Evelyn De Morgan Night and Sleep 1878

https://twitter.com/bennyjohnson/status/2057129253444202498?s=20 https://twitter.com/elonmusk/status/2057337929589039126?s=20

The SpaceX team is incredible! https://t.co/eqSByVrEW0

— Elon Musk (@elonmusk) May 21, 2026

Obama was a one-man Trojan Horse for radical Islam. He flooded America with Muslims by the millions in the dark of night and funded Iran’s efforts to build nuclear weapons. Let’s face the fact that every conspiracy theory about this traitor was true. https://t.co/3UeHPe0K6k

— James Woods (@RealJamesWoods) May 21, 2026

Are they imitating themselves, or Trump?

• Iranian President: Won’t Back Down (ZH)

Iranian President Masoud Pezeshkian has stated, “We will not bow our heads, our ministers and experts are working day and night, without a single day off.” He added, per state sources: “We are willing to sacrifice as much as possible for the honor and pride of Iran, and we are not afraid of martyrdom.” And just like that… Markets reversed earlier gains as Iran’s President said on state TV that they won’t back down in talks. The momentum then picked up when a “high-level source” told Al-Arabiya that the Pakistani Army Chief will not head to Tehran tonight.Read more …

The Pakistani were supposed to head to Iran only when the reach of an agreement was in sight, so this kind of denies the earlier reports of a US and Iran draft agreement. US stock indices erased more than half of earlier gains. We’ve seen the same reaction in oil, FX and bond markets but now they are consolidating. Still, Al Jazeera is reporting that “negotiators are very close to reaching a deal, and are currently working on a draft text. At the same time, another source told Al Jazeera that it is too early to judge whether a serious, final agreement is within reach.”IRNA has cited a Pakistani official who says the talks are “moving in the right direct” – though it’s anyone’s guess at this point. The prior reported draft did not take up the nuclear issue. Trump continues to press the nuclear issue. US President Donald Trump has again pledged to seize Iran’s stockpile of highly enriched uranium as part of any agreement over Tehran’s nuclear program.

“Look, we’re going to make sure they don’t have a nuclear weapon or we’re going to have to do something very drastic. I believe when it’s put to the people of our country, they will all agree we cannot let Iran get a nuclear weapon,” Trump told reporters at the White House. Asked whether Iran could retain its enriched uranium, Trump replied: “No, we will get it. We don’t need it, we don’t want it, we’ll probably destroy it after we get it. But we’re not going to let them have it.”

Russia’s the best we can do for him. If Trump agrees.

,The illusion of a grand diplomatic breakthrough in the Middle East is once again colliding with reality. The White House has been busy trying to paint a picture of a total capitulation by Tehran, which hasn’t been demonstrated given its consistent position defying Washington’s demands on the nuclear issue. According to two senior Iranian officials speaking to Reuters, Iranian Supreme Leader Mojtaba Khamenei has drawn a hard line in the sand, ordering that Iran’s stockpile of uranium enriched to 60% remain strictly inside Iranian territory.Read more …

Reuters underscores that “Ayatollah Mojtaba Khamenei’s order could further frustrate U.S. President Donald Trump and complicate talks on ending the U.S.-Israeli war on Iran.” “Israeli officials have told Reuters that Trump has assured Israel that Iran’s stockpile of highly enriched uranium, needed to make an atomic weapon, will be sent out of Iran and that any peace deal must include a clause on this,” the report continues.The officials noted that within Tehran, there is deep suspicion that the ceasefire is in fact “a tactical deception by the US,” designed to lull Iran into a “false sense of security… before the fighting resumes.”The fresh directive from from the supreme leader flies directly in the face of the narrative being spun by Washington and Tel Aviv, given Israeli officials maintain that President Trump explicitly promised Israel that Iran’s highly enriched stockpile would be completely removed from the country as part of any negotiated settlement. Trump has also recently proclaimed this publicly, for example in a phone interview with CBS News last month, wherein he confidently proclaimed that Iran “agreed to everything” and would cooperate fully to ship its enriched uranium out of the country.

Extraction of nuclear material would of course rely heavily on the assumption of total Iranian compliance, given Trump has also lately appeared to rule out out a hostile invasion force, stating, “No. No troops.” There seems to be widespread agreement among national security officials at this point that some kind of special forces op to covertly go in and take it would be tantamount to a ‘suicide mission’. According to more of what Trump (prematurely) proclaimed in the prior CBS interview: “Our people, together with the Iranians, are going to work together to go get it. And then we’ll take it to the United States.” The reality is all along the two sides’ positions have been very far apart, and largely unbending:

And on a potential deal: “We’ll be getting it together because by that time, we’ll have an agreement and there’s no need for fighting when there’s an agreement. Nice right? That’s better. We would have done it the other way if we had to” – he sought to explain. At the moment, Iranian officials are reportedly reviewing the latest updated US proposals for peace, having reportedly asked Pakistan for time to assess and study the American points for negotiations.”

I don’t quite get it. The date on that is May 1. What gives?

• Trump Posts Article Laying Out How To Crush Tehran In Three Moves (ZH)

President Trump on Thursday posted to Truth Social a New York Post article which was first published over two weeks ago, on May 1st, with the headline “Here’s how to crush Tehran in three moves.” Trump’s new social media post, issued without additional comment, comes just after news of Iranian Supreme Leader Mojtaba Khamenei having drawn a hard line in the sand, ordering that Iran’s stockpile of uranium enriched to 60% remain strictly inside Iranian territory. So now the world awaits what’s next at a moment the White House has renewed threats of massive military strikes if Iran doesn’t quickly come to the table and conform.Read more …

The NY Post article had straight-faced and without a hint of intended irony proclaimed: “President Trump has the upper hand.” That statement was issued on day 63 of Trump’s Iran war. Today is day 83. What did the interim look like as the world’s most powerful military force has been unable to reopen the Strait of Hormuz, amid constant threats to take new, bigger military action – but which never actually materializes (at least not yet) no matter how many times the Iranians reject Washington’s terms?

