John M. Fox Midtown Dealers Corp. and Hudson showroom, Broadway at W. 62nd Street, NY 1947

Head and shoulders.

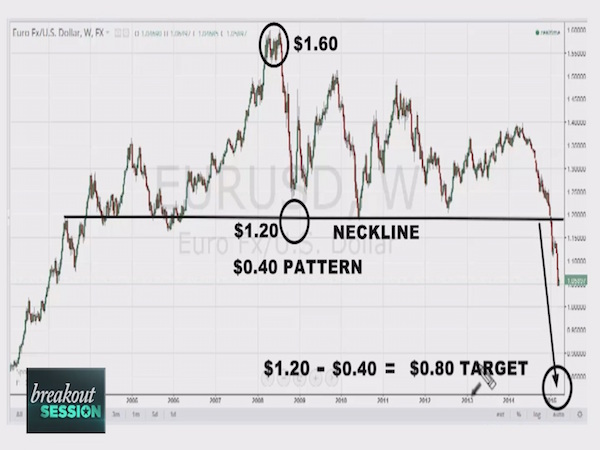

• This Chart Says Euro Could Plunge Another 30% (CNBC)

The sharp and explosive move higher by the euro Wednesday may have some thinking the worst is over for Europe’s common currency. But as it retraces its gains, one top technician’s chart work suggests the euro is going significantly lower. “Historically oversold conditions in the euro set the stage for an incendiary move [Wednesday],” said Evercore ISI’s Rich Ross, who added that the euro could see touch $1.12 in the coming weeks. “But ultimately the euro is going lower.” Using a weekly chart, Ross explained that euro broke a key technical pattern that could presage more pain. Specifically, he pointed to the fact that the euro has gone below the “neckline” of a long-term head and shoulders pattern. Technicians often look to this type of price action as confirmation to sell. “Any way you cut it, this breakdown is bad,” he said.

As Ross sees it, given the severity of the technical breakdown, the euro is likely to test or even make a new all-time lows of 80 U.S. cents. He arrived at his target by subtracting the lowest point of the pattern, in this case the neckline at $1.20, from the height point, which is the top of the “head” at $1.60. He then subtracts that total of 40 cents from the neckline, which gives him his target of 80 cents. Of course, Ross doesn’t feel the euro’s decline will happen overnight, and in the medium term, he does expect it will find support at the lower end of its trend channel around $1.05, at which point the currency could bounce. But in any event, Ross’ message is clear. “Ultimately, the euro is going a lot lower.”

Ain’t that a fact?!

• Britain’s Obsession With Ownership Has Made Housing A Ponzi Scheme (Guardian)

Rather like pyramid-selling scams, housing markets need a constant stream of fresh-faced hopefuls coming in at the bottom in order to keep delivering big returns at the top. No new buyers equals no more sellers’ market, equals no pressing reason all of a sudden to pay half a million for a four-bedroom modern box in Worcester or a one-bedroom flat in much of London – and what then? No more baby-boomer pensions made of bricks and mortar; no more house that earns more than you do, no piggybank of equity to raid in a crisis.

The chancellor isn’t just hauling more people aboard this financial lifeboat, but thinking about the millions already in it. Suddenly you see why, for this government, subsidising the rents of the poor via housing benefit is deemed to be wasteful and wrong – but subsidising roofs over middle earners’ heads (to the tune of nearly a billion a year through the new Isas by 2020, plus £3.7bn on cheap house loans under the existing help-to-buy scheme), weirdly enough, is not.

But what if all we’re really doing – by accepting crazed property prices as the norm, to be alleviated only by the fiscal equivalent of chucking tenners into a crowd – is sucking first-time buyers into a sort of national Ponzi scheme? What if we’re luring them in at what would otherwise have been the peak, just to keep the boom rolling a little bit longer, and leaving them horribly exposed to negative equity if another crash comes?

No money to bail out Greece, but plenty to bail out bondholders.

• Goebbelnomics – Austerian Duplicity and the Dispensing of Greece (Parenteau)

So let’s get this straight. The Troika does not have enough money to roll over Greek debt (in a Ponzi scheme like fashion, mind you) – debt that was incurred not so much as a bailout of Greece, but more as a bailout of German and other core nation banks and insurance companies and private investors who made stupid loans to or investments in Greece, but refused to fob them off on their own taxpayers. But the Troika does have enough money to adequately perform damage control for the eurozone if Greece, because, you know, Greece is a “dispensable” eurozone member – even though ECB lawyers themselves say there is no legal mechanism for disposing of eurozone members in any such fashion.

