Herbert Mayer Honi soit qui mal y pense: Aug 1939

This is not the first time I’ve written on this topic, but I want to do it again, because rate hikes, when they come, will have a tremendous effect on everybody’s loves and economies, wherever you live. And because I think there’s still far too much complacency out there, far too much ‘conviction’ that higher rates will come only after a comfortable period of time, and even then only gradually.

There are three steps in the Fed’s ‘policies’. There’s QE, which will end in October. There’s ultra low interest rates, which have so far been maintained. And then there’s the dollar, whose rate many people still think is determined by the ‘markets’, even if the Fed is in effect the ‘markets’. When the Fed buys, or makes third parties buy, bonds and stocks (and we know it has), it’s not going to let the dollar roam free. That makes no sense.

Which means the rising dollar (about 10% vs the euro in mere weeks) is due to Fed actions. The Fed manipulates what it can. It’s the motivation behind its actions that catches people on the wrong foot. Most continue to have this idea that Janet Yellen, and Ben Bernanke before her, seek and sought their alleged dual mandate of full employment and price stability. Ironically, those are two things they have zero control over.

What they do instead, what motivates their actions, is seek to maximize Wall Street bank profits, and, in the same vein and same breath, hide these banks’ losses. Once you realize and acknowledge that, policies over the past 8 years – and before, cue Greenspan – make a lot more sense then when you try to see them through that alleged dual mandate view.

QE is all but done. This alone already has started a capital flight move away from emerging markets. Many of whom will soon look a whole lot less emerging because of it. The capital will continue to flow back to the global financial center from the periphery, leaving dozens of countries and companies scrambling to find dollars to pay off the loans that looked so cheap.

The rising dollar will only make that worse. And moreover, it will catch many other countries, for instance southern European ones, in the same dragnet the emerging economies were already in. If and when your currency loses 10%+ against the currency more commodities and debts are denominated in, and you have such debts and need such commodities, you stand to lose, in all likelihood, a lot.

That leaves interest rates. Given the recent Fed actions on QE and the dollar, why would it NOT raise rates? The dual mandate? To affect price stability in the US? With the dollar moving the way it has, that’s gone anyway. To help Americans get jobs? The only reason US jobless numbers are not much higher is A) millions left the job market altogether and B) millions who were once account managers are now burger flippers, WalMart greeters and self-employed.

The definitions were changed as we went along, that’s why, at least officially, unemployment is not at 15% or 20%. And that is al part of the same opaque truth, that nothing the Fed did since 2008 has mattered one bit when it comes to jobs for Americans. All it has effectively achieved is that trillions of dollars in Main Street money and future obligations were shifted to Wall Street.

The objectives of the Fed’s dual mandate have turned out to be a total joke when the chips came down. Not surprising, because they were always a joke to begin with. A central bank should not be involved in job creation, and it should not hand trillions of dollars to the banks that are its owners, to ostensibly keep prices stable in the real economy, where none of those trillions end up. It’s all just a joke, albeit a very costly one.

QE was never meant to benefit Main Street. Neither was the suppression of the dollar. Why then would the Federal Reserve NOT hike rates only to protect the real American economy? Nothing it has done so far has been aimed at that goal, so why start now? There’s no logic there.

The Fed will continue to do what it’s done all these years: enact those policies that promise to bring the greatest profits to the banks that own it. And right now, those profits are not in more bond buying, and not in artificially low rates, and not in an artificially low dollar. Simply because that’s what everybody else is betting on, and the money when that happens is on the opposite side of the bet.

