Pamir, Last Commercial Sailing Ship To Round Cape Horn 1949

We have written little on the topic of energy lately, other than related to oil prices going up and down, empty OPEC ‘promises’ to cut oil production, and the incredible debt load threatening to crush US -and Canadian- unconventional oil and gas. It’s a logical outcome of focusing more on finance than energy, because we feel the former has a shorter timeline than the latter. Something that harks back to our Oil Drum days.

But that doesn’t mean that the idea and/or principle of peak oil has disappeared, or that we have completely forgotten it. It has just been snowed under by the financial crisis (and by unconventinal oil and gas). And while we continue to find that the financial world will dump us into a bigger crisis sooner than energy will, it’s useful to look at oil et al from time to time.

Please note: we don’t wish to deny that oil depletion has its own dynamics, but in our view those dynamics will be hugely affected by the financial crisis that is looming big and will strike first. A crisis that, by the way, will affect not just oil and gas, but solar and wind just as much. You can get only as much ‘alternative’ energy as you can pay for, and that is before we even mention solar and wind’s EROEI (Energy Return On Energy Investment).

What the world needs to do, but we very much doubt it will voluntarily, is not to look for other forms of energy to replace oil and gas, but to look for ways to use much less energy (90% or so) while still maintaining societies that function as best they can. We doubt this because man is no more made to volunteer for downsizing than any other species.

The interview below with Louis Arnoux by the SRSrocco Report, combined with an article Louis wrote in July on the site of our old friend Ugo Bardi (is Florence really 6 years ago already?), is an excellent opportunity to catch up on energy issues.

The discussion of energy relative to finance will no doubt continue, and Louis doesn’t seem to have the exact same view as us, but that’s fine, or at least it shouldn’t deter us from listening. This graph from his work, for instance, contains a great depiction of what EROEI really means, and how it works out, and that is important to know.

And yes, we are aware of the contradiction between the provocative title of this post (borrowed from SRSrocco Report) and our own view that it’s not energy that will bring the economy down; the internal dynamics of finance don’t need any help on their way towards crashing the system. But it’s a great title nonetheless.

First, here’s the SRSrocco Report interview, below it you’ll find the article. Note: this is part 1, links to parts 2 and 3 are provided.

Louis Arnoux: Some reflections on the Twilight of the Oil Age – part I:

Alice looking down the end of the barrel

This three-part post was inspired by Ugo’s recent post concerning “Will Renewables Ever ReplaceFossils?” and recent discussions within Ugo’s discussion group on how is it that “Economists still don’t get it”?It integrates also numerous discussion and exchanges I have had with colleagues and business partners over the last three years.

Introduction

Since at least the end of 2014 there has been increasing confusions about oil prices, whether so-called “Peak Oil” has already happened, or will happen in the future and when, matters of EROI (or EROEI) values for current energy sources and for alternatives, climate change and the phantasmatic 2oC warming limit, and concerning the feasibility of shifting rapidly to renewables or sustainable sources of energy supply.Overall, it matters a great deal whether a reasonable time horizon to act is say 50 years, i.e. in the main the troubles that we are contemplating are taking place way past 2050, or if we are already in deep trouble and the timeframe to try and extricate ourselves is some 10 years. Answering this kind of question requires paying close attention to system boundary definitions and scrutinising all matters taken for granted.

It took over 50 years for climatologists to be heard and for politicians to reach the Paris Agreement re climate change (CC) at the close of the COP21, late last year.As you no doubt can gather from the title, I am of the view that we do not have 50 years to agonise about oil.In the three sections of this post I will first briefly take stock of where we are oil wise; I will then consider how this situation calls upon us to do our utter best to extricate ourselves from the current prevailing confusion and think straight about our predicament; and in the third part I will offer a few considerations concerning the near term, the next ten years – how to approach it, what cannot work and what may work, and the urgency to act, without delay.

In his recent post, Ugo contrasted the views of the Doomstead Diner‘s readers with that of energy experts regarding the feasibility of replacing fossil fuels within a reasonable timeframe.In my view, the Doomstead’s guests had a much better sense of the situation than the “experts” in Ugo’s survey.To be blunt, along current prevailing lines we are not going to make it.I am not just referring here to “business-as-usual” (BAU) parties holding for dear life onto fossil fuels and nukes.I also include all current efforts at implementing alternatives and combating CC.Here is why.

The energy cost of system replacement

What a great number of energy technology specialists miss are the challenges of whole system replacement – moving from fossil-based to 100% sustainable over a given period of time.Of course, the prior question concerns the necessity or otherwise of whole system replacement.For those of us who have already concluded that this is an urgent necessity, if only due to CC, no need to discuss this matter here.For those who maybe are not yet clear on this point, hopefully, the matter will become a lot clearer a few paragraphs down.

