Jack Delano Foggy night in New Bedford, Massachusetts 1941

“This year, for the first time in more than 30 years, US productivity growth will almost certainly turn negative..”

“Unless we become smarter at how we work, growth will start to exhaust itself too.” Er, no, that has already happened.

“For the first time the next generation of US workers will be less educated than the previous..”

• The Mystery of Weak US Productivity (Luce)

Look around you. From your drone home delivery to that oncoming driverless car, change seems to be accelerating. Warren Buffett, the great investor, promises that our children’s generation will be the “luckiest crop in history”. Everywhere the world is speeding up except, that is, in the productivity numbers. This year, for the first time in more than 30 years, US productivity growth will almost certainly turn negative following a decade of sharp slowdown. Yet our Fitbits seem to be telling us otherwise. Which should we trust — the economic statistics or our own lying eyes? A lot hinges on the answer. Productivity is the ultimate test of our ability to create wealth. In the short term you can boost growth by working longer hours, for example, or importing more people.

Or you could lift the retirement age. After a while these options lose steam. Unless we become smarter at how we work, growth will start to exhaust itself too. Other measures bear out the pessimists. At just over 2%, US trend growth is barely half the level it was a generation ago. As Paul Krugman put it: “Productivity isn’t everything, but in the long run it is almost everything.” It is possible we are simply mismeasuring things. Some economists believe the statistics fail to capture the utility of setting up a Facebook profile, for example, or downloading free information from Wikipedia. The gig economy has yet to be properly valued. Yet this argument cuts both ways. Productivity is calculated by dividing the value of what we produce by how many hours we work — data provided by employers.

But recent studies — and common sense — say our iPhones chain us to our employers even when we are at leisure. We may thus be exaggerating productivity growth by undercounting how much we work. The latter certainly fits with the experience of most of the US labour force. It is no coincidence that since 2004 a majority of Americans began to tell pollsters they expected their children to be worse off — the same year in which the internet-fuelled productivity leaps of the 1990s started to vanish. Most Americans have suffered from indifferent or declining wages in the past 15 years or so. A college graduate’s starting salary today is in real terms well below where it was in 2000. For the first time the next generation of US workers will be less educated than the previous, according to the OECD, which means worse is probably yet to come. Last week’s US productivity report bears that out.

“All the risks are accumulating in an overcrowded financial system.”

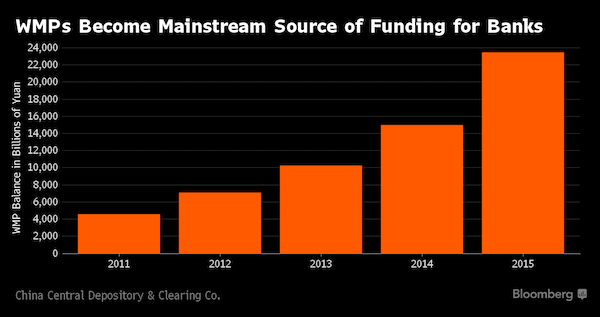

• China Default Chain Reaction Threatens Products Worth 35% of GDP (BBG)

The risk of a default chain reaction is looming over the $3.6 trillion market for wealth management products in China. WMPs, which traditionally funneled money from Chinese individuals into assets from corporate bonds to stocks and derivatives, are now increasingly investing in each other. Such holdings may have swelled to as much as 2.6 trillion yuan ($396 billion) last year, based on estimates from Autonomous Research this month. The trend has China watchers worried. For starters, it means that bad investments by one WMP could infect others, causing a loss of confidence in products that play an important role in bank funding. It also suggests WMPs are struggling to find enough good assets to meet their return targets.

In the event of widespread losses, cross-ownership will create more uncertainty over who’s vulnerable – a key source of panic in 2008 when soured U.S. mortgage securities triggered a global financial crisis. Those concerns have become more pressing this year after at least 10 Chinese companies defaulted on onshore bonds, the Shanghai Composite Index sank 20% and China’s economy showed few signs of recovery from the weakest expansion in a quarter century. “There’s abundant liquidity in the financial system, but a scarcity of high-yielding assets to invest in,” said Harrison Hu, the chief Greater China economist at RBS in Singapore. “All the risks are accumulating in an overcrowded financial system.”

