Arnold Genthe “Chinatown, San Francisco. The street of the gamblers at night” 1900

The most interesting and thought-provoking thing I’ve read about the election amidst a river of blubber.

• Why I Switched My Endorsement from Clinton to Trump (Scott Adams)

5. Pacing and Leading: Trump always takes the extreme position on matters of safety and security for the country, even if those positions are unconstitutional, impractical, evil, or something that the military would refuse to do. Normal people see this as a dangerous situation. Trained persuaders like me see this as something called pacing and leading. Trump “paces” the public – meaning he matches them in their emotional state, and then some. He does that with his extreme responses on immigration, fighting ISIS, stop-and-frisk, etc. Once Trump has established himself as the biggest bad-ass on the topic, he is free to “lead,” which we see him do by softening his deportation stand, limiting his stop-and-frisk comment to Chicago, reversing his first answer on penalties for abortion, and so on.

If you are not trained in persuasion, Trump looks scary. If you understand pacing and leading, you might see him as the safest candidate who has ever gotten this close to the presidency. That’s how I see him. So when Clinton supporters ask me how I could support a “fascist,” the answer is that he isn’t one. Clinton’s team, with the help of Godzilla, have effectively persuaded the public to see Trump as scary. The persuasion works because Trump’s “pacing” system is not obvious to the public. They see his “first offers” as evidence of evil. They are not. They are technique. And being chummy with Putin is more likely to keep us safe, whether you find that distasteful or not. Clinton wants to insult Putin into doing what we want. That approach seems dangerous as hell to me.

6. Persuasion: Economies are driven by psychology. If you expect things to go well tomorrow, you invest today, which causes things to go well tomorrow, as long as others are doing the same. The best kind of president for managing the psychology of citizens – and therefore the economy – is a trained persuader. You can call that persuader a con man, a snake oil salesman, a carnival barker, or full of shit. It’s all persuasion. And Trump simply does it better than I have ever seen anyone do it. The battle with ISIS is also a persuasion problem. The entire purpose of military action against ISIS is to persuade them to stop, not to kill every single one of them. We need military-grade persuasion to get at the root of the problem. Trump understands persuasion, so he is likely to put more emphasis in that area.

Most of the job of president is persuasion. Presidents don’t need to understand policy minutia. They need to listen to experts and then help sell the best expert solutions to the public. Trump sells better than anyone you have ever seen, even if you haven’t personally bought into him yet. You can’t deny his persuasion talents that have gotten him this far. In summary, I don’t understand the policy details and implications of most of either Trump’s or Clinton’s proposed ideas. Neither do you. But I do understand persuasion. I also understand when the government is planning to confiscate the majority of my assets. And I can also distinguish between a deeply unhealthy person and a healthy person, even though I have no medical training. (So can you.)

The Dream ended decades ago, it’s just a matter of picking which decade.

• When America Was Great, Taxes Were High, Unions Strong, and Government Big (A.)

There is plenty about GOP hopeful Donald Trump to which potential primary voters respond. He’s successful. He’s plainspoken. At a time when politicians are historically unpopular, he’s not a politician. And he has a great slogan. That slogan resonates with his supporters, according to Republican pollster Frank Luntz, who ran a recent focus group, the results of which were written about in Time. “I used to sleep on my front porch with the door wide open, and now everyone has deadbolts,” one man told Luntz. “I believe the best days of the country are behind us.” Luntz concluded that people see Trump as a “real-deal fixer-upper,” able to make repairs that others have bungled. “We know his goal is to make America great again,” one woman astutely observed. “It’s on his hat.”

It could be on your hat too—Trump has begun selling “Make America Great Again” merchandise—if you can find one, that is. They have a tendency to sell out. As Russell Berman pointed out in The Atlantic earlier this month, many white Americans these days are pessimistic to the point of despair: “White Americans—and in particular those under 30 or nearing retirement age—have all but given up on the American Dream. More than four out of five younger whites, and more than four out of five respondents between the ages of 51 and 64 said The Dream is suffering.” No wonder Trump’s message is so powerful—it’s a sugar pill coated with nostalgia. He is not promising to make America great, he’s promising to make it great again. But to what era does he intend to take the nation back?

