The United States has spent nearly $6 trillion on wars that directly contributed to the deaths of around 500,000 people since the 9/11 attacks of 2001. Brown University’s Watson Institute for International and Public Affairs published its annual “Costs of War” report Wednesday, taking into consideration the Pentagon’s spending and its Overseas Contingency Operations account, as well as “war-related spending by the Department of State, past and obligated spending for war veterans’ care, interest on the debt incurred to pay for the wars, and the prevention of and response to terrorism by the Department of Homeland Security.”

The final count revealed, “The United States has appropriated and is obligated to spend an estimated $5.9 trillion (in current dollars) on the war on terror through Fiscal Year 2019, including direct war and war-related spending and obligations for future spending on post 9/11 war veterans.” “In sum, high costs in war and war-related spending pose a national security concern because they are unsustainable,” the report concluded. “The public would be better served by increased transparency and by the development of a comprehensive strategy to end the wars and deal with other urgent national security priorities.”

[..] Wednesday’s report found that the “US military is conducting counterterror activities in 76 countries, or about 39 percent of the world’s nations, vastly expanding [its mission] across the globe.” In addition, these operations “have been accompanied by violations of human rights and civil liberties, in the US and abroad.” Overall, researchers estimated that “between 480,000 and 507,000 people have been killed in the United States’ post-9/11 wars in Iraq, Afghanistan, and Pakistan.” This toll “does not include the more than 500,000 deaths from the war in Syria, raging since 2011”..

The military-industrial complex asking for more money, though the US already spends ten times more than Moscow, which spends its money far more efficiently.

The US could lose a future war against Russia or China, a new report to Congress has suggested. America is losing its edge while rivals innovate and blend conventional, cyber and even non-military capabilities to gain the upper hand in key regions, according to a dozen national security experts tasked by politicians with scrutinising Donald Trump’s national defence strategy. The bipartisan group, led by former undersecretary of defence Eric Edelman and Gary Roughead, an ex-chief of naval operations, wrote: “The US military could suffer unacceptably high casualties and loss of major capital assets in its next conflict.

“It might struggle to win, or perhaps lose, a war against China or Russia. The United States is particularly at risk of being overwhelmed should its military be forced to fight on two or more fronts simultaneously. US military superiority is no longer assured and the implications for American interests and American security are severe.” The unquestioned dominance the US enjoyed at the end of the Cold War no longer holds, the expert commission concluded following interviews with key defence officials and reviews of secret documents, and Washington faces serious challenges to its interests in Asia, Europe and the Middle East. The experts identified Mr Trump’s tax reform bill – which greatly benefited the most wealthy – as having drained potential defence funding, alongside tax cuts by both his immediate predecessors.

The White House should look to increase taxation and slash entitlements to drastically increase funding available for the military despite the short-term “pain” the move would cause, they suggested. [..] the commission recommended that the base defence budget be increased by between 3 and 5 per cent above inflation over the next several years. According to the authors, Barack Obama’s 2011 Budget Control Act had had “pronounced detrimental effects on the size, modernisation, and readiness of the military”. Mr Trump made building up America’s armed forces a central campaign pledge and the experts said his strategy was on the right track, but did not go far enough.

The UK government has inflicted “great misery” on its people with “punitive, mean-spirited, and often callous” austerity policies driven by a political desire to undertake social re-engineering rather than economic necessity, the United Nations poverty envoy has found. Philip Alston, the UN’s rapporteur on extreme poverty and human rights, ended a two-week fact-finding mission to the UK with a stinging declaration that despite being the world’s fifth largest economy, levels of child poverty are “not just a disgrace, but a social calamity and an economic disaster”. About 14 million people, a fifth of the population, live in poverty, and 1.5 million are destitute, unable to afford basic essentials, he said, citing figures from the Institute for Fiscal Studies and the Joseph Rowntree Foundation.

He highlighted predictions that child poverty could rise by 7% between 2015 and 2022, possibly up to a rate of 40%. “It is patently unjust and contrary to British values that so many people are living in poverty,” he said, adding that compassion had been abandoned during almost a decade of austerity policies that had been so profound that key elements of the post-war social contract, devised by William Beveridge more than 70 years ago, had been swept away. In a coruscating 24-page report, which will be presented to the UN human rights council in Geneva next year, the eminent human rights lawyer said that in the UK “poverty is a political choice”.

Theresa May is battling to halt a growing revolt from the Tory right after half a dozen more backbenchers came out in favour of a no-confidence vote and the organiser of the rebellion publicly predicted more MPs would follow next week. The prime minister held a conference call with local association chairmen on Friday afternoon as she fought to head off a coup and sell her hard-won Brexit deal to a sceptical and partially hostile party. Her efforts came after the number of backbenchers calling publicly for a no-confidence vote in May’s leadership increased to 23. Rebellious MPs said they were confident of reaching the required threshold of 48 letters to Sir Graham Brady, the chairman of the party’s 1922 Committee. Adam Holloway, one of the MPs demanding a vote, said his letter had been delivered “with regret”.

But, complaining about May’s Brexit plans, he added: “You cannot have someone leading a mission who does not believe in the mission. The country needs leadership.” Others who went public with their demand to hold a vote included the former cabinet minister John Whittingdale, Maria Caulfield, Marcus Fysh, and Chris Green. David Jones was also named as being among those who had written to Brady. The party rules allow for a no-confidence vote if 15% of the party’s MPs – currently 48 – submit letters. Brady would organise a vote within a couple of working days of the threshold being met. Whittingdale said he wanted the government “to pursue a proper free trade agreement” but he believed that May was not willing to do so. “Therefore I felt there is no alternative but to seek a vote of confidence,” he said.

Cabinet ministers are planning a final push to remould parts of Theresa May’s Brexit strategy in a bid to find a way through the political crisis engulfing the government. Brexit-backing members of Ms May’s team will meet within days to discuss their approach, with a drive to change the text of the UK’s withdrawal agreement not ruled out. It emerged as Ms May sought to shore up her leadership following a wave of resignations, by appointing staunch ally Amber Rudd back to the cabinet six months after she was forced to resign over the Windrush scandal. Downing Street is on high alert as rebel backbenchers submitted further letters calling on Ms May to quit, ahead of a possible vote of no confidence next week. The Independent understands that House of Commons leader Andrea Leadsom is set to convene the meeting of Brexiteer frontbenchers to decide how Ms May’s strategy might evolve ahead of a critical European summit in just over a week.

There is “no question” of further Brexit negotiations if the deal struck by Theresa May is rejected, Angela Merkel has said. Speaking in Berlin, the German chancellor welcomed the deal but warned a chaotic exit was still possible as a “worst case” scenario. “We have a document on the table that Britain and the EU 27 have agreed to, so for me there is no question at the moment whether we negotiate further,” the Chancellor said. The warning follows EU officials close to talks saying the controversial document, which has been panned on all sides in Westminster, is “the best we can do” given the prime minister’s red lines and the bloc’s own rules.

Ms May has publicly stood by the plan, but the Huffington Post reported on Thursday night that allies of the prime minister are trying to win over Brexiteer rebels in the Conservative party with the offer of further concessions from Brussels if they fall in line. Speaking at a news conference ostensibly about her government’s digital strategy, Ms Merkel told reporters: “I am very happy that after long negotiations which were not easy, a proposal has been pulled together.

Drivers plan to disrupt traffic across France on Saturday by blocking roads, bridges and toll booths in a mass protest at rising fuel prices. Dubbed the “yellow vests” after the high-visibility jackets they use as their symbol, they are expected to muster in at least 700 locations. They accuse President Emmanuel Macron of abandoning “the little people”. Mr Macron admitted this week that he had not “really managed to reconcile the French people with its leaders”. Nonetheless, he accused his political opponents of hijacking the movement in order to block his reform programme.

Officials have warned that, while they will not stop the protests, they will not allow them to bring the French road network to a standstill. The price of diesel, the most commonly used fuel in French cars, has risen by around 23% over the past 12 months to an average of €1.51 ($1.71) per litre, its highest point since the early 2000s, AFP news agency reports. World oil prices did rise before falling back again but the Macron government raised its hydrocarbon tax this year by 7.6 cents per litre on diesel and 3.9 cents on petrol, as part of a campaign for cleaner cars and fuel. The decision to impose a further increase of 6.5 cents on diesel and 2.9 cents on petrol on 1 January 2019 was seen as the final straw.