Issuance of WMPs, which are sold by banks but often reside off their balance sheets, exploded over the past three years as lenders competed for funds and fees while savers sought returns above those offered on deposits. The products, which offer varying levels of explicit guarantees, are regarded by many as having the implicit backing of banks or local governments. The outstanding value of WMPs rose to 23.5 trillion yuan, or 35% of China’s gross domestic product, at the end of 2015 from 7.1 trillion yuan three years earlier, according to China Central Depository & Clearing Co. An average 3,500 WMPs were issued every week last year, with some mid-tier banks, such as China Merchants Bank and China Everbright Bank, especially dependent on the products for funding.

Interbank holdings of WMPs swelled to 3 trillion yuan as of December from 496 billion yuan a year earlier, according to figures released by the clearing agency last month. As much as 85% of those products may have been bought by other WMPs, according to Autonomous Research, which based its estimate on lenders’ public disclosures and data on interbank transactions. The firm speculates that in some cases the products are being “churned” to generate fees for banks. “We’re starting to see layers of liabilities built upon the same underlying assets, much like we did with subprime asset-backed securities, collateralized debt obligations, and CDOs-squared in the U.S.,” Charlene Chu, a partner at Autonomous who rose to prominence in her former role at Fitch Ratings by warning of the risks of bad debt in China, said in an interview on May 17.

“The unconsolidated structured entities managed by the Group consist primarily of collective investment vehicles (“WMP Vehicles”) formed to issue and distribute wealth management products (“WMPs”), which are not subject to any guarantee by the Group of the principal invested or interest to be paid.”

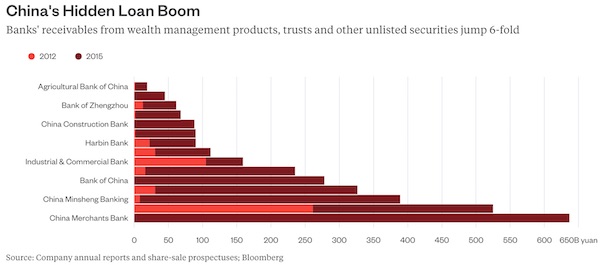

• China’s Veiled Loans May Prove Lethal (BBG)

Credit is a risky business, but loans that dare not speak their name? They are possibly even more dangerous, as China is about to find out.As many as 15 publicly traded Chinese lenders, large and small, report roughly $500 billion of such debt between them, which they hold not as loans but as receivables from shadow banking products. While the traditional credit business of these banks is 16 times bigger, receivables have jumped sixfold in three years. Explosive growth of this type usually ends badly. It’s hard to see why it’ll be different for the People’s Republic. Before they can brace themselves – or embrace the risk, if they think the rewards are worth it – equity investors need to know where to look. Flitting from one explanatory note to another in dense annual reports isn’t everybody’s idea of a day well spent.

But the effort may be worth it. For instance, page 184 of Agricultural Bank’s 2015 annual report informs us that the bank has 557 billion yuan ($85 billion) worth of assets tied in “debt instruments classified as receivables.” On page 245, we further learn that most of this is old hat, and the only fast-growing portion is an 18.7 billion yuan chunk helpfully titled as “Others.” A footnote adds that the category primarily consists of “unconsolidated structured entities managed by the group.” Give up? Then you miss the big reveal that occurs 34 pages later: “The unconsolidated structured entities managed by the Group consist primarily of collective investment vehicles (“WMP Vehicles”) formed to issue and distribute wealth management products (“WMPs”), which are not subject to any guarantee by the Group of the principal invested or interest to be paid.” That’s broadly how Chinese lenders disclose their cryptic linkages with shadow banks.

The names keep changing, from “investment management products under trust scheme” and “investment management products managed by securities companies” to “trust beneficiary rights” and “wealth management products.” The latter have swelled to the equivalent of 35% of GDP, and account for 3 trillion yuan of interbank holdings. The common thread to these products is that they’re all exposed to corporate credit and designed to get around lenders’ minimum capital requirements and maximum loan-to-deposit norms, with scant loss provisioning in case things go wrong.There’s plenty that could. The reported nonperforming loan ratio of 1.75% is a joke. CLSA says bad loans have already snowballed to 15 to 19% of the loan book; Autonomous Research partner Charlene Chu estimates the figure will reach 22% by the end of this year. A 20% loss on a $500 billion portfolio of loans masquerading as receivables would wipe out 58% of annual profit of the 15 banks under our scanner.

