Roger Sturtevant Auburn, Placer County, California March 27, 1934

Arseniy Yatsenyuk, PM in name only of certain parts of what was once Ukraine, today solemnly declared that Russia wants to start World War III. I am not kidding you. He said it this way: “The world has not yet forgotten World War II, but Russia already wants to start World War III.” An estimated 28 million Russians died in World War II, which might be more than in all other nations combined, so if there’s one country that has not forgotten it, it’s Russia. Yatsenyuk’s remark needs to be seen in that light, because he knows very well how it will be received in Russia. That’s why he says it. It’s such a dark sort of provocation that one might suspect it’s meant to start a war. It’s not that different from accusing a group of Jewish people of wanting to start a holocaust.

But Russia knows that Yatsenyuk may be a fool, but much more than that he’s a shill and a tool, and his words are scripted. As Russian FM Lavrov said a few days ago, the US runs the show in Ukraine. Which is why discontented protesters in eastern cities, who may be armed but are still Yatsenyuk’s own people and compatriots, can first be labeled terrorists, then have their own army set against them, and when that army refuses to shoot their own neighbors, see it be replaced by Special Forces, in which there can be no doubt Blackwater mercenaries play an increasingly large role. Putin said turning your army against your own people proves you’re a junta. He may have a point.

The little man inside says that Yatsenyuk is not the only scripted puppet in this wargame theater. Obama looks like he’s playing that same role. He had maintained a good working relationship with Lavrov and Vladimir Putin, which greatly helped defuse tensions in the Middle East. And now all of a sudden it seems as if America is no longer interested in defusing anything, no dialogue, no diplomacy, it’s all just words of war. Headlines in media such as Forbes have even started to talk about nuclear war. And you wonder; where is all this coming from? US Secretary of Hair John Kerry manages to outshout the foot in his mouth, and anything that comes out is takes by western reporters as gospel, damn proper journalistic standards. RT, labeled by Kerry today as a “propaganda bullhorn” (which is at least a little funny), used these words:

Kerry’s described protesters as those brandishing “the latest issue from the Russian arsenal, hiding the insignias on their brand new matching military uniforms, and speaking in dialects that every local knows comes from thousands of miles away.” Kerry again cited photographs – the most notorious of which Kiev claimed proved the involvement of Russians in Ukraine. “Some of the individual special operations personnel, who were active on Russia’s behalf in Chechnya, Georgia and Crimea have been photographed in Slavyansk, Donetsk, and [Lugansk],” he said.

The New York Times, which carried the photos and unverified claims from Kiev, published a climbdown two days later – ‘Scrutiny Over Photos Said to Tie Russia Units to Ukraine’, where it admitted failing to properly verify the Kiev photo dossier. The photographer who took and published a key photo contradicted Kiev’s claim it had been taken in Russia. While the State Department acknowledged the error, Kerry continued to refer to ‘evidence’.

Kerry cited NATO’s top military commander Gen. Philip M. Breedlove, who claims “a military operation” is being “carried out at the direction of Russia.” Contrarily EU intelligence head, Commodore Georgij Alafuzoff, assessed the so-called ‘green men’ are “mostly people who live in the region who are not satisfied with the current state of affairs.” Speaking on behalf of “the world,” Kerry “rightly judged” that Ukraine’s interim government is “working in good faith” and has implemented all the points of the Geneva agreement.

Now I don’t want to widely wax into a story about neocons, but I do wonder who got to Obama to make him do his about-face. For all of his long list of failures, he’s never before sought to draw blood in his public speeches. And if you want to figure out who’s started to overrule him, you easily, if not inevitably, end up in the far right corner of America. Some two weeks ago, I think it was Bloomberg that ran a piece saying Putin wouldn’t dare take Alaska, and I was thinking that is the craziest thing I’ve read in a while. And it doesn’t really matter that Putin last week at his press-op said Alaska was too cold to annex, it’s about the ideas US media try to plant in people’s brains. and get away with. It’s all such an insult to the few remaining American functioning neurons left, and they should not take that sitting down. I suggest you tell those blood thirsty octogenarian wankers like McCain and Brzezinski you don’t want to send your kids into another war. They won’t live to see the end of it anyway.

Besides, the US might be well advised to focus on another kind of war that picking up speed, that of global currencies. Unless all the shouting over Ukraine is merely an attempt to hide the fact that it has already conceded defeat, and all bets are now on the armed forces. The loss of value in the Chinese yuan (renminbi) is taking on “real proportions”, and that has Tyler Durden wonder what it all means:

The PBOC’s willingness to a) enter the global currency war (beggar thy neighbor), and b) ‘allow’ the Yuan to weaken and thus crush carry traders and leveraged ‘hedgers’ is about to get serious. The total size of the carry trades and hedges is hard to estimate but Deutsche believes it is around $500bn and as Morgan Stanley notes the ongoing weakness means things can get ugly fast as USDCNY crosses the crucial 6.25 level where losses from hedge products begin to surge. This is a critical level as it pre-dates Fed QE3 and BoJ QQE levels and these are pure levered derivative MtM losses – not a “well they will just rotate to US equities” loss – which means major tightening on credit conditions…

Remember, as we noted previously, these potential losses are pure levered derivative losses… not some “well we are losing so let’s greatly rotate this bet to US equities” which means it has a real tightening impact on both collateral and liquidity around the world… yet again, as we noted previously, it appears the PBOC is trying to break the world’s most profitable and easy carry trade – which has created a massive real estate bubble in their nation (and that will have consequences). [..]

