Dorothea Lange “Georgia road sign” July 1937

Looking out over the European landscape, metaphorically speaking, the more I read up on things that are developing, the more I think: what a web you guys have spun. Europe will stress test its banks, again, this year. And, obviously, everybody knows that stress tests in Europe, like in the US, have been conducted in ways that have left behind far more questions than answers. Financial shadow theater. So ECB president Mario Draghi said last year that there would have to be bank failures to make this year’s tests credible. He may not realize it, but that’s quite a condemnation of the ECB’s, and therefore his, earlier tests: he states outright that they were not credible.

The EU’s new head of its Single Supervisory Mechanism (SSM), Daniele Nouy says: “It seems precisely what markets expect from such an exercise; I do not have any idea of how many banks have to fail. What I know is that we want to have the highest level of quality. … A failure of a bank may happen.” Yeah. well put. What this means is they’re going to, by lack of a better term, ritually sacrifice a number of (perhaps even) pre elected banks, just in order to look believable.

But Europe, like the US, has too-big-to-fail banks (they like to use the term “systemic”), so those banks won’t be touched, and certainly not in public. Which banks are those? Well, quite a few EU countries have bought and bailed out their largest banks, so they’re off-limits when it comes to letting them fail. They’ll end up closing some of the smaller banks, which may not even be the worst off.

Moreover, the stress test will be based on valuations that are, let’s say, not necessarily realistic. Unless you think that stock markets and housing prices propped up by the stimulus credit handed out by Draghi reflect free market reality. And that the “threat” of unlimited support through the OMT program that was put in doubt by Germany’s upper court last week, will still stand, and keep PIIGS sovereign debt yields at historic lows.

And even that’s not all. When it became clear that the ECB would not be allowed to buy up sovereign debt, but it had no problem supporting banks, peripheral nations locked a deal with their banks where the latter would borrow from the ECB, and buy domestic bonds with the loans. Everybody happy. Or, until the next stress test.

The EU is complicit in this complex scheme, but would never admit it. Bloomberg: When Europe’s leaders set out in June 2012 to break the “vicious circle” between banks and sovereigns, they left rules for treating government bonds untouched, an oversight that may subvert their drive to prevent a recurrence of the debt crisis. Under EU rules, banks can rate all debt issued by the bloc’s 28 national governments as risk-free, avoiding any increase in their capital requirements. This encourages so-called carry trades, whereby lenders borrow at low cost from the European Central Bank and plow the money into state debt that offers higher returns.

Without the OMT, which – see German court – may be exposed as a stark naked emperor soon, there is no outright support for peripheral nations, and not for their bonds, and that might have a huge impact on stress tests results of Spanish, Italian and even French banks. We’re on thin ice here.

What’s the risk in EU banks, what sort of debt/money are we talking about? Funny you should ask, and funny that’s hard to say. The Telegraph yesterday cites Davide Serra, a banking advisor for the UK Government, as saying “Eurozone banks face $69 billion ‘capital black hole”. However, a report that was revealed last month , written by Viral Acharya, New York University Professor and European Systemic Risk Board advisor and Sascha Steffen of Berlin’s European School of Management and Technology, implies that an objective stress test of the Eurozone’s biggest banks could reveal a capital shortfall of more than $1 trillion and, as they noted, trigger further public bailouts.

You tell me. Interestingly, the same Davide Serra the Telegraph quotes there says that Germany has ” one of the worst banking systems in the world”>. And that several Landesbanken may be “wound up”. Several people from Landesbank Baden-Wuerttemberg and its auditor PricewaterhouseCoopers are already on trial in Germany over fraud to the tune of many billions. Talking about fraud, European banks are strong medal contenders when it comes to – convictions for – price fixing, rate rigging etc.:

So European banks need anywhere in the range from $69 billion to $1 trillion. Spanish banks have shed 35% of their – domestic – sovereign debt holdings since August, and 29% in December alone, which of course puts Spanish bonds under pressure. Cue Draghi. Word has it that Italian banks need $15 billion, in an economy that sees its manufacturing numbers still going down. Cue Draghi. Will Greek and Portuguese banks do any better? No. So cue Draghi. But what does Draghi have left?