See, the square, it is a circle. No money in Greece for humanitarian aid in a country that may be on its way to becoming a failed nation state. No money outside Greece to roll over existing debt, or when necessary to extend and pretend, add more debt on existing debt to service the old debt, Charles Ponzi style. But somehow there is still “sufficient” money to ring fence Greece from the rest of the eurozone once Greece figures out is dispensable and so must exit. Wait, what? Oh, right, the square is a circle. Duplicity? Nah. Not in the eurozone. Not amongst Austerians.

But that is not even the whole deception. It turns out the ECB does happen to have enough money to buy €60 billion per month of bonds from now until at least September 2016. Which means the same bondholders who are benefitting from the misnamed “bailout” funds used to keep the core nation financial institutions from collapsing under the weight of failed loans, can now count on a monthly government handout, courtesy of the ECB. Since the ECB has to bid up the prices of these bonds in order to purchase them from bondholders, this is, for all intents and purposes, a government subsidy payment to bondholders. Bondholders will be receiving free capital gains from their bond sales to the ECB. You will notice there does not appear to be much of a budget constraint on the ECB. Funny, that.

One could not possibly make this stuff up. We are first told there is no more money for Greece, but then in the next breath, we are told there is enough money for ring fencing Greece, should it recognize it has become dispensable (and the sooner the better, it would seem, according to Belgium’s Finance Minister). Then, as if we had not been told there is not enough money for Greece, the ECB commits to creating money out of thin air for the next 18 months to subsidize eurozone bondholders, who will tend to be either the 1%, or to be eurozone financial institutions. Government handouts are apparently available for finanzkapital only, so perhaps we should conclude that unlike Greece, finanzkapital is indispensable.

David is of little faith when it comes to Syriza.

• C’mon Angela, Let Them Greexit (David Stockman)

With each passing day it becomes more obvious that Europe is heading for an epochal financial conflagration. So buy-the-dip if you must, but don’t believe for a minute that the US has decoupled. When the euro and EU eventually implode it will rattle the bones of every gambler and algo left in the casinos anywhere on the planet. Yes, the school yard name calling and roughhousing now going on in Europe makes it appear that behind the sturm und drang there is some negotiations happening. But the truth is there is nothing to negotiate. Greece is so completely and terminally bankrupt that there is no solution other than default and greexit.

To insist that Greece service the entirely of its staggering $350 billion of debt, as does Germany and the troika apparatchiks, is to advocate the extinguishment of democracy in Greece and its reduction to a colonial mandate of Brussels; and in the process, to eliminate any semblance of economic life among the debt serfs who would inhabit it. Its just math. Sooner or later interest rates must normalize. For a country with Greece’s profligate fiscal history, there is no possibility that the interest carry cost on a public debt load equal to 175% of GDP could be any less than 6-7% in the absence of EU guarantees.That means that the Greek state’s annual interest bill would approach 10% of GDP before paying down a single dime of principal. You can’t govern a democracy when one-quarter of revenues are preempted for debt service.

That’s especially the case given the sprawling expanse of the Greek state and the vast dependency of its population on public jobs, pensions and other welfare state entitlements. Indeed, for all the protestations about “austerity” Greece spending ratio to GDP just keeps getting worse. So what Greece’s fiscal equation amounts to is a deathly political food fight over upwards of 60% of GDP which must be funded with nearly an equivalent tax claim on current income – since Greece has no credit in any known financial market absent EMU advances and guarantees. Throw in the diversion of a substantial share of the punishing taxes needed to finance the current commitments of the Greek state to lenders and coupon clippers and you have a non-starter.

Must it come to this? Praise be to Oslo, though.

• Athens Mayor Unveils Scheme To Support Poor With Help From Norway (Kathimerini)

Athens Mayor Giorgos Kaminis, Norwegian Ambassador Sjur Larsen and the president of nongovernmental organization Solidarity Now, Stelios Zavvos, on Wednesday inaugurated a new program to provide support to the Greek capital’s poor. The Solidarity & Social Reintegration scheme comprises a food program benefiting 3,600 households, as well as a space provided by City Hall and managed by Solidarity Now where the organization will provide social, medical and legal aid, among other services. “The aim is the immediate relief of those in need by providing food, medical care, social services, legal support, help finding employment, and support for single-parent families, children and other vulnerable groups,” said Larsen, whose country has donated 95.8% of the €4.3 million needed to fund the program. The other donors are Iceland and Liechtenstein.

Not impossible.

• Does Greece Want To Get ‘Kicked Out’ Of The Eurozone? (CNBC)

With relations between Greece and its European neighbors at an all-time low, and the country’s politicians appearing increasingly defiant in the face of criticism, analysts are questioning whether Greece actually wants to get kicked out of the single currency. Encounters between Greece and the euro zone have become increasingly acrimonious over the last few weeks, as Greece’s commitment to its bailout program and reforms has been questioned. Greece was granted a four-month extension to its aid program in February, but there are concerns over the pace of reforms implemented by the government. Richard Lewis, fund manager at Fidelity Worldwide Investment, told CNBC he believed that Greek Prime Minister Alexis Tsipras wanted a Greek exit from the euro zone.