The CIA has determined that Saudi Crown Prince Mohammed bin Salman ordered the assassination of journalist Jamal Khashoggi, NBC News reported Friday, citing a person briefed on the CIA’s assessment. The CIA declined NBC News’ request for comment Friday night. The Washington Post, which first reported the CIA findings, said the U.S. intelligence agency has high confidence in its findings. Khashoggi was a resident of the United States from Saudi Arabia, and he was a columnist for the Washington Post. The Saudi Embassy in Washington denied the reports. “The claims in this purported assessment are false,” the embassy said in a statement.

“We have and continue to hear various theories without seeing the primary basis for these speculations.” According to the Post’s report, the CIA looked into a phone call between the crown prince’s brother, who also serves as the Saudi ambassador to the U.S., Khalid bin Salman and Khashoggi. Sources told the Post that during that call, Khashoggi was directed to pick up documents at the consulate. While the Post said it was not clear whether Khalid bin Salman knew that Khashoggi would be killed, sources told the Post that he made the call at his brother’s request.

Turkey has a complete record of communications in and out of Saudi Arabia’s Istanbul consulate in the week of Jamal Khashoggi’s murder, a senior Turkish source has told Middle East Eye. The communications will be used to tear apart Riyadh’s latest version of the killing. These recordings, MEE has learned, have given Turkey a detailed picture of the various operatives, teams and missions issued from Saudi Arabia. And the contents of these communications, the source said, will turn the screw on a Saudi leadership that has sought to insulate itself from the scandal. According to the source, Turkey intends to drip feed the information gleaned from the communications to the media, as it has been doing ever since Khashoggi was brutally murdered by a team of 15 Saudis on 2 October.

The Khashoggi-related conversations that Turkish intelligence intercepted began when the Washington Post columnist first came to his country’s consulate on 28 September in an attempt to get papers required to remarry. The plan to kill Khashoggi, who was told to return to the consulate four days later, began to be hatched the moment he left the building, the source said. Key conversations, the source said, were those between Consul-General Mohammed al-Otaibi and Saudi security attache Ahmed Abdullah al-Muzaini. Muzaini has so far been spared much of the spotlight. It is unknown if he is one of at least 21 suspects detained in Saudi Arabia. But Turkish newspaper Sabah, which is close to the government, has described Muzaini as the brains behind the plot.

On the day of Khashoggi’s murder, the conversations of one man are especially important. MEE understands that Maher Abdulaziz Mutrib, the leader of the death squad sent to kill the journalist, made 19 calls to Riyadh on 2 October. [..] Puzzling to the Turkish source, however, is US intelligence’s knowledge of a phone conversation between Mutrib and Riyadh, where the team leader is apparently heard saying “tell your boss” following Khashoggi’s death. [..] When CIA chief Gina Haspel visited Turkey on 23 October for consultations over Khashoggi, she apparently arrived with a team of some 35 people. Amongst them were experts in deciphering recordings, linguists, people familiar with the Saudi accent and people who could enhance audio, the source said.

A Saudi team had planned all along to kill journalist Jamal Khashoggi and never tried to talk him into anything, a Turkish daily reports, citing recordings held by police that call Riyadh’s statement on the matter into question. An audio tape, allegedly in the possession of Turkish investigators, features a 15-minute conversation, in which “the Saudi team discusses how to execute Khashoggi,” the Turkish Hurriyet Daily wrote on Friday, citing its columnist Abdulkadir Selvi. In a recording that was allegedly made even before the journalist entered the Saudi consulate, “they are reviewing their plan, which was previously prepared, and reminding themselves of the duties of each member,” he said.

The Hurriyet report contradicts the statement made by the Saudi deputy public prosecutor, Shaalan al-Shaalan, who said that the team was actually sent to Istanbul to retrieve the journalist and bring him back to Saudi Arabia. A decision to murder the reporter –and outspoken critic of Riyadh– was allegedly taken by the head of the team after its ‘persuasion’ failed. Some other audio evidence obtained by the Turkish investigators also allegedly shows that the version of Khashoggi’s killing presented by Riyadh just does not add up, Selvi reports. “Khashoggi’s desperate attempts to survive could be heard in a seven-minute audio recording. There is no hint of anyone trying to persuade him,” he says, referring to another tape, which allegedly proved that “Khashoggi was strangulated in 7-8 minutes.”

Recall that the DNC itself is currently suing WikiLeaks and Assange for publishing the DNC and Podesta emails they received: emails deemed newsworthy by literally every major media outlet, which relentlessly reported on them. Until this current Trump DOJ criminal prosecution of Assange, that DNC lawsuit had been the greatest Trump-era threat to press freedoms – because it seeks to make the publication of documents, which is the core of journalism, legally punishable. The Trump DOJ’s attempts to criminalize those actions is merely the next logical step in this descent into a full-scale attack on basic press rights.

The arguments justifying the Trump administration’s prosecution of Assange are grounded in a combination of legal ignorance, factual falsehoods, and dangerous authoritarianism. The most common misconception is that unlike the New York Times and the Washington Post, WikiLeaks can be legitimately prosecuted for publishing classified information because it’s not a “legitimate news outlet.” Democrats who make this argument don’t seem to care that this is exactly the view rejected as untenable by the Obama DOJ. To begin with, the press freedom guarantee of the First Amendment isn’t confined to “legitimate news outlets” – whatever that might mean.

The First Amendment isn’t available only to a certain class of people licensed as “journalists.” It protects not a privileged group of people called “professional journalists” but rather an activity: namely, using the press (which at the time of the First Amendment’s enactment meant the literal printing press) to inform the public about what the government was doing. Everyone is entitled to that constitutional protection equally: there is no cogent way to justify why the Guardian, ex-DOJ-officials-turned-bloggers, or Marcy Wheeler are free to publish classified information but Julian Assange and WikiLeaks are not.

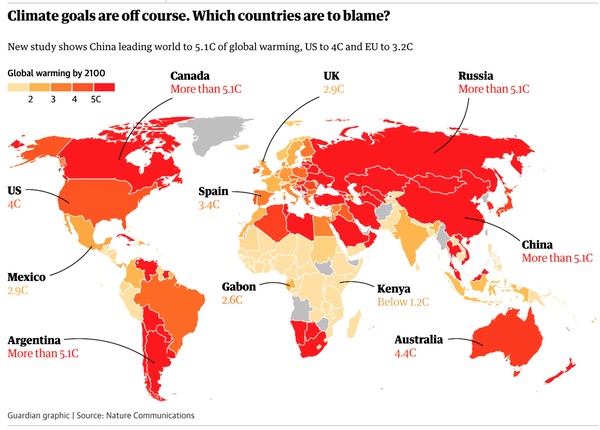

China, Russia and Canada’s current climate policies would drive the world above a catastrophic 5C of warming by the end of the century, according to a study that ranks the climate goals of different countries. The US and Australia are only slightly behind with both pushing the global temperature rise dangerously over 4C above pre-industrial levels says the paper, while even the EU, which is usually seen as a climate leader, is on course to more than double the 1.5C that scientists say is a moderately safe level of heating. The study, published on Friday in the journal Nature Communications, assesses the relationship between each nation’s ambition to cut emissions and the temperature rise that would result if the world followed their example.

The aim of the paper is to inform climate negotiators as they begin a two-year process of ratcheting up climate commitments, which currently fall far short of the 1.5-to-2C goal set in France three years ago. [..] India is leading the way with a target that is only slightly off course for 2C. [..] On the opposite side of the spectrum are the industrial powerhouse China and major energy exporters who are doing almost nothing to limit carbon dioxide emissions. These include Saudi Arabia (oil), Russia (gas) and Canada, which is drawing vast quantities of dirty oil from tar sands. Fossil fuel lobbies in these countries are so powerful that government climate pledges are very weak, setting the world on course for more than 5C of heating by the end of the century.

The late Prof Mick Moran, who taught politics and government at Manchester University for most of his professional life, had, according to his colleagues, once had “a certain residual respect for our governing elites”. That all changed during the 2008 financial crisis, after which he experienced an epiphany “because it convinced him that the officer class in business and in politics did not know what it was doing”. After his epiphany, Moran formed a collective of academics dedicated to exposing the complacency of finance-worship and to replacing it with an idea of running modern economies focused on maximising social good. They called themselves the Foundational Economy Collective, based on the idea that it’s in the everyday economy where there is most potential for true social regeneration: not top-down cash-splashing, but renewal and replenishment from the ground upwards.