Switzerland, not an EU nation, yesterday voted to curb immigration. That will be more fuel on the fire for right wing Europe. Who were already set to win this spring’s European parliament election. There are very serious riots going on in Ukraine and more recently in Bosnia. It’s not the periphery inside the EU, this time (so far), but the one just outside of it. Bosnia: 40% unemployment. Go figure.

And Italy is trying to lock up my buddy Beppe Grillo, often conveniently painted into the right wing corner just because he claims the EU hurts his country and he manages to get his compatriots to leave their couches, on a bunch of silly trumped up charges. Italy’s old order fears Beppe. Whose 5-star movement now has 25% of the votes in Italy. And they don’t want to throw out immigrants. They want to throw out Mario Draghi.

Europe will maybe look “normal” for a while longer. We’re only human, we’re very good at keeping up appearances. But what’s the value of that, why do people find it so important to keep failed models, to keep failure itself, alive? We do that because the very people responsible for failure are still in power. It’s the normal order of things. And it won’t be long now. That’s only normal too.

Tyler Durden dives in to the US unemployment numbers again, and it’s all so convoluted it’s simply hilarious. Between seasonal adjustments and birth/death models the BLS manages to hide a dark picture.

• About Those 2.9 Million Jobs Lost In January… (Zero Hedge)

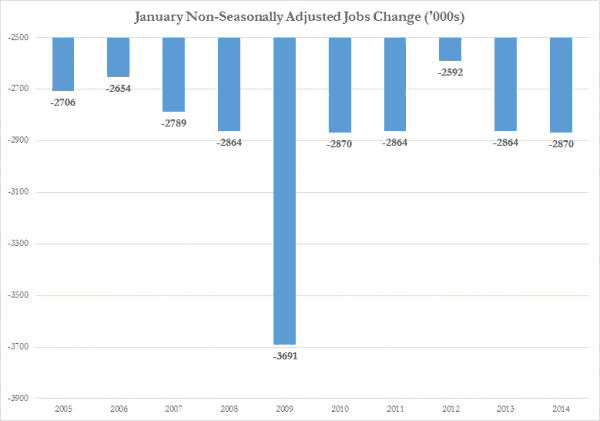

Much has been said about the January Non-farm payrolls number, which rose by 113K on expectations of a 180K increase, most of which has been focused on the US atmospheric conditions during the winter. There is a problem with those numbers: they don’t really exist. So what really happened in January?

For the real answer we have to go to the BLS’ non-seasonally adjusted data series. It is here that we find that in January, some 2.870 million real, actual jobs were lost, not gained. Putting this further in perspective, the number of NSA jobs losses in January 2014 was greater than in January of 2013, 2012, 2011 and tied that of 2010. In fact only during the peak of the depression in January 2009 was there a greater NSA drop in the first month of the year when 3.691 million jobs were lost.

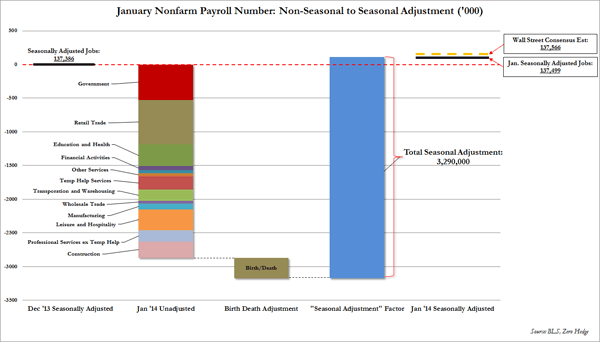

So how does a loss of 2.9 million jobs become a “gain” of 113K jobs in the same month? Simple: through the magic of seasonal adjustments.

Incidentally, for all those confused, it is these same seasonal adjustments that at least on paper, are supposed to account for such things as seasons, and, well, weather. Only sometimes they apparently don’t, like right now. Which is also the reason why one can completely ignore the entire seasonal adjustment process because one after another economist is lining up to inform anyone caring to listen that the seasonal adjustment number is actually not adjusted enough. Below we break down which jobs comprised the 2.9 million jobs lost when ignoring the ARIMA fudge factors.

On one hand the transition from 137.386 million seasonally adjusted December jobs to 137.499 million seasonally adjusted January jobs is simple: just add 113K jobs. On the other, the one has to consider that the actual number of January 2014 jobs was a far lower 135.396 million jobs. Furthermore, one has to recall that his unadjusted number is the one impacted by the monthly Birth-Death adjustment. For those who don’t recall this nuance, here is the BLS’ explanation of this incremental adjustment factor to the final number.

