Marion Post Wolcott Farmer’s son making sorghum molasses, Racine, West Virginia Sep 1938

Yesterday, we saw that despite a tepid rebound in new home sales, the underlying numbers are far from promising. In particular, prices, which had been holding up despite sagging sales, are down YoY. We also saw that some big investors are now -openly – betting against housing. We saw that the Fed is as a rule so far off in its official forecasts that one needs to wonder about its level of honesty. But what I think was the main item yesterday is the fact that world trade has landed in negative growth territory. The implications of that are hard to overestimate. Global GDP until now has been up quite a bit more than that of the US, Europe, Japan. But now all are tipping their toes on the other side of the much feared red line. And it’s high time for everyone, including Americans, to start realizing what’s going on, and that it looks nothing like the brightly colored pictures of grandeur just around the corner that are consistently being painted for your consumption.

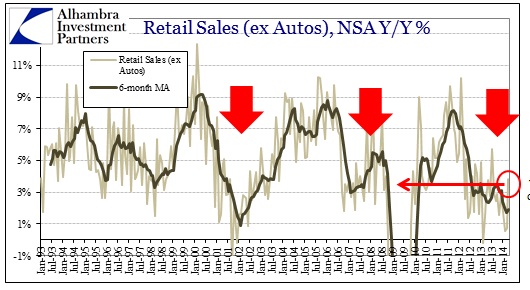

Yesterday afternoon Bloomberg reported that US Q1 retail numbers were hugely and painfully below analysts’ estimates.

U.S. Retailers Missing Estimates by Most in 13 Years

U.S. retailers’ first-quarter earnings are trailing analysts’ estimates by the widest margin in 13 years after bad weather and weak spending by lower-income consumers intensified competition [..] … the expectations the chains are missing have been significantly lowered. While analysts now project retailers’ earnings fell an average of 4.1%, back in January they had estimated a 13% gain. Lower- and moderate-income consumers had little discretionary spending power [..]

That difference is so stunning one must wonder what goes on. As Alhambra Investment Partners’ Jeffrey P. Snider does, in a piece posted by David Stockman:

We keep hearing about pent up demand as if it is a foregone conclusion. For some, particularly orthodox economists, it really is – it has to be. If there is no pent up demand awaiting some ephemeral trigger, then their whole theory of the economy is wrong, from the ground up. [..]

Back-to-school sales were “unexpectedly” low, leading to whispers about retailers stuffed with inventory. That was fine, though, because Christmas sales were going to be the first real treat since before the panic. Even though Kmart started advertising its Christmas deals in September, that was dismissed as idiosyncratic. Then it turned out Kmart was actually emblematic and Christmas (for the retail industry) ended up as the worst since 2009. But that, too, was fine, because holiday hangover would be less significant. So retailer expectations, as with those for overall economic growth, were tremendously optimistic until it snowed in winter.

In the space of only three months or so, retailers went from (yet again) expecting fortune and finding instead more “mysterious headwinds.” But this is beyond the usual ridiculous affair, to miss by that much implies something far more serious. To go from +13% to -4% that quickly is an outrage, not just to the economy as it sinks further under the weight of these commandments, but also in those businesses that continue to rely on orthodox forecasts and assumptions.

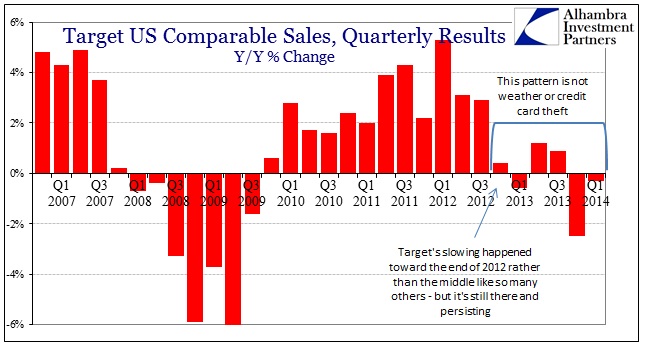

In another article, at Real Clear Markets, Snider backs up the numbers with a look at sales at the biggest US retail chains:

Target, Staples And The Same Poor Mess (Alhambra)

At what point do “struggling consumers” begin to register as something more than a mysterious headwind? The state of US households is more like a recession than some tangential factor that is just running below expectations. The results speak for themselves – there was an obvious slowdown in 2012 followed by revenue and spending patterns that very much equate to late 2007 and early 2008. [..] The ups and downs throughout the chronology of the past seven years sure look like two recession cycles. It really doesn’t get much clearer than this:

You can make the case that the current down cycle is nowhere near as bad as 2008, especially into 2009, but that is an exceedingly low standard. We have been promised repeatedly and assuredly that there would be a recovery, even to the point of having to withstand four separate, immense QE paroxysms. To what gain? To what loss? If it was only Target and the rest of the retail industry was doing fine, then you can dismiss these results (actual dollars spent as they are, in contrast to sentiment surveys) as Target’s individual missteps. But Wal-Mart has shown the same exact pattern, though actually faring far worse in terms of its 2008 comparisons. Wal-Mart and Target are #1 and #3 in terms of size.

That suggests that consumers were downgrading their shopping impulses in 2008 from more expensive outfits to bare bones essentials. In other words, the Great Recession almost benefitted Wal-Mart by shifting the whole retail scale toward “cheap.” Now, in 2013 and 2014, they can’t even get away with that. It’s almost as if the country and economic system have grown far poorer throughout this “recovery.”