Foundational activities are the materials and services without which we cannot live a civilised life: clean, unrationed water; affordable electricity and gas without cuts to supply; collective transport on smooth roads and rails; quality health and social care provided free at the point of use; and reliable, sustainable food supply. Then there’s the “overlooked economy” – everyday services such as hairdressing, veterinary care, catering and hospitality and small-scale manufacturing – which employ far more people, across a wider geographical range, than the “high-skill, hi-tech” economy with which recent governments have been obsessed.

For the Foundational Economy authors, focusing on the fundamental value of invisible and unglamorous jobs “restores the importance of unappreciated and unacknowledged tacit skills of many citizens”. It’s a way of looking at economics from the point of view of people rather than figures, and doing something revolutionary (yet so blindingly obvious) in the process. What is the point of “growth” if the basic elements of a decent life are denied to a large and growing number?

“The Kingdom affirms its total rejection of any threats and attempts to undermine it, whether by threatening to impose economic sanctions, using political pressures, or repeating false accusation,” a government source reportedly told the official Saudi Press Agency. “The Kingdom also affirms that if it receives any action, it will respond with greater action.” Hence, Saudi-owned Al Arabiya channel’s general manager Turki Aldakhil, in our call of the day, warned we could see an explosive move in oil prices. “If U.S. sanctions are imposed on Saudi Arabia, we will be facing an economic disaster that would rock the entire world,” he wrote in an op-ed.

“If the price of oil reaching $80 angered President Trump, no one should rule out the price jumping to $100, or $200, or even double that figure.” This mess could ultimately throw the entire Muslim world “into the arms of Iran, which will become closer to Riyadh than Washington,” Aldakhil said. “The truth is that if Washington imposes sanctions on Riyadh, it will stab its own economy to death, even though it thinks that it is stabbing only Riyadh.”

Saudi Arabia enjoys a privileged position both in geopolitical and economic terms. It will have a powerful hand to play if tensions with the US and the west escalate and it follows through with Sunday’s warning of retaliation. Its vast oil reserves – it claims to have about 260bn barrels still to extract – afford the most obvious advantage. The kingdom is the world’s largest oil exporter, pumping or shipping about 7m barrels a day, and giving Riyadh huge clout in the global economy because it wields power to push up prices. An editorial in Arab News by Turki Aldhakhil, the general manager of the official Saudi news channel, Al Arabiya, offers a hint of what could be in the offing.

He said Riyadh was weighing up 30 measures designed to put pressure on the US if it were to impose sanctions over the disappearance and presumed murder of Jamal Khashoggi inside the country’s Istanbul consulate. These would include an oil production cut that could drive prices from around $80 (£60) a barrel to more than $400, more than double the all-time high of $147.27 reached in 2008. This would have profound consequences globally, not just because motorists would pay more at the petrol pump, but because it would force up the cost of all goods that travel by road.

The Ecuadorian government has decided to partly restore communications for WikiLeaks founder Julian Assange. They were cut in March, denying the Australian access to the internet or phones and limiting visitors to members of his legal team. He has been living inside Ecuador’s embassy in London for more than six years. The Ecuadorian government said in March it had acted because Assange had breached “a written commitment made to the government at the end of 2017 not to issue messages that might interfere with other states”.

WikiLeaks said in a statement: “Ecuador has told WikiLeaks publisher Julian Assange that it will remove the isolation regime imposed on him following meetings between two senior UN officials and Ecuador’s President Lenin Moreno on Friday.” Kristinn Hrafnsson, WikiLeaks’ editor-in-chief, added: “It is positive that through UN intervention Ecuador has partly ended the isolation of Mr Assange although it is of grave concern that his freedom to express his opinions is still limited. “The UN has already declared Mr Assange a victim of arbitrary detention. This unacceptable situation must end. “The UK government must abide by the UN’s ruling and guarantee that he can leave the Ecuadorian embassy without the threat of extradition to the United States.”

Media outlets removed by Facebook on Thursday, in a massive purge of 800 accounts and pages, had previously been targeted in a blacklist of oppositional sites promoted by the Washington Post in November 2016. The organizations censored by Facebook include The Anti-Media, with 2.1 million followers, The Free Thought Project, with 3.1 million followers, and Counter Current News, with 500,000 followers. All three of these groups had been on the blacklist. In November 2016, the Washington Post published a puff-piece on a shadowy and up to then largely unknown organization called PropOrNot, which had compiled a list of organizations it claimed were part of a “sophisticated Russian propaganda campaign.”

The Post said the report “identifies more than 200 websites as routine peddlers of Russian propaganda during the election season, with combined audiences of at least 15 million Americans.” The publication of the blacklist drew widespread media condemnation, including from journalists Matt Taibbi and Glenn Greenwald, forcing the Post to publish a partial retraction. The newspaper declared that it “does not itself vouch for the validity of PropOrNot’s findings regarding any individual media outlet.” While the individuals behind PropOrNot have not identified themselves, the Washington Post said the group was a “collection of researchers with foreign policy, military and technology backgrounds.”

After years of Sears Holdings staying afloat through financial maneuvering and relying on billions of CEO Eddie Lampert’s own money, the 125-year-old retailer filed for bankruptcy. The filing comes more than a decade after Lampert merged Sears and Kmart, hoping that forging together the two struggling discounters would create a more formidable competitor. It comes after Lampert shed assets and spun out real estate, all to pay down the debt the retailer accumulated when that plan went askew. The company still has roughly 700 stores, which have at times been barren, unstocked by vendors who have lost their trust.

Many of the stores have never been visited by a generation of shoppers that can barely recall it was once the the country’s biggest retailer. Lampert, who has a controlling ownership stake in Sears, personally holds some 31 percent of the retailer’s shares outstanding, according to FactSet. His hedge fund ESL Investments owns about 19 percent. Ultimately, it was a $134 million payment that did the company in. The company had a payment due Monday it had not the money to pay.

With great flourish, Theresa May last week announced that she was lifting the borrowing cap which constrains local councils’ ability to finance new housebuilding. “We will only fix this broken market by building more homes,” the prime minister said. “Solving the housing crisis is the biggest domestic policy challenge of our generation. It doesn’t make sense to stop councils from playing their part in solving it. So today I can announce that we are scrapping that cap.” Nope. In reality, councils – or anyone else for that matter – building more homes will do very little to address the fundamental problem in the housing market, and if you want to understand why, there’s a new book which explains it.

‘Why Can’t You Afford To Buy A Home?’ by Josh Ryan-Collins – a researcher at University College London’s Institute for Innovation and Public Purpose – is about the phenomenon which he dubs ‘residential capitalism’. It follows on from his less snappily-titled volume ‘Rethinking The Economics of Land and Housing’, which was written jointly with fellow economist Laurie Macfarlane and policy wonk Toby Lloyd and published last year. Both books address the question of why a growing number of people are being priced out of the property market, with rising house prices accelerating away from household incomes. The answer is financialisation – and it is not an aberration, according to Ryan-Collins.

The ‘housing crisis’ needs to be understood primarily as a product of the banking system. For starters it’s not just a British problem; this is a trend which has gripped developed economies across the world over the past three decades. “Two of the key ingredients of contemporary capitalist societies, private home ownership and a lightly regulated commercial banking system, are not mutually compatible,” he writes. Instead they “create a self-reinforcing feedback cycle”. [..] In the early 1980s, business lending equated to around 40 per cent of GDP on average in advanced economies, while mortgage lending was around 25 per cent. By the time of the financial crisis, mortgage lending had grown to 75 per cent of GDP while business lending had only grown slightly, to 45 per cent.

