Unknown Kewpee Hotels hamburger stand 1930

The very definition of lowballing.

• Too-Big-to-Fail Banks Face Up to $870 Billion Capital Gap (Bloomberg)

Too big to fail is likely to prove a costly epithet for the world’s biggest banks as regulators demand they increase debt securities to cover losses should they collapse. The shortfall facing lenders from JPMorgan Chase to HSBC could be as much as $870 billion, according to estimates from AllianceBernstein, or as little as $237 billion forecast by Barclays. The range is so wide because proposals from the Basel-based Financial Stability Board outline various possibilities for the amount lenders need to have available as a portion of risk-weighted assets. With those holdings in excess of $21 trillion at the lenders most directly affected, small changes to assumptions translate into big numbers.

“The direction is clear and it is clear that we are talking about huge amounts,” said Emil Petrov, who heads the capital solutions group at Nomura in London. “What is less clear is how we get there. Regulatory timelines will stretch far into the future but how quickly will the market demand full compliance?” The FSB wants to limit the damage the collapse of a major bank would inflict on the world economy by forcing them to hold debt that can be written down to help recapitalize an insolvent lender. For senior bonds to suffer losses under present rules the institution has to enter bankruptcy, a move that would inflict huge damage on the financial system worldwide if it happened to a global bank.

And counting.

• Richest 1% Of People Own Nearly 50% Of Global Wealth (Guardian)

The richest 1% of the world’s population are getting wealthier, owning more than 48% of global wealth, according to a report published on Tuesday which warned growing inequality could be a trigger for recession. According to the Credit Suisse global wealth report, a person needs just $3,650 – including the value of equity in their home – to be among the wealthiest half of world citizens. However, more than $77,000 is required to be a member of the top 10% of global wealth holders, and $798,000 to belong to the top 1%. “Taken together, the bottom half of the global population own less than 1% of total wealth. In sharp contrast, the richest decile hold 87% of the world’s wealth, and the top%ile alone account for 48.2% of global assets,” said the annual report, now in its fifth year.

The report, which calculates that total global wealth has grown to a new record – $263tn, more than twice the $117tn calculated for 2000 – found that the UK was the only country in the G7 to have recorded rising inequality in the 21st century. Its findings were seized upon by anti-poverty campaigners Oxfam which published research at the start of the year showing that the richest 85 people across the globe share a combined wealth of £1tn, as much as the poorest 3.5 billion of the world’s population. “These figures give more evidence that inequality is extreme and growing, and that economic recovery following the financial crisis has been skewed in favour of the wealthiest. In poor countries, rising inequality means the difference between children getting the chance to go to school and sick people getting life saving medicines,” said Oxfam’s head of inequality Emma Seery.

This is how we’re making the poor our bitches. Even more than they have always been. It’s warfare.

• Poor Nations ‘Pushed Into New Debt Crisis’ (Guardian)

A sharp rise in lending to the world’s poorest countries will leave them with crippling debt payments over the next decade, a few years after many had loans written off, a report has warned. The Jubilee Debt Campaign said as many as two-thirds of the 43 developing countries it analysed could suffer large increases in the share of government income spent on debt payments over the next decade. Coinciding with the World Bank’s annual meeting in Washington, the anti-poverty campaigners accuse the international lender and other public bodies of “leading the lending boom” to poor countries without checking how repaying debts will divert resources from cutting poverty. The report highlights that for 43 poor countries, half of lending is from multilateral institutions such as the International Monetary Fund, World Bank and African Development Bank. Total lending to the group of poor countries has increased by 60% from $11.4bn (£7.1bn) a year in 2009 to $18.5bn in 2013.

“There is a real risk that today’s lending boom is sowing the seeds of a new debt crisis in the developing world, threatening to reverse recent gains in the fight against poverty and inequality,” said Sarah-Jayne Clifton, director of the Jubilee Debt Campaign. “The shocking thing is that public bodies like the World Bank are leading the lending boom, not just reckless private lenders hunting for returns.” The campaigners are calling for measures to make lending more responsible and for aid-giving to be shifted away from bodies like the World Bank that give loans towards sources that give it in the form of grants. The analysis uses IMF and World Bank data on developing country debts and projects the cost of payments under the following three scenarios: predictions of continuous high economic growth are realised; estimates of one economic shock over the next decade prove correct; and economic growth is lower than the standard prediction.