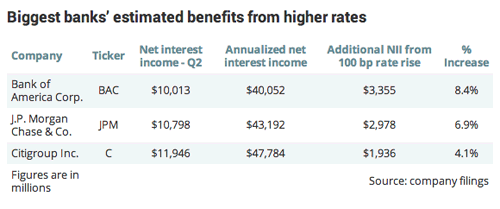

I cited this piece by Philip Van Doorn at MarketWatch 5 weeks ago, and it’s as relevant now as it was then:

Big US Banks Prepare To Make Even More Money

[..] … the debate at the Federal Reserve has now shifted to the timing of interest rate increases. Most economists expect the federal funds rate to begin climbing in the second half of 2015, but it could well happen sooner than that. For most banks, the extended period of low interest rates has become quite a drag on earnings. Net interest margins – the spread between the average yield on loans and investments and the average cost for deposits and borrowings – are still being squeezed, since banks realized the bulk of the benefit of very low interest rates years ago …

Once you you’ve metastasized that, and the truth about the dual mandate thing, and you’ve read the ‘Secret Goldman Tapes’ stories earlier this week, which showed in a blinding fashion how Goldman Sachs controls the Fed, not the other way around, then maybe your idea about those ‘soft slow’ rate hikes are due for a review as well.

Just look at what Dallas Fed head Richard Fisher had to say over the weekend:

Fisher Says Fed Must Weigh Wage Pressures in Setting Rate Policy

“I don’t want to fall behind the curve here,” Fisher said in a Fox News interview. “I think we could suddenly get a patch of high growth, see some wage-price inflation, and that is when you start to worry.” Fisher dissented on Sept. 17 at the last meeting of the Federal Open Market Committee, when the Fed retained a pledge to keep rates near zero for a “considerable time” after its asset purchases halt at the end of next month.

He called U.S. second-quarter growth “uber strong,” referring to the upward revision last week to an annualized rate of 4.6% from 4.2% previously estimated, and said history had shown that wage pressures could accelerate when unemployment got below current levels of 6.1%. In addition, Fisher said surveys of wage-price pressures in the Dallas Fed’s district, which includes Texas, northern Louisiana and southern New Mexico, were the highest since before the recession, and other indictors were also buoyant. “We’re going to be releasing some data on Monday and Tuesday, our new surveys, that I think will just knock your socks off,” he said.

I’d say Fisher is uber happy, and those data did come in as he predicted – though I think everyone wearing socks still has them on. Fisher wants that rate hike now, not next summer or fall. And he has a voice, even if he himself and fellow hawk Philly Fed head Charles Plosser are poised to step down some 6 months from now. I’m reading ‘experts’ who claim that will relieve the pressure on Yellen and her doves, but it’s the other way around: they’re going to make sure their – departing – voices will be heard one last time.

But of course down the line that’s all theater. The rate hike is a foregone conclusion. As is the mayhem it will give birth to. Prepare yourselves accordingly. And from now on always keep in the back of your mind what the Fed really is. It is not your friend. Unless you too own a piece.

• Why A Strong Dollar Is Scarier Than Taper Tantrum (CNBC)

Expectations that the Federal Reserve is on course to start tightening policy has spurred fears of a return of last year’s emerging market turmoil, but Societe Generale tips a strong dollar as a bigger risk. “A strong dollar tantrum could be a more worrying scenario than a Fed tightening tantrum,” Michala Marcussen, global head of economics at Societe Generale, said in a note dated Sunday. The U.S. dollar index has climbed around 7% this year, with the Fed now nearly completing the tapering of its asset purchases, with markets widely expecting interest rate increases to begin sometime next year. Some analysts are concerned this will spur a repeat of the “taper tantrum,” when concerns about the Fed’s move to begin tapering caused a brutal selloff in emerging market assets earlier this year and last year.

“Hope today is that a strong dollar will cap U.S. inflation, delay Fed tightening and boost exports to the U.S.,” Marcussen noted, but she believes for that to happen, the U.S. dollar would need to strengthen so much that it would signal much weaker growth in the rest of the world. To delay Fed rate hikes, the euro would need to fall to $1.10, while the U.S. dollar would need to fetch around 120 yen and 6.50 yuan, she said. Early Tuesday, the euro was around $1.2690 and the dollar was fetching 109.40 yen and 6.1495 yuan. “In such a scenario, [a strong] dollar would equate to further capital outflows, placing further pressure on already vulnerable economies,” she said. “A ‘dollar tantrum’ scenario could well prove more painful than a ‘Fed tightening tantrum,’ assuming the latter comes with better growth in the rest of the world.” To be sure, she doesn’t believe the dollar’s move yet qualifies the currency as “strong,” with it still trading just below its long term average, although Societe Generale expects the trade-weighted dollar will rise further into 2015.