“My personal view is that the Greek politicians are angling to get kicked out of the euro” he told CNBC Europe’s “Squawk Box” on Thursday, adding that it would be “entirely rational” for the country to want a so-called “Grexit” given its economic situation. However, he highlighted that in order to get his Syriza party elected, Tsipras had to campaign on staying part of the single-currency region. “If they want to leave the euro, which is rational to want to do so, they have to get kicked out. It would involve turmoil, but the alternative is death by a thousand cuts,” he said, referring to Greece’s austerity drive that has been pushed by Greece’s creditors.

Curious.

• Varoufakis Says Predecessor Took IMF Loan Agreement Home (Kathimerini)

Greek Finance Minister Yanis Varoufakis on Thursday told Parliament that his predecessor, Gikas Hardouvelis, had taken a document regarding the country’s loan agreement with the International Monetary Fund home with him after leaving the ministry. Speaking to MPs on Thursday, Varoufakis said that when he asked ministry staff to locate a document regarding the two-month extension of the IMF loan he was told that the letter was among the confidential documents that the former minister had taken with him following his departure. “They told me, and I must emphasize this, that this was an absolutely legal thing to do,” Varoufakis told Parliament.

According to the minister, there were no copies of the original agreement at the ministry and he had to personally contact the IMF in order to ask for one, a procedure which took three-and-a-half days. On Thursday, Varoufakis asked for the drafting of legislation that would put an end to this kind of practice, a move that would “begin to heal the great wounds of the Greek public sector,” he said. Reacting to Varoufakis’s comments, opposition MPs noted that this kind of information was available on the Parliament’s website as well as the government gazette.

There’s some common sense left there somewhere.

• ECB Said To Reject Supervisory Move On Greek Banks Before Talks (Bloomberg)

The ECB rejected a proposal by its supervisory arm to prohibit Greek banks from increasing their holdings of short-term government debt, amid concern that such a move would endanger political negotiations. The Single Supervisory Mechanism, the ECB’s new bank oversight body, wanted to cap Greek banks’ holdings of domestic treasury bills, a key financing source for the cash-strapped government, euro-area officials familiar with the discussions said. While supervisors are concerned about the default risk that the assets carry, the higher-ranking Governing Council sent back the proposal on Wednesday. ECB President Mario Draghi is due to join four-way talks between Greece’s leadership, French President Francois Hollande and German Chancellor Angela Merkel starting in Brussels late Thursday.

Draghi is faced with finding a balance between not deliberately worsening Greece’s financial plight as it struggles to stay in the euro, and not riding roughshod over the rules of his own institution. The SSM, led by Daniele Nouy, has pushed Greece’s banks not to assent to government demands that they buy unlimited treasury bills. In February, the body readied a measure to force lenders to sell assets should a previous round of talks fail. SSM officials are reassessing the measures they can take to protect the banking system, the people said. On Wednesday, the ECB Governing Council approved a small increase in the amount of emergency liquidity assistance that Greece’s central bank can offer.

And must it come to this too?!

• German Couple Pays €875 To Greece For Their Share Of WWII Reparations (RT)

A German couple visiting Greece have handed over a check for €875 to the mayor of the seaport town of Nafplio, saying they wanted to make amends for their government’s attitude for refusing to pay Second World War reparations. Nina Lahge, who works a 30-hour week, and Ludwig Zacaro, who is retired, made the symbolic gesture and explained that the amount of €875 would be the amount one person would owe if Germany’s entire war debt was divided by the population of 80 million Germans. “If we, the 80 million Germans, would have to pay the debts of our country to Greece, everyone would owe €875 euros. In [a] display of solidarity and as a symbolic move we wanted to return this money, the €875 euros, to the Greek population,” they said.

They apologized for not being able to afford to pay for both of them. “We are ashamed of the arrogance, which our country and many of our fellow citizens show towards Greece,” they told local media in Nafplio, southern Greece. The Greek people are not responsible for the fiasco of their previous governments, they believe. “Germany is the one owing to your country the World War II reparation money, part of which is also the forced loan of 1942,” they added. The couple was referring to a loan which the Nazis forced the Greek central bank to give the Third Reich during the WWII thus ruining the occupied country’s economy. The mayor of Nafplio, Dimitris Kotsouros, said the money had been donated to a local charity.

And somehow the BBC manages to squeeze Yats into that story?!

