Marjory Collins Sunday picnic in Rock Creek Park, Washington DC July 1942

James Gorman, CEO – and anagram – of Morgan Stanley, has an article in the Wall Street Journal on the future of finance. After reading it, I have the distinct impression – suspicion – that Mr. Gorman owes his job to his lack of contact with reality, that anyone less prone to delusions would not be able to do the job he does the way he does it. Of course there’s the option he’s faking the entire article – and his “vision”, but something tells me that’s not the case. He leaves me with the idea he means it. And that is troubling. There is no, or hardly any, serious financial crisis in his view, let alone any other crises.

His global vision of banking depends on goods continuing, even increasingly, to be transported around the globe, and on the world’s largest banks financing all that increasing activity. It essentially depends on everything becoming bigger, except for retail banking’s customer service. Let’s have a look:

The Future of Finance: Big Banks Will Get Bigger

Will banks continue to exist? The answer is yes, because society will still need the two essential functions they provide: mobilization of capital from providers to users, and facilitation of payments for goods and services. But technology, globalization and demographics will change the shape of banking as dramatically in the next 100 years as they have in the last. [..] technology will continue to breed competition and disintermediation. Traditional consumer banking will come under extreme pressure as its central deposit-taking and lending functions are challenged by online savings vehicles, crowdfunding and loan syndicating by such nontraditional competitors as insurance companies, pension and hedge funds.

Universal adoption of mobile devices puts a bank branch in everyone’s pocket and renders bricks and mortar obsolete. Of the 97,000 bank branches that exist across the U.S. today, all but about 10,000 will disappear. Those remaining will become social gathering places where people go to be educated about finance, engage in discussion groups about savings and investment and, at the high end, get exclusive exposure to luxury goods and services.

I understand some of what he’s saying here, we all do, but other things I don’t get at all. Banks become AA-like social gatherings?! Why not throw in a church while you’re at it? People in the future will go to banks to engage in discussion groups about savings and investment? Really? Raise your hands if you’re planning to go. As far as banks becoming purveyors of cologne, watches and Ferrari’s is concerned, I’ll gladly leave that to your imagination.

At the same time, ample opportunities will continue to exist for big global banks in providing large-scale finance for corporations, institutions and governments. Inexorable consolidation will make the big banks even bigger. Economies of scale and the boundary-less nature of electronic technology will doom most small institutions [..]

Regulation will become ever more globally harmonized. A century ago, the Federal Reserve had just been created, and U.S. banking regulation was largely state-level. Increases in global trade flows have fueled a harmonization process that began in 1944 at Bretton Woods and continued through the Basel Accords of today. Nationalism in financial regulation will not go away entirely, but the reality of economic interconnectedness will tip the scales in favor of a global regulatory architecture.

In the capital markets, state ownership will decrease as developing nations become developed and privatize productive enterprises, and as industrial sectors continue their cycles of creative destruction. This bodes well for continuing vital, if volatile, global equity markets.

Mark the choice of words: “harmonization process” sounds might positive, in the same way that “healthy growth” does. But not all growth is healthy, and neither is all “harmonization” of global banking rules. Not if it leads to even more concentration of financial and political power into the hands of ever fewer players. As far as a line like “state ownership will decrease as developing nations become developed and privatize productive enterprises” is concerned, there is precious little proof that privatizing enterprises works well across the spectrum.

It’s purely finance-religious wishful thinking that can be expected from someone like Gorman who wants more power and more money every single day, but that doesn’t mean it’s good for the rest of us; quite the contrary. As for state ownership of essential services like water, heat, power systems, healthcare etc., no country should ever leave those in the hands of private interests, simply because they’re too important to always and ever be decided on profit principles.

Asset management will become the single-largest segment of financial services, as users of capital become providers of capital in newly developed economies and an aging global demographic creates an inevitable shift from consumers to savers. A burgeoning global middle class will create an enormous pool of savings in search of investment, for which they will seek professional advice and execution. While this new investor class will expect adequate financial returns, they increasingly will demand, too, that their capital generates a positive social return.

Many also will value human relationships with financial advisers, even if they conduct their meetings across continents or oceans via digital video-conferencing. Underfunded defined-benefit and government pension plans will finally have to be dealt with, and reforms will push more people into private investment programs, further propelling asset management. Too much money chases too few returns, potentially setting the stage for the next “100-year” global financial crisis.

“Digital” human relationships, did you catch that? What a curious phrase. Of course, Gorman isn’t talking about talking to you, but about the people who decide what your pensions and investments will be moved into. And he – or his bank – has the answers to prevent a next financial crisis, even if they’re the very parties who caused the present one.

And when Gorman mentions “a positive social return” being demanded by a “new investor class”, i.e. a “burgeoning global middle class [that] will create an enormous pool of savings”, how can anyone take that serious? Has he been asleep for the past 10 years? We all know he’s been bailed out with our money, but that doesn’t allow him the privilege of wearing blinders to work, does it?

When he says that “an aging global demographic creates an inevitable shift from consumers to savers”, does he think at all about the millions of Americans who can no longer afford to retire, who must keep working, often as WalMart greeters or equally demeaning jobs, or about the millions of people in Greece, Italy, Spain, France, who don’t have neither the funds nor the income to either consume or save? Asset management is an empty term for those who have no assets to be managed, and their numbers increase very rapidly. Not least of all because even their potential future earnings have already been used to prop up bankrupt institutions like the one Gorman heads.

Technology, of course, holds both promise and threats. Big-data applications dramatically enhance institutions’ ability to reduce loan losses and identify financial fraud through margin calls and detection of suspicious fund flows in real time. As powerful as these tools are, determined cybercriminals will find ways to steal so much they will force nations to establish deposit-insurance-like entities extending beyond traditional banks to cover theft.

“Determined cybercriminals”? They are the main threat? Not the established financial behemoths? As far as I can see, Mr. Gorman’s Morgan Stanley, and all of its ilk, will take every single penny they can from pensions funds and other institutions that manage the man in the street’s money, as they’ve done through history. To try and present Wall Street banks as friends of the people is quite a ways off the scale. But it’s still all he’s got.

