Fred Lyon Embarcadero lunch San Francisco 1948

Double or nothing?!

• Americans Are Dying With An Average Of $61,500 In Debt (ZH)

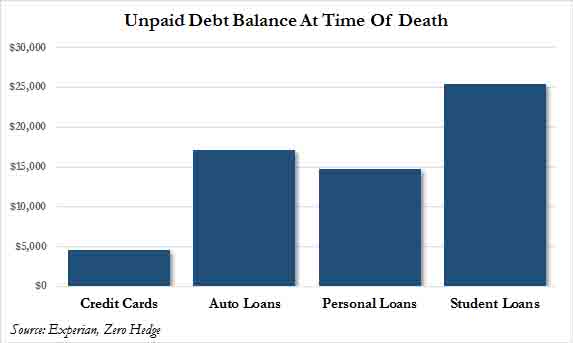

According to a recent study, the average total household debt in America is just over $132,500, broken down as per the chart below… and thanks to the Fed’s recent and ongoing rate increases, the repayment of said debt will become increasingly more difficult. So difficult, in fact, that most Americans will be saddled with a sizable chunk of it at the time of their death. Actually, most already are. According to December 2016 data from credit bureau Experian provided to credit.com, 73% of American consumers had outstanding debt when they were reported as dead. Those consumers carried an average total balance of $61,554, including mortgage debt. Without home loans, the average balance was $12,875. As credit.com reports, the data is based on Experian’s FileOne database, which includes 220 million consumers.

To determine the average debt people have when they die, Experian looked at consumers who, as of October 2016, were not deceased, but then showed as deceased as of December 2016. Among the 73% of consumers who had debt when they died, about 68% had credit card balances. The next most common kind of debt was mortgage debt (37%), followed by auto loans (25%), personal loans (12%) and student loans (6%). The breakdown of unpaid balances was as follows: credit cards, $4,531; auto loans, $17,111; personal loans, $14,793; and student loans, $25,391. And, as a reminder, debt doesn’t just disappear when someone dies.

What happens to that debt when you die, aside from it continuing to accrue interest until someone remembers to inform the creditors? “Debt belongs to the deceased person or that person’s estate,” said Darra L. Rayndon, an estate planning attorney with Clark Hill in Scottsdale, Arizona. If someone has enough assets to cover their debts, the creditors get paid, and beneficiaries receive whatever remains. But if there aren’t enough assets to satisfy debts, creditors lose out (they may get some, but not all, of what they’re owed). Family members do not then become responsible for the debt, as some people worry they might. That’s the general idea, but things are not always that straightforward. The type of debt you have, where you live and the value of your estate significantly affects the complexity of the situation. For example, federal student loan debt is eligible for cancellation upon a borrower’s death, but private student loan companies tend not to offer the same benefit. They can go after the borrower’s estate for payment.

Let’s do a stress test that assumes the Fed is no longer around, see what happens.

• 34 Biggest Banks in US Clear First Hurdle In Fed’s Annual Stress Tests (R.)

The 34 largest U.S. banks have all cleared the first stage of an annual stress test, showing they would be able to maintain enough capital in an extreme recession to meet regulatory requirements, the Federal Reserve said on Thursday. Although the banks, including household names like JPMorgan Chase and Bank of America, would suffer $383 billion in loan losses in the Fed’s most severe scenario, their level of high-quality capital would be substantially higher than the threshold that regulators demand, and an improvement over last year’s level. “This year’s results show that, even during a severe recession, our large banks would remain well capitalized,” said Fed Governor Jerome Powell, who leads banking regulation for the central bank. “This would allow them to lend throughout the economic cycle, and support households and businesses when times are tough.”