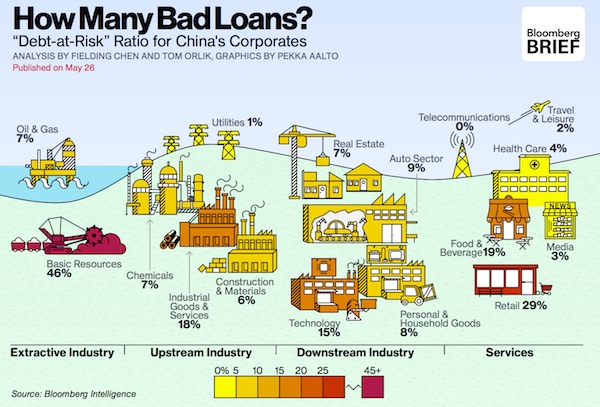

” In the basic resources sector, 46% of loans are with firms without enough income to cover interest payments. ”

• How Many Bad Loans Might China Have? (BBG)

How many of China’s loans could turn bad? The official data show a non-performing loan ratio of 1.75%, but that’s widely believed to reflect optimistic accounting. Bloomberg Intelligence Economics has estimated the %age of “at risk” loans – those where the borrower doesn’t have sufficient earnings to cover interest payments. The results show 14% of corporate borrowing at risk of default, up from a low of 5% in 2010. By sector, the basic resources, retail and industrial sectors are among the highest risk. In the basic resources sector, 46% of loans are with firms without enough income to cover interest payments.

Telecommunications, utilities, and travel and leisure sectors look more secure, reflecting stronger earnings and lower debt. The methodology is based on an approach used by the IMF. For a universe of 2,865 Chinese listed firms (excluding financial companies), we screened for firms with interest costs higher than their EBITDA. We then calculated total debt of those firms as a %age of total debt of all listed firms. We assume that the ratio of “at risk” loans for the corporate sector as a whole is the same as for listed companies.

“..over-investment produces slow growth and falling prices while ever-more-aggressive monetary policy distorts markets beyond recognition and encourages new over-investment in different sectors, which then proceed to follow oil and steel into the deflationary abyss.”

• Easy Money = Overcapacity = Trade Wars = Deflation (Rubino)

So what happens to all that Chinese steel that was on its way to the US and EU before slamming into those prohibitively high tariffs? One of three things: Either it’s sold elsewhere, probably at even steeper discounts, thus pricing US and EU steel exports out of those markets. Or it’s stockpiled in China for future use, thus lowering future demand for new steel production and, other things being equal, depressing tomorrow’s prices. Or many of China’s newly-built steel mills will close, and China will eat the losses related to this malinvestment. Each scenario results in lower prices and financial losses somewhere. Put another way, as far as steel is concerned, the world’s fiat currencies are rising in value, which is the common definition of deflation.

And since steel is just one of many basic industries burdened with massive overcapacity, it’s safe to assume that the process which began with oil and recently spread to steel will continue to metastasize throughout the developed and developing worlds. Next up: real estate. “Modern” monetary policy, designed to achieve exactly the opposite outcome (that is, rising prices for real things), will in response be ratcheted up to ever-more-extreme levels — which in this analytical framework is like trying to douse a fire with gasoline. The result is a world in which past over-investment produces slow growth and falling prices while ever-more-aggressive monetary policy distorts markets beyond recognition and encourages new over-investment in different sectors, which then proceed to follow oil and steel into the deflationary abyss. And so on, until the system collapses under the weight of its own absurdity.

Because they are deflationary.

