Grete Stern Sueño No. 1: Artículos eléctricos para el hogar 1949

There is no escape. No matter what anyone says about recovery etc., the piper will come calling.

• Global Debt Crisis II Cometh (Goldcore)

• Global debt ‘area of weakness’ and could ‘induce financial panic’ – King warns

• Global debt to GDP now 40 per cent higher than it was a decade ago – BIS warns

• Global non-financial corporate debt grew by 15% to 96% of GDP in the past six years

• US mortgage rates hit highest level since May 2014

• US student loans near $1.4 trillion, 40% expected to default in next 5 years

• UK consumer debt hit £200b, highest level in 30 years, 25% of households behind on repayments

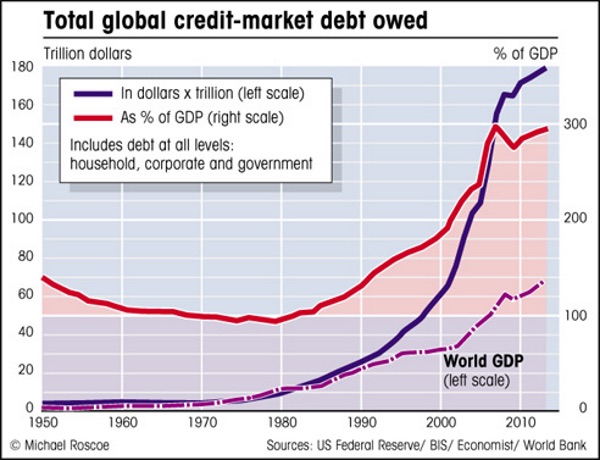

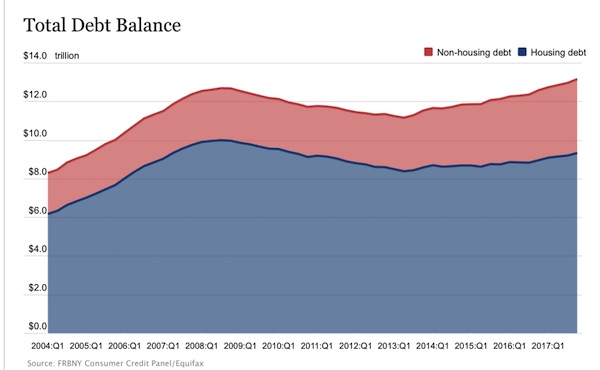

The ducks are beginning to line up for yet another global debt crisis. US mortgage rates are hinting at another crash, student debt crises loom in both the US and UK, consumer and corporate debt is at record levels and global debt to GDP ratio is higher than it was during the financial crisis. When you look at the figures you realise there is an air of inevitability of what is around the corner. If the last week has taught us anything, it is that markets are unprepared for the fallout that is destined to come after a decade of easy monetary policies. Global debt is more than three times the size of the global economy, the highest it has ever been. This is primarily made up of three groups: non financial corporates, governments and households. Each similarly indebted as one another.

Debt is something that has sadly run the world for a very long time, often without problems. But when that debt becomes excessive it is unmanageable. The terms change and repayments can no longer be met. This sends financial markets into a spiral. The house of cards is collapsing and suddenly it is revealed that life isn’t so hunky-day after all. Rates are set to rise and as they do they will spark more financial shocks, as we have seen this week. Mervyn King, former Governor of the Bank of England, gave warning about global debt levels earlier this week: “The areas of weakness in the current system are really focused on the amount of debt that exists, not just in the U.S. and U.K. but across the world,” he said on Bloomberg Radio last Wednesday. “Debt in the private sector relative to GDP is higher now than it was in 2007, and of course public debt is even higher still.”

When you see US debt is out of hand, don’t stop there. All global debt is.

• The % Puzzle Coming Together (Northman)

The US is drowning in debt and as long as rates are low it’s all fun and giggles, but there is a point where it cramps on growth and the simple question is when and where. In recent weeks we have had a nasty correction coinciding with technical overbought readings and both bonds and stocks testing 30 year old trend lines. In the meantime we continue to get data that keeps sending the same message: It’s a debt bonanza that keeps expanding and is unsustainable. Janet Yellen a few months ago said the debt to GDP ratio keeps her awake at night. Yesterday the Director of National Intelligence came out and described the national debt on an unsustainable path and a national security threat. This is literally where we are as a nation.