The below timeline and outline, stretching from last week into this one, basically illustrates the weekly Trump pattern that’s been on display going back many weeks at this point:

Wed: Iran wants a deal. They called us

Thu: We are looking at proposals

Fri: We might be close. Very close

Sat: Iran knows what to do

Sun: OBLITERATION. TOTAL. COMPLETE. They have 24 hrs.

Mon: The storm is coming

Tue: I’m giving it more timeThis is what ‘winning’ looks like according to the NY Post, apparently. The publication also feels itself in a position to give ‘advice’ and guidance to the White House on executing a war. “His best path forward is to pursue three lines of effort in parallel,” author Richard Goldberg (of Foundation for Defense of Democracies) wrote. It must be remembered that very recently a former senior official from FDD Action, the think tank’s lobbying arm, joined Trump’s Iran negotiating team – his name is Nick Stewart.

Here are the three:

• Sustain the blockade and accompanying economic warfare to destabilize the regime’s hold on the state;

• Remake the world in America’s energy dominance image to mitigate long-term price impacts while undermining China’s global ambition to defeat the United States;

• Order the US military to forge a path through the Strait of Hormuz to restore freedom of navigation on our terms not Tehran’s.

…if only simply ordering a military “path through” was that easy!“You might call the latter Operation Epic Passage — a combined naval and air mission of self-defense that offers escort to tankers and restores freedom of navigation, all while making clear to Tehran the devastating consequences of breaking cease-fire,” Goldberg, who openly boasts of his close ties to the Israeli government, also wrote. He further offered the mission name of “Blockade Plus”. After the opening days and weeks of Operation Epic Fury, when it became clear that the large-scale US and Israeli bombardment would not produced regime change in Iran, pundits widely questioned whether the Trump White House actually had a plan, or long-term strategic vision for the military mission.

And now, after more than 80 days in, the public gets Trump posting a NY Post article by a hawkish FDD writer, which seems more focused merely on ways to mitigate the blowback and ‘make the best’ of a failed regime change operation, in the wake of the administration’s constantly evolving stated goals.

“..more than one billion Class B shares when and if the company establishes “a permanent human colony on Mars with at least one million inhabitants,”

How long do you think it will take to get one million people living on Mars? Will Musk live to see it?

• Elon Musk Wants a Trillion-Dollar Payday, but There’s One Little Catch (Green)

The world finally got a peek at SpaceX’s closely held financials, after Elon Musk’s closely held space launch company filed for its initial public offering on Wednesday — and the details made a bigger splash than one of the company’s Starships making an uncontrolled water landing. The first shocker is that Musk’s salary last year was just $54,000. That’s about the same as a new human resources assistant or an apprentice electrician. That’s the only small figure you’ll see in the rest of this column because after this, the zeros get added on in a hurry. You know what? Forget the tease, and let’s go straight to the biggest figure.Read more …

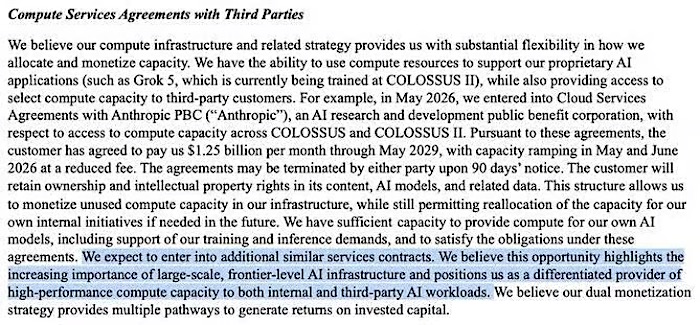

In SpaceX’s nearly 400-page S-1 filing with the U.S. Securities and Exchange Commission, the company projects a Total Addressable Market (TAM) of $28.5 trillion. That’s a two and an eight and a five followed by 11 zeros. TAM is business jargon for “What’s the size of our market if everybody who needed our product or service actually bought our product or service?” SpaceX’s TAM includes launch customers, Starlink users, and xAI (that’s the company’s AI division) compute services. It’s the company’s compute ambitions that account for the lion’s share of the TAM.Of the $28.5 trillion, “only about $2 trillion is directly related to space or the company’s Starlink network,” Ars Technica reported. “The remaining $26.5 trillion is believed to come from AI, largely from enterprise applications.” I had no idea how big xAI had already gotten until the Wall Street Journal revealed Wednesday night that “SpaceX is renting out compute capacity across its two large data centers to Anthropic, for some $1.25 billion a month.” And Anthropic is a rival. It’s no small feat when your competitor pays you nine figures, 12 times a year, for the privilege of using the same data centers you use for your LLM to run theirs. Nice work if you can get it, right?

“We believe we have identified the largest TAM in human history,” the company boasted in its S-1 report. “We believe our next trillion-dollar market is AI compute, which we contemplate will leverage our rockets and satellites for massive orbital deployment.” Putting computer centers in orbit solves the power problem with unlimited solar, and also clears a lot of regulatory hurdles. By hundreds of miles. The problem, of course, is getting all those birds flying. In January, SpaceX applied to the FAA for permission to launch one million satellites into Earth’s orbit to power xAI. One million satellites might be nothing more than a dream, but Starship — aka The Most Powerful Rocket in the World and Getting More Powerful All the Time — is key to realizing just a fraction of it.

The launch window for Starship Flight Test 12 opens at 6:30 p.m. Eastern today. So what’s this about Musk’s trillion-dollar payday? Musk’s salary might not be any bigger than a typical base-level IT support specialist’s, but he also has two yuge equity packages based on stellar performance. In March, SpaceX awarded Musk more than 300 million shares. But those shares only vest when and if the company completes construction of its “non-Earth-based data centers,” including 12 market cap goals that add $6.6 trillion in shareholder value. That’s more than triple the best current estimate of SpaceX’s worth. That’s not the big payout, however.