In January the Birth-Death adjustment resulted in a further 307K jobs being subtracted from the final NSA number as an intermediate adjustment step.So what happened next? Instead of explaining, we’d rather show it:

The bottom line is that through the magic of the BLS’ statistical gimmickry, a NSA change of -2,870K, impacted by a further -307K “Birth/Deaths” (or -3,177K total), became a positive 113K change in the seasonally adjusted jobs series, or a total “seasonal adjustment” factor of 3.290 million!

And here, keep in mind, that the Wall Street estimate for a payroll “beat” was the addition of 180K. Of course, in keeping with the above “seasonal” transformation, what this means is that instead of having added a total of 3.290 million “statistical” jobs, the Bureau simply had to bump up the “fudge factor” to 3.357K or over, to match or beat the expectations. The difference between the 3.290MM and 3.357MM numbers? 2%.

Which begs the question: why did whatever prompted the BLS to add just under 3.3 million “excel” jobs, not also prompt them to add another 57K jobs to the final adjustment number which was a minute fraction of the total fudge factor, and beat Wall Street estimates, reincarnating the narrative that the US economy is now back in “escape velocity” mode, it is “self-sustaining” and all those other spins and stories serious economists tell themselves to justify that QE has worked? Unless, it was specifically the intention of the BLS to not give such an impression.

Whether the reason was precisely to give the Fed the loophole it needs to taper the taper in a few weeks time when the latest “economic recovery” thesis crashes and burns, will be uncovered over the next several months.

Finally, for all those same very serious economists who lament the impact of the weather on the Establishment survey, and yet point to the surge in the Household Survey which “added” 638K seasonally-adjusted jobs, the unadjusted change there was a drop of 403K jobs. So there’s that.

Watch the USD. It ain’t over yet by a long stretch.

• The Greater the Turmoil, the Stronger the Dollar. Again. (NY Times)

Chronic problems have been flaring up in financial markets lately, and some of them may emanate from the United States. Yet none of these issues have seriously damaged the exalted status of what Washington Irving once called “the almighty dollar.” In fact, a familiar pattern has been emerging: When the world’s financial system runs into trouble, the position of the dollar as the world’s crucial currency becomes more formidable. [..]

It’s not that the dollar is universally viewed as an ideal linchpin for global finance, or that other countries believe that the United States should enjoy the “exorbitant privilege” of minting the world’s money. That’s what Valery Giscard d’Estaing called it when he was French finance minister in the 1960s. D’Estaing and Charles de Gaulle, the French president, sought unsuccessfully to reduce the dollar’s clout.

The United States, de Gaulle said, was using the dollar to expand American influence, making it cheaper for US companies to operate and for the US government to finance its activities. All of this, he said, amounted to hidden subsidies paid by the rest of the world. [..]

Richard Madigan, chief investment officer of J.P. Morgan Private Bank, agrees that many of these developments have occurred because of a “global dollar trap.” “People have moved money into Treasurys and made interest rates on US government debt much lower than they probably ought to be,” he said. “It’s counterintuitive, but even when finances are unsettled in the United States, it’s still the center of the global financial system, and it’s where people go for safety.”

It’s where they go, even though in some ways the United States is a very odd place to seek financial security. On Friday, after all, the Treasury had to resume its now-familiar routine of taking “extraordinary measures” to avoid a sovereign debt default. Yet investors were generally not alarmed.

China. Much more to come. Long way away from balance. “It would be best if the government will allow defaults”, says someone. Yes, but I tell you, the government is too afraid to let that happen.

• Junk Yield Premiums Soar on China’s Looming First Default (Bloomberg)

The extra cost to borrow for China’s riskiest companies is at the highest in 20 months as soaring interest rates heighten concern the nation will experience its first onshore bond default.

The failure of coal companies to meet payment deadlines for trust products has increased concern over debt defaults, with the equivalent of $53 billion of bonds sold by renewable energy, construction materials, metals and mining companies due in 2014. A report on Jan. 30 signaled China’s factories are contracting for the first time since August amid signs of financial stress including mounting losses and bailouts.

