Pablo Picasso Head of a Woman 1946 ..gifted to Greece’s National Gallery by Picasso in 1946 in recognition of Athens’s resistance to Nazi occupation; he inscribed on the back: “For the Greek people, a tribute from Picasso.”

Palantir

AI teaching itselfBreaking

— Kim Dotcom (@KimDotcom) February 15, 2026

Palantir was allegedly hacked. An AI agent was used to gain super-user access and here”s what the hackers allegedly found:

Peter Thiel and Alex Karp commit mass surveillance of world leaders and titans of industry on a massive scale.

They have thousands of hours of…

Google, $GOOGL, CEO said that they don't know how AI is teaching itself skills it is not expected to have. pic.twitter.com/dAfyZPB4m0

— unusual_whales (@unusual_whales) February 15, 2026

Elon predicts brain-to-brain thought sharing.

— Mario Nawfal (@MarioNawfal) February 15, 2026

Facts move mind to mind. No “lossy compression.”

Talking becomes optional. Thoughts sent directly.

Bandwidth replaces vocabulary.@neuralink @elonmusk pic.twitter.com/J7J0HTOFx7

$145 MBen Affleck just explained AI better than 99% of tech Twitter.

— Sukh Sroay (@sukh_saroy) February 15, 2026

I build with AI. I write a newsletter about it. I still couldn't frame it that cleanly.

Sometimes the outsider sees what the insider can't. pic.twitter.com/bzs2ffzYeX

https://twitter.com/gabrelyanov/status/2023241194684264472?s=20 CybercabThe US government just dropped $145M to train workers in AI, semiconductors, and nuclear energy… as apprenticeships.

— Min Choi (@minchoi) February 15, 2026

Not college degrees. Apprenticeships. Learn while you earn.

AI is officially a skilled trade now. Same category as shipbuilding and healthcare.

The goal: 1… pic.twitter.com/Ydn7eK03qw

Cybercab, which has no pedals or steering wheel, starts production in April https://t.co/yShxZ2HJqp

— Elon Musk (@elonmusk) February 16, 2026

“..It doesn’t matter if the target is a child rapist or a murderer. Opposing Trump’s immigration policies matters more than anything else.”:”:

• Trump Derangement Syndrome Has Hit a Sick New Low (Matt Margolis)

A Minnesota woman just put on full display the moral rot at the heart of the anti-ICE movement, and she did it with a camera rolling. Last week, Olivia Jensen stalked ICE agents around Rochester, Minn., harassing them while they tried to track down an illegal immigrant accused of child rape and murder. When an agent finally told her what kind of monster they were after, Jensen’s response cut through every pretense the left hides behind: “No, I don’t care.” This wasn’t some slip of the tongue. Jensen said this, and posted her confrontation to Facebook and TikTok like a trophy, complete with a lengthy explanation of how she followed the agents from Walmart to her old address in Claremont, 30 miles away.Read more …

“Today, 2/11/26, I went to a NW area of Rochester after hearing that there was ICE activity in the area. I located the dark Gary Durango […] with 3 agents inside following a woman in her car,” Jensen posted on Facebook. “They followed her to Walmart north where I interacted with them while completely staying within my rights. They took pictures of me and the inside and outside of my car for simply exercising my rights. I will share the video of this interaction below. They very clearly were running my plates and trying to obtain information about me in an effort to intimidate me.”She accused them of intimidation for running her plates and visiting her former home. But the agents were just making sure she got home safely after she’d been tailing them across southeast Minnesota. The exchange stripped away any illusion about what drives these ICE agitators. After Jensen screamed “race traitor” at a Hispanic agent, he calmly explained they were hunting a child molester. She called him a liar. The other agent stepped in with a reality check: “If you actually cared, you would care about the child who got raped and also by the person who got murdered by the person we are looking for.”

That’s when Jensen said the quiet part out loud. She admitted she didn’t care. Then she pivoted to the standard talking point about how ICE should only go after “illegal, violent immigrants” before insisting “that’s not what you are doing.” Except it was exactly what they were doing. They were literally chasing a suspect wanted for raping a child and murder. “If you actually cared, you probably would care about the child who got raped and the person who got murdered by the person we’re looking for, but you see, you don’t care,” an ICE agent told Jensen. “No, I don’t care,” Jensen admitted.

This is what Trump Derangement Syndrome looks like. The activist class wants Americans to believe their beef is with detaining and deporting otherwise law-abiding illegal immigrants. They frame it as compassion, as standing up for families just trying to build better lives. But when push comes to shove, and ICE is hunting someone accused of the most heinous crimes imaginable, the mask comes off. These agitators don’t want ICE arresting anyone, period. It doesn’t matter if the target is a child rapist or a murderer. Opposing Trump’s immigration policies matters more than anything else.

“In one email, it says that “Reid will spend the night at 71st,” which is a reference to Epstein’s Upper East Side townhouse. ”

• Reid Hoffman Funded Suit Against Trump Alleging Rape (Tim O’Brien)

The disclosures from the Epstein files have been enlightening to say the least, particularly if you wonder if you are seeing what you think you’re seeing. More to the point, do you remember that 2023 lawsuit against candidate Donald Trump from E. Jean Carroll? That’s the one where Carroll, who is now 82 years old, waited all these years and, after two of Trump’s presidential races and one term as president, decided to sue the billionaire on allegations of defamation, rape, and sexual abuse.Read more …

The case was mostly based on unsubstantiated accusations that Trump sexually abused and raped Carroll in 1996, 23 years earlier. In the end, a jury awarded Carroll $5 million in a judgement that rejected the plaintiff’s claim that she was raped, but it found Trump responsible for sexual abuse. The jury verdict also gave Trump’s dishonest critics the opportunity to falsely claim he raped someone. Before, during, and after the trial, Carroll made a number of curious statements that make you wonder just how right in the head she is. Like the time in 2019 that she told CNN’s Anderson Cooper, “Most people think of rape as being sexy.” Now the Epstein files are providing some new context to that case and, more specifically, to the man with the money behind the lawsuit.Since 2023, we knew that billionaire leftist and founder of LinkedIn Reid Hoffman bankrolled the litigation. He provided most, if not all, of the money needed to pay those blue-chip lawyers who represented Carroll. The Denver Gazette reported in 2023 this fact, along with the fact that he’s donated to “Democratic causes including former 2016 presidential candidate Hillary Clinton,” adding, “He also partnered with megadonor George Soros in 2021 to form an organization to combat disinformation.” Hoffman is a certified never-Trumper with advanced-stage TDS (Trump Derangement Syndrome). Hoffman was all too happy to take credit for the role his funding played in supporting Carroll’s lawsuit.