Musk will also earn more than one billion Class B shares when and if the company establishes “a permanent human colony on Mars with at least one million inhabitants,” and another series of market cap goals that increase the company’s worth by $7.5 trillion. With this IPO, Musk will almost certainly become the world’s first trillionaire. If he completes just one of the company’s two (admittedly ambitious) payouts, he’ll instantly become the first multitrillionaire.But let’s bring all this back down to Earth for a moment. Asa Fitch noted for the WSJ that “SpaceX made $18.7 billion of revenue last year. Getting to trillions will take quite a while, if it happens at all.”

That is an awfully big if. But if investors had to bet on anybody being able to do it — and they’ll finally get their chance with this IPO — it has to be the company’s $54,000 man.

Impressive wherever you look.

• SpaceX Files For Nasdaq IPO Under Symbol SPCX (ZH)

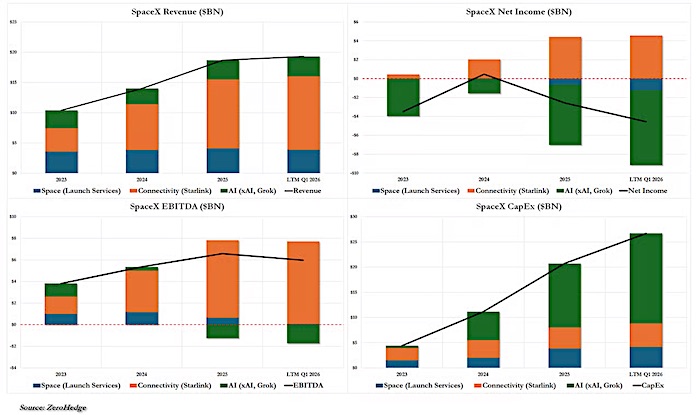

As expected, SpaceX filed its S1. The stock is expected to list on Nasdaq and Nasdaq Texas under the ticker “SPCX.” No specific share count, price range, or total offering size is finalized yet (placeholders are used). But, with expectations of a $1.5 trillion market cap, that means SPCX will trade at a 77x LTM Revenue multiple!

Mission and Overview SpaceX’s mission is to make life multiplanetary, advance scientific understanding of the universe, and extend consciousness to the stars. It positions itself as a vertically integrated builder across Space, Connectivity (Starlink), and AI (via xAI acquisition). The company has revolutionized space access with reusable rockets (Falcon family, Starship development), built the world’s largest LEO satellite constellation for broadband, and is scaling AI compute and frontier models (Grok) with real-time data from X.Key Corporate Details

Dual-class structure: Class A (1 vote/share) and Class B (10 votes/share). Elon Musk (founder, CEO, CTO, Chairman) will retain dominant voting control post-IPO (majority of the board via Class B and overall voting power), making SpaceX a “controlled company” under Nasdaq rules. Basis of presentation: Financials include retrospective recasts for the xAI acquisition (Feb 2026) and X Holdings (via xAI, 2025), plus a 5-for-1 stock split (May 2026). Underwriters: Led by Goldman Sachs, Morgan Stanley, BofA, Citigroup, J.P. Morgan, and others.Consolidated Financial Highlights (preliminary/selected):

Q1 2026: Revenue $4.69B, operating loss $1.94B, Adjusted EBITDA $1.13B. FY 2025: Revenue $18.67B, operating loss $2.59B, Adjusted EBITDA $6.58B. Heavy capex (especially AI) and Starship R&D; Starlink (Connectivity) is the current profit engine.Business Segments (as of/through Q1 2026 and FY 2025)

Space (launches, Dragon, Starship development): Dominant global launch provider (>80% of mass-to-orbit in recent years, >99% Falcon success rate). Key vehicles: Falcon 9 (reusable, ~23t to LEO), Falcon Heavy (~64t), Dragon (cargo/crew to ISS), Starship (in testing, targeting full reusability and massive scale).Revenue: $619M (Q1 2026), $4.1B (2025). Still investing heavily in R&D/Starship.Connectivity (Starlink):

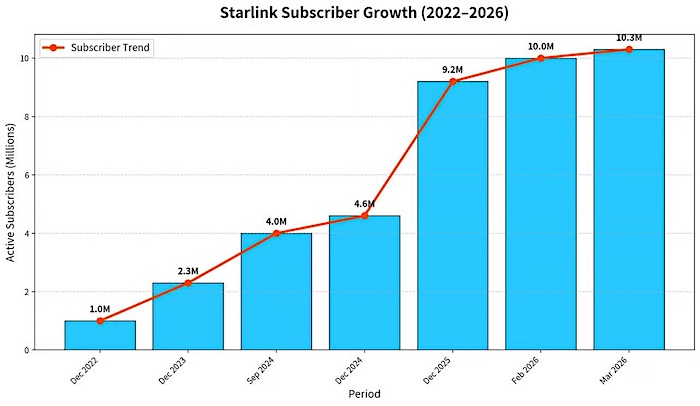

~9,600 broadband/mobile satellites in LEO (~10.3M subscribers across 164 countries/territories as of Mar 31, 2026). High-speed, low-latency broadband (median ~225 Mbps peak for residential); expanding enterprise, government, maritime/aviation, and satellite-to-mobile (direct-to-phone, ~650 dedicated satellites, ~7.4M devices in ~30 countries). Strong growth: Revenue $3.26B (Q1 2026), $11.4B (2025, +~50% YoY); highly profitable at segment level.AI (xAI/Grok/X integration):

Gigawatt-scale terrestrial AI training clusters (e.g., COLOSSUS); plans for orbital AI compute satellites (using solar power, starting ~2028).