Even if high growth rates are achieved, 11 of the 43 poor countries would still see the share of government income spent on debt payments increase rapidly, or by more than five percentage points of government revenue, the report says. Under the second scenario, 25 countries are at risk. That rises to 29 countries under the third. The report highlights that aside from the rise in lending, on the other side of the equation government revenues are not rising to keep pace with repayments. As such, the campaigners are urging the UK government to push for policies that support developing countries in increasing their tax revenues by clamping down on tax avoidance and evasion.

“Back in July, Goldman Sachs estimated that U.S. shale producers needed $85 a barrel to break even. That’s about where we are right now. The futures market points to even lower prices next year, with contracts for oil next April trading at about $82 a barrel.”

• US Oil Producers Could Drill Their Way Into Oblivion (BW)

Remember the fall of 2008? As the world spun out of control and the price of everything crashed, a barrel of oil lost 70% of its value over about five months. Of course, prices never should’ve been as high as $146 that summer, but they shouldn’t have crashed to $40 by the end of that year either. As the oil market has recovered, there have since been three major corrections, when prices have fallen at least 15% over a few months. We’re now in the midst of a fourth, with oil prices down more than 20% since peaking in late June at around $115 a barrel. They’re now hovering in the mid-$80 range and could certainly go lower. That’s good news for U.S. consumers, who are finally starting to reap the rewards of the shale boom through low gasoline prices. But it could spell serious trouble for a lot of oil producers, many of whom are laden with debt and exaggerating their oil reserves. In a way, oil companies in the U.S. are perpetuating the crash by continuing to drill and push up U.S. oil production to its fastest pace ever.

Rather than pulling back in hopes of slowing the amount of supply on the market to try and boost prices, drillers are instead operating at full tilt and pumping oil as fast as they can. Just look at the number of horizontal rigs in the field: Over the past five years, the amount of horizontal rigs deployed in the U.S. has almost quadrupled, from 379 in early 2009 to more than 1,300 today. This is of course purely a fracking story. Almost all the recent gains in U.S. oil production are the result of horizontal drilling techniques being used across much of the Midwest, from Texas to North Dakota. Unlike conventional vertical wells, where more wells do not always equal more oil, the strategy in a shale field appears to be to drill as many as possible to unlock oil trapped in rock formations. As the number of horizontal drill rigs has exploded, the number of vertical rigs in the U.S. has gone in the opposite direction, falling almost 70% over the past seven years.

So will U.S. oil producers frack their way into bankruptcy? That’s a real possibility now. They’ve certainly gotten more efficient at drilling, and don’t need the same price they did to remain profitable. But we’re getting pretty close. Back in July, Goldman Sachs estimated that U.S. shale producers needed $85 a barrel to break even. That’s about where we are right now. The futures market points to even lower prices next year, with contracts for oil next April trading at about $82 a barrel. Certainly, some producers need higher prices than others. Those at the bottom of the cost curve could benefit from a potential wave of bankruptcy that spreads across the oil patch; they could then scoop up some assets on the cheap.

“Several big, smart commodity hedge funds said oil is going to zero …”

• Speculators Push Oil Into Bear Market as Supply Rises (Bloomberg)

Money managers reduced bets on rising oil prices by the most in five weeks, helping push U.S.- traded futures into a bear market. Hedge funds and other large speculators lowered net-long positions in West Texas Intermediate crude by 4.8% in the seven days ended Oct. 7, U.S. Commodity Futures Trading Commission data show. Short positions climbed 8%, the most in almost a month. WTI joined Brent, the European benchmark, in falling more than 20% from its June peak, meeting a common definition of a bear market. U.S. oil inventories rose the most since April in the week ended Oct. 3 as domestic production rose to a 28-year high and refineries shut units for maintenance. Demand nationwide will slip this year to the lowest since 2012, the government predicted Oct. 7. “The extended decline is compounded mainly by supply-driven concerns,” Harry Tchilinguirian, BNP Paribas SA’s London-based head of commodity markets strategy, said in an interview in New York on Oct. 10. “The U.S. is not short of crude oil.”

U.S. crude stockpiles climbed by 5.02 million barrels to 361.7 million in the seven days ended Oct. 3, according to the Energy Information Administration. Weekly production averaged 8.88 million barrels a day, the highest since March 1986. “Several big, smart commodity hedge funds said oil is going to zero,” Seth Kleinman, Citigroup’s global head of energy strategy, said Oct. 7 at the Energy Department’s Winter Energy Outlook Conference in Washington. “They are being somewhat dramatic, but they were incredibly bearish.” Output will climb to 9.5 million barrels a day next year, the most since 1970, the EIA estimated Oct 7. Production is surging as a combination of horizontal drilling and hydraulic fracturing, or fracking, unlocks supplies from shale formations. Refineries processed 15.6 million barrels a day of crude in the week ended Oct. 3, down from 16.6 million in July, according to the EIA. U.S. refiners schedule maintenance for September and October as they transition to winter from summer fuels.

