Brassaï La Bande du Grand Albert 1931-32

“The formation of another ‘technical’ government, under a former IMF apparatchik, is a fantastic gift to Mr Salvini.”

• President Mattarella Of Italy: From Moral Drift To Tactical Blunder (Varoufakis)

I concede that there are issues over which I would welcome the Italian President’s use of constitutional powers that (in my humble opinion) he should not have. One such issue is the outrageous policy of the Lega and the promise of its leader, Mr Salvini, to expel five hundred thousand migrants from Italy. Had President Mattarella refused Mr Salvini the post of Interior Minister, on the basis that he rejects such a monstrous project, I would be compelled to support him. But, no, Mr Mattarella had no such qualms. Not even for a moment did he consider vetoing the formation of a 5S-Lega government on the basis that there is no place in a European country for scenes involving security forces rounding up hundreds of thousands of people, caging them, and forcing them into trains, buses and ferries before expelling them goodness knows where.

No, Mr Mattarella vetoed the formation of a government backed by an absolute majority of lawmakers for another reason: His disapproval of the Finance Minister designate. And what was this disapproval based on? The fact that the said gentleman, while fully qualified for the job, and despite his declaration that he would abide by the EU’s eurozone rules, has in the past expressed doubts about the eurozone’s architecture and has favoured a plan of euro exit just in case it is needed. It was as if President Mattarella were to declare that reasonableness in a prospective Finance Minister constitutes grounds for his or her exclusion from the post!

Let’s face it: There is no thinking economist anywhere in the world who does not share a concern about the eurozone’s faulty architecture. And there is no prudent finance minister who does not have a plan for euro exit; indeed, I have itr on good authority that the German finance ministry, the ECB, every major bank and corporation have plans in place for the possible exit from the eurozone of Italy, even of Germany. Is Mr Mattarella telling us that only the Italian Finance Minister is not allowed to imagine having such a plan? Beyond his moral drift (as he condones Mr Salvini’s industrial-scale misanthropy while vetoing a legitimate concern about the eurozone’s capacity to let Italy breathe in its midst), President Mattarella has made a major tactical blunder.

In short, he fell right into Mr Salvini’s trap. The formation of another ‘technical’ government, under a former IMF apparatchik, is a fantastic gift to Mr Salvini. Mr Salvini is secretly salivating at the thought of another election – one that he will fight not as the misanthropic, divisive populist that he is but as the defender of democracy against the Deep Establishment. Already last night hescaled the high moral with the stirring words: “Italy is not a colony, we are not slaves of the Germans, the French, the spread or finance.”

More than half of Italy feel utterly betrayed by their own president.

• Italy President Vetoes Savona As Economy Minister, May Mean New Election (R.)

Italy’s president rejected Prime Minister-designate Giuseppe Conte’s pick for the economy ministry, a political source said on Sunday, a veto that may lead to another election this year.Conte, a little-known law professor with no political experience, took his list of ministers to President Sergio Mattarella, but the president rejected Conte’s candidate to the Economy Ministry, the 81-year-old eurosceptic economist Paolo Savona. Before Conte or Mattarella had finished their meeting, far-right League leader Matteo Salvini said that the only option now was to hold another election, probably later this year, without directly confirming the president’s veto.

“In a democracy, if we are still in democracy, there’s only one thing to do, let the Italians have their say,” Salvini said in a fiery speech to supporters in central Italy. Salvini and 5-Star leader Luigi Di Maio had met Mattarella informally on Sunday to try to find a solution. “The problem is Savona,” the coalition source said, explaining that the economist had not sufficiently softened some of his more eurosceptic positions. On Sunday, Savona tried to allay concerns about his views in his first public statement on the matter. Savona has been a vocal critic of the euro and the EU, but he has distinguished credentials, including as industry minister in the early 1990s. “I want a different Europe, stronger, but more equal,” Savona said in a statement.

Another technocrat. That won’t go well this time around.

• Italy’s President Calls In Former IMF Official Amid Political Turmoil (R.)