Grok frontier models (truth-seeking, strong scientific reasoning benchmarks); integrated with X (~1.3B supported accounts, 550M MAUs, hundreds of millions of daily posts).

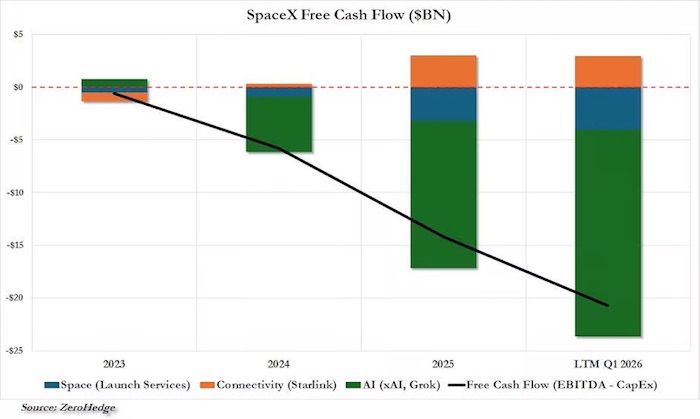

Revenue $818M (Q1 2026), $3.2B (2025), but heavy losses due to compute/infrastructure investments.Here’s the financials visualized (xAI is represented by the green slabs)…

Free cash flow struggling under the weight of that giant green slabs…

So, xAI is the giant money suck while Starlink keeps the engine running (but despite breaking out in 2025, Starlink user growth seems to be slowing a little):

Finally, one thing that stood out was that Anthropic is paying xAI $1.25BN per month (through May 2029) to utilize ‘Colossus’ for AI compute.

Musk took to X to explain further his vision for this segment:

“As the recently expanded partnership with Anthropic demonstrates, SpaceX is offering AI compute as a service at significant scale.

We are in discussions with other companies to do the same.

Over time, especially with orbital data centers, we expect to serve AI at extremely high scale.

If you build it (in space), they will come?

As a Democrat, perhaps, yes.

• Is This the Beginning of the End for John Fetterman? (Matt Margolis)

John Fetterman’s chief of staff, Cabelle St. John, resigned on Wednesday, according to a source who spoke to Axios. She had been with the Pennsylvania Democrat since he first arrived in Washington roughly three-and-a-half years ago and was elevated to chief of staff in 2025. Her official last day is still weeks away, but the writing was on the wall long before this week. This isn’t a one-off. Fetterman experienced a staff exodus in 2025, and the pattern of turnover is a sign that his rare independent streak is just too much for his party to tolerate. Former aides have cited frustration with his unwavering support for Israel, his noticeably warmer relationship with President Donald Trump, and what they describe as a difficult working environment on a personal level.Read more …

“This is a guy who came in talking about being a champion for labor and he’s gone pretty quiet on it,” the former aide said last year. “This is a guy who, since Trump won, is, for lack of a better word, basically a useful idiot for Republicans. He’s supporting stuff, and it gives them cover to say, ‘Look it’s bipartisan, we got Fetterman.'” None of this seems to bother Fetterman. After Axios published the story, he fired off a text to the outlet dismissing the whole thing. “So much for the turnover issue. Clicks!” he wrote, attaching an image claiming other Senate offices have higher turnover rates.It sounds like he’s not exactly losing sleep over it.In a recent appearance on Jesse Watters’ show, Fetterman cut to the heart of what separates him from the rest of his party. “Why can’t we just, you know, root for our military?” he said. “Why can’t we just say I don’t have to agree with everything the president has done or the kind of things that he says. But, you know, we should be on the side of America, and we should be on the side of civilization and the free world. And I’m on that side. And I don’t know why I’m the only Democrat that says those kinds of things at this point.”

And that’s the whole problem for his party, anyway. He’s asking a question that should have an obvious answer, and it doesn’t, because the modern Democratic Party instinctively opposes Trump on everything, including things that are just plain old stupid to oppose. They’re even whining about repairing the reflecting pool, for crying out loud.

The message from the left to Fetterman is: You’re not staying in your lane, and you have to be punished. Support the war in Iran? Support strong borders? Support Israel? Well, sorry, you’re way out of touch with the Democratic Party today. This isn’t a good sign for him. Sure, congressional staff experience turnover all the time, but how many Democratic staffers are going to want to join his staff to replace those who left? Working for Fetterman is likely to become a career-ender for those who want to work in Washington, and I can totally see Democrats using this as a means to pressure Fetterman into compliance.

The resignation of Fetterman’s chief of staff may be just the latest domino to fall, but the real question looming over Fetterman’s political future is whether this staff exodus marks the beginning of the end for a senator who refuses to play by his party’s rules. Democrats demand ideological conformity, and Fetterman’s rare independent streak will become a liability, making his office radioactive to potential staffers — staffers he needs to function.

We’ll see more about this. Funny it’s just a report, but everyone seems to call it an autopsy.

• The DNC 2024 Autopsy Is Here, and It’s a Disaster (Amy Curtis)

The DNC 2024 Autopsy Is Here, and It’s a Disaster. Last week, Kamala Harris was telling donors she wanted the DNC’s 2024 election report, probably better referred to as an autopsy, released. Now the report is coming out, and it’s bound to be a doozy. DNC Chair Ken Martin released a statement on the report, admitting it’s not up to his standards. And you’ll soon see why.Read more …

Read more about what I have to say here: https://t.co/9wochQttN5 pic.twitter.com/2REle6FPY3

— Ken Martin (@kenmartin73) May 21, 2026

Here’s what the statement says: “When I was elected DNC chair, I commissioned an after-action review of the 2024 election that I wanted to be honest and transparent, and with actionable and specific takeaways for the future of the Democratic Party. When I received the report late last year, it wasn’t ready for primetime — not even close — and because no source material was provided, it would have meant starting over. I could not in good faith put the DNC’s stamp of approval on the report that was produced.After last November’s massive Democratic wins, I didn’t want to create a distraction, but by not putting the report out, I ended up creating an even bigger distraction. For that, I sincerely apologize. For full transparency, I am releasing the report as we received it, in its entirety, unedited and unabridged. It does not meet my standards, and it won’t meet your standards, but I am doing this because people need to be able to trust the Democratic Party and trust our word.