So, you heard Hoffman, right? He said, “Her (Carroll’s) voice should be heard, that because she was challenging someone who was so much more wealthy and powerful that shouldn’t be squashed.…Providing that voice for, you know, people who otherwise would be ground down by the system, or the powerful, is I think a good thing, obviously especially in the case of women, and especially in the case of sexual, and other, kind of torture, and attack…So, providing that support was something I was very happy to do.” As a leftist billionaire, all of this is very on brand for Hoffman. Hypocrisy and double standards are also on brand for the left. In that spirit, it appears Hoffman has not disappointed.

Hoffman was mentioned quite a bit in the Epstein files, and it would appear not as a mere acquaintance of Epstein. That said, it’s important to know that not everyone mentioned in the files did anything wrong. In a few cases that we already know of, some who are mentioned explicitly rejected Jeffrey Epstein and what he was all about. Others were simply people who had crossed paths with Epstein along the way. Hoffman’s interactions with Epstein suggest he did a lot more than simply cross paths with Epstein. His name is mentioned in the files 2,658 times. The New York Post has reported that some of the recently released Epstein email files “reveal LinkedIn co-founder Reid Hoffman discussing visits to Epstein’s infamous private island, his New Mexico ranch, and his New York apartment.”

In one email, it says that “Reid will spend the night at 71st,” which is a reference to Epstein’s Upper East Side townhouse. The Post also reported, “An apparent 2014 scheduling memo lists a variety of dinners and parties, as well as the line: ‘Jeffrey will have Joi Ito and Reid Hoffman will go to the ranch for the weekend (JE did not give exact dates).’” Ito is a notable Japanese venture capitalist. Here are some of the emails in question. While there is nothing specifically incriminating in the wording of the emails, Hoffman’s obviously close relationship with Epstein raises a number of questions, especially for a man who, when he funded Carroll’s lawsuit against Trump, said that in providing that funding, he was supporting “people who otherwise would be ground down by the system, or the powerful.”

And then he added that he thought this was “a good thing, obviously especially in the case of women, and especially in the case of sexual, and other, kinds of torture, and attack.” Let’s say, for sport, that Hoffman didn’t engage in the perks of spending all that time on Epstein’s island or in his pervert Bed and Breakfast. Do you think he knew what an unsavory character Epstein was? Do you think he ever offered to pay for lawsuits on behalf of Epstein’s victims? Do you think Hoffman had his share of opportunities to get to know any of them? I guess we just need to stay tuned.

“These disastrous policies began under Obama, were reversed during Trump’s first term, and then roared back under Biden. The result? A staffing crisis filled with underqualified controllers who couldn’t handle the job. ..”

• The Trump Administration Officially Kills DEI at the FAA (Matt Margolis)

Last year’s deadly midair collision at Reagan National Airport, which killed all 67 people aboard an American Airlines plane and a U.S. Army helicopter, was a wake-up call that many on the left refused to hear. President Donald Trump, however, understood the problem and sought to fix it. He pointed directly at the Barack Obama and Joe Biden DEI policies that prioritized checkbox diversity over actual competence in air traffic control. He was absolutely right. Air traffic control whistleblowers confirmed that the FAA’s obsession with Diversity, Equity, and Inclusion initiatives has led to a shortage of qualified personnel. These disastrous policies began under Obama, were reversed during Trump’s first term, and then roared back under Biden. The result? A staffing crisis filled with underqualified controllers who couldn’t handle the job.Read more …

The whistleblowers revealed that meeting diversity quotas became more important than actual ability. I’m sorry, but when you’re juggling planes full of passengers through the skies, “good enough for diversity” doesn’t cut it. The problems were so severe that near misses occurred multiple times a week. Reagan National wasn’t a random tragedy; it was an inevitable disaster created by DEI. But those days are over. Last week, Transportation Secretary Sean Duffy announced that the FAA issued a mandatory “Operations Specification” that forces every commercial airline to commit to merit-based hiring for pilots. No more woke hiring practices and no more prioritizing race and sex over skill. If airlines don’t comply, they face federal investigation.“When families board their aircraft, they should fly with confidence knowing the pilot behind the controls is the best of the best,” Duffy said. “The American people don’t care what their pilot looks like or their gender—they just care that they are most qualified man or woman for the job.” This shouldn’t be controversial. It’s just common sense. But under the Biden-Buttigieg regime, common sense got tossed out the window. The FAA spent years focused on renaming cockpits to “flight decks” and investigating racist roads and bridges while actual safety standards crumbled.The new mandate requires all U.S. carriers to certify they’ve terminated race and sex-based hiring practices. Airlines must prove they’re identifying candidates based on specific experience and technical aptitude that match their operating environment.v

Imagine that: hiring people who can actually do the job. Such a novel concept, right?“At the FAA, the safety of passengers is our number one priority,” said FAA Administrator Bryan Bedford. “It is a bare minimum expectation for airlines to hire the most qualified individual when making someone responsible for hundreds of lives at a time. Someone’s race, sex, or creed, has nothing to do with their ability to fly and land aircraft safely.” This action follows Trump’s Executive Order on Ending Illegal Discrimination and Restoring Merit-Based Opportunity and his Presidential Action on Keeping Americans Safe in Aviation. The FAA has already raised performance standards, dismantled DEI offices and contracts, and scrapped the worst of the Biden-era directives. But until now, allegations of airlines hiring based on race and sex persisted.

The safety of our skies should never take a backseat to diversity quotas. Period. Americans deserve to know that the people monitoring their flights and flying their planes earned those positions through competence, not because they checked the right demographic boxes on a form. It’s about time the FAA refocused on hiring the most competent individuals who can ensure the safety of everyone traveling through our airspace. And you can bet this fix wouldn’t have happened under a Democrat administration — it would still be prioritizing DEI initiatives and then scratching its head over what caused preventable crashes.

“..if you are a banker and you lose a fortune, then you are always bailed out with tax money. This is why they never improve.”

