MC Escher Still life and street 1937

How much longer?

• China Is Going To Hit A Wall (FuW)

Anne Stevenson-Yang, co-founder and research director at J Capital, warns that the monster bubble in the Chinese housing market is ripe to pop and that the Chinese currency will crash. There have been warnings about a bubble in China’s housing market for some time now. How hot is the real estate market? So far this year has been crazy, particularly in the area around Beijing. Just a few weeks ago I was in this little rustbelt city called Zhuozhou in the Hebei province where the steel mills are. It’s a very unpleasant place to spend time. It’s very polluted, there’s nothing to do, the food is bad and the landscape is awful. It’s just no place you want to be and yet property prices have doubled, tripled and in some places even quadrupled in a year.

What’s fueling this boom? It’s like in every property bubble: People build these stories. In Florida for example, the idea in the housing bubble was that all Americans are going to retire there. Florida has nice beaches, it’s warm and Americans are getting older, so everybody’s going to retire there. In China, the idea is that all these areas 200 miles outside of Beijing are going to be bedrooms for the working class of Beijing. So they’re going to build subways, schools, hospitals and other public facilities there and the prices are going to go up. The story goes that all these people who can’t afford to live in Beijing but work there are going to live in places like Zhuozhou instead and that they are going to take the high speed rail into Beijing. Everybody is speculating like mad but in the end nobody wants to live there.

And how are such ghost towns financed? There is probably no company that is more representative of the investment bubble than Evergrande. It’s the biggest pyramid scheme the world has yet seen. Evergrande is highly leveraged and has like 270 projects all over the country. I have been easily to 40 of them yet I have only seen one that was fully occupied. Many of these projects are megalomaniac visions and totally empty. Yet you go to these places and you see their sales room filled with young buyers. When I open my eyes I see crumbling stone and empty jungles or deserts. What they see is a future with wealthy Europeanized people strolling on modern paths. It’s just amazing. It’s a mass illusion and Evergrande more than any of these developers plays to this illusion by building developments that are specifically positioned for the investor, not to live there but to buy for some future appreciation in price.

How long can these crazy times last? I’ve been wondering that for years now. In a few places, property bubbles already have popped but the government keeps information from going out. Back in 2011 for instance, there was a property bust in the region of Ordos where most of China’s coal is. Prices dropped like 50% but if you looked at the official statistics they may have dropped 4%. Another place was in Wenzhou which is a place in China’s Zhejiang province where there is a lot of private money. After the bubble popped the central government had to go in and had to create a bailout fund. But nobody ever got information about it. In fact, all the newspapers put out information about how actually Wenzhou is fine. So will China’s housing frenzy ever come to an end at all? China is going to hit a wall. They’re not positioned to take the political pain that’s entailed by just stopping with all that madness.

So there will be a bust but it’s very hard to say exactly how long it takes. Basically, there are two paths. One of them is you break public confidence in some way. For that to happen you have to have a bank failure, a well-known investment product that doesn’t pay or some property developer that goes bust. You’ve had that locally in all sorts of places but you have to have a really big bust that everyone is aware of. And what would be the other path? The other thing that eventually has to happen is that the Chinese currency has to devalue. The reason why the developers can just keep on selling is because they keep getting refinanced. All the refinancing means that China has to keep on expanding the money supply and when you keep on expanding the money supply you have too much money and the value of the money declines. Obviously it’s not quite that simple but that’s basically what’s going on.

Nomi is asked the same question: how much longer? She thinks it could be a few years yet.

• Nomi Prins: Big Bank Concentration and Counterparty Risk Expands (DR)

Prins notes, “As we learned from the global financial crisis, the Federal Reserve has done a lousy job at regulating the risks that were coming into the financial system from the major private banks.” “Not only did it do a bad job at detecting risks, it did the opposite and deflected concerns from those highlighting the risks. From the standpoint of monetary policy, looking ten years out, its pursuit of policy with absolutely no limitation from the outside (printing money, buying securities) was a failure.” “If the Federal Reserve policies were able to make a real impact, we wouldn’t have needed them to go on for ten years following the financial crisis. What we are seeing right now is that there is no particular end in sight. The fact that there is no jurisdiction that can instruct the Fed what to do, where it is currently working under unconventional policy for artificial markets, has created more risk instead of less.”