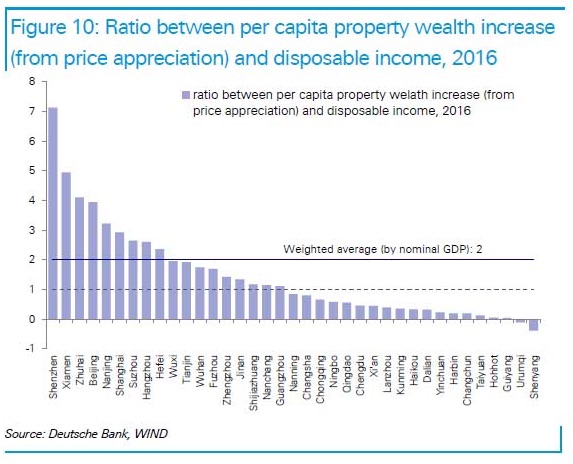

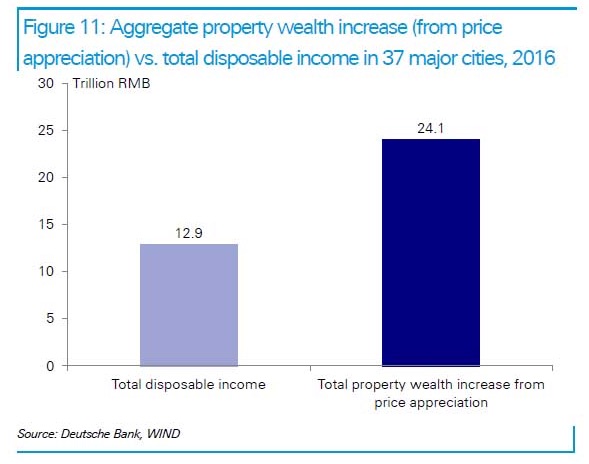

Last March, we discussed why few things are as important for China’s wealth effect and economy, as its housing bubble market. Specifically, as Deutsche Bank calculated at the time, “in 2016 the rise of property prices boosted household wealth in 37 tier 1 and tier 2 cities by RMB24 trillion, almost twice their total disposable income of RMB12.9 trillion.” The German lender added that this (rather fleeting) wealth effect “may be helping to sustain consumption in China despite slowing income growth” warning that “a decline of property price would obviously have a large negative impact.” Naturally, as long as the housing bubble keeps inflating and prices keep rising, there is nothing to worry about as the population will keep spending money buoyed by illusory wealth appreciation.

It is when housing starts to drop that Beijing begins to panic. Fast forward to today, when Beijing may be starting to sweat because whereas Chinese property developers usually count on September and October to be their “gold and silver” months for sales, this year has turned out to be different. As the SCMP reports, not only were sales figures grim for September, but the seven-day national holiday last week also brought at least two “fangnao” incidents – when angry, and often violent, homeowners protest against price cuts offered by developers to new buyers.

These protests are often directed at sales offices, with varying levels of intensity – from throwing rocks to holding banners and putting up funeral wreaths. The risk, of course, is that as what has gone up (wealth effect) will come down, and as home ownership has remained the most important channel of investment for urban households in China in the past decade, price cuts have become increasingly unacceptable and a cause for social unrest. Just last week, angry homeowners who paid full price for units at the Xinzhou Mansion residential project in Shangrao attacked the Country Garden sales office in eastern Jiangxi province last week, after finding out it had offered discounts to new buyers of up to 30%.

The European Union’s top Brexit negotiator says urgent talks with Britain’s point person did not result in their reaching agreement on outstanding issues. EU negotiator Michel Barnier said: “Despite intense efforts, some key issues are still open” in the divorce talks between the European Union and Britain. Barnier and his British counterpart, Dominic Raab, met in Brussels for surprise talks on Sunday. The discussion prompted rumors that a full agreement might be imminent, but Barnier says the future of the border on the island of Ireland remain a serious obstacle. He says the need “to avoid a hard border” between Ireland and the U.K’s Northern Ireland is among the unsettled issues. An EU official says no further negotiations are planned before an EU leaders summit on Wednesday.

The “Irish backstop” is the main hurdle to a deal that spells out the terms of Britain’s departure from the EU and future relationship with the bloc. After Brexit, the currently invisible frontier between Northern Ireland and Ireland will be the U.K.’s only land border with an EU nation. Britain and the EU agree there must be no customs checks or other infrastructure on the border, but do not agree on how that can be accomplished. The EU’s “backstop” solution — to keep Northern Ireland in a customs union with the bloc — has been rejected by Britain because it would require checks between Northern Ireland and the rest of the U.K.

Over the last three years, net exports shaved 0.5 percent off Italy’s quasi stagnant 1.1 percent GDP growth. And while exports in the first seven months of this year increased 4 percent from the year earlier, that did absolutely nothing to revive the country’s manufacturing output. The industrial production during the January-to-July period dropped at an annual rate of 0.5 percent. That, of course, bodes ill for business investments because the weakness in the manufacturing sector indicates plenty of spare production capacity. In other words, Italian businesses need no new machines and bigger factory floors; they already have what they need to meet the current and expected sales demand.

So, what’s left to support Italy’s jobs and incomes? Nothing — emphatically nothing — keeps screaming the German-run EU: Italy has no independent monetary policy, and, according to the EU Commission, the fiscal stance should remain frozen in a restrictive mode of indefinite duration. Italy knows what that means. Before the onset of the last decade’s financial crisis, and the German-imposed fiscal austerity, Italy’s budget deficit in 2007 was whittled down to 1.5 percent of GDP (compared to nearly 3 percent of GDP in France), the primary budget surplus (budget before interest charges on public debt) was driven up to 1.7 percent of GDP, helping to bring down the public debt to 112 percent of GDP from an annual average of 117 percent in the previous six years.

But then all hell broke loose once the Germans — defiantly rejecting Washington’s call to reason — set out to teach a lesson to “fiscal miscreants” by imposing austerity policies on the euro area’s sinking economies. Italy should never allow that to happen again. What, then, should Italy do? The answer is simple: Exactly what it says it wants to do in the 2019 budget passed last Thursday by an overwhelming majority in the Senate (61 percent of the votes) and in the Parliament’s Lower House (63.4 percent of the votes).

Angela Merkel’s conservative partners in Bavaria have had their worst election performance for more than six decades, in a humiliating state poll result that is likely to further weaken Germany’s embattled coalition government. The Christian Social Union secured 37.3% of the vote, preliminary results showed, losing the absolute majority in the prosperous southern state it had had almost consistently since the second world war. The party’s support fell below 40% for the first time since 1954. Markus Söder, the prime minister of Bavaria, called it a “difficult day” for the CSU, but said his party had a clear mandate to form a government.

Among the main victors was the environmental, pro-immigration Green party, which as predicted almost doubled its voter share to 17.8% at the expense of the Social Democratic party (SPD), which lost its position as the second-biggest party, with support halving to 9.5%. Annalena Baerbock, the co-leader of the Greens, said: “Today Bavaria voted to uphold human rights and humanity.” Andrea Nahles, the leader of the SPD, delivered the briefest of reactions at her party’s headquarters in Berlin, calling the results “bitter” and blaming them on the poor performance of the grand coalition in Berlin.

The late physicist and author Prof Stephen Hawking has caused controversy by suggesting a new race of superhumans could develop from wealthy people choosing to edit their and their children’s DNA. Hawking, the author of A Brief History of Time, who died in March, made the predictions in a collection of articles and essays. The scientist presented the possibility that genetic engineering could create a new species of superhuman that could destroy the rest of humanity. The essays, published in the Sunday Times, were written in preparation for a book that will be published on Tuesday. “I am sure that during this century, people will discover how to modify both intelligence and instincts such as aggression,” he wrote.

“Laws will probably be passed against genetic engineering with humans. But some people won’t be able to resist the temptation to improve human characteristics, such as memory, resistance to disease and length of life.” In Brief Answers to the Big Questions, Hawking’s final thoughts on the universe, the physicist suggested wealthy people would soon be able to choose to edit genetic makeup to create superhumans with enhanced memory, disease resistance, intelligence and longevity. Hawking raised the prospect that breakthroughs in genetics will make it attractive for people to try to improve themselves, with implications for “unimproved humans”. “Once such superhumans appear, there will be significant political problems with unimproved humans, who won’t be able to compete,” he wrote. “Presumably, they will die out, or become unimportant. Instead, there will be a race of self-designing beings who are improving at an ever-increasing rate.”

Every time I write about my ‘adventures’ in Greece for the Automatic Earth for Athens Fund, which I initiated in June 2015, I think it’s been way too long, but also every time I realize that I’ve already written so much about it (which makes every new article harder to write as well). Still, it’s been three months since the last one, and as always lots has happened; we’re not sitting still. As always, there’s a full list of previous articles at the bottom of this one.