• Big Losses for Banks Coming in 2026 – Charles Nenner (USAW)

Last April, renowned geopolitical and financial cycle expert Charles Nenner predicted a depression cycle starting at the end of 2025 into 2026. The economy is clearly slowing down, and the latest “1 million plus” negative jobs revision that comes out Wednesday (2/11/26) certainly points to a tanking economy. Nenner says, “I have to adjust for all the immigrants let into the country, but we will soon see unemployment numbers go up.” The next big downward surprise for the economy is big losses for the banks. Nenner predicts, “The institutions I work with that are selling real estate in New York are telling me a lot of banks are already negative. If you look in their books in California, they already had these big losses.Read more …

“They did not get out of their bonds because they thought interest rates would never go up. There are a lot of things that are already wrong, but it has not come out yet. I don’t know if there are going to be failures, but it will come out, and they will have big losses when they have to show the books.” So, what is Nenner predicting will happen with the troubled banks? Nenner says, “I guess the Fed will step in or the government will step in . . . because if you are a banker and you lose a fortune, then you are always bailed out with tax money. This is why they never improve.”With gold and silver, there is good news and bad news. First comes the bad news. I asked Nenner if he would be a buyer of silver and gold now? Nenner says, “No, not right now because the cycle is down for the moment. . .. It is the same thing for gold. The cycle is down. If we close below $4,700, we will get some downside price targets. Usually, things that go up fast also go down fast. It’s not over for gold and silver; it’s just a correction.” Nenner put his clients in gold at $1,600 an ounce, and he bought silver at $29 per ounce. Now comes the good news, as Nenner points out, “The bull market for gold and silver will continue to the end of 2027. By then, we can do some fine tuning.”

On the war cycle, good news—for now. In the Middle East, Nenner says, “Right now, the war cycle is not going to heat up.” How about the war cycle for Europe and Russia? Nenner says, “No, they are not going to heat up either. The war cycles are topping right now. It’s not going to heat up for the short term.” Nenner is still worried about China and Taiwan at some point in the future. The really bad news on the war cycle comes in the 2030 to 2032 time frame. Nenner says, “The 2030 to 2032 war cycle is going to be very bad. There are going to be a lot of casualties. They start shooting rockets, and how many people are going to die? I think it will be in the billions of people, and that is what the numbers show.”

Nenner warns of terrorists let into the country by the Biden Administration that could set off bombs in the US “on a big scale.” Nenner contends this will be part of the war cycle that comes at the end of this decade. Nenner also said Trump could help cushion the financial fall of the USA, but he could not stop the down financial cycle. Nenner pointed out, “You cannot stop winter, but you can get a winter coat, and Trump is a winter coat.” Now, Nenner says, “There was so much damage done to America that Trump can’t fix it. . .. The cycle is turning down, and you can’t do anything about it.” Nenner also predicted in January of 2024 that President Trump “would be coming back.”

So, let’s all pray to God the Father and His Son Jesus for divine help.

“So how about a devastating debt spiral to perk you up on this fine Presidents’ Day? “:

• Welp, Here Comes the ‘Death Spiral’ (Stephen Green)

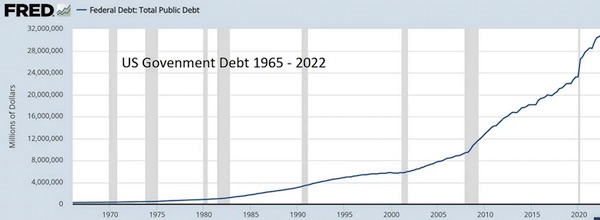

So how about a devastating debt spiral to perk you up on this fine Presidents’ Day? The latest Congressional Budget Office report — with the thrilling title “The Budget and Economic Outlook: 2026 to 2036” — doesn’t use the phrase “debt spiral,” but Fortune’s Jason Ma did on Saturday, and I’m totally stealing it. Ma wrote of a debt “tipping point” that most people aren’t aware of but that could “arrive soon” with potentially devastating effects. I think I lose readers every time I write about this stuff, and yet I persist.Read more …

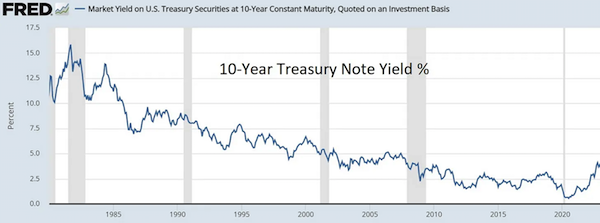

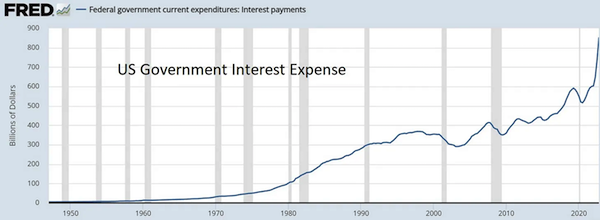

Before we get to that spiral, let’s set the stage. Ma noted that “publicly held debt is currently at $31 trillion and is about 100% of GDP. By fiscal year 2030, debt is expected to exceed the 106% record set after World War II, then surge to 120% by 2036.” Of course, we won the war in short order, spending returned to normal, and the debt became manageable.&; I think pretty much everybody reading PJ Media is at the very least vaguely aware of these current figures, but the Committee for a Responsible Federal Budget warned last week: “Later in the decade, under CBO’s baseline, the average interest rate on all federal debt will exceed nominal economic growth, which could represent the start of a debt spiral.”“Fearing the political backlash of fiscal austerity, lawmakers often point to the prospect of robust economic growth as an alternative way to keep U.S. debt under control over the long term,” Ma wrote, “But the threat of interest costs growing faster than the economy risks sending debt into escape velocity and forcing more drastic measures to prevent a crisis.” So let’s talk about the reality that few people seem willing to address. And Another Thing: Maybe people would pay more attention to these CBO reports if they gave them titles like, “Louisiana Johnson and the Spiral of Doom.”There are three ways out from under trillions and trillions in debt. Only three.

Washington can inflate away the debt, which is the preferred method of corrupt governments throughout history. The Biden Cabal managed to knock the real value of our debt down by 20% or so in just a couple of years, and all they had to do was set the typical American’s income back by years (not to mention wipe out any cash savings) to do it. The second option is default, although it does come in two flavors. There could be an orderly default, where Washington goes to our creditors at home and abroad and says, “Look, you and I both know we can’t pay back all the interest we owe you. So let’s negotiate how big a haircut you’re going to take while we get our finances in order.” Then there’s a disorderly default, where Washington just stops paying and there’s a global run on the dollar, markets collapse, and savings evaporate. The first flavor is almost too foul for even a small taste. The second melts your face off.