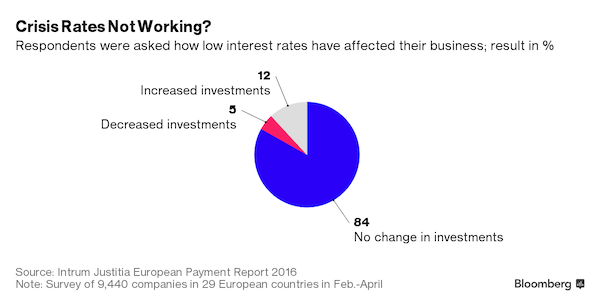

• Negative Rates Fail to Spur Investment for Corporate Europe (BBG)

A prolonged period of negative interest rates is failing to revive investment at Europe’s companies, with the vast majority of businesses in the region saying the stimulus measures have had no affect at all on their growth plans. Some 84% of the 9,440 companies surveyed by Swedish debt collector Intrum Justitia AB for its European Payment Report 2016 say low interest rates haven’t affected their willingness to invest. And perhaps more alarmingly, the number is up from 73% last year. “Creating economic growth requires stability and optimism,” Intrum Justitia Chief Executive Officer Mikael Ericson said in the report. “Evidently, the strategy of keeping interest rates record low for more than a year has not created the much sought-after stability.”

Signs of stalling investment mark a blow to central banks hoping to revive growth across Europe through negative rates and quantitative easing. Europe needs its businesses to invest more if it’s to create the jobs needed to spur growth. In the euro area, where interest rates have been negative since mid-2014, gross domestic product will slow to 1.6% this year, compared with 2.3% in the U.S., the European Commission estimates. “A calculation of an investment includes assumptions of the future,” Intrum said. “To get the calculation to go together those assumptions need to include a belief in stability and prosperity in that future. Perhaps the negative interest rates do not signal that stability at all – rather that we are still in an extraordinary situation?”

The survey also identified another threat to growth, namely late payments. Some 33% of survey participants said they regard not being paid on time as a threat to overall survival while 25% said they are likely to cut jobs if clients pay late or not at all. That problem is more pronounced among Europe’s 20 million small and medium-sized companies, with many reporting that bigger firms are forcing them to accept late payments. “It is a market failure that costs job opportunities for millions of Europeans that big corporations deliberately force SMEs to finance their cash flow,” Ericson said. “As much as two out of five SMEs say late payments prohibit growth of the company. That large corporations use their much smaller sub-suppliers to act as financier of their own cash-management processes is not only wrong, it also creates an imbalance in society.”

Might as well devalue now.

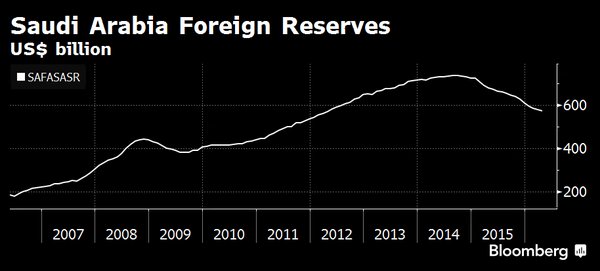

• Saudi Arabia’s Petrodollar Reserves Fall to 4-Year Low (BBG)

Saudi Arabia’s net foreign assets fell for a 15th month in April, as the kingdom announced its “vision” for a post-oil future. The Saudi Arabian Monetary Agency said on Sunday net foreign assets declined 1.1% to $572 billion, the lowest level in four years. The slump in crude prices has forced the government to sell bonds and draw on its currency reserves, still among the world’s largest. Net foreign assets fell by $115 billion last year, when the kingdom ran a budget deficit of nearly $100 billion.

The fiscal crunch has pushed Saudi Arabia’s rulers to look beyond oil, consider new taxes, and plan an initial public offering of state giant Saudi Arabian Oil Co. Deputy Crown Prince Mohammed bin Salman sketched out the planned changes dubbed Saudi Vision 2030 on April 25. The strain on reserves has also fueled speculation that the kingdom will adjust its decades-old riyal peg to the dollar. New central bank Governor Ahmed Alkholifey told Al-Arabiya on Thursday that Saudi Arabia doesn’t plan to change its exchange rate policy.

Firesale. Given what’s happened in commodities the past year, not surprising.

• CEO of No. 1 Asian Commodity Trader Noble Group Resigns In Surprise Move (R.)