“If we were to create an external benchmark that at the very least pulls them into some coordinated approach, that would be a better way of maintaining stability. Whether that is a standard currency approach or whatever that might be.” When speaking on how long the central banks might be able to stall and what tools in the face of another crisis Nomi Prins elaborates on her most recent research. “There has been collusion and collaboration amongst the G7 central banks. They have been ensuring that central banks like the Federal Reserve and others coordinate in their policy consortium moves. In effect we have seen a consistent global zero % interest rate policy and ongoing quantitative easing policy be unveiled, even if some banks reduce their engagement. That’s why we have been able to perpetuate this system for so long.”

“This is not one individual central bank but a coordinated, collusive approach. Can that continue? The guidance, as well as the actions of the central banks has indicated there could be multiple years of this to come. Because there is no external limitation on their policy and there’s no voting them out I’d say this could go on for at least a few more years. For the most part the people in power are going to stay in power. Even in the case of the U.S, if we were to see Janet Yellen leave and Gary Cohn step in at the Fed, I’d expect we would see much of the same.”

Control illusion.

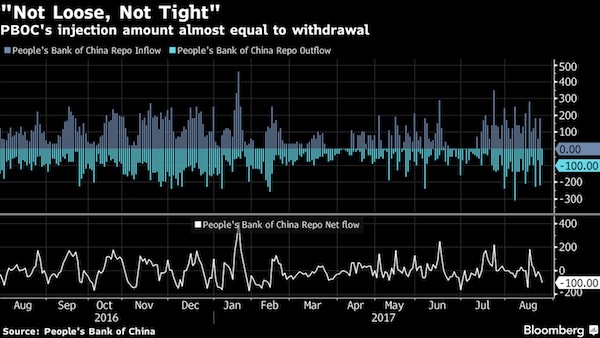

• China’s Central Bank Is Working Hard to Stand Still (BBG)

While some of the biggest central banks are agonizing over changing direction, the People’s Bank of China is working hard to stay right where it is. That’s because, as the U.S. Federal Reserve or the European Central Bank are heading into phases of tighter policy, China’s monetary authority is engaged in an increasingly complex effort to preserve the status quo while the world changes around it. According to 60 % of economists in a Bloomberg survey conducted this month, the PBOC’s broad policy stance will remain “roughly the same” through the end of 2017. It’s how they maintain the hold, though, that matters. Through the use of a wide range of monetary instruments, the PBOC is attempting to meet two seemingly conflicting goals at once – weed out excessive borrowing in the financial system while ensuring credit to an economy that’s on a long-term slowdown.

The need to maintain the balance is especially acute amid the political sensitivity around the approaching leadership transition of the 19th Party Congress in the fall. “High leverage has put the central bank in a dilemma where easing could further expand the scale of debt and where tightening pushes up interest expenses and weighs on growth,” said Wen Bin at China Minsheng Banking in Beijing. “The PBOC is using open-market monetary tools to stay flexible and strike a balance.” Achieving those aims, without a change in the benchmark lending rate, in practice means constant fine-tuning of daily conditions in the inter-bank money market. Over the past year, the PBOC has poked and prodded traders using an array of lending and cash-absorbing instruments of different maturities. Here’s that process in charts:

Using different tenors to inject and withdraw funds from markets is the practical aspect of the PBOC’s stated policy of keeping liquidity “neither tight nor loose.” Yet at the same time, for much of the past year, gradually-rising interbank rates have been desirable amid a push to stabilize debt — crimping incentives to lend short-term within the financial system, while remaining wary of choking off credit to the real economy. The PBOC’s preference for longer-dated tools such as 28-day reverse repo has raised borrowing costs. Now, as the economy may be set for deceleration in the second half of the year and some progress in debt reduction has been achieved, use of longer-dated repurchase agreements has been pared back.