The third option is to grow out way out, and this is Trump’s preference. Mine, too, for that matter. Washington needs to do everything in its power to spur growth — primarily deregulation and tax cuts — while Congress keeps spending growth smaller (even just slightly smaller) than GDP growth. If the bond markets saw Congress rein in spending growth, those long-term interest rates would come down fairly quickly. Until that happens, however, the bond markets must — must — price in the risk of inflation and/or default. What that means in, no matter how low the Fed cuts short-term rates, those long-term rates will remain stubbornly high.

And Another Thing: Come to think of it, there is a fourth option, and that’s send the military into foreign countries to steal what we can’t pay. That’s a bad way, mmkay? That isn’t the Fed’s fault, and we can’t blame Jerome Powell for this one. It’s simple economic reality. Or as Bill Clinton advisor James Carville put it more than 30 years ago, when a nasty bond market reaction put the kibosh on Clinton’s grander spending plans, “I used to think that if there was reincarnation, I wanted to come back as the President or the Pope or as a 400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody.” Everybody, it seems, but those reckless fools in Congress who hold the nation’s purse strings — and all our fates — in their hands.

Vance or Rubio in ’28? Place your bets here.

• Marco Rubio Joint Press Conference with Hungarian PM Viktor Orban (CTH)

Secretary Marco Rubio went out of his way in this joint presser to emphasize the personal relationship between Hungarian Prime Minister Viktor Orban and U.S. President Donald Trump. Orban is facing a serious election challenge this April and all of the EU/NATO systems are actively trying to create pressure points to remove him. Secretary Marco Rubio is in Budapest today for meetings with Prime Minister Viktor Orbán and his government to include the signing of a civilian-nuclear cooperation agreement heralded by the Trump administration.Read more …

Hungary is one of the few voices within the European Union who is pushing back against Brussels efforts to go to war against Russia. Prime Minister Orban has been very critical of Ukraine, openly stating his opposition to EU membership for the embattled country. In response President Zelenskyy has weaponized Ukraine’s geographical stewardship of oil and gas pipelines to shut down Hungarian energy and drive-up prices.

“.. politicians stage themselves retroactively as initiators of the new, attempting to position themselves at the forefront of developments they have ignored or actively obstructed for decades..”:

• Macron’s AI Clown Show: Europe’s Digital Dilemma (ZH)

The European Union has lost its place in the global race for artificial intelligence. In a single tweet on platform X, France’s President Emmanuel Macron inadvertently outlined the convoluted situation while simultaneously revealing his personal emotional fragility. The leading representatives of the European Union like to present themselves as emotionless technocrats. Maintaining the greatest possible distance from citizens, they execute their agenda of societal transformation toward what they understand as a net-zero transformation economy. This ostentatious distance from the citizenry acts as a simulacrum of power, which, in politicians like Emmanuel Macron, often veers into the caricatural.Read more …

Macron’s striking presence in foreign affairs—whether regarding the Ukraine war or recurring provocations toward the United States—correlates with his aggressive censorship policy toward his own population. A president without a people, steering his minority government through a budgetary crisis that brings France ever closer to the fiscal abyss.In Macron’s persona, the European misstep is condensed: economically failed, deeply unpopular among his own people, geopolitically essentially irrelevant—and yet imbued with lofty, messianic plans. This performative play of power, coupled with hardly disguised impotence and incompetence, inevitably produces an effect that can be described as clownish. It is the expression of a political style that can no longer reconcile claim with reality—and thus delivers less leadership than a tragicomic performance.Politicians like the French president are indeed aware of the growing public anger over their policies and, behind the technocratic façade, very much experience emotional states—Macron revealed this for a brief moment on February 7 on the platform “X,” which he otherwise fights. This moment of exposure was triggered by a reaction to Israeli AI investor Dr. Eli David. The entrepreneur had ridiculed the French government’s plan to initiate an AI revolution with a mere initial investment of €30 million, publicly calling the president a “clown.”

“This clown wants to make France an AI leader with €30M.”

— Emmanuel Macron (@EmmanuelMacron) February 7, 2026

€30 million → to attract and support around forty top-tier international researchers. They chose France for its values and its commitment to science.

Sometimes it’s too slow…… pic.twitter.com/UHlSpIIaI9Macron responded in classic social media fashion: fast, unconsidered, emotional. And this was precisely the real revelation. His message not only displayed personal fragility but simultaneously exposed Europe’s fatal economic strategy in the field of artificial intelligence. Macron directly addressed David’s criticism and slid into a rhetorical trap, writing: Yes, exactly this “clown,” meaning himself, would trigger an investment boom with €30 million, eventually mobilizing over €100 billion in private funds. Macron plans a French Silicon Valley south of Paris and intends to catapult his country to the Olympus of artificial intelligence—with €30 million of state money, initially benefiting those who provide the technological framework for the upcoming rollout of digital IDs.

In this sentence, Europe’s dilemma crystallized: self-assurance and denial, the familiar pathos of EU Europeans combined with an astonishing detachment from reality—and a political style that reveals more about Europe’s position in the global AI race than any sober analysis could. Those familiar with the codes, memes, and recurring keywords of digital platforms understand the significance of this label. When “clown world” or “clown politics” is mentioned, it refers precisely to the comedy we witness daily: the routine evasion of European top politicians from the consequences of their centrally controlled policies—be it economic and industrial policy, migration, or the grotesquely perceived energy policy.

The clown meme condenses the cynically self-ironic perception of the viewer of this comedy—a viewer aware that they are not only the target of these policies but will ultimately bear their consequences.Clown politics takes many forms. These include the countless crisis or innovation summits in which politicians stage themselves retroactively as initiators of the new, attempting to position themselves at the forefront of developments they have ignored or actively obstructed for decades. These summits are a particularly pernicious form of masking incompetence: political self-validation rituals simulating activity while merely covering up structural stagnation.

” Both seemed to put the onus on the Justice Department to protect them from their own folly..”