Embattled commodity trader Noble Group announced the surprise resignation of CEO Yusuf Alireza on Monday and said it planned to sell a U.S. unit to bolster its balance sheet as it seeks to regain investor confidence. Alireza, a former Goldman Sachs banker had steered Asia’s biggest commodity trader to sell assets, cut business lines and take big writedowns as it battled weak commodity markets and the fallout from an accounting dispute. “With this transformation process now largely complete, Mr. Alireza considered that the time was right for him to move on,” Noble said in a statement. It appointed senior executives William Randall and Jeff Frase as co-chief executive officers and said it would begin a sale process for Noble Americas Energy Solutions, “expected to generate both significant cash proceeds and profits to substantially enhance the balance sheet.”

Noble came under the spotlight in February last year when it was accused by Iceberg Research of overstating its assets by billions of dollars, claims which Noble rejected. Its shares have since plunged by about 75% and its debt costs have risen as the company has been hit hard by credit rating downgrades and weak investor confidence. “The first task is to stabilize the situation and convey stability and continuity,” said Nirgunan Tiruchelvam at Religare Capital Markets. “That would be the immediate task of somebody in this business which has volatility,” he said. Noble won the backing of banks earlier this month to refinance its debt. In February, Noble reported its first annual loss since 1998, battered by a $1.2 billion writedown for weak coal prices. The company’s shares slumped 65% last year, knocking it out of the benchmark Straits Times index.

So a delay in the tax hike would trigger elections. And Abe counts on the Japanese to be blind enough to re-elect him.

• Japan Must Delay Sales-Tax Rise to Recover, Abe Aide Says (BBG)

Japan needs to delay increasing its sales tax until late 2019 to sustain its economic recovery, an aide to Prime Minister Shinzo Abe said Sunday. There is a possibility that such a move could trigger a general election. The government will probably hold off raising the tax because it needs to give priority to economic growth, Abe aide Hakubun Shimomura said on Fuji television. Japan’s lower house of parliament would need to be dissolved for a general election if the planned increase is delayed again, Finance Minister Taro Aso was cited by Kyodo News as saying on Sunday at a meeting of the ruling party’s members. Abe has said he’ll make a decision before an upper-house election this summer on whether to go ahead with a planned increase in the levy next April to 10%, from 8% at present.

He had previously said the matter would be decided at an appropriate time and that it would be postponed only if there was a shock on the scale of a major earthquake or a corporate collapse like that of Lehman Brothers. An increase in the levy in 2014 pushed Japan into a recession. “We have no other options but to postpone the sales-tax increase,” Shimomura said. “If the increase means a decline in tax revenue for the government, that would threaten the achievement of the goals under Abenomics.” The prime minister told Finance Minister Taro Aso and LDP’s Secretary General Sadakazu Tanigaki on Saturday to delay the sales-tax increase to October 2019, NHK reported.

Aso advised the prime minister to be cautious about the idea, NHK said. “If the tax increase is delayed, a general election is needed to put the plan to the public,” Aso was quoted by Kyodo News as saying on Sunday. Kyodo reported later that Abe doesn’t plan to call snap elections on the same day as the Upper House vote. If Abe fails to go ahead with his plan of raising the tax in April, it means his economic policies have failed and he and his cabinet members should resign to take responsibility, Tetsuro Fukuyama, vice secretary general of the opposition Democratic Party of Japan, said in a program aired by public broadcaster NHK on Sunday.

Unexpected advantages.

• The Butterfly Effect: Cheap Oil Means Fewer Nose Jobs (BBG)

Oil slumps. Middle Eastern patients cancel treatments abroad. Thai hospital stocks slide. It’s the butterfly effect in action. Weak growth outlooks in the Gulf states are prompting greater competition from local clinics, stemming the flow of visitors to the world’s top medical tourism destination. That’s clouding the outlook for Thailand’s health-care shares, which surged more than 800% over the past seven years, as valuations start to look stretched amid the falling demand. Bangkok’s Bumrungrad Hospital, known as the grandaddy of international clinics, has slumped 16% since early March after patient volumes from the United Arab Emirates, its second-biggest source of overseas visitors, fell 20% in the first quarter.

Thailand attracted as many as 1.8 million international patients in 2015, many of whom stayed on afterward for a beach holiday. More than one in three foreigners treated at Bumrungrad are from the Gulf states and Kasikorn Securities says declining growth in the region and a rise in competition from clinics in the U.A.E., where the government is encouraging its citizens to stay home for medical care, are curbing demand. “In the short term, the economic slowdown in the the Middle East will weaken some investors’ confidence on earnings growth for domestic hospital operators,” said Jintana Mekintharanggur at Manulife Asset Management. “We are still bullish on the sector” in the long term as it will benefit from growth in countries like Myanmar and Vietnam that have less-developed health systems, she said.