And what would that look like, practically speaking? The boundaries of America’s “golden age” are clear on one end and fuzzy on the other. Everyone agrees that the midcentury boom times began after Allied soldiers returned in triumph from World War II. But when did they wane? The economist Joe Stiglitz, in an article in Politico Magazine titled “The Myth Of The American Golden Age,” sets the endpoint at 1980, a year until which “the fortunes of the wealthy and the middle class rose together.” Others put the cut-off earlier, at the economic collapse of 1971 and the ensuring malaise. Regardless of when it ended, it would not be unfair to use the ’50s as shorthand for this now glamorized period of plenty, peace, and the kind of optimism only plenty and peace can produce.

Ever more debt is the only way to keep the facade upright enough that people believe in it.

• Global Debt Reaches Fresh High As Companies And Countries Keep Borrowing (Tel.)

Global debt issuance is on course to hit a record high in 2016 as figures showed sales this year topped $5 trillion (£3.9 trillion) at the end of September. Debt issuance rose to $5.02 trillion in the nine months to September 22, according to Dealogic, putting 2016 on course to beat the all-time high of $6.6 trillion recorded in 2006. Record low interest rates have encouraged countries and companies to issue debt as central banks around the world try to stimulate growth. The data also showed corporate issuance of investment-grade debt reached a record high of $1.54 trillion since the start of the year, up from $1.41 trillion in the same period a year earlier. Dealogic’s figures also highlighted the impact of the Brexit vote.

Sterling-denominated investment grade debt rose to $21.3bn in the first nine months of the year, up slightly from $20.9bn raised in the same period of 2015. Volumes in July fell to their lowest since 2000 as the referendum result slowed issuance, with just $564m issued, according to Dealogic. However, issuance is expected to pick up later this year following the Bank of England’s decision to buy £10bn of corporate debt as part of its revamped bond-buying programme. Sterling issuance in August jumped to six times the average following the Bank’s announcement. Green bonds – which raise money for environmentally friendly projects and often carry tax exemptions – are also rising in popularity.

Activity surpassed full-year 2015 levels in September as volumes reached a record high, worth $48.2bn. Mark Carney, the Governor of the Bank of England, has spoken out in favour of green finance, describing it as a “major opportunity” for investors. In a speech last week, he said long-term financing of green projects in emerging markets could help to promote financial stability. “By ensuring that capital flows finance long-term projects in countries where growth is most carbon intensive, financial stability can be promoted,” he said. More than $13 trillion of global sovereign and corporate debt trades at negative yields, highlighting the influence of central banks.

Draghi’s comments on small banks remind me of Ken Rogoff’s war on cash.

There are plenty of reasons to be worried about the state of Europe these days, but if one had to choose one thing above all others, it would be the gaping disconnect between reality and senior European policy makers’ willful misperception of reality. A perfect case in point was a speech given in Frankfurt by ECB president Mario Draghi. He was addressing a conference of the European Systemic Risk Board (ERSB), an organization created in 2010 by the European Commission to warn about and mitigate systemic financial risks in Europe. During his address Draghi discussed what he saw as the biggest threats to Europe’s financial system.

Just as you’d expect from any senior central banker worth his or her salt, he did not point to the most obvious risk: the zombifying banks at the very top of the financial food chain — the same banks that coincidentally constitute the ECB’s number-one constituency and whose balance sheets are still filled to the rafters with toxic assets dating back to even before the last major crisis, in 2008. By now, virtually all of these banks are fully dependent on the never-ending and ever-growing welfare assistance provided by the ECB. Nor did Draghi mention the excessive complexity and interconnectedness of the banking system, routinely fingered as potential causes of the next global financial crisis.