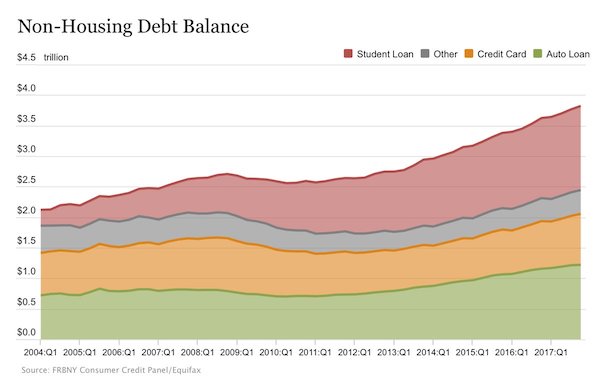

What’s Congress’s and the White House’s response? Spend more and blow up the deficit into the trillion+ range heading toward 2-3 trillion. What is there to say but stand in awe at the utter hubris that is being wrought. Last night the Fed came out with the latest household debt figures and it’s equally as damning, record debt and ever more required to keep consumer spending afloat:

The non-mortgage piece is particularly disturbing:

Higher interest rates will ultimately trigger the next recession as the entire debt construct will be weighted down by the burdens of cost of carry. And today’s inflation and correlated weakening retail sales data suggested that there’s price sensitivity already at these, historically speaking, still very low rates. The Fed may find itself horribly behind the curve and this will have consequences.

Makes a lot of sense. Therefore not going to happen.

• Trump Surprises Democrats, Supports 25 Cent Federal Gas Tax Hike (ZH)

President Trump surprised a group of lawmakers during a Wednesday meeting at the White House by repeatedly mentioning a 25-cent-per-gallon increase on federal gasoline and diesel tax in order to help pay for upgrading America’s crumbling infrastructure by addressing a serious shortfall in the Highway Trust Fund, which will become insolvent by 2021. The tax increase was first pitched by the U.S. Chamber of Commerce in January, while the White House had originally been lukewarm towards the idea. The federal gasoline and diesel tax has been at 18.4 and 24.4-cents-per-gallon respectively since 1993, with no adjustments for inflation. It currently generates approximately $35 billion per year, while the federal government spends around $50 billion annually on transportation projects.

Senator Tom Carper (D-DE), the top Democrat on the Senate Environment and Public Works Committee, seemed pleasantly surprised at Trump’s repeated mention of the tax as a solution to pay for upgrading American roads, bridges and other public works. “While there are a number of issues on which President Trump and I disagree, today, we agreed that things worth having are worth paying for,” Carper said in a statement. “The president even offered to help provide the leadership necessary so that we could do something that has proven difficult in the past.” Rep. Peter DeFazio (D-OR) – the top Democrat on the House Transportation and Infrastructure Committee was also present at the meeting, in which he says President Trump told lawmakers he would be willing to increase federal spending beyond the White House’s $200 billion, 10-year proposal. “The president made a living building things, and he realizes that to build things takes money, takes investment,” DeFazio said.

[..] Republican leaders have already rejected the idea, however, along with various other entities tied to billionaire industrialists Charles and David Koch. [..] Republican Senator Chuck Grassley (R-IA) doesn’t think the gas tax has any chance of even coming up for a vote in the Senate. “He’ll never get it by McConnell,” said Grassley, referring to Senate Majority Leader Mitch McConnell.

Bloomberg always has graphs for everything. But now that I would like to see how fast personal debt has grown in China, nada. Still, this is a whole new thing: Chinese never used to borrow, and now it’s the new national pastime.

• Household Debt Is China’s Latest Time Bomb (BBG)

For years, economists and policymakers have hailed the propensity of Chinese to save. Among other things, they’ve pointed to low household debt as reason not to fear a financial crash in the world’s second-biggest economy. Now, though, one of China’s greatest economic strengths is becoming a crucial weakness. Over the past two weeks, as they’ve held their annual work meetings, China’s various financial regulatory bodies have raised fears that Chinese households may be overleveraged. Banking regulators sound especially concerned, and understandably so: Data released Monday showed that Chinese households borrowed 910 billion renminbi ($143 billion) in January – nearly a third of all RMB-denominated bank loans extended that month.