In other words: Is Beijing merely trying to damage the USDCNY carry trade in an effort to diminish the role and size of the shadow banking system, or is that merely a sleight of hand behind which it – desperately – tries to regain the trade and related growth numbers it’s losing hand over fist? Durden:

The bottom line is the question of whether the PBOC’s engineering this CNY weakness is merely a strategy to increase volatility and thus deter carry-trade malevolence (in line with reform policies to tamp down bubbles) OR is it a more aggressive entry into the currency wars as China focuses on its trade (exports) and keeping the dream alive? (Or, one more thing, the former morphs into the latter as a vicious unwind ensues OR the market tests the PBOC’s willingness to break their momentum spirit). The escalation of the unwind in recent days suggests the vicious circle is beginning.

The flood of less than positive numbers emanating from China recently, despite the leadership’s attempts to play them down, tell us China is seriously hurting. And by now it’s large enough to spread that hurt around the world, if only to lessen its own pain. What Durden doesn’t mention but also plays a major role here is Japan’s troubles in exports and trade deficits. If China plays beggar thy neighbor, the closest main neighbor it has after all is Japan. And the yen is already down 20%. Which is painful for China. The Chinese government pretends it can do a controlled demolition of its credit bubble, but how many times has that been done successfully? As anyone knows who’s ever stuck needles and pins in a fully inflated air balloon, bubbles tend to pop in unexpected ways and places. Durden quotes Russell Napier:

“Mercantilist alchemy transmutes China’s external surpluses into foreign exchange reserves and renminbi. But with capital outflows from China at record highs, those surpluses are only maintained due to its citizens’ foreign-currency borrowing. Bank-reserve and M2 growth are already near historical lows and are driving tighter monetary policy. This will lead to severe credit-quality issues and force the authorities to accept a credit crunch or opt for a major devaluation of the renminbi. They will do the latter; and despite five years of QE, the world will get deflation anyway.”

I think it should be obvious that the US is not the first and foremost casualty here for now, since the Euro picks up much more of the hurt for now, late as the EU is to the currency musical chairs game (that really is a good metaphor). But when you start talking trade in general and and carry trades in particular, the USD is still the reserve currency, and even if Europe suffers the first blows and will stumble if not start falling, the American dollar has a lot more exposure. In unflattering terms not meant to hurt anyone, the US has a much bigger and therefore slower ass to put down on that chair when the music stops.

That, I would think, is a bigger risk to Washington than Ukraine war games. Unless, as I said earlier above, it has already conceded defeat. If that’s the case, a war over pipeline access may have to be seen in a whole other light.

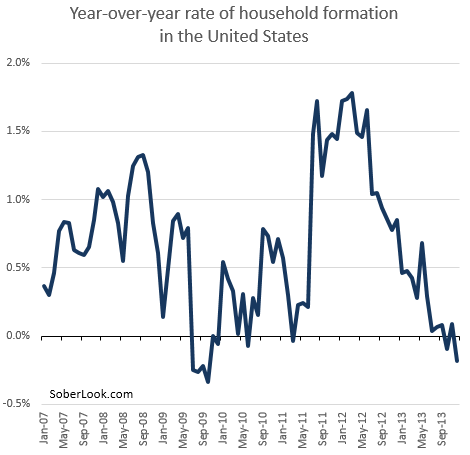

Lance Roberts: “The housing market is driven by what happens at the margins.” Well, household formation is frozen over solid. That’s what happens.

• Schadenfreude: Economists “Stunned” By Housing Fade (STA)

The housing market is driven by what happens at the margins. At any given point, there are a finite number of people wanting to “buy” a home and those that have a “for sale” sign in their yard. As with all markets, changes in the housing market are driven by the “supply/demand” equation. There is notably five important points that should be considered.

1) What is forgotten by the majority of economists and analysts is that individuals buy “payments,” not “houses.” Incremental increases in interest rates have a direct effect on a buyer’s “willingness” and “ability” to make certain monthly payments. Since, the majority of American’s are already primarily living paycheck-to-paycheck, any increase in the monthly payment may change both affordability and qualification for a loan.

2) Since individuals are “backward looking,” increases in interest rates may put a hold on activity as they “hope” that the payment, mortgage rate or home price they just missed out on will be available again soon. While individuals will eventually adjust upward, it will take some time for them to become “convinced” that a change has permanently occurred.

3) Many of the homes that have been purchased to date were by “all cash” buyers and institutions for conversions to rental properties. Now, with “price-to-rent” ratios reach levels of low profitability – the demand for that activity is decreasing. As I stated last year: “We are likely witnessing the beginning of that slowdown.” Furthermore, with institutions now moving to liquidate their rental investments either through direct sale or IPO – the increase in supply without an increasing pool of available and willing buyers could intensify downward pressure.