Italy’s president is expected to ask a former IMF official on Monday to head a stopgap government amidst political and constitutional turmoil, with early elections looking inevitable. President Sergio Mattarella has called in Carlo Cottarelli after two anti-establishment parties angrily abandoned their plans to form a coalition in the face of a veto from the head of state over their choice of economy minister. In a televised address, Mattarella said he had rejected the candidate, 81-year-old eurosceptic economist Paolo Savona, because he had threatened to pull Italy from the single currency. “The uncertainty over our position has alarmed investors and savers both in Italy and abroad,” he said, adding: “Membership of the euro is a fundamental choice. If we want to discuss it, then we should do so in a serious fashion.”

Financial markets tumbled last week on fears the coalition being discussed would unleash a spending splurge and dangerously ramp up Italy’s already huge debt, which is equivalent to more than 1.3 times the nation’s domestic output. After Mattarella’s move, the euro gained ground, adding 0.6% against the Japanese yen and ticking up against other major trading partners as well. The far-right League and anti-establishment 5-Star Movement, which had spent days drawing up a coalition pact aimed at ending a stalemate following an inconclusive March vote, responded with fury to Mattarella, accusing him of abusing his office.

5-Star leader Luigi Di Maio called on parliament to impeach the mild-mannered Mattarella, while League chief Matteo Salvini threatened mass protests unless snap elections were called. “If there’s not the OK of Berlin, Paris or Brussels, a government cannot be formed in Italy. It’s madness, and I ask the Italian people to stay close to us because I want to bring democracy back to this country,” Salvini told reporters. [..] Cottarelli would be a calming choice for the financial markets, but any technocratic administration would likely only be a short-term solution because the majority of parliamentarians have said they would not support such a government.

Portugal is supposed to be the Prince of the PIIGS.

• First Greece, Now Italy, Portugal Next? (ZH)

While most investors are focused on Italian politics – the parallel currency ‘mini-BoT’ fears and potential for a constitutional crisis – Spain is now facing its own political crisis amid calls for a no-confidence vote against Rajoy. However, ‘Spaxit’ remains a distant concern for investors as another member of the PIIGS peripheral problems is starting to signal concerns about ‘Portugone’?

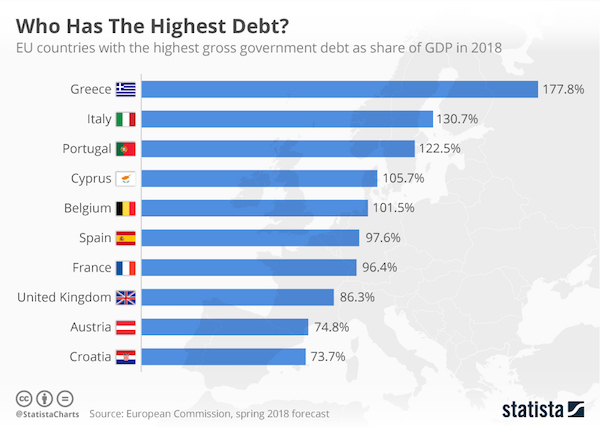

And the fundamental data confirms Portugal is next in line for a debt crisis… As Statista’s Brigitte van de Pas notes, on average, European Union countries had a gross government debt of roughly 81% of GDP in 2018. This average disguises real differences between EU countries. Whereas Greece had a government debt of 177.8% in 2018, Estonia had a debt of only 8.8% – the lowest in the entire EU zone.

While, the high Greek debt is well-known, a number of other countries however also have a debt that is higher than their own GDP. The Italian debt, for example, is lower than the Greek but still significant, at over 130% of GDP. Portugal, in third place, had a debt of 122.5%. One small positive note though: all three countries had even higher debts in 2017, and the European Commission forecasted a slow, but further decrease of their government debt in 2019. Whether this holds true for Italy, with their newly-elected government of Movimento 5 Stelle and Lega remains to be seen.

