dodged the end-of-the-century dotcom bubble and the 2007-09 blowup in the US housing market – two of the best calls anybody could have made in the past 20 years. Grantham’s default setting, as you would expect, tends to be bearish, or at least cautious. If he’s talking melt-up, that’s newsworthy.

Besides, GMO, the Boston-based fund management group he founded, manages $75bn of assets – he’s a player. A second reason is that Grantham is certainly not arguing that shares are cheap. “We can be as certain as we ever get in stock market analysis that the current price is exceptionally high,” he states. Instead, his melt-up thinking is driven by a “mish-mash of statistical and psychological factors based on previous eras”. On the statistical side, he points out that the global economy is in sync, profit margins are fat and president Trump’s corporate tax cuts could make them even fatter and “perhaps provide the oomph to keep stock prices rising”. Then there’s the fact that the current strength in the stock market is fairly broad-based. In past bubbles, the end was nigh when gains were concentrated in an increasingly small collection of “winners”.

The likes of Apple are roaring this time, but the same divergence has not occurred – yet. For “touchy-feely” evidence of excess about to appear, Grantham looks at media coverage. US newspapers and TV stations are getting interested in financial markets (with bitcoin, “a true, crazy mini-bubble of its own”, to the fore) but not yet with the wild obsession of the frenzied dotcom years. “Keep an eye on what the TVs at lunchtime eateries are showing,” he says.

So much for OPEC cuts.

• US on The Cusp of Enjoying ‘Energy Superpower’ Status (CNBC)

The U.S. is well-placed to join the likes of Saudi Arabia and Russia as one of the world’s leading energy powerhouses, an analyst said Thursday. “There is a big shift in market structure taking place and I think, so far, it really hasn’t got the attention it deserves. The U.S. is emerging as, not only a military and economic superpower, but as an energy superpower,” Martin Fraenkel, president at S&P Global Platts, told CNBC. “We are expecting that by 2020, the U.S. is going to be one of the top 10 oil exporters in the world,” he added. In recent years, America’s unprecedented oil and gas boom has been driven by one factor above all others — and that’s shale.

The so-called shale revolution could help to alleviate Washington’s reliance on foreign oil, including from turbulent Middle Eastern states, while also helping to export to more countries around the world. In November, the International Energy Agency (IEA) projected a dramatic increase in shale production could transform the U.S. into the world’s largest exporter of liquefied natural gas by the mid-2020s. The same forecast also predicted that the U.S. would likely notch another milestone a couple of years later. The Paris-based organization said that by the late-2020s, the U.S. would begin to ship more oil to foreign markets than it imports. “This is a big, big shift in the dynamics of energy markets and, in my view, will be a shift in geopolitical markets as well,” Fraenkel said.

Not sure Germany and France are too likely to philosophize their dominance away.

• A Good German Idea for 2018 (Varoufakis)

No god is necessary, no moralizing is required, to demonstrate our duty to tell the truth. Practical reasoning is all it takes: A world where everyone lies is one in which human rationality, which depends entirely on language, dies. So it is our rational duty to tell the truth, regardless of the benefits lying might bring in practice. Applied to market societies, Kant’s idea yields fascinating conclusions. Strategic reductions in price to undercut a competitor pass the test of rational duty (as long as prices do not fall below costs). After all, producing maximum quantities at minimum prices is the holy grail of any economy. But strategic reductions of wages to ever lower levels (the Uberization of society) cannot be rational, because the result would be a catastrophic collapse, owing to disappearing aggregate demand.

Turning to Europe, Kant’s principle implies important duties for governments and polities. And Germany and France would be held to be in dereliction of their duties to a functioning Europe. If Germany’s current-account surpluses, currently running at 9% of GDP, were universalized, with every member state’s government, private sector, and households net savers, the euro would shoot through the roof, destroying most of Europe’s manufacturing. Equally, universalized Greco-Latin deficits would turn Europe into a basket case.