Of course he doesn’t mean ‘it’s almost as if’, he means America has gotten poorer and is well on its way to get poorer still. The very prolific Snider takes on US housing while he’s on a roll:

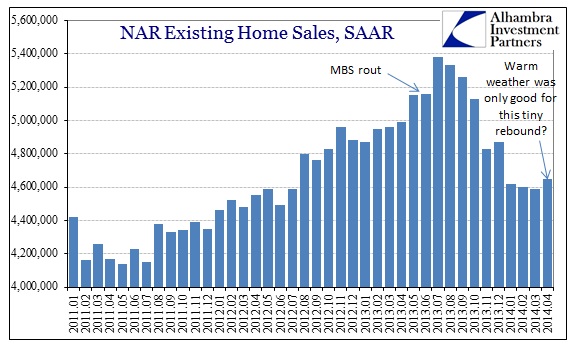

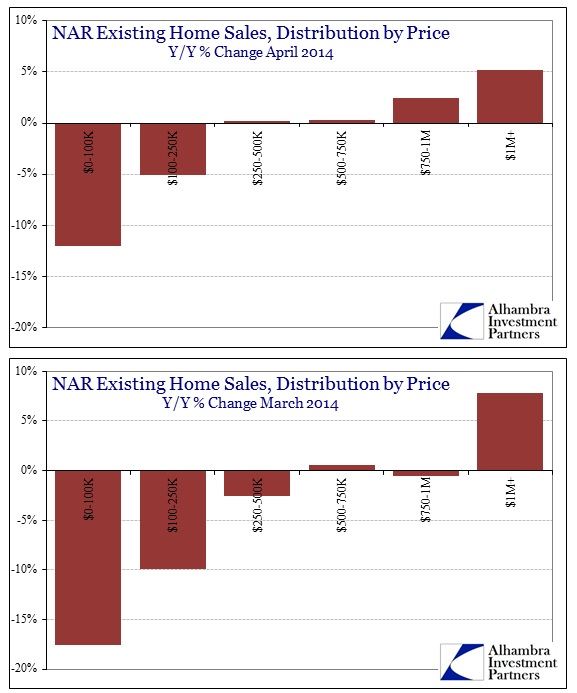

• Total Y/Y Home Sales Down 7%, But Plunged 17% At Bottom

The depressed level of existing home sales throughout 2014 so far continued into April despite all projections of pent up demand after a cold and wintry start. There was some growth in the month-to-month change of the seasonally adjusted figures, but even there the clear problem that has been evident since mortgage finance collapsed starkly remains. [..] Protestations aside, the future of real estate will be decided by these financial factors, including both mortgage finance and household impoverishment.

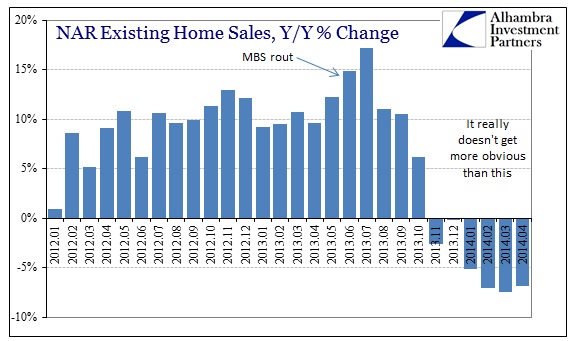

The true pattern really jumps out when viewing these figures Y/Y.

First time home buyers continue to be absent from the housing market. The level of this category of purchasers remains at about only 29% of all sales. That speaks to both affordability (lack of) and household formation. It also shows clearly the shortcomings of the continuous appeal to the insidious wealth effect as it fails to trickle to anyone other than those directly experiencing asset inflation.

The picture that emerges of the new America is starting to get into focus. We can see what goes on, no longer distracted by the media, the markets or the political system. At least, it is there for us to see, and the need to be distracted is gone. Whether we will actually choose the clearer picture over the rosier fuzzy one is another matter altogether. Do we even want to know why American housing and retail are getting so much worse so fast? Why not turn to Jeffrey P. Snider again?

Interest Rate Manipulation Comes Back to Haunt Its Most Ardent Supporters

It is difficult to give too much deference to commentators, particularly economists, that speak to the value of quantitative easing in such bland and generic terms. It almost sounds exceedingly easy, as if the Federal Reserve buys a bunch of mortgage bonds, mortgage rates decline, more people can afford to buy houses and the world is full of sunshine again. It usually doesn’t get more detailed than that, partly because it is now ironclad law that in order to reach a mass market demands such simplicity, but also partly because that is the extent and depth of the profession’s actual knowledge of the inner workings. I hear it all the time when these same persons, who are nearly monolithic in their undying devotion to the sanctity of the FOMC, try to describe something so basic as the “money supply.”

Such a notion in the 21st century is so entirely fungible as to lose all proper and tangible meaning, yet that doesn’t stop a considerable number of respected commentators from removing all real world complexity. For example, Deutsche Bank announced last weekend a new “capital” campaign whereby the bank will raise €8 billion in order to focus more on the high yield and leveraged debt markets in the United States (this is not a joke). Part of the reason is that those debt markets are where all the action is now (thanks to what, exactly?) given that FICC [fixed income, currencies, commodities] trading, boring fixed income and bond trading, is almost completely dead today – the very segment that had sustained the global banking enterprise from the depths of near total despair.