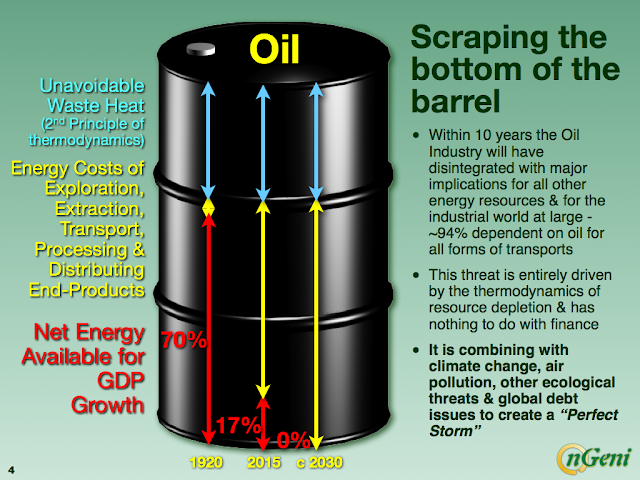

So coming back for now to whole system replacement, the first challenge most remain blind to is the huge energy cost of whole system replacement in terms of both the 1st principle of thermodynamics (i.e. how much net energy is required to develop and deploy a whole alternative system, while the old one has to be kept going and be progressively replaced) and also concerning the 2nd principle (i.e. the waste heat involved in the whole system substitution process).The implied issues are to figure out first how much total fossil primary energy is required by such a shift, in addition to what is required for ongoing BAU business and until such a time when any sustainable alternative has managed to become self-sustaining, and second to ascertain where this additional fossil energy may come from.

The end of the Oil Age is now

If we had a whole century ahead of us to transition, it would be comparatively easy.Unfortunately, we no longer have that leisure since the second key challenge is the remaining timeframe for whole system replacement. What most people miss is that the rapid end of the Oil Age began in 2012 and will be over within some 10 years.To the best of my knowledge, the most advanced material in this matter is the thermodynamic analysis of the oil industry taken as a whole system (OI) produced by The Hill’s Group (THG) over the last two years or so (https://www.thehillsgroup.org).

THG are seasoned US oil industry engineers led by B.W. Hill.I find its analysis elegant and rock hard.For example, one of its outputs concerns oil prices.Over a 56 year time period, its correlation factor with historical data is 0.995.In consequence, they began to warn in 2013 about the oil price crash that began late 2014 (see: https://www.thehillsgroup.org/depletion2_022.htm).In what follows I rely on THG’s report and my own work.

Three figures summarise the situation we are in rather well, in my view.

For purely thermodynamic reasons net energy delivered to the globalised industrial world (GIW) per barrel by the oil industry (OI) is rapidly trending to zero.By net energy we mean here what the OI delivers to the GIW, essentially in the form of transport fuels, after the energy used by the OI for exploration, production, transport, refining and end products delivery have been deducted.

However, things break down well before reaching “ground zero”; i.e. within 10 years the OI as we know it will have disintegrated. Actually, a number of analysts from entities like Deloitte or Chatham House, reading financial tealeaves, are progressively reaching the same kind of conclusions.[1]

The Oil Age is finishing now, not in a slow, smooth, long slide down from “Peak Oil”, but in a rapid fizzling out of net energy.This is now combining with things like climate change and the global debt issues to generate what I call a “Perfect Storm” big enough to bring the GIW to its knees.

In an Alice world

At present, under the prevailing paradigm, there is no known way to exit from the Perfect Storm within the emerging time constraint (available time has shrunk by one order of magnitude, from 100 to 10 years).This is where I think that Doomstead Diner’s readers are guessing right. Many readers are no doubt familiar with the so-called “Red Queen” effect illustrated in Figure 2 – to have to run fast to stay put, and even faster to be able to move forward.The OI is fully caught in it.

The top part of Figure 2 highlights that, due to declining net energy per barrel, the OI has to keep running faster and faster (i.e. pumping oil) to keep supplying the GIW with the net energy it requires.What most people miss is that due to that same rapid decline of net energy/barrel towards nil, the OI can’t keep “running” for much more than a few years – e.g. B.W. Hill considers that within 10 years the number of petrol stations in the US will have shrunk by 75%…

What people also neglect, depicted in the bottom part of Figure 2, is what I call the inverse Red Queen effect (1/RQ). Building an alternative whole system takes energy that to a large extent initially has to come from the present fossil-fuelled system.If the shift takes place too rapidly, the net energy drain literally kills the existing BAU system.[2] The shorter the transition time the harder is the 1/RQ.