While too much can be made of the headline number – lending is always disproportionately large in January, and bank loans are rising as regulators crack down on more shadowy forms of financing – the pace of growth for household debt is worrying. Between January and October last year, according to recent data from Southwestern University of Finance and Economics, Chinese household leverage rose more than eight percentage points, from 44.8% to 53.2% of GDP – a record increase. By contrast, between 2009 and 2015, households had added an average of just three percentage points to their debt-to-GDP ratio each year, and that includes a large jump of 5.5 percentage points in 2009 as banks ramped up lending in response to the global financial crisis. Before 2009, household debt levels had hovered around 18% of GDP for five years.

In other words, the debt burden for Chinese consumers has nearly tripled in the past decade. Part of that rapid debt expansion has been deliberate. China’s government has encouraged increased borrowing and spending on items like cars and houses, to boost both consumption and investment. At the G-20 summit in February 2016, China’s sober central bank chief Zhou Xiaochuan remarked that rising household leverage had “a certain logic to it.” Most worryingly, though, skyrocketing home prices seem to be driving much of the increase in household debt. Higher mortgage rates – and, especially, government policy – have compounded the problem. In order to slow rising prices, officials have raised down-payment requirements, pushed banks to slow mortgage lending and placed administrative restraints on purchases. That’s led buyers to borrow from different, often more expensive, channels.

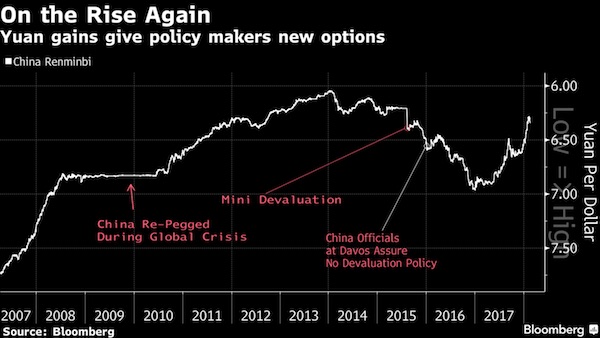

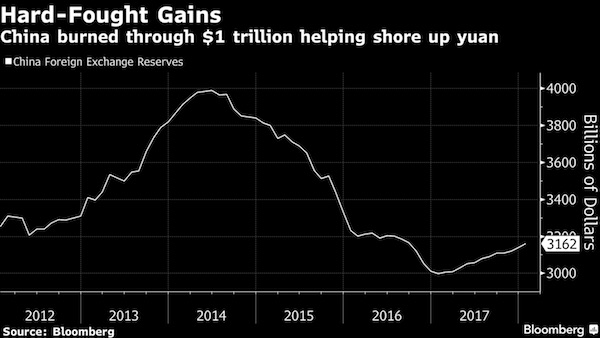

Beijing’s dilemma: allowing capital outflows (a no-no) would bring down the yuan (a yes please). Ergo: they can achieve what they want by allowing what they can’t afford to let happen.

• China’s Currency Policy May Be Facing a New Chapter (BBG)

In the fraught history of Chinese currency policy, a new chapter could be looming this year as authorities consider the consequences of a yuan that’s testing its strongest levels since mid-2015. After successfully shutting off potentially destabilizing capital outflows and putting a floor under the yuan, policy makers may now have the luxury of looking at relaxing some of the strictures on domestic money. But China watchers warn that any moves are likely to be gradual and calibrated, given the turmoil of 2015 – when a sliding yuan spooked global markets. “Big changes in the capital account are less likely, but some slight easing can be expected,” said Xia Le at Banco Bilbao Vizcaya Argentaria in Hong Kong. Policy makers have put a priority on deleveraging, “which is likely to cause instability,” he said – all the more reason to go cautiously on cross-border flows.

The yuan has strengthened 2.6% this year, after posting its first annual gain in four years in 2017. While no officials have clearly signaled an intent to relax controls, recent comments and moves hint at the potential for modification of the one-way capital account opening that China has been pursuing since 2016 – in which it has encouraged inflows but not outflows. The State Administration of Foreign Exchange, which oversees foreign-exchange reserves, said last week it sees more balanced capital flows. Pan Gongsheng, the director of SAFE, said last week that there will be a “neutral” policy in managing cross-border transactions. In a free trade zone in Shenzhen, near Hong Kong, officials have revived a program allowing for overseas investment that was suspended in 2015. Authorities in January removed a “counter-cyclical” factor from the daily fixing of the yuan, a move seen to let the market take more of a role.