The Fed introduced the stress tests in the wake of the financial crisis to ensure the health of the banking industry, whose ability to lend is considered crucial to the health of the economy. Since the first test was conducted in 2009, big banks have seen losses abate, loan portfolios improve and profits grow. The banks that now undergo the exam have also strengthened their balance sheets by adding more than $750 billion in top-notch capital, the Fed said. Banks and their investors have been hoping the improvements would prompt the Fed to allow them to use more capital for stock buybacks and dividends, especially as the Trump administration is seeking to relax financial regulations. Wall Street analysts and trade groups quickly cheered the results on Thursday, saying regulators should feel comfortable easing tough rules put in place since the financial crisis. “We see today’s…stress test results as a positive for Trump administration efforts to deregulate the banks,” said Jaret Seiberg, a policy analyst with Cowen & Co.

The biggest debts are still in mortgages. Falling home prices will hurt most.

• Credit-Card Debt Slaves Move to Top of Fed’s Bank Worries (WS)

The comforting news in the results from the Federal Reserve’s annual stress test is that the largest 34 bank holding companies would all survive a recession. Based on this glorious accomplishment, the clamoring has already started for regulators to allow these banks to pay bigger dividends and to blow more money on share buybacks, and for these regulators to slash regulation on these banks and make their life easier and riskier in general. We don’t want these banks to survive a recession in too good a condition apparently. And it would likely be better for Wall Street anyway if banks could lever up with risks so that a few of them would get bailed out during the next recession. Let’s remember, for the Fed’s no-holds-barred bailout-year 2009, Wall Street executives and employees were doused with record bonuses.

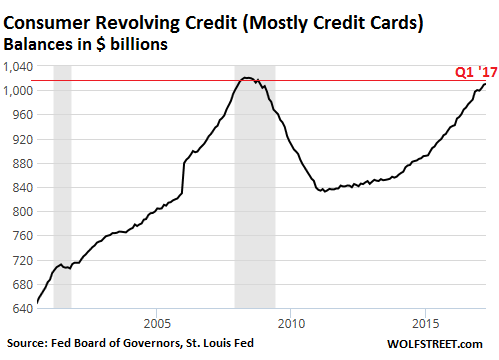

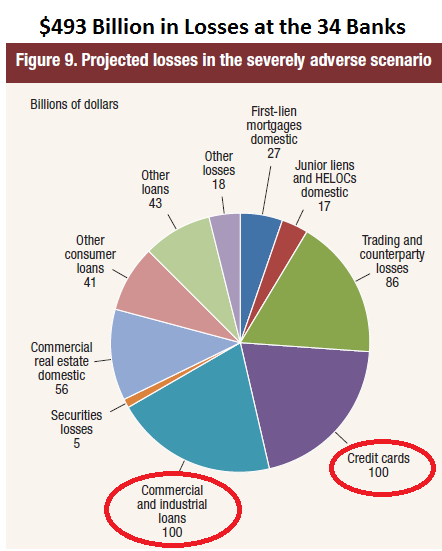

The Fed’s bailouts were good for them. And it has been good for them ever since. The less comforting news in the stress test is that credit card debt – generally the most expensive and risky debt for consumers – has now moved to the top of the Fed’s worry list in the “severely adverse scenario” of the stress test. The projected losses for the 34 largest banks – not counting the losses at the 4,997 smaller banks – are expected to hit $100 billion, up nearly 9% from the stress test a year ago. The projected losses rose for several reasons, including that credit card balances have grown by 5.6% from a year ago to over $1 trillion. The delinquency rate has risen to 2.4%. The Fed is also blaming looser lending standards. Sharing the top spot on the Fed’s worry list in the “severely adverse scenario” are Commercial & Industrial loans, whose balances are over twice as large, at $2.1 trillion, but whose projected losses are also pegged at $100 billion. In total, the “severely adverse scenario” sees $493 billion in losses for these 34 banks:

“..investors, drunk with the liquor of loose money..”