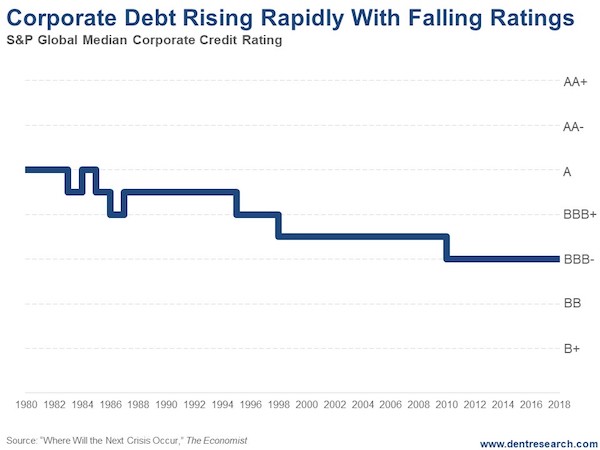

“U.S. corporate debt has risen from $40 trillion to $70 trillion since the top of the last bubble in 2007. That’s 63% in 10 years. It’s risen 135% since 2000! [..] China is the worst by far, going from $6 to $36 trillion or a 500% increase!”

• Corporate Debt Soars While Credit Ratings Fall (Harry Dent)

[First], Congress’s approving a bill to roll back the Dodd-Frank Act. If this passes, smaller financial institutions will find relief from the strict rules that have applied to Wall Street banks since after the 2008 crisis. This is sheer idiocy! It will not end well. The second is the U.S. corporate debt is suffering one of its worst sell-offs since 2000. This is another disaster in the making. U.S. corporate debt has risen from $40 trillion to $70 trillion since the top of the last bubble in 2007. That’s 63% in 10 years. It’s risen 135% since 2000! Only government debt has risen faster, from $35 to $64 trillion, or 83%. China is the worst by far, going from $6 to $36 trillion or a 500% increase! Of course, many of these bonds are simply financial engineering to buy back stock to increase earnings per share.

Uber-low long-term interest rates thanks to QE have allowed companies to do this cheaply. The problem is these long-term rates have been rising since just July 2016. They’ve gone from 1.38% to 3.10%. That’s an increase of 172 basis points in the risk-free 10-year Treasury bond. That naturally reverberates up through the risk spectrum from investment grade corporate bonds to junk bonds. You see, here’s the thing…Governments have artificially pushed down bond yields for so long that companies have embraced speculation rather than productive investment (i.e. they’re not spending money on productive assets that will serve them and the economy well in the long-term). This mentality only creates financial asset bubbles that burst.

When companies buy back their own shares at historically high valuations, they’re speculating, just like an investor or hedge fund. When stocks crash ahead, shareholders will demand to know why these corporations used the money they will need to survive the crisis to speculate in their own stock… at the highest prices in history! Well, as the numbers are now showing, this corporate bond bubble is starting to burst, and of course that will ultimately hit junk bonds the worst… then stocks and real estate. But the real story here is that we’ve been in this bond bubble since 1981. And the quality of this corporate debt has been falling for nearly 40 years now. QE has only accelerated the decline. We’re now at the point where the median corporate bond rating is borderline junk…

You don’t say…

• Fed Relies On Biased Data That Makes ‘B- Economy’ Look Like ‘A+’ – Bianco (CNBC)

A veteran market researcher is out with a warning — saying the Federal Reserve is relying too heavily on economic surveys skewed by social media to mold their policies. According to Bianco Research President James Bianco, most economists mistakenly believe that leading indicators are signaling an “A+” economy that can withstand rising interest rates. “It’s more like a B- economy,” he told CNBC’s “Trading Nation” on Friday. “It’s not this screaming home run that everybody thinks it is based on the survey data.” Bianco said social media is creating the bandwagon effect among survey respondents, a psychological phenomenon characterized by people following the herd.

“The advent of social media is allowing us basically to be inundated with financial news or economic news,” he said, adding the bulk of the news about the world’s largest economy has been largely favorable. “When somebody is asked ‘what do you think about the economy,” they are not answering ‘what do you think about the economy,’ Bianco said. “They are answering ‘What have you read about the economy?'” Bianco fears the Fed will make a policy error based on respondents’ answers. “Economists like at the Fed say ‘Wow, look at that data. It’s even better than we thought. We have to raise rates even faster,'” he said, adding that the tightening could derail the bull market. “The 10-Year [yield] could very well be at 3% by the end of next year with a 3% funds rate,” Bianco said. “[That’s when] you get an inverted yield curve.”