To start with the latest development, I gave Konstantinos Polychronopoulos of O Allos Anthropos another €1,000 (the last funds I had) on March 15, which he needed to go to Lesbos, where he’s been asked to help set up a ‘Multi-Center’, to be jointly built by Greeks and refugees. It’s an initiative of a privately funded organization named Swisscross, to be located outside of the horrible Moria camp.

The center, which will have no sleeping facilities, is designed to make life more bearable for the refugees stuck inside Moria. It will provide shower rooms, laundry facilities, a kindergarten, a school (remedial teaching), a cinema, cafeteria and a restaurant.

O Allos Anthropos will be in charge of the restaurant, which will also be very much geared towards providing space, equipment, food and resources for the refugees themselves to cook. An often overlooked part of the refugee tragedy here in Greece is that preparing food is an important aspect of family- and community life, a source of dignity and pride, that has been taken away from them and replaced by real bad catering.

Thank you to the Texan girls who donated their Santa hat to me for Konstantinos on December 25. Perfect fit!

We’ve had the fifth anniversary of O Allos Anthropos in December, and of course Christmas. Then we had New Year’s, and on January 8 Greek New Year. February 16 was Tsikno Pempti (aka Charcoal Thursday or Greek Cholesterol Day), when everyone eats roasted meat – there’s a connection with carnival there-, and the Monday after that was Clean Monday, the end of carnival and the start of what is probably best compared to Lent, what once upon a time was a 40-day period of ‘fasting’ all the way to Easter. No Fat Tuesday or Ash Wednesday, as far as I could find.

Konstantinos and his people made sure that everyone, homeless and refugees, had a Christmas and New Year’s party like ‘normal’ people. Someone had donated a whole lot of turkey for Christmas, there was some meat to eat, and on Cholesterol Day there was even over 1000 kilos of meat to be spread to the Social Kitchens all over the country. It’s the kind of thing that makes people feel they do count, and they do belong, despite the misery they find themselves in.

Just as important, if not more, was the fact that all children who were present in the Big House in Athens, many of whom are homeless, received presents on Greek New Year. That means so much to them. Holidays without presents is cruel to children. I’ll sprinkle some pictures through this article.

Nobody gets left out at Christmas

Through all these events one thing that kept popping into my head was how close they brought joy and misery together. It’s pretty much priceless to see the happiness in people’s faces when they are served a real Christmas meal, a sign that they belong to the ‘human tribe’, that they ARE important, and there ARE people who care about them. Being able to do that for people is a very precious thing. As I said to someone also involved in refugee work a while ago: I’m sure that when we look back on this years from now, we’re going to say this is the best thing we’ve done in our lives, or right up there.

But at the same time, you can’t look at the joy without realizing where it comes from, why a simple meal or a Christmas present means so much; it comes from the every day misery so many people live in, in Greece these days. Looking at people knowing they’ll have no place to sleep that night, while it’s pretty cold outside too (colder than I thought Athens would be), it will never be easy. The misery is always close to the surface.

So I want to thank you once again, Automatic Earth readers, for having made much of this possible through your donations. You help make a lot of people feel better, help them eat, shower, give them a sense of dignity. In the process, you make me feel better too. Thank you. (Update: Saw a video the other day of a girl tattoo artist who set up a program to change self-mutilated arms into beautiful works of body art. Her reason to do this: “You don’t know what happiness is within yourself until you do something for another person.” That. You rock.

Happiness is a little girl’s face

That €1000 I gave Konstantinos was again the last money I had to donate to him, so I will call on you once more, and shamelessly so (which I allow myself to do because it’s for others, and it really helps). The Automatic Earth for Athens Fund has so far generated over $50,000(!) -one wonderful soul sent me a check for $10,000…-, and it’s a bit of a victim of its own success. The more there is, the more gets spent; we don’t want to not help people. And already the number of meals O Allos Anthropos can prepare and serve is dropping again, for monetary reasons; the number should be going up instead. We’re rowing against a strong current, which is awfully ironic, as you can see in the rest of this article.

I was reading an article earlier this week from AFP about an Italian program for refugees that shows everything that is wrong about how the crisis is being dealt with in Europe. Italy has started flying in Syrian refugees from Beirut, so they don’t have to spent a fortune on a risky sea voyage only to be locked up for months in camps. There are other ways. Kudos to Italy, and may many other countries follow their example:

Just before midnight in a sleepy district of Beirut, dozens of Syrian refugees huddle in small groups around bulging suitcases, clutching their pinging cellphones and one-way tickets to Italy. “Torino! Pronto! Cappuccino!” They practise random Italian words in a schoolyard in the Lebanese capital’s eastern Geitawi neighbourhood, waiting for the buses that will take them to the airport, and onwards to their new lives in Italy. Under an initiative introduced last year by the Italian government, nearly 700 Syrian refugees have been granted one-year humanitarian visas to begin their asylum process in Italy. The programme is the first of its kind in Europe: a speedy third way that both avoids the United Nations lengthy resettlement process and provides refugees with a safe alternative to crammed dinghies and perilous sea crossings.

[..] A country of just four million people, Lebanon hosts more than one million Syrian refugees. For members of Mediterranean Hope, the four-person team coordinating Italy’s resettlement efforts from Lebanon, “humanitarian corridors” are the future of resettlement. The group interviews refugees many times before recommending them to the Italian embassy, which issues humanitarian visas for a one-year stay during which they begin the asylum process for permanent resettlement. “It’s safe and legal. Safe for them, legal for us, says Mediterranean Hope officer Sara Manisera. “After people cross the Mediterranean on the journey of death, they are put into centres for months while they wait. But with this programme, there are no massive centres, it costs less, and refugees can keep their dignity,” she tells AFP.

Since March 20 was the 1st anniversary of the EU-Turkey refugee deal, many articles were published about what happened during the past year. And I haven’t seen one that was positive, which makes a lot of sense. There may be fewer refugees arriving in Greece now, but the situation of those who are in the country has gotten much worse. They are now prisoners, ‘housed’ in squalid conditions and with very little idea what will happen to them, how long their asylum applications will take to be heard, if they can or will be sent back to Turkey.

And now, with Erdogan getting ever more desperate in his quest to become the over-powerful president of Turkey, with just 4 weeks left till the referendum that should make him so, and with polls showing he’s behind, the EU-Turkey deal may well fall victim to petty politics. As it always looked to do. Who will suffer if that happens? The usual suspects, Greece and the refugees. The walls to fortress Europe are still shut tight. And it’s always election time somewhere.

Live cooking in Monastiraki Square, Athens

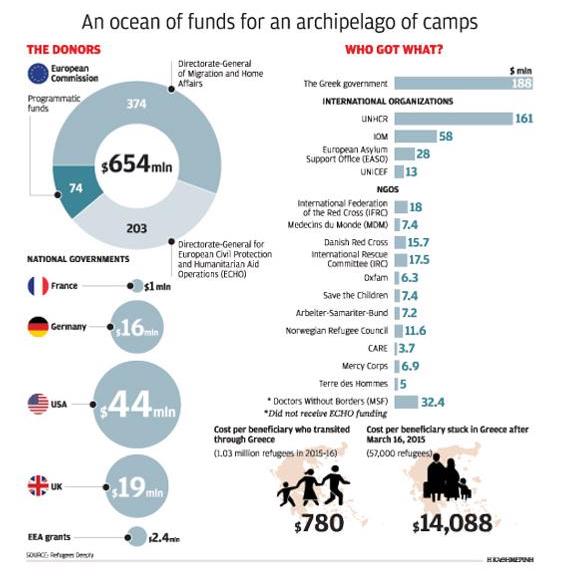

A friend recently translated something for me that Konstantinos had written on the O Allos Anthropos Facebook page. He said that every refugee who, before the EU-Turkey deal, passed through Greece on his/her way to Europe, cost the EU €800. For a family of 5 that adds up to €4,000, which would have been more than enough to pay for transport, stay at decent hotels and eat in normal restaurants for the duration of their trip (7-10 days). Suffice it to say, that was not what they got.

After the EU-Turkey deal made it impossible for refugees to leave Greece, €15,000 has been spent per capita. That is €75,000 per family of 5, more than enough to rent a villa on the beach, hire a butler and eat gourmet food for 8 months. Instead, the refugees are stuck in old abandoned factories with no facilities, in old tents in the freezing cold and in the rain, and forced to eat a dirt poor version of rice with chickpeas and lentil soup.