• Citizens Will Soon Turn Their Rage Towards Central Bankers (Albert Edwards)

Albert Edwards pwrites “Theft redux: the citizens will soon turn their rage towards Central Bankers.” The core of his argument is familiar: “While politics in the West reels from a decade of economic crisis and stagnation, asset prices continue to surge on the back of continued rapid growth in G3 QE. In an age of “radical uncertainty” how long will it be before angry citizens tire of blaming an impotent political system for their ills and turn on the main culprits for their poverty – unelected and virtually unaccountable central bankers? I expect central bank independence will be (and should be) the next casualty of the current political turmoil.” That’s just the beginning from Edwards, who appears to be getting increasingly angrier and more frustrated with a market that makes increasingly less sense: his fiery sermon continue with the following preview of the “inevitable catastrophe that lies ahead.”

“Evidence of the impact of monetary madness on assets prices is all around if we care to look. I read that a parking spot in Hong Kong was just sold for record HK$5.18 million ($664,200). What about the 3.5x oversubscribed 100 year Argentine government bond? Sure, everything has a market clearing price, even one of the most regular defaulters in history. But what concerned me most about the story was it was demand from investors (“reverse enquires”) that prompted the issue. Is it just me or can I hear echoes of the mechanics of the CDO crisis? But no one cares when the party is still raging and investors, drunk with the liquor of loose money, are blind to the inevitable catastrophe that lies ahead. There is a lot of anger out on the streets, as demonstrated most visibly in recent elections.

Even in France where investors feel comforted that a “moderate” has gained (absolute?) power, it is salutary to remember that the two establishment parties have just been decimated by a man who had never before stood for public office! This is perhaps even more radical than Trump’s anti-establishment victory under the Republican umbrella. The global political situation is incredibly fluid and unpredictable. While a furious electorate has turned its pent up anger on the establishment political parties, the target for their rage is misguided. I am not completely alone in thinking it is the unelected and virtually unaccountable central bankers who are primarily responsible for the poverty of working people and who will be ultimately held to account in the next crisis.

In other news: ” Government-funded new social housing has fallen 97% since 2010″.

• UK Homelessness Surges 34% Under Tories Since 2010 (Ind.)

The number of families being declared homeless has rocketed by more a third since the Conservatives took power in 2010, analysis of new official statistics by The Independent has revealed. Between April 2016 and March 2017, 59,100 families were declared homeless by local authorities in England – a rise of 34% on the same period in 2010-11. The statistics paint a bleak picture of the UK housing crisis and the impact a lack of decent, affordable homes is having on thousands of families. There has been a 60% increase in the number of families being housed in insecure temporary accommodation. In particular, bed and breakfast-type hotels are increasingly being used to house families for long periods of time as local councils struggle to find them proper homes to live in.

There are now 77,240 families in England currently living in temporary accommodation – up from 48,240 just six years ago. Of these, almost fourth-fifths (78%) are families with children, meaning there are currently 120,500 children living in insecure, temporary homes. Of those being housed temporarily, 6,590 households are living in B&Bs, including 3,010 families with children. Almost half have been living in this type of accommodation, which often sees families crammed into one room and forced to share limited bathroom and cooking facilities with strangers, for more than six weeks. This is illegal under the Homelessness (Suitability of Accommodation) Order 2003, which banned local authorities from housing families with children in B&Bs for more than a six-week period.

The Tories are done. Someone should tell them.

• UK High Court Judges Tory Policy Causes ‘Real Misery For No Purpose’ (Ind.)

Today, the High Court ruled that the benefits cap, one of the Tories’ flagship welfare policies, is unlawful, because it amounts to illegal discrimination against single parents with small children. It’s likely that the Government will be forced to alter or completely scrap their benefits cap, a policy that limits the total amount a household can receive in benefits to £23,000 in London and £20,000 elsewhere in the UK. High Court judge Justice Collins described the benefit cap as causing “real damage” to single parent families and said “real misery is being caused to no good purpose”. This is the fundamental truth at the heart of Tory welfare policy – misery without progress or reason.