Nor for that matter did he mention the destructive side effects of the ECB’s negative interest rate policy (NIRP), which – besides sacrificing millions of savers and retirees via their pension funds on the altar of rampant debt creation and completely undermining the crucial micro-economic role played by capital formation – is making it difficult for Europe’s largest banks to turn a meaningful profit. No, for Draghi, the biggest financial problem in Europe these days is that it is over-banked. “Over-capacity in some national banking sectors, and the ensuing intensity of competition, exacerbates this squeeze on margins,” he said. Put simply, there’s just too much competition from the thousands of smaller banks that are crowding out the profits for the big banks.

“The weakness in real GDP growth is of greatest concern, because it’s largely the consequence of policies that encourage repeated cycles of bubbles and collapses..”

• Structural Growth and Dope Dealers on Speed-Dial (Hussman)

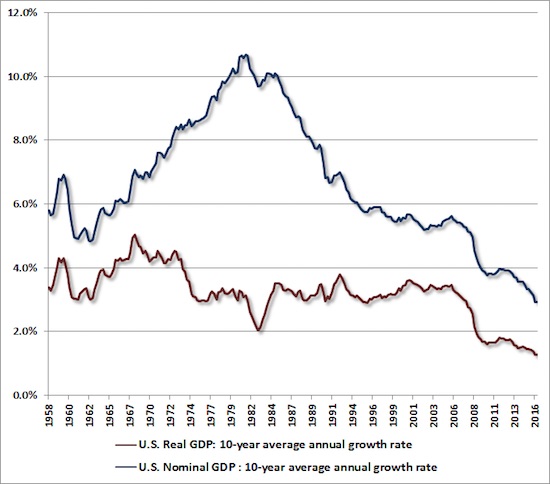

In recent years, the U.S. equity market has scaled the third steepest cliff in history, eclipsed only by the 1929 and 2000 peaks, as investors rest their full confidence and weight on the protrusions of a structurally deteriorating economy, imagining that they are instead the footholds of a robust investment environment. The first of these is the current environment of low interest rates. While investors take this as quite a positive factor, it’s largely a reflection of a steep downturn in U.S. structural economic growth, magnified by reckless monetary policy. Over the past decade, the average annual nominal growth rate of GDP has dropped to just 2.9%, while real GDP growth has plunged to just 1.3%; both the lowest growth rates in history, outside of the Depression (see the chart below).

Indeed, probably the most interesting piece of information from last week’s FOMC meeting was that the Federal Reserve downgraded its estimate for the central tendency of long-run GDP growth to less than 2% annually. The weakness in real GDP growth is of greatest concern, because it’s largely the consequence of policies that encourage repeated cycles of bubbles and collapses, and chase debt-financed consumption instead of encouraging productive real investment. Indeed, growth in real U.S. gross domestic investment has collapsed since 2000 to just one-fifth of the rate it enjoyed in the preceding half-century, and has averaged zero growth over the past decade. While labor force growth has slowed, it’s really the self-inflicted collapse of U.S. productivity growth, enabled by misguided policy, that’s at the root of the problem.

This is some investing tactic anymore. It’s about parties needing cash.

• Treasury Market’s Biggest Buyers Are Selling as Never Before (BBG)

They’ve long been one of the most reliable sources of demand for U.S. government debt. But these days, foreign central banks have become yet another worry for investors in the world’s most important bond market. Holders like China and Japan have culled their stakes in Treasuries for three consecutive quarters, the most sustained pullback on record, based on the Federal Reserve’s official custodial holdings. The decline has accelerated in the past three months, coinciding with the recent backup in U.S. bond yields. For Jim Leaviss at M&G Investments in London, that’s cause for concern. A continued retreat could lead to painful losses in a market that some say is already too expensive.