Hey, look, we are born as liars. And we will lie to ourselves about that, too.

• The Source of Failure: We Optimize What We Measure (CH Smith)

The problems we face cannot be fixed with policy tweaks and minor reforms. Yet policy tweaks and minor reforms are all we can manage when the pie is shrinking and every vested interest is fighting to maintain their share of the pie. Our failure stems from a much deeper problem: we optimize what we measure. If we measure the wrong things, and focus on measuring process rather than outcome, we end up with precisely what we have now: a set of perverse incentives that encourage self-destructive behaviors and policies. The process of selecting which data is measured and recorded carries implicit assumptions with far-reaching consequences. If we measure “growth” in terms of GDP but not well-being, we lock in perverse incentives to boost ‘growth” even at the cost of what really matters, i.e. well-being.

If we reward management with stock options, management has a perverse incentive to borrow money for stock buy-backs that push the share price higher, even if doing so is detrimental to the long-term health of the company. Humans naturally optimize what is being measured and identified as important. If students’ grades are based on attendance, attendance will be high. If doctors are told cholesterol levels are critical and the threshold of increased risk is 200, they will strive to lower their patients’ cholesterol level below 200. If we accept that growth as measured by GDP is the measure of prosperity, politicians will pursue the goal of GDP expansion.

If rising consumption is the key component of GDP, we will be encouraged to go buy a new truck when the economy weakens, whether we need a new truck or not. If profits are identified as the key driver of managers’ bonuses, managers will endeavor to increase net profits by whatever means are available. The problem with choosing what to measure is that the selection can generate counterproductive or even destructive incentives. This is the result of humanity’s highly refined skill in assessing risk and return. All creatures have been selected over the eons to recognize the potential for a windfall that doesn’t require much work to reap.

Can’t leave out the ones that are diabetic without knowing it. Oh, and: “..these obesity rates are calculated from self-reported heights and weights.”

• 30.4% Of Americans Were Obese In 2015 (Forbes)

If recent headlines are to be believed, we are rapidly approaching the future depicted in Wall-E, with a morbidly obese population that can get from place to place only with the help of a hover-scooter. “Americans are fatter than ever, CDC finds,” trumpets CNN. “This Many Americans Need To Go On A Diet ASAP, According To New CDC Report,” content farm Elite Daily smugly proclaims. But is it really that cut-and-dried? The report both articles refer to is succinctly titled “Early Release of Selected Estimates Based on Data from the National Health Interview Survey, 2015.” It was released on Tuesday, and it provides an early look at annual data from the titular survey on 15 different points, from health insurance and flu shots to smoking rates and, yes, obesity.

The publication says 30.4% of Americans were obese in 2015, with a 95% confidence interval (so somewhere between 29.62% and 31.27%). That’s compared to 19.4% in 1997. Obesity rates were higher among middle-aged people (ages 40 to 59), with the rate for that group hitting 34.6%. Ages 20 to 39, perhaps predictably, were the least obese, with 26.5% of that population having a BMI of 30 or more. Obesity was highest for black women (45%), followed by black men (35.1%), Latina women (32.6%), Latino men (32%), white men (30.2%) and white women (27.2%). The data in the release didn’t provide any information on other ethnic or racial groups, nor did it break obesity rates down by household income.

In concert with rising obesity rates, Americans are getting more diabetic. In 1997, 5.1% of U.S. adults had been diagnosed with diabetes. By 2015, that number had nearly doubled, to 9.5%. Although, again, the data here don’t break everything down to my satisfaction–there are no numbers for each specific type of diabetes, for instance–it’s safe to say that these correlations are the consequence of rising obesity, as 95% of people diagnosed with diabetes have type 2.

Managed to monopolize the entire Brexit debate, but they can’t leave well enough alone…

• Tory Turmoil Escalates With Open Call For Cameron To Quit (G.)