4) In order to continue to drive the housing recovery forward you need fresh entrants into the housing market in the form of household formations. As discussed by Walter Kurtz recently:

“The biggest issue, however, remains household formation. As of the end of last year, for example, the number of American households was not growing at all. This is likely due to record low marriage rates as well as a slew of other factors (lack of employment, wage growth, etc.). Whatever the reason, household formation needs to stabilize before we see stronger results in the US housing market.”

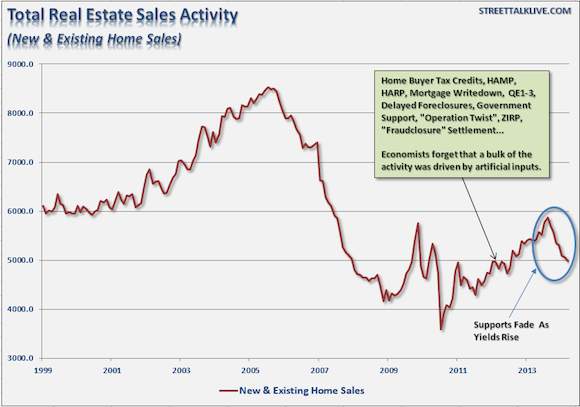

5) Lastly, with the Federal Reserve now tapering it ongoing stimulative activities and the government support programs either ended (cash for houses) or losing effectiveness (HAMP, HARP) the support for housing activity is fading. The chart below shows the Total Real Estate Sales Activity Index (TRESAI), which is a composite of the seasonally adjusted new and existing home sales data. For the purpose of this article, which is focusing on the actual buy and sell of homes, this is the most appropriate index.v

Forever blowing bubbles.

• How The Fed Ravaged The Main Street Housing Market, Again (David Stockman)

Now that the $5k suits are riding out of town on their John Deere lawnmowers, the “flash” boom in housing prices during the past 20 months is showing its true nature. It was the handiwork of the Fed’s free money gift to Wall Street. In less than two years more than 400,000 busted mortgages were scooped up by LBO funds on the theory that single family suburban housing had become a new “asset class”—-and that the “buy-to-rent” investment models put together by spreadsheet jockeys was the next Big Thing.

There was even going to be a new version of the Wall Street slice-and-dice machine—this time in the form of securitized rental payment streams rather than mortgage payments. That way renters in Scottsdale AZ could send their rent checks to Wall Street where they would be forwarded in pieces to the proverbial Norwegian fishing village retirement fund. But the grand scheme didn’t attain lift-off—other than to drastically and suddenly inflate housing prices in the default-ridden lower-end of the bombed-out sub-prime housing markets. In some areas, prices exploded upwards by 25-50% in less than two years, but that wasn’t evidence of healing and recovery as was so loudly brayed by Wall Street and Fed economists.

It was just fast-ignition hot money piling into another momentum trade. All the other factors which were supposed to get better according to the spreadsheet models, however, didn’t track their appointed paths. In the real world the cost of rehabbing the foreclosures purchased in bulk on the courthouse steps ended up higher; vacancy rates fell more slowly than modeled; renter churn was greater; maintenance costs were higher; rents rose more slowly; and the Norwegian fishing villages were not quite so eager to buy the latest product from Wall Street’s meth labs.

‘Albert Edwards said the next shoe to drop in world the economy is a systematic attempt by China to export its deflation to any other sucker willing to accept it… ‘

• Is China Exporting Deflation Worldwide By Driving Down Yuan? (AEP)

The Chinese Yuan weakened yet again this morning, punching through the key line of 6.25 against the dollar. It is almost back to where it was two years ago. This is the biggest story in the global currency markets. Yuan devaluation has reached 3.1% this year. The longer this goes on, the harder it is to accept Beijing’s story that it is one-off measure to teach speculators a lesson and curb hot money inflows. The US Treasury clearly suspects that the Chinese authorities have reverted to their mercantilist tricks, driving down the exchange rate to keep struggling exporters afloat. Officials briefed journalists in Washington two weeks ago in very belligerent language.

The Treasury’s currency report this month accused China of trying to “impede” the market by boosting foreign reserves by $510bn last year to $3.8 trillion – “excessive by any measure”. It gave a strong hint that China is disguising its reserve accumulation. You don’t have to dig hard. Simon Derrick from BNY Mellon said a recent buying spree of US Treasuries and agency debt by Belgium of all places looks like a Chinese front.

Holdings by entities in Belgium have jumped to $341bn from $169bn last August. This would appear to explain how China’s FX reserves have kept rising to $3.95 trillion even as its custody holdings in the US itself have been falling. If so, China is playing dirty pool. Hans Redeker from Morgan Stanley says China seems to have adopted a “beggar thy neighbour policy” to counter the slowdown at home and soak up excess manufacturing capacity. Albert Edwards from Societe Generale said in a note today that China is “sliding inexorably towards deflation”. Factory gate prices have been falling for 25 months in a row. [..]