How will Deutsche Bank get its new euro capital from Frankfurt to NYC? It’s all the more amazing since 60 million shares are to be (have been) sold to the investment company of a (the?) Qatari Sheikh. There will be a wonderful trip through derivatives markets and bank balance sheets (no doubt including Deutsche’s London and US subs), requiring the accounting and finance acumen of dozens of systems including risk management. Do we include or exclude the Sheikh’s initial funding toward the US$ money supply?

More interesting is why FICC trading has become so unprofitable. The short answer is the very same people who thought interest rate manipulation was a terrific idea in the first place. But such a generic statement plays right into the very critique I offered at the outset. There is obviously, given this setup, much more “nuance” and “texture” to how policy built up FICC only to tear it apart and set the world of finance into a much more unsettled position. First, you have to realize that the Fed through FRBNY’s Open Market desk doesn’t just buy some mortgage bonds as if they were like US treasuries. QE actually operates deep within the bowels of mortgage bond trading in a place called TBA [to-be-announced, some portion of a pending pool of as-yet unspecified mortgages]. The entire purpose of the TBA market is to provide liquidity to something that is, at its core, completely and totally illiquid. A mortgage loan is about as static as it gets in banking.

The manipulation of interest rates by central banks must at some point backfire. First of all because, as I wrote not long ago, if a market cannot set interest rates, it is by definition dysfunctional, since there’s no way to tell which asset is worth what price. That is of course the reason why the Fed suppresses rates: so highly indebted TBTF corporations can borrow at gutter-scraping rates, and made to look like they’re doing just fine, thank you. But the manipulation also drags down rates that those corporations once used to make money with, so the ‘policy’ is essentially self-defeating from the get-go.

It’s all just a matter of time. And the players in the financial world would like to pride themselves on being able to get the timing right. A tempting self-image for those who make millions a year, and think that means they’re smart. In fact, they’re not, and it all only works as long as the Fed makes up for their losses. Which it will no longer be able to do once upward pressure on interest rates becomes too strong. Or US housing and retail, together good for over 70% of GDP, plunge too much. As they inevitably must, precisely because of the near-freezing-point rates the Fed has set. It’s a closed circuit vicious circle. To put it mildly: we may be close. As for what to expect from the Fed going forward, count on it being found wanting, a lot. And count on the real economy, here’s looking at you, being the real victim, not the broke(n) financial institutions the Fed is tasked with saving. David Stockman:

Financial Storm Chasing With Blinders On: How The Fed Is Driving The Next Bust

The latest iteration of the Fed’s meeting minutes is surreal. Its another economic weather report consisting of trivial, random observations about the quarter just ended that are as superficial as CNBC sound bites. Along with that prattle comes guesses and hopes about the next 30-90 days—including the expectation that the weather will “seasonally normalize” and that auto production schedules, for instance, which were down in March, will stabilize at that level “in the months ahead”. Likewise, after noting that consumption spending moved “roughly sideways” during January and February, it detected that “recent information on factors that influence household spending were positive” – a guess that turned out to be wrong based on data we already know from April retail sales.

The data on new and existing home sales had indicated the continuation of a 5-month trend of sharp drops from prior year, but the minutes could muster only an on-the-one-hand-and-on-the-other-hand whitewash, accented with hopeful indicators on single-family permits and pending home sales. Business investment was treated the same way – that is, it was down in the first quarter but “modest gains” are expected soon based on sentiment surveys. And as you read further the noise just keeps getting more foolish, including the hope that the negative net export performance in Q1 would be off-set by improving global developments. That fond hope included this doozy: “In Japan, industrial production rose robustly, and consumer demand was boosted by anticipation of the April increase in the consumption tax.”

… the monetary politburo does indeed believe that it can steer our $17 trillion economy on a month-to-month basis, and attempts to do so with primitive “in-coming” data from the Washington statistical mills that is so tentative, imputed, guesstimated, seasonally maladjusted and subsequently revised as to be no better than anecdotal sound bites.[..] … its one size fits all control panel includes only interest rate pegging, risk asset propping and periodic open mouth blabbing by Fed heads. But these are no longer efficacious tools for driving the real Main Street economy because to boost the latter above its natural capitalist path of productivity and labor hours based growth requires artificial credit expansion – that is, a persistent leveraging up of balance sheets so that credit bloated spending rises faster than production and income.

I know many, if not most, people see Nicole and I as doomers and pessimists, and if only we did what Shinzo Abe told the Japanese to do: believe in Abenomics, things would be alright, since pessimism is such an corrosive attitude. But if pessimism means refusing to look the other way when confronted by lies, manipulations and tens of trillions in hidden losses, I guess we must accept the label, perhaps even with a shot of pride. Still, of course I realize that as the picture of the new America emerges and it’s not a rosy one, there are always plenty of sources to turn to that will serve a dose of optimism at demand.

The best thing I can do, as always, is to say: look at the data. What do you think you see? I can tell you what I see, and what I’ve been seeing for years, is a load of debt so gigantic that not restructuring it could only have been the worst possible decision, and yet it was made. The fact that this didn’t only happen stateside is no comfort, it just makes things worse: no-one left to unload your debt on. The Fed, the government and the media have ‘shielded’ Americans (and Europeans, and Japanese) from their own reality for many years now, so they wouldn’t notice how private debt was transferred to them. Retail and housing appear to be indicating that is not an effective strategy anymore, people overall are too stretched and stressed financially. What comes next is a scary thing to ponder. But it’ll be a new America, that’s for sure.