There’s a lot to parse in this statement. The first takeaway is that the DNC is such a mess that they looked at this report and had no way of actually fixing it. This tells us their party is just as big a disaster as this report. Second, the ‘massive Democratic wins’ Martin touts have largely been a disaster. Spanberger got smacked down by both the Virginia state Supreme Court and the U.S. Supreme Court, Democrats are losing House seats across the country, and approval of Congressional Democrats is at a new all-time low.

Hey Democrats, put down the champagne. Here are your numbers: 70% of voters DISAPPROVE of the way Democrats are handling their job. Only 21% approve. Only 41% of Democrats approve. PITIFUL. All-time LOW.

— Larry Sabato (@LarrySabato) June 11, 2025Ouch.

Parts of the report are being summarized and shared online. The biggest takeaways are not surprises to those who paid attention. It turns out President Trump’s ‘they/them’ messaging was highly effective, Democrats neglected rural voters and local parties, and the Democrats failed to define themselves but relied on ‘not Trump’ messaging instead. We’re all aware that there was significant tension and backroom fighting between Kamala Harris’ campaign staff and the Biden administration. The autopsy shows the Biden team was criticized for not adequately preparing Kamala Harris.

DNC Chair Ken Martin released an incomplete 2024 election autopsy:

— Political Polls (@PpollingNumbers) May 21, 2026

• Trump’s “they/them” attacks on Harris were seen as highly effective

• Biden team criticized for failing to prepare Harris

• Democrats accused of neglecting rural voters and local parties

• Report says party… pic.twitter.com/MXkcPA28aoThere are also no mentions of Israel, Gaza, or Palestine.

Incredible. The DNC autopsy of 2024 is 192 pages.

— Prem Thakker (@prem_thakker) May 21, 2026

*Zero* mentions of the words "Israel," "Palestine," or "Gaza."

(DNC Chair Ken Martin concedes the autopsy does not meet his standards, nor would it meet yours). https://t.co/t1202zQlCs pic.twitter.com/sNjgotf0lmThis is sure to tick off both sides of the aisle. The Left’s anti-Israel, antisemitic base will say the Democrats’ position on Gaza was problematic, while other voters will see their increasingly antisemitic candidates and office holders as alarming.

What's going on here? In February, Axios reported that top party officials who worked on the autopsy of 2024 concluded that Kamala Harris lost significant support because of the Biden admin's approach to Gaza.

— Prem Thakker (@prem_thakker) May 21, 2026

But the newly-released autopsy…doesn't even mention Gaza or Israel? https://t.co/mj0A5Zz237

Law-bending.

• What Really Happened in Virginia’s Redistricting Case (Von Spakovsky)

“Shocking.” “Deflating.” “Sickening.” “It’s not good news.”Read more …

If someone heard the reactions of House Democratic lawmakers to the Virginia Supreme Court’s decision on the Commonwealth’s recent partisan gerrymandering scheme, they might be forgiven for assuming the ruling posed some kind of existential threat to the rule of law in the Commonwealth. In a letter to his party, House Minority Leader Hakeem Jeffries referred to the decision as “egregious” and “dripping with far-right partisanship,” the result of “MAGA extremists desperate to rig the midterm elections.”Chalk these wildly hyperbolic statements up as yet another reason to disbelieve left-wing partisan hype. In fact, Jeffries must have been looking in the mirror when he made those claims, since it was Virginia Democrats’ “egregious” misbehavior “dripping with far-left partisanship” that was the culmination of “Democratic extremists trying to rig the midterm elections” in the state.The Virginia Supreme Court’s decision in Scott v. McDougle was, in fact, a full-throated defense of the state’s constitution, the rule of law, and the people of Virginia’s right to make informed decisions on possible alterations to the Commonwealth’s constitution.

What was lost in the frenzied hysteria of Democrats and their allies in the media in the immediate aftermath of the decision was that the majority opinion, written by Justice D. Arthur Kelsey, simply upheld the process outlined in the Constitution that was required to adopt the proposed redistricting amendment. The Democrats’ hasty process violated Article XII, Section 1 of the Virginia Constitution. There was no partisanship in the opinion at all, with the exception perhaps of the dissent by three justices who refused to enforce the constitutional requirements.

Article XII requires the General Assembly to vote on any proposed amendment to the Constitution twice, with a general election of members to the House of Delegates occurring between the two votes. The court’s ruling centers on that (supposedly) intervening House election, held in 2025, not the recent vote on the amendment itself. The Virginia Supreme Court found that the 2025 House election did not actually occur after the first time and before the second time the General Assembly voted on the amendment.

Early voting (Virginia law allows voting to start 45 days before Election Day) for the House of Delegates elections began on September 19, but the General Assembly didn’t vote on the proposed amendment until October 31 in a “special” session that was itself open to challenge. Accordingly, 1.3 million votes, 40% of the election total, had already been cast when the legislature approved the referendum. That was 1.3 million people who had already voted who had no way of knowing their future representative’s position on an amendment to their Constitution.

The violation of Article XII, Section 1 here is obvious—to everyone but the Virginia government, now entirely controlled by Democrats, which argued that when the state constitution said the Assembly’s vote needed to occur before the election, it meant Election Day. Justice Kelsey’s opinion masterfully dissects this argument as lacking any meaningful support from law or history.

