DPC Snow removal – Ford tractor Washington, DC 1925

As Germany is set to reject a Greek loan extension request (and no, international press, that is not the same as an extension of the bailout program), Steve Keen uses proprietary numbers issued by the OECD – which is supposed to be on Germany’s side?! – to show how dramatically austerity has failed in Europe- that is, if the recovery of the Greek and Spanish economies was ever the real target. It certainly failed the populations of the countries.

The problem is that nobody, not even the OECD can for Germany to answer to a report. But that does not make the case that is made, any less obvious, or bitter for that matter. Not many people remain ready to think that Greece will do what it has said it will, but I think they have been very consistent in their stated goals, and people get distracted too much by semantics at their own peril.

As Steve shows, and Syriza proclaims, more of the same is not on the table, for good reason. It will and can only make matters worse for Greece. Germany – and the ECB – choose to entirely ignore the consequences of their theories, in particular the humanitarian crisis they have caused in Greece. And any political union that ignores the misery it unloads upon its citizens has a short shelf life.

I see a majority voices out there claiming that Syriza is busy capitulating, but I don’t think that. They’ve always said they are willing to go far to reach consensus with Brussels in order to stay in the EU and eurozone. And that’s what they’re showing. In the world of political dealing and scheming, the Greeks have been remarkable consistent; so much so that this is itself leads people to claim they are not.

But I still wouldn’t rule out the possibility that Varoufakis has long come to the conclusion that the eurozone must and will implode no matter what anybody does, and that he’s simply jockeying for the best position when the time comes to leave the eurozone.

Germany’s bullying- which is how its actions are being perceived by fast growing numbers of people – will come back to hurt it. The eurozone is made up of independent nations, most with their own specific culture and their own language. Trying to browbeat them all into submission, and yes, that is where Germany’s stance is leading, will only lead to much bigger trouble.

But first, it’s still ‘merely’ and economic issue, and it’s therefore the economic ideas behind EU policies that need to be discussed and revised. Unleashing misery on entire nations is indefensible not only from a humanitarian point of view, but also from a historical one. Who in the present context would know that better than Germany?

What Germany holds in its hands, but does not at all realize, is the survival of the European common currency. It must realize that the euro will fail if it tries only to dictate all policies to everyone at every turn. If Germany insists on applying the kind of dictatorship to Europe that it has been doing, the euro is dead. Both for political and historical reasons – nobody will accept being bullied by the Germans for long – and for economic reasons, because Germany’s economic ideas are simply too damaging for other eurozone nations.

Germany – and Holland – are so full of themselves at present – both the politicians and the people – that they are busy blowing up the EU, their cash cow, without realizing this even one moment.

If Greece gives in, Germany will have won, but its bully status will come to bite it in the face. European nations don’t accept bullying, and certainly not from Germany. It’ll be a Pyrrhic victory: the beginning of the end. If Greece however stands firm in its demands, it’s also curtains for the EU. If Greece leaves, it won’t leave alone.

Only the third option, Germany caving to Greek demands, can save the EU. But Merkel and Schäuble have prepped their people to such an extent with the wasteful lazy Greeks narrative that they would have a hard time explaining why they want to give in. The EU may thus fall victim to its own propaganda. That would be funny, no matter how tragic it is at the same time. But it would be an open invitation to the far right as well.

Steve Keen:

For Greece And Many Others, Economic Reform Is Bad For Your Economic Health

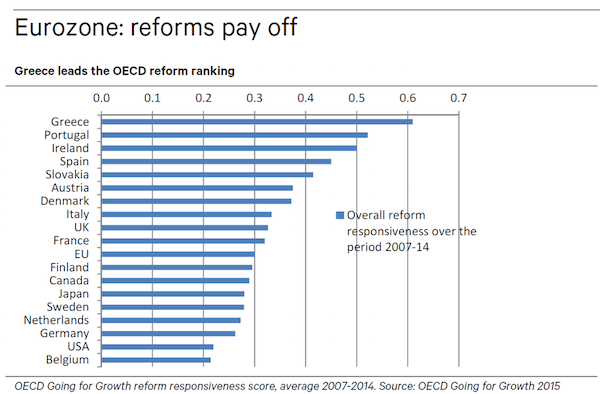

A quick quiz: which four countries do you think have done the most to reform their economies over the last seven years? OK, who said Greece, Portugal, Ireland and Spain? No one? Actually, someone did: the OECD. Yes, I kid you not, according to the OECD, the country that has done the most to reform its economy over the last seven years—that is, from before the 2008 economic crisis until well after it—is Greece. Followed at some distance by Portugal, Ireland and Spain.