Welfare reform as part of the coalition government’s austerity measures has driven thousands more people into poverty and in many tragic cases, some deaths occurred after individuals were declared fit to work. Austerity was not inevitable. It was an ideologically-motivated programme designed to force the poorest and most vulnerable in our society to shoulder the burden of a financial crisis that they had less than nothing to do with creating. Four claimants brought this case to court. Two of them had been made homeless as a result of domestic violence, and were trying to work as many hours as possible while taking care of children under the age of two. Imagine fleeing an abusive partner, seeking support from a domestic violence service that’s had its funding brutally slashed by the Tory government, trying to work and look after a small child, then having your benefits cut, again by the Tory government.

The claimants are not alone. The benefits cap has inflicted a massive amount of suffering, with 200,000 children from the very lowest income families affected, as their parents’ income has fallen drastically. In real terms, this means that these children’s lives have become even more difficult, and they weren’t easy to begin with. This means a colder house, less food to eat, more shame at school due to unwashed clothes, uniforms that are too small, worn-through shoes. It means stressed, unhappy and increasingly desperate parents, and in family, children can’t fail to pick up on this mood of misery. [..] In this wealthy, highly developed country, poverty is the single biggest threat to the wellbeing of children and families. Poverty affects a quarter of all children in Britain, a massive, disgraceful, inexcusable proportion. one in five parents are struggling to feed their children, and 50% of all parents living in food poverty have gone without meals in order to give their children more to eat.

There goes the bubble. Look out below.

• Buy-to-Let Uk Property Sales Fall By Almost 50% In A Year (G.)

The number of properties bought by landlords has almost halved in a year after a tax and regulatory clampdown, prompting a leading banking body to downgrade its forecasts for buy-to-let lending in 2017 and 2018. The Council of Mortgage Lenders said buy to let had had a weak start to 2017, with lending falling faster than expected as landlords withdrew from the market in response to major tax changes and tighter lending rules. The data follows a series of recent surveys and indices suggesting the housing market is running out of steam. However, the crackdown on buy to let may have helped young people trying to get a foot on the property ladder. CML said house purchase activity was being driven predominantly by first-time buyers, with their numbers up 8% in the 12 months to April.

Buy-to-let homebuying activity was “nearly half what it was a year ago” and had averaged around 6,000 purchases a month over the last 12 months, said the body, which represents banks and building societies. The number of landlord purchases involving a mortgage was 5,300 in April this year. This compared with 10,300 in February 2016 and 11,800 in July 2015. As a result, the CML has cut its forecast for buy-to-let lending from £38bn being lent in both 2017 and 2018 to £35bn in 2017 and £33bn in 2018. The organisation warned against hitting landlords with any further changes to taxation and lending rules, saying the figures “re-emphasise the case for avoiding further changes to the tax and regulatory framework until the effect of these already in train have been properly assessed”.

Download report here: Addicted to Debt – Tracking Canada’s rapid accumulation of private sector debt .

• Canada’s Private Sector Debt Growing Faster Than Any Advanced Economy (PA)

For the first time ever, Canada’s private sector is racking up debt faster than any other of the world’s 22 advanced economies, putting the country at risk of serious economic consequences, according to new research by the Canadian Centre for Policy Alternatives. A new report authored by CCPA Senior Economist David Macdonald reveals that Canada added $1 trillion in private sector debt over the past five years ($2016), with the corporate sector responsible for the majority of it. Economies can become dependent on debt in order to fuel economic and asset price growth. With both rapid private debt accumulation and a high private debt-to-GDP ratio, even a small change in debt growth rates, brought on by changes in interest rates for instance, could have a devastating impact on the larger economy.