And that makes me think of pitchforks. But they’ll likely be a while yet. Wolf Richter provides a good example of the reason why:

No Politician Is Allowed to Oppose Banks For Long, Not Even the French President

On January 22, 2012 [French President François Hollande], in a speech in Bourget that instantly went viral on a global scale, he’d pointed out, had dared to point out, the true nature of finance, not of the bank branch down the street, but that part of finance that had brought down the financial system and had triggered the great recession, a part of finance that is aided and abetted by central banks to this day: “I’ll tell you who my opponent is, my true opponent,” he said at the time. “He has no name, no face, no party. He will never run for office. He will not be elected. And yet he governs. My opponent is the world of finance.”

He promised he’d rein in that world. He’d impose a tax on all its financial transactions, “a real tax,” and he’d eliminate stock options, and he’d curtail bonuses, and he’d do a million other things. And the huddled masses began to dream. But soon after he was anointed President of France, nuances began to appear. In September 2013, his Industrial Renewal Minister, now re-baptized Economy Minister, Arnaud Montebourg explained it this way: “Finance is like cholesterol, there is the good and the bad.”

Morgan Stanley’s James Gorman can write things like his Wall Street Journal op-ed piece because he knows he and his brethern have the political power to do what they want. That power will be hard to beat, because they’ve bought everything and everyone they want and need to perpetuate it. Every president, every congressman, every central banker.

But maybe his last paragraph – written in the jest of the ruler – hints at a way that you and I and everyone else can use to slow them down (we can – may should – try)

Cash as a physical entity will virtually cease to exist, with coins and checkbooks consigned to museums. As people conduct their financial transactions on hand-held devices made secure by advanced biometrics, even tipping will be done electronically. Paper currency does not disappear entirely, however. You’ll still need it to buy a beer at a certain dusty bar in the Australian outback, where the proprietor sticks stubbornly to a cash-only policy, “because you never know, mate!”

If and or when all our financial transactions are electronic – excuse me, digital -, they’re all traceable too. Is that what we want? For many of us, I’m sure, it’s not. Which means that at some point someone will be smart and driven enough to start a “campaign” calling upon people everywhere to pay cash as much as they can. Most stores still accept cash, though perhaps not in all aisles. Dollars and euros and zloty’s and what not are still legal tender. There are plenty businesses, second hand cars etc., that accept only cash.

We find it comfy and easy to pay with plastic. But the more we do that, the more the power and wealth of the Mr. Gorman’s of this world increases. Literally at our cost, don’t forget that. And the power of the NSA and related global “services” increases at the same time, they can trace our whereabouts and purchases.

So why not take everything you need for your groceries and other shopping out of an ATM first, and only then complete your purchase? Just to slow down Mr. Gorman’s takeover of your lives? A subtle act of disobedience. If that’s too much to ask of you, isn’t it perhaps simply true that you get what you deserve?

Ain’t that the truth ….

• Central Banks Are Borrowing Returns From The Future (FuW)

Felix, a bit more than a year ago, the mere announcement of tapering by the US Federal Reserve triggered a shock wave through financial markets. You called this the butterfly effect which might feed into a worldwide correction. Now we have had tapering since the beginning of the year, and all major asset classes are gently moving up on very low volatility. Is tapering really a problem?

Felix Zulauf: It was a butterfly effect for the moment because the world feared a liquidity tightening which immediately sent emerging market interest rates higher and their currencies lower while the dollar firmed as capital flowed back to the US. The Fed will be done tapering by September or October, but other central banks will take over. We have seen for many months now that the Chinese are printing more money than the US. On average, they have created Renminbi for the countervalue of $50 billion per month over the last six months. This is an enormous amount. Then the European Central Bank is willing to add €1100 billion over the next two years which equals an expansion of 50% of its balance sheet. So we will continue to swim in a sea of liquidity. The question is whether there might be other events and developments that may not be camouflaged by liquidity which could cause a change of investor expectations. Liquidity is one thing, but there are fundamentals also.

What fundamental development could that be?

Zulauf: We think it could be China. In every cycle you have a dominating excess which reinforces the cycle on the upside, but when it turns, it reinforces it on the downside. Last time, it was US and parts of European housing and in the previous cycle technology investments that created excesses and overcapacity. In the current cycle it is emerging markets, and the big gorilla is China.Can’t Beijing control that?

Zulauf: The dimension of the Chinese cycle was enormous. In 2011 and 2012 alone, China has consumed as much cement as the US had in all of the 20th century. The credit creation in the last five or six years is mounting to the total loan outstanding by the US banking system. The excesses are mind boggling. Now anecdotal evidence tells us that the Chinese investment and construction boom has not broken yet, but it has cooled. But when it cools after a boom like we had, it’s probably the end of the cycle. However, investors still believe that the Chinese authorities can manage it because it is an autocracy. Once this assumption changes, it will have a negative effect on markets, but we do not know when exactly that will be.

The only boom there is is a bubble.

• Welcome To The Everything Boom, Or Maybe The Everything Bubble (NY Times)

In Spain, where there was a debt crisis just two years ago, investors are so eager to buy the government’s bonds that they recently accepted the lowest interest rates since 1789. In New York, the Art Deco office tower at One Wall Street sold in May for $585 million, only three months after the going wisdom in the real estate industry was that it would sell for more like $466 million, the estimate in one industry tip sheet. In France, a cable-television company called Numericable was recently able to borrow $11 billion, the largest junk bond deal on record — and despite the risk usually associated with junk bonds, the interest rate was a low 4.875%.

Welcome to the Everything Boom — and, quite possibly, the Everything Bubble. Around the world, nearly every asset class is expensive by historical standards. Stocks and bonds; emerging markets and advanced economies; urban office towers and Iowa farmland; you name it, and it is trading at prices that are high by historical standards relative to fundamentals. The inverse of that is relatively low returns for investors. The phenomenon is rooted in two interrelated forces. Worldwide, more money is piling into savings than businesses believe they can use to make productive investments. At the same time, the world’s major central banks have been on a six-year campaign of holding down interest rates and creating more money from thin air to try to stimulate stronger growth in the wake of the financial crisis.