• Ro Khanna and the Impunity of “Wealthy, Powerful Men” (Turley)

Last year, I wrote a column expressing concerns over the move to release the Epstein files en masse, including grand jury material. The files include a wide range of tangential figures and unsupported allegations common to criminal investigations. Politicians eager to capitalize on the scandal would likely show little concern for the underlying facts in “outing” names and repeating unproven allegations. That fear was realized this week with the chest-pounding speech of Rep. Ro Khanna (D., Cal.) on the House floor in which he took credit for outing six “wealthy, powerful men” who he suggested were actively shielded by the DOJ from public exposure. After the DOJ unredacted the names at his request, he read them on the floor. It turns out that four have nothing to do with Epstein.Read more …

Had Khanna made these comments outside of the House floor, he would be looking at four defamation lawsuits. However, Khanna knew the men could not sue him because of the immunity afforded to him under the Constitution’s Speech and Debate Clause.Khanna has been clearly positioning himself for a 2028 presidential run by pandering to the far left of his party. That includes his support for a wealth tax that has already reportedly led to a trillion dollars leaving the state and could harm his own Silicon Valley constituents. The Epstein files offer an easy platform for another “Spartacus moment” for politicians, who portray themselves as public avengers. That was evident on the House floor as Khanna took credit for exposing these six men.It would turn out to be another Rep. Jasmine Crockett disaster where a gotcha moment became a spectacular face-planting. Khanna portrayed himself and Rep. Thomas Massie (R., KY) as ferreting out the names of the “wealthy, powerful men” whom the Trump Administration has fought to conceal. The Justice Department had previously agreed to let any members review the unredacted material. I have spoken with members who were part of the conference on the petition to force the release of these documents. They have told me that Massie, Khanna, and Marjorie Taylor Greene opposed repeated efforts to amend the petition to allow for greater resources and protection in the review of the millions of documents to avoid this danger.

In the conference, their colleagues specifically raised the danger of the release of entirely innocent names like the ones released by Khanna on the floor. They dismissed the danger and refused to amend the petition to avoid this type of error. (Indeed, in the hearing with Attorney General Pam Bondi, Rep. Brad Knott, R-N.C., makes reference to that failed effort to give the staff and resources to avoid the release of names with no connection to the underling criminal conduct). The media, again, eagerly spread the false claim of six men “likely incriminated” in the Epstein scandal. Khanna congratulated himself and his colleague for discovering the cover-up: “Why did it take Thomas Massie and me going to the Justice Department to get these six men’s identities to become public? And if we found six men that they were hiding in two hours, imagine how many men they are covering up for in those 3 million files.”

There is another possible explanation. Four of these men have little or nothing to do with Epstein. One of the names was previously connected to Epstein in public files. That is Les Wexner. Another, Sultan Ahmed Bin Sulayem, was the head of a Dubai logistics company called DP World. However, the other four were just photos used in a photo lineup. In other words, they were just random individuals used by the police to fill out a lineup. The Justice Department responded to Khanna’s public demonstration by declaring that “Rep Ro Khanna and Rep Thomas Massie forced the unmasking of completely random people selected years ago for an FBI lineup – men and women. These individuals have NOTHING to do with Epstein or Maxwell,” the spokesperson told the Guardian…”

What is curious is that Khanna blamed the Justice Department for his going to the floor to out the men as suspected wealthy and powerful predators. However, Massie admitted that he previously raised the possibility that the men were just used randomly in a line up. Both seemed to put the onus on the Justice Department to protect them from their own folly. [..]

“The West-West Divide: What Remains of Common Values..”

• Hillary Clinton Admits Mass Migration Is “Disruptive & Destabilizing” (ZH)

After U.S. Secretary of State Marco Rubio spoke earlier on Saturday at the Munich Security Conference, where he said the U.S. and Europe “belong together” and argued for a stronger West, former Secretary of State Hillary Clinton, who served under former President Barack Obama, appeared on a panel later that afternoon and made surprising remarks about mass migration. Clinton participated in a panel titled, “The West-West Divide: What Remains of Common Values,” and said that mass migration invasion involving millions of illegal aliens has been “destabilizing” to society.Read more …

Clinton continued: “So this debate that’s going on is driven by an effort to control people, to control who we are, how we look, who we love. And I think we need to call it for what it is. There is a legitimate reason to have a debate about things like migration. It went too far. It’s been disruptive and destabilizing, and it needs to be fixed in a humane way, with secure borders that don’t torture and kill people, and with a strong family structure, because it is at the base.”

Clinton’s comments about how mass migration has been an utter failure probably made White House border czar Tom Homan blush. In fact, unhinged Democrats, such as the Democratic Socialists of America, are probably furious with Clinton, given her very blunt public stance on immigration policy. In fact, if we circle back to Rubio’s comments earlier in the day, he slammed “mass migration”. Let’s not forget that Rubio’s State Department last fall recognized that mass migration was an “existential threat” to the West and risks “undermining the stability of key American allies.”Hillary Clinton admits illegal immigration went too far:

— RNC Research (@RNCResearch) February 14, 2026

“It went too far, it’s been disruptive and destabilizing.”

REMINDER: Biden let millions of unvetted illegal criminals pour into the country for four years. pic.twitter.com/JeqUxJsU7B

“America First” politicians are coming to their senses about the illegal alien invasion, as it was a move by globalists, NGOs, and their Democratic Party allies to install a new voting bloc and transform America into a one-party rule of left-wing kings and queens (think California). That’s why “America First” politicians and Elon Musk are pushing hard for the Safeguarding American Voter Eligibility (SAVE) Act to secure the integrity of elections.The World Awakens Part 1: Pawn Storms

— Winter_Rewind (@WinterRewind) May 31, 2024

The elites are using illegal immigrants as pawns worldwide to gain control. Even Cesar Chavez fought against it, pointing out that it was an attack on locals.

If you liked this content, pls consider following. It would be a big help in… pic.twitter.com/ubiEozxJwt

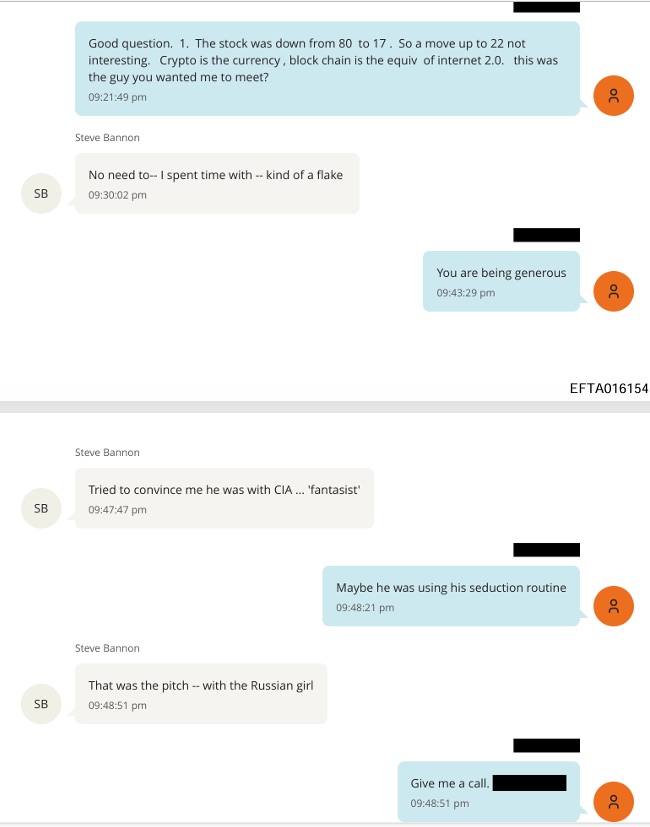

“Bannon and Epstein were very close and talked to each other about seemingly everything.”