The trick, and our rational duty, is to embrace policies and to build institutions that are consistent with balanced trade and financial flows. Put differently, authentic German rectitude cannot be achieved without a form of redistribution that is bound to clash with the interests of, say, a French or a Greek oligarchy too lazy to come to terms with its own unsustainability. A critic of this German idea for reforming Europe might credibly ask why anyone should do their rational duty, rather than remain on the time-honored path of narrow self-interest? The only sound answer is: because there is no truly rational alternative. Or, rather, the alternatives are all cant.

We’re running out of time to block Monsanto.

• Monsanto Forecasts Profit Increase as Farmers Plant More Soy (BBG)

Everything’s pointing to another year of growth for U.S. seed giant Monsanto. Pretax earnings in the fiscal year through August are expected to increase, the company said Thursday is its first-quarter earnings statement. Commodity prices have stabilized from the free-fall of recent years, with corn prices starting 2018 at the same price they began 2017. Like last year, farmers are expected to buy the most expensive, newest hybrid seeds, and companies won’t have to slash prices to keep customers. Prices “are challenging for growers, but when the environment is stable, they can figure out how to operate in that environment,” Brett Wong at Piper Jaffray & Co., said by phone. “The industry has stabilized and there’s good demand for new products.”

While the company isn’t providing detailed guidance for full-year earnings, as its $66 billion takeover by Germany’s Bayer is still pending, Monsanto will be helped by growth in its soybean business. U.S. farmers are planting the crop more than ever, devoting as many acres to the oilseed as they will to corn. Adoption of Xtend, the company’s new herbicide system for soy, is expected to double in acreage this year. South American farmers are also buying more of the company’s Intacta-branded soybean seeds, which are resistant to caterpillars, and at higher prices, Christopher Perrella, a Bloomberg Intelligence analyst, said in a note last month. Recent U.S. tax reform legislation will have a positive impact on Monsanto’s effective tax rate in fiscal 2019, the company said. Early estimates are that the rate for the current financial year shouldn’t be more than 30%, and could be lower.

Monsanto expects the Bayer deal to close in early 2018, with about half of regulatory approvals secured so far. It also said its digital agriculture platform, Climate FieldView, was on 35 million paid acres last year, and expects the total to grow to 50 million acres. Roundup, Monsanto’s blockbuster herbicide, is also making a comeback. The price of glyphosate, the active ingredient in the weedkiller, is rebounding faster than expected as Chinese producers of generic brands cut output due to environmental restrictions, Don Carson, an analyst at Susquehanna Financial Group, said in a note. The increase for gross profit in 2018 for the company’s unit that produces glyphosate will exceed $1 billion for the first time in three years, according to Carson.

The Greek state is in a very bad position to auction off properties.

• Greek State To Start Its Own E-auctions (K.)

The Greek state is planning to launch its own online auctions – to be conducted according to properties’ market value – with a legislative intervention that will bring the country in line with its commitments to international creditors. The Finance Ministry is expected to presents lawmakers with the relevant clause by the end of the month – along with dozens of other pending prior actions – so that the state’s online auctions can begin in February or early March at the latest. In any case, as of the first quarter of the new year homes, land plots, stores and corporate buildings owned by state debtors will go under the hammer at market rates, which tend to be far below the taxable ones, known as “objective values,” as dictated by the law.

Ministry officials say the state will use the same platform as the one used by banks or other private creditors, arguing that there is no reason to create a separate system. It is noted that the state did not conduct a single auction in 2017, while in 2016 there were just 11 conventional auctions – all requested by the debtors themselves so they could pay off their arrears to tax authorities. However, one ministry official expressed concerns about the impending state auctions, arguing that the state comes low in the ranking of creditors – as others take precedent – and that tax authorities have a slew of other procedures for collecting debts, such as the ongoing repayment programs and the most recent out-of-court settlement plan for debts of up to 50,000 euros.

He added that after the above clause is ratified, the government will have to decide on the policy the state will follow in the auctions. Each of its 4 million debtors will have to be judged separately and according to their property assets, as “owning a house in Kolonos is very different to having one in Kolonaki,” he said, referring to one poor and one affluent Athens neighborhood. The official also expressed reservations over the result of the state’s initiative to push for auctions where several other creditors are likely to secure more benefits by ranking higher on the creditor list.

Playing off one group of people against the next.