Mr Edwards said the next shoe to drop in world the economy (leaving aside the Donbass) is a systematic attempt by China to export its deflation to any other sucker willing to accept it by driving down the yuan. Those countries that have failed to build adequate defences by keeping inflation safely above 1% could face a nasty shock when this happens. The eurozone looks like the sucker of last resort. A Chinese deflationary tide would push Southern Europe over the edge. Perhaps that is why the ECB’s Mario Draghi sounded ever more alarmed today in his efforts to talk down the euro today.

‘About to get serious’.

• The “Real Pain” Is About To Begin As Yuan Slumps To 19-Month Low (Zero Hedge)

The PBOC’s willingness to a) enter the global currency war (beggar thy neighbor), and b) ‘allow’ the Yuan to weaken and thus crush carry traders and leveraged ‘hedgers’ is about to get serious. The total size of the carry trades and hedges is hard to estimate but Deutsche believes it is around $500bn and as Morgan Stanley notes the ongoing weakness means things can get ugly fast as USDCNY crosses the crucial 6.25 level where losses from hedge products begin to surge. This is a critical level as it pre-dates Fed QE3 and BoJ QQE levels and these are pure levered derivative MtM losses – not a “well they will just rotate to US equities” loss – which means major tightening on credit conditions… [..]

Remember, as we noted previously, these potential losses are pure levered derivative losses… not some “well we are losing so let’s greatly rotate this bet to US equities” which means it has a real tightening impact on both collateral and liquidity around the world… yet again, as we noted previously, it appears the PBOC is trying to break the world’s most profitable and easy carry trade – which has created a massive real estate bubble in their nation (and that will have consequences). [..]

The bottom line is the question of whether the PBOC’s engineering this CNY weakness is merely a strategy to increase volatility and thus deter carry-trade malevolence (in line with reform policies to tamp down bubbles) OR is it a more aggressive entry into the currency wars as China focuses on its trade (exports) and keeping the dream alive? (Or, one more thing, the former morphs into the latter as a vicious unwind ensues OR the market tests the PBOC’s willingness to break their momentum spirit). The escalation of the unwind in recent days suggests the vicious circle is beginning. Finally, putting aside speculative trader P&L losses, many of which are said to be of Japanese origin and thus will hardly enjoy much or any PBOC sympathies, here is CLSA’s Russel Napier on what the long-tern fate of the Renminbi will be:

“Mercantilist alchemy transmutes China’s external surpluses into foreign exchange reserves and renminbi. But with capital outflows from China at record highs, those surpluses are only maintained due to its citizens’ foreign-currency borrowing. Bank-reserve and M2 growth are already near historical lows and are driving tighter monetary policy. This will lead to severe credit-quality issues and force the authorities to accept a credit crunch or opt for a major devaluation of the renminbi. They will do the latter; and despite five years of QE, the world will get deflation anyway.”

Might be.

• Might Be Time to Short the Euro (A. Gary Shilling)

In parts 1 and 2 of this series, I explored looming deflation in Europe and why central banks fret over it. The European Central Bank is gearing up to depress the euro, which it blames for much of the deflation threat in the euro area, or at least the portion it can influence. The ECB reduced its overnight reference interest rate from 0.5% to 0.25% in November. If it cut the rate again, the ECB would join the Federal Reserve and the Bank of Japan with rates of essentially zero. With all the central-bank-created liquidity sloshing around the world, these rates are largely symbolic. Yet another ECB reduction could make foreign investment in the euro area less attractive, to the detriment of the euro.

Currently, ECB member banks are paid nothing on their deposits. A negative rate – charging banks to leave their money at the central bank – would encourage them to lend and invest elsewhere. That would push down returns in the euro area and discourage foreign investors, also to the detriment of the euro. Austrian central banker Ewald Nowotny backs this approach. Bundesbank President Jens Weidmann and Bank of Finland Governor Erkki Liikanen, like Nowotny members of the ECB’s governing council, have expressed interest. Denmark introduced negative rates on deposits in 2012, but no major central bank has followed so far.

The Fed, the Bank of England and the Bank of Japan have bought government securities extensively, but such quantitative easing would be difficult in the euro area. One reason is that corporate and other types of financing are concentrated in the banks and not in the bond markets, as in the U.S., where QE works its way into the economy rapidly. QE would also be harder because there are 18 euro-area countries and, therefore, 18 bond markets for the ECB to consider. Still, the ECB could purchase securities backed by mortgages, auto and small-business loans, corporate debt, and packages of bank loans, as well as government debt. ECB President Mario Draghi and governing council members Liikanen, Weidmann, Jozef Makuch of Slovakia and Benoit Coeure of France have all expressed interest.

US banks can do whatever they want. Too big to fail.

• US Banks Return To Lax Standards And Subprime Loans (Guardian)

Where are the profits of yesteryear? Hard to find, it seems. Certainly, the glee with which Jamie Dimon, CEO of JP Morgan Chase, and his fellow top bankers welcomed the government-assisted recovery in banking (and banking profits) in 2009 has dwindled and faded. Indeed, most of the tailwinds helping banks have become headwinds holding them back. Homeowners aren’t refinancing any more, and new home sales hit their lowest levels in eight months in March. The result? Double digit dips in mortgage lending, already buffeted by an uptick in long-term interest rates. Fixed-income trading is in the doldrums, too. That leaves new mortgage lending at a 14-year low.