“We’re in a world where there are very few unambiguously cheap assets,” said Russ Koesterich, chief investment strategist at BlackRock, one of the world’s biggest asset managers, who spends his days scouring the earth for potential opportunities for investors to get a better return relative to the risks they are taking on. “If you ask me to give you the one big bargain out there, I’m not sure there is one.” But frustrating as the situation can be for investors hoping for better returns, the bigger question for the global economy is what happens next. How long will this low-return environment last? And what risks are being created that might be realized only if and when the Everything Boom ends?

• The Future of Finance: Big Banks Will Get Bigger (Morgan Stanley CEO)

The threshold question: Will banks continue to exist? The answer is yes, because society will still need the two essential functions they provide: mobilization of capital from providers to users, and facilitation of payments for goods and services. But technology, globalization and demographics will change the shape of banking as dramatically in the next 100 years as they have in the last. In particular, technology will continue to breed competition and disintermediation. Traditional consumer banking will come under extreme pressure as its central deposit-taking and lending functions are challenged by online savings vehicles, crowdfunding and loan syndicating by such nontraditional competitors as insurance companies, pension and hedge funds. Universal adoption of mobile devices puts a bank branch in everyone’s pocket and renders bricks and mortar obsolete.

Of the 97,000 bank branches that exist across the U.S. today, all but about 10,000 will disappear. Those remaining will become social gathering places where people go to be educated about finance, engage in discussion groups about savings and investment and, at the high end, get exclusive exposure to luxury goods and services. At the same time, ample opportunities will continue to exist for big global banks in providing large-scale finance for corporations, institutions and governments. Inexorable consolidation will make the big banks even bigger. Economies of scale and the boundary-less nature of electronic technology will doom most small institutions, though some may survive under protectionist regulation or niche strategies. Regulation will become ever more globally harmonized. A century ago, the Federal Reserve had just been created, and U.S. banking regulation was largely state-level.

Increases in global trade flows have fueled a harmonization process that began in 1944 at Bretton Woods and continued through the Basel Accords of today. Nationalism in financial regulation will not go away entirely, but the reality of economic interconnectedness will tip the scales in favor of a global regulatory architecture. In the capital markets, state ownership will decrease as developing nations become developed and privatize productive enterprises, and as industrial sectors continue their cycles of creative destruction. This bodes well for continuing vital, if volatile, global equity markets. Asset management will become the single-largest segment of financial services, as users of capital become providers of capital in newly developed economies and an aging global demographic creates an inevitable shift from consumers to savers. A burgeoning global middle class will create an enormous pool of savings in search of investment, for which they will seek professional advice and execution.

• No Elected Politician Is Allowed to Oppose Banks For Long (WolfStreet)

French President François Hollande should have been ecstatic when US Federal and New York State authorities slammed French megabank BNP Paribas with a slew of charges related to the bank’s dealings with Iran in violation of US sanctions. Under intense pressure, BNP agreed to pay a $8.9 billion penalty and plead guilty. It was the largest penalty for a European bank ever. Some heads rolled at the bank. But Hollande was not amused. Yet it should have been the sweetest moment of his dreary Presidency. He should have relished that attack on the French monster bank, and he should have turned motorcade victory laps around rush-hour Paris.

Because on January 22, 2012, as Socialist presidential candidate, in a speech in Bourget that instantly went viral on a global scale, he’d pointed out, had dared to point out, the true nature of finance, not of the bank branch down the street, but that part of finance that brought down the financial system and triggered the great recession, and that is aided and abetted by central banks to this day:

“I’ll tell you who my opponent is, my true opponent,” he said. “He has no name, no face, no party. He will never run for office. He will not be elected. And yet he governs. My opponent is the world of finance.” He promised he’d rein in that world. He’d impose a tax on all its financial transactions, “a real tax,” and he’d eliminate stock options and he’d curtail bonuses, and he’d do a million other things. And the huddled masses began to dream. But soon after he was anointed President of France, nuances began to appear. In September 2013, his Industrial Renewal Minister, now re-baptized Economy Minister, Arnaud Montebourg explained it this way: “Finance is like cholesterol, there is the good and the bad.”

[..] The French government’s deal with megabanks has come full circle, from being a sacred relationship under President Nicholas Sarkozy to enmity during Hollande’s campaign and now back to sacred relationship. No democratically elected government in a major country – not in France, not in Germany, least of all in the US – is allowed to oppose the banks and the central banks that stand behind them, though extracting penalties to the tune of a few quarters worth of earnings – extracting them from stockholders – is now considered an easy price to pay, and part of the costs of doing business, to buy some protection from the restless populists.

No, it already has.

• Is Shadow Banking Set To Take Off Globally? (CNBC)

Shadow banking may get tagged as a big risk in China, but it’s actually on the rise globally as low interest rates spur yield chasing and tougher regulations constrain lending by traditional banks. “Banks have had to pull back from a lot of traditional areas they’ve been active in,” such as corporate lending, said Jonathan Liang, senior portfolio manager for fixed income at AllianceBernstein, which has around $466 billion under management. “As banks withdraw, these companies are still going to need financing and that is giving us as an investor, an opportunity to step in.” AllianceBernstein is currently expanding its team, aiming to target middle-market lending as well as infrastructure and real-estate financing, he said. The liquidity premium, or extra yield, for extending loans that are less liquid than bonds is around 150-200 basis points over bond yields, he said. Compared with the 10-year U.S. Treasury yielding around 2.65%, it gooses returns nicely.

Within hedge funds, it’s usually done in credit multi-strategy funds, rather than a “stand-alone” strategy, Hedge Fund Research said, but it noted those funds are up over 7% so far this year and their assets have grown to more than $425 billion. The segment saw around $9.7 billion in net fresh inflows in the first quarter, compared with $14.8 billion in inflows for all of 2013, HFR said. Investors are calling it “credit disintermediation,” but it’s broadly similar to the high-yield lending that takes place off banks’ balance sheets in China. Widely publicized defaults of some of China’s trusts and wealth management products, which made loans to risky borrowers and promised investors returns higher than the around 3% bank deposit rate, have spurred fears of a credit crisis.