“China’s bond market will definitely see its first default this year,” said Xu Hanfei, a bond analyst in Shanghai at Guotai Junan Securities Co., the nation’s third-biggest brokerage. “The economy is slowing while the government seems still confident about growth, which means the authorities probably won’t announce any measures to avert the slowdown. This is the worst scenario.” [..]

China’s central bank signaled in a Feb. 8 report that volatility in money-market interest rates will persist and borrowing costs will rise, further underscoring the risk of defaults which could weigh on confidence and drag down growth. [..]

“It would be best if the government will allow defaults,” Zhang Ming, a senior research fellow at the government-backed Chinese Academy of Social Sciences in Beijing, said in a Jan. 22 interview. “The bubbles are gradually inflating, and sooner and later there will be a collapse. The best scenario is that you allow defaults in some places when you are ready so that some risks can be released. The later the default, the more damaging.”

Every government likes the appeal of their citizens pension money, and China is no exception.

• China to Form Unified Pension System to Boost Social Mobility (BusinessWeek)

China will combine its urban and rural pension insurance systems to promote social mobility without concerns of loss of retirement income. A unified pension system will help consumption, according to a statement posted on the central government’s website after a State Council meeting today led by Premier Li Keqiang.

The Chinese government is shifting focus to providing higher-quality public services and simplifying bureaucracy to stabilize economic growth and create more jobs. The world’s second-largest economy is forecast to expand by 7.4 percent this year, the slowest pace since 1990.. China’s Communist Party leadership on Nov. 15 detailed changes including easing the one-child policy and scrapping aspects of the household registration system, or hukou, that impeded migration between villages and cities. The government is also ending a freeze on stock listings and seeking to curb pollution.

Japan is starting to feel like a bad dream that won’t end. The tax hike on April 1 is 7 weeks away.

• Japan’s December Current-Account Deficit Widens to Record (Bloomberg)

Japan’s current-account deficit widened to a record in December on soaring imports, adding to Prime Minister Shinzo Abe’s challenges as he tries to drive a recovery in the world’s third-biggest economy.

The 638.6 billion yen ($6.2 billion) shortfall surpassed November’s gap of 592.8 billion yen, the finance ministry said in Tokyo today. The deficit was smaller than the 685.4 billion yen median forecast of 27 economists in a Bloomberg survey. Comparable data go back to 1985.

The yen’s slide and increased demand for foreign energy due to nuclear plants closures are causing imports to outstrip exports, dragging on an economy that is forecast to contract after the government lifts a sales tax in April. A surplus in overseas investment income is staving off the risk of a sustained deficit that could undermine investor confidence in a nation with the world’s largest debt burden.

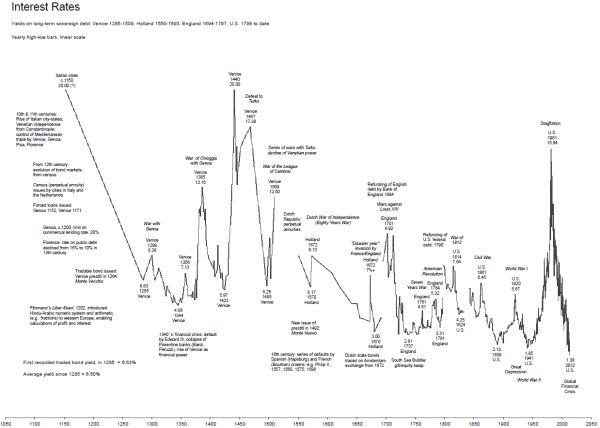

A series of great graphs depicting developments over the past 1000 years. I’ll post the one on interest rates. For gold, commodities and stocks, please click the link and see the article.

• Western Markets Since The Middle Ages: Charts (Zero Hedge)

We previously examined 240 years of US market history for a sense of ‘trend’ or sustainability but some were not satisfied. In order to get a truly long-term perspective, we reach back 1000 years to The Middle Ages and look at how stock prices, interest rates, commodity prices, and gold have changed in a millennia (and most notably how the key historical events have shaped those price changes).