“Private sector debt growth is one of the best predictors of economic crisis, and Canada is now the only advanced economy squarely in the debt ‘danger zone’ of having high private sector debt that continues to rise rapidly,” Macdonald says. The report identifies several areas of concern:

• Canada has never before led the advanced economies in private debt growth;

• The last time Canada was close to leading the world in private debt growth was the early 1990s, just as housing prices plummeted and then stagnated for a decade;

• The country’s private debt-to-GDP ratio has risen by a fifth since 2011, from 182% to 218%. The US ratio currently stands at 152%;

• The $315 billion increase in household debt since 2011 ($2016) is almost entirely attributable to the rise in mortgage debt related to rapid home prices increases;

• Corporate debt is less well studied, and rose $671 billion since 2011 ($2016), accounting for two thirds of private debt accumulation over that time;

• Corporate debt was largely spent on mergers and acquisitions as well as real estate purchases, neither of which make the country more productive.“Canada’s economy has become addicted to binging on ever more private sector debt, and weaning us off it should be our primary public policy concern,” adds Macdonald, who recommends further study of corporate debt and consideration of a housing speculators’ tax to further reign in mortgage debt increases.

Well, it can’t be because Buffett see a bright future in Canada’s housing market. So draw your own conclusion.

• Warren Buffett Becomes Lender Of Last Resort For Canada’s Home Capital (BBG)

Warren Buffett has become the lender of last resort for Home Capital. The billionaire investor agreed to buy shares at a deep discount and provide a fresh credit line for the Canadian mortgage company, tapping a formula he used to prop up lenders from Goldman Sachs to Bank of America. Buffett’s Berkshire Hathaway Inc. will buy a 38% stake for about C$400 million ($300 million) and provide a C$2 billion credit line with an interest rate of 9% to backstop the embattled Toronto-based lender, Home Capital said late Wednesday in a statement. The interest on the one-year loan would net Berkshire at least C$180 million if it’s fully tapped.

“While the terms of the new credit line with Berkshire Hathaway remain harsh, we believe the purpose of this loan is to motivate Home Capital’s management to bolster their own funding sources,” said Hugo Chan at Kingsferry Capital in Shanghai, which owns shares in Home Capital. “This again shows Mr. Buffett’s masterful capital allocation skills,” said Chan, citing his investment motto: “be greedy when others are fearful.” The financial backing from Buffett sent the stock higher Thursday, though it comes at a cost, in keeping with his past bailouts of financial firms. Buffett has buoyed some of the biggest U.S. corporations in times of trouble, including a combined $8 billion injection to prop up Goldman Sachs and General Electric when credit markets froze during the 2008 financial crisis.

In the Home Capital deal, Buffett’s firm agreed to pay an average price of C$10 a share, a 33% discount to Wednesday’s closing price of C$14.94. Berkshire would become the largest shareholder in Home Capital, which has a market value of about C$1 billion. Home Capital surged 27% to C$19 in Toronto on Thursday. That gives Buffett a 90% return on paper for the equity investment, assuming the deal goes through.

They always have, it’s an MO.

• EU Political Class Rides Roughshod over Citizens’ Concerns & Frustrations (DQ)

Merkel has expressed a willingness to go along with two central French demands — the appointment of a Eurozone finance minister and the creation of a common budget — as long as certain conditions are met. “We can of course think about a Eurozone budget as long as it’s clear that this is really strengthening structures and achieving sensible results,” she said. [..] Back on the table is a proposal to upgrade the grossly unaccountable Luxembourg-based European Stability Mechanism (ESM) into a full-fledged European Monetary Fund. As we’ve noted before, creating a European Monetary Fund (EMF) would be an important statement of intent. If Europe’s core countries are truly set on taking the EU project to a whole new level, such as by pursuing the creation of an EU army, an EU border force (with full powers), fiscal union, and ultimately political union, some form of burden sharing will ultimately be necessary.

The establishment of a fully operational EMF could be an important move in that direction. The EMF would essentially act as a fiscal backdrop to the banking system, something the Eurozone has desperately needed ever since its creation. As Bruegel proposes, it would serve as a fiscal counterpart of the ECB to guarantee the financial stability of the euro area in the event of a sovereign or banking crisis, or a threat thereof — of which there are plenty these days, in particular emanating from Italy’s broken banking system. Naturally, the creation of an EMF would deal a further blow to the fading remnants of national sovereignty in Europe. But that’s a price that many (but certainly not all) of Europe’s elite is more than happy to pay; some would say that destroying national sovereignty was the ultimate goal of the EU all along.