I estimate the limit growth rate for the alternative whole system at 7% growth per year.

In other words, current growth rates for solar and wind, well above 20% and in some cases over 60%, are not viable globally.However, the kind of growth rates, in the order of 35%, that are required for a very short transition under the Perfect Storm time frame are even less viable – if “we” stick to the prevailing paradigm, that is.As the last part of Figure 2 suggests, there is a way out by focusing on current huge energy waste, but presently this is the road not taken.

On the way to Olduvai

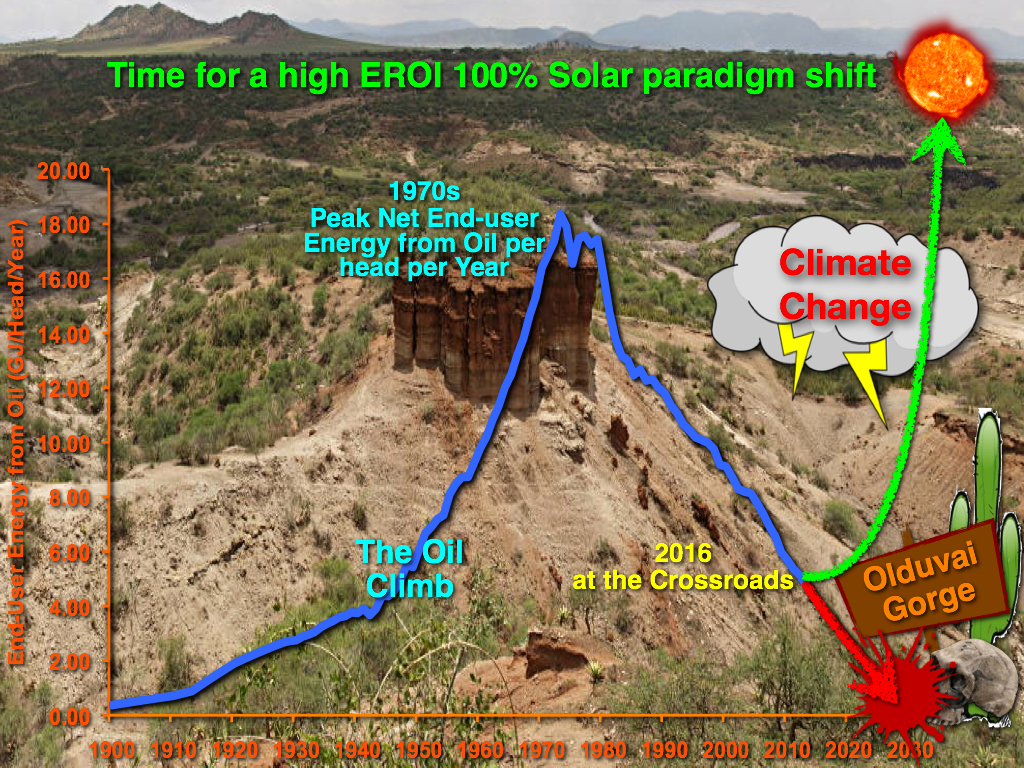

In my view, given that nearly everything within the GIW requires transport and that said transport is still about 94% dependent on oil-derived fuels, the rapid fizzling out of net energy from oil must be considered as the defining event of the 21st century – it governs the operation of all other energy sources, as well as that of the entire GIW.In this respect, the critical parameter to consider is not that absolute amount of oil mined (as even “peakoilers” do), such as Million barrels produced per year, but net energy from oil per head of global population, since when this gets too close to nil we must expect complete social breakdown, globally.

The overall picture, as depicted ion Figure 3, is that of the “Mother of all Senecas” (to use Ugo’s expression). It presents net energy from oil per head of global population.[3]The Olduvai Gorge as a backdrop is a wink to Dr. Richard Duncan’s scenario (he used barrels of oil equivalent which was a mistake) and to stress the dire consequences if we do reach the “bottom of the Gorge” – a kind of “postmodern hunter-gatherer” fate.

Oil has been in use for thousands of year, in limited fashion at locations where it seeped naturally or where small well could be dug out by hand.Oil sands began to be mined industrially in 1745 at Merkwiller-Pechelbronn in north east France (the birthplace of Schlumberger).From such very modest beginnings to a peak in the early 1970s, the climb took over 220 years.The fall back to nil will have taken about 50 years.