Nobo’s popular at home anymore. Except for Putin.

• Blowing Up the Iran Deal Brings Eurasia Closer to Integration (Pieraccini)

Washington finds itself increasingly isolated in its economic and military policies. Merkel’s visit to Russia reaffirms the desire to create an alternative axis to the one between Brussels and Washington. The victory in Italy of two parties strongly opposed to new wars and the annulment of the JCPOA, and especially the sanctions against Russia, serves to form a new alliance, accentuating internal divisions within Europe. Macron, Merkel and May are all grappling with a strong crisis of popularity at home, which does not aid them in their decision-making. Exactly the same problems affect MbS, Trump, and Netanyahu in their respective countries. These leaders find themselves adopting aggressive policies in order to alleviate internal problems.

They also struggle to find a common strategy, often displaying schizophrenic behavior that belies the fact that they are meant to be on the same side of the barricades in terms of the desired world order. In direct contrast, China, Russia, Iran, and now India, are trying to respond to Western madness in a rational, moderate, and mutually beneficial way. And as a result, Europeans may perhaps begin to understand that the future lies not in piggybacking on Israel, Saudi Arabia and the United States. Trump seems to have offered the perfect occasion for European leaders to assert their sovereignty and start to move away from their traditional servility shown towards Washington.

“This, as the saying goes, could be it.”

• Sudden Chaos In Spanish Politics (Spain Report)

PSOE leader Pedro Sánchez really wants to be Prime Minister. The Socialist Party has been mostly flat in the polls for months, slowly trending down from 23% at the beginning of the year to 19% in the Metroscopia poll in El País on May 13. Articles had recently appeared wondering if Mr. Sánchez had anything relevant to say at all. His only notable intervention of late had been a meeting with Mariano Rajoy at Moncloa, the Prime Minister’s office, to agree on a joint response to the challenge posed by Quim Torra, the new separatist First Minister of Catalonia, whom Mr. Sánchez then decided to frame as “Spain’s Le Pen”, “a racist and a supremacist”.

With the publication of the Gürtel fraud case judgement on Thursday, the Socialist Party, which holds 84 out of 350 seats in Congress, has seized on an opportunity to move back into the political spotlight and oust the Popular Party from power with a motion of no confidence. Mariano Rajoy, famously unresponsive as political scandals erupt and opponents die off, wants to stay on as Prime Minister, of course, but this is a serious crisis: El País has characterised it as a “national emergency”. It is such a big mess that the PM felt he had to cancel his trip to Kiev to watch Real Madrid in the Champions League final.

He gave an unscheduled press conference on Friday afternoon, accompanied by his ministers, and accused Mr. Sánchez of wanting to destabilise Spain and wreck the country’s economic recovery. Moncloa sent out an unsigned, unofficial, unstamped “economic report” on Saturday, warning that the socialist motion of no confidence would cost €5 billion and 6,500 jobs. PP spokesman Fernando Martínez Maíllo said Mr. Sánchez would become the “Judas of Spanish politics” if he did a deal with Catalan separatists to take power. The Popular Party and Mr. Rajoy himself—also sliding inexorably downwards in the polls—sense real danger in the PSOE’s move. This, as the saying goes, could be it.

“By early May this year, 4,409 people had reached Spain and 217 people had died in the attempt.”

• Spain Struggling To Deal With Escalating Migration Crisis (G.)

Spain’s maritime rescue service has rescued hundreds of people trying to cross the Mediterranean into Europe this weekend amid growing concerns that the country is struggling to cope with the migration crisis. The service said its crews had rescued 293 people from nine boats on Saturday. On Sunday, a further 250 migrants were rescued from eight boats, three of which were in poor condition and later sank, they added. The migrants were from various countries in North and sub-Saharan Africa. On a single day in August last year, Spanish rescuers saved 593 people from 15 small paddle boats – including 35 children and a baby – after they attempted to cross the seven-mile Strait of Gibraltar.