• Tsipras Calls For ‘Bold’ Moves As EU Summit Starts (BBC)

The Greek prime minister has called for “bold initiatives” to reinvigorate his country’s economy as EU leaders gather for a summit in Brussels. Alexis Tsipras is due to hold crucial talks on the sidelines of the summit later with the leaders of Germany, France and the EU institutions. EU leaders are also due to discuss energy security and relations with Russia amid the crisis in Ukraine. Ukraine’s PM has urged the EU to stand firm on sanctions against Moscow. Arseniy Yatsenyuk told the BBC that Russia should pay the price for its actions, and suggested that any attempt to lift EU sanctions for financial reasons would be “disgusting and unacceptable”. The summit is expected to declare that the sanctions should be kept in place until the peace deal agreed in Minsk in February is implemented in full.

The dispute between Greece and its international creditors is not on the formal agenda of the summit. However, correspondents say the meeting is likely to be dominated by the issue. “The European Union needs bold political initiatives that respect both democracy and the treaties, so [as] to leave behind the crisis and to move towards growth,” Mr Tsipras, Greece’s new leftist leader, said as he arrived on Thursday. He is trying to persuade EU leaders that proposed reforms are enough to unlock vital funds, needed to avoid possible bankruptcy and a eurozone exit.

International creditors say they are are ready to extend help on Greece’s €240bn bailout until the end of June. But Mr Tsipras’s plans have met resistance from EU leaders, with Germany among the most critical. European Council President Donald Tusk is to hold a meeting on the issue late on Thursday evening with the leaders of Greece, Germany, France, the European Commission and the ECB, as well as the chairman of eurozone finance ministers. But German Chancellor Angela Merkel told reporters when she arrived at the summit that a breakthrough was unlikely. “Don’t expect a solution,” she said. “Decisions are made in the Eurogroup and that’s how it will remain.”

I think I’ll file this under humor, and not because I don’t get how serious it is.

• Greek Defense Official Seeks Proof In Moscow To Back WWII Claims (Kathimerini)

Alternate Defense Minister Costas Isichos told Russian media that he plans to ask authorities there to allow the Greek state access to archives pertaining to the destruction of infrastructure by Nazi forces during World War II. Speaking to daily Russkaya Gazeta on Wednesday, the first of a four-day visit to Moscow, Isichos said that Greece is looking for evidence to back its demands for World War II reparations from Germany in the archives of allied forces Russia, the United States, Great Britain and France. “There is a chance that relevant documents will be found in the Russian archives,” Isichos said.

“The Greek government is trying to collect similar evidence all over the world in order to strengthen with written proof its demands for war reparations and a return of the forced loan.” Last week Isichos said he had received a large collection of Wehrmacht documents from the US. “These documents do not just substantiate a historic truth – they are the documents of the Wehrmacht itself, the occupation forces,” said Isichos. “They are diaries, reports by officers to their superiors… these were not written for publicity, they were mainly secret documents.” In response to successive Greek demands, Berlin has repeated that the issue of war reparations has long been settled and refuses to further discuss the issue.

Thanks to Dijsselbloem…

• Greek Bank Deposits Outflow Spikes On Statements And Fears (Kathimerini)

Greek banks are suffering from fresh turbulence due to the tension and the apparent collision course between Athens and its creditors. Bank stocks gave up more than 8% of their value on Wednesday, while the outflow of deposits was far greater than on previous days. Credit sector officials estimated that the flight of deposits yesterday alone amounted to €350-400 million, which was some five times higher than the daily average in previous days. They added that Wednesday’s withdrawals totaled the most since an agreement was reached at the February 20 Eurogroup meeting. This followed Tuesday’s statement by Eurogroup chief Jeroen Dijsselbloem regarding the possibility of imposing capital controls in Greece.

There was also a flurry of statements from Greek and European officials that aggravated the climate between the two sides, a phenomenon that continued on Wednesday. In this context banks are worried about a new surge of withdrawals while the credit system is at a marginal point and with the European Central Bank only supplying liquidity drop by drop. On Thursday the governing council of the ECB is expected to renew the financing of Greek lenders through the Bank of Greece’s emergency liquidity assistance (ELA) mechanism and will probably increase the limit of funding that now stands at €69.4 billion euros.

The increase will again be small, just as was the case at the last few meetings of the ECB board, aimed only at covering necessary cash needs. Deposits and the credit system have taken a big blow in the last few months due to the political and economic uncertainty as well as the absence of any progress toward finding a solution to the standoff between Greece and its creditors. Banks estimate that the deposits of households and enterprises have declined by as much as €26 billion since the end of November, and today amount to no more than €138 billion.

“The point is that there is always at least one alternative investment with a minimum positive value for all asset backed currencies and thus must always have positive nominal rates.”