If you don’t understand what inflation is, how can you do what’s needed to influence it? What’s more, why are you trying in the first place?

• Bond Market Convinced Fed Inflation Goal Unreachable This Decade (Bloomberg)

When it comes to spurring inflation in the U.S. economy, the bond market is becoming convinced that the Federal Reserve has almost no chance of achieving its 2% target before the end of the decade. Inflation expectations have plummeted in the past three months, with yields of Treasuries implying consumer prices will rise an average 1.5% annually through the third quarter of 2019. In the past decade, those predictions have come within 0.1 percentage point of the actual rate of price increases in the following five years, data compiled by Bloomberg show. Even after the Fed inundated the economy with more than $3.5 trillion since 2008, bond traders are showing little fear of inflation. That may help influence U.S. monetary policy and make it harder for Fed officials to raise interest rates from close to zero as global growth weakens and the International Monetary Fund points to disinflation as a more imminent concern.

“The longer inflation rates stay below their targets, the longer the Fed’s going to stay on hold,” Gregory Whiteley, a money manager at DoubleLine Capital, said. “The burden of proof is more on the hawks and the people arguing for a rise in rates. They’re the people who have to make the case.” As the Fed winds down the most-aggressive stimulus measures in its 100-year history, the debate has intensified over how soon the central bank needs to raise rates and whether the shift will herald the long-awaited bear market in bonds. While Dallas Fed President Richard Fisher and Philadelphia Fed’s Charles Plosser dissented at the bank’s last meeting and have both warned that keeping rates too low for too long may trigger excessive inflation, the bond market’s predictive power helps to explain why U.S. government debt remains in demand. Instead of falling, as just about every Wall Street prognosticator predicted at the start of the year, Treasuries have returned 5.1% in 2014. The gains have outstripped U.S. stocks, gold and commodities this year.

“When economic inequality translates into political inequality – as it has in large parts of the US – governments pay little attention to the needs of those at the bottom.”

• America’s GDP Fetishism Is A Rare Luxury In An Age Of Vulnerability (Stiglitz)

Two new studies show, once again, the magnitude of the inequality problem plaguing America. The first, the US Census Bureau’s annual income and poverty report, shows that, despite the economy’s supposed recovery from the recession, ordinary Americans’ incomes continue to stagnate. Median household income, adjusted for inflation, remains below its level a quarter-century ago. It used to be thought that America’s greatest strength was not its military power but an economic system that was the envy of the world. But why would others seek to emulate an economic model by which a large proportion – even a majority – of the population has seen their income stagnate while incomes at the top have soared? A second study, the United Nations development programme’s human development report 2014, corroborates these findings. Every year, the UNDP publishes a ranking of countries by their human development index (HDI), which incorporates other dimensions of wellbeing besides income, including health and education.

America ranks fifth according to HDI, below Norway, Australia, Switzerland, and the Netherlands. But when its score is adjusted for inequality, it drops 23 spots – among the largest such declines for any highly developed country. Indeed, the US falls below Greece and Slovakia, countries that people do not typically regard as role models or as competitors with the US at the top of the league tables. The report emphasises another aspect of societal performance: vulnerability. It points out that while many countries succeeded in moving people out of poverty, the lives of many are still precarious. A small event – say, an illness in the family – can push them back into destitution. Downward mobility is a real threat, while upward mobility is limited. In the US, upward mobility is more myth than reality, whereas downward mobility and vulnerability is a widely shared experience. This is partly because of the US healthcare system, which still leaves poor Americans in a precarious position, despite Barack Obama’s reforms.

Those at the bottom are only a short step away from bankruptcy with all that that entails. Illness, divorce, or the loss of a job often is enough to push them over the brink. The 2010 Patient Protection and Affordable Care Act (or “Obamacare”) was intended to ameliorate these threats – and there are strong indications that it is on its way to significantly reducing the number of uninsured Americans. But, partly owing to a supreme court decision and the obduracy of Republican governors and legislators, who in two dozen US states have refused to expand Medicaid (insurance for the poor) – even though the federal government pays almost the entire tab – 41 million Americans remain uninsured. When economic inequality translates into political inequality – as it has in large parts of the US – governments pay little attention to the needs of those at the bottom.

No doubt there.