Any return to the sustained appreciation the yuan saw over the decade to 2015 could hurt Chinese exporters’ profits – just as big companies face challenges from the leadership’s drive to reduce excess credit and cut back polluting industries. Yet the disorderly moves that followed 2015 efforts to promote international use of the yuan serve as a warning against any sudden lifting of barriers to capital outflows. “A degree of undershooting” in the dollar against the yuan “is probably necessary to provide reformists in China’s policy circle a window of opportunity to lobby for more capital account liberalization,” analysts led by David Bloom, global head of currency strategy at HSBC in London, wrote in a recent report.

Merkel should have stepped down. This can only end in chaos.

• Angela Merkel Pays a Steep Price to Stay in Power (BBG)

Angela Merkel once claimed she had bested Vladimir Putin during their first meeting in the Kremlin, employing what she said was an old KGB technique: staring at the Russian leader in silence for several long minutes. As the sun rose over a frigid Berlin on Feb. 7, the German chancellor’s rivals from the Social Democratic Party used the same tactic. This time, Merkel blinked. Merkel and her team had spent the previous day and night at the headquarters of her Christian Democratic Union locked in tense negotiations with the SPD leadership. The SPD had issued an ultimatum that broke with long-standing protocol of German coalition-building: Off the bat, they demanded three key posts, including the finance and foreign ministries, power centers from which the SPD planned to set the government’s agenda, especially on Europe.

An earlier attempt at an alliance with the Greens and the Free Democrats had failed. A second collapse in talks, more than four months after the September election, threatened to sweep out the governing elite, including the chancellor who has dominated German politics for 12 years. As delegates were summoned back to the CDU building, they could barely believe what Merkel and her party’s Bavarian sister group, the Christian Social Union, had negotiated. With so much at stake, she surrendered the portfolios for finance, foreign affairs, and labor to the Social Democrats (though the deal still needs to be approved by the SPD’s 464,000 members). CDU lawmaker Olav Gutting captured the mood with gallows humor. “Puuuh! At least we kept the Chancellery!” he tweeted Wednesday. On Sunday, Merkel took to the airwaves to explain her position. “It was a painful decision,” she told the ZDF television network. “But what was the alternative?”

The New York Times making the case for Trump’s border wall?

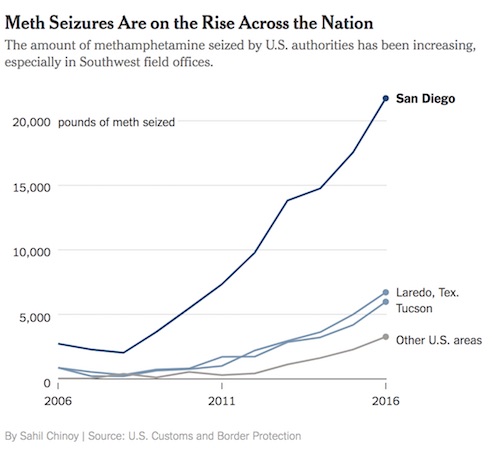

• Meth, the Forgotten Killer, Is Back in America. And It’s Everywhere. (NYT)

The scourge of crystal meth, with its exploding labs and ruinous effect on teeth and skin, has been all but forgotten amid national concern over the opioid crisis. But 12 years after Congress took aggressive action to curtail it, meth has returned with a vengeance. Here in Oregon, meth-related deaths vastly outnumber those from heroin. At the United States border, agents are seizing 10 to 20 times the amounts they did a decade ago. Methamphetamine, experts say, has never been purer, cheaper or more lethal. Oregon took a hard line against meth in 2006, when it began requiring a doctor’s prescription to buy the nasal decongestant used to make it. “It was like someone turned off a switch,” said J.R. Ujifusa, a senior prosecutor in Multnomah County, which includes Portland. “But where there is a void,” he added, “someone fills it.”

The decades-long effort to fight methamphetamine is a tale with two takeaways. One: The number of domestic meth labs has declined precipitously, and along with it the number of children harmed and police officers sickened by exposure to dangerous chemicals. But also, two: There is more meth on the streets today, more people are using it, and more of them are dying. [..] In the early 2000s, meth made from pseudoephedrine, the decongestant in drugstore products like Sudafed, poured out of domestic labs like those in the early seasons of the hit television show “Breaking Bad.” Narcotics squads became glorified hazmat teams, spending entire shifts on cleanup. In 2004, the Portland police responded to 114 meth houses. “We rolled from meth lab to meth lab,” said Sgt. Jan M. Kubic of the county sheriff’s office. “Patrol would roll up on a domestic violence call, and there’d be a lab in the kitchen. Everything would come to a screeching halt.”