• Nobody Would Design The Market We Have Now (MarketWatch)

U.S. markets will be back in the congressional spotlight Tuesday with a Senate Banking Committee hearing on regulation and electronic trading. Some big names are testifying at the hearing, including Intercontinental Exchange CEO Jeffrey Sprecher, and Joe Ratterman, CEO of BATS Global Markets. Here’s the purpose of the hearing, according to Kate Cichy, a spokeswoman for Senate Banking Committee Chairman Tim Johnson: “Chairman Johnson is holding this hearing to examine how regulation has influenced equity market structure and to consider whether regulation has kept up with developments in trading technology and is sufficient to maintain market stability.”

In his prepared testimony, Ratterman says he agrees with Securities and Exchange Commission Chairwoman Mary Jo White that markets are not rigged. But he says markets aren’t perfect and that he supports reviewing SEC rules designed to provide transparency into broker-order routing practices and execution quality. Sprecher will tell senators that competition for orders should be enhanced by giving deference to regulated trading centers, and so-called “maker-taker” pricing schemes should be eliminated. Another witness, meanwhile, will say rules on markets haven’t kept pace.

“Our rules are antiquated, the product of a time when electricity had reached just 70% of households, not an era in which a gigabyte of data can be transmitted around the world in seconds,” David Lauer, president and managing partner of KOR Group, says. Lauer told MarketWatch in an email he will continue to push the Securities and Exchange Commission to enhance its data analysis capabilities and to open up access to the data to academics studying market structure. Read Lauer’s prepared testimony. Georgetown University finance professor James Angel bluntly says the U.S.’s national regulatory structure needs to be massively overhauled and there is a risk of another 2008-style meltdown from not acting. “Nobody with a clean sheet of paper would design what we have now,” Angel told MarketWatch in a phone interview.

Yawn.

• Banks Face Added Capital Requirements (WSJ)

Global banking regulators are considering new measures that would make it harder for banks to understate the riskiness of their assets, including potentially ending the long-standing treatment of all government bonds as automatically risk-free, according to people familiar with the discussions. The changes under consideration by the Basel Committee on Banking Supervision, the Switzerland-based group that sets global banking rules, could force banks to raise billions of dollars in extra capital. The Basel Committee is considering new regulations that would reduce banks’ latitude to measure the riskiness of their own assets, a key determinant of how much capital they need to hold, these people said. The panel is looking at barring banks from assigning very low risk levels to certain types of assets, a tactic some lenders have used to reduce their capital requirements, these people said.

The potential changes would address two of the most controversial elements of bank accounting. Banks’ treatment of government bonds as without risks became a punch line during Europe’s financial crisis when Greece defaulted on its widely held debts; investors continue to treat some European government bonds as far from risk-free. Meanwhile, banks’ discretion to estimate the riskiness of their own assets has contributed to the perception among many investors that banks’ capital ratios aren’t reliable indicators of their financial health. The question of how banks assess their assets’ risks is pivotal because of how regulators and investors measure lenders’ ability to absorb future losses. A key gauge is the ratio of a bank’s equity to its “risk-weighted” assets. As a bank’s risk-weighted assets decline, its capital ratios rise. Thus, banks have an incentive to play down the riskiness of the loans and securities they hold.

Junk is junk like shit is shit.

• Complacency Breeds $2 Trillion of Junk Debt as Sewage Funded (Bloomberg)

The value of bonds in the Bank of America Merrill Lynch Global High Yield Index has soared to more than $2 trillion. It took 12 years for the gauge, started at the end of 1997, to get to $1 trillion, and only four years to add another $1 trillion. More than $338 billion of the debt has been sold this year, putting 2014 on track to top last year’s record $477 billion. Investors who say they have no choice but to seek ever-riskier securities to generate any type of return are buying junk bonds and loans at a pace suggesting low default rates have blinded them to the potential minefields ahead. Even Japan’s risk-averse $1.25 trillion Government Pension Investment Fund said it’s considering loosening its practice of only buying investment-grade debt and venturing into junk bonds. So eager are investors for the debt that borrowers increasingly are dictating their own terms.

A measure of the strength of junk-bond covenants that are written into offering terms to protect buyers is about the weakest since Moody’s Investors Service started tracking the data in 2011. After pumping trillions of dollars into the global economy to end the financial crisis, central bankers say they’re worried that investors are too complacent, increasing chances for future market instability. A measure of risk that uses options to forecast volatility in equities, currencies, commodities and bonds has fallen to its lowest level on record. “The market has been picked over” and to get more yield money managers may need to “add more risk or seek opportunities that may be less liquid,” said Jason Rosiak, the head of portfolio management at Newport Beach, California-based Pacific Asset Management, which oversees about $4.4 billion. “The portfolio manager needs to decide what is worth the price of admission.”

The warnings are growing louder and more numerous. Fed Chair Janet Yellen told reporters last month she was concerned about “reach-for-yield behavior.” Bank of England Deputy Governor Charlie Bean said conditions were “eerily reminiscent” of the pre-crisis era. Bundesbank board member Andreas Dombret said last month that “we do see risks, despite the fact that the markets are calm.” The Bank for International Settlements in Basel, Switzerland, said in its June 29 annual report that central bankers shouldn’t moan too loudly about complacency because they’re responsible. Record-low rates and unconventional monetary easing by the Fed, European Central Bank and the Bank of Japan reduced price swings across markets, the BIS wrote in the report.

• Krugman’s Bathtub Economics (David Stockman)

It is fortunate that Paul Krugman writes a column for New York Times readers who want the party line sans all the economist jargon and regression equations. So here is the plain English gospel straight from the Keynesian oracle: The US economy is actually a giant bathtub which is constantly springing leaks. Accordingly, the route to prosperity everywhere and always is for agencies of the state—especially its central banking branch—to pump “demand” back into the bathtub until its full to the brim. Simple.