“So we believe in making America great again. You can’t do that unless you protect your borders. I’d encourage our friends in the UK to follow the same path.”

• Vance Urges UK Patriots To Defend Their Culture Against Starmer (MN)

US Vice President JD Vance has sent a direct message of support to Britons standing up for their culture, telling attendees of the Unite the Kingdom rally to push forward despite Keir Starmer’s attempts to silence opposition to mass migration. The rally, held this past weekend in London and organised by Tommy Robinson, saw thousands of patriots turn out waving British flags. Starmer’s government had tried to sabotage the event by blocking visas for 11 foreign speakers it labelled “far-right agitators.”Read more …

The Prime Minister openly boasted about the bans on X, writing “I’ll always champion peaceful protest. But the Unite the Kingdom march organisers are peddling hatred and division. We’ve already blocked visas for far-right agitators who want to come here to spew their extremist views. They don’t speak for the decent, fair, respectful Britain I know.” He followed up: “Today the voices of division will be loud. They don’t speak for the country I know, one that belongs to all of us.” A video from the event captured a striking contrast, showing a left-wing woman in tears hugging her masked companion in fright at the sight of the national flag.https://twitter.com/OliLondonTV/status/2056257812469018990?ref_src=twsrc%5Etfw%7Ctwcamp%5Etweetembed%7Ctwterm%5E2056257812469018990%7Ctwgr%5E5764f5a7abbc04d69e0037cffdd0fe954dcbc4e6%7Ctwcon%5Es1_c10&ref_url=https%3A%2F%2Fmodernity.news%2F2026%2F05%2F20%2Fwatch-vance-urges-uk-patriots-to-defend-their-culture-against-starmer-mass-migration-betrayal%2F

Vance rejected the establishment narrative that wanting secure borders equals extremism. “To everybody in the UK who rejects 3rd world migration, I’d encourage them to just KEEP ON GOING! It’s OK to want to defend your culture!” Vance stated. He added, “All over the West is this idea that the way to generate prosperity is to bring in MILLIONS and millions of unvetted people and DROP them into your neighborhoods — and we simply reject that idea!” “It’s OK to want to live in a safe neighborhood. It’s okay to want your job to go to yourself and your neighbors and not to a stranger who you don’t even know. It is reasonable for the people in Western societies to want to control who comes into their country and who doesn’t,” Vance stressed.

He added: “A lot of people, frankly, a lot of people in the media have tried to persuade all of those people that it’s somehow racist to want to protect your borders… even though very often the very people who are most affected by low wage immigration are lower income black and Hispanic Americans right here in the United States of America, and I guarantee that’s true in the UK.” Vance concluded by drawing a direct link to America First: “So we believe in making America great again. You can’t do that unless you protect your borders. I’d encourage our friends in the UK to follow the same path.”

This latest intervention builds on Vance’s repeated clashes with Starmer and European leaders. He previously called out the British Prime Minister to his face over the UK’s free speech crackdown. The US later vowed to use its “full arsenal of tools” against Starmer’s policies. Vance has also long warned about the dangers of Europe’s migration experiment, describing it as “civilisational suicide” He has cautioned that Islamist extremists could seize control of European nukes within 15 years. Vance has also triggered globalist outrage with his blunt speeches on replacement-level migration.

While Starmer brands patriotic pushback as “hatred and division,” ordinary Britons at the rally made clear they simply want what Vance described as basic common sense: safe streets, jobs for locals, and control over their borders. Vance’s words arrive as frustration with open borders boils over across the West. Working-class communities on both sides of the Atlantic are paying the price through suppressed wages, overburdened services, and rising insecurity — effects the political class routinely dismisses. By standing with those who reject cultural erasure, Vance is highlighting a fundamental truth: people of free nations have the sovereign right to preserve their identity and security.

“..If this modality in the behavior of Europeans changes in favor of dialogue, we will only welcome it..”

• ‘Russians Ready For Conversation’ With Europe — Kremlin (TASS)

Russia is hearing statements from European capitals that they will have to talk to Moscow, and it confirms its readiness for such a conversation, Kremlin Spokesman Dmitry Peskov said when asked by TASS about Europe’s discussions of candidates for the role of negotiator with Russia. “Indeed, in the last 3-4 weeks we have heard statements from Mr. [Finnish President Alexander] Stubb, and we have also heard statements from Berlin that sooner or later it will be necessary to talk to the Russians directly,” he said.Read more …“Russians are ready to engage,” Peskov noted. “We believe that talking is always better than leading to complete confrontation, which is exactly what the Europeans are doing now. If this modality in the behavior of Europeans changes in favor of dialogue, we will only welcome it,” he said. The very fact that expert discussions are underway in the EU around this topic is a good thing, Peskov said, adding that “just a few months ago, even such discussions weren’t taking place in Europe.”

According to Russian Foreign Ministry’s Ambassador-at-Large for the crimes of the Kiev regime Rodion Miroshnik, the European Union’s actions show a complete lack of willingness to follow a peaceful path

• Europe Seeks To Block Any Talks On Ukraine Settlement — Russian Diplomat (TASS)

European countries seek to sabotage any negotiations on a peaceful settlement of the Ukrainian conflict, Rodion Miroshnik, the Russian Foreign Ministry’s Ambassador-at-Large for the crimes of the Kiev regime, told TASS in an interview during a working visit to Bangkok.Read more …

“Judging by official statements from EU leaders and the so-called E3 group (the United Kingdom, Germany, and France – TASS), one can see an irreconcilable desire to derail any form of negotiations and reject a political and diplomatic path to resolving the conflict. They declare that they want talks, but at the same time they decide to issue yet another package of sanctions, allocate multi-billion-euro loans to Ukraine, and launch new programs to train Ukrainian troops and supply weapons. There is an old rule: look at what politicians do, not what they say. The European Union’s actions show a complete lack of willingness to follow a peaceful path,” he said.“I believe it is not enough to simply say it would be good to talk to Russia, this must be backed by actions that would prove that the EU is ready to stop financing the bloodshed in Ukraine. It is no secret that if Western funding stops, the war will end. This is acknowledged both in the West and by all external observers. But for now, Western countries continue to supply weapons and finance Ukraine,” Miroshnik added.