The amazing economic growth in the three post WWII decades was actually fuelled by a 321% growth in net energy/head.The peak of 18GJ/head in around 1973, was actually in the order of some 40GJ/head for those who actually has access to oil at the time, i.e. the industrialised fraction of the global population.

In 2012 the OI began to use more energy per barrel in its own processes (from oil exploration to transport fuel deliveries at the petrol stations) than what it delivers net to the GIW.We are now down below 4GJ/head and dropping fast.

This is what is now actually driving the oil prices: since 2014, through millions of trade transactions (functioning as the “invisible hand” of the markets), the reality is progressively filtering that the GIW can only afford oil prices in proportion to the amount of GDP growth that can be generated by a rapidly shrinking net energy delivered per barrel, which is no longer much.Soon it will be nil. So oil prices are actually on a downtrend towards nil.

To cope, the OI has been cannibalising itself since 2012. This trend is accelerating but cannot continue for very long.Even mainstream analysts have begun to recognise that the OI is no longer replenishing its reserves.We have entered fire-sale times (as shown by the recent announcements by Saudi Arabia (whose main field, Ghawar, is probably over 90% depleted) to sell part of Aramco and make a rapid shift out of a near 100% dependence on oil and towards “solar”.

Given what Figure 1 to 3 depict, it should be obvious that resuming growth along BAU lines is no longer doable, that addressing CC as envisaged at the COP21 in Paris last year is not doable either, and that incurring ever more debt that can never be reimbursed is no longer a solution, not even short-term.

Time to “pull up” and this requires a paradigm change capable of avoiding both the RQ and 1/RQ constraints.After some 45 years of research, my colleagues and I think this is still doable.Short of this, no, we are not going to make it, in terms of replacing fossil resources with renewable ones within the remaining timeframe, or in terms of the GIW’s survival.

Next:

Part 2 – Enquiring into the appropriateness of the question Part 3 – Standing slightly past the edge of the cliff

“.. it leaves young people paying twice, saving for their own pensions while also paying for the pensions of older generations through taxation.”

“Since 2007, the real disposal income of pensioners has risen by almost 10%. Those over the age of 65 have harvested fully two-thirds of that £2.7tn increase in national wealth. By contrast, since 2007, working-age households with children have achieved income gains of only about 3%, while the incomes of those without children have fallen by 3%,” he said.

This can only go horribly wrong, there is no other possible outcome, but it’s a topic politicians either don’t understand or don’t want to touch. Which is why I wrote Basic Income in The Time of Crisis a month ago. There is not much time left.

Older people have saddled the younger generation with an excessive bill for state pensions while grabbing an ever-greater share of NHS spending, according to a report that calls for intergenerational rebalancing. The report from the Intergenerational Foundation (IF) said spending promises on state and public sector pensions are “overwhelming young people’s prospects”. The thinktank is calling on the prime minister, Theresa May, to abandon triple lock protection, which promises that the state pension will rise each year by whatever is highest out of inflation measured by the consumer price index, average earnings growth or 2.5%. The former pensions minister Ros Altmann has called for the triple lock to be scrapped. The Department for Work and Pensions has declined to rule out a review of the “totemic” policy in the coming months.

The report estimates that workers are paying £2,846 a year each to cover the cost of paying state pensions. Public sector pension liabilities, for schemes such as retired civil servants, have risen by 12% to nearly £44,000 per worker, with total liabilities at £1.4tn, it added. Angus Hanton, the co-founder of IF, said: “Public sector pensions represent one of the largest unfunded burdens for younger taxpayers, who will not retire at the same age, or on the same terms, while having to contribute more to their own pensions. “Increasing retirement ages and moving to career average pensions will not be enough to stall the pension burden avalanche that is bearing down on the young.

Auto-enrolment is an apparent success, except that it leaves young people paying twice, saving for their own pensions while also paying for the pensions of older generations through taxation.” But charity Age UK said the vast majority of pensioners have contributed throughout their life to the state pension, which remains lower than the amount paid in many other western countries. Caroline Abrahams, the charity director at Age UK, pointed out that 1.6 million older people live in poverty in the UK. “A strong pensions system that provides a decent quality of life in retirement is central to a civilised society and in the best interests of us all,” she said.

“Postal-service operator Royal Mail said last week it may not be able to keep its program running beyond 2018. That’s because its annual contributions could more than double to over £900 million.”