I saw this in a tweet, and I simply had to go searching to see for myself. And there it was, on page 111 of the OECD’s publication Going For Growth 2015, released on February 9. The top economic reformers were the basket cases of Europe and the world in general. Unemployment in Greece is 27%; in Portugal it’s 15%, Ireland 12%, and Spain 25%. Those are very, very sick economies. And yet they are also the OECD’s top reformers.

You are, I hope, wondering “how come? Isn’t reform supposed to be good for you?” Well, that’s the fairy story—sorry, theory: reform your economies according to our recommendations, and—whatever else happens—your economy will grow more rapidly and be more stable to boot. Unfortunately for those purveying this fairytale, they also developed metrics by which the degree of reform could be measured, so that a decade later, we can compare the fairy story to the reality.

The EU program that Greece is currently refusing to continue implements part of what is known as the ”Stability and Growth Pact” or SGP—which a radio interviewer last week realized has (with just a slight rearrangement of the letters) a much more apt acronym of GASP. And the other countries that are also under the control of GASP include… Portugal, Ireland and Spain.

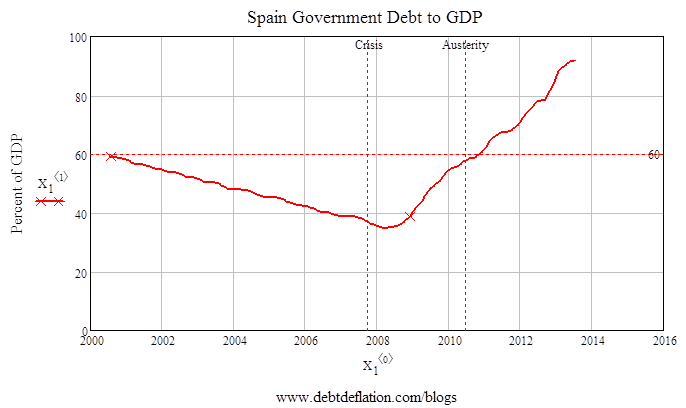

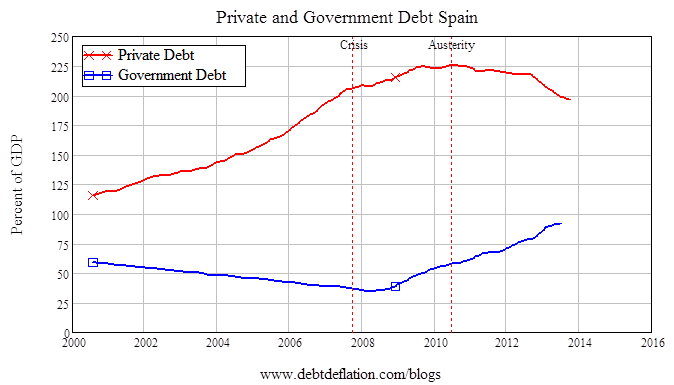

Greece is refusing to continue with this program, not because it is “refusing its medicine”, but because the medicine is actually poison. And Greece itself is not the proof of that: the other countries on this list are—especially Spain. Spain did everything that the GASP and mainstream economics recommended, not merely after the crisis but before it as well. The GASP required that member countries of the Eurozone have a government debt to GDP ratio of 60% or below, and run a maximum deficit of 3% or less of GDP.

Spain was doing both before the crisis. Its government debt ratio was below 60% from early 2000, and trending down—hitting a low of below 40% shortly after the crisis began.

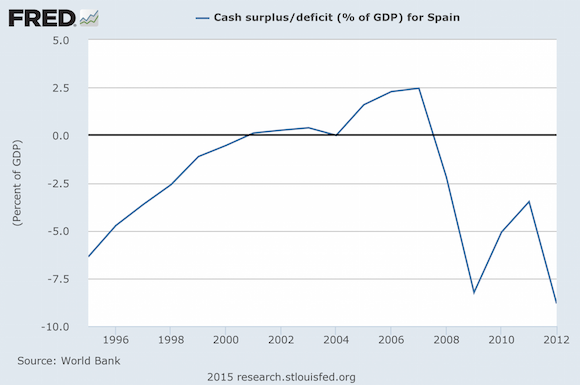

Its deficit was even better—not only was it below 3% of GDP at the introduction of the Euro, by 2001 it was in surplus—hitting a peak of 2.5% of GDP in 2007.

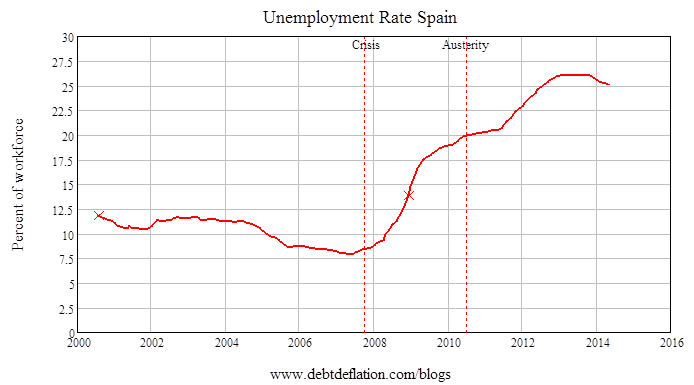

Before the crisis hit, Spain was being lauded as a success story for the GASP, and superficially for good reason: not only was it following the GASP program by running surpluses, and reducing its government debt, its economy was booming. Unemployment, which had always been high, trended down from 12.5% at the start of the Euro to 8% by 2007. And then it all went pear-shaped.

This raises two questions, the answers to which cement the case that the EU’s austerity program should end everywhere—and not just in Greece. Firstly, how did Spain appear to be doing so well, and then collapse so badly? And did the EU’s policies contribute to Spain’s problems?

The answer to the first question involves what happened to the debt that GASP ignores (as do conventional economists everywhere): private debt. While the GASP imposed strict controls on government debt, it ignored the blowout in private debt on the erroneous argument that private debt is economically unimportant. Private debt rose from about 120% of GDP in early 2000 to over 200% by the time the crisis began, and peaked at 225% of GDP when the GASP’s austerity program kicked in, as Figure 5 shows.

The growth in private debt gave the economy an enormous boost as it financed Spain’s housing bubble, and the tax revenue from this bubble was the main reason that the government was in surplus from 2000 until the crisis hit. The rise in private debt dwarfed the decline in government debt, and the huge stimulus from private sector borrowing more than compensated for the drag on the economy from the government surplus. As the government was “salting away pennies”, the private sector was wallowing in new debt-financed spending.

But to do so, the private non-bank sector had to get more indebted to the banks—as Figure 5 shows. When growth in private debt turned around, the housing bubble collapsed and private sector borrowing went into free-fall. Then, and only then, did government debt rise—as increased government spending slightly compensated for the plunge in private debt-financed spending. Ultimately, by 2010, the stimulus from rising government spending slowed down the decline in private borrowing. But then austerity kicked in and the government stimulus stalled. Consequently the private sector went from mild deleveraging into heavy deleveraging—reducing its debt by as much as 20% of GDP per year.

Don’t get me wrong here: I am a critic of private debt financed spending when it finances Ponzi Schemes like Spain’s housing bubble, and I believe that sustained recovery will not happen until private debt levels are drastically reduced. But when a private debt bubble bursts, government spending attenuates the downturn. To limit the growth in the government deficit makes the crisis worse, without doing much to reduce private debt compared to GDP because GDP collapses along with the falling private debt.

So these crises—in the OECD’s pin-up countries of Greece, Spain, Italy and Portugal—are the product of the EU’s policies. The only way out of the crisis is to end the policies themselves, as Greece is demanding now.

And if Syriza gives in and the EU’s policies are maintained? Then this will go from being an economic and social tragedy to a political one as well. If Syriza caves in, then the Greeks who voted for a left anti-austerity party will switch allegiance to a right anti-austerity party—the fascist Golden Dawn—because they will claim that only they have the balls to actually do in office what they promise in opposition.

Home › Forums › How Germany Is Blowing Up The European Union