• U.S. Retailers Missing Estimates by Most in 13 Years (Bloomberg)

U.S. retailers’ first-quarter earnings are trailing analysts’ estimates by the widest margin in 13 years after bad weather and weak spending by lower-income consumers intensified competition. Chains are missing projections by an average of 3.1%, with 87 retailers, or 70% of those tracked, having reported, researcher Retail Metrics Inc. said in a statement today. That’s the worst performance relative to estimates since the fourth quarter of 2000, when they missed by 3.3%. Over the long term, chains typically beat by 3%, the firm said. Extreme winter weather through February and March forced store closings and stifled sales, Swampscott, Massachusetts-based Retail Metrics said.

Lower- and moderate-income consumers had little discretionary spending power, and chains also faced price competition from e-commerce sites. “The American consumer is not fully back and remains cautious,” Ken Perkins, Retail Metrics’ president, wrote in the report. What’s more, the expectations the chains are missing have been significantly lowered. While analysts now project retailers’ earnings fell an average of 4.1%, back in January they had estimated a 13% gain. Most retail segments are showing profit declines, with department stores, teen-apparel chains and home-furnishing stores faring the worst, Retail Metrics said. About 41% of retailers have missed estimates, while 45% have beat.

• Q1 Retail Profit Outlook Went From +13% to -4% (Actual) In 90 Days (Alhambra)

We keep hearing about pent up demand as if it is a foregone conclusion. For some, particularly orthodox economists, it really is – it has to be. If there is no pent up demand awaiting some ephemeral trigger, then their whole theory of the economy is wrong, from the ground up. The Fed reduced interest rates throughout the economy (though it is far more complicated than that) and thus had to spur a growth impulse. We haven’t seen it yet because of the continual interference of exogeny. Back-to-school sales were “unexpectedly” low, leading to whispers about retailers stuffed with inventory. That was fine, though, because Christmas sales were going to be the first real treat since before the panic. Even though Kmart started advertising its Christmas deals in September, that was dismissed as idiosyncratic. Then it turned out Kmart was actually emblematic and Christmas (for the retail industry) ended up as the worst since 2009.

But that, too, was fine, because holiday hangover would be less significant. So retailer expectations, as with those for overall economic growth, were tremendously optimistic until it snowed in winter. What’s more, the expectations the chains are missing have been significantly lowered. “While analysts now project retailers’ earnings fell an average of 4.1%, back in January they had estimated a 13% gain.” In the space of only three months or so, retailers went from (yet again) expecting fortune and finding instead more “mysterious headwinds.” But this is beyond the usual ridiculous affair, to miss by that much implies something far more serious. To go from +13% to -4% that quickly is an outrage, not just to the economy as it sinks further under the weight of these commandments, but also in those businesses that continue to rely on orthodox forecasts and assumptions.

• Total Y/Y Home Sales Down 7%, But Plunged 17% At Bottom (Alhambra)

The depressed level of existing home sales throughout 2014 so far continued into April despite all projections of pent up demand after a cold and wintry start. There was some growth in the month-to-month change of the seasonally adjusted figures, but even there the clear problem that has been evident since mortgage finance collapsed starkly remains. While it may be encouraging that April was at least better than March, there was also a small rebound in December over November that told us nothing about the future path other than to remind about normal monthly volatility. Protestations aside, the future of real estate will be decided by these financial factors, including both mortgage finance and household impoverishment.

The true pattern really jumps out when viewing these figures Y/Y.

First time home buyers continue to be absent from the housing market. The level of this category of purchasers remains at about only 29% of all sales. That speaks to both affordability (lack of) and household formation. It also shows clearly the shortcomings of the continuous appeal to the insidious wealth effect as it fails to trickle to anyone other than those directly experiencing asset inflation.

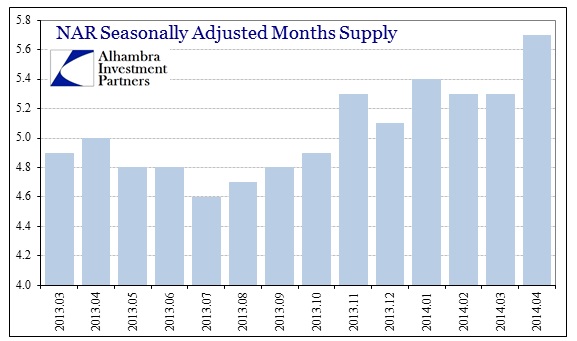

The overall distribution of sales was better across all segments except the highest, but the distribution remains heavily skewed in that direction. With all that in mind, there is a new development that may influence future price gains and overall housing momentum. First, the NAR estimates that the average home price was up only 3.7% in April, down significantly from the 7.1% gain in February. The median price fared somewhat better, as you would expect given the persisting favorability of higher end sales, but the price growth is also clearly decelerating there too.