Then over the weekend I saw this confirmed in a graph issued by Refugees Deeply (with slightly lower numbers, but those are just margin errors). Note: March 16 2015 in the graph should of course read March 16 2016:

Refugees Deeply are a bit of a new kid on the block, they’re a year old, and I have no doubt they do care and have the best intentions. But since they operate throughout the world, not just in Greece, they run the same risk many international NGOs do, of spreading their resources too thin. Moreover, one thing that’s become obvious is that if you approach and treat Greece the same way as Somalia, for instance, you’re certain of making some major mistakes. Greece was a modern and prosperous country until Europe tried to turn it into Somalia.

What’s good is that it focuses on the failures of the Greek government in the never-ending refugee tragedy, because that was a part that had largely been missing. But what’s not so good is that it focuses almost exclusively on that. And that’s far from the whole story.

You see, there are three separate parties involved in the saga that have access to serious funding, and all three have their own reasons NOT to solve the problems to the best of their abilities. There’s the EU, there’s Greece, and there are dozens of NGOs, many of whom are large and operate internationally (iNGOs).

The EU wants to use Greece as a deterrent. It aims to create an image to the world of Greece as a sordid inhumane place that no potential refugee should ever wish to flee to. Because it doesn’t want any more refugees. 1 million refugees is too much for a continent, and a political union, of 500 million people. Rich Europe is overwhelmed by 0.2% more people. (Note: I’m not advocation open borders or anything, I’m just saying we need to take care of people in need, which is basically what the Geneva Convention says. Until we decide to stop bombing countries like Syria, and start rebuilding them, people will come to our territory to seek help.)

The EU also wants to put Greece in an even harder predicament, for politico-economic reasons. Brussels hands out a lot of money, but it doesn’t- from what I’ve been reading- seem to keep proper tabs of where that money is going, or how it’s spent. That way its hands are always clean: we gave all this money, you can’t blame us! And their hands will remain clean until someone calls them on their lack of oversight of what happens to taxpayers’ money. But taxpayers don’t even know who to call on, Europe is faceless.

The Greek government, too, likes the deterrent idea, albeit for slightly different reasons. While the EU has money to burn, Greece has none. The country doesn’t have the means to handle the refugee influx; it doesn’t even have the means to deal with its own domestic austerity-driven misery. The last thing it wants to do is give the impression that it is able to deal with the whole thing.

That might give refugees the idea that Greece is a good place to go to, and it might give Brussels the idea that Greece can handle this, so it must be doing fine. Also, there are (party-) political issues, there is rampant corruption, and there are egos. Greece is a country that politically, socially and economically has been robbed of any and all certainties and confidence. Where the poor take care of each other and the rich only have eye for themselves. But it’s hardly a functioning society anymore, it’s a bankruptcy fire sale.

The only thing surprising about the letter bombs (parcels) for Dijsselbloem, the IMF and Schäuble sent from Greece is that it took so long. Punishing a country into paying more than they could possibly afford is Versailles redux. But sure, the Greek part in the refugee crisis needs serious scrutiny as well: how Mouzalas can still be migration minister after the Refugees Deeply piece is hard to see. Then again, sources on the ground tell me it’s not -only- him, it’s the overall chaos and infighting.

And there are protests

The third party, the NGOs, is a bit tricky to talk about. For one, because there are so many of them, and in many lots of people work with the best possible intentions. That coming to a country where you don’t know the language or culture is not a perfect plan may often get lost in translation, certainly for unpaid bright-eyed young volunteers looking for a holiday but with a meaning.

It’s tricky also because NGOs, as I’ve written before, have become an industry in their own right, institutionalized even. As someone phrased it: we now have a humanitarian-industrial complex. Which in Greece has received hundreds of millions of euros and somehow can’t manage to take proper care of 60,000 desolate souls with that.

I’ve even been warned that if I speak out too clearly about this, they may come after Konstantinos and his people and make their work hard and/or impossible. This is after all an industry that is worth a lot of money. Aid is big business. And big business protects itself.

Still, if we’re genuinely interested in finding out how and why it is possible that hundreds of millions of taxpayer euros change hands, and people still die in the cold and live in subhuman conditions, we’re going to have to break through some of the barriers that the EU, Greece and the iNGOs have built around themselves.

If only because European -and also American- taxpayers have a right to know what has made this ongoing epic failure possible. And of course the first concern should be that the refugees have the right, encapsulated in international law, to decent and humane treatment, and are not getting anything even remotely resembling it.

Refugees Deeply quotes ‘a senior aid official’ (they don’t say from what) anonymously saying that €70 out of every €100 in aid is wasted. I see little reason to question that; if anything, it could be worse. But on the sunny side that means it need not take much to improve things. If ‘only’ one third of the aid were wasted, the portion that actually helps could potentially be doubled.

Most importantly: how do you waste at least €560 million (7/10 of €800 million) when that was intended for people in misery, in peril, in desperate need? I find it hard to wrap my mind around this, can’t seem to understand how actual people in Brussels can allow that to happen, when it’s about taxpayers’ money supposed to help people in grave distress. And I can’t figure out how Greece can allow that people freeze to death on its territory, when that could obviously have been easily prevented.

Nor can I fathom how iNGOs, who together have received hundreds of millions, can fail to build a number of decent winter camps, having been warned and funded months in advance. A lot of money goes to contractors, to the caterers who provide the awful meals at ten times the cost that O Allos Anthropos does, to the builders who don’t build, to the ubiquitous wheeler-dealers who can smell a cheap profit from miles away. And NGO executives want their often hefty salaries to be paid in time.

But even then I keep on thinking: where has all the money gone? They could have built or rented great facilities for all 60,000 refugees, and fed them, and schooled their children, and still have plenty of profit left. Why must greed be so unbridled?

In view of all this wasted money, we, Konstantinos and his people, can do so much more and so much better. But then again, of course, we can’t, because we don’t have that kind of funding, not even to spend wisely. And we won‘t either since we don’t want to comply with rules that would force O Allos Anthropos to refuse a meal to a hungry person, Greek or refugee, who doesn’t have ‘the proper ID’.

That ID thing fits ‘wonderfully’ into the EU model that has turned so many refugees into de facto prisoners, and has made so many Greeks destitute. In the end, aid must come from the heart, not from a wallet. Once humanitarian aid becomes a profit-based industry, as it so clearly has here, situations like the ones I describe here become inevitable. It all must come from the desire to help fellow human beings, and that should never be something that someone gets rich off of.

And compromising that in order to let the same machine fund you that has created so much mayhem feels like a road to some place between hell and nowhere. It’s sort of the opposite of Sartre’s “L’enfer c’est les autres” (Hell is other people). O Allos Anthropos means ‘The Other Human’. In other words, heaven is other people too. I could make a good case arguing that this is the very meaning of life, that we are here to help others. But that of course is just me. And thankfully and hopefully, bless you, many of our readers.

I don’t want to spend too much time being angry over the whole thing. The best we can all do is be positive, work with we have, and help as many people as we can. Of course Konstantinos and I, and many others, talk about becoming an NGO. But in his view, that would mean becoming a part of the machine, the industry, that does so much harm, wastes so much money and precious resources, and hurts so many needy people in the process.

Konstantinos is very much opposed to that, and I agree with him (not everyone always does). For him, it’s about never forgetting the reason why you do what you do, and certainly not forgetting it for money. But at the same time, yes, with more money we could do so much more. The number of projects that don’t get done, the people who don’t get fed, because the money is simply not there, is for lack of a better term, embarrassing. Especially, obviously, because that same money does get wasted somewhere else.

So we ask you once again for your help:

For donations to Konstantinos and O Allos Anthropos, the Automatic Earth has a Paypal widget on our front page, top left hand corner. On our Sales and Donations page, there is an address to send money orders and checks if you don’t like Paypal. Our Bitcoin address is 1HYLLUR2JFs24X1zTS4XbNJidGo2XNHiTT. For other forms of payment, drop us a line at Contact • at • TheAutomaticEarth • com.

To tell donations for Kostantinos apart from those for the Automatic Earth (which badly needs them too!), any amounts that come in ending in either $0.99 or $0.37, will go to O Allos Anthropos. Every penny goes where it belongs, no overhead. Guaranteed. It’s a matter of honor.

Please give generously.

A list of the articles I wrote so far about Konstantinos and Athens.