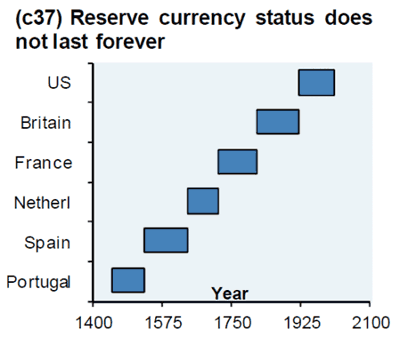

And just for good measure, perhaps the most important chart going forward – Nothing lasts forever…

Europe is shaking all over.

• Europe faces economic and electoral instability (Reuters)

The threat to its survival may have passed but the euro zone faces electoral and economic crosswinds this year which could push the region to break policy taboos while challenging its ability to do so. The threat of deflation is stalking the single currency area and increasing pressure on the European Central bank (ECB) to act. Anti-euro parties look set to perform well at elections to the European Parliament in May and could hamper the bloc’s ability to enact measures to bind its member states together more closely.

Euro zone leaders are still struggling to generate solid economic growth that can eat away at unemployment rates running at 25 percent and more in the hardest hit countries, and efforts to create a banking union to prevent a future financial crisis are widely viewed as having fallen short. [..]

The latest threat to the euro zone is the evaporation of inflation. Japan’s lost decade is a vivid reminder of what could be at stake and that the only cure may be printing money, a difficult pill for the ECB to swallow. The ECB left rates at a record low 0.25 percent last week but its president, Mario Draghi, signalled that its next meeting next month might be a different matter. By then, it will have fresh forecasts for growth and inflation and if they are lowered, action could follow.

Draghi insists deflation is not in prospect but if the latest bout of emerging market turmoil persists, that could well push the euro higher and exert further downward pressure on prices. High unemployment, austerity fatigue and paltry growth offer the perfect backdrop for fringe parties to prosper at the EU elections in May.

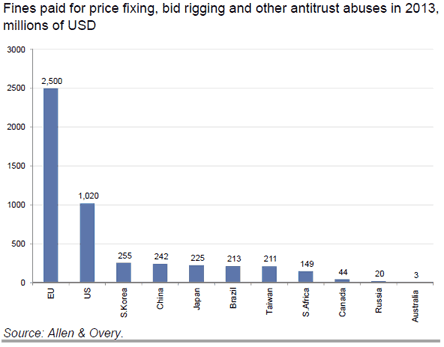

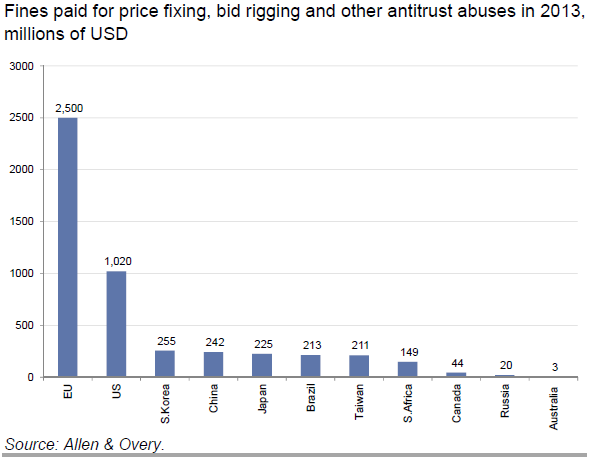

But it’s all just make believe. Real numbers are far worse. The fines are but a reminder of that.

• Why You Shouldn’t Trust Europe In One Simple Chart (Zero Hedge)

While China (or Russia) are held up as the world’s most corrupt among developed nations among the status-quo-huggers, it would seem there are two other nations that dominate when it comes to getting caught. Europe paid more in fines (in fact double the US and 10 times China) for price-fixing, bid-rigging, and other anti-trust abuses in 2013.

So why would we believe them that ‘recovery’ is right around the corner?

A normal reaction, too try and leave your society be what it was when you were young. But they’ll keep on coming as long as you have much more than they do. Like the wind blows from high pressure to low pressure.

• European right-wing hails Swiss vote to curb immigration (AFP)

Right-wing parties in Europe hailed Swiss voters for approving curbs Sunday on EU immigration while mainstream European media worried about potential ripple effects across the continent. The European Commission said it would assess close European Union ties with non-member Switzerland following the vote, raising the prospect of restricted trade or other retaliatory measures.