• Thiel: We Are In A Government Bubble Of Massive Size (CNBC)

Silicon Valley venture capitalist Peter Thiel told CNBC on Monday that we are in a “government bubble of massive size,” and that the bond market is the most distorted of all the markets. In a wide-ranging interview on CNBC’s “Squawk on the Street,” Thiel also spoke about tech investing, the PayPal-eBay split, Alibaba, cybersecurity and Elon Musk. “I think the thing that is most distorted is the bond market and fixed income, and perhaps less on the equity side, but we certainly are back on a government bubble of massive size,” he said. Tech stocks are quite a different story, he added. “They’re somewhat overvalued but that’s not the core of the insanity,” he said. “Tech investors always overrate growth and always underrate durability. You can measure growth but you can’t measure durability.”

He said he thinks Airbnb is undervalued. “If I had to bet on one that would be the next hundred-billion- dollar company it would be Airbnb and the consumer space,” Thiel said. “It’s a giant market and it keeps growing very fast. Investors are very biased towards things that they understand.” He said that since investors tend to drive around in black cars and stay in five-star hotels, they are more comfortable with Uber than with a couch or house-sharing service. For that reason, he said, “Uber is overvalued, Airbnb is undervalued.” On the recently announced plan to split PayPal from eBay, Thiel said the companies have gone separate ways. “It makes sense for them to naturally spin it out again and for PayPal to focus 100% on payments,” he said.

Two curiously overlapping pieces by Ambrose Evans-Pritchard, who’s been talking with Beppe Grillo’s right hand behind the scenes man Gianroberto Casaleggio. Interestingly, Ambrose is losing his former aggressive tone vs Grillo and the Cinque Stelle, though he still calls them Italy’s UKIP. They are not.

• The Great Lira Revolt Has Begun In Italy (AEP)

The die is cast in Italy. Beppe Grillo’s Five Star movement has launched a petition to drive for Italian withdrawal from Europe’s monetary union and for the restoration of economic sovereignty. “We must leave the euro as soon as possible,” said Mr Grillo, speaking at a rally over the weekend. “Tonight we are launching a consultative referendum. We will collect half a million signatures in six months – a million signatures – and we will take our case to parliament, and this time thanks to our 150 legislators, they will have to talk to us.” Ever since the pugnacious comedian burst on the political scene, the eurozone elites have comforted themselves that the party is not really Eurosceptic at heart, and certainly does not wish bring back the lira. This illusion has been shattered. A referendum itself would not be binding, but a “law of popular initiative” certainly would be. For the first time, a process is underway in Italy that will set off a national debate on monetary union and may force a vote on EMU membership that cannot easily be controlled.

Gianroberto Casaleggio, the party’s co-founder and economic guru, told me today that the Five Star Movement – or Cinque Stelle – had set out its demands in May, calling for the creation of Eurobonds to back up EMU, as well as the abolition of the EU Fiscal Compact. “Five months have gone by and we have had no reply. They have totally ignored us,” he said. The Fiscal Compact is economic insanity. It would force Italy to run massive fiscal surpluses for decades. These would cause an even deeper depression, pushing the debt ratio even higher, and would therefore be scientifically self-defeating. Historians will issue a damning verdict on the scoundrels who foisted this atrocity on Europe. My own view is that Italy could not restore viability within EMU even if Germany agreed to the two conditions (an impossible idea). It is already too late for that. Italy has lost 40pc in unit labour cost competitiveness against Germany since the Deutsche Mark and the lira were fixed in perpetuity in the mid 1990s.

What I also find interesting is that nobody ever mentions that Grillo is a trained accountant.

• Beppe Grillo Demands Euro Referendum As Italy’s Depression Drags On (AEP)

Italy’s Five Star Movement has launched a petition drive for withdrawal from the euro to lift the country out of depression and protect Italian democracy, a dramatic turn for a country that was passionately pro-European for sixty years. “We must leave the euro as soon as possible,” said Beppe Grillo, the combative comedian-politician and founder of the protest party that swept into Italy’s parliament last year with 26pc of the vote. “We will collect half a million signatures in six months – a million signatures – and we will take our case to parliament, and this time thanks to our 150 legislators, they will have to talk to us.” Gianroberto Casaleggio, the party’s economic strategist, said the movement had set out its minimum demands in May, calling for Eurobonds and the abolition of the EU Fiscal Compact, a straitjacket that will force Italy into decades of debt-deflation. “Five months have gone by and we have had no reply. They have totally ignored us,” he said.