• We Must Rethink Risk, Cost of Capital, Currency and the Economy (Beversdorf)

Let’s think about risk, cost of capital and interest rates. The idea is that the price of risk is built into interest rates. Now we discussed that major economy Sovereign debt like Euro or USD Notes are considered risk free debt. And so interest rates represent a cost of capital only. If those Notes are paying negative interest rates it suggests that the cost of capital, which is just the opportunity cost of that money, is negative. Meaning if I didn’t lend this money to a borrower the next best return I could get on this money is actually a loss. If we look at Corporate paper like Nestle borrowing at negative rates, this actually suggests that the opportunity cost (or next best return) for the lender is a loss so great that it actually offsets all of the risk represented by the the borrower because we know that risk requires positive interest be paid.

This tells us that the economy is severely broken in Europe. For in stable economies we have positive return opportunities. None of this is arbitrary. It means in order to get investors into Sovereign debt you need to pay them in accordance with other similar investments. When economies are strong there are lots of similar investments that are paying higher and higher returns. Meaning Treasuries/Sovereigns need to increase rates to compete for capital. This has a natural balancing effect that prevents an overheating of an economy. However, when the economy is bad there are very few, and currently it would seem in Europe, no similar investments that are paying even a positive return. Meaning Euro ‘Treasuries’ can offer negative rates and still get investors. As rates increase so does demand for that currency increase and results in a strengthening of that currency.

Alternatively, when interest rates move lower and further negative a fiat currency sees less and less demand thus weakening that currency, as has been the case with the Euro. This is how rates, the economy and currency strength are tied together. What this means is that if an economy continues to decline a fiat currency’s purchasing power valuation can actually move to absolute zero (meaning it is worthless) and that rate of moving to zero is going to be your negative interest rate. It would get to zero when an economy shows no possibility of a positive return investment. What we find is that with asset backed currencies this actually cannot happen. Because an asset backed currency actually derives its value, or at least its minimum value, based on the underlying asset and so it isn’t dependent on the respective economy.

It has a minimum purchasing power valuation equal to the cost to produce or extract the underlying asset. Because that will always be a positive figure you could never see negative interest rates with an asset backed currency. It is an impossibility, which until recently most would have agreed was the case for even fiat currencies. The point is that there is always at least one alternative investment with a minimum positive value for all asset backed currencies and thus must always have positive nominal rates. This is the biggest and most fundamental difference between fiat and asset backed currencies.

The bottomless bribes pit. When will Rousseff be arrested?

• Switzerland Freezes $400 Million Amid Petrobras Laundering Probe (Bloomberg)

Switzerland has frozen $400 million of assets in more than 30 banks as the country’s attorney general probes money laundering related to Petroleo Brasileiro SA’s widening corruption scandal. Nine investigations have been opened since last April based on allegations of corruption involving eight Brazilian citizens, the Bern-based Federal Prosecutors’ Office said in an e-mailed statement on Wednesday. More than $120 million of those frozen funds were released for repatriation to Brazil, it said. “The Swiss criminal proceedings will continue with the aim of holding the perpetrators accountable and establishing the origin of the remaining frozen assets,” the Federal Prosecutors’ Office said in the statement.

Petrobras is mired in a corruption scandal in which company executives allegedly directed hundreds of millions of dollars from overpriced contracts to politicians. Disagreement about the corruption writedown led to the departure of the state-owned company’s Chief Executive Officer Maria das Gracas Foster. More than 1 million Brazilians demonstrated on Sunday against corruption and President Dilma Rousseff. The beneficial owners of more than 300 Swiss bank accounts used to process bribery payments include senior executives at Petrobras, according to the Federal Prosecutors’ Office, which is handling requests for legal assistance from Brazil and The Netherlands.

Swiss Attorney General Michael Lauber held talks with his Brazilian counterpart Rodrigo Janot in Brasilia on the prospects of working together to resolve the scandal, according to the statement. Switzerland updated its anti-money laundering legislation at the end of 2014 to reflect international standards. Its Money Laundering Reporting Office is a member of the Egmont Group of nations that share information to combat illicit financial transactions. “The Brazilian bribery scandal affects Switzerland’s financial center and its anti-money-laundering strategy,” the Federal Prosecutors’ Office said. The office “has a close interest in contributing fully to the resolution of the scandal through its own investigations,” it said.

And here’s the result of the Petrobras culture.

• Economic Downturn Pushes Brazilians Into Informal Economy (Reuters)

Mounting job losses are pushing more and more Brazilians into the informal economy as self-employed workers, leaving them vulnerable to what could be the country’s worst recession in 25 years. Tens of thousands of people who lost full-time jobs are now freelancing as bricklayers, truck drivers and maids to make ends meet as they look for increasingly scarce jobs. In the process, they often lose access to welfare benefits and face greater credit restrictions. Self-employed workers, most of them earning no more than about $450 a month, now represent 19.5% of employees in Brazil’s main cities – the highest level in eight years and up from 17.5% in 2012, according to official data for January.