Britain’s millennials, already suffering for the economic mistakes of the past, now face the prospect of having to pay for the country’s future. Pension-fund liabilities in the U.K. increased to a record £1 trillion ($1.3 trillion) after the Bank of England’s interest-rate cut this month, hurt by quantitative easing and razor-thin yields. It’s Britain’s version of what Duquesne Chairman Stanley Druckenmiller calls “Generational Theft” in the U.S. Plunging bond yields have caused pension liabilities to balloon and it could get even worse because the BOE will probably reduce interest rates further this year. Deficits for defined-benefit-pension funds already rose by more than 40% in the two months through July, following the vote to leave the EU and the central bank’s subsequent decision to increase quantitative easing, according to consulting firm Mercer.

“The Bank of England clearly believes that the effect on our pension system is acceptable long-term collateral damage” to prevent a short-term recession, said David Blake, professor of pension economics at London’s Cass Business School. Younger workers will “have to save more – which they appear reluctant to do – or be prepared to work much longer.” The increased bond-purchase program has had a relatively limited impact on pension deficits, according to the minutes of the BOE’s Monetary Policy Committee meeting on Aug. 3. While the fund managers have to move into riskier assets, that helps to support the economy, Governor Mark Carney said Aug. 4. “That makes it less likely that we will have a very long period of high unemployment, low output, and very low interest rates,” Carney said.

Money managers, however, appear to be unwilling to offload their higher-yielding gilts because they’re worried about generating enough returns to pay their members. The BOE last week failed to find enough investors who were prepared to sell their longer-maturity gilts, a slice of the credit market dominated by pensions and insurers. Companies that run defined-benefit pension funds are also starting to worry. Postal-service operator Royal Mail said last week it may not be able to keep its program running beyond 2018. That’s because its annual contributions could more than double to over £900 million.

Stock investors have had one sweet summer so far watching the markets edge higher. With the Standard & Poor’s 500-stock index at record highs and nearing 2,200, what’s not to like? Here’s something. As shares climb, so too do the prices companies are paying to repurchase their stock. And the companies doing so are legion. Through July of this year, United States corporations authorized $391 billion in repurchases, according to an analysis by Birinyi Associates. Although 29% below the dollar amount of such programs last year, that’s still a big number. The buyback beat goes on even as complaints about these deals intensify. Some critics say that top managers who preside over big stock repurchases are failing at one of their most basic tasks: allocating capital so their businesses grow.

Even worse, buybacks can be a way for executives to make a company’s earnings per share look better because the purchases reduce the amount of stock it has outstanding. And when per-share earnings are a sizable component of executive pay, the motivation to do buybacks only increases. Of course, companies that conduct major buybacks often contend that the purchases are an optimal use of corporate cash. But William Lazonick, professor of economics at the University of Massachusetts Lowell, and co-director of its Center for Industrial Competitiveness, disagrees. “Executives who get into that mode of thinking no longer have the ability to even think about how to invest in their companies for the long term,” Mr. Lazonick said in an interview. “Companies that grow to be big and productive can be more productive, but they have to be reinvesting.”

[..] The net profit test, said Gary Lutin, a former investment banker who heads the forum, “cuts through to the essential logic of comparing a process that grows a bigger pie – reinvestment – to a process that divides a shrunken pie among fewer people: share buybacks. “It’s pretty obvious,” he continued, “that even mediocre returns from reinvesting in the production of goods and services will beat what’s effectively a liquidation plan.” Investors may be dazzled by the earnings-per-share gains that buybacks can achieve, but who really wants to own a company in the process of liquidating itself? Maybe it’s time to ask harder questions of corporate executives about why their companies aren’t deploying their precious resources more effectively elsewhere.