Any referendum would not be binding but the party may be able to push through a “law of popular initiative” if eurosceptics in other parties join forces. Italians have become bitterly disenchanted with Europe after a 9pc fall in GDP over the last five and a half years, and a 24pc fall in industrial output. Most voters think it was a mistake to join the euro but are wary of withdrawal, fearing that a return to the lira would risk a crippling crisis. Even so Datamedia Ricerche poll in March found that 59pc would view a return to the lira as a good idea. Italy’s GDP has fallen back to levels first reached fourteen years ago, a catastrophic reversal unseen in any major country in modern times, even during the 1930s. It has lost 40pc in labour competitiveness against Germany since the mid-1990s, and is now trapped inside EMU with an over-valued exchange. It cannot cut easily cut wages with an “internal devalution” because this would cause havoc for debt dynamics.

Lip service.

• ECB Dark Room Crunches Bank-Test Data Amid D-Day Nerves (Bloomberg)

Deep in the European Central Bank’s Frankfurt headquarters, there’s a room sealed off from the world. In the Dark Room, as it’s referred to internally, staffers are combing through almost 39,000 points of data on the euro area’s 130 biggest banks before the results of the ECB’s Comprehensive Assessment are released on Oct. 26. The security precautions – no Internet connection or external phone lines – being taken are part of a plan to ensure that “Disclosure Day” arrives without leaks, lawsuits or glitches. When it starts to supervise euro-zone banks on Nov. 4, the ECB will embark on its biggest new mission since the introduction of the single currency, one that also poses the biggest threat to its reputation. The challenge between now and then is to publish the results of its year-long bank audit and convince the world that it’s tougher, fairer and more credible than any test that came before.

“The ECB understands that they’ve only got one chance at getting this right, and if they don’t their reputation will be severely damaged,” said Christian Thun, a senior director at Moody’s Analytics in Frankfurt. “It has been a massive undertaking, but I think they will achieve their aim of restoring confidence in the banking system.” The Comprehensive Assessment started in October 2013 as a way to ensure that when the ECB became the euro zone’s single supervisor it would know exactly what it was dealing with. Since then, at least 25 million data points have been collected on credit files, collateral and provisioning. This knowledge of asset quality has been fed into a stress test, an innovation the ECB says makes this better than previous tests run by the European Banking Authority. Banks will be required to show that their ratio of capital to risk-weighted assets can remain above 8% under current circumstances, and above 5.5% over three years after a hypothetical recession and bond-market collapse.

Germany’s troubles run the gamut, all the way into the political arena, and they run much deeper than anyone thought mere weeks ago.

• German Investor Morale Falls Sharply As Contraction Looms (CNBC)

German investor morale fell sharply in October, new data showed on Tuesday, raising fears that the euro zone engine could contact in the third quarter of 2014. Germany’s ZEW index of economic sentiment fell into negative territory for the first time since November 2012 as pessimism mounted over the outlook for the euro zone’s largest economy. The ZEW index fell to -3.6 points versus 6.9 points in September. The euro fell to a day’s low of $1.2666 following the data. ZEW, an influential center for European economic research, said the disappointing figures concerned incoming orders, industrial production and foreign trade.

“[These] have likely contributed to the growing pessimism among financial market experts,” ZEW President Professor Clemens Fuest remarked on the data. “ZEW’s financial market experts expect the economic situation in Germany to decline further over the medium term. Geopolitical tensions and the weak economic development in some parts of the euro zone, which is falling short of previous expectations, are a source of persistent uncertainty,” he added. The ZEW Indicator of Economic Sentiment for the euro zone also decreased in October. The respective indicator has declined by 10.1 points compared to the previous month, reaching 4.1 points.

The rising dollar will move mountains.

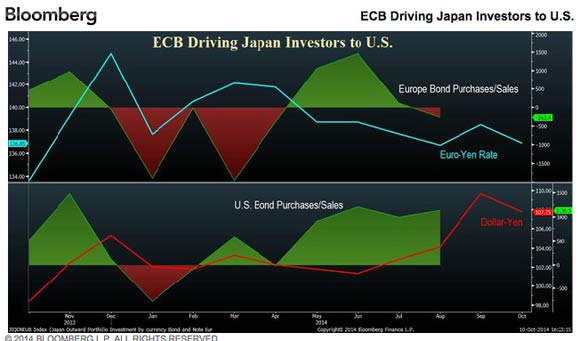

• Euro Drop Seen as ECB Sends Yen Assets to US (Bloomberg)

The European Central Bank’s record-low interest rates are pushing Japanese investors out of the region and into the U.S., and that’s weighing down the euro, according to Mizuho Bank Ltd. The CHART OF THE DAY shows Japanese investment managers were net sellers in August of German, French and Italian bonds while they snapped up U.S. Treasuries for a sixth-straight month. The 18-nation euro has weakened about 6% against Japan’s currency this year, while the dollar reached a six-year high of 110.09 yen this month. German 10-year yields tumbled to a record 0.858% last week from 1.93% on Dec. 31. “Yields in Europe are getting crushed, reducing the allure for foreign investors,” said Daisuke Karakama, a markets economist at Mizuho Bank in Tokyo. “Europe is forced to continue easing, and carry trades funded in euros will drag the common currency lower. It’s inevitable that the U.S. will be more attractive for investors.”