Beijing may have averted a crisis in its stock markets with heavy-handed intervention, but the world’s biggest corporate debt pile – $16.1 trillion and rising – is a much greater threat to its slowing economy and will not be so easily managed. Corporate China’s debts, at 160% of GDP, are twice that of the United States, having sharply deteriorated in the past five years, a Thomson Reuters study of over 1,400 companies shows. And the debt mountain is set to climb 77% to $28.8 trillion over the next five years, credit rating agency Standard & Poor’s estimates. Beijing’s policy interventions affecting corporate credit have so far been mostly designed to address a different goal – supporting economic growth, which is set to fall to a 25-year low this year.

It has cut interest rates four times since November, reduced the level of reserves banks must hold and removed limits on how much of their deposits they can lend. Though it wants more of that credit going to smaller companies and innovative areas of the economy, such measures are blunt instruments. “When the credit taps are opened, risks rise that the money is going to ‘problematic’ companies or entities,” said Louis Kuijs, RBS chief economist for Greater China. China’s banks made 1.28 trillion yuan ($206 billion) in new loans in June, well up on May’s 900.8 billion yuan.

The effect of policy easing has been to reduce short-term interest costs, so lending for stock speculation has boomed, but there is little evidence loans are being used for profitable investment in the real economy, where long-term borrowing costs remain high, and banks are reluctant to take risks. Manufacturers’ debts are increasingly dwarfing their profits. The Thomson Reuters study found that in 2010, materials companies’ debts were 2.8 times their core profit. At end-2014 they were 5.3 times. For energy companies, indebtedness has risen from 1.1 to 4.4 times core profit. For industrials, from 2.5 to 4.2.

Turbulence on China’s equity market is starting to rock the country’s property market. Investors are quickly pulling their cash out of housing they purchased to cover losses incurred by stock investments. Some have begun offering discounts on property due to difficulties with finding buyers. Continued turmoil on the stock market looks as though it will have a heavy impact on the country’s real estate market. China’s stock market rally also helped drive up sales of domestic homes. The Shanghai Composite Index surged 60% from its low of around 3,200 in early March, rising to 5,166 logged on June 12. China Securities Depository and Clearing said that the number of accounts opened to trade yuan-denominated A-shares reached 980,000 in May in Shenzhen, where property prices are climbing faster than other areas.

The figure accounted for roughly 80% of the total 1170,000 accounts in Guangdong Province, where large numbers of such account holders reside. Many newbie investors, who have just jumped into the stock market, likely gave a fresh impetus to the property market. China’s share price upswing prompted investors to reach out for new investments, including houses and other properties. A property analyst at major Chinese brokerage Guotai Junan Securities said that sales of luxury properties worth over 10 million yuan ($1.61 million) each for the first half of the year topped annual sales last year in Shanghai and Beijing. After this, Chinese stocks began to crumble. In early July, the Shanghai Composite Index dropped more than 30%, after hitting a seven-year high in mid-June.

Investors who suffered big losses on the stock market were forced to sell property and cancel real estate purchase agreements. The Hong Kong Economic Times said that consumers are increasingly asking real estate firms for grace periods on down payments for mortgage loans, as they run out of cash because of weak stocks. Some canceled home purchase contracts, while others canceled mortgage loans, according to China’s largest property developer China Vanke, which has a strong foothold in Shenzhen. Local media reported that an official at China Vanke is concerned about massive numbers of cancellations in the future.

For now I think we can safely say the panic is finally over, but none of the fundamental questions have been resolved and I expect continued volatility. Because I also think the market remains overvalued, however, I have little doubt that we will see at least one more very nasty bear market. Either way the panic and the policy responses have opened up a ferocious debate on China’s economic reforms and Beijing’s ability to bear the costs of the economic adjustment. Among these costs are volatility. Rebalancing the economy and withdrawing state control over certain aspects of the economy, especially its financial system, will reduce Beijing’s ability to manage the economy smoothly over the short term but it may be necessary in order to prevent a very dangerous surge in volatility over the longer term. Sunday’s Financial Times included an article with the following:

Critics of the measures unleashed by Beijing last week argue that they point to a fundamental tension at the heart of China’s political economy that a free-floating renminbi would test even more severely. The ruling Chinese Communist party, they argue, is ultimately incapable of surrendering control of crucial facets of the country’s economic and financial system. As one person close to policymakers in Beijing puts it: “The problem with this system is that it cannot tolerate volatility and markets are all about volatility.”

It’s not just that markets are about volatility. It is that volatility can never be eliminated. Volatility in one variable can be suppressed, but only by increasing volatility in another variable or by suppressing it temporarily in exchange for a more disruptive adjustment at some point in the future. When it comes to monetary volatility, for example, whether it is exchange rate volatility or interest rate and money supply volatility, central banks can famously choose to control the former in exchange for greater volatility in the latter, or to control the latter in exchange for greater volatility in the former.

Regulators can never choose how much volatility they will permit, in other words. At best, they might choose the form of volatility they least prefer, and try to control it, but this is almost always a political choice and not an economic one. It is about deciding which economic group will bear the cost of volatility.

A prominent economist says China’s banks are circling debt-stricken countries like Greece, offering an alternative to the brutal austerity measures proposed by the IMF and EU. Former adviser to the IMF and the World Bank, John Perkins, told the ABC’s The Business that China’s Asian Infrastructure Investment Bank (AIIB) and the BRICS bank were courting countries like Greece. Mr Perkins said he believed China had sent people to Greece to offer an alternative bailout deal. “If I were the finance minister running the system I would seriously be looking at that alternative. I think that the Chinese are presenting a competitive edge here,” he said.

Mr Perkins revealed in his international bestseller, Confessions of an Economic Hit Man, how international organisations like the IMF and the World Bank enslave countries like Greece by offering crippling and unsustainable loans which never deliver the economic growth they promise. He said he believed Greece and the other European countries in similar positions should turn to China as a means of breaking the debt spiral. “These austerity programs are not the right program, even the IMF said recently there has to be more debt forgiveness we have to readjust the debt and the Europeans don’t seem willing to do this,” he said. Mr Perkins was surprised by the IMF’s public criticism of the eurozone’s bailout deal this week and said it shows the growing influence of China’s banks.

“I think the motivation may have been the Chinese because the Chinese have stepped in before, in Ecuador and several other countries, and we now have these very powerful banks that the Chinese are heading up,” he said. Mr Perkins said the growing strength of the banks will result in a major shift of power away from the United States and European Union. He conceded that there is nothing to stop China from becoming another “economic hit man” but said the Chinese have a good record so far, particularly in South American countries like Ecuador. “I recently met with a minister of Ecuador – and he said ultimately that he has no idea what China will do but we do know that the IMF, the World Bank, the Europeans and the US have screwed us over,” he said. “They’ve put military bases around here and threatened us and China hasn’t done that, so right now we trust China more than the US.”

Europe’s next recession will “kill the euro” according to economist, writer and journalist David McWilliams. McWilliams, who is among the best economics commentators from the only Anglophone nation in the euro – Ireland, warns that we only have a few months to plan an alternative to the disastrous consequences on peripheral nations of what he sees as German hegemony. He describes the mismanagement of the euro currency as “both laughable and terrifying”. Marathon negotiation sessions are not conducive to clear headed, rational decision making on the future of a nation or the eurozone. Indeed, it smacks of coercion. He lambasts the suggestion offered that Greece could have a “temporary euro”, adding, “If the board and management of a public company dealt with problems like this, the share price would collapse. There is quite simply no corporate governance within the euro”.

David McWilliams believes that Germany is out control. France is no longer strong enough to offer a counterweight and Britain is happy to allow the circus to continue as they focus on potentially getting out of the EU. He describes last weekends negotiations in Brussels as a “teutonic kangaroo court”. Should Britain successfully navigate its way out of the EU, other countries will likely follow rather than exist as provinces of Germany. Norway and Switzerland have coped just as well from the outside as their EU neighbours. He makes the obvious, though seldom heard assertion that “when economic negotiations stop making economic sense, you should begin to question the motives of the EU”. Pointing to the plundering of Greek state assets to pay off creditors whilst forcing further austerity on the Greek people.

Each previous round of austerity has caused the economy to contract further – thus forcing Greece into a debt trap from which it cannot escape. We believe this is a crucial point. While Germany have played a major role it in the subjugation of Greece it is worth asking who truly benefits from economic negotiations that have stopped making economic sense. Could it be the large banks who, following a similar model imposed on countries in Latin America, Southeast Asia and Africa since the 1970’s, continue to extract wealth from the poorest people on earth? Has not almost every development in the EU in the past ten years served to consolidate the power of financial institutions at the expense of the citizenry?