“You need to either thoroughly refute every single argument against the narrative you’ve been spinning or admit publicly that you’ve been catastrophically wrong. ”

• Pundits And Politicians Are Tacitly Admitting They Lied About Russia (M.)

It has been nearly three weeks since The Nation pushed an explosive memo from the Veteran Intelligence Professionals for Sanity into mainstream consciousness with an article detailing the evidence that the DNC leaks last year could not have been the result of a Russian hack. By continuing to ignore it, the US intelligence community and all the pundits and politicians who have advanced the Russian hacking narrative are tacitly admitting that they lied. The report is unequivocal. Not only could Russian hackers not have obtained the DNC emails in the way they are alleged to have obtained them, but metadata was in fact manipulated to implicate Russia in the leak. Since publication of the viral Nation article, even more evidence has come to light showing that a hack is far more improbable even than originally suspected. This means that there is currently more publicly-available evidence indicating that Russia did not hack the DNC than there is that it did.

These earth-shattering revelations have gone all but ignored by the mainstream media, which had until the report surfaced been pummelling the American psyche with relentless fearmongering about the Great Russian Menace. The unquestioned narrative that Russia attacked American democracy in what many establishment politicians have horrifyingly labeled an “act of war” quickly transformed into ridiculous unsubstantiated claims about the Kremlin having taken over the highest levels of the US government and McCarthyite witch hunts against anyone who questioned these baseless assertions. This fact-free hysteria was used to manufacture support for new cold war escalations which remain in place to this day, threatening the existence of all life on earth.

Far from addressing the massive, gaping plot holes that have suddenly emerged in its frenzied narrative, the mass media has all but ghosted from the scene. Russia gets an occasional mention now and again, but the fever-pitch shrieking panic has unquestionably been dialed down by several orders of magnitude. This is unacceptable. You don’t get to lie to the American people for nine months, terrify them with fact-free ghost stories that their nation has been taken over by a hostile foreign body, use their terror to manufacture support for a new cold war, and then change the subject to Nazis and Joe Arpaio as soon as evidence emerges that you’ve been reporting blatant falsehoods. That is not a thing. You need to either thoroughly refute every single argument against the narrative you’ve been spinning or admit publicly that you’ve been catastrophically wrong.

You need to either (A) prove that you have not knowingly and/or unknowingly deceived the world, or (B) do everything you can to fix the damage that you have done. Until the US intelligence community, the mainstream media, and the politicians who’ve been advancing this Russian hacking narrative do one of these two things, their silence on the matter should be interpreted as a tacit admission that they’ve been lying to us this entire time. After Iraq there was already no reason to give these institutions the benefit of the doubt, and since the VIPS report there is every reason in the world to believe that they’ve been lying to advance domestic and foreign agendas. They either refute the VIPS report in its entirety, or we must treat their refusal to do so as a tacit admission of nothing less than a crime against humanity.

I like Taibbi. He’s a good writer. But he’s gotten awkwardly close to the whole anti-Trump frenzy. Suggesting that CNN has been covering Trump ‘responsibly’ is simply not credible. See article above. CNN et al go after Trump because it’s profitable in the echo chamber. Where it doesn’t matter whether what you say is true.

• The Media Is the Villain – for Creating a World Dumb Enough for Trump (Taibbi)

No news director would turn off the feed in the middle of a Trump-meltdown. This presidency has become the ultimate ratings bonanza. Trump couldn’t do better numbers if he jumped off Mount Kilimanjaro carrying a Kardashian. This was confirmed this week by yet another shruggingly honest TV executive – in this case Tony Maddox, head of CNN International. Maddox said CNN is doing business at “record levels.” He hinted also that the monster ratings they’re getting have taken the sting out of being accused of promoting fake news. “[Trump] is good for business,” Maddox said. “It’s a glib thing to say. But our performance has been enhanced during this news period.” Maddox, speaking at the Edinburgh TV festival, added that most of the outlets that have been singled out by Trump are doing a swimming business.