Bond trading is in no better shape, as risk aversion keeps market participants sitting grumpily on the sidelines. Commodities trading has been profitable, but has attracted far too much regulatory scrutiny – and legal bills – to make it worthwhile. (Deutsche Bank and JP Morgan Chase are just two to have walked away from those businesses.) “Revenue growth in banking this decade for the banks is on pace to be worst since the Great Depression,” says Mike Mayo, an analyst with CLSA Americas LLC, who has tracked the banking industry for about a quarter of a century. Just to make matters worse, a recent source of extra profits – the release of loan loss reserves, once set aside to provide a cushion against bad loans – is running low. It’s going to get tougher for the banks to make their earnings look better than they really are.

If all these falling profits are the banks’ problem, their solution to the problem could end up being worse.That’s because whenever growth falters, profit-hungry banks have a history of taking on more risk: risk they can’t afford, that they don’t understand or that they can’t manage. They relax lending standards (remember no-doc loans and the subprime lending debacle?) or underwriting standards (the junk bond and leveraged buyout boom of the late 1980s; and during the dot.com bubble). Allegations of mis-selling of products, ranging from annuities to complex derivatives, multiply like rabbits left unattended.

Part of the Russia sanctions.

• S&P Cuts Russia to Step Above Junk (Bloomberg)

Russia’s sovereign rating was cut to the lowest investment level at Standard & Poor’s and may face further downgrades if growth deteriorates and the U.S. and Europe apply wider sanctions over the conflict in Ukraine. S&P cut Russia’s rating to BBB- from BBB after lowering its outlook to negative in March, according to a statement today. S&P last downgraded Russia in December 2008. “The tense geopolitical situation between Russia and Ukraine could see additional significant outflows of both foreign and domestic capital from the Russian economy and hence further undermine already weakening growth prospects,” S&P said in the statement.

The U.S. and its allies have an additional list of sanctions ready and will act on it if there is no progress de-escalating the crisis in Ukraine, where security forces are moving against pro-Russia separatists in the country’s east, U.S. President Barack Obama said yesterday in Tokyo. Russia was placed on review for a downgrade by Moody’s Investors Service on March 28 and Fitch Ratings cut its outlook to negative. “The decision is partially expected — Russia is almost in recession, even without sanctions,” Dmitry Dorofeev, a money manager at BCS Financial group, said by phone.

Corporations are just slushing zombie money around, nothing productive for miles. These days, that’s called the global financial system.

• Merger Boom Tarnishes Ratings as Borrowing Soars (Bloomberg)

Corporate dealmaking that helped propel the Standard & Poor’s 500 stocks index to a record is playing out differently for debt investors, who must contend with the biggest threat to credit grades since 2009. With borrowings to fund mergers and acquisitions accelerating amid an improving economy, the number of credit-ratings cuts linked to such deals is exceeding increases by the most since the fourth quarter of 2009, according to data from Moody’s Analytics. The firm’s credit-assessment unit lowered 96 ratings during the year ended March, while raising the rankings on 78.

The damage to balance sheets is coming amid a growing chorus of concerns that a sixth year of record-low interest rates engineered by the Federal Reserve has left bond prices overvalued and allowed borrowers to get away with financings that they wouldn’t be able to do in normal times. Valeant Pharmaceuticals International Inc. is pursuing Allergan Inc. in a takeover that may drop the Botox maker to junk status. “Perhaps we’re being far too complacent about the outlook for credit,” John Lonski, chief financial markets economist at the Moody’s unit in New York, said by telephone April 9. “We might be shocked to find out that by 2016, we have more problems on the credit front than we currently anticipate in part because companies are now and over the near-term using leverage a little bit too aggressively.”

Think anyone will do time for this?

• GM Confirms Multiple Investigations Under Way (WSJ)

General Motors confirmed in a government filing that it is under investigation by federal prosecutors, the Securities and Exchange Commission, a state attorney general, Congress and the National Highway Traffic Safety Administration for its handling of a recent rash of recalls, including those involving 2.6 million cars with faulty ignition switches. GM formally confirmed the existence of a federal criminal probe of the recall by the U.S. Attorney for the Southern District of New York, in its quarterly report to the SEC filed today. GM had earlier reported an 82% drop in first quarter earnings, largely because of a $1.3 billion charge related to the ignition switch and other recalls.

GM said it believes it is “cooperating fully” with requests for information from the various investigating agencies, although it is paying fines to NHTSA for missing an April 3 deadline to respond fully to questions from the auto-safety regulator. It isn’t clear from GM’s filing what aspects of the ignition-switch recall matter the SEC or the unidentified state attorney general are investigating. The company says in the filing it isn’t currently able to estimate the potential costs of lawsuits or investigations tied to the ignition recall, but adds resolving the probes could have a “material adverse impact” on the company’s finances.

They should go for $130 billion. And criminal trials. But they won’t. BofA is too big to fail.