Others expect some emerging market assets will react negatively to the dollar’s recent advance. “The upcoming Fed exit will continue to lead front-end rates higher in the quarters ahead,” Goldman Sachs said in a note last week. “In a market environment where China growth expectations decline, front-end U.S. rates gradually push higher and emerging market front-end yields remain anchored around current levels, there is room for emerging market currencies (particularly high-yielding ones) to weaken further.” But Goldman is looking to Europe for cues on whether any emerging market selloff will be confined to the currencies or if it will spill over to other assets. “Heightened Euro area growth concerns can weigh on risky assets, including parts of emerging market credit and equities,” it said.

Nah.

• Strong Dollar Bolsters Fed Patience on Rates Amid Growth Impact (Bloomberg)

The dollar’s strongest year since 2008 is a source of growing concern among some Federal Reserve policy makers, who say further gains have the potential to curb economic growth and keep inflation too low. Atlanta Fed President Dennis Lockhart, New York’s William C. Dudley and Chicago’s Charles Evans have all said in the past week they are watching the dollar as officials debate the timing of the first interest-rate increase since 2006. A strong dollar tends to restrain exports by making them more expensive, holding back growth, while reducing the cost of imported goods. “We’re going to take that into account, the way it’s affecting the economy in terms of net exports and GDP growth and what it means for our inflationary developments,” Evans told reporters yesterday after a speech in Chicago. Evans and Dudley are among policy makers who argue that the Fed can afford to be patient on raising interest rates, and that tightening prematurely poses a greater risk to the world’s largest economy than waiting too long.

“They are worried about the durability of the labor-market recovery and inflation still running below their target, and the dollar feeds into that,” said Guy Berger, U.S. economist at RBS Securities Inc. in Stamford, Connecticut. “If you have a stronger dollar you’re going to have less inflation, and that’s the reason they’re focusing on it,” said Joseph LaVorgna, chief U.S. economist at Deutsche Bank Securities in New York and a former New York Fed economist, who said the dollar’s gains so far are unlikely to affect monetary policy. “If the dollar keeps going up obviously it may have implications for the timing of tightening,” he said. On the other side of the debate are officials such as Dallas Fed President Richard Fisher, who favors an interest-rate increase at the end of the first quarter of next year. In a Bloomberg Radio interview yesterday, Fisher called the strength of the dollar “a vote of confidence” in the U.S. economy. “Everybody is finding the things that are favorable to their side of the argument,” Berger said. “In the case of the doves, the dollar is one of them.”

Could=Will.

• Record World Debt Could Trigger New Financial Crisis (Guardian)

Global debts have reached a record high despite efforts by governments to reduce public and private borrowing, according to a report that warns the “poisonous combination” of spiralling debts and low growth could trigger another crisis. Modest falls in household debt in the UK and the rest of Europe have been offset by a credit binge in Asia that has pushed global private and public debt to a new high in the past year, according to the 16th annual Geneva report. The total burden of world debt, excluding the financial sector, has risen from 180% of global output in 2008 to 212% last year, according to the report. The study by a panel of senior academic and finance industry economists accuses policymakers in many countries of failing to spur sustainable growth by capitalising on historically low interest rates while deterring exuberant lending.

It called for Brussels to write off the debts of the eurozone’s worst-hit countries and urgently embark on a “sizeable” programme of electronic money creation or quantitative easing to push down long-term interest rates. It said unless policymakers kept a lid on risks in the financial system, especially overvalued property and stock markets, a trend for investing in assets with borrowed money could run out of control. The Geneva report, which is commissioned by the International Centre for Monetary and Banking Studies, follows a study earlier this year by the Bank of International Settlements (BIS), which diagnosed the same problem, but said risky borrowing could only be discouraged by higher interest rates. The Geneva report instead argued a concerted effort to tackle the after-effects of the crisis was needed to mitigate a “poisonous combination of high and rising global debt and slowing nominal GDP [gross domestic product], driven by both slowing real growth and falling inflation”.