According to statistics from the International Organisation for Migration (IOM) 21,468 migrants and refugees arrived in Spain by sea in 2017, with 224 people dying on the journey. The arrival figures showed a threefold increase on 2016, when 6,046 people reached Spain and 128 people died en route. By early May this year, 4,409 people had reached Spain and 217 people had died in the attempt. The UN refugee agency, UNHCR, has already warned that Spain is facing “another very challenging year” when it comes to helping and protecting those arriving on its shores.

His case looks solid. But we’re talking the heart of these companies’ business models.

• Google, Facebook Hit With $8.8 Billion In Lawsuits on New EU Privacy Rules (ZH)

Accusing Facebook, Google, WhatsApp, and Instagram of “intentionally” violating Europe’s strict new privacy rules that officially went into effect on Friday, Austrian lawyer and privacy activist Max Schrems filed four lawsuits against the tech companies arguing they are still “coercing users into sharing personal data” despite rolling out new policies ostensibly aimed at complying with the new regulations.

Titled the General Data Protection Regulation (GDPR), the new rules require companies to explicitly and clearly request consent from users before mining their data, and Schrems argues in his complaints – which seek fines totaling $8.8 billion – that Google, Facebook, and the Facebook-owned Instagram and WhatsApp are still utilizing “forced consent” strategies to extract users’ data when “the law requires that users be given a free choice unless a consent is strictly necessary for provision of the service,” TechCrunch explains. “It’s simple: Anything strictly necessary for a service does not need consent boxes anymore. For everything else users must have a real choice to say ‘yes’ or ‘no,'” Schrems wrote in a statement.

“Facebook has even blocked accounts of users who have not given consent. In the end users only had the choice to delete the account or hit the ‘agree’-button—that’s not a free choice.” While Facebook—which is currently embroiled in international controversy following the Cambridge Analytica scandal—insists that its new policies are in compliance with Europe’s new regulatory framework, Schrems argues that Facebook and Google aren’t even attempting to follow the new law. “They totally know that it’s going to be a violation, they don’t even try to hide it,” Schrems told the Financial Times. Schrems believes that courts can curtail companies’ ability to poke around in our private lives and wean them off their idea that, “ ‘We’re Silicon Valley, we know what’s right for everybody else.’ ”

Strong lobby for this in Washington.

• US Congressman: F-35s Could Be ‘Used Against Greece’ If Sold To Turkey (K.)

The United States should freeze the sale of the Lockheed Martin F-35 fighter jets to Turkey because they are more likely to used against Greece than against terrorists, Democratic US Congressman Brad Sherman told US Secretary of State Mike Pompeo, during a Foreign Affairs Hearing on May 23. “I hope that the administration will oppose and prevent the sale of F-35s [to Turkey]. They are not a weapon to be used against terrorists. They are a weapon to be used against Greece,” he said.

A US Senate committee passed earlier this week a defense policy bill that includes a measure to prevent Turkey from purchasing the F-35s, citing the country’s detention of US citizen Andrew Brunson and its agreement with Russia to buy its weapons systems in December. Sherman also called on the State Department not to block a House resolution on genocidal campaigns committed by the Ottoman Empire. “I hope the State Department will at least be neutral should Congress consider, as we are considering, the remembrance of the millions of Armenian, Greek, Assyrian, Chaldean and Syriac victims of the Ottoman Empire at the beginning of the last century,” he added.

Fastest growing industry.

• Huge Rise In Food Redistribution To People In Need Across UK (G.)

The UK’s largest food redistribution charity is helping to feed a record 772,000 people a week – 60% more than the previous year – with food that would otherwise be , new figures reveal. One in eight people in the UK go hungry every day – with the most needy increasingly dependent on – yet perfectly good food is wasted every day through the food production supply chain. FareShare said it was now redistributing food that otherwise would have been wasted with an annual value of £28.7m, up from £22.4m last year. “Three years ago we were helping to feed 211,000 people a week – today it’s three-quarters of a million,” said FareShare’s chief executive, Lindsay Boswell. “We reported in 2015 that we provided food across 320 towns and cities – now it’s 15,000. It’s not rocket science to see there has been a massive hike in demand for food from frontline charities.”