• US To Seek More Than $13 Billion From BofA Over RMBS (Bloomberg)

U.S. prosecutors are seeking more than $13 billion from Bank of America Corp. to resolve federal and state investigations of the lender’s sale of bonds backed by home loans in the run-up to the 2008 financial crisis, according to people familiar with the matter. The settlement would come on top of the $9.5 billion the bank agreed last month to pay to resolve Federal Housing Finance Agency claims, said two people who asked not to be named because the negotiations are private. A deal could come within the next two months, the people said.

If the Justice Department gets its way, the case against Bank of America will eclipse JPMorgan Chase’s record $13 billion global settlement over similar issues in November. That settlement, which included a $4 billion agreement with the FHFA, encompassed loans JPMorgan took over with its purchases of Washington Mutual and Bear Stearns. Bank of America, the second-biggest U.S. lender, is among at least eight banks under investigation by the Justice Department and state attorneys general for misleading investors about the quality of bonds backed by mortgages amid a drop in housing prices. Many of the loans in question were inherited by Bank of America when it purchased subprime lender Countrywide and Merrill Lynch, the people said.

First, Help to Buy blows a giant bubble. When it starts deflating, tougher lending rules are introduced. These guys got some nerve.

• Horse, Barn: Tougher Mortgage Rules For UK Homebuyers (Guardian)

Homebuyers and remortgagors will face tougher checks before being granted a mortgage under new rules for lenders that come into force on 26 April. The changes, which follow the City regulator’s mortgage market review (MMR), will see would-be borrowers asked to give more detail about their spending when they apply for a home loan. Borrowing will be based on how much they have left after regular expenditure, rather than on their income, and lenders will have to check that people can still afford repayments if interest rates rise.

Lloyds Banking Group, which is the country’s biggest mortgage lender and offers mortgages through Halifax, Lloyds Bank and Bank of Scotland, said the changes meant interviews with new customers could take around 15 minutes longer, taking the average length up to around two hours. It said the additional questions would be focused on imminent changes to their lives that can be backed up with evidence. For example, this could relate to someone planning to cut back on their working hours or take out a loan. The regulator behind the new rules, the Financial Conduct Authority (FCA), said they would “hardwire common sense into the mortgage market”, and prevent a return to irresponsible lending that took place in the runup to the credit crisis.

It’s time for Steve Keen.

• BOE Chief Economist-To-Be: “It’s Time To Rethink Everything” (Zero Hedge)

Andrew Haldane, who is well known among readers as being one of the most outspoken and truthy central bankers in the world, will become Bank of England’s Chief Economist in June. That fact is what makes his comments – however factually honest – extremely uncomfortable for the Keynesian status quo DSGE modelers alive and well in every central bank in the world. To summarize his thoughts in the following letter – the models are useless and it’s time to rethink everything… Via Andrew Haldane,

• In the light of the financial crisis, those [macro and micro model] foundations no longer look so secure. Unbridled competition, in the financial sector and elsewhere, was shown not to have served wider society well. Greed, taken to excess, was found to have been bad. The Invisible Hand could, if pushed too far, prove malign and malevolent, contributing to the biggest loss of global incomes and output since the 1930s. The pursuit of self-interest, by individual firms and by individuals within these firms, has left society poorer.

• The crisis has also laid bare the latent inadequacies of economic models with unique stationary equilibria and rational expectations. These models have failed to make sense of the sorts of extreme macro-economic events, such as crises, recessions and depressions, which matter most to society. The expectations of agents, when push came to shove, proved to be anything but rational, instead driven by the fear of the herd or the unknown.

• The economy in crisis behaved more like slime descending a warehouse wall than Newton’s pendulum, its motion more organic than harmonic.

• … we are a co-operative species every bit as much as a competitive one. This is hardly a surprising conclusion for sociologists and anthropologists. But for economists it turns the world on its head.

• In this light, it is time to rethink some of the basic building blocks of economics.

Bit of a hype perhaps?

• How A 700-Page Economics Book Surged To No. 1 On Amazon (CBS)

“Capital in the Twenty-First Century,” at first glance, seems an unlikely candidate to become a best-seller in the U.S. After all, it’s 700 pages long, translated from French, and analyzes centuries of data on wealth and economic growth. But the book, from economist Thomas Piketty, is now No. 1 on Amazon.com’s best-seller list, thanks to rave reviews and positive word of mouth. Beyond that, however, the book has something else going for it: “Capital” has hit a nerve with Americans with its message about income inequality.

An economics book becoming a best-seller is “unusual, and it speaks to the fact that Piketty is addressing a really fundamental issue,” said Lawrence Mishel, president of the Economic Policy Institute. “He has his finger on a great dynamic, and is changing the terms of our discussion. Rather than asking why low-wage workers are not doing well, it focuses on the wealthy and the role of capital.” The main thrust of the book is that, in the jargon of economists, the rate of return on capital has far outstripped the rate of economic growth. The book also portrays the post-World War II period of economic progress across all classes as an anomaly, not the norm.