“If you look at the groups that Trump has primarily targeted: CNN, The New York Times, The Washington Post, Saturday Night Live, Stephen Colbert,” he said, “every single one of those has seen a quite remarkable growth in their viewing figures, in their sales figures.” Everyone hisses whenever they hear quotes like these. They recall the infamous line from last year by CBS chief Les Moonves, about how Trump “may not be good for America, but he’s damn good for CBS.” Moonves was even cheekier than Maddox. He laughed and added, “The money’s rolling in, and this is fun. They’re not even talking about issues, they’re throwing bombs at each other, and I think the advertising reflects that.” For more than two years now, it’s been obvious that Donald Trump is a disaster on almost every level except one – he’s great for the media business.

Most of us who do this work have already gone through the process of working out just how guilty we should or should not feel about this. Many execs and editors – and Maddox seems to fall into this category – have convinced themselves that the ratings and the money are a kind of cosmic reward for covering Trump responsibly. But deep down, most of us know that’s a lie. Donald Trump gets awesome ratings for the same reason Fear Factor made money feeding people rat-hair tortilla chips: nothing sells like a freak show. If a meteor crashes into jello night at the Playboy mansion, it doesn’t matter if you send Edward R. Murrow to do the standup. Some things sell themselves.

All you need is the power to print money.

• The 5 Steps to World Domination (CHS)

1. Turn everything into a commodity that can be traded on the global market: land, leases on land, options to purchase land, houses, buildings, rooms in slums, labor, tools, robots, water, water rights, mineral rights, rights to air routes, ships, aircraft, political power, shares in corporations, government bonds, municipal bonds, corporate bonds, student loans that have been bundled into debt-based instruments, the income from city parking meters, electricity, software, advertising, marketing, media, social media, food, energy, insurance, gold, metals, credit, interest-rate swaps and last but not least, financial instruments that control and/or pyramid all the real-world goods and assets that have been commoditized (i.e. almost everything).

Why is this the essential first step in World Domination? Once something has been commoditized, it can be bought and sold in the global marketplace in fiat currencies–currencies that are not backed by any real-world asset and that can be created out of thin air by central and private banks. You see the dynamic, right? Create credit-currency out of thin air, and then use this “free money” to buy up the real world. Quite a trick, isn’t it? Get a means of exchange for essentially nothing (i.e. money at near-zero interest rates) and then trade this for assets that produce goods and services everyone else needs or wants. Now we understand steps 2 and 3:

2. Enable private banks to create money out of thin air via fractional reserve banking. You know the drill: banks can issue $15 in new loans for every $1 in cash they hold in reserve. (Depending on the current regulations, it might as little as $10 or as much as $35 that can be created and lent out for every $1 held in cash reserve.) In the current zero-interest rate environment, this new money can be borrowed for near-zero carrying costs by corporations and financiers.

3. Establish a central bank with essentially unlimited ability to bring money into existence and use it to backstop the private banking sector. If the private banks get in trouble, no problem, the central bank is there to bail them out with unlimited lines of credit and an unlimited ability to create new money.

4. Undermine/destroy local economies’ ability to organize production and consumption without using credit and fiat currencies (i.e. money controlled and issued by central and private banks). Trading goods on barter? Get rid of that. Using social ties rather than cash or bank credit to organize production and consumption? Eliminate that capability. Locally issued currencies? That’s against the law. Using cash? bad, very bad–everyone must use banks and bank credit instead. Once these four steps are in place, the 5th step is easy:

5. Buy up all the productive assets and income streams of the world with nearly free credit-money. No saver can compete with corporations and financiers with access to billions of dollars in nearly-free credit-money. It doesn’t matter if you earn $1,000 or $100,000 a year–you will be outbid.