Carry trades involve borrowing in low interest-rate currencies to buy higher-yielding assets elsewhere. The Federal Reserve is on course to end its bond buying this month, even as the Bank of Japan maintains record stimulus. President Mario Draghi repeated over the weekend he’s ready to expand the ECB’s balance sheet by as much as 1 trillion euros ($1.3 trillion.) Japanese money managers offloaded 4.9 trillion yen ($45.7 billion) of German bonds this year, capping eight straight months of reductions with sales of 86.8 billion yen in August, data from Japan’s ministry of finance and central bank show. The traders offloaded more than 50 billion yen each of French and Italian securities in August and bought 789.8 billion yen of Treasuries.

“A ruling that would say the ECB’s Outright Monetary Transactions mechanism isn’t in line with the EU Treaty would be the end of the euro ..” [..] “Politically, they cannot do that.”

• Draghi’s ‘Whatever It Takes’ Plan Faces Trial at EU Court (Bloomberg)

European Central Bank President Mario Draghi’s pledge to do “whatever it takes” with a bond-buying plan to save the euro-area goes on trial before the European Union’s top judges today. The Court of Justice, the bloc’s highest court, will weigh whether Draghi’s ECB overstepped its powers in 2012 with the mechanism to buy the debt of stressed countries if needed. While Germany’s own top court earlier this year expressed doubts about the plan’s legality, the EU tribunal’s 15-judge panel is unlikely to overturn it, according to legal scholars. “A ruling that would say the ECB’s Outright Monetary Transactions mechanism isn’t in line with the EU Treaty would be the end of the euro,” said Pierre-Henri Conac, a professor of financial-markets law at the University of Luxembourg.

“Politically, they cannot do that. There is no real suspense about the way the ruling will go, but there will be suspense about the actual content of the decision.” The Frankfurt-based ECB announced the details of its unprecedented bond-purchase plan in September 2012 as bets multiplied that the euro area would break apart and after Draghi’s promise to do whatever was needed to save the currency. The calming of financial markets that the still-untapped OMT program produced helped the euro area emerge from its longest-ever recession in the first half of last year. From the statements, the ECB expects wide-ranging support for its argument that it should be allowed to determine independently how to reach its goal of price stability, a spokesman for the ECB said.

It’s the cold. No wait, it’s the heat. Summers hit sales, winters hit sales, and never is it people simply not having any money. “The prolonged Indian summer wilted retail sales in September, leaving clothing retailers hot under the collar. Selling woolly jumpers in warm weather is a tough ask…”

• UK Retail Sales Plummet To Financial Crisis Lows (CNBC)

U.K. retail sales fell to the lowest levels last month since December 2008, as food sales continued to decline and clothing and footwear sales hit record lows, according to widely followed report. In a monthly joint report, the British Retail Consortium (BRC) and KPMG noted that a very warm summer had resulted in exceptionally low demand for “winter” items such as boots and coats in September. This led to the lowest monthly fashion sales since April 2012. Retail sales last month were down 2.1% on a like-for-like basis from September last year, when they increased 0.7% on 2012 levels.

“The prolonged Indian summer wilted retail sales in September, leaving clothing retailers hot under the collar. Selling woolly jumpers in warm weather is a tough ask, even for the most talented of sales staff,” David McCorquodale, head of retail at KPMG, said in the report. Grocers also had a challenging month, with many announcing further price cuts. Earlier data from the BRC showed food inflation hit an all-time low in September, as supermarkets tried to attract customers with special offers. Fresh food prices remained flat in September, for the first time since February 2010.

Isn’t that timely?!