Nigel Farage, the head of the UK Independence Party, Britain’s main eurosceptic party, said Switzerland had stood up to “bullying” from unelected bureaucrats in Brussels. “This is wonderful news for national sovereignty and freedom lovers throughout Europe,” said Farage, who is a member of the European parliament (MEP).

The German newspaper Tagesspiegel said: “With the (Swiss) referendum, it becomes more likely that the anti-Europeans will represent the biggest group in the European parliament, with a quarter of the MEPs. In France, the business daily Les Echos, described the result as one with “economic consequences that are difficult to predict”.

The vote obliges the Bern government to renegotiate within three years a 2007 deal struck with Brussels that gave most EU citizens free access to the Swiss labour market. It was one of a series of accords reached in 1999 after five years of talks that were seen as a way for Switzerland and the EU to enjoy access to each other’s markets without Switzerland having to opt for full EU membership. Brussels, though, has warned that Switzerland cannot cherrypick from the binding package of deals, which were themselves approved in a 2000 referendum.

The Belgian newspaper Le Soir noted that “it’s the whole scaffolding of Switzerland’s bilateral accords with the European Union which is assured of collapse”. Centre-left El Pais, Spain’s top selling newspaper, worried about ripple effects of the vote in an editorial called “Perverse Consequences” published in Monday’s edition. “While by a narrow majority (50.3% of votes cast), the victory of those who oppose ‘mass immigration’ in Switzerland will have consequences for all of Europe,” it said.

Spanish conservative daily ABC wrote on its website that the outcome of the referendum “caused a real political earthquake in this central European nation and it puts its ties with the European Union in danger”.

• Eurozone banks face $69 billion ‘capital black hole’ (Telegraph)

Eurozone banks are facing a new capital black hole of as much as €50bn (£42bn), according to one of the UK’s most respected financial analysts. Davide Serra, the chief executive of Algebris, who advises the Government on banking, said that this year’s stress tests by the European Banking Authority and the European Central Bank were likely to find fresh problems in the eurozone banks.

He said that Germany had one of “the worst banking systems in the world”> and that three or four regional Landesbanken were likely to be wound up. He also said banks in Portugal and Greece were likely to need more capital. “The country where I expect bad news is the country which has not been scrutinised and has been deemed to be the strongest,” Serra said.

“I expect more bad news coming out of Germany. The strongest German Panzer was unbeatable, but there is only one problem – they have one of the worst banking systems in the world. If you are a bright engineer in Germany you work for BMW or Mercedes, you do not become a banker. “I expect at least three or four [regional] Landesbanken to be put in run-off mode. The German regulator, BaFin, is one of the weakest. It has always been lobbied by local politicians.”[..]

With combined assets of a trillion euros, the [German] banks account for 12% of the country’s total banking assets, and 3% of Europe’s as measured by the ECB. Many believe that a number of them are sitting on badly performing property loans which have never been properly accounted for. “I think the ECB exercise will actually allow them to do what is right,” Serra said of the German regulators. “That is one of the reasons why the Bundesbank has been very forceful – requiring auditors to be in the process. Why? They need a legal piece of paper so they can go to the local Landesbanken and say: ‘Sorry, game over’.”

Central bankers look eerily like similar to politicians.

• Some EU banks need to fail to make stress tests ‘credible’ (Reuters)

Some banks need to fail a sector-wide review of their financial health in order to make the exercise credible, the head of the euro zone’s new banking supervisor told the Financial Times. As part of a broad push for closer integration of Europe’s banks to avert future crises, the Single Supervisory Mechanism (SSM) will monitor the bloc’s largest lenders from November under the auspices of the European Central Bank.

Before then, the SSM is running the rule over the quality of the assets on the balance sheets of the bloc’s 128 biggest banks. That will run in parallel with broader stress tests of the whole banking sector under the control of Europe’s regulator, the European Banking Authority (EBA).

ECB president Mario Draghi said last year there needed to be bank failures to make the battery of tests credible, comments SSM head Daniele Nouy underlined in an interview published today. “It seems precisely what markets expect from such an exercise; so, yes, probably that’s the case,” she told the FT. “I do not have any idea of how many banks have to fail. What I know is that we want to have the highest level of quality. … A failure of a bank may happen.”

“Resolving this isn’t easy.” Well, for some people, lying never is.