You often find people talking about our economic difficulties as if they were complicated and mysterious, with no obvious solution. As the economist Dean Baker recently pointed out, nothing could be further from the truth. The basic story of what went wrong is, in fact, almost absurdly simple: We had an immense housing bubble, and, when the bubble burst, it left a huge hole in spending. Everything else is footnotes. [..] And the appropriate policy response was simple, too: Fill that hole in demand.

True enough, the housing and credit bubbles did burst. But that’s exactly where the rubber meets the road in the debate between Keynesians and Austrians. The latter see bubbles as an artificial expansion of economic activity owing to cheap credit and the malinvestments which flow from it. When bubbles inevitably burst, therefore, the artificial bloat in investment, output, jobs and incomes is eliminated—or in the old fashioned phrase, liquidated. Moreover, liquidation is the equivalent of purging a cancer; it removes a malignant growth, but does not reduce the true wealth of society or the sustainable living standard of the people.

The reason for this proposition is Say’s Law. That is, sustainable demand must originate in production; valid “spending” must be derived from the income earned in the process of supplying real goods and services. That includes spending that is financed by savers out of their own current incomes, and spending by transfer payment recipients that is financed by taxes on producers. In that context, “money” is just an intermediary: it facilitates efficient exchanges between producers, but does not give rise to incremental “demand” that is independent of goods and services already delivered. Accordingly, when a credit bubble bursts there is no loss of honest, production-based aggregate demand. What disappears is artificial monetary demand that was originally enabled by the central bank and the financial system, not the productive main street economy.

[..] The unsustainability of nominal GDP growth financed by an ever increasing ratchet of the leverage ratio is evident from simple arithmetic. Just assume that the massive credit expansion of 2001-2008 was a good thing and that the trend needed to be preserved another 7-years, according to the Keynesian injunction on the conservation of demand. Moreover, even though credit expansion was rapidly loosing its efficacy during the last bubble as more debt bought less new GDP each year, assume that nominal GDP also managed to grow at 4.8% a year— compared to the actual rate of only 2.4% annually that has been recorded since 2008. Under those assumptions, a “cut and paste” of the 2001-2008 trend would result by 2015 in $100 trillion of credit market debt on $20.6 trillion of GDP. The national leverage ratio would then also ratchet to a mind-numbing 4.8X GDP.

• US Scrutiny For Banks Shifts To Commerzbank And Germany (NY Times)

A trail of illicit money led the American government on a hunt through the European financial system, generating criminal cases against banks in Britain, Switzerland and most recently, France. Now the crackdown is bound for another European financial center: Germany. State and federal authorities have begun settlement talks with Commerzbank, Germany’s second-largest lender, over the bank’s dealings with Iran and other countries blacklisted by the United States, according to people briefed on the matter. The bank, which is suspected of transferring money through its American operations on behalf of companies in Iran and Sudan, could strike a settlement deal with the state and federal authorities as soon as this summer, said the people briefed on the matter, who were not authorized to speak publicly.

The contours of a settlement, which the authorities have only begun to sketch out, are expected to include at least $500 million in penalties for Commerzbank, the people added. Although prosecutors were still weighing punishments, the people briefed on the matter said that the bank would most likely face a so-called deferred prosecution agreement, which would suspend criminal charges in exchange for the financial penalty and other concessions. A potential deal with Commerzbank — which is expected to pave the way for a separate settlement with Deutsche Bank, Germany’s largest bank – would pale in comparison to the case announced last week against France’s biggest bank, BNP Paribas. The French bank agreed to pay a record $8.9 billion penalty and plead guilty to criminal charges for processing transactions on behalf of Sudan and other countries that America has hit with sanctions, a rare criminal action against a financial giant.

UK needs to leave, ASAP, since they will anyway.

• UK To Fight For City Of London In Court Clash With ECB (Bloomberg)

Bruised by David Cameron’s defeat over the leadership of the European Union’s executive arm, the U.K. faces its next clash with the EU tomorrow. It touches a sensitive point — the City of London. Britain’s lawyers will take on the European Central Bank in a hearing at the bloc’s top court — fighting policies they argue would punish the nation’s financial hub because the U.K. has kept the pound sterling. Cameron’s government is attacking ECB policy documents stating that clearinghouses handling trades in euros should be based in the single currency area. Britain says that amounts to an ultimatum that London-based clearers must relocate to the euro area or “be precluded from access to the financial markets in the Eurosystem” on the same terms as rivals that are located there.

“This is one more example of the gradual transformation of the single market into a euro-zone market, which is not what the U.K. or other non-euro countries have signed up to,” Syed Kamall, leader of the EU Parliament’s European Conservatives and Reformists group, said in an e-mail. “It is absolutely vital that we get legal clarity as to whether this is an acceptable shift or not.” The hearing at the court in Luxembourg is the latest in a series of U.K. maneuvers against EU responses to the financial crisis, including a possible tax on transactions and curbs on bankers’ bonuses. The U.K. is on a losing streak at the European Court of Justice. It failed to overturn EU powers to ban short selling and was told that an early challenge against the transaction-tax plan was premature.

• QE Should Only Be Emergency Tool, ECB Board Member Says (Bloomberg)

European Central Bank Executive Board member Sabine Lautenschlaeger said policy makers should only consider radical programs such as quantitative easing if the euro area is on the verge of deflation. “While such measures are in general part of the toolkit, the prerequisites for such a monetary-policy measure must be particularly high as the side effects are especially significant,” Lautenschlaeger said in Hamburg yesterday. “Only in a real emergency situation, for example in the case of imminent deflation, could in my view such an instrument be considered. Those risks are neither visible, nor do we expect them.”

The ECB stepped up its fight against the risk of falling consumer prices last month with a raft of stimulus measures including a benchmark interest rate near zero, a negative deposit rate and a flood of liquidity for banks aimed at reviving lending to the real economy. ECB President Mario Draghi has pledged further measures such as quantitative easing if the outlook for consumer prices in the euro area deteriorates.

A 20% drop in the yen, and even that doesn’t help one bit ?!