But perhaps more important are the consequences for America’s finances. With the U.S. facing deficits that are poised to swell the public debt burden by $10 trillion over the next decade, foreign demand will be crucial in keeping a lid on borrowing costs, especially as the Fed continues to suggest higher interest rates are on the horizon. The selling pressure from central banks is “something you have to bear in mind,” said Leaviss, whose firm oversees about $374 billion. “This, as well as the Fed, all means we are nearer to the end of the low-yield environment.” Overseas creditors have played a key role in financing America’s debt as the U.S. borrowed heavily in the aftermath of the financial crisis to revive the economy.

Since 2008, foreigners have more than doubled their investments in Treasuries and now own about $6.25 trillion. Central banks have led the way. China, the biggest foreign holder of Treasuries, funneled hundreds of billions of dollars back into the U.S. as its export-based economy boomed. Now, that’s all starting to change. The amount of U.S. government debt held in custody at the Fed has decreased by $78 billion this quarter, following a decline of almost $100 billion over the first six months of the year. The drop is the biggest on a year-to-date basis since at least 2002 and quadruple the amount of any full year on record, Fed data show.

“No one really knows where the losses would end up, or what the knock-on impact would be. It would almost certainly land a fatal blow to the Italian banking system, and the French and Spanish banks would be next.”

• Deutsche Bank Crisis Could Take Angela Merkel Down – And The Euro (Tel.)

True, Merkel’s position is understandable. The politics of a Deutsche rescue are terrible. Germany, with is Chancellor taking the lead, has set itself up as the guardian of financial responsibility within the euro-zone. Two years ago, it casually let the Greek bank system go to the wall, allowing the cash machines to be closed down as a way of whipping the rebellious Syriza government back into line. This year, there has been an unfolding Italian crisis, as bad debts mount, and yet Germany has insisted on enforcing euro-zone rules that say depositors – that is, ordinary people – have to shoulder some of the losses when a bank is in trouble. For Germany to then turn around and say, actually we are bailing out our own bank, while letting everyone else’s fail, looks, to put it mildly, just a little inconsistent.

Heck, a few people might even start to wonder if there was one rule for Germany, and another one for the rest. In truth, it would become impossible to maintain a hard-line in Italy, and probably in Greece as well. And yet, if Deutsche Bank went down, and the German Government didn’t step in with a rescue, that would be a huge blow to Europe’s largest economy – and the global financial system. No one really knows where the losses would end up, or what the knock-on impact would be. It would almost certainly land a fatal blow to the Italian banking system, and the French and Spanish banks would be next. Even worse, the euro-zone economy, with France and Italy already back at zero growth, and still struggling with the impact of Brexit, is hardly in any shape to withstand a shock of that magnitude.

A rock and a hard place are hardly adequate to describe the options Merkel may soon find herself facing. The politics of a rescue are terrible, but the economics of a collapse are even worse. By ruling out a rescue, she may well have solved the immediate political problem. Yet when the crisis gets worse, as it may do at any moment, it is impossible to believe she will stick to that line. A bailout of some sort will be cobbled together – even if the damage to Merkel’s already fraying reputation for competence will be catastrophic. In fact, Merkel is playing a very dangerous game with Deutsche – and one that could easily go badly wrong. If her refusal to sanction a bail-out is responsible for a Deutsche collapse that could easily end her Chancellorship. But if she rescues it, the euro might start to unravel.

Beijing purposely blows a giant bubble with money people don’t have.

• China’s Runaway Housing Market Poses Latest Challenge for Yuan (BBG)