In a survey of more than 10,000 EU citizens and 1,800 EU elites carried out by Chatham House, of the elites, 37% believe the EU should get more powers, 28% want to keep the status quo and 31% would prefer to return more powers to individual member countries. This enthusiasm for a more centralized, more powerful EU is not shared with equal enthusiasm by European citizens: 48% want powers returned to the individual member countries. Citizens, overall, do not feel they have benefited from European integration in the same way Europe’s elite does. Whereas 71% of elites report feeling they have gained something from the EU, the figure among the public is only 34%. Even more worrisome for national leaders, a clear majority of the public — 54% — feel that their country was a better place to live 20 years ago, before the euro existed.

I’ve seen a few parts. Liked them quite a bit.

• Dear Oliver: About Those Putin Interviews (RM)

Dear Mr. Stone: I have just finished watching all four episodes of The Putin Interviews. May I give you my critique? Overall, I felt that the series is Very Good but felt just short of Great. I will explain below what I feel could have made it Great. First, I want to tell you what I really loved about it. 1. You have an easy style. I felt as if Mr. Putin was at ease with you, and you with him. You have a warm command of the English language and can transmit your ideas into language in a very personable way — an art that is missing among so many American media people these days. I felt that you drew out a candid side of Putin, well, that is, as far as a man of his intellectual prowess and disciplined self-control will allow. 2. Best moment of the show: Sitting next to Vlad and watching Dr. Strangelove! Oh my goodness, most people would not even dream of adding such a thing to their bucket list.

3. I loved the walking tour of the President’s offices and the general background of the Kremlin architecture and decor. I pay attention to the daily, tweeted photos from the Kremlin’s official account. I have seen those desks and tables a million times in the photos. But now I have them all within a mental frame, thanks to your film. Question: I was burning to know why Vlad had a pair of scissors and multi-colored construction paper in the middle of his desk, did you happen to ask him, off-camera?

Where It Fell Short Mr. Stone, I hated that so much time was wasted talking about the contrived “Russia hacked the election” meme. Hillary might not know why she lost the election, but the rest of the nation does. When my father would get on a roll with his bad jokes, Mom would tell us kids: “Don’t encourage him.” Well, you too need to stop encouraging the MSM to keep breathing life into a dead meme.

You also wasted time re-hashing Crimea. “Read My Lips,” Vlad said, “the Crimeans ASKED, BEGGED, AND VOTED to rejoin Russia.” Good grief, when McCain’s and Nuland’s beloved neo-Nazi Svoboda party took illegal control of Ukraine, their first move was to try and make it illegal to speak Russian. Geez, half the people in Ukraine ARE Russian! Mr. Putin has exercised considerable restraint towards Ukraine.

Mr. Stone, I have been following the development of BRICS, the “Silk Road Project,” and the EEU (European Economic Union) for a half-decade now. I can’t have a conversation with my neighbors and friends about all of that here in America because not one of them has heard anything about it! You had a great opportunity to ask Mr. Putin to school us on the Sino-Russian version of a multi-polar world without war, but you totally blew it. I don’t think you ever asked Vlad about China, did you?

Saudi Arabia accuses Qatar of supporting terrorism. Rich.

• Arab States Send Qatar 13 Demands To End Crisis (R.)

Four Arab states boycotting Qatar over alleged support for terrorism have sent Doha a list of 13 demands including closing Al Jazeera television and reducing ties to their regional adversary Iran, an official of one of the four countries said. The demands aimed at ending the worst Gulf Arab crisis in years appear designed to quash a two decade-old foreign policy in which Qatar has punched well above its weight, striding the stage as a peace broker, often in conflicts in Muslim lands. Doha’s independent-minded approach, including a dovish line on Iran and support for Islamist groups, in particular the Muslim Brotherhood, has incensed some of its neighbors who see political Islamism as a threat to their dynastic rule.