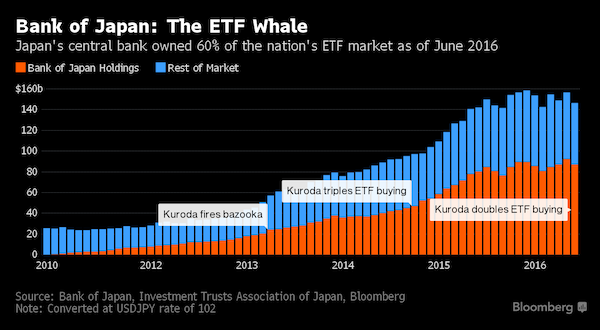

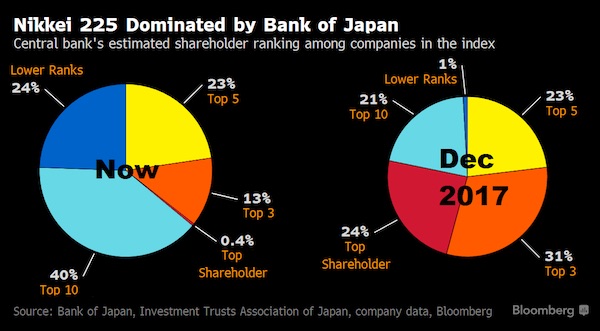

The Bank of Japan’s controversial march to the top of shareholder rankings in the world’s third-largest equity market is picking up pace. Already a top-five owner of 81 companies in Japan’s Nikkei 225 Stock Average, the BOJ is on course to become the No. 1 shareholder in 55 of those firms by the end of next year, according to estimates compiled by Bloomberg from the central bank’s exchange-traded fund holdings. BOJ Governor Haruhiko Kuroda almost doubled his annual ETF buying target last month, adding to an unprecedented campaign to revitalize Japan’s stagnant economy. While bulls have cheered the tailwind from BOJ purchases, opponents say the central bank is artificially inflating equity valuations and undercutting efforts to make public companies more efficient.

Traders worry that the monetary authority’s outsized presence will make some shares harder to buy and sell, a phenomenon that led to convulsions in Japan’s government bond market this year. “Only in Japan does the central bank show its face in the stock market this much,” said Masahiro Ichikawa at Sumitomo Mitsui Asset Management. “Investors are asking whether this is really right.” While the BOJ doesn’t acquire individual shares directly, it’s the ultimate buyer of stakes purchased through ETFs. Estimates of the central bank’s underlying holdings can be gleaned from the BOJ’s public records, regulatory filings by companies and ETF managers, and statistics from the Investment Trusts Association of Japan. Forecasts of the BOJ’s future shareholder rankings assume that other major investors keep their positions stable and that policy makers maintain the historical composition of their purchases.

[..] Japan’s government bond market offers a guide to the risks of further intervention in stocks, said Akihiro Murakami, the chief quantitative strategist for Japan at Nomura in Tokyo. JGB volatility soared to the highest level since 1999 in April, while trading volume has slumped as the central bank’s holdings swelled to about a third of the market. It’s still buying at an annual rate of 80 trillion yen. “If the BOJ does not sell stocks, then liquidity will disappear,” Murakami said. “As liquidity falls, the number of shares you can buy starts to decline – the same thing that’s happening in the JGB market.” The central bank owned about 60% of Japan’s domestic ETFs at the end of June, according to Investment Trusts Association figures, BOJ disclosures and data compiled by Bloomberg. Based on a report released on Friday by the Investment Trusts Association, that figure rose to about 62% in July.

Japan’s economic growth ground to a halt in April-June after a stellar expansion in the previous quarter on weak exports and capital expenditure, putting even more pressure on premier Shinzo Abe to come up with policies that produce more sustainable growth. The world’s third-largest economy expanded by an annualized 0.2% in the second quarter, less than a median market forecast for a 0.7% increase and a marked slowdown from a revised 2.0% increase in January-March, Cabinet Office data showed on Monday. The weak reading underscores the challenges policymakers face in putting a sustained end to two decades of deflation with the initial boost from Abe’s stimulus programs, dubbed “Abenomics,” fading. “Overall it looks like the economy is stagnating. Consumer spending is weak, and the reason is low wage gains.

There is a lot of uncertainty about overseas economies, and this is holding back capital expenditure,” said Norio Miyagawa, senior economist at Mizuho Securities. “The government has already announced a big stimulus package, so the next question is how the Bank of Japan will respond after its comprehensive policy review, which is sure to lead to a delay in its price target.” On a quarter-on-quarter basis, GDP marked flat growth in April-June, weaker than a median market forecast for a 0.2% rise. Private consumption, which accounts for roughly 60% of GDP, rose 0.2% in April-June, matching a median market forecast but slowing from a 0.7% increase in the previous quarter. Capital expenditure declined 0.4% in April-June after a 0.7% drop in the first quarter, the data showed, suggesting that uncertainty over the global economic outlook and weak domestic markets are keeping firms from boosting spending.

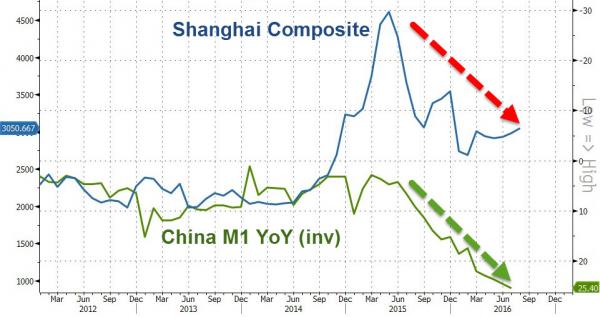

The last few months have seen trillions of dollars of fresh credit puked into existence in China to enable goal-seeked growth numbers to creep lower (as opposed to utterly collapse). The problem is… the Chinese are hoarding that cash at the fastest pace since Lehman as liquidity concerns flood through the nation. China’s M2, a broad gauge of money supply including savings deposits, rose at the slowest pace in 15 months and trailed the government’s full-year target of +11% in July. But, as Bloomberg details, by contrast, M1, the total of cash, checks and demand deposits, rose at the quickest pace in six years…

That shows companies “are holding all this cash, but investment returns are low and there are few options for projects,” said Liu Dongliang, a senior analyst at China Merchants Bank Co. in Shenzhen.