• Steve Bannon and Jeffrey Epstein (CTH)

Through the years I didn’t really have much of an opinion of Steve Bannon, I approached any story of interest that surrounded him by simply looking at the factual details of the current event in question. CTH well understood that Bannon, and subsequently his expressed opinion and objective, was simply an outcome of his position – downstream from the billionaire of the moment who paid him. In essence, Steve Bannon always seemed to be, much like Kellyanne Conway, an advocate for whoever was financing him. From Robert/Rebekah Mercer at Breitbart forward to any endeavor thereafter, it always just appeared the same.That said, with the release of the Epstein files, the relationship between Steve Bannon and Jeffrey Epstein is something CTH did not expect. {HERE} Bannon and Epstein were very close and talked to each other about seemingly everything.Read more …

I can never unsee what I have read. Nor will CTH ever entertain the possibility that Bannon was ever a good element within the MAGA effort. There is a solid argument to be made that the Bannon War Room was funded, or organized in the funding mechanisms, by Jeffrey Epstein. {HERE} The files of messages between them contain some shocking stuff happening in the background while Steve Bannon was in very close proximity to candidate and President Trump. The level of disdain Bannon had for Donald Trump’s family and for Donald Trump himself is really something CTH did not expect to see. {examples: HERE and HERE} I am left to wonder now how much of the vitriol against Jared Kushner and Ivanka Trump, ie. “Javanka hatred”, actually originated from the Braintrust behind Bannon and the assembly of people in his immediate orbit.Initially, I saw some Twitter accounts attempt to defend Steve Bannon by saying Epstein did all the talking in their text exchanges and Bannon was less communicative. However, that only applied to the first batches of files reviewed. As a few days went along and people started citing files, reading them gives a much more fulsome picture of the relationship. Steve Bannon may have been focused on the financial gains and perhaps networks of people in his association with Epstein; but he certainly got deep into it and expressed extreme praise for Epstein, even going so far as to call him a god. {LINK} These were two men in a very close friendship. There is no political or ideological distance between Bannon and Epstein.

The level of expressed skullduggery that has been going on for years in the background is very unsettling to accept, and I say that as a person who doesn’t customarily get shocked by duplicity. This is not about division; this is about something more akin to betrayal. While putting on a MAGA face for the War Room broadcasts, in the background Bannon was actually plotting and advising of ways to eliminate Donald Trump from republican politics. This is Brutus level disloyalty, even accepting the guy has no moral compass other than his bank account. I can never unsee what has been seen.

There’s also some weird stuff in the exchanges about contextual things from years past. As an example, in one set of text messages Bannon and Epstein were discussing Patrick Byrne who is now part of the Emerald Robinson/Mike Flynn network. Bannon notes in 2018 that Byrne told him he was working for the CIA, and apparently Bannon did not believe him. This is the same November, 2018, message exchange where Epstein is advising Steve Bannon on how to set up a media network to maximize privacy, structure the financing and eliminate the problems with transparency. This is the origin of what would less than a year later become Bannon’s War Room on Real Voice America. Did Jeffrey Epstein provide the seed capital to assist the start-up of Bannon’s War Room? That question isn’t clear, but sheesh, the creepy irony of the possibility is really over-the-top.

I guess in the big scheme of things, considering all of the potential creepy stuff that is far more consequential to the Epstein file release, the relationship with Steve Bannon is not at the top of the issues of concern. However, the reality of seeing this relationship and reading how much they both hated MAGA is just so darn deflating. Trust lost can never be reestablished.Ugh. All of it. Just, ugh. Now we reevaluate everyone who openly, frequently and willingly associated themselves with Steve Bannon on that “War Room” platform. Including: Julie Kelly, Mike Davis, Jack Posobiec, Lara Logan, John Solomon, Laura Loomer, Harmeet Dhillon and so many more. Did they know about this Bannon-Epstein network?

“If you tolerate the intolerable, you’re communicating that it’s okay to mistreat you.” —Aimee Terese on X

• Epstein-itis (James Howard Kunstler)

Did you think the American zeitgeist — our collective spirit plus our thinking — could not get crazier? Gird your loins. It’s getting worse by the hour. The Jeffrey Epstein files suggest that people will do anything and that people will believe anything. Pizza, hot dogs, white sharks. . . boys, girls, babies, teens, Russian whores. . . celebrities by the score. . . billionaires. . . cannibal orgies. . . vivisection parlors. . . adrenochrome. . . blood. . . dead bodies. . . demon worship. . . a depraved and insane global leadership. . . lemme outa here!Read more …I don’t know what’s real in Epstein and what’s not — but neither do you. What you ought to know is that the colossal inventory of Epstein files is perhaps the greatest instrument of mass mind-fuckery ever seen in the history of Western Civ. How interesting, too, that the deluge of material coincides exactly with the critical capability emergence of Artificial Intelligence as a tool for the manipulation of documentary evidence. And also consider all the years since 2019 that interested parties have had to mess with, destroy, possibly fabricate, and catalog all this stuff.

Apparently, the Woke-Jacobin-Marxist eruption was not enough to destabilize the consensus about reality. The absurdities you were asked to swallow about all-women-are-women-including-men. . . the police killed George Floyd. . . mostly peaceful riots. . . the vaccine is safe and effective. . . the free-est, fairest elections ever. . . “Joe Biden” is president. . . the border is secure. . . speaking English is white supremacy — did not push America deeply enough into Crazyland. More was required to completely demolish your sense of an ordered world.

Donald Trump was correct, at least, that releasing the Epstein files would bring on more chaos than clarity and impede the effort to get our country back on the rails with an economic engine based on the production of goods instead of financialized hyper-casino voodoo. Well, now we’re in a maelstrom of innuendo, code-talk, gossip, and redaction, and you can hardly begin to sort it out. The Attorney General of the USA, bless her heart, has already botched the management of this monster.