Median home prices were up only 5.2% in April, down from 8.7% growth in February and a 13% increase in August when this mortgage mess (driven by taper threats) really began to strike. The deceleration in bubble pricing, particularly in the past few months, is somewhat unsurprising as inventory levels have gained dramatically alongside the drop in sales pace. That is a very unwelcome trend. The NAR, in particular, has been trying to sell this housing market on a shortage of homes for sale. That may have been the case when sales growth was at a high point last summer, but it is no longer evident now.

In some important markets, particular those like Phoenix, AZ, inventory levels are through the roof (+49% Y/Y). Combined with construction, the real estate market is once again searching for a bottom. Artificiality giveth; taper taketh. The economic growth offset? Conspicuously absent.

• Interest Rate Manipulation Comes Back to Haunt Its Most Ardent Supporters (RCM)

It is difficult to give too much deference to commentators, particularly economists, that speak to the value of quantitative easing in such bland and generic terms. It almost sounds exceedingly easy, as if the Federal Reserve buys a bunch of mortgage bonds, mortgage rates decline, more people can afford to buy houses and the world is full of sunshine again. It usually doesn’t get more detailed than that, partly because it is now ironclad law that in order to reach a mass market demands such simplicity, but also partly because that is the extent and depth of the profession’s actual knowledge of the inner workings. I hear it all the time when these same persons, who are nearly monolithic in their undying devotion to the sanctity of the FOMC, try to describe something so basic as the “money supply.”

Such a notion in the 21st century is so entirely fungible as to lose all proper and tangible meaning, yet that doesn’t stop a considerable number of respected commentators from removing all real world complexity. For example, Deutsche Bank announced last weekend a new “capital” campaign whereby the bank will raise €8 billion in order to focus more on the high yield and leveraged debt markets in the United States (this is not a joke). Part of the reason is that those debt markets are where all the action is now (thanks to what, exactly?) given that FICC [fixed income, currencies, commodities] trading, boring fixed income and bond trading, is almost completely dead today – the very segment that had sustained the global banking enterprise from the depths of near total despair.

How will Deutsche Bank get its new euro capital from Frankfurt to NYC? It’s all the more amazing since 60 million shares are to be (have been) sold to the investment company of a (the?) Qatari Sheikh. There will be a wonderful trip through derivatives markets and bank balance sheets (no doubt including Deutsche’s London and US subs), requiring the accounting and finance acumen of dozens of systems including risk management. Do we include or exclude the Sheikh’s initial funding toward the US$ money supply?

More interesting is why FICC trading has become so unprofitable. The short answer is the very same people who thought interest rate manipulation was a terrific idea in the first place. But such a generic statement plays right into the very critique I offered at the outset. There is obviously, given this setup, much more “nuance” and “texture” to how policy built up FICC only to tear it apart and set the world of finance into a much more unsettled position. First, you have to realize that the Fed through FRBNY’s Open Market desk doesn’t just buy some mortgage bonds as if they were like US treasuries. QE actually operates deep within the bowels of mortgage bond trading in a place called TBA [to-be-announced, some portion of a pending pool of as-yet unspecified mortgages]. The entire purpose of the TBA market is to provide liquidity to something that is, at its core, completely and totally illiquid. A mortgage loan is about as static as it gets in banking.

What the Fed is buying through the Open Market Desk are largely “production coupons.” The TBA market is a highly standardized operation allowing millions of individual mortgage loans to be packaged into MBS securities in such a fashion that these otherwise immovable loans can be turned to cash in a moment’s notice. But mortgage originators need to “buy” GSE guarantees and factor that cost into the setting of MBS prices (along with a set aside for servicing costs). So whatever the net yield on the mortgage pool, say for argument’s sake it is 5%, the originator will pay 50 bps to the GSE for its guarantee, set aside 25 bps for servicing costs and then subtract its own spread. If that profit spread is 25 bps, the “production coupon” that is left is 4% to the market.

The Open Market Desk’s purchase of production coupons amounts to a retail purchase out of what is really a wholesale product. The generic ideal is that by purchasing more production coupons than might have otherwise been bought it will allow more room for originators to pocket a spread. In other words, if the Fed purchases bump up demand to the point that the “market” is competing for production coupons at 3.75% instead of 4%, the originator can gain some additional bps in profit spread and even pass some of those savings to new mortgage loans in the form of lower interest rates. The increased spread should, theoretically, entice more participation and increase production of mortgage loans to add to the TBA pool (because there is more profit to be had).

That amounts to an artificial subsidy to this type of finance, meaning any increase in activity is done so because of this sponsorship rather than the fundamentals of actual mortgage and real estate conditions. The Fed wants what it wants, including and especially an artificial “pump priming” process that it believes (wrongly, as it is turning out) will restart the housing market. There doesn’t seem anything too evidently amiss by this QE process as I’m sure there is no surprise that the Fed is “greasing the wheels” of finance. But there are costs to such grease, some that are only being discussed now in the deep recesses of global banking.

The danger of Open Market operations to such a scale in the TBA market coincides with its position as a futures/forward operation. The actual purchase of production coupons is not immediate, but upon settlement that may be several months into the future. This framework helps originators because they can “lock in” financial factors without having to take on risk of conditions changing between the filing of a mortgage application and the funding of a mortgage loan. That upside to originators poses a bit of a problem in that the pipeline is susceptible to large swings.