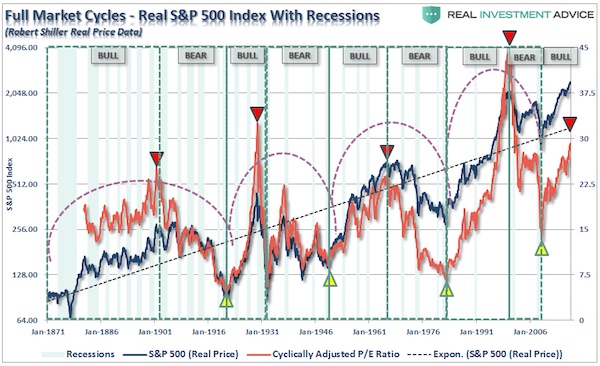

Too much focus on Buffett. Like there was on Greenspan.

• Pure Rubbish? What The Buffett Indicator Is Really Predicting (Roberts)

While we are indeed currently in a very bullish trend of the market, there are two halves of every market cycle. “In the end, it does not matter IF you are ‘bullish’ or ‘bearish.’ The reality is that both ‘bulls’ and ‘bears’ are owned by the ‘broken clock’ syndrome during the full-market cycle. However, what is grossly important in achieving long-term investment success is not necessarily being ‘right’ during the first half of the cycle, but by not being ‘wrong’ during the second half.” Will valuations currently pushing the 3rd highest level in history, it is only a function of time before the second-half of the full-market cycle ensues. That is not a prediction of a crash. It is just a fact.

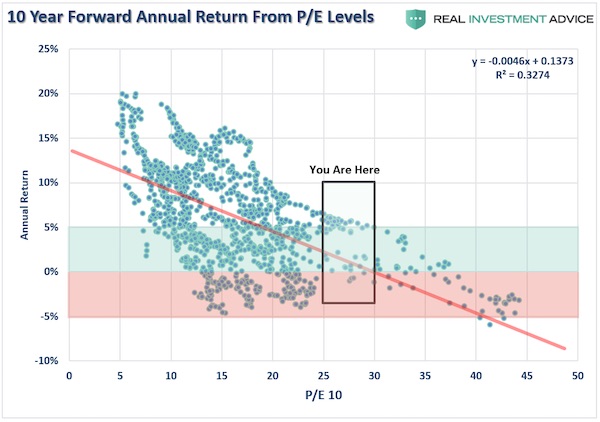

[..] valuations DO NOT predict market crashes. Valuations are predictive of future returns on investments from current levels. Period. I recently quoted Cliff Asness on this issue in particular: “Ten-year forward average returns fall nearly monotonically as starting Shiller P/E’s increase. Also, as starting Shiller P/E’s go up, worst cases get worse and best cases get weaker. If today’s Shiller P/E is 22.2, and your long-term plan calls for a 10% nominal (or with today’s inflation about 7-8% real) return on the stock market, you are basically rooting for the absolute best case in history to play out again, and rooting for something drastically above the average case from these valuations.” We can prove that by looking at forward 10-year total returns versus various levels of PE ratios historically.

“Ordinarily, failure to raise the debt ceiling would lead to a government shut-down, including hurricane recovery operations, unless the president invoked some kind of emergency powers.”

• When the Butterfly Flaps Its Wings (Jim Kunstler)

It remains to be seen what the impact will be from Mother Nature putting the nation’s fourth largest city out-of-business. And for how long? It’s possible that Houston will never entirely recover from Hurricane Harvey. The event may exceed the physical damage that Hurricane Katrina did to New Orleans. It may bankrupt large insurance companies and dramatically raise the risk of doing business anywhere along the Gulf and Atlantic coasts of the USA — or at least erase the perceived guarantee that losses are recoverable. It may even turn out to be the black swan that reveals the hyper-fragility of a US-driven financial system.

Houston also happens to be the center of the US oil industry. Offices can be moved elsewhere, of course, but not so easily the nine major oil refineries that sprawl between Buffalo Bayou over to Beaumont, Port Arthur, and then Lake Charles, Louisiana. Harvey is inching back out to the Gulf where it will inhale more energy over the warm ocean waters and then return inland in the direction of those refineries. The economic damage could be epic. Much of the supply for the Colonial Pipeline system emanates from the region around Houston, running through Atlanta and clear up to Philadelphia and New York. There could be lines at the gas stations along the eastern seaboard in early September.