The quest of people like José Lúcio da Silva, 55, illustrates how Brazil’s economy and labor market have over the last two years lost the vigor of the previous decade. “The boss said things were slowing and then he fired us,” said Silva, who had a formal job as a sealant installer at building sites in Brasilia for nearly 30 years. He is only five years away from retirement, provided he finds another full-time “registered” job with benefits. “You can’t find a freelance job every day. You can take a few of them here and there, but sometimes these jobs take a while to appear,” he added.

The loss of secure jobs is a blow to an already weak economy and to President Dilma Rousseff, who won re-election in October thanks in large part to low unemployment. Since then, her popularity has plunged with 62% of people in a new poll saying her government was “bad” or “terrible” Although recent data does not offer a breakdown by income or education, surveys show the typical self-employed worker in Brazil is a middle-aged, low-paid male household head. More than half work at farms, building sites and in commerce, either hawking goods on the streets or as door-to-door salespeople.

And that’s just the start.

• Iran Could Add Million More Barrels a Day to the Oil Glut (Bloomberg)

Iran says it could add a million barrels to daily oil production shortly after a deal to lift sanctions, reclaiming the position of OPEC’s second-largest supplier. While such a boost would take months because sanctions may be rolled back slowly, industry observers agree the capacity is there. Going further than that and adding a second million barrels – as the government has said it plans to do – will prove a much bigger challenge. It would take some five years and tens of billions of dollars of investment, according to two former oil-industry executives who worked in the country. “The number one need is investment,” said Mohsen Shoar, an analyst with Continental Energy. “To get anywhere beyond 4 million barrels a day” will require foreign assistance, he said by phone.

Iran is seeking a final agreement with international powers by June that would curb its nuclear program in exchange for phasing out sanctions that have cut its crude exports, choked cash flow and halted most oil investment. The country produced 2.8 million barrels of oil a day last month, compared with 3.6 million at the end of 2011, according to data compiled by Bloomberg. Oil Minister Bijan Namdar Zanganeh said March 16 that the Persian Gulf nation would be able to raise production by a million barrels a day, bringing it to 3.8 million, “within a few months,” placing it behind only Saudi Arabia in the OPEC. Once the restrictions are eased – a process that itself could take many months – Iran would need to seek foreign partners to boost output beyond pre-sanctions levels, said Robin Mills at Manaar Energy Consulting.

The lower prices fall, the more they have to try to produce and sell.

• Kuwaiti Oil Minister: We ‘Have No Choice’ On Output (CNBC)

Oil prices fell once again Thursday, after a minister from OPEC said the group did not have a choice with regards to cutting oil production because it did not want to lose its global market share. Speaking to reporters in Kuwait City, Ali al-Omair, the Kuwaiti oil minister, said the dramatic drop in the price of oil would affect the country’s revenues and its fiscal budget for the year, Reuters reported Thursday. “Within OPEC we don’t have any other choice than keeping the ceiling of production as it is because we don’t want to lose our share in the market,” he said Thursday morning, according to the news agency. “If there is any type of arrangement with (countries) outside OPEC, we will be very happy.”

Weak global demand and booming U.S. shale oil production are seen as two key reasons behind the price plunge, as well as OPEC’s reluctance to cut its output. OPEC is next due to meet in June, when it will decide on its output policy after deciding to keep its production steady at the end of 2014. Rumors of an unscheduled meeting in January were quashed by United Arab Emirates Oil Minister, Suhail bin Mohammed al-Mazroui, who said he was adamant the strategy would not change. The group produces about 40% of the world’s crude oil. Prices have slumped around 60% since last June and tipped lower again on Thursday morning after a volatile week. The drop was compounded by a larger-than-expected build up in U.S. crude inventories, according to new data on Wednesday.

“Yatsenyuk is even less popular with less than a quarter of those surveyed believing he is doing a good job.”

• Poll Shows Majority of Ukrainians Unhappy With Their Government (RT)

A recent poll by a Ukrainian research group shows how unhappy the country is with their politicians. Only 8% say the country is going in the right direction, while almost two-thirds assert they don’t approve of the president’s actions. The figures should make for worrying viewing for President Petro Poroshenko and his government as Ukraine is currently mired in economic turmoil and political instability. A poll carried out by the Kiev-based Research & Branding Group from March 6-16, shows just how fed-up Ukrainians are with the way their country is being run. Poroshenko may have been in power for just over nine months, but it would appear his ‘honeymoon’ period has well and truly ended.