The list, compiled by Saudi Arabia, the United Arab Emirates (UAE), Egypt and Bahrain, which cut economic, diplomatic and travel ties to Doha on June 5, also demands the closing of a Turkish military base in Qatar, the official told Reuters. Qatar must also announce it is severing ties with terrorist, ideological and sectarian organizations including the Muslim Brotherhood, Islamic State, al Qaeda, Hezbollah, and Jabhat Fateh al Sham, formerly al Qaeda’s branch in Syria, he said, and surrender all designated terrorists on its territory, The four Arab countries accuse Qatar of funding terrorism, fomenting regional instability and cozying up to revolutionary theocracy Iran. Qatar has denied the accusations.

[..] on Monday, Foreign Minister Sheikh Mohammed bin Abdulrahman al-Thani said Qatar would not negotiate with the four states unless they lifted their measures against Doha. The countries give Doha 10 days to comply, failing which the list becomes “void”, the official said without elaborating, suggesting the offer to end the dispute in return for the 13 steps would no longer be on the table.

Bunch of sicko’s.

Edward Snowden on Twitter: “Biggest @AP scoop in a long time: US government behind UAE torture in Yemen, with some reportedly grilled alive.”

• In Yemen’s Secret Prisons, UAE Tortures and US Interrogates

Hundreds of men swept up in the hunt for al-Qaida militants have disappeared into a secret network of prisons in southern Yemen where abuse is routine and torture extreme — including the “grill,” in which the victim is tied to a spit like a roast and spun in a circle of fire, an Associated Press investigation has found. Senior American defense officials acknowledged Wednesday that U.S. forces have been involved in interrogations of detainees in Yemen but denied any participation in or knowledge of human rights abuses. Interrogating detainees who have been abused could violate international law, which prohibits complicity in torture. The AP documented at least 18 clandestine lockups across southern Yemen run by the United Arab Emirates or by Yemeni forces created and trained by the Gulf nation, drawing on accounts from former detainees, families of prisoners, civil rights lawyers and Yemeni military officials.

All are either hidden or off limits to Yemen’s government, which has been getting Emirati help in its civil war with rebels over the last two years. The secret prisons are inside military bases, ports, an airport, private villas and even a nightclub. Some detainees have been flown to an Emirati base across the Red Sea in Eritrea, according to Yemen Interior Minister Hussein Arab and others. Several U.S. defense officials, speaking on condition of anonymity to discuss the topic, told AP that American forces do participate in interrogations of detainees at locations in Yemen, provide questions for others to ask, and receive transcripts of interrogations from Emirati allies. They said U.S. senior military leaders were aware of allegations of torture at the prisons in Yemen, looked into them, but were satisfied that there had not been any abuse when U.S. forces were present.

“We always adhere to the highest standards of personal and professional conduct,” said chief Defense Department spokeswoman Dana White when presented with AP’s findings. “We would not turn a blind eye, because we are obligated to report any violations of human rights.” In a statement to the AP, the UAE’s government denied the allegations. “There are no secret detention centers and no torture of prisoners is done during interrogations.” Inside war-torn Yemen, however, lawyers and families say nearly 2,000 men have disappeared into the clandestine prisons, a number so high that it has triggered near-weekly protests among families seeking information about missing sons, brothers and fathers.

None of the dozens of people interviewed by AP contended that American interrogators were involved in the actual abuses. Nevertheless, obtaining intelligence that may have been extracted by torture inflicted by another party would violate the International Convention Against Torture and could qualify as war crimes, said Ryan Goodman, a law professor at New York University who served as special counsel to the Defense Department until last year

Home › Forums › Debt Rattle June 23 2017