McWilliams highlights the dramatic u-turn in policy where membership of the EU is now conditional. When Mario Draghi initiated the “whatever-it-takes” mass purchase of bonds of peripheral nations the message was clear – the euro is forever. Now, however, countries must bend to Germany’s demands which are the demands of politicians who want to keep their electorate happy if they are to be re-elected. “Countries that don’t play ball with Germany will see their banking system used against their democratically elected politicians. The banking system is the soft underbelly and the Germans are prepared to orchestrate bank runs in member states to get their way. This is not only new, it is outrageous.”

Deeper fiscal integration in the eurozone is a “huge mistake” that could end up tearing the bloc apart, Sweden’s former finance minister has warned. Anders Borg said forcing countries to cede sovereignty could trigger a right-wing backlash across Europe, as he predicted that countries such as Sweden and Poland, which are obliged to join the euro, would not adopt the single currency for “decades”. “If you go for tighter co-operation that basically brings higher taxes to the north to subsidise the south, you build in a political divide that is not sustainable in the long term,” he said. Mr Borg, who stepped down in October 2014, said that while the current structure of the eurozone was problematic, the only way to secure a broad-based recovery across the bloc without creating a political rift was to focus on competitiveness.

“We’re not talking about good and bad outcomes here, we are talking about only very problematic alternatives. If you push for further fiscal integration, moving more decisions to Brussels, taxing northern European countries more heavily and subsidising countries with long-term competitive issues and deep problems in the south you would obviously have a strong Right-wing reaction that would undermine the political support for that direction and create a less open, less liberal and less dynamic Europe,” he said. “I think there are great risks in connection to the course that we now hear from political integration. There is no voter base for that and it’s not certain either that you’re dealing with the right focus.”

Mr Borg said the eurozone and the wider EU area, which includes the UK, should focus on policies such as “completing the single market, voting for free trade co-operation with the US and increasing infrastructure investment”. “[Countries] are under-spending on infrastructure. We are under-spending in education. Our labour markets are over-regulated and we have tax levels for investment and work that are too high, so we need to do fundamental tax reforms and we need to fix our expenditure so that we are concentrating on the areas where public expenditures have most return.” Mr Borg, who voted for Sweden to join the euro in 2003, said the country’s membership was unlikely for “decades”. “It’s very difficult to argue today to your population that it’s a well functioning system,” he said.

Mr Borg, who predicted in 2012 that Greece would leave the euro, welcomed the news that the eurozone had opened the door to a third Greek bail-out package to begin. He said he was in “full agreement” with the IMF that creditors needed to write off some of the country’s debt “substantially”. “There is a need to establish a credible long-term programme for financing Greece. There is serious rethinking that has to be done on the Greek side but also on the creditors’ side. I would hope that people are ready to do this because the alternative is catastrophic for Greece. It’s clear that we’re not out of the woods yet,” he said.

Unravelling the tangled logic of Greece’s bail-out talks, Charlemagne has learned, is a little like trying to explain the rules of cricket to an American. How to make sense of a process in which Greek voters loudly spurn a euro-zone bail-out offer in a referendum, only to watch Alexis Tsipras, their prime minister, immediately seek a worse deal that is flatly rejected by the euro zone, which in turn presses a yet more stringent proposal to which Mr Tsipras humbly assents? Better, perhaps, not to try. After six months of this nonsense, little wonder everyone is depressed. The immediate danger of Grexit has at least been averted, after Mr Tsipras and his fellow euro-zone heads of government pulled a brutal all-nighter in Brussels this week.

But it comes at the price of a vast taxpayer-funded bail-out for Greece, worth up to €86 billion over three years, and a humiliating capitulation by Mr Tsipras. Greece’s economy is in tatters, its creditors are fuming and Europe’s institutions are in despair. Much to Britain’s disgust even non-euro countries have been sucked into the nightmare: a bridge loan designed to keep Greece afloat while the bail-out talks proceed looks set to tap a fund to which all EU countries have contributed. But wasn’t this week’s agreement a triumph for the shock troops of austerity? Hardly. Finland’s coalition, formed only two months ago, tottered at the prospect of funding a third Greek bail-out. The Dutch prime minister, Mark Rutte, has admitted that it would violate an election pledge he made in 2012.

One euro-zone diplomat says that 99% of her compatriots would say “no” to the bail-out if offered a Greece-style referendum. Even Angela Merkel, Germany’s chancellor and Mr Tsipras’s chief tormentor, is damaged. The deal, crafted largely by Mrs Merkel, Mr Tsipras and François Hollande, France’s president, has exposed the German chancellor to competing charges: of cruelty abroad and of leniency at home, notably among Germany’s increasingly irritable parliamentarians, who must vote twice on the Greek package. Europe’s single currency, designed to foster unity and ease trade between its members, has thus become a ruthless generator of misery for almost all of them.

More than five years have passed since May 2010, when Greece was enticed to borrow €73 billion from the IMF, EC and ECB with painful strings attached. That 2010 program, said the IMF, “had two broad aims: to make fiscal policy and the fiscal and debt position sustainable, and to improve competitiveness.” There was no emphasis on improving domestic economic growth or employment — just “competitiveness” in trade. The IMF speculated that “restoring confidence” would “lead to a growth recovery” in 2012. When that didn’t happen, another €154 billion in loans was provided. And the IMF blamed the bad “investment climate” on a “lack of confidence,” rather than any lack of after-tax income.

Prominent U.S. economists blame the seven-year depression in Greece on savage cutbacks in government spending. “The contraction in government spending has been predictably devastating,” wrote Joseph Stiglitz in February. And Paul Krugman later criticized the period “from 2009 to 2013, the last year of major spending cuts” in Southern Europe. In reality, however, Greek government spending rose from 44.9% of GDP in 2006 to 53.7% from 2009 to 2012 and to 60.1% in 2013. That 2009-2013 “fiscal stimulus” was precisely when the economy contracted — by 4.4% in 2009, 5.4% in 2010, 8.9% in 2011, 6.6% in 2012 and 3.9% in 2013. By contrast, the economy grew slightly in 2014 when government spending was “only” half of GDP.

That is, the economy fell when government’s share rose, and the economy rose when government’s share fell. What is rarely or never mentioned in the typically one-sided misperception of spending “austerity” is the other side of the budget — namely, taxes. The latest Greek efforts to appease creditors would raise corporate tax again to 28%, raise the 5% “solidarity surcharge” on personal incomes, and discourage tourism by raising the VAT on restaurants and island shopping. Looked at separately, each of these suffocating tax rates might appear almost reasonable. Looked at together, they are totally unreasonable.

To offer a Greek employee an extra €100 requires that €42 be first subtracted for Social Security tax, and then up to €46 more subtracted for income tax. Out of the original €100 of marginal labor cost, the remaining €14 of after-tax income going to a skilled worker could only buy about €10 worth of goods after value-added tax is paid. The tax wedge between what employers pay for labor and what workers have left to spend, after taxes, is 43.4% for a Greek family of four with average earnings — the highest in the OECD and more than double the comparable U.S. wedge of 20.6%. This demoralizing tax wedge, which grows even larger at higher incomes, clearly depresses hiring and working in the formal economy. It also helps explain why a third of the Greek labor force is self-employed (making tax avoidance easier).

“..an economic death spiral — contraction leading to banking failure, banking failure leading to contraction — first in Greece and, later on, elsewhere in Europe.”

The Greek parliament has now voted to surrender control of the Greek state to platoons of bureaucrats from Brussels, Frankfurt and Berlin, who will now re-impose the full policy regime against which Greeks rebelled in January 2015 — and which they again rejected, by overwhelming majority, in the referendum of July 5. The orders from Brussels will impose strict new rules on the Greek people in the interest of paying down Greece’s debt. In return, the Europeans and the IMF will put up enough new money so that they themselves can appear to be repaid on schedule — thus increasing Greece’s debt — and the ECB will continue to prop up the Greek banking system. A hitch has already appeared in the plan: the IMF, whose approval is required, has pointed out — correctly — that the Greek debt cannot be paid, and so the Fund cannot participate unless the debt is restructured.