• Target, Staples And The Same Poor Mess (Alhambra)

Now that we have results for both Wal-Mart and Target, the retail, and thus consumer, picture has been largely filled out. Both companies continue to blame other factors (both cold; Target credit card theft) while dancing around with soft presentations of minor allusions to struggling consumers. At what point do “struggling consumers” begin to register as something more than a mysterious headwind? The state of US households is more like a recession than some tangential factor that is just running below expectations. The results speak for themselves – there was an obvious slowdown in 2012 followed by revenue and spending patterns that very much equate to late 2007 and early 2008. In fact, going back to 2012, the similarities are almost exact right up until the collapse after the September 2008 panic.

The ups and downs throughout the chronology of the past seven years sure look like two recession cycles. It really doesn’t get much clearer than this:

You can make the case that the current down cycle is nowhere near as bad as 2008, especially into 2009, but that is an exceedingly low standard. We have been promised repeatedly and assuredly that there would be a recovery, even to the point of having to withstand four separate, immense QE paroxysms. To what gain? To what loss? If it was only Target and the rest of the retail industry was doing fine, then you can dismiss these results (actual dollars spent as they are, in contrast to sentiment surveys) as Target’s individual missteps. But Wal-Mart has shown the same exact pattern, though actually faring far worse in terms of its 2008 comparisons. Wal-Mart and Target are #1 and #3 in terms of size.

That suggests that consumers were downgrading their shopping impulses in 2008 from more expensive outfits to bare bones essentials. In other words, the Great Recession almost benefitted Wal-Mart by shifting the whole retail scale toward “cheap.” Now, in 2013 and 2014, they can’t even get away with that. It’s almost as if the country and economic system have grown far poorer throughout this “recovery.”

And since Staples also reported, I might as well throw them in here too. One more large retailer (this one with a propensity to serve small and medium businesses) showing exactly the same slowdown/pattern since 2012.

• How The Fed Is Driving The Next Bust (David Stockman)

The latest iteration of the Fed’s meeting minutes is surreal. Its another economic weather report consisting of trivial, random observations about the quarter just ended that are as superficial as CNBC sound bites. Along with that prattle comes guesses and hopes about the next 30-90 days—including the expectation that the weather will “seasonally normalize” and that auto production schedules, for instance, which were down in March, will stabilize at that level “in the months ahead”. Likewise, after noting that consumption spending moved “roughly sideways” during January and February, it detected that “recent information on factors that influence household spending were positive”—-a guess that turned out to be wrong based on data we already know from April retail sales.

The data on new and existing home sales had indicated the continuation of a 5-month trend of sharp drops from prior year, but the minutes could muster only an on-the-one-hand-and-on-the-other-hand whitewash, accented with hopeful indicators on single-family permits and pending home sales. Business investment was treated the same way—that is, it was down in the first quarter but “modest gains” are expected soon based on sentiment surveys. And as you read further the noise just keeps getting more foolish, including the hope that the negative net export performance in Q1 would be off-set by improving global developments. That fond hope included this doozy: “In Japan, industrial production rose robustly, and consumer demand was boosted by anticipation of the April increase in the consumption tax.”

That particular phrase actually translates into big speed bumps ahead, but that’s beside the point. What this item and all of the rest of the commentary amounts to is bus driver chatter about road conditions at the moment. Stated differently, the monetary politburo does indeed believe that it can steer our $17 trillion economy on a month-to-month basis, and attempts to do so with primitive “in-coming” data from the Washington statistical mills that is so tentative, imputed, guesstimated, seasonally maladjusted and subsequently revised as to be no better than anecdotal sound bites.

Worse still, it pretends to be executing its monetary central planning model without any of the “gosplan” tools that would really be needed to drive the thousands of variables and millions of actors which comprise an open $17 trillion economy that is deeply intertwined in the trade, capital and financial flows of the world’s $75 trillion GDP. Alas, its one size fits all control panel includes only interest rate pegging, risk asset propping and periodic open mouth blabbing by Fed heads. But these are no longer efficacious tools for driving the real Main Street economy because to boost the latter above its natural capitalist path of productivity and labor hours based growth requires artificial credit expansion—that is, a persistent leveraging up of balance sheets so that credit bloated spending rises faster than production and income.

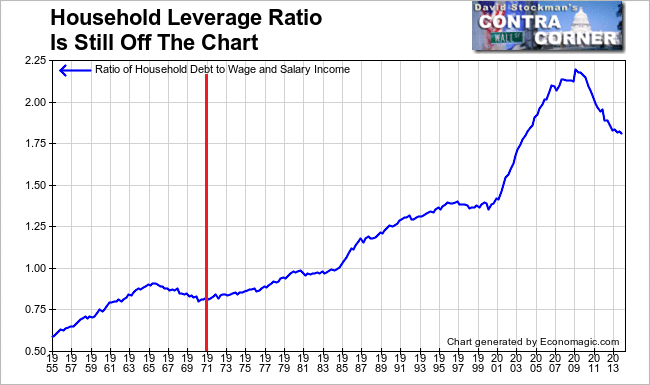

As should be evident after six continuous years of frantic money pumping that old secret sauce doesn’t work any more because the American economy has reached a condition of peak debt. During the Keynesian heyday between 1970 and 2007 the nation’s total leverage ratio—that is, total public and private credit market debt relative to national income—soared right off the historic charts, rising from a 100-year ratio of +/- 150% of national income to a 350% leverage ratio by 2007. Since the financial crisis, the components of national leverage have been shuffled from the household sector to the public sector, but the ratio has remained dead in the water at 3.5X. That means that contrary to all the ballyhoo about deleveraging, it has not happened in the aggregate, but where it has happened at the sector level actually proves that the Fed’s credit transmission channel is over and done.