Epstein’s relations with Israel and its Mossad intel blob, along with his connections to global banking interests, have aroused the zestiest breakout of antipathy to Jews since the SS busied itself loading the crematoriums of Europe. Hatred of Jews is a recurring symptom of civilization distress. But it is also possible that Israel has behaved badly — and it is certain that many political intellectuals are reevaluating the way that nation was established after World War Two. To some degree, Israel has become a paranoid state (though even paranoiacs have real enemies).

Where does that go from here? Thoughtful people are pessimistic. For sure, they resent the money and influence seeded by Israel in the US Congress. They might be concerned as well about all the other interests pounding money into American politics. Grift is everywhere, and everyone can see it now. The looming end of the grift orgy is probably behind the Democratic Party’s current psychotic disposition. Having lost its 20th century base of factory workers, the party has had to work the extreme margins of American life to build a coalition of the feckless, the reckless, the brainles

s, and the shameless. They have become the party’s wards in a reimagined patronage system even more pernicious than the old one under characters like Boss Tweed and Mayor Richard Daley-the-First of Chicago. The Democratic Party can’t win elections without rigging them and it’s astonishing that they’ve gotten away with building such sturdy armature of ballot fraud in plain sight with next to zero objection from the supposed guardians in officialdom. The features of it are so arrant that a political class with any sense or dignity would have laughed it straight into the criminal courts — and its perps straight into the penitentiary. The fraud became especially acute with the 2020 and 2022 elections. It is about to be revealed in the troves of evidence extracted lately from Fulton County, GA, and presently from Maricopa County, AZ. These birds are cooked. Not a few people will eventually go to jail over these shenanigans. And meanwhile, the SAVE Act pulsates in the Senate like a lump of kryptonite.

Now, you may realize that a political party based entirely on socially marginal persons — many of them mentally ill — will adopt a roster of ideas and policies that are patently marginal, which is to say, crazy. The party elders are now straining to eliminate some of that. Last week, Barack Obama unloaded on California Governor Gavin Newsom’s botched handling of the state’s epic homeless crisis. “We should recognize that the average person doesn’t want to have to navigate around a tent city in the middle of downtown,” the ex-president said in an interview with progressive YouTuber Brian Tyler Cohen.

Hillary Clinton, dropping in on the Munich Security Conference, said, amazingly, “There is a legitimate reason to have a debate about things like migration. It went too far, it’s been disruptive and destabilizing. . .” before tossing in some Woke word-salad: “. . . and it needs to be fixed in a humane way with secure borders that don’t torture and kill people and how we’re going to have a strong family structure because it is at the base of civilization.” Say, what. . . ?

But then, poor Hillary, who can’t help being a Cluster-B psycho, turned up moderating a panel at the same Munich meet-up to take up the issue: “Girls Just Want to Have Fundamental Rights: Fighting the Global Pushback.“ To nail down her point, Hillary brought onstage as the featured speaker, Rep. Sarah McBride (D-DE), known previously as Tim McBride, a man. The insanity is, of course, self-evident. The take-away from all this. They’re not trying hard enough to get their minds right.

And in the meantime, America and the other nations of Western Civ, must contend with the gigantic trip laid on them that is the Epstein files. We know the newspapers and cable news channels are hopeless. Is there anyone or any sense-making institution that can usher us through this nightmare back into the daylight?

“..58 percent of voters believe their party is “too liberal.” But Newsom and Ocasio-Cortez found a welcoming audience in Europe.”

• Newsom and AOC Go to Europe to Pitch High Tax, High Regulation Policies (Turley)

This week, California Gov. Gavin Newsom (D) joined the many Californians now seeking their fortune elsewhere. The difference is that Newsom is planning to come back to California, even as billionaires, investors, and companies flee his state for greener pastures. Newsom and Democrats such as Rep. Alexandria Ocasio-Cortez (D-N.Y.) were selling a brave new world that looked a lot like the broken old world. It was an ironic moment. They were addressing countries at the Munich Security Conference that had previously destroyed their economies through socialist and far-left policies. The rush of liberal Democratic officeholders to Europe was telling. A new poll shows that a record 58 percent of voters believe their party is “too liberal.” But Newsom and Ocasio-Cortez found a welcoming audience in Europe.Read more …

The global elite gushed over Ocasio-Cortez and sat enraptured as she rattled off socialist platitudes. That included New York Times correspondent Katrin Bennhold, who thrilled the audience by treating it as a given that Ocasio-Cortez will run for president.Both Newsom and Ocasio-Cortez spoke of returning the U.S. to the good graces of the global elite. Newsom assured the Europeans that Trump’s reign is temporary, and that the U.S. will soon enough dismantle the “wrecking ball” that the administration has taken to the EU.Newsom offered his leadership and his state as the model, proclaiming that “California is a stable and reliable partner” for Europe. The model includes high taxes, massive spending programs and greater bureaucratic regulations — precisely the policies that have driven the European economy into its current stagnation. In other words, Democrats were in Europe to offer precisely what Newsom outwardly condemned: “doubling down on stupid.” When not fumbling with security questions about issues such as Taiwan, Ocasio-Cortez was demanding that wealth taxes be implemented in the U.S. “expeditiously.” Such a tax on billionaires’ wealth, including unrealized gains, is currently being pushed in California. The predictable result is that billionaires and other wealthy citizens are rushing to leave the state and taking their investments and companies with them.

Ocasio-Cortez had the audience at hello. Rather than having Vice President J.D. Vance shaming them for their attacks on free speech, the Europeans positively gushed over Democratic leaders pushing far-left agendas. It did not matter that such policies devastated European economies in the 20th century. In my book “Rage and the Republic,” I discuss the rise of support for socialism in both the U.S. and Europe. Many of those supporting it are young voters with no memory of the collapse of socialist economies in the 20th Century. In 1977, Labour Prime Minister James Callaghan pursued many of the same socialist policies, leading to what was called the “winter of discontent” as inflation hit 25 percent.

With the collapse of the British pound, the United Kingdom had to take the demoralizing step of securing a loan from the International Monetary Fund, as if it were a developing country. In France, François Mitterrand was also elected to pursue his “rupture with capitalism.” The French economy collapsed; Mitterrand quickly had to reverse himself and restore capitalist policies. That history is rarely discussed or taught today. The “warmth of collectivism,” as New York Mayor Zohran Mamdani put it, is back in vogue. It does not matter that, in Argentina, President Javier Milei is achieving one of the most impressive economic turnarounds in history — dramatically curtailing runaway inflation, government deficits and poverty — by reinstating free-market policies and reducing government spending.