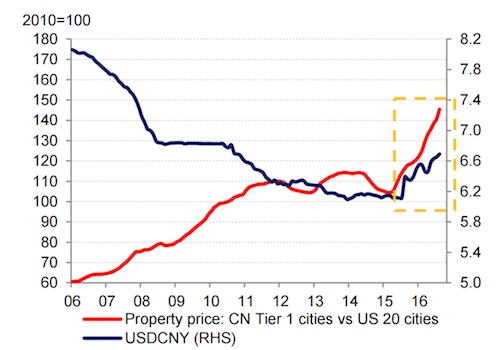

Here’s the latest uncertainty facing China’s currency: sky high house prices. A runaway boom in the largest cities will push investors to look for cheaper alternatives overseas, draining money out of China and putting downward pressure on the yuan in the process, according to analysis by Harrison Hu at Royal Bank of Scotland in Singapore. An “enlarged differential between domestic and foreign asset prices will lead to capital outflows and depreciation, until parity is restored,” Hu wrote in a note. He said that the 30% year-on-year price gain in Tier 1 and leading Tier 2 cities implies a 25% rise in dollar terms, which far outpaces the 5% gain in major U.S. cities. That ratio is here in red:

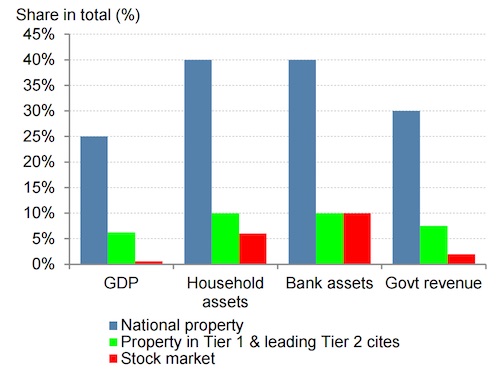

“It’s commonly believed that China’s policymakers will sacrifice the yuan exchange rate to avoid a sharp correction in domestic property prices, as the latter will more significantly derail China’s economy and the financial system,” Hu wrote. That’s because the importance of the property market in the world’s second largest economy far outweighs many sectors, including the stock market. Hu compares property as a percentage of economic output to the far lighter footprint of stocks. A real estate crash in China could have far reaching consequences and it would be a long time before investors regained their confidence, according to Hu.

That will put policy makers in a very difficult position. While the government has some cards in its hand, such as an ability to control land supply and enforce curbs on new home-buying, history shows that some tightening measures risk backfiring and only stoking speculative behavior such as “panic buying” like that seen in Shanghai earlier this year. Besides, the regulator’s handling of last year’s stock market turmoil did little to inspire confidence in the government’s ability to oversee the bubbly housing market. “No bubble has a happy ending,” Hu wrote.

Someone should calculate the losses at a 25% price drop. And do 50% too. Losses for ‘owners’ and for lenders.

• Sydney Home Prices Need To Drop 25% To Help First Time Buyers (Abc)

First home buyers are facing the biggest barrier in recent history to entering the housing market, with deposits at record high levels relative to incomes in the Sydney market. Research by Deutsche Bank’s chief Australian economist Adam Boyton shows it would take a 25% drop in Sydney home prices to bring the size of deposit required back to average levels over the past 20 years. Mr Boyton studied the Sydney market because it is the biggest, has seen rapid recent price growth and has the highest housing costs in the nation. In contrast to the record deposit needed – now estimated to be almost twice the typical annual earnings of a Sydney household – rising incomes over the early 2000s and falling interest rates since the global financial crisis have seen the burden of mortgage repayments remain comparatively stable relative to income.

Mr Boyton expresses this as “borrowing power”, which has broadly increased in line with Sydney home prices, albeit with prices jumping ahead somewhat during the most recent boom. At the low point in 2003, a Sydney household with a typical income could only borrow half what a typical house cost if their repayments were to be 30% of their gross incomes. At the best points for affordability, households could comfortably afford to borrow between 60-68% of the typical Sydney house price. Currently that figure is just over 50%.

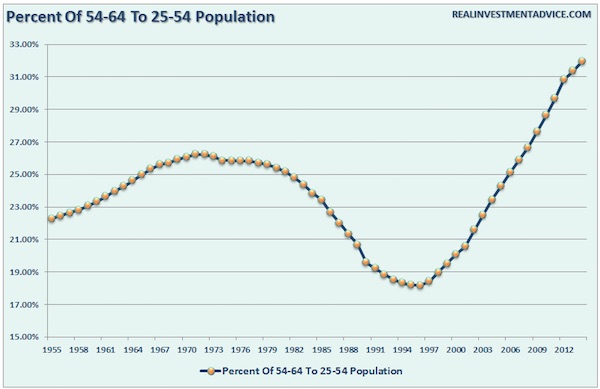

An epic clash unfolds before our eyes.