The result: mounting income inequality, as the wealthiest Americans gain a growing share of the nation’s economic spoils – and political power. “When the rate of return of return on capital exceeds the rate of growth of output and income, as it did in the nineteenth century and seems quite likely to do again in the twenty-first, capitalism automatically generates arbitrary and unsustainable inequalities that radically undermine the meritocratic values on which which democratic societies are based,” Piketty writes.

• ‘Bitcoin Better Than Any Form Of Money That Has Ever Existed Before’ (RT)

Bitcoin is shaping up to be the currency of the future, enabling people to send and receive money anywhere in the world free of charge in a currency that govts are unable to control, Roger Ver, bitcoin investor and the CEO of Memory Dealers told to RT.

RT: Why do you think this Moscow Bitcoin conference is important?

Roger Ver: Bitcoin is a global phenomenon. It’s important to everybody on the entire planet. Anybody who uses money, bitcoin is important to them.RT: Russia isn’t banning bitcoin but when it comes to Russia’s central bank and prosecutor’s office, they are against it; does that suggest bitcoin is not welcome, is that going to change do you think?

RV: I don’t have a direct insight into what goes on inside of Russia but one guy at the conference just a moment ago when I asked that same question, he said nobody cares, so that may be the attitude of the people within Russia. And at the end of the day nobody can block or stop or prevent anyone using bitcoin if they want to, it’s just a protocol and it just works.RT: If you had to name three reasons why bitcoin is better than traditional money what would they be?

RV: Bitcoin is the first time anyone can send and receive any amount of money with anyone anywhere on the planet. So that’s one reason. You can now send and receive that money without having to pay any fees to Western Union or a bank or anybody like that, so there’s a second. And it’s impossible to have your account frozen or seized, that’s just three out of many. I can go on for hours and hours. But bitcoin is so much better than any form of money that’s ever existed before in the history of the world.RT: What other reasons are there?

RV: No counterfeiting, right? When you or I counterfeit money, we go to jail for counterfeiting, when central banks do it, they call it fancy names like quantative easing or economic stimulus. With bitcoin that can’t happen. There’s a fixed supply of bitcoins, there will never be more than 21 million bitcoins and that’s a fantastic benefit that bitcoin has over traditional government issue currencies. Another issue is that there are no charge backs, once you’ve been paid with bitcoin you know the money is yours and you don’t have to worry about it being taken away from you months later like you do with a credit card or other forms.

This is a huge development in Europe. The Netherlands have for decades lived grandly off the sales of their giant gas field. Now the rest of Europe is going to need Putin even more.

• Netherlands To Become Net Gas Importer In 10 Years – IEA (RT)

Europe’s second largest gas producer, the Netherlands, could shift from exporter to importer within a decade, says the International Energy Agency (IEA). The study suggests seeking alternative energy sources in nuclear, unconventional fuels or renewables. Declining production at the large Groningen gas field will turn the Netherlands into a net importer of natural gas, the IEA report says. The IEA sees opportunities for developing indigenous resources, as well as re-assessing its energy security and looking at different cost-effective paths. Since 2005 the Netherland’s consumption of renewable energy has increased from 2.3% to 4.5% in 2013 and is expected to reach 14% by 2020 and 16% by 2023, the IEA says.

“Promoting lower-carbon energy use, especially in industry and transport, makes economic sense and can improve both sustainability and competitiveness,” said Maria Van der Hoeven, IEA Executive Director. She says the Netherlands can benefit from cooperating with its neighbors in competitive electricity markets, particularly for combining reserves to meet demand peaks at the regional level.

“Integrating the electricity systems across borders with new interconnections ensures resource efficiency. Europe’s energy markets need to be efficient and make renewable energy an integral part,” Van der Hoeven said. Meanwhile the Netherlands remains one of the most fossil-fuel-intensive economies among IEA members. The share of fossil fuels in the Netherlands energy mix is above 90%. The IEA says the country needs to develop a longer term energy policy up to 2030, which would involve huge investment into, and the promotion of, green projects like energy efficient buildings.

Not surprising, but good that David put it into hard data: the EIA contradicts its own numbers.