What is chilling about Europe is that the EU has strangled growth with its increasingly centralized controls and massive bureaucracy. My book describes the instability of the EU and its global governance model. Europe is facing populist movements and, like many Democrats, the response has been calls for further consolidation of power. This included the creation of a new, uniform European corporate law, known as the “28th Regime.” With an economy crushed by a massive EU bureaucracy and regulations, the solution of many is all too familiar: borrow more money. French President Emmanuel Macron and others want to issue “Euro bonds” to spend their way into an economic recovery — another policy ideal shared with many on the American left.

This week was only the latest effort of the American left to strengthen an alliance with the EU. Previously, American leaders such as Hillary Clinton pushed the EU to censor Americans online after free speech protections were restored by companies like Twitter. Likewise, the American left is enamored with the EU’s global bureaucracy and regulations. Newsom and Ocasio-Cortez certainly found their element in Munich, and the EU certainly found the “reliable partners” it has longed for in creating “a new World Order with European Values.”

“..already in a “pre civil war” state, with “dire social instability,” “economic decline,” and “elite pusillanimity” as key precursors..”

• No Prospect’ Of EU Governments Preventing CIVIL WAR: British Army Colonel (MN)

Major unrest looms as political leaders kick the can down the road on immigration and integration failures, according to a seasoned military expert. Retired Colonel Richard Kemp, a former commander of British forces in Afghanistan, has issued a stark warning about the trajectory of social cohesion in Europe and Britain. Speaking to Israeli broadcaster i24News, Kemp highlighted how integration breakdowns have worsened over the past two decades, paving the way for inevitable conflict.“Things have been getting worse, getting bad, for many years, and they are only going to get worse,” Kemp stated, pointing to the reluctance of governments to confront the issues head-on.Read more …

Kemp, who also served in counter-insurgency operations in Northern Ireland and held intelligence roles in Westminster and the Cabinet Office, emphasized the lack of political will to address what he termed the “Islamification” of the UK. “No government, the government now or any prospective government of the UK, has the guts to stop it,” he said. “If they want to take strong action to prevent the Islamification of the UK, it’s going to mean big trouble for them. They don’t want trouble, they look four years ahead, they will kick the can down the road to someone else. ”This political shortsightedness, according to Kemp, is fueling the risk of “civil war in Europe.” He described a potential scenario resembling Northern Ireland but on a far more intense scale, where “you have the indigenous British and some of the immigrant population and the British government all on three different sides fighting against each other.”The officer attributed the slim chances of maintaining social order to democratic dysfunction and a lack of real choice for voters. “The big problem that British people have is they don’t have political choice. We don’t really live in a democracy,” Kemp asserted. “Whatever party you vote for, you get the same policies. That applies also to immigration and to the way in which the Islamic population is allowed to grow in numbers and dominance.” Kemp also noted the rise of Islamist politics in the UK, with Gaza-focused candidates winning seats in high-migration areas. “We’re going to see much more of that in the next election,” he predicted, referencing concerns within the Labour Party, including Health Minister Wes Streeting’s private message:

“I fear we’re in big trouble here – and I am toast at the next election. We just lost our safest ward in Redbridge (51% Muslim, Ilford S) to a Gaza independent. At this rate, I don’t think we’ll hold either of the two Ilford seats.”This isn’t the first time Kemp has raised the alarm. As we highlighted last year, he previously warned of growing unrest over mass migration and allegations of child sexual abuse by new arrivals, stating: “There’s only so much that I think people can take of that, and they’ve been very quiet up until now, the people in the UK have not really raised their voices against this, or in a very limited way only. But the more it develops, and it is going to develop more and more, the more unrest we are going to see.”

In that earlier commentary, Kemp went further: “And they have no option. I’m not encouraging or supporting this, but I think the people will feel they have no option than to take action into their own hand rather than rely on political leaders who are doing nothing, in their eyes. I think there is every likelihood, I don’t know what the timeframe is, but I would go so far as to not just predict civil unrest, but civil war in the UK in the coming years if this situation continues which I believe it will.” Kemp’s views align with broader expert analyses on Europe’s fracturing societies. King’s College London Professor David Betz has warned that countries like the UK, France, and Sweden are already in a “pre civil war” state, with “dire social instability,” “economic decline,” and “elite pusillanimity” as key precursors.

Betz stated: “We’re already past the tipping point, is my estimation… we are past the point at which there is a political offramp. We are past the point at which normal politics is able to solve the problem… almost every plausible way forward from here involves some kind of violence in my view.” Betz further urged: “I would probably avoid big cities. I would suggest you reduce your exposure to big cities if you are able,” and concluded: “Things are bad now, but they are going to get very much worse. Hopefully after they will get better, but you will have to go through the period of very much worse before you get there.”Echoing these concerns, academic Michael Rainsborough described Britain’s path as intentional rather than accidental, rooted in elite strategies of division.

He referenced historical policies under Tony Blair aimed “to rub the Right’s nose in diversity,” and warned of a “descent into what we termed dirty war,” involving internal repression and low-intensity strife. Rainsborough highlighted the erosion of national sentiment, noting public spaces filled with “Pride flags, Palestinian flags, Ukrainian flags — anything, it seems, but the Cross of St George.” He cautioned that such dynamics could lead to “Balkanisation — or, in the local idiom, Ulsterisation,” drawing parallels to Northern Ireland’s troubles. These repeated warnings from military and academic figures underscore a pattern: unchecked mass migration, elite detachment from public will, and a refusal to enforce borders are eroding the fabric of Western societies. As globalist policies prioritize appeasement over security, the pushback from ordinary citizens grows—demanding leaders who put their own people first, before the powder keg ignites.

https://twitter.com/Real_RobN/status/2023175702938554542?s=20 Tucker

https://twitter.com/VigilantFox/status/2023412775851110657?s=20Tucker Carlson explains how the FBI and CIA conducted a coup to take out President Richard Nixon with help from journalist Bob Woodward.

— conspiracybot (@conspiracyb0t) February 15, 2026

“Richard Nixon was taken out by the FBI and CIA, and with the help of Bob Woodward.”

“[Woodward] was that guy. And who is his main source for… pic.twitter.com/e1hjOd5zCu

Support the Automatic Earth in wartime with Paypal, Bitcoin and Patreon.