Foreign ministers of EU countries are set to discuss candidates for a possible mediator role in talks with Russia, the Financial Times newspaper previously reported. According to sources cited by the paper, the issue will be raised at an informal meeting on May 27-28 in Cyprus. Potential candidates reportedly include former Italian and German prime ministers Mario Draghi and Angela Merkel, Finnish President Alexander Stubb and his predecessor Sauli Niinisto.

On May 9, Russian President Vladimir Putin, answering journalists’ questions, said that former German Chancellor Gerhard Schroeder is the preferred candidate for possible negotiations between the EU and Russia. Moscow has never been closed to negotiations, he added.

“Drills Are Intended To Send A Signal”:

• Russia Holds Massive Nuclear Drills On Land, Sea And Air (ZH)

Trucks carrying intercontinental ballistic missiles rumbled over forest roads, atomic-powered submarines set sail from Arctic and Pacific ports, and crews scrambled into warplanes as Russia and neighboring Belarus held the final stage of their joint nuclear drills Thursday. Russian President Vladimir Putin discussed the maneuvers in a video call with his Belarusian counterpart Alexander Lukashenko. “The use of nuclear weapons is an extreme, exceptional measure for ensuring the national security of our states,” Putin said, according to AP. Lukashenko earlier inspected Russian short-range nuclear-capable Iskander ballistic missiles at a military unit involved in the drills and declared: “I dreamed about this machine a long time ago.”Read more …

The three-day drills that began Tuesday come amid a surge in Ukrainian drone strikes. including on Moscow’s suburbs that killed three people and damaged several buildings and industrial facilities. The strikes made it harder for officials in the Kremlin to cast the conflict in Ukraine — now in its fifth year — as something so distant that it doesn’t affect the daily routines of Russian civilians.Drills involve wide array of nuclear weapons

Russia’s Defense Ministry said the exercise involved 64,000 troops, over 200 missile launchers, more than 140 aircraft, 73 surface warships and 13 submarines, including eight armed with nuclear-tipped ICBMs. The drills focused on the “preparation and use of nuclear forces under the threat of aggression,” it said. The maneuvers also practice cooperation with Belarus, an ally that hosts Russian nuclear weapons. Russian arsenals in Belarus include its latest intermediate range nuclear-capable Oreshnik missile system.Along with nuclear-tipped ground- and submarine-launched ICBMs, the maneuvers featured a broad assortment of short- and medium-range weapons. Unlike the intercontinental missiles that can destroy entire cities, tactical nuclear weapons intended for use against troops on the battlefield are less powerful. They include aerial bombs and warheads for short- and medium-range missiles and artillery munitions. The Defense Ministry said the Russian armed forces test-fired Yars and Sineva ICBMs, as well as medium-range sea-launched Zircon and air-launched Kinzhal missiles, noting that all missiles hit their designated practice targets. Belarusian troops test-fired a short-range Iskander ballistic missile inside Russia.

Putin has repeatedly reminded the world about Moscow’s nuclear arsenals since the war in Ukraine started in February 2022 to deter the West from ramping up support for Kyiv. In 2024, the Kremlin adopted a revised nuclear doctrine, noting that any nation’s conventional attack on Russia that is supported by a nuclear power will be considered a joint attack on his country. That threat was clearly aimed at discouraging the West from allowing Ukraine to strike Russia with longer-range weapons and appears to significantly lower the threshold for the possible use of Moscow’s nuclear arsenal.

The revised doctrine also placed Belarus under the Russian nuclear umbrella. Putin has said that Moscow will retain control of its nuclear weapons deployed in Belarus, which borders Ukraine and NATO members Latvia, Lithuania and Poland, but would allow its ally to select the targets in case of conflict. The maneuvers are held amid an increase in drone activity in the Baltic nations. On Tuesday, a NATO jet shot down a Ukrainian drone over southern Estonia. Ukraine apologized for that “unintended incident,” without specifying what had happened.

On Wednesday, an emergency announcement about a drone flying over Belarus prompted residents of the Lithuanian capital of Vilnius, including top officials and lawmakers, to take shelter and led to a brief closure of its airport. Ukrainian drones targeting Russia’s Baltic ports and energy facilities have recently crossed or come down in NATO territory on several occasions. Amusingly, instead of blaming the source, Ukraine, Western officials blamed Russian electronic jamming of the drones.

Russia’s Foreign Intelligence Service said Tuesday that Ukraine is preparing drone attacks against Russia from the territory of the Baltic countries and warned of retaliation It alleged Ukrainian military personnel had been deployed to Latvia and warned that the country’s membership in NATO wouldn’t protect it from “just retribution.” Latvian authorities said the allegation was not true. Last month, the Russian Defense Ministry published a list of factories in Europe that it said were involved in producing drones and their components for Ukraine. It warned that attacks on Russia involving drones manufactured in Europe are fraught with “unpredictable consequences.”

Some commentators interpreted the bellicose statements from Moscow and this week’s exercise featuring short- and medium-range nuclear weapons capable of reaching targets in Europe as part of Kremlin efforts to discourage Western allies from bolstering support for Ukraine. Asked what message the nuclear exercise was intended to send, Kremlin spokesman Dmitry Peskov responded that “any drills are intended to send a signal,” but wouldn’t elaborate.

“Europe is the ‘jungle’ now. No garden left to speak of.”