• EU Banks’ Debt Addiction Threatens ECB-Led Overhaul (Bloomberg)

When Europe’s leaders set out in June 2012 to break the “vicious circle” between banks and sovereigns, they left rules for treating government bonds untouched, an oversight that may subvert their drive to prevent a recurrence of the debt crisis.

Under EU rules, banks can rate all debt issued by the bloc’s 28 national governments as risk-free, avoiding any increase in their capital requirements. This encourages so-called carry trades, whereby lenders borrow at low cost from the European Central Bank and plow the money into state debt that offers higher returns.

Twenty months after leaders pledged to change this behavior, banks hold more sovereign paper than ever. ECB President Mario Draghi said in December that when the Frankfurt-based central bank offered about €500 billion ($680 billion) of new low-cost liquidity two years ago, lenders used it “mostly to buy government bonds,” rather than for lending to stimulate the economy.

“We are working very hard to try to sever this bank-sovereign link, but the more we examine it, the more it seems that it’s never-ending,” said Sharon Bowles, chairwoman of the European Parliament’s Economic and Monetary Affairs Committee. “At least we’ve got to a position in the last few years that everyone recognizes the problem” of the zero-risk loophole, she said. “Resolving this isn’t easy.”

Knowing Beppe, I think he’s not afraid. “He questioned the wisdom, as Italy struggles to rein in its finances, of spending public money on a trial against 20 people for breaking a seal.”

• Prosecutor seeks nine-month jail term for Italy’s Beppe Grillo (Reuters)

An Italian prosecutor on Friday asked for a nine-month jail sentence for Beppe Grillo, the leader of the anti-establishment 5-Star Movement, who is accused of breaking a police seal on a building during a protest, a courtroom official said. The 5-Star Movement rode a popular wave of disgust at a political class perceived as corrupt and took a quarter of the votes in its first-ever national election a year ago. Grillo is the dynamo behind the movement, whose success is fuelled by his fiery speeches in town squares and by his blog, one of Italy’s most popular. The 5-Star Movement currently has the support of 20 to 25 percent of Italy’s voters, polls show.

Former comedian Grillo and about 20 activists of the No TAV movement, which campaigns against a high-speed train line between France and Italy, are accused of breaking a police seal on a wooden hut close to the train line that had been cordoned off by authorities in December 2010. The 5-Star support base overlaps with the No TAV movement, which says a Turin-Lyon train line is a vanity project that takes money from struggling ordinary Italians and threatens the environment.

In a light-hearted entry on his blog Grillo wrote that he admitted entering the hut, which was built by the protesters, and having a bowl of cornmeal porridge and a glass of wine inside, but there was no seal on the door for him to break. He questioned the wisdom, as Italy struggles to rein in its finances, of spending public money on a trial against 20 people for breaking a seal.

According to Italian media reports, Grillo is also under investigation on suspicion of “inciting activists to break the law” due to a open letter he wrote to the police and army asking them not to stand between protests and the Italian political class.The next hearing in the Turin trial is due on February 14.

No demand = deflation.

• Venice is safe, but a dearth of demand has Europe sinking (Guardian)

The Italian economy, in common with most members of the eurozone, has been, and is, suffering from the double blow of the financial crisis itself and the faulty structure of the arrangements for what used to be called “the single currency”. And this is an economy which, for all its intrinsic faults – known technically as structural or labour market rigidities – somehow or other managed to get by quite well for years, and was admired for the ingenuity of its small and medium-sized firms.

Of course, Italy had a chronic “competitiveness” problem, with a rate of inflation persistently higher than that of Germany, a very important trading partner. It used to annoy the German economic establishment that Italy would get back in step via occasional adjustments to its currency (that is, devaluation) and I can testify that there was joy in German official circles when, as a result of joining the euro, Italy lost this important instrument of economic policy.

This year I was particularly struck by a remark made by one senior figure in Venice, who, after an elaborate disquisition on the many “supply side” reforms that were under way, suddenly confessed at the end that it was difficult to introduce reforms “when people are scared and there is no [economic] expansion”.

It had been the worst crisis and “recovery” in the nation’s history, he said. “Tensions are growing … We know we are at risk.” He speculated about whether “growth was for democratic capitalism what repression is for authoritarian societies”. Did we know how to manage a society that had lost the mechanism of growth?