• Ireland To Close ‘Double Irish’ Tax Loophole (Guardian)

Apple and other multinationals based in Ireland are to be given a four-year window before the phasing out of a scheme that cuts their tax bills. Amid mounting international criticism of the arrangements, which save foreign companies billions of euros, Ireland’s finance minister, Michael Noonan, is expected to announce the end of the “double Irish” scheme when he delivers his budget on Tuesday. The European commission is investigating “sweetheart” tax deals between the Irish state and Apple, and last month Brussels provisionally found that the iPhone maker’s tax arrangements in Ireland were so generous as to amount to state aid. Noonan’s move may pre-empt measures hinted at by the UK chancellor last month, when he announced a crackdown on technology firms’ tax strategies at the Conservative party conference. George Osborne said: “Some of the biggest technology companies in the world … go to extraordinary lengths to pay little or no tax here … We will put a stop to it.”

Party officials briefed that he had companies using the double Irish scheme in his sights. On the international stage, the G20 group of powerful economies has commissioned the Organisation for Economic Cooperation and Development to produce a package of tax reforms to rein in multinationals. This work is expected to be completed by summer 2015. Accompanying a pledge to remove the tax loophole, Noonan’s budget is expected to contain incentives for multinationals, such as lower tax rates for companies that centre their research and development facilities on Ireland. The so-called “patent box” will reward foreign firms that base their technological developments in the Irish state. This echoes the UK’s regime, which has attracted criticism from other countries as well as the EU’s code of conduct committee.

The oil price drop can finish them off, those commies! Big Oil would love nothing more than to get access to the Orinoco, with arguably the biggest oil reserves on the planet.

• Venezuela Default Almost Certain, Harvard Economists Say (Bloomberg)

Venezuela will probably default on its foreign debt as a shortage of dollars makes it impossible for the government to meet its citizens’ basic needs, Harvard University economists Carmen Reinhart and Kenneth Rogoff said. The economy is so badly managed that per-capita gross domestic product is 2% below 1970 levels, the professors wrote in an column published by Project Syndicate yesterday. A decade of currency controls has made dollars scarce in the country with the world’s biggest oil reserves, causing shortages of everything from deodorant to airplane tickets. “They have extensive domestic defaults and an economy that is really imploding,” Reinhart said in a telephone interview from Cambridge, Massachusetts. “What they really need to do is get their house in order. If an external default would trigger such a possibility, that’s not a bad thing.”

The suggestion that the country stop servicing its bonds comes a month after Harvard colleagues Ricardo Hausmann and Miguel Angel Santos wrote that Venezuela should consider defaulting given that it was piling up arrears to importers. Venezuela owes about $21 billion to domestic companies and airlines, according to Caracas-based consultancy Ecoanalitica. Venezuelan debt is the riskiest in the world, yielding 15.42 percentage points more than similar maturity Treasuries, according to data compiled by JPMorgan Chase & Co. The cost to insure the country’s bonds against default with credit-default swaps is also the highest for any government globally. “Given that the government is defaulting in numerous ways on its domestic residents already, the historical cross-country probability of an external default is close to” 100%, Reinhart and Rogoff wrote in their piece.

Man’s folly in all its glory.

• Car-Maggedon: The $4.4 Trillion Traffic Problem (CNBC)

Traffic congestion over the next 17 years is set to give the U.S. and the biggest economies in Europe a $4.4 trillion headache, according to a U.K.-based economic consultancy firm. France, Germany, the U.K and the U.S. will face a combined toll of $200.7 billion in 2013 across their whole economies and that figure is expected to rise to $293.1 billion by 2030, according to the Centre for Economics and Business Research (CEBR). This would mark a 46% increase in the costs imposed by congestion and is calculated from direct costs, like fuel and wasted time, as well as indirect costs like the inflated household bills passed on by idle freight traffic.”This report shows that advanced economies could be heading for ‘car-maggedon’,” said Kevin Foreman, the general manager of geoanalytics at INRIX who provided the data for the CEBR.

“The scale of the problem is enormous, and we now know that gridlock will continue to have serious consequences for national and city economies, businesses and households into the future,” he said in a press release on Tuesday. The U.K. is expected to see the biggest increase in costs due to congestion, with the U.S. in second place. Londoners faced the biggest impact – with a 71% rise – while Los Angeles is due for a 65% increase, according to the report. Road users spend, on average, 36 hours in gridlock every year in urban areas across these four economies, it added. It also noted that idle vehicles in these developed nations released 15,434 kilotons of carbon dioxide last year and forecast this to rise by 16% between 2013 and 2030.

Always seemed a pretty useless idea to me. What they don’t say is you’re suspect when you have a fever AND you’re black.