• Work To Improve Greek Island Centers For Refugees Moving Slowly (K.)

Efforts to improve living conditions at reception centers for migrants on the islands of the eastern Aegean are progressing slowly amid continuing resistance from locals toward expanding facilities to accommodate hundreds of new arrivals from neighboring Turkey. On Tuesday alone, 196 undocumented migrants reached Aegean islands from Turkey, being sent to reception centers that are already cramped. On Lesvos and Chios, the facilities are hosting more than double the number of people they were designed to hold: 7,520 and 2,063 respectively. Hundreds of migrants have been transferred from the island facilities to less crowded camps on the mainland but, as the pace of arrivals is faster than that of the transfers and conditions remain substandard at the island camps.

The general secretary for migration policy, Miltiades Klapas, traveled to Chios on Wednesday to inspect progress in the erection of prefabricated buildings around the island’s main reception center to host scores of asylum seekers sleeping in tents. A total of 50 structures were sent to the island before the holidays but, by Wednesday, only eight had been set up. Works to upgrade the electricity and drainage systems for the accommodation are also dragging. A key reason for the delays is the continuing objection of local authorities to the presence of thousands of undocumented migrants on the island. The municipality of Chios has appealed to the Greek justice system, seeking the evacuation of the Vial reception center.

Ten-fold in coastal regions.

• Oceanic ‘Dead Zones’ Quadruple In Volume In 50 Years (Ind.)

The volume of water in the world’s oceans that is totally devoid of oxygen has more than quadrupled over the past 50 years, according to a new study. Over the past half century, the open ocean has lost around 2% of its dissolved oxygen, vital for sustaining fish and other marine life. There has also been a ten-fold increase in low oxygen sites, known as “dead zones”, in coastal regions during this period. Oxygen saturation is a major limiting factor that affects ocean productivity, as well as the diversity of creatures living in it and its natural geochemical cycling. The new study, published in the journal Science, represents the most comprehensive view yet of ocean oxygen depletion.

Pollution and climate change both play significant roles in depleting the ocean’s oxygen levels and the authors emphasise the role humans must play in addressing these issues. “Oxygen is fundamental to life in the oceans,” said lead author Dr Denise Breitburg, a marine ecologist with the Smithsonian Environmental Research Centre. “The decline in ocean oxygen ranks among the most serious effects of human activities on the Earth’s environment.” [..] In dead zones oxygen levels tend to be so low that any animals living there suffocate and die. As a result, marine creatures avoid these areas, resulting in their habitats shrinking. Even in areas where oxygen depletion is less severe, smaller decreases in oxygen levels can impact animals in various non-lethal ways such as stunting their growth and hindering reproduction.

Just for the headline.

• Iguanas Rain From Trees As Animals Struggle With US Cold Snap (G.)

As New Englanders bundle up and hunker down to ride out the “bomb cyclone” that is currently hammering the eastern United States with freezing temperatures, heavy winds and snow, they can take comfort in one thing: at least it’s not raining iguanas. That’s the situation in Florida, where unusually cold temperatures have sent the green lizards tumbling from their perches on trees – a result of the cold-blooded creatures basically shutting down when it gets too chilly. The iguanas are likely not dead, experts say, but merely stunned and will reanimate when they warm up. Iguanas aren’t the only species struggling to cope with the cold snap. In Texas, the temperature in the waters of the Gulf of Mexico has dipped low enough to cold-stun sea turtles, causing them to float to the surface where they are vulnerable to predators.

The National Park Service had rescued 41 live but freezing turtles by midday Tuesday. Meanwhile on Massuchusetts’ Cape Cod, the Atlantic White Shark Conservancy has reported the strandings of three thresher sharks. Two of the sharks were likely suffering from “cold shock”, the group said, while the third had frozen solid. “A true sharkcicle!” the group wrote on Facebook. Even animals that seem particularly well-suited to frigid temperatures are feeling the chill. The Calgary Zoo announced Sunday that it was moving its king penguins inside amid -13F (-25C) temperatures. King penguins are native to the subantarctic islands surrounding Antarctica. And a group of snowmobilers in Canada rescued a bull moose buried in 6ft of snow.