In fact, no matter what has been done since the Chinese stock market crashed, the Chinese have been hoarding cash…

In fact, the hoarding of cash in China corresponded with the top in 1999/2000, and the top in 2007…

“..If people don’t feel like they are beneficiaries of economic development, if they don’t think their lot in life is improving, that’s when they start getting all kinds of ideas.” We wouldn’t want that, would we?

China expects next month’s summit of the G20 which it is hosting will focus on boosting economic growth and other financial issues rather than disputes like the South China Sea, senior officials said on Monday. The summit of the world’s 20 biggest economies in the eastern city of Hangzhou will be the highlight of President Xi Jinping’s diplomatic agenda this year, and the government is keen to ensure it proceeds smoothly. The Sept 4-5 leaders’ meeting comes as clouds continue to hover over global growth prospects and worries about China’s own slowing economy. Last month’s meeting of G20 policymakers was dominated by the impact of Britain’s exit from Europe and fears of rising protectionism.

Yi Gang, a vice governor of the People’s Bank of China, said the summit will focus on how to stimulate sluggish global economic growth through open, inclusive trade and the development of robust financial markets. “We need to instil market confidence and ensure there are no competitive devaluations but rather let the market determine exchange rates,” Yi told a news briefing, adding this would be the first G20 to discuss foreign exchange markets in such detail. The G20 will also discuss how to better monitor and respond to risks presented by global capital flows, he said. Despite increasingly protectionist rhetoric around the world, the G20 is strongly opposed to anti-trade and anti-investment sentiment, Vice Finance Minister Zhu Guangyao said.

“We really do need to make sure that the people, the public, benefit from economic development and growth. If people don’t feel like they are beneficiaries of economic development, if they don’t think their lot in life is improving, that’s when they start getting all kinds of ideas.”

Germany, for example, does not want zero interest rates and those trillions of euros created through ECB’s massive asset purchases. Germany is a fully-employed economy with balanced public finances and an exploding current account surplus of 9% of GDP. With a 1.8% annual growth in the first half of this year, the economy is running almost an entire percentage point above its potential and noninflationary growth. [..] Now, for a sharp contrast, take a look at Italy. On a quarterly basis, there has been virtually no growth in the first half of this year. In fact, the economy has been declining and stagnating over the last four years, and is currently experiencing a price deflation. Italy’s 3 million of unemployed in June (10.6% of the labor force) are only slightly below that level in the same month of last year. A shocking 36.5% of the country’s youth is out of work.

[..] Germany, close to one-third of the euro area’s products and services, does not need, and does not want, the ECB’s extraordinarily loose monetary policy. But the hard-pressed economies of France, Italy, Spain, Portugal and Greece – another 50% of the euro area output – need that oxygen to survive. Easy money is all they got. Their budget deficits of 2-5% of GDP, and their rising public debt of 120-185% of GDP, leave no room for fiscal policy to support demand, output and employment. The EU authorities, whoever they are, have relented from imposing penalties on Spain and Portugal – and have looked the other way in the case of France – for transgressing the euro area budget deficit commitments. But they continue to insist on labor market deregulations and on other socially and politically sensitive measures that act as short-term growth and employment killers.

Budget deficits may be coming out of retirement. With economies all over the world growing too slowly and little scope left for new monetary stimulus, governments are turning their attention back to fiscal policy. This shift in thinking is overdue. In many countries, though not all, fiscal expansion is not just possible but also necessary. A resumption of budget activism, if it happens, won’t be riskless, so caution will be needed. A stubborn commitment to fiscal austerity, though, would be riskier still. The immediate response to the 2008 crash included fiscal easing – sometimes deliberate and sometimes the automatic consequence (higher public spending, lower tax revenues) of slumping activity. In most cases, expansionary budgets lessened the impact of collapsing demand, but they also pushed up public debt.