[..] But meth, it turns out, was only on hiatus. When the ingredients became difficult to come by in the United States, Mexican drug cartels stepped in. Now fighting meth often means seizing large quantities of ready-made product in highway stops. The cartels have inundated the market with so much pure, low-cost meth that dealers have more of it than they know what to do with. Under pressure from traffickers to unload large quantities, law enforcement officials say, dealers are even offering meth to customers on credit. In Portland, the drug has made inroads in black neighborhoods, something experienced narcotics investigators say was unheard-of five years ago.

Will they sponsor this in Greek cities too?

• German Cities To Trial Free Public Transport To Cut Pollution (G.)

“Car nation” Germany has surprised neighbours with a radical proposal to reduce road traffic by making public transport free, as Berlin scrambles to meet EU air pollution targets and avoid big fines. The move comes just over two years after Volkswagen’s devastating “dieselgate” emissions cheating scandal unleashed a wave of anger at the auto industry, a keystone of German prosperity. “We are considering public transport free of charge in order to reduce the number of private cars,” three ministers including the environment minister, Barbara Hendricks, wrote to EU environment commissioner Karmenu Vella in the letter seen by AFP Tuesday. “Effectively fighting air pollution without any further unnecessary delays is of the highest priority for Germany,” the ministers added.

The proposal will be tested by “the end of this year at the latest” in five cities across western Germany, including former capital Bonn and industrial cities Essen and Mannheim. The move is a radical one for the normally staid world of German politics – especially as Chancellor Angela Merkel is presently only governing in a caretaker capacity, as Berlin waits for the centre-left Social Democratic party (SPD) to confirm a hard-fought coalition deal. On top of ticketless travel, other steps proposed Tuesday include further restrictions on emissions from vehicle fleets like buses and taxis, low-emissions zones or support for car-sharing schemes. Action is needed soon, as Germany and eight fellow EU members including Spain, France and Italy sailed past a 30 January deadline to meet EU limits on nitrogen dioxide and fine particles.

Never sell your basic needs to foreigners.

• Who Keeps Britain’s Trains Running? Europe (NYT)

The privatization of public services “was one of the central means of reversing the corrosive and corrupting effects of socialism,” Margaret Thatcher wrote in her memoirs. “Just as nationalisation was at the heart of the collectivist programme by which Labour governments sought to remodel British society, so privatisation is at the centre of any programme of reclaiming territory for freedom.” Those sentiments fueled a sell-off that put nearly every state-owned service or property in Britain on the auction block in the final decade of the 20th century, eventually including the country’s expansive public transportation infrastructure. Enshrined by parliamentary acts under Mrs. Thatcher and implemented by her two immediate successors, John Major, a Conservative, and Tony Blair of New Labour, the gospel of privatization was embraced by leaders around the world, notably including Mrs. Thatcher’s closest overseas ally, President Ronald Reagan.

In the realm of transportation, that gospel was soon betrayed by its own chief disciples. Put simply, there were few private-sector buyers with the expertise and deep pockets necessary to maintain control of a transit system that serves approximately seven billion passengers per year. With minimal transparency, operational ownership of the network of train and bus lines that crisscross the 607-square-mile sprawl of Greater London, linking it to the far-flung corners of Britain, was peddled in bits and pieces by the British state or acquired in corporate takeovers. But the new bosses were not private, business-savvy British firms. By 2000, the masters of British public transit — thanks to a scheme that was intended to replace state waste and sloth with soundly capitalist business principles — were foreign governments, most of them members of the European Union.

In short, the privatization devolved into a de facto re-nationalization — but under the direction of foreign states — that somehow went largely unnoticed. It now poses a startling and unprecedented dilemma thanks to Brexit, which will soon divorce Britain from the state bureaucracies beyond the English Channel that literally keep its economy in motion. The largest single stakeholder and operator in British transit is the Federal Republic of Germany [..] Germany is followed closely in the ranks of British transit bosses by France, proprietor of the London United bus system, among many other holdings. Its iconic red double-deckers openly announce themselves as the property of the RATP Group (Régie Autonome des Transports Parisiens), the state-owned Paris transport company, and are emblazoned with its logo of a zigzagging River Seine flowing through an abstract representation of the French capital.