Just a third of those asked believe he is doing a good job, while almost 60% say they aren’t happy with the way the billionaire is running the country. If elections were carried out today, just under 20% of Ukrainians would back Poroshenko, while 30% would either vote against every candidate or not bother going to the polls. However, Poroshenko seems to be getting off lightly. Ukraine’s nationalist Prime Minister Arseny Yatsenyuk is even less popular with less than a quarter of those surveyed believing he is doing a good job in helping to run the country.

The Ukrainian media has repeatedly been reporting stories of how thousands of Russian troops are supposed to be helping anti-government militia’s in the east of the country in their fight against Ukrainian government forces. But the vast majority of those asked think their media and the stories they produce are untrustworthy, with almost 60% not believing the stories published and broadcast by the Ukrainian press. The most damaging statistics for the Ukrainian government show that a meager 8% say they are happy with the direction their country is taking and only 5% say Ukraine is politically stable.

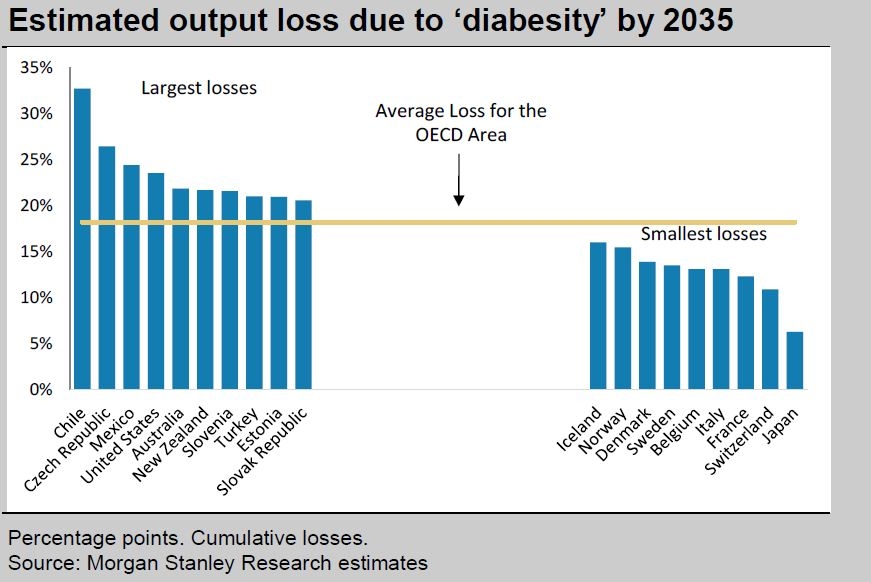

Diabesity.

• Here’s How Much Sugar Consumption Is Hurting the Global Economy (Bloomberg)

Sugar may not be so sweet when it comes to its effects on the world economy. That’s the conclusion of Morgan Stanley analysts in a new research report. They say that because health is a key driver of economic growth, rising diabetes and obesity rates cloud the outlook in both emerging markets and developed economies. Sugar consumption is one major culprit behind such health problems — making it a liability for global output. Taking into account reduced productivity caused by diabetes and obesity, the Morgan Stanley team, led by economist Elga Bartsch in London, finds that gross domestic product growth will average 1.8% annually over the next 20 years across nations in the OECD. That’s below OECD long-term forecasts for 2.3% growth.

In the same period, the cumulative loss from sugar’s not-so-sweet effects totals 18.2 percentage points. Chile, the Czech Republic, Mexico, the U.S. and Australia stand to see the worst sweet-tooth-spurred GDP drag. Japan, Korea, Switzerland, France, Italy and Belgium are looking at smaller output losses from what some call “diabesity.” Morgan Stanley finds that productivity growth in the OECD region drops to 1.5% annually over the coming decades when taking into account the sugar-related drag. That compares with the group’s forecast of 1.9% yearly growth.

The outlook for averting sugar-caused economic harm is dim. While there’s “burgeoning evidence” that sugar consumption is starting to decline in developed markets, it’s on the rise in emerging economies, driven by trends such as wider and cheaper availability of sugar-laden goods, as well as a rising preference for the sweet stuff. Sugar consumption rates are expected to continue dropping in North America and Europe as the population ages, yet Africa, Central America and Latin America are projected to increasingly demand the sweetener, based on the Morgan Stanley simulations. Asia shows a mixed pattern: If only for aging trends, sugar consumption would drop, yet an ongoing shift to a higher-sugar diet could push up consumption.

Your own personal Jesus.

• Revealed: Gates Foundation’s $1.4 Billion In Fossil Fuel Investments (Guardian)

The charity run by Bill and Melinda Gates, who say the threat of climate change is so serious that immediate action is needed, held at least $1.4bn (£1bn) of investments in the world’s biggest fossil fuel companies, according to a Guardian analysis of the charity’s most recent tax filing in 2013. The companies include BP, responsible for the Deepwater Horizon disaster, Anadarko Petroleum, which was recently forced to pay a $5bn environmental clean-up charge and Brazilian mining company Vale, voted the corporation with most “contempt for the environment and human rights” in the world clocking over 25,000 votes in the Public Eye annual awards.