• Don’t Blame “Baby Boomers” For Not Retiring – They Can’t Afford To (Roberts)

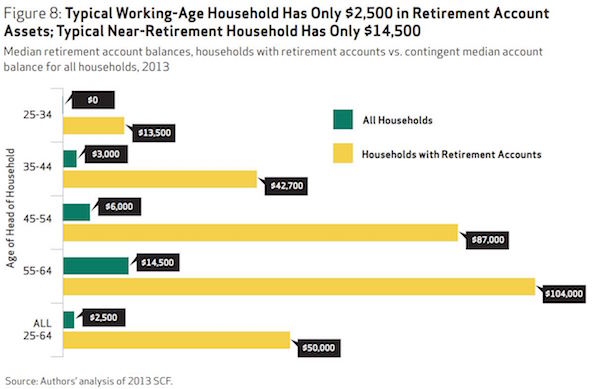

In business, the 80/20 rule states that 80% of your business will come from 20% of your customers. In an economy where more than 2/3rds of the growth rate is driven by consumption, an even bigger imbalance of the “have” and “have not’s” presents a major headwind. I have often written about the disconnect between Wall Street and Main Street. As shown in the chart below, while asset prices were inflated by continued interventions of monetary policy from the Federal Reserve, it only benefited the small portion of the population with assets invested in the market.

Cheap debt, excess liquidity and a buyback spree, led to soaring Wall Street and corporate profits, surging executive compensation and rising incomes for those in the top 10%. Unfortunately, the other 90% known as “Main Street” did not receive many benefits. This divide is clearly seen in various data and survey statistics such as the recent survey from National Institute On Retirement Security which showed the typical working-age household has only $2500 in retirement account assets. Importantly, “baby boomers” who are nearing retirement had an average of just $14,500 saved for their “golden years.”

[..] The gap between the young and elderly population has shrunk dramatically in recent years as the demographic trends have shifted. Old people are living longer and young people are delaying marriage and children. This means fewer people paying into a social welfare system, while more or taking out. Of course, the burden on the social safety net remains the 800-lb gorilla in the room no one wants to talk about. But with the insolvency of the welfare system looming in less than a decade, I am sure it will become a priority soon enough.

Of course, as we will discuss in a moment, the problem is that while the “baby boom” generation may be heading towards retirement years, there is little indication a large majority of them will be actually retiring. With a large majority of individuals being dependent on the welfare system in retirement, the burden will fall on those next in line. Welcome to the “sandwich generation” when more individuals will be “sandwiched” between supporting both parents and children in the same household. It should be no surprise multi-generational households in the U.S. are at their highest levels since the “Great Depression.”

Obama’s fist veto override?

• Saudi Lobbyists Plot New Push Against 9/11 Bill As Veto Override Looms (Pol.)

Saudi Arabia is mounting a last-ditch campaign to scuttle legislation allowing families of victims of the Sept. 11, 2001 attacks to sue the kingdom — and they’re enlisting major American companies to make an economic case against the bill. General Electric, Dow Chemical, Boeing and Chevron are among the corporate titans that have weighed in against the Justice Against Sponsors of Terrorism Act, or JASTA, which passed both chambers unanimously and was vetoed on Friday, according to people familiar with the effort. The companies are acting quietly to avoid the perception of opposing victims of terrorism, but they’re responding to Saudi arguments that their own corporate assets in the kingdom could be at risk if the law takes effect.