[..] … in the case of Italy and other non-German members of the eurozone the problem is not one of bubbles but of a lack of growth stemming principally from a dearth of economic demand: this is associated with the eurozone’s austerity policies, and aggravated by the loss of the exchange rate instrument of economic policy.

And if anyone tells me that the restitution of exchange rate flexibility within Europe would lead to a series of self-destructive competitive devaluations, I should reply that that would demonstrate – guess what? – a serious lack of demand.

When the winter began, the US was supposed to rival Saudi Arabia. How’s that looking now, guys?

• High heating bills ravage American consumers (Yahoo)

The polar vortex caused nationwide shivers when it swept across the United States in early January. Now it’s causing convulsions and hyperventilating as millions of American open their latest heating bill. [..]

Weather often wreaks havoc with household budgets, especially in the winter. Economists estimate the unusually cold weather that has frozen much of America during the past two months could cut $5 billion off economic activity, mainly because increased demand for energy has pushed prices higher, which means people are spending more for the same amount of fuel.Overall, the added cost — so far — probably isn’t enough to cut economic growth by much. “Most people have enough experience with heating bills that they know they’ve got to be a little careful in the winter,” says economist Chris Christopher of forecasting firm IHS Global Insight. “They’re on the lookout for higher bills.” [..] The cold snap could clip the economy more if it persists into spring, since by then many people will have exhausted any extra money put aside for winter expenses. “Where bad winter weather has an impact on consumers is at the bookends of the season,” says Christopher.

There could also be unanticipated problems other than high heating bills, if the cold lingers. Scott Spaulding, a veterinarian in Janeville, Wisc., hasn’t paid a dime more than expected for heat this winter, even though temps in Wisconsin have routinely fallen below 0. That’s because he planned ahead and locked in a price for propane of $1.60 per gallon last summer. His propane supplier assures him they’ll honor that price, even though propane has recently fetched $6 per gallon or more, due to temporary shortages caused by soaring demand.

But Spaulding noticed that, instead of filling his tank during a recent delivery, the supplier only left it about 40% full. He looked into it and discovered that many local propane companies are rationing supplies to reduce the chances of running out. “The company tells us there’s nothing to worry about, but what if they go bankrupt?” he says. “Other suppliers in our area aren’t taking any new customers.”

“The great unknowns of the open ocean” are 10 times more numerous than thought. We know nothing about the deep oceans. But we still dump our toxics in them like there’s no tomorrow.

• Fish Biomass in Ocean Is Ten Times Higher than Estimated (FNA)

With a stock estimated at 1,000 million tons so far, mesopelagic fish dominate the total biomass of fish in the ocean. However, a team of researchers with the participation of the Spanish National Research Council (CSIC) has found that their abundance could be at least 10 times higher. The results, published in Nature Communications journal, are based on the acoustic observations conducted during the circumnavigation of the Malaspina Expedition.

Mesopelagic fishes, such as lantern fishes (Myctophidae) and cyclothonids (Gonostomatidae), live in the twilight zone of the ocean, between 200 and 1,000 meters deep. They are the most numerous vertebrates of the biosphere, but also the great unknowns of the open ocean, since there are gaps in the knowledge of their biology, ecology, adaptation and global biomass. During the 32,000 nautical miles traveled during the circumnavigation, the researchers of the Malaspina Expedition (a project led by CSIC researcher Carlos Duarte) took measurements between 40°N and 40°S, from 200 to 1,000 meters deep, during the day.

Duarte states: “Malaspina has provided us the unique opportunity to assess the stock of mesopelagic fish in the ocean. Until now we only had the data provided by trawling. It has recently been discovered that these fishes are able to detect the nets and run, which turns trawling into a biased tool when it comes to count its biomass.”

Xabier Irigoyen, researcher from AZTI-Tecnalia and KAUST (Saudi Arabia) and head of this research, states: “The fact that the biomass of mesopelagic fish (and therefore also the total biomass of fishes) is at least 10 times higher than previously thought, has significant implications in the understanding of carbon fluxes in the ocean and the operation of which, so far, we considered ocean deserts.”

This article addresses just one of the many issues discussed in Nicole Foss’ new video presentation, Facing the Future, co-presented with Laurence Boomert and available from the Automatic Earth Store. Get your copy now, be much better prepared for 2014, and support The Automatic Earth in the process!

Home › Forums › Debt Rattle Feb 10 2014: A Tear For The First World