• Weak Yen No Help For Japanese Exporters (Bloomberg)

Japanese exporters looking to boost shipments after the first monthly decline in more than a year can’t rely on a weaker yen for support, according to economists led by Mary Amiti of the Federal Reserve Bank of New York. While depreciation typically favors exporters, a decline in the yen would boost the cost of the fuel imports needed by Japanese companies to manufacture products, according to a post today on the New York Fed’s Liberty Street Economics blog. “Yen depreciation drives up the marginal costs of Japanese exporters,” Amiti wrote, with Oleg Itskhoki of Princeton University and Jozef Konings at University of Leuven. This “results in a smaller share of the depreciation being passed on into their export prices.”

Prime Minister Shinzo Abe is deploying a three-pronged program of monetary easing, government spending and business deregulation as he seeks to lift Japan from two decades of economic stagnation. His measures have yielded mixed results, with exports falling for the first time in 15 months in May after the economy expanded at the fastest pace since 2011 in the first quarter. The yen strengthened 0.2% to 101.88 per U.S. dollar as of 2:12 p.m. in New York. The currency is forecast to slide to 106 by the end of the year, after gaining 3.4% since Dec. 31. Japan’s fuel imports have surged since the 2011 earthquake shuttered nuclear plants across the country, with imports rising from 4.4% of gross domestic product to 5.9%, Amiti wrote. “The replacement of nuclear power with imported fuels works to increase the impact of the weaker yen on the production costs of exporters,” Amiti wrote. The economists’ study appears in the American Economic Review’s July edition.

• Japan’s Current-Account Surplus Masks Export Weakness (Bloomberg)

Japan posted a fourth straight current-account surplus, as income from overseas investments masks the failure of the yen’s slide to boost exports. The excess in the widest measure of trade was 522.8 billion yen ($5.1 billion) in May, the finance ministry reported in Tokyo today, beating the median forecast of 417.5 billion yen in a Bloomberg survey. Exports rose 2% from a year earlier. Export volumes remain under the level when Prime Minister Shinzo Abe came to power in December 2012, despite the yen’s 16% slide against the dollar over the period. Abe’s task is to ensure his growth strategy — the third of his so-called three arrows of Abenomics – gives companies enough of an edge over overseas rivals to boost outgoing shipments.

“The strength of recovery in global demand will play a bigger role than the currency in affecting Japanese exports,” said Koichi Fujishiro, an economist at Dai-ichi Life Research Institute in Tokyo. “Sluggish exports can be attributed to the rising ratio of overseas production.” While a drop in a country’s currency tends to favor its exporters, the weaker yen boosts the cost of the fuel imports needed by Japanese companies to manufacture products, according to research by economists led by Mary Amiti of the Federal Reserve Bank of New York. “Yen depreciation drives up the marginal costs of Japanese exporters,” Amiti wrote in the note posted yesterday, with Oleg Itskhoki of Princeton University and Jozef Konings at University of Leuven. This “results in a smaller share of the depreciation being passed on into their export prices.”

Fading star.

• Italian PM Renzi Seeks to Abandon Austerity In EU (FT)

It is less than a month since Britain’s prime minister David Cameron badly misread German politics and was left isolated and spitting mad after Chancellor Angela Merkel abandoned him over the appointment of the European Commission president. Is the leader of another leading EU country about to make the same mistake? Matteo Renzi, the new Italian prime minister, has started Italy’s six-month presidency of the EU touting a turning point in Europe’s fight over austerity: a seven-page “strategic agenda” in which all EU leaders – including Ms Merkel – agreed to “flexibility” in interpreting the eurozone’s contentious budget rules. Those rules, adopted three years ago at the height of the eurozone crisis, require all euro members to slash deficits and quickly reduce national debt or face potentially heavy sanctions from the bean-counters in Brussels. But without the freedom to invest more Mr Renzi fears he will be unable to pull Italy out of economic despair.

Officials in Italy, whose sovereign debt level is second only to Greece, argued that with the acute phase of the eurozone crisis over it was time to loosen those rules. They believe they have achieved precisely that with the new agreement. “This is an important political point for us,” Mr Renzi said after the deal was reached. “We have obtained a document which, for the first time, concentrates on growth.” In some respects, Mr Renzi is correct. Just four months ago, the German finance ministry was arguing that Brussels was interpreting the rules too leniently, insisting the commission had incorrectly given Spain and France two additional years to hit the EU’s deficit targets. Now, Ms Merkel has signed an agreement which calls for “making best use of the flexibility” in those same rules. Score one for Mr Renzi.

Europe lost the beggar they neighbor game.

• ECB Under Pressure To Tackle ‘Crazy’ Euro (FT)

Fabrice Brégier, chief executive of Airbus’s passenger jet business, said the ECB should intervene to push the value of the euro against the dollar down by 10 per cent from an “excessive” $1.35 to between $1.20 and $1.25. “[Europe] cannot be the only economic zone of the world that doesn’t consider its currency as a weapon … as a key asset to promote its economy”, he told the Financial Times in an interview. Mr Bregier’s comments coincide with calls from the International Monetary Fund and politicians in some eurozone countries – France in particular – for the bank to consider a programme of quantitative easing to tackle low inflation, sluggish economic growth and the strong euro.

Benoît Coeuré, a member of the ECB’s executive board, acknowledged in an interview that the stronger the euro became, the more the bank would come under pressure to act. “A lot of the low level of inflation … is due to the strength of the euro so the stronger the euro the more we have to do monetary accommodation. ” However, he rejected calls to focus on the exchange rate explicitly. “It is not possible to target it because exchange rates are set on global markets, so it wouldn’t be wise or possible for us to have it as a policy target”. He also insisted there was no pressing need for the ECB to embark on a round of QE. “I see the odds as being low,” he said. “I am very convinced that what we decided already will work and will prop up inflation.”

In June, the ECB set out several exceptional measures, including cutting a key interest rate below zero, to tackle the threat of deflation. Despite the strength of these measures, the euro has barely weakened, and was worth $1.36 on Monday. Some economists believe the euro is unlikely to depreciate against the dollar considerably unless the ECB engages in quantitative easing. Mr Coeure expressed doubts about the effectiveness of QE, which has been used by the US Federal Reserve and the Bank of England. “Something that has worked in the US or in the UK may not work in the eurozone because we are financed by banks, not by financial markets. The level of government bond yields is very low. Why would we need QE?”