FareShare currently redistributes about 13,500 tonnes of surplus food every year donated by supermarkets, wholesalers and suppliers to 9,653 charities including hospices, homeless shelters, care homes and women’s refuges, but its annual target is 100,000 tonnes. Demand for surplus food has soared against a background of growing dependence on food banks and rising in the UK. FareShare says it has the capacity – and a waiting list of charities wanting help – but needs access to more food. Its solution is a government fund that would cover the costs of storage and transport. Available to any charity or producer that incurs the costs of redistributing food, it would also save charities and other beneficiaries £150m by making free food available to them. A public petition supporting this move attracted more than 16,000 signatures, which guarantees a government response.

People will start leaving in droves sson.

• In Britain, Austerity Is Changing Everything (NYT)

For a nation with a storied history of public largess, the protracted campaign of budget cutting, started in 2010 by a government led by the Conservative Party, has delivered a monumental shift in British life. A wave of austerity has yielded a country that has grown accustomed to living with less, even as many measures of social well-being — crime rates, opioid addiction, infant mortality, childhood poverty and homelessness — point to a deteriorating quality of life. When Ms. Lewis and her husband bought their home a quarter-century ago, Prescot had a comforting village feel. Now, core government relief programs are being cut and public facilities eliminated, adding pressure to public services like police and fire departments, just as they, too, grapple with diminished funding.

By 2020, reductions already set in motion will produce cuts to British social welfare programs exceeding $36 billion a year compared with a decade earlier, or more than $900 annually for every working-age person in the country, according to a report from the Center for Regional Economic and Social Research at Sheffield Hallam University. In Liverpool, the losses will reach $1,200 a year per working-age person, the study says. “The government has created destitution,” says Barry Kushner, a Labour Party councilman in Liverpool and the cabinet member for children’s services. “Austerity has had nothing to do with economics. It was about getting out from under welfare. It’s about politics abandoning vulnerable people.”

They should do that for all Americans stationed abroad today. Bring the living ones home while they’re still alive.

• ‘We’re Gonna Keep Riding Till We Get Everybody Back Home, From All Wars’ (AFP)

Wearing bandanas, cowboy hats or gleaming helmets, tens of thousands of bikers descended on Washington Sunday to parade in honor of US soldiers missing in action in foreign wars, a now 30-year-old tradition known as “Rolling Thunder.” “We’re gonna keep riding until we get everybody back home, from all wars,” said Jack Richardson, who at 73 crossed the country from California for the 13th time to participate in the annual Memorial Day weekend spectacular. Dressed in a leather jacket emblazoned with patches, this Vietnam War veteran had assembled with thousands of other bikers in a parking lot near the Pentagon, awaiting the start of the parade.

The route will take them into the center of official Washington, past the monuments on the National Mall and the austere black marble memorial engraved with the names of the nearly 60,000 US soldiers killed during the Vietnam War. “Still there are families waiting back home here in the United States that have not found out where their dads, their fathers, their brothers – they don’t know where they are,” said Richardson, a retired Los Angeles police officer who served two tours in Vietnam in the 1960s. “They don’t know if they’re still in Vietnam, they don’t know if they’re still alive, they don’t know if they’re dead, they don’t know if they’re captured,” he said.

According to organizers, more than 85,000 US soldiers remain unaccounted for in conflicts as far back as World War I. Most are from World War II, but 1,598 of the missing are from the war in Vietnam, a conflict still fresh in the memories of older veterans. The parade was begun in 1988 with some 2,500 motorcycles under the motto “We will never forget” to press for an accounting of the Vietnam missing. It has grown every year since into a rumbling, roaring extravaganza that organizers say attracts over a million people, including spectators. Besides the missing, the bikers also come to remember their fallen comrades.