• Irrelevant Europe (J.B. Shurk)

Josep Borrell is a Spanish socialist who held several high-ranking positions in the European Union. Until 2024, he was a vice-president of the European Commission and the high representative of the European Union for foreign affairs and security policy. In that capacity, he ran Europe’s External Action Service, which is the diplomatic body that executes Europe’s foreign policy decisions around the world. He remains a man with a great deal of influence over European perspectives.Read more …

In 2022, Borrell created a bit of an international incident when he described Europe as a “garden” and the rest of the world as a “jungle.” “We have built a garden,” he told aspiring European diplomats in Bruges, Belgium. “Most of the rest of the world is a jungle. The jungle could invade the garden. The gardeners should take care of it.” As the head of the European Defense Agency, Borrell’s comments made strategic sense. As he said in that same speech, “The jungle has a strong growth capacity…Walls will never be high enough to protect the garden. The gardeners have to go to the jungle, Europeans have to be much more engaged with the rest of the world. Otherwise, the rest of the world will invade us, by different ways and means.”Borrell’s speech came seven years after German Chancellor Angela Merkel’s decision to open her country’s borders to millions of Islamic immigrants. Originally touted as a humanitarian policy designed to temporarily shelter refugees from war-torn Syria, Germany’s generous welfare programs quickly became a magnet for young men across the Middle East and North Africa. When Merkel declared on August 31, 2015, “We can do this,” she initiated an all-of-society “welcome culture” that quickly produced a full-blown migrant crisis for the whole continent. Over ten years later, the influx of millions of Muslims into Europe has transformed school demographics and local politics, unleashed an explosion in sex crimes and anti-European violence, strained Europe’s hospital services and social safety nets, and exacerbated government debt.

Speaking after the “jungle” had already successfully invaded Europe’s “garden,” Borrell knew there was no way to put the genie back in the bottle. Merkel’s fateful decision to “welcome” Middle Easterners to Europe transformed cities and towns across Europe into the Middle East. Borrell also knew that the European Union’s patchwork defense agency did not have the requisite military and espionage assets to effectively protect the continent. So he tried to fashion his corps of young diplomats into a network of information and persuasion agents who could do Europe’s bidding around the world.

Borrell’s message got lost in the ensuing international kerfuffle over his “garden” / “jungle” division of the world. From Russia to Canada, Africa to Southeast Asia, every self-described “foreign policy expert” took umbrage at Borrell’s bluntness. Perpetually offended virtue-signalers hadn’t gotten so worked-up since President Trump had called Haiti a “shithole country” four years earlier. Just as Conan O’Brien felt compelled to white-knight for Haiti’s dystopian, cannibal gangland by visiting a heavily guarded resort in the Caribbean country and recklessly encouraging vacationers to join him, legions of politically correct snobs from around the planet recorded social media videos from their country estates in which they turned tsk-tsk-ing into a veritable lingua franca for the vicariously aggrieved.

All the “very best people” denounced Borrell for promoting a scarcely disguised restoration of European imperialism, colonialism, fascism, and genocide. Young international students enjoying university scholarships and living in Europe for free made sure to remind Borrell that “diversity is our strength.” Borrell’s socialist comrades beat him over the head with Europe’s prime directive: multiculturalism über alles. Mohammadbagher Forough, a random research fellow at the German Institute for Global and Area Studies, publicly reprimanded Europe’s foreign minister thusly: “This kind of comment puts a serious dent in the enterprise of European strategic autonomy. It upsets, at the most profound level, countries in the rest of the world, because of the history of colonialism.”

In other words, Europe’s “ruling class” and auxiliary straphangers condemned Borrell for daring to defend the beneficiaries of Western civilization. He was encouraged by threat of high-culture social banishment to follow Chancellor Merkel’s example in supplicating before the migrant hordes. The message was clear: Europe’s minister of defense cannot properly “defend” Europe unless he allows non-Europeans to take over the continent. It was further proof that Europe is irreparably lost.

Since his departure from the European Union’s foreign policy perch at the end of 2024, Borrell has spent most of his time in public lambasting President Trump’s global leadership. A staunch supporter of Ukraine who once threatened to “annihilate” the Russian army, Borrell has frequently defended the honor of Volodymyr Zelenskyy by claiming that Ukraine’s holdover president is leading “the resistance” and “deserves respect.” After President Trump described Zelenskyy as a “dictator without elections,” Borrell called the “accusation” the “height of dishonesty.” When President Trump and Vice President Vance took offense to Zelenskyy’s sense of entitlement and disregard for American taxpayers who have paid the salaries and pensions of Ukraine’s government workforce, Borrell screamed on X, “Trump and Vance have put on a disgraceful show. I am ashamed of that behavior.”

In response to Vance’s speech at the Munich Security Conference last year during which the vice president excoriated Europe’s crackdown on free speech and political dissent, Borrell lectured his erstwhile colleagues: “This is a declaration of political war against the European Union.” Going further, Europe’s former defense minister declared, “Europe must stop pretending that Trump is not an adversary and assert its technological, security, and political sovereignty with clarity and strength.”

https://twitter.com/elonmusk/status/2057261488256303134?s=20 https://twitter.com/GuntherEagleman/status/2057605618085548082?s=20The hydraulic pin holding the tower arm in place did not retract.

— Elon Musk (@elonmusk) May 21, 2026

If that can be fixed tonight, there will be another launch attempt tomorrow at 5:30 CT. https://t.co/DJAdvDYQpH

https://twitter.com/Rainmaker1973/status/2057327151964131432?s=20We once considered a Cholesterol Level of 350 perfectly normal & healthy.

— Valerie Anne Smith (@ValerieAnne1970) May 21, 2026

Then it was lowered to 300.

Then to 240.

Then to 190.

Now doctors want your levels as low as statins can force them — no matter what.

Every single time the “safe” number drops, millions more… pic.twitter.com/eqMDLuWKaB

Support the Automatic Earth in wartime with Paypal, Bitcoin and Patreon.