Total non-financial business debt has risen from $11 trillion to $13.6 trillion since the financial crisis, but virtually all of that gain has gone into shrinkage of business equity capital—that is, LBOs, stock buybacks and cash M&A deals which levitate the price of shares in the secondary market, but do not fund productive assets and the wherewithal of future growth. In fact, as of Q1 business investment in plant and equipment was still nearly $70 billion or 5% below its late 2007 peak. In the case of the household sector, the 40-year sprint into higher and higher leverage ratios has reversed and is now significantly below its peak at 220% of wage and salary income in 2007. At 180% today household leverage is off the mountain top—but it is still far above historically healthy levels, especially for an economy with rapidly aging demographics and soaring ratios of dependency on government benefits that requires tax extraction from debt-burdened households or debt levies on unborn taxpayers.

So the traditional credit expansion channel of Fed policy is busted, but the monetary politburo is like an old dog that is incapable of learning new tricks. It plans to keep money market rates are zero for seven years running through 2015 on the misbegotten notion that it can restart America’s unfortunate 40-year climb into the nosebleed section of the debt stadium. That isn’t happening, of course, but the $3.5 trillion of new liquidity that it has poured through the coffers of the primary bonds dealers since September 2008 has not functioned like the proverbial tree falling in an empty forest. Just the opposite. It has been a roaring siren on Wall Street—guaranteeing free short-term money to fund the carry trades, while providing a transparent “put” under the price of debt and risk assets. In short, it has fueled the Wall Street gambling channel like never before in recorded history.

Do the Fed minutes evince a clue that six years into this frantic money printing cycle that speculation, financial leverage strategies and momentum chasing gamblers are setting up for the next bursting bubble? Well no. Aside from pro forma caveats about possible future financial risks, the minutes claimed that all is well in the casino:

“In their discussion of financial stability, participants generally did not see imbalances that posed significant near-term risks to the financial system or the broader economy….

Perhaps they did not review the two charts that follow. Both are ringing the bell loudly to the effect that we are reaching the same bubble asymptote—or curve that has reached its limit— as was recorded right before the crashes of 2000-2001 and 2007-2008. The margin debt explosion is especially significant because it had reached a higher ratio to GDP (2.73%) than either of the two pervious bubble cycles. Back in the day of William McChesney Martin, the Fed watched margin debt like a hawk because it was comprised of veterans of the 1929 crash. Accordingly, they did not hesitate to take preemptive tightening actions when speculation began to get out of line, such as in the summer of 1958. But this month’s meeting minutes did not even take note of the margin data.

• Fear Strikes Out On Wall Street (Reuters)

Whatever investors are worried about right now, those concerns are not showing up in Wall Street’s fear gauge. That scares some. On the other hand, it more than likely means that stocks will keep taking things slow and steady. The CBOE Volatility Index, or VIX, closed on Friday at 11.36, its lowest level since March 2013. That means investors see less risk ahead, particularly with the S&P 500 ending at a record high again on Friday. With the typically slow summer months just ahead and little on the horizon to shake the market from its current course, investors could be looking at even lower VIX levels, some analysts said. “It’s not that there’s no likelihood of a correction. It’s that people don’t perceive anything to derail the train at this point,” said Andrew Wilkinson, chief market analyst at Interactive Brokers LLC in Greenwich, Connecticut. “So I think people are beginning to wonder: Are we heading back to single-digit volatility?”

The S&P 500’s record high and the drop in the VIX are not the only signs that fear is not a factor on Wall Street. Volume is down as well. S&P 500 E-mini futures volume was below the 1.52 million daily average of the past year on every day this week except Tuesday. The market’s gain has come despite concerns about a slowdown in China and weakness in small-cap names. Typically small-cap stocks lead the market’s advance when the U.S. economy is improving. However, the recent selloff in small-cap stocks, which drove the Russell 2000 index briefly into correction territory last week, seems to have slowed. The Russell gained 2.1% this week, its biggest weekly bounce in more than a month. The index is less than 7% below its record close of 1,208.65 in early March.

At the same time, the Dow Jones Transportation Average hit record territory late Friday, nearly breaking above the 8,000 level. “One of the reasons the VIX is so low, we haven’t really done anything this year. We haven’t moved an awful lot,” said J.J. Kinahan, chief derivatives officer of TD Ameritrade in Chicago. For the year, the S&P 500 has gained just 2.8%. To be sure, some analysts say the lack of volatility suggests a complacency that could encourage excessive risk-taking. New York Federal Reserve Bank President William Dudley and Dallas Fed President Richard Fisher have both expressed such concerns in recent days. “The lower the VIX, the more overbought the market gets, leaving it vulnerable to some kind of setback,” said Donald Selkin, chief market strategist at National Securities in New York.