The event is converging with the US government running out of money this fall without new authority to borrow more by congress voting to raise the US debt ceiling. Perhaps the emergency of Hurricane Harvey and its costly aftermath will bludgeon congress into quickly raising the debt ceiling. If that doesn’t happen, and the debt ceiling is not raised, the federal government might have to pretend that it can pay for emergency assistance to Texas and Louisiana. That pretense can only go so far before government contractors balk and maybe even walk.

Ordinarily, failure to raise the debt ceiling would lead to a government shut-down, including hurricane recovery operations, unless the president invoked some kind of emergency powers. That would be decisive action, but it could also be the beginning of something that looks like a full-out dictatorship. Powers assumed are often not surrendered when the original emergency is over. And what would the president use for money if a substantial enough number of congresspersons and senators are prompted by their distaste for Mr. Trump to drag out the process of financially re-liquefying the government? (And nevermind even passing a budget.)

Kabuki theater for the home front. Empty nonsense.

• France, Germany, Italy, Spain Agree on Plan to Stem Migration Flows (BBG)

France, Germany, Italy and Spain agreed a plan to stem migration across the Mediterranean at talks with Libya, Chad and Niger in Paris, as summit host President Emmanuel Macron called for asylum seekers to be processed on African soil. Safe zones should be set up in Chad and Niger to “identify” asylum seekers in Africa, under the supervision of the United Nations High Commissioner for Refugees, Macron told reporters after the talks in the Elysee Palace Monday. “There’s a lot of work to be done, but I think we have a framework in which we can move forward,” German Chancellor Angela Merkel said at the briefing.

Leaders said in a joint statement that they would work with countries of origin and transit to boost the fight against smuggler networks. France, Germany, Italy and Spain stressed their commitment “to stopping irregular migration flows well ahead of the Mediterranean coast.” In reaction to reports about poor humanitarian conditions in refugee camps in Libya, leaders also promised to set up “facilities with adequate humanitarian standards” for refugees stranded there. France, Germany and Spain remained committed to giving further help to Italy – which has often complained in the past that it was left alone to cope with the migrant flows – by stepping up relocations and appropriately staffing the European Union’s Frontex border management force, they said.

Maybe Greece’s best hope is for Merkel to dump him.

• Debt Cut For Greece Not On Agenda For Now, Schaeuble Says (R.)

Greece must press ahead with implementing its reforms-for-aid program and become more competitive, German Finance Minister Wolfgang Schaeuble was quoted as saying, adding that debt relief for Athens was “currently” not on the agenda. Eurozone finance ministers and the IMF reached an agreement on Greece in June, paving the way for new emergency loans for Athens while leaving the contentious issue of debt relief for later. Asked in an interview with the newspaper Mannheimer Morgen if he could envisage a partial cut in debt for Greece, Schaeuble said, “That’s currently not on the agenda at all.” Chancellor Angela Merkel and Schaeuble do not want to discuss any details of debt relief for Greece before federal elections on September 24, in which the far-right euro-skeptic AfD party is forecast to enter parliament for the first time.

Starting a discussion about debt relief would send the wrong signal to Athens at a time when the economy was doing better and recovering, Schaeuble told Mannheimer Morgen. “The country doesn’t need a debt cut now, but it must continually work on its competitiveness,” Schaeuble said. He pointed out that Greece’s borrowing costs for the next 10 to 15 years were already relatively low. “Above all, as long as member states are responsible for financial and economic policy, they must also bear the consequences of their own decisions themselves”, he said. Schaeuble, whose insistence on reforms to public finances in Athens have long made him a hate figure for many Greeks, has signaled his readiness to deepen eurozone integration as long as risks and liabilities arising from political decisions remain linked.

Merkel’s conservative Christian Democrats are leading the center-left Social Democrats by about 15 percentage points in opinion polls and are the heavy favorites to retain power after the election. Schaeuble, who has been finance minister since 2009 and will turn 75 on September 18, has signaled his willingness to continue as finance minister. But Merkel could be forced to sacrifice him to secure a coalition deal.