As EU growth is at 10-year highs, boomers keep it all to themselves.

• Europe’s Poverty Time Bomb (PS)

The poor don’t often decide elections in the advanced world, and yet they are being wooed heavily in Italy’s current electoral campaign. Former Prime Minister Silvio Berlusconi, the leader of Forza Italia, has proposed a “dignity income,” while Beppe Grillo, the comedian and shadow leader of the Five Star Movement, has likewise called for a “citizenship income.” Both of these proposals – which would entail generous monthly payments to the disadvantaged – are questionable in terms of their design. But they do at least shed light on the rapidly worsening problem of widespread poverty across Europe. Poverty represents an extreme form of income polarization, but it is not the same thing as inequality. Even in a deeply unequal society, those who have less do not necessarily lack the means to live a decent and fulfilling life.

But those who live in poverty do, because they suffer from complete social exclusion, if not outright homelessness. Even in advanced economies, the poor often lack access to the financial system, struggle to pay for food or utilities, and die prematurely. Of course, not all of the poor live so miserably. But many do, and in Italy their electoral weight has become undeniable. Almost five million Italians, or roughly 8% of the population, struggle to afford basic goods and services. And in just a decade, this cohort has almost tripled in size, becoming particularly concentrated in the country’s south. At the same time, another 6% live in relative poverty, meaning they do not have enough disposable income to benefit from the country’s average standard of living.

The situation is equally worrisome at a continental level. In the EU in 2016, 117.5 million people, or roughly one-fourth of the population, were at risk of falling into poverty or a state of social exclusion. Since 2008, Italy, Spain, and Greece have added almost six million people to that total, while in France and Germany the proportion of the population that is poor has remained stable, at around 20%. In the aftermath of the 2008 financial crisis, the probability of falling into poverty increased overall, but particularly for the young, owing to cuts in non-pension social benefits and a tendency in European labor markets to preserve insiders’ jobs. From 2007 to 2015, the proportion of Europeans aged 18-29 at risk of falling into poverty increased from 19% to 24%; for those 65 and older, it fell from 19% to 14%.

“..Greece is no match for Turkey’s might. It would be like a “fly picking a fight with a giant..” What will the world do when the fighting starts? It could at any moment now.

• Erdogan’s Chief Advisor: US Has Plan To Make Greece Attack Turkey (K.)

The chief advisor to Turkish President Recep Tayyip Erdogan has told Turkey’s TRT channel that he is “in no doubt” that the US has a plan to make Greece attack Turkey while its military is engaged in Syria. Turkey’s response, Yigit Bulut said, will be tough, adding that Greece is no match for Turkey’s might. It would be like a “fly picking a fight with a giant,” he said and warned that terrible consequences would follow for Greece. Bulut made similar comments earlier in the month referring to Imia over which Greece and Turkey came close to war in 1996. “We will break the arms and legs of any officers, of the prime minister or of any minister who dares to step onto Imia in the Aegean,” Bulut said.

It may take Putin to halt Erdogan. But he will expect a reward for that.

• Greece Looks at USA to Calm Down Turkey (GR)

Greece is expecting the US administration to intervene and de-escalate the crisis with Turkey over the Imia islets, according to diplomatic sources in Athens. The Greek government is hoping that US Secretary of State Rex Tillerson, who is currently in Ankara for an official visit, will persuade the Turkish leadership to tone down its actions in the Aegean. The US Ambassador to Greece Geoffrey R. Pyatt will also be in Ankara and will brief Tillerson about recent developments. On Monday night, a Turkish patrol boat rammed into a Greek coast guard vessel near Imia, in the most serious incident between the two NATO allies in recent years. The two countries went almost to war in 1996 over sovereignty of Imia islets (Kardak in Turkish).

A confrontation was avoided then largely due to the intervention of Washington. The Department of State issued a statement on Tuesday stressing that Greece and Turkey should take measures to reduce the tension in the region. On Wednesday, Greek defense minister Panos Kammenos briefed Greece’s NATO allies on the incident at Imia and presented audiovisual material that prove Turkey’s provocation. “The Imia islets are Greek, the Greek Coast Guard and Navy are there and we will not back down on issues of national sovereignty for any reason. We ask our allies in the EU and NATO to adopt a clear stance,” he told AMNA. He also said that it was inconceivable that Turkey, a NATO ally, behaved like this toward another ally, in this case Greece.