The most quoted Newsweek story ever ……

• 40-Year-Old “Cooling World” Story Still Haunts Climate Science (P. Gwynne)

“The central fact is that, after three quarters of a century of extraordinarily mild conditions, the Earth seems to be cooling down. Meteorologists disagree about the cause and extent of the cooling trend, as well as over its specific impact on local weather conditions. But they are almost unanimous in the view that the trend will reduce agricultural productivity for the rest of the century.” – Newsweek: April 28, 1975

That’s an excerpt from a story I wrote about climate science that appeared almost 40 years ago. Titled “The Cooling World,” it was remarkably popular; in fact it might be the only decades-old magazine story about science ever carried onto the set of a late-night TV talk show. Now, as the author of that story, after decades of scientific advances, let me say this: while the hypotheses described in that original story seemed right at the time, climate scientists now know that they were seriously incomplete. Our climate is warming — not cooling, as the original story suggested. Nevertheless, certain websites and individuals that dispute, disparage and deny the science that shows that humans are causing the Earth to warm continue to quote my article. Their message: how can we believe climatologists who tell us that the Earth’s atmosphere is warming when their colleagues asserted that it’s actually cooling?

Well, yes, we should trust them, despite the views of detractors such as comedian Dennis Miller, who brought my story to The Tonight Show in 2006. Several atmospheric scientists did indeed believe in global cooling, as I reported in the April 28, 1975 issue of Newsweek. But that was then. In the 39 years since, biotechnology has flowered from a promising academic topic to a major global industry, the first test-tube baby has been born and become a mother herself, cosmologists have learned that the universe is expanding at an accelerating rate rather than slowing down, and particle physicists have detected the Higgs boson, an entity once regarded as only a theoretical concept. Seven presidents have served most of 11 terms. And Newsweek has become a shadow of its former self. And on the climate front? The vast majority of climatologists now assure us that Earth’s atmosphere is not cooling. Rather it’s warming up. And the main responsibility for the phenomenon lies with human activity.

• May 24: Global March Against Monsanto Day (RT)

Over 400 cities worldwide will see millions marching against the US chemical and agricultural company Monsanto in an effort to boycott the use of Genetically Modified Organizms in food production. Marches are planned in 52 countries in addition to some 47 US states that are jointing in the protest. “MAM supports a sustainable food production system. We must act now to stop GMOs and harmful pesticides,” said Tami Monroe Canal, founder of March Against Monsanto (MAM) in a press release ahead of the global event. The movement was formed after the 2012 California Proposition 37 on mandatory labeling of genetically engineered food initiative failed, prompting activists to demand a boycott of the GMO in food production. “Monsanto’s predatory business and corporate agriculture practices threatens their generation’s health, fertility and longevity,” Canal said.

The main aim of the activism is to organize global awareness for the need to protect food supply, local farms and environment. It seeks to promote organic solutions, while “exposing cronyism between big business and the government.” Activists claim that Monsanto spent hundreds of millions of dollars to “obstruct all labeling attempts” while suppressing all “research containing results not in their favor.” Birth defects, organ damage, infant mortality, sterility and increased cancer risks are just some of the side-effects GMO is believed to cause. “That is what the scientists have learned about, that the genetically modified foods will increase allergies that they are going to be less nutritious and that they can possibly or very contain toxins that can make us ill,” Organic Consumers Association’s political director Alexis Baden-Mayer told RT.

GMOs have been partially banned in a number of countries, including Germany, Japan, and Russia but yet in most countries across the globe still feed GMOs to their animals. Citing the US example, Baden-Mayer told RT that “it is hard to distinguish the company Monsanto from the players in the US government.” “Most of the genetically modified crops grown in the US, almost all of them end up in factory farms, concentrated in animal feeding operations,” stating that US has enough grassland to pasture and raise “100 percent grass-fed beef” and produce even more grass fed beef than is raised on “modified corn and soy.”

Oh, sweet Jesus ….

• Fukushima Daiichi Begins Pumping Groundwater Into Pacific (Guardian)

The operator of the wrecked Fukushima Daiichi nuclear power plant has started pumping groundwater into the Pacific ocean in an attempt to manage the large volume of contaminated water at the site. Tokyo Electric Power (Tepco) said it had released 560 tonnes of groundwater pumped from 12 wells located upstream from the damaged reactors. The water had been temporarily stored in a tank so it could undergo safety checks before being released, the firm added. The buildup of toxic water is the most urgent problem facing workers at the plant, almost two years after the environment ministry said 300 tonnes of contaminated groundwater from Fukushima Daiichi was seeping into the ocean every day. The groundwater, which flows in from hills behind the plant, mixes with contaminated water used to cool melted fuel before ending up in the sea.

Officials concede that decommissioning the reactors will be impossible until the water issue has been resolved. The bypass system intercepts clean groundwater as it flows downhill toward the sea and reroutes it around the plant. It is expected to reduce the amount of water flowing into the reactor basements by up to 100 tonnes a day – a quarter – and relieve pressure on the storage tanks, which will soon reach their capacity. But the system does not include the coolant water that becomes dangerously contaminated after it is pumped into the basements of three reactors that suffered meltdown after the plant was struck by an earthquake and tsunami in March 2011.

That water will continue to be stored in more than 1,000 tanks at the site, while officials debate how to safely dispose of it. The problem has been compounded by frequent technical glitches afflicting the plant’s water purification system. Tepco and the government are also preparing to build an underground frozen wall around four reactors to block groundwater, although some experts doubt the technology will work on such a large scale. The utility is also building more tanks to increase storage capacity. Dale Klein, a senior adviser to Tepco, recently warned the firm that it may have no choice but to eventually dump contaminated water into the Pacific.

Home › Forums › A Picture of the New America