Strange innuendo-laced piece from NYT. It’s all they do these days. “While the Europeans are acting towards Greece like medieval leeches, the Chinese keep bringing money..” Varoufakis made a deal with China in spring 2015. Merkel called Beijing to say: keep your hands off. That should have been part of this article.

• Chastised by EU, a Resentful Greece Embraces China’s Cash and Interests (NYT)

After years of struggling under austerity imposed by European partners and a chilly shoulder from the United States, Greece has embraced the advances of China, its most ardent and geopolitically ambitious suitor. While Europe was busy squeezing Greece, the Chinese swooped in with bucket-loads of investments that have begun to pay off, not only economically but also by apparently giving China a political foothold in Greece, and by extension, in Europe. Last summer, Greece helped stop the European Union from issuing a unified statement against Chinese aggression in the South China Sea. This June, Athens prevented the bloc from condemning China’s human rights record. Days later it opposed tougher screening of Chinese investments in Europe.

Greece’s diplomatic stance hardly went unnoticed by its European partners or by the United States, all of which had previously worried that the country’s economic vulnerability might make it a ripe target for Russia, always eager to divide the bloc. Instead, it is the Chinese who have become an increasingly powerful foreign player in Greece after years of assiduous courtship and checkbook diplomacy. Among those initiatives, China plans to make the Greek port of Piraeus the “dragon head” of its vast “One Belt, One Road” project, a new Silk Road into Europe. When Germany treated Greece as the eurozone’s delinquent, China designated a recovery-hungry Greece its “most reliable friend” in Europe. “While the Europeans are acting towards Greece like medieval leeches, the Chinese keep bringing money,” said Costas Douzinas, the head of the Greek Parliament’s foreign affairs and defense committee and a member of the governing Syriza party.

China has already used its economic muscle to stamp a major geopolitical footprint in Africa and South America as it scours the globe for natural resources to fuel its economy. If China was initially welcomed as a deep-pocketed investor — and an alternative to America — it has faced growing criticism that it is less an economic partner than a 21st-century incarnation of a colonialist power. If not looking for natural resources in Europe, China has for years invested heavily across the bloc, its largest trading partner. Yet now concerns are rising that Beijing is using its economic clout for political leverage. Mr. Douzinas said China had never explicitly asked Greece for support on the human rights vote or on other sensitive issues, though he and other Greek officials acknowledge that explicit requests are not necessary. “If you’re down and someone slaps you and someone else gives you an alm,” Mr. Douzinas said, “when you can do something in return, who will you help, the one who helped you or the one who slapped you?”

We need Kenya to show us how to do this?!

• Kenya Gets World’s Toughest Plastic Bag Ban: 4 Years Jail Or $40,000 Fine (R.)

Kenyans producing, selling or even using plastic bags will risk imprisonment of up to four years or fines of $40,000 (£31,000) from Monday, as the world’s toughest law aimed at reducing plastic pollution came into effect. The east African nation joins more than 40 other countries that have banned, partly banned or taxed single use plastic bags, including China, France, Rwanda, and Italy. Many bags drift into the ocean, strangling turtles, suffocating seabirds and filling the stomachs of dolphins and whales with waste until they die of starvation. “If we continue like this, by 2050, we will have more plastic in the ocean than fish,” said Habib El-Habr, an expert on marine litter working with the UN environment programme in Kenya.

Plastic bags, which El-Habr says take between 500 to 1,000 years to break down, also enter the human food chain through fish and other animals. In Nairobi’s slaughterhouses, some cows destined for human consumption had 20 bags removed from their stomachs. “This is something we didn’t get 10 years ago but now it’s almost on a daily basis,” said county vet Mbuthi Kinyanjui as he watched men in bloodied white uniforms scoop sodden plastic bags from the stomachs of cow carcasses. Kenya’s law allows police to go after anyone even carrying a plastic bag. But Judy Wakhungu, Kenya’s environment minister, said enforcement would initially be directed at manufacturers and suppliers.[..] Kenya is a major exporter of plastic bags to the region.