Before long, governments started tightening their budgets to get debt back under control. With demand still lacking, the hope was that monetary expansion would be enough to support recovery. It wasn’t. Governments have found that monetary policy is losing its potency. Interest rates are close to zero in many countries, and in some even negative. Huge bond-buying programs – QE – have delivered an additional monetary punch, but again with diminishing effects, and with a growing risk of financial instability as well. So fiscal policy, despite the recent growth of public debt, is back on the agenda. Central banks have been leading the call. In June, Fed Chair Janet Yellen told the Senate Banking Committee that U.S. fiscal policy had “not played a supportive role.”

In July, the ECB’s chief economist, Peter Praet, said “monetary policy cannot be the only remedy to our current economic challenges.” Governments are responding. Following the U.K.’s decision to quit the EU, the new Chancellor of the Exchequer, Philip Hammond, has promised a break with his predecessor’s approach and says he will “reset” fiscal policy. Added investment in infrastructure is under consideration as part of a new industrial strategy.

London could bear the brunt of a post-Brexit vote downturn, according to economic indicators in the weeks since the EU referendum pointing to job cuts, falling house prices and a decline in business activity in the capital. London’s economy was relatively unaffected by the previous downturn, compared with other UK regions, but early signs from the latest bout of turmoil suggest that it might not get off so lightly again, economists have said. This could have consequences for the government’s tax receipts and overall growth, given the city’s contribution to the UK economy. One key concern about the impact on London of the vote to leave the EU stems from the capital’s dependence on financial services.

London could lose its status as Europe’s financial capital if the UK leaves the single market and City banks are stripped of their lucrative EU “passports” that allow them to sell services to the rest of the bloc. Samuel Tombs, the chief UK economist at consultancy Pantheon Macroeconomics, said: “London was unscathed by the last recession, but its dependence on finance now is its achilles heel.” He highlighted a potential change of fortunes for London in a note to clients after surveys showed that companies in the capital had taken a hit from the referendum result. London has been the UK’s growth star for the past two decades, outperforming the rest of the country, Tombs said. “Surveys since the referendum, however, indicate that the capital is at the sharp end of the post-referendum downturn.” added.

London was the worst performer out of 12 regions on one measure of business activity for the weeks following 23 June, the day of the referendum. Companies in the capital cut jobs and suffered the sharpest fall in output since early 2009, when the UK was mired in recession, according to the Lloyds Bank regional purchasing managers’ index. Clients appeared reluctant to commit to new contracts, London businesses said, leading to a slump in order books. “The capital was hit harder than any other UK region,” said Paul Evans, the regional director for London at Lloyds commercial banking.

The EU should grant Turks visa-free travel in October or the migrant deal that involves Turkey stemming the flow of illegal migrants to the bloc should put be put aside, Foreign Minister Mevlut Cavusoglu told a German newspaper. Asked whether hundreds of thousands of refugees in Turkey would head to Europe if the EU did not grant Turks visa freedom from October, he told Bild newspaper’s Monday edition: “I don’t want to talk about the worst case scenario – talks with the EU are continuing but it’s clear that we either apply all treaties at the same time or we put them all aside.” Visa-free access to the EU – the main reward for Ankara’s collaboration in choking off an influx of migrants into Europe – has been subject to delays due to a dispute over Turkish anti-terrorism legislation and Ankara’s crackdown after a failed coup.

When Ambrose starts talking about energy -or anything other than finance, for that matter- I brace myself. He tends to go into cheerleading mode. In this piece, the only problem he sees is intermittency, and even that mostly as not a real issue. Advancements in technology, don’t you know…

Wind power has few friends on the political Right. No other industry elicits such protest from the conservative press, Tory backbenchers, and free market economists. The vehemence is odd since wind generates home-made energy and could be considered a ‘patriotic choice’. It dates back to the 1990s and early 2000s when the national wind venture seemed a bottomless pit for taxpayer subsidies. Pre-modern turbines captured trivial amounts of energy. The electrical control systems and gearboxes broke down. Repair costs were prohibitive. Yet as so often with infant industries, early mishaps tell us little. Costs are coming down faster than almost anybody thought possible. As the technology comes of age – akin to gains in US shale fracking – the calculus is starting to vindicate Britain’s vast investment in wind power.

The UK is already world leader in offshore wind. The strategic choice now is whether to go for broke, tripling offshore capacity to 15 gigawatts (GW) by 2030. The decision is doubly-hard because there is no point dabbling in offshore wind. Scale is the crucial factor in slashing costs, so either we do it with conviction or we do not do it all. My own view is that the gamble is worth taking. Shallow British waters to offer optimal sites of 40m depth. The oil and gas industry knows how to operate offshore. Atkins has switched its North Sea skills seamlessly to building substations for wind. JDR in Hartlepool sells submarine cables across the world. Wind power is a natural fit.