Deflation is all that’s left. Until debts are restructured.

• Japan’s Industrial Production, Household Spending and Real Wages Fall (WSJ)

A raft of economic data released Tuesday continues to paint a picture of sluggish growth for the third quarter in Japan, despite a tight labor market and rising wages. Industrial production fell a surprising 1.5% on month in August. Retail sales grew 1.9% on month, but separate data adjusted for inflation and expenditure on services showed household spending fell 4.7% on year. At the same time, the unemployment rate fell to 3.5%, a 17-year low. The tightening labor market has contributed to a run of year-on-year wage increases not seen in six years. But those wage gains are outpaced by inflation, meaning real wages are still down 2.6% on year. The government and the Bank of Japan believe wage growth will eventually filter through the economy and start a virtuous cycle of higher private spending and increased production and investment. But some private economists are skeptical about this rosy scenario. Others say that even if such a virtual cycle eventually materializes, the economy will likely lack a robust growth engine for some time.

Repeat: Deflation is all that’s left. Until debts are restructured.

• Eurozone Inflation Drops To Fresh 5 Year Low, Euro Tumbles (Zero Hedge)

Anyone confused why futures are doing their best to surge in the overnight session, the answer is simple: first it was Japan reporting the latest batch of atrocious economic data, which an hour ago was followed by Europe own abysmal econofreakshow, where Eurostat just reported that in September Eurozone inflation rose a meager 0.3% from a year ago, the lowest annual increase since October 2009.This marks the 12th straight month that Euro inflation has been below 1%, and far below the ECB’s goal of 2% inflation.

More importantly, it also shows that some 3 months of a sliding Euro have not only had zero impact on European export competitiveness, as the entire continent is careening into a triple dip recession, but that the ECB is completely powerless to create an inflationary spark, as not only is the bulk of the Eurozone flirting with disinflation but more and more European countries are in outright deflation. Also of note, while headline inflation was in line with expectations, it was core CPI that missed expectations of a 0.9% increase, and rose by only 0.7%, confirming that the most recent bout of deflation in Europe is about far more than just sliding energy prices. In fact for the culprit, perhaps look at Japan which is now exporting deflation hand over fist.

Tick tick tick.

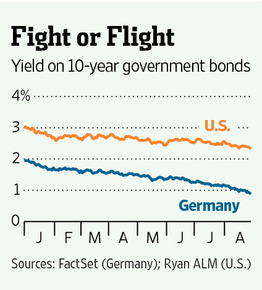

• Europe Ticking All the Wrong Boxes Starts Mirroring Japan (Bloomberg)

Similarities between the euro region and Japan are intensifying, heaping pressure on Mario Draghi while offering good news for bond holders. Sluggish credit growth? Check. Slowing economy? Check. Falling market expectations for inflation? Check. Aging population? Yes, it has that too, placing Europe in a similar situation to what was encountered by the world’s third-largest economy after the bubble burst on its postwar Economic Miracle. That’s a concern for DZ Bank AG, the most bullish forecaster of German bunds in data compiled by Bloomberg. It estimates the 10-year yields will fall to a euro-era record of 0.5% by the first quarter, leaving them below the 0.65% percent median estimate for their Japanese peers.

With the official interest rate near zero, European Central Bank President Draghi may need to do more to steer the region away from the deflation and debt traps that condemned Japan to two decades of stagnation. “Renewed ECB activism offers hope that the euro area will not follow the path Japan embarked on in the 1990s,” said Nikolaos Panigirtzoglou, London-based global market strategist at JPMorgan Chase. “Low growth leads to low income growth. Combine that with persistently high unemployment and you’ve got a lack of confidence.” Europe should be on a roll. It’s never been cheaper for euro-area governments or individuals to borrow money and the ECB is seeking to put cash into the economy through cheap loans to banks and a pledge