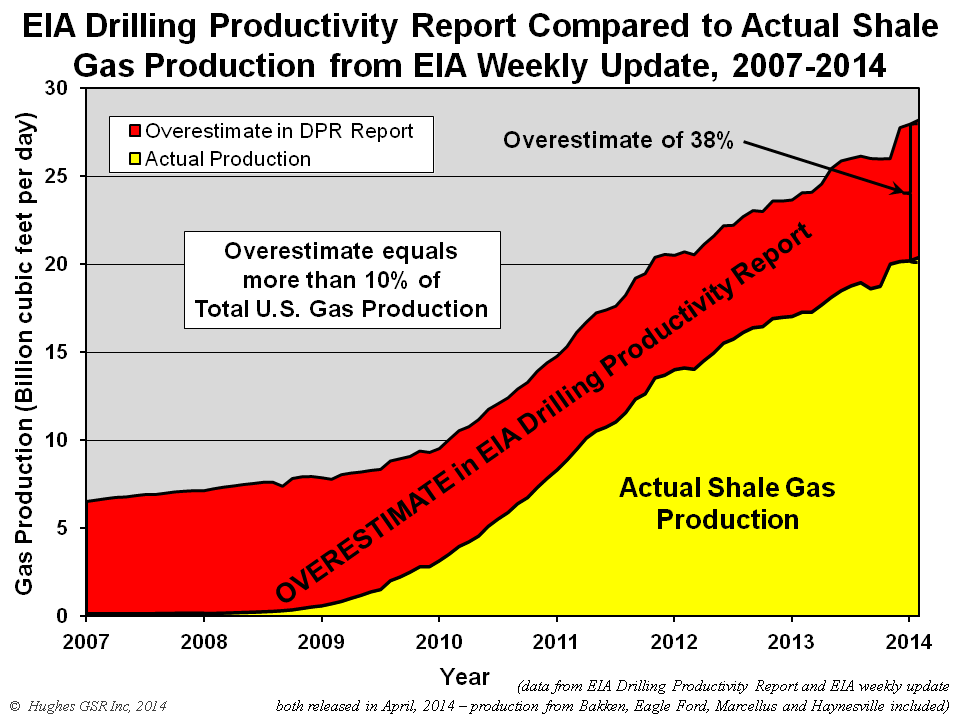

• The EIA Is Seriously Exaggerating Shale Gas Production (David Hughes)

“Natural gas output from US’ Marcellus edges closer to 15 Bcf/d: EIA” declared the headline in Platts that attracted my attention, since the latest data on the Marcellus shale gas play of PA and WV indicated production was less than 12 bcf/d. This headline was based on the latest issue of the EIA’s new monthly Drilling Productivity Report published April 14. Reading further, the article claimed that the Haynesville shale play “peaked at about 10 Bcf/d in 2012”, when in fact it had peaked at closer to 7 bcf/d in 2011. These errors are serious exaggerations of reality and bear further investigation, as the EIA Drilling Productivity Report is widely read and quoted in the media.

Fortunately the EIA also publishes independent production data by shale play in its Natural Gas Weekly Update. A check of production data for the Marcellus revealed that it was at 11.8 bcf/d in February and that the Haynesville had indeed peaked at 7.2 bcf/d in November 2011. These figures are also corroborated by Drillinginfo, a commercial database which is used by the EIA. There are four shale plays in common between the two EIA reports: the Marcellus, Haynesville, Bakken, and Eagle Ford.

Let’s go!

• Family Awarded $3 Million In First US Fracking Trial (RT)

After three years of legal wrangling, a Texas family has won its case against a company engaged in hydraulic fracturing near their home. The family, which suffered tangible health deterioration after the fracking began, was awarded $3 million. A Dallas jury ruled Tuesday in favor of the Parr family, which sued Aruba Petroleum in 2011 after each member of the family noticed a decline in health that, their attorneys argued in court, was the result of dozens of gas wells surrounding their home in Wise County, Texas. The family was awarded nearly $3 million in what is believed to be the first fracking trial in US history.

“They’re vindicated,” the family’s attorney David Matthews wrote in a blog post. “I’m really proud of the family that went through what they went through and said, ‘I’m not going to take it anymore’. It takes guts to say, ‘I’m going to stand here and protect my family from an invasion of our right to enjoy our property.’ “It’s not easy to go through a lawsuit and have your personal life uncovered and exposed to the extent this family went through.” Aruba Petroleum will appeal the jury’s decision, according to MSNBC. The company argues that there are dozens of gas-drilling operations in the area, thus it is difficult to tell who is responsible for the family’s degenerative health. Other companies that own wells around the Parr’s home settled with the family, EcoWatch reported.

This is from research done by UK grocery giant Asda. Kudos for taking the initiative.

• 95% Of Fresh Produce Already At Risk From Climate Change (Guardian)

Some 95% of the entire fresh produce range sold by Asda is already at risk from climate change, according to a groundbreaking study by the supermarket giant. The report, which will be published in June, is the first attempt by a food retailer to put hard figures against the impacts global warming will have on the food it buys from across the world. Asda, which is owned by Walmart, brought in consultants PwC to map its entire global fresh produce supply chain against the models being used by the Intergovernmental Panel on Climate Change.

Chris Brown, Asda’s senior director for sustainable business, said the study shows the impacts are already being felt and will get progressively worse as time goes on. The results have already gone to the highest levels of management and Brown said some of the results were surprising. “It did highlight things which we did not expect to see as well as quantifying the impacts.” “Quite a lot of the debate is illuminated by opinions, this provides some much-needed data.” The only produce that would remain unaffected by a rise in temperatures would be those with easily moved production, like fresh herbs.

Brown said the results show that it is imperative that supermarkets start to think strategically about how to cope with the impacts of rising emissions. Tackling views that the UK food supply might benefit from a warmer climate, Brown said: “If we do nothing, we will leave a rubbish legacy for our children and the future would go one of two ways. One is that rich western economies can try to buy their way out of trouble although that is morally not acceptable, and emerging economies such as China will equally be able to use their economic power to secure access to food.

Home › Forums › Debt Rattle Apr 25 2014: Is America Preparing For The Wrong War?