• Ebola Airport Checks: ‘A Net With Very Wide Holes’ (CNBC)

After Texas reported its second case of Ebola on Sunday, experts told CNBC that airport screening was unlikely to prevent another potential victim of the killer disease from entering the U.S. Last week, the U.S. government ordered five airports to start screening travelers for Ebola, following the first case on American soil—Thomas Eric Duncan, who died last week after arriving from Liberia in September. Texas Health Presbyterian Hospital has now announced that a female caregiver who treated Duncan has caught the disease. By instigating screening at five airports, including New York’s John F. Kennedy International Airport, the U.S.’s Centers for Disease Control and Prevention (CDC) hopes to evaluate over 94% of travelers arriving from Guinea, Liberia and Sierra Leone—the countries worst hit by the outbreak. Visitors will have their temperature taken, be observed for symptoms of Ebola and asked questions to determine their risk of the disease.

Epidemiologists have warned that there is little evidence that this screening will prevent another victim from entering the U.S., or other countries, such as the U.K., which have also adopted screening. “Airport temperature screening is ‘a net with very wide holes’,” Ran Balicer, a policy adviser and infectious diseases expert at Ben-Gurion University, Israel, told CNBC. “If your perceived aim would be to prevent most cases of imported disease, you are likely to fail.” The epidemiologist noted that the gap between sufferers contracting Ebola and developing a fever could be as long as 21 days—meaning that the likelihood of potential patients being detected as they disembark was slim. “Beyond the logistical difficulties, there is also a serious issue of false alarms, especially in the flu/RSV season (respiratory syncytial virus) when random fever may be not infrequent among travelers.”

And so it spreads.

• UN Medical Official Dies Of Ebola In German Hospital (Guardian)

A UN employee infected with Ebola has died in Germany, officials say. The 56-year-old Sudanese man had been flown from Liberia to Leipzig last Thursday, where he received treatment at a specialist unit at the St Georg clinic. On his arrival, doctors at the hospital had described his condition as “highly critical, but stable”. On Tuesday morning the clinic confirmed in a statement that their patient had died on Monday night, “in spite of intensive medical measures and the best efforts on behalf of the medical staff”. The Leipzig clinic has assured the public that there is no risk of infection for people in the area. The man had arrived in Germany on a specially adapted Gulfstream jet with an isolation chamber, and had been treated on an isolation unit by staff wearing protective gear.

According to the World Health Organisation, around 8,400 people have been infected with Ebola after the current outbreak of the disease in Africa, out of which more than 4,000 people have died. The epidemic is still out of control in the west African states of Liberia, Guinea and Sierra Leone. The Sudanese man was the third Ebola victim to receive treatment in Germany. A doctor from Uganda is being treated in an isolation unit in Frankfurt, while a Senegalese man was recently released from a Hamburg clinic after a five-week treatment. The German government claims to be well prepared for an outbreak of Ebola in Germany. Isolation units at hospitals in Frankfurt, Berlin, Düsseldorf, Leipzig, Munich, Stuttgart and Hamburg could hold a total of 50 Ebola patients, it said. There are currently no plans to increase the number of stations.

Not a new suspicion, but good they go public with their research. Key word: Aerosols.

• “There Is Scientific Evidence Ebola Has The Potential To Be Airborne” (ZH)

When CDC Director Tim Frieden first announced, just a week ago and very erroneously, that he was “confident we will stop Ebola in its tracks here in the United States”, he hardly anticipated facing the double humiliation of not only having the first person-to-person transmission of Ebola on US soil taking place within a week, but that said transmission would impact a supposedly protected healthcare worker. He certainly did not anticipate the violent public reaction that would result when, instead of taking blame for another epic CDC blunder, one which made many wonder if last night’s Walking Dead season premier was in fact non-fiction, he blamed health workers for “not following protocol.”

And yet, while once again casting scapegoating and blame, the CDC sternly refuses to acknowledge something others, and not just tingoil blog sites, are increasingly contemplating as a distinct possibility: namely that Ebola is, contrary to CDC “protocol”, in fact airborne. Or as, an article posted by CIDRAP defines it, “aerosolized.” Who is CIDRAP? “The Center for Infectious Disease Research and Policy (CIDRAP; “SID-wrap”) is a global leader in addressing public health preparedness and emerging infectious disease response. Founded in 2001, CIDRAP is part of the Academic Health Center at the University of Minnesota.” The full punchline from the CIDRAP report:

We believe there is scientific and epidemiologic evidence that Ebola virus has the potential to be transmitted via infectious aerosol particles both near and at a distance from infected patients, which means that healthcare workers should be wearing respirators, not facemasks.

In other words, airborne. And now the search for the next LAKE, i.e., a public company maker of powered air-purifying respirator (PAPR), begins.