The shadows want their place in the sun.

• China Developers Slow to Pay Realtors Amid Rout (Bloomberg)

Chinese developers, hit by tighter liquidity and a widespread anti-graft campaign, are delaying paying fees to realtors who help them sell new projects, according to the nation’s biggest real estate brokerage. Centaline Group, which owns Centaline Property Agency Ltd., has about 1 billion yuan ($161 million) of uncollected receivables due, group founder Shih Wing Ching said in an interview. Developers pay the fees only after they they get the sales proceeds, he said. “It used to be easy for buyers to obtain mortgages, then the developers will pay commissions,” Shih said on July 4 from his office in Hong Kong, where Centaline is based.

Property services businesses such as Centaline are being affected by the slowdown in China’s property industry, prompted by the government’s four-year effort to rein in prices and a surplus of empty units. Home sales from January to May slumped 10% from a year earlier, a stark contrast to the 27% surge in 2013, even as developers tried to boost sales by slashing prices and offering incentives. Project launches are also being delayed as developers can no longer “offer advantages” to officials in order to speed up pre-sale approvals amid a fledging crackdown on corruption, Shih said. The old system of doing business is being overturned, he said. “Aside from disruption to the developers’ liquidity, our customer base is also affected by the anti-corruption drive,” he said. “In the past, officials and their relatives made up between one-fourth and one-third of buyers.”

Centaline, which receives about 10 billion yuan in commissions a year, has cut about 10 percent of staff in China from last year to about 40,000 people, according to Shih. Home prices will continue to fall, especially in second- and third-tier cities where even offering discounts won’t be enough to stimulate enough demand, he said. New-home prices in May fell in 35 of the 70 cities tracked by the government, the most in two years, China’s statistics bureau said last month. Prices in Hangzhou, considered a second-tier city, fell 1.4 percent on month, the largest decline, while they gained 0.2 percent in Beijing.

HA!

• Greece Resists Troika on Third Bailout as Draghi Protests Delays (Bloomberg)

Greece fought off calls to consider a third bailout as European Central Bank President Mario Draghi warned that the pace of economic fixes is slowing, officials said after euro-area finance ministers met yesterday. Greece has ruled out further aid – which would come with another raft of conditions – after its current rescue ends, a Greek official told reporters in Brussels. According to the so-called troika of International Monetary Fund, ECB and euro-area authorities, Greece may need one anyway, an EU official said. Further emergency aid will probably be needed as the government still faces a funding shortfall, can’t count on financial-market support and is slipping further behind on its commitments to overhaul the economy, the EU official said.

The troika’s concerns were underlined by Draghi’s warning to Greek Finance Minister Gikas Hardouvelis that Greece should not assume its reforms have been completed. At stake is Greece’s ability to win debt relief from its euro-area creditors. This writedown is the main reward that authorities have to offer if Greece meets its commitments – or withdraw if the Mediterranean nation falls short. The troika wants Greece to focus on its economic overhauls rather than rely on fragile and tenuous links to markets, the EU official said. Greece faces a 12 billion-euro ($16 billion) financing gap in 2015 before taking into account money raised in possible bond sales.

” … the real economy is somewhere between the toilet and a rat hole”.

• We Are All Ninja Turtles Now (Jim Kunstler)

The Fourth of July rolled in just in time to celebrate the disintegration of Iraq following our eight-year, three trillion dollar campaign to turn it into a suburb of Las Vegas. Me and my girl went over to the local fireworks show, held on the ballfield of a fraternal order lodge on the edge of town. The fire department had hung up a gigantic American Flag — like, fifty feet long! — off the erect ladder of their biggest truck, in case anybody forgot what country they were in. Personally, I was wondering what planet I was on. It was a big crowd, and every male in it was dressed in a clown rig.

The complete outfit, which has (oddly) not changed in quite a few years (suggesting the tragic trajectory we’re on), includes the ambiguous long-short pants, giant droopy T- shirt (four-year-olds have proportionately short legs and long torsos), “Sluggo” style stubble hair, sideways hat (or worn “cholo” style to the front ), and boat-like shoes, garments preferably all black, decorated with death-metal band logos. You can see, perhaps, how it works against everything that might suggest the phrase: “competent adult here.” Add a riot of aggressive-looking tattoos in ninja blade and screaming skull motifs and you get an additional message: “sociopathic menace, at your service.” Finally, there is the question: just how much self-medication is this individual on at the moment? I give you: America’s young manhood.

Does it seem crotchety to dwell on appearances? Sorry. The public is definitely sending itself a message disporting itself as it does in the raiment of clowning. Here in one of the “fly-over” zones of America — 200 miles north of New York City — the financial economy is mythical realm like Shangri-La and the real economy is somewhere between the toilet and a rat hole. Under the tyranny of chain stores, there really is no true local commercial economy. The few jobs here are menial and nearly superfluous to the automatic workings of the giant companies.

Wow!

• Egypt President Sisi Defends 78% Fuel Price Rise (Guardian)

Cairo’s taxi and microbus drivers have staged impromptu protests in anger at a surprise rise in fuel prices, providing an early test of the popularity of Egypt’s new president, Abdel Fatah al-Sisi. In several Cairo neighbourhoods roads were temporarily blocked as fleets of the city’s distinctive white taxis came to a standstill, while in the canal cities of Suez and Ismailia police used tear gas to disperse a small gathering of microbus drivers. Egyptians woke up on Saturday to the news that petrol prices had risen by up to 78%, part of a broader swath of price increases that the government says is necessary to boost Egypt’s ailing economy. Food and energy subsidies traditionally eat up a quarter of state spending and the government is taking steps to reform its subsidy programme and revive an economy badly scarred by three-and-a-half years of political upheaval.