The Bill and Melinda Gates Foundation and Asset Trust is the world’s largest charitable foundation, with an endowment of over $43bn, and has already given out $33bn in grants to health programmes around the world, including one that helped rid India of polio in 2014. A Guardian campaign, launched on Monday and already backed by over 95,000 people is asking the Gates to sell their fossil fuel investments. It argues: “Your organisation has made a huge contribution to human progress … yet your investments in fossil fuels are putting this progress at great risk. It is morally and financially misguided to invest in companies dedicated to finding and burning more oil, gas and coal.”

Existing fossil fuel reserves are several times greater than can be burned if the world’s governments are to fulfil their pledge to keep global warming below the danger limit of 2C, but fossil fuel companies continue to spend billions on exploration. In addition to the climate risk, the Bank of England and others argue that fossil fuel assets may pose a “huge risk” to pension funds and other investors as they could be rendered worthless by action to slash carbon emissions. [..] In their annual letter in January, Bill and Melinda Gates wrote: “The long-term threat [of climate change] is so serious that the world needs to move much more aggressively – right now – to develop energy sources that are cheaper, can deliver on demand, and emit zero carbon dioxide.”

Yeah, that’ll work: a voluntary new corporate model.

• Justice, Capitalism And Progress: Paul Tudor Jones II (TED)

Can capital be just? As a firm believer in capitalism and the free market, Paul Tudor Jones II believes that it can be. Jones is the founder of the Tudor Investment Corporation and the Tudor Group, which trade in the fixed-income, equity, currency and commodity markets. He thinks it is time to expand the “narrow definitions of capitalism” that threaten the underpinnings of our society and develop a new model for corporate profit that includes justness and responsibility. It’s a good time for companies: in the US, corporate revenues are at their highest point in 40 years. The problem, Jones points out, is that as profit margins grow, so does income inequality.

And income inequality is closely linked to lower life expectancy, literacy and math proficiency, infant mortality, homicides, imprisonment, teenage births, trust among ourselves, obesity, and, finally, social mobility. In these measures, the US is off the charts. “This gap between the 1% and the rest of America, and between the US and the rest of the world, cannot and will not persist,” says the investor. “Historically, these kinds of gaps get closed in one of three ways: by revolution, higher taxes or wars. None are on my bucket list.” Jones proposes a fourth way: just corporate behavior. He formed Just Capital, a not-for-profit that aims to increase justness in companies. It all starts with defining “justness” — to do this, he is asking the public for input.

As it stands, there is no universal standard monitoring company behavior. Tudor and his team will conduct annual national surveys in the US, polling individuals on their top priorities, be it job creation, inventing healthy products or being eco-friendly. Just Capital will release these results annually – keep an eye out for the first survey results this September. Ultimately, Jones hopes, the free market will take hold and reward the companies that are the most just. “Capitalism has driven just about every great innovation that has made our world a more prosperous, comfortable and inspiring place to live. But capitalism has to be based on justice and morality…and never more so than today with economic divisions large and growing.”

“A recent study found that Arctic sea ice had thinned by 65% between 1975 and 2012.”

• Arctic Winter Sea Ice Extent Lowest On Record (BBC)

Sea ice in the Arctic Ocean has fallen to the lowest recorded level for the winter season, according to US scientists. The maximum this year was 14.5 million sq km, said the National Snow and Ice Data Center at the University of Colorado in Boulder. This is the lowest since 1979, when satellite records began. A recent study found that Arctic sea ice had thinned by 65% between 1975 and 2012. Bob Ward of the Grantham Research Institute on Climate Change and the Environment at the London School of Economics said: “The gradual disappearance of ice is having profound consequences for people, animals and plants in the polar regions, as well as around the world, through sea level rise.”

The National Snow and Ice Data Center (NSIDC) said the maximum level of sea ice for winter was reached this year on 25 February and the ice was now beginning to melt as the Arctic moved into spring. The amount measured at the end of February is 130,000 sq km below the previous record winter low, measured in 2011. An unusually warm February in parts of Alaska and Russia may have contributed to the dwindling sea ice, scientists believe. Researchers will provide the monthly average data for March in early April, which is viewed as a better indicator of climate effects. NSIDC scientist Walt Meier said: “The amount of ice at the maximum is a function of not only the state of the climate but also ephemeral and often local weather conditions. “The monthly value smoothes out these weather effects and so is a better reflection of climate effects.”

Home › Forums › Debt Rattle March 20 2015