Meanwhile, Trent Lott, the former Senate majority leader who now co-leads Squire Patton Boggs’ lobbying group, e-mailed Senate legislative directors on Monday warning that the bill could lead other countries to withdraw their assets from the United States and retaliate with laws allowing claims against American government actions. “Many foreign entities have long-standing, intimate relations with U.S. financial institutions that they would undoubtedly unwind, to the further detriment of the U.S. economy,” reads one of the attachments, obtained by POLITICO. “American corporations with interests abroad may be at risk of retaliation, a possibility recently expressed by GE and Dow.” Still, the Saudis and their agents face a significant uphill battle, with lawmakers loath to take a vote against victims of the 9/11 attacks right before an election.

There was little public opposition to the bill as it made its way through the Capitol, and even now, efforts to tweak the bill haven’t caught much traction. Senate Majority Leader Mitch McConnell (R-Ky.) announced Monday that the Senate will vote Wednesday on a motion to override President Barack Obama’s veto, and if override advocates are successful there, the House will take the same vote Thursday or Friday, a House Republican leadership aide said. But even if Obama receives the first veto override of his presidency, the story won’t end there: the Saudis will seek a new bill to scale back the law in the lame-duck session or in the next session, after lawmakers are relieved from the heat of the campaign, people familiar with the plans said. “It’s Washington at its finest,” one of the people said.

How to kill off your own species.

• Over 90% Of World Breathing Bad Air-WHO (AFP)

Nine out of 10 people globally are breathing poor quality air, the World Health Organization said Tuesday, calling for dramatic action against pollution that is blamed for more than six million deaths a year. New data in a report from the UN’s global health body “is enough to make all of us extremely concerned,” Maria Neira, the head of the WHO’s department of public health and environment, told reporters. The problem is most acute in cities, but air in rural areas is worse than many think, WHO experts said. Poorer countries have much dirtier air than the developed world, according to the report, but pollution “affects practically all countries in the world and all parts of society”, Neira said in a statement. “It is a public health emergency,” she said.

“Fast action to tackle air pollution can’t come soon enough,” she added, urging governments to cut the number of vehicles on the road, improve waste management and promote clean cooking fuel. Tuesday’s report was based on data collected from more than 3,000 sites across the globe. It found that “92% of the world’s population lives in places where air quality levels exceed WHO limits”. The data focuses on dangerous particulate matter with a diameter of less than 2.5 micrometres, or PM2.5. PM2.5 includes toxins like sulfate and black carbon, which can penetrate deep into the lungs or cardiovascular system. Air with more than 10 microgrammes per cubic metre of PM2.5 on an annual average basis is considered substandard.

Funny little story against a very serious backdrop.

• Canadians Are Embracing Syrian Refugees. Why Can’t We? (G.)

Nobody warned the Hendawis about Canadian girls. Wadah and Raghdaa Hendawi survived the civil war in Syria, fleeing the devastation of Aleppo with their children for the relative safety of Lebanon. For three years their teenage sons missed out on an education while they worked to support the family. Then they hit the immigration jackpot – Canada. They were greeted at Halifax airport not by immigration officials or social workers, but by their sponsors – a bunch of well-meaning locals whose fundraising efforts would support the family for the next 12 months. And so the Hendawis arrived in the small fishing town of Shelburne, Nova Scotia, swaddled in new ski jackets, blinded by the winter sunshine bouncing off fresh February snow.

They were the only Syrians in the village, and had no idea what was in store for them. The Rev. Joanne McFadden knew the names and ages of the family she was helping to sponsor, but apart from that she too didn’t know what to expect. She certainly wasn’t prepared for the phone call that came three days after Saed (18), Mohamad (16) and Ahmed (15) started attending Shelburne Regional High School. I get a phone call from the principal. ‘Uhhh, Joanne, we have a problem.’ ‘What’s the problem, Mary?’ ‘Well, all the girls in the school are chasing the boys.’ This hadn’t even crossed our mind, right, that this was even a possibility. It was like, pardon me, we’ve got some things to figure out.

Home › Forums › Debt Rattle September 27 2016