Successive governments have avoided such a decision, fearful of a potential backlash from a population already faced with rising food prices and an unemployment rate of 13.4%. More than a quarter of Egypt’s 82-million strong population lives in poverty. How the country reacts to the new price hikes, just one prong of the government’s broader austerity strategy, will provide clear indications of the strength of Sisi’s popularity. Although he was elected with over 96% of a public vote in May, turnout was sluggish. A year after the overthrow of former president Mohamed Morsi, Egypt remains jaded and divided. Although Egypt’s prime minister defended the subsidy cuts on Saturday, saying that the savings would be channelled towards improving health and education, Egypt’s newspaper front pages gave his words short shrift the following morning. “The hour of suffering has struck,” read the headline on privately owned daily Al-Masry Al-Youm. “The fire of fuel lights the street,” said Al-Shorouk, an independent newspaper.

Love this!

• Newspaper Fights Dengue With Mosquito-Repellent Ink, Sales Soar (Independent)

A newspaper in Sri Lanka has saved lives be imprinting its pages with mosquito repellent to stop the spread of deadly dengue fever. According to the Mawbima newspaper, the illness has reached “epidemic proportions”, with more than 30,000 people infected in 2013. Young children are among those who have been killed by the virus. Spread by mosquitos, dengue is widespread in tropical regions and starts with high temperatures and flu-like symptoms. No medication is known to treat the disease and although it usually clears up itself within a fortnight, severe cases can cause shock, bleeding, organ damage and death. Mawbima, a national newspaper, worked with Leo Burnett in Sri Lanka on a campaign to raise awareness and stop its spread around National Dengue Week.

They discovered that mixing citronella essence, which repels mosquitos, with ink, the paper itself would stop mosquitos biting. Most people read Mawbima in the early morning and evening – the very time the Aedes aegypti mosquito that carries dengue bites. The combination was first tested in adverts where large letters were printed with the special ink, then on posters at bus stops. The paper also ran articles on how to prevent dengue and gave mosquito repellent patches to schoolchildren. On World Health Day, in April, Mawbima published what it believes is the world’s first mosquito-repelling newspaper, with every word printed in the citronella ink. It is not clear whether the paper will continue the special printing but the company may be inspired by the effect it had on sales. The paper reportedly sold out by 10am – a sales increase of 30 per cent – and increasing its readership by 300,000 people.

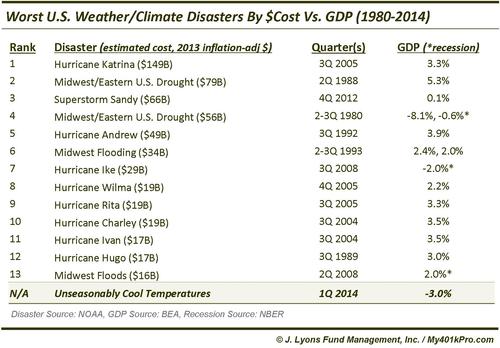

One more nail into the “weather caused -3% GDP” coffin.

• Worst US Weather/Climate Disasters By Cost Vs. GDP – 1980-2014 (JLFMI)

A couple weeks ago we posted a table of the 25 Worst Quarterly GDP Prints in U.S. History, which included the 1Q 2014 reading of -2.96% at the #17 spot. [..] The sole purpose of the post was to present a data-based counter-argument to the seemingly unanimous voice of mainstream media pundits and investment bank economists casually suggesting that the GDP print be dismissed out-of-hand as a weather-induced aberration. To us, the suggestion seemed somewhat outrageous considering, as the table showed, the -2.96% print was nearly twice as bad as any in history not associated with a recession. We’re not saying that a recession is at hand necessarily. There is a first time for everything. All we are saying is that the reading should not be so casually dismissed.

Today’s ChOTD is a follow-up table taking to task the object of our other objection surrounding the 1Q 2014 GDP release: the weather excuse. Presented here is the list of the top weather/climate disasters, based on economic damage, in the U.S. from 1980-2014 and the GDP reading for the quarter(s) during which each event took place. We also included the 1Q 2014 GDP print for the sake of comparison (for those wondering, the disaster data comes from the National Oceanic and Atmospheric Administration, the official scorekeeper of such data. Economic costs related to disasters before 1980 were not included as they were not readily available).

The first thing that jumps out at us is that, by and large, these disasters were not accompanied by concomitantly weak GDP readings. In fact, only 2 of the worst 13 disasters saw negative GDP’s during the quarter(s) they took place. And those 2 (1980 and 2008) occurred when the U.S. was already in a recession (as later determined by the National Bureau of Economic Research). GDP during the other 11 disaster-related quarters averaged +2.9%, with 7 of the 11 sporting prints of +3% or higher. Additionally, there were two quarters (3Q 2004 and 3Q 2005) that had the misfortune of experiencing more than one of these worst disasters. Despite the duel challenges, those quarters recorded +3.5% and +3.3% GDP figures.

Now let’s assume (generously) that the “unseasonably cool temperatures” were in fact the cause of the negative GDP print in the 1st quarter. That would imply that weather shaved more than $118 Billion off of GDP from the 4th quarter of 2013. That sum would make it the 2nd costliest “weather disaster” of all-time, after Hurricane Katrina. And that merely gets GDP to positive territory from -3%. If, hypothetically, we assume that the disasters above caused a 3% reduction in concurrent GDP (rather than merely the estimated costs in the table), the non-recession disaster-related quarters would have averaged nearly +6% GDP readings. Readings that high have only occurred in 10% of the quarters during this entire period.

We’re not suggesting that weather played no part in the weak 1Q GDP number. Perhaps it did. We simply take exception to the suggestion that a -3% GDP print be written off as a “weather-induced” outlier. This is particularly so when comparing the figure with historical GDP readings occurring during quarters encompassing the worst weather-related disasters in U.S. history, which generally fared just fine. Perhaps we’re just not smart enough to understand the nuanced effects that cold weather can have on 3 months of economic activity across 50 states. But when we see a GDP figure that far outside the norm of even disaster-related quarters, it raises our BS-meter.

Home › Forums › Debt Rattle Jul 8 2014: The Future Of Banking Is Pay Cash Only