David Cameron’s hopes of being able to avoid terminal damage to Conservative party unity after the EU referendum campaign were dented on Sunday when two rebel MPs openly called for a new leader and a general election before Christmas. The attacks came from Andrew Bridgen and Nadine Dorries – both Brexiters, and longstanding, publicity-hungry opponents of the prime minister – and their claim that even winning the EU referendum won’t stop Cameron facing a leadership challenge in the summer was dismissed by fellow Tories. But their comments coincided with the ministers in charge of the leave campaign launching some of their strongest personal attacks yet on Cameron, prompting Labour’s Alan Johnson to say that the Tory infighting was getting “very ugly indeed”.

Bridgen told the BBC’s 5 Live that Cameron had been making “outrageous” claims in his bid to persuade voters to back remain and that, as a consequence, he had effectively lost his parliamentary majority. “The party is fairly fractured, straight down the middle and I don’t know which character could possibly pull it back together going forward for an effective government. I honestly think we probably need to go for a general election before Christmas and get a new mandate from the people,” he said. Bridgen said at least 50 Tory MPs – the number needed to call a confidence vote – felt the same way about Cameron and that a vote on the prime minister’s future was “probably highly likely” after the referendum.

Dorries told ITV’s Peston on Sunday she had already submitted her letter to the chairman of the Tory backbench 1922 committee expressing no confidence in the prime minister. “[Cameron] has lied profoundly, and I think that is actually really at the heart of why Conservative MPs have been so angered. To say that Turkey is not going to join the European Union as far as 30 years is a lie.”

Australia will keep debating this while the last bits die off.

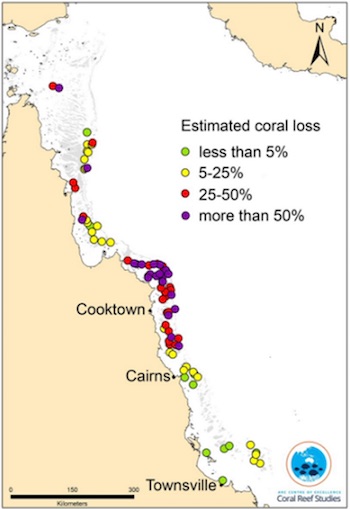

• Half Of Central, Northern Great Barrier Reef Corals Are Dead (SMH)

More than one-third of the coral reefs of the central and northern regions of the Great Barrier Reef have died in the huge bleaching event earlier this year, Queensland researchers said. Corals to the north of Cairns – covering about two-thirds of the Great Barrier Reef – were found to have an average mortality rate of 35%, rising to more than half in areas around Cooktown. The study, of 84 reefs along the reef, found corals south of Cairns had escaped the worst of the bleaching and were now largely recovering any colour that had been lost. Professor Terry Hughes, director of the ARC Centre of Excellence for Coral Reef Studies at James Cook University, said he was “gobsmacked” by the scale of the coral bleaching which far exceeded the two previous events in 1998 and 2002.

“It is fair to say we were all caught by surprise,” Professor Hughes said. “It’s a huge wake up call because we all thought that coral bleaching was something that happened in the Pacific or the Caribbean which are closer to the epicentre of El Nino events.” The El Nino of 2015-16 was among the three strongest on record but the starting point was about 0.5 degrees warmer than the previous monster of 1997-98 as rising greenhouse gas emissions lifted background temperatures. Reefs in many regions, such as Fiji and the Maldives, have also been hit hard. Bleaching occurs when abnormal conditions, such as warm seas, cause corals to expel tiny photosynthetic algae, called zooxanthellae. Corals turn white without these algae and may die if the zooxanthellae do not recolonise them.

The northern end of the Great Barrier Reef was home to many 50- to 100-year-old corals that had died and may struggle to rebuild before future El Ninos push tolerance beyond thresholds. “How likely is it that they will fully recover before we get a fourth or a fifth bleaching event?” Professor Hughes said. The health of the reef has been a contentious political issue, with Environment Minister Greg Hunt pledging more funds in the May budget to improve water quality – one aspect affecting coral health. But Mr Hunt has also had to explain why his department instructed the UN to cut out a section on Australia from a report that dealt with the threat of climate change to World Heritage sites including the Great Barrier Reef and Kakadu.

Home › Forums › Debt Rattle May 30 2016