DPC Masonic Temple, New Orleans 1910

UniCredit, Credit Suisse, Standard Chartered and Deutsche Bank. Next!

• Deutsche Bank: Tip of the Iceberg for Cutbacks at European Banks? (WSJ)

Deutsche Bank’s warning that it expects a €6.2 billion third-quarter loss highlights a potentially bumpy financial-reporting season looming for European banks, as a slate of new chief executives confront concerns over profitability. Credit Suisse, Standard Chartered and Deutsche Bank, all under new chief executives, are among banks facing muted growth in their home markets and coping with more stringent regulation and capital requirements. Those issues, coupled with factors including uncertainty over China’s growth, U.S. interest rates and the slide in global commodities prices, have combined to depress profits for European banks. Meanwhile, U.S. rivals, most of which restructured fairly quickly following the global financial crisis, are now in growth mode, winning business away from European rivals, who have been slower to adapt.

European banks need to rethink quickly or risk losing more ground, according to analysts. Restructuring “remains top of the agenda” for Europe’s banks, analysts at Morgan Stanley wrote in a note this week, predicting U.S. banks once again would put in a better revenue performance this year in fixed income and equities and continue beating European rivals next year across investment banking. Deutsche Bank late on Wednesday took a multi-billion-dollar charge against assets in its investment bank and retail- and private-banking operations for the third quarter. It said the charge would materially impact third-quarter results, which it reports on Oct. 29. New CEO John Cryan on that day will announce a new strategy, widely expected to ratchet up the bank’s earlier attempts to cut costs and shed unwanted assets.

Credit Suisse Chief Executive Tidjane Thiam, who joined the bank in July, is expected to outline sharp investment banking cuts, as part of an effort to meet global capital rules and new Swiss bank-specific requirements. The bank is also thought to be readying a substantial capital increase to be unveiled alongside Mr. Thiam’s grand plan. A poll of investors by Goldman Sachs analysts found 91% expected the bank to raise more than 5 billion Swiss francs ($5.16 billion) in fresh capital. On Thursday, in response to an article in the Financial Times that reported that Credit Suisse planned to raise an amount in line with that figure, the bank said: “we are conducting a thorough assessment of Credit Suisse’s strategy, evaluating all options for the group, its businesses and its capital usage and requirements.”

US banks are dropping too.

• Banks Take Spotlight As Earnings Season Heats Up (Reuters)

The financial sector, recently a weak performer in the stock market, will garner the majority of investor attention next week as a number of big banks post their quarterly results. Goldman Sachs, Bank of America, Wells Fargo, Citigroup and JPMorgan – the five biggest U.S. banks by market cap – are due to report results as the sector has trailed the market in recent weeks and earnings estimates have fallen. Financial companies are expected to show earnings growth of 8.4%, behind only telecoms and consumer discretionary companies in expected growth for the quarter. However, that growth is down from the 14.8% expected at the start of the quarter, and down by half from the 17.8% growth expected at the start of the year.

In the last 30 days, banks have seen their estimates steadily lowered, with Goldman the biggest victim. Its estimates for the quarter are down by 25% in that time period. While the broader market has recovered from losses sustained in the latter half of August, banks have struggled. The Fed’s decision not to raise rates, coupled with economic concerns and worries about trading revenues, have tethered shares of the big banks. The S&P 500 financials index has underperformed the broader market, and has slumped 5.6% this year so far, compared with a 2.2% decline in the S&P 500. In the last month, the S&P 500 has gained 2.2%, but the five biggest financial institutions are all flat or down.

That’s 1000 senior staff who were no longer contributing any profits.

• Standard Chartered ‘To Cut 1,000 Senior Jobs’ (BBC)

Standard Chartered bank, a London-based lender that makes most of its profit in Asia, could cut up to 1,000 senior jobs, according to an internal memo sent to staff. The move from chief executive Bill Winters is meant to cut costs. The bank has grown very quickly since the financial crisis and some roles are now not needed, sources told the BBC. Standard Chartered said it had disclosed before “that there would be further personnel changes to come”. “We have already acted to reduce management layers, and a result will have up to 25% fewer senior staff,” the bank said in a statement. Mr Winters told staff in the memo that about a quarter of senior managers, of director level or above, would be cut. There are about 4,000 bankers in the grades affected by the decision.

The bank employs about 88,000 people in total. It has grown rapidly, from about 44,000 in 2005. Mr Winters took over from former diplomat Peter Sands in June and said he would simplify Standard Chartered with a “new management team and simpler organisational structure”. The bank has already shed some businesses, in Hong Kong, China and Korea, booking a gain of $219m and improving its capital position. Standard Chartered hired Mark Smith from Asia-focused rival HSBC to join as new chief risk officer. Mr Winters also cut the dividend to help the bank strengthen its capital base – a safety net protecting it from unexpected financial knocks. He has also not ruled out raising more capital if needed.

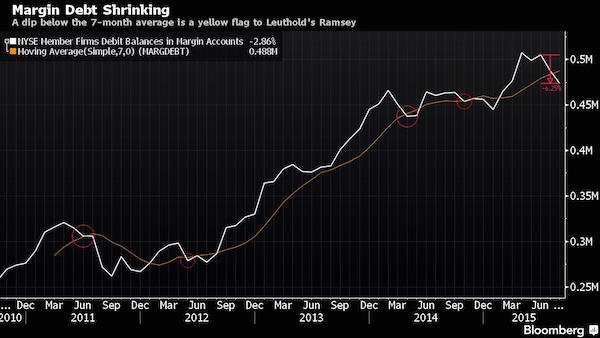

Freefall? That little drop is nothing. Wait till it falls back to, say, 2010 levels. Margin debt levels simply indicate to what extent markets are casino’s.

• Margin Debt in Freefall Is Another Reason to Worry About S&P 500 (Bloomberg)

Most people get concerned about margin debt when it’s shooting up. To Doug Ramsey, the problem now is that it’s falling too fast. The CIO of Leuthold Weeden whose pessimistic predictions came true in August’s selloff, says the tally of New York Stock Exchange brokerage loans flashed a bearish sign when it slid more than 6% in July and August. The retreat took margin debt below a seven-month moving average that suggests demand for stocks is dropping at a rate that should give investors pause. For years, bull market skeptics have warned that surging equity credit portended disaster for U.S. shares, pointing to a threefold runup between the market low in March 2009 and the middle of this year. Ramsey, who says that surge was never strong enough to form the basis of a bear case, is now worried about how fast it’s unwinding.

“Margin debt contracting is a sign of loss of investor confidence and it’s confirmation of a lot of other evidence we have that we’ve entered a cyclical bear market,” Ramsey said in a phone interview. “We got a lot of traditional warning signs leading up to the high in terms of market action, and deteriorating breadth and margin debt is important to the supply-demand analysis.” Margin debt, compiled monthly by the NYSE, represents credit extended by brokerages for clients to buy stock. It hews closely to benchmark indexes such as the S&P 500, primarily because equity is used to back the loans and as its value rises, so does the capacity to lend. “There’s a natural progression of the two moving together,” Tim Ghriskey at Solaris Asset Management said. “We look at it as being predictive if it gets too extreme on either side.”

NYSE margin debt surged from $182 billion to $505 billion in the six years ended in June 2015, roughly tracing the trajectory of the S&P 500, which tripled over the period. The biggest gains came in 2013, with credit rising 35% as U.S. stocks climbed 30% for the best returns in 16 years. Since June, it’s been the other way around, with margin debt falling 6.3% to $473 billion at the NYSE’s last update, which covered August. The S&P 500 slid 4.4% at the end of that period as stocks entered a correction. To Ramsey, a decline as precipitous as that is more worrisome than the preceding run-up. “A lot of people intimated when we broke out to a new high in margin debt a couple years ago that it was out of control, but the%age change in margin debt from the low of 2009 was almost identical to the S&P’s,” Ramsey said. “Now that trend has rolled over.”

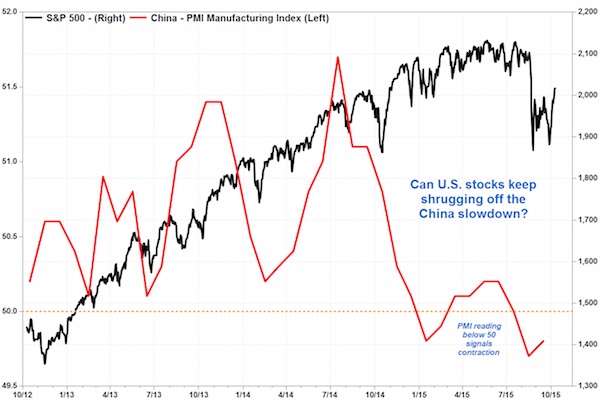

Sudden plunges on over-optimistic models.

• China Is Becoming A Big Red Flag For US Stocks (MarketWatch)

China is fast becoming a major source of worry for the stock market again, after commentary from a number of U.S. companies this week warned that demand from the second-largest economy may have dropped sharply over the past month. That doesn’t bode well for the third-quarter earnings reporting season, which was already expected to be the worst quarter for U.S. companies in six years. Worries about a slowdown in China aren’t new. The more than 40% tumble in the Shanghai Composite and the devaluation of the yuan over the summer helped fuel the selloff on Wall Street in late August, when the S&P 500 index entered correction territory for the first time in about three years.

But those worries had been soothed somewhat, after the Chinese market stabilized in September, and following upbeat comments from some U.S. companies about how business in the country had improved. Nike helped spark some of that optimism in late September, after the blue-chip athletic apparel and accessories giant reported a 30% jump in sales in Greater China in its fiscal first quarter, which ended Aug. 31. But dire outlooks on China from Alcoa, Yum Brands and Nu Skin Enterprises this week could wipe away that optimism, especially considering how sudden the companies’ outlooks soured.

“Over the last year, productivity has increased by just 0.7%, far below the long-run average of 2.2%. Why it is falling remains a puzzle.”

• Buried In The Fed Minutes Is Another Downgrade To The US Economy (MarketWatch)

A goal of a 4% economy? That objective, mentioned frequently in the 2016 presidential race, is getting farther away, according to the latest projections from the staff of the Federal Reserve. Minutes of the Fed’s Sept. 16-17 policy meeting disclose the Fed staff further trimmed its assumptions for the rates of productivity and potential growth over the medium term. The minutes did not specifically quantify the new forecast of the Fed’s in-house economists. The Fed staff’s view was already gloomy. A mistaken leak this summer by the U.S. central bank revealed, going into the Fed’s June policy committee meeting, the U.S. central bank’s staff penciled in potential growth averaging just 1.74% over 2015-2020, according to the document now on the Fed’s website. That’s down from an average growth rate of 3.1% over the past 50 years.

Ordinarily those forecasts would have been kept secret for five years. Fed officials – in other words, the people who get to vote on interest rates – think the economy can growth a little faster than the staff. They pencil in 2.0% for the economy’s long-run growth rate. Potential growth in the long run is a function of two things: population growth and productivity. Productivity is the secret sauce of the economy but it has dropped off sharply since the Great Recession. Over the last year, productivity has increased by just 0.7%, far below the long-run average of 2.2%. Why it is falling remains a puzzle. With trend growth so low, the economy is in a pickle. Even moderate gross domestic product in the range of 2.0-2.5% that the Fed expects can produce inflation. “It’s a bad place to be,” said Robert Brusca, chief economist at FAO Economics.

It went wrong when it began.

• BofA: Here’s The Precise Moment When We Should Have Known QE Went Wrong (BBG)

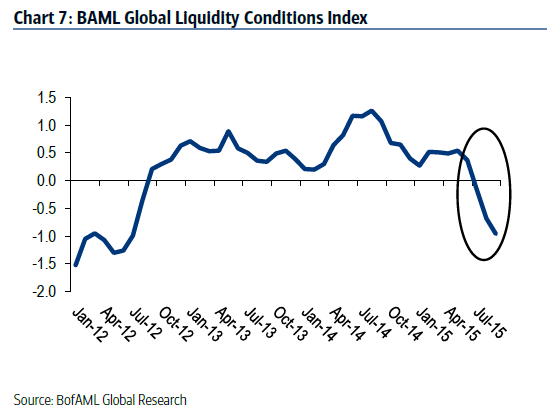

“There’s no such thing as a free lunch” is an oft-quoted maxim in economics, and it seems like a maxim that could easily be applied to the Federal Reserve’s bond-buying program known as quantitative easing. In a new note titled “The real cost of QE,” Bank of America’s FX strategist Athanasios Vamvakidis takes a critical look at the U.S. central bank’s particular brand of unconventional monetary policy, and its changing relationship with financial markets. He contends that “excessive reliance on unconventional monetary policy” is not without side effects, many of which are only now being felt in markets.

At some point during Fed QE, the markets started reacting positively to bad news. In our view, this is when things started going wrong. Bad news became good news for asset prices, as markets expected more QE by the Fed. Asset prices were increasingly deviating from fundamentals, as the markets were trading the Fed instead of the economic reality. This was clearly not sustainable.

Vamvakidis argues that the market’s violent reaction to the Fed’s announcement in the spring of 2013 that it planned to “taper” its bond purchases was one sign that QE had already gone wrong.

We should have known something is wrong. The Fed “taper tantrum” could have been the first signal that QE had gone too far. The second warning may have been the across-the-board emerging markets sell-off that started in mid-2014, as QE tapering was coming to an end and the market started pricing Fed tightening, a sell-off that intensified substantially this year.

All of this doesn’t mean Vamvakidis believes QE should have never happened, of course. He does recognize that the Fed policy helped the U.S. avert another Great Depression in the aftermath of the financial crisis, but he doesn’t believe that bond-buying should be the first choice for action whenever something goes south in the economy. He calls the first round of QE “a necessity,” but is more skeptical of the Fed’s subsequent programs known as QE2 and QE3. Moreover, he notes that despite the continued expansion of balance sheets at a number of central banks around the world, monetary policy conditions have tightened and liquidity has fallen, as shown in the below BofAML chart:

EU refuses to do anything in next 30 years?!

• Greek Debt Has Become Highly Unsustainable: IMF (Reuters)

Greece cannot deal with its public debt through reforms alone and needs a significant extension of grace periods and longer maturities from its European creditors, the head of the IMF’s European department said. The European Commission has forecast in May that Greek debt would reach more than 180% of its gross domestic product this year and euro zone governments, the main creditors of Greece, have promised to start debt relief talks later this year, once Athens implements agreed reforms. “We think that Greek debt… has become highly unsustainable,” Poul Thomsen told a news conference in Lima, on the sidelines of a meeting of the IMF. “We think that Greece cannot deal with its debt without debt relief. Greece cannot deal with debt just through reforms and adjustment,” he said.

Thomsen said that the discussion on how to provide debt relief to Greece has shifted from a nominal haircut on the stock of its debt to capping gross financing needs. The chairman of euro zone finance ministers told Reuters on Thursday that there was broad support for capping Greece’s financing needs at 15% of GDP annually. “What the exact targets should be, we will have to discuss, but there is no doubt in our mind that if Europe wants to go the route of providing relief by lengthening the grace period and lengthening the repayment period, we are looking at a significant lengthening of the grace period and significant lengthening of the repayment period,” Thomsen said.

Too late now.

• ECB Should Focus Asset-Backed Purchases on Periphery: Pimco (Bloomberg)

The ECB should refocus its asset-backed securities purchase program on the countries most in need of its help, according to Pacific Investment Management Co. The ECB is too cautious in its acquisitions and should concentrate on buying bonds from nations with higher debt and deficits such as Spain and Portugal, Pimco money managers Felix Blomenkamp and Rachit Jain wrote in a note to investors. It has mainly bought notes secured by high-quality collateral, including prime mortgages and auto loans, from safer countries such as Germany, France and the Netherlands, they said.

Pimco is expanding on a similar call it made earlier this week for the ECB to concentrate on buying peripheral government bonds. The ECB is acquiring debt including asset-backed securities, which bundle individual loans into bonds that can transfer risk to investors from banks, to encourage lenders to offer more credit and stimulate Europe’s economy. “The ECB’s low risk appetite in ABS has guided its purchases primarily to select sectors in core countries, which in our view never really needed help to begin with,” they said. “ABSPP should be refocused to more specific sectors, especially in peripheral economies, where loan margins remain high and credit availability is scarce.”

What to watch for going forward in EM: Derivatives and credit events.

• The Hidden Debt Burden of Emerging Markets (Carmen Reinhart)

[..] it was not until after the eruption of the 1994-1995 peso crisis that the world learned that Mexico’s private banks had taken on a significant amount of currency risk through off-balance-sheet borrowing (derivatives). Likewise, before the 1997 Asian financial crisis, the IMF and financial markets were unaware that Thailand’s central-bank reserves had been nearly depleted (the $33 billion total that was reported did not account for commitments in forward contracts, which left net reserves of only about $1 billion). And, until Greece’s crisis in 2010, the country’s fiscal deficits and debt burden were thought to be much smaller than they were, thanks to the use of financial derivatives and creative accounting by the Greek government.

So the great question today is where emerging-economy debts are hiding. And, unfortunately, there are severe obstacles to exposing them – beginning with the opaqueness of China’s financial transactions with other emerging economies over the past decade. During its domestic infrastructure boom, China financed major projects – often connected to mining, energy, and infrastructure – in other emerging economies. Given that the lending was denominated primarily in US dollars, it is subject to currency risk, adding another dimension of vulnerability to emerging-economy balance sheets. But the extent of that lending is largely unknown, because much of it came from development banks in China that are not included in the data collected by the Bank for International Settlements (the primary global source for such information).

And, because the loans were rarely issued as securities in international capital markets, it is not included in, say, World Bank databases, either. Even where data exist, the figures must be interpreted with care. For example, data collected on a project-by-project basis by the Global Economic Governance Initiative and the Inter-American Dialog could provide some insight into Chinese lending to several Latin American economies. For example, it seems that, from 2009 to 2014, total Chinese lending to Venezuela amounted to 18% of the country’s annual GDP, and Ecuador received Chinese loans exceeding 10% of its GDP.

The blessings of modern-day trade deals. The debt is 30 years old…

• US Hedge Fund Threatens Peru With Lawsuit Over Debt (BBC)

A US hedge fund has threatened to sue Peru over bonds issued by the country’s former military regime. Hedge fund Gramercy purchased the defaulted debt at a discount in 2008 after other bondholders failed to reach a deal. Peru’s finance minister said the government would oppose any legal action outside its borders. Purchasing defaulted bonds on the cheap to make a profit in a settlement is a common hedge fund tactic. The country defaulted on the $5.1bn in bonds in the 1980s. Gramercy has threatened to bring a claim against Peru under a tribunal system established in a US-Peruvian trade deal. This type of action has been called “predatory” by groups in favour of sovereign debt relief plans. Argentina has been engaged in a prolonged court battle with hedge funds over bonds it defaulted on in 2005. This week Peru has played host to meetings of the World Bank and IMF. Among the topics discussed was how to help country’s restructure debt after a default to avoid drawn-out court battles.

Brazil’s hole will get much deeper. How on earth can they stage a World Cup in 2018?

• Brazil: In A Hole And Still Digging (Ogier)

Brazil has long been hailed as the country of the future. But the decision last month by Standard & Poor’s to strip Latin America’s largest economy of its coveted investment grade status provided confirmation — if any were needed — of its fall from grace. “Brazil is going through its worst period,” says Nicola Tingas, chief economist at Acrefi, a credit association for non-banking institutions. “There is structural disorder, which goes beyond the mere economic cycle. It destroys capital. Confidence has been destroyed. The economy has been weakened.” For a long time, the resilience of the Brazilian economy had confused the most pessimistic economists and offered bright opportunities for high yield investors. Dilma Rousseff herself challenged such “pessimists” during the latest presidential campaign.

But a year after she won a second presidential term, Brazil is in a terrible mess. Debt financing costs have soared and Brazil’s CDS spreads became greater than Russia’s that month when they neared 400 points. “The fiscal deterioration is now faster than our baseline scenario and the political risks remain challenging,” said Shelly Shetty, head of Latin American sovereigns at Fitch Ratings, during Fitch’s global sovereigns conference in New York in September. Joaquim Levy, the embattled finance minister, has publicly admitted the scale of the problem. “Obviously, the house is not in order,” he said in Congress after the government presented a budget blueprint that included a R$30bn ($7.6bn) deficit in early September. This marked the beginning of the end of the fiscal credibility of the government, according to most observers.

“People were aware of the risk of a downgrade,” says Monica de Bolle, a researcher at the Peterson Institute in Washington “Under these circumstances, nobody could have sent a budget that includes a deficit just under the nose of the credit rating agencies. And even after the downgrade, the [Brazilian] government has kept adopting a form of ostrich policy.” Recession has now settled in. The official forecast is one of a severe GDP contraction of 2.44%. Figures were revised last month from 1.5%. Marcelo Carvalho, the BNP Paribas Latin America chief economist, has forecast a further 2% decline next year. “A recession that lasts for two consecutive years is a very rare occurrence in Brazil. We have data that span a hundred years and this only happened once before in the early 1930s, just after the Great Depression. So we now have a scenario that is similar, despite the fact the world economy is not as ugly as it was after the 1929 crisis,” he says.

The flipside of the western narrative.

• War on Islamic State: A New Cold War Fiction (Nafeez Ahmed)

Russia is bombing “terrorists” in Syria, and the US is understandably peeved. A day after the bombing began, Obama’s Defence Secretary Ashton Carter complained that most Russian strikes “were in areas where there were probably not ISIL (IS) forces”. Anonymously, US officials accused Russia of deliberately targeting CIA-sponsored “moderate” rebels to shore-up the regime of Bashir al-Assad. Only two of Russia’s 57 airstrikes have hit ISIS, opined Turkish Prime Minister Ahmet Davutoglu in similar fashion. The rest have hit “the moderate opposition, the only forces fighting ISIS in Syria,” he said. Such claims have been dutifully parroted across the Western press with little scrutiny, bar the odd US media watchdog. But who are these moderate rebels, really?

The first Russian airstrikes hit the rebel-held town of Talbisah north of Homs City, home to al-Qaeda’s official Syrian arm, Jabhat al-Nusra, and the pro-al-Qaeda Ahrar al-Sham, among other local rebel groups. Both al-Nusra and the Islamic State have claimed responsibility for vehicle-borne IEDs (VBIEDs) in Homs City, which is 12 kilometers south of Talbisah. The Institute for the Study of War (ISW) reports that as part of “US and Turkish efforts to establish an ISIS ‘free zone’ in the northern Aleppo countryside,” al-Nusra “withdrew from the border and reportedly reinforced positions in this rebel-held pocket north of Homs city”.

In other words, the US and Turkey are actively sponsoring “moderate” Syrian rebels in the form of al-Qaeda, which Washington DC-based risk analysis firm Valen Globals forecasts will be “a bigger threat to global security” than IS in coming years. Last October, Vice President Joe Biden conceded that there is “no moderate middle” among the Syrian opposition. Turkey and the Gulf powers armed and funded “anyone who would fight against Assad,” including “al-Nusra,” “al-Qaeda in Iraq (AQI),” and the “extremist elements of jihadis who were coming from other parts of the world”. This external funding enabled Islamist factions to systematically displace secular Free Syria Army (FSA) leaders, culminating in the rise of IS. In other words, the CIA-backed rebels targeted by Russia are not moderates.

They represent the same melting pot of al-Qaeda affiliated networks that spawned the Islamic State in the first place. And they rose to power in Syria not in spite, but because of the US rubber-stamping the jihadist funnel through the so-called “vetting” process. This summer, for instance, al-Qaeda led rebels received accelerated weapons shipments in a US-backed operation to retake Idlib province from Assad. Notice here that the US priority was to rollback Assad’s forces from Idlib – not fight IS. Yet the brave Western press, so outspoken on Russian duplicity, somehow overlooked how this anti-ISIS coalition operation failed to target a single IS fighter.

At least and at last one bit of good news.

• Gene Patents Probably Dead Worldwide Following Australian Court Decision (ArsT)

Australia’s highest court has ruled unanimously that a version of a gene that is linked to an increased risk for breast cancer cannot be patented. The case was brought by 69-year-old pensioner from Queensland, Yvonne D’Arcy, who had taken the US company Myriad Genetics to court over its patent for mutations in the BRCA1 gene that increase the probability of breast and ovarian cancer developing, as The Sydney Morning Herald reports. Although she lost twice in the lower courts, the High Court of Australia allowed her appeal, ruling that a gene was not a “patentable invention.” The court based its reasoning on the fact that, although an isolated gene such as BRCA1 was “a product of human action, it was the existence of the information stored in the relevant sequences that was an essential element of the invention as claimed.”

Since the information stored in the DNA as a sequence of nucleotides was a product of nature, it did not require human action to bring it into existence, and therefore could not be patented. Although that seems a sensible ruling, the pharmaceutical and biotechnology industry has been fighting against this self-evident logic for years. The view that genes could be patented suffered a major defeat in 2013, when the US Supreme Court struck down Myriad Genetics’ patents on the genes BRCA1 and the similar BRCA2. The industry was hoping that a win in Australia could keep alive the idea that genes could be owned by a company in the form of a patent monopoly. The victory by D’Arcy now makes it highly likely that other judges around the world will take the view that genes cannot be patented.

This is a result that will have major practical consequences, and is likely to save thousands of lives. In the past, holders of gene patents were able to stop other companies from offering tests based on them, for example to detect the presence of the BRCA1 and BRCA2 genes that were linked with a greater risk of breast and ovarian cancers. This patent monopoly allowed companies like Myriad to charge $3,000 (£2,000) or more for their own tests, potentially placing them out of the reach of those unable to afford this cost, some of whom might then go on to develop cancer because they were not aware of their higher susceptibility, and thus unable to take action to minimise their risks.

The shameless EUs reponse to tragedy: lock ’em up.

• EU Gets Ready To Lock Up, Deport Migrants (CNBC)

European authorities have relocated its first group of migrants that have flocked to Europe as part of a bloc-wide plan to share the weight of the growing refugee crisis. However, those who fail to gain asylum may not be so lucky. A group of Eritrean refugees prepare to board a plane to travel to Sweden as part of a new programme of the European Union to relocate refugees at the Ciampino airport of Rome. Italy Friday sent 19 Eritrean men and women to Sweden as part of the first batch of migrants taking part in the relocation program. This, albeit small, start is part of the commitment made by EU member countries last month to relocate 160,000 asylum seekers throughout Europe over the next two years.

The agreement was reached in order to help alleviate pressure on countries like Italy and Greece, where over 470,000 migrants have landed since January alone, according to EU border agency Frontex. At the same time, however, Italy was deporting 28 Tunisians and 35 Egyptians back home. A press release by justice and interior ministers from across the EU Thursday revealed plans to ramp up deportations and prepare dedicated detention centers that would lock up migrants as a “last resort.” “When we talk about refugees, we need to also talk of those who are not refugees,” Dimitris Avramopoulos, European Commissioner for Migration, Home Affairs and Citizenship, said in a statement. “We need to be better and more effective, not just at helping people and offering refuge, but also at returning those who have no right to stay.”

“All of these actions have to go together,” he said. An expanded return program would see more migrants who fail to gain asylum status deported to their home countries. Ministers believe the move will deter migrants who lack legitimate asylum claims from making the journey to Europe, the statement explains. The €3.1 billion Asylum, Migration and Integration Fund will help finance the return program, along with the €800 million set aside for deportations by member states for the six years between 2014 and 2020. But EU countries should also be prepared to lock up migrants temporarily until they can safely return home , the statement adds.. “All measures must be taken to ensure irregular migrants’ effective return, including use of detention as a legitimate measure of last resort,” the press release stated.

“All of a sudden, with the kind of weather that you have in the Balkans, this can be a tragedy at any moment..” Not can be, is, and has been for a long time.

• Greek Islands See Surge In Refugee Arrivals (Kath.)

The number of refugees arriving on Greek islands has risen from 4,500 a day in late September to 7,000 over the past week, the International Organization for Migration (IOM) said Friday, as a toddler was found dead off the coast of Lesvos in the eastern Aegean. Speaking ahead of a visit to Lesvos Saturday and a meeting with Prime Minister Alexis Tsirpas in Athens later in the week, UN High Commissioner for Refugees Antonio Guterres said asylum seekers appeared to be making a move before weather conditions deteriorate. “All of a sudden, with the kind of weather that you have in the Balkans, this can be a tragedy at any moment,” Guterres said. The IOM data came as a baby died after the motor of the rubber dinghy carrying him and another 56 people broke down off Levsos, the coast guard said Friday.

The 1-year-old boy, whose nationality was not reported, was found unconscious and taken to a hospital, where he was pronounced dead. Also Friday, sources said that a police officer who was photographed kicking a refugee in a temporary reception center on Lesvos had been identified. He is expected to be summoned to explain himself following an urgent investigation into the incident. Meanwhile, the UN refugee agency (UNHCR) welcomed the departure Friday of a first group of asylum seekers from Italy to Sweden under the EU’s relocation scheme and expressed hope that the Greek program will start soon. “We think it will be a slow start but will accelerate once the process functions,” UNHCR spokesperson Melissa Fleming said.

Running out of nameless graves.

• No Place Left To Die On Greece’s Lesbos For Refugees Lost At Sea (Reuters)

He stood on the mud, crows cawing overhead, pointing at unmarked graves. “Here’s a mother with her baby. And here’s another young woman. Over there, that’s a 60-year-old man.” Buried beneath low mounds of earth, facing Mecca, lay Afghan, Iraqi and Syrian refugees who drowned this summer in the Aegean Sea trying to reach Europe in flimsy inflatable boats. Scanning the area, Christos Mavrakidis, a somber, hardened man who looks after one of the main cemeteries on Greece’s Lesbos island, listed the years of other deaths: “2013, 2014, 2015.” Now there is no room left in the narrow plot of land in the pauper’s section of St. Panteleimon cemetery, close to where the colonnaded tombs of wealthy Greeks are built in the classical Greek style, and flowers adorn lavish marble graves.

“Something must be done,” he said. “They are a lot. They are too many.” No one can say where the next bodies will be buried. Nearly half a million people, mostly Syrians, Afghans and Iraqis fleeing war and persecution, have made the dangerous journey to Europe this year. Almost 3,000 have died, the U.N. refugee agency estimates. Just 4.4 km off the Turkish coast, Lesbos, Greece’s third-biggest island and popular with tourists, is one of the preferred entry points for migrants into the EU. Arrivals surged in late summer to sometimes thousands a day as people rushed to beat autumn storms that make the Aegean Sea even more treacherous. The number of burials at St. Panteleimon has also risen. More than three dozen migrants are buried in a tiny, dusty plot on a hill overlooking the island. Four were buried there last week alone.

Some of the makeshift, earthen graves bear a small marble plaque with a name in paint or marker: “Saad 4-9-2015.” Others state simply: “Unknown 25-8-2015”; “Unknown 28-8-2015”; “No 14 5-1-2013”. The most recent graves lack any marking. Mavrakidis placed his hand over his mouth and nose, the air filled with what he called “the stench of death” rising from the open grave of a young Iraqi man whose body was exhumed that morning after his family managed to trace him through DNA. Many more dead have never been found. Locals say fishermen sometimes dump bodies back into the sea, like fish they are not permitted to catch, to avoid having to hand them over to the authorities and face questioning and bureaucracy.

Home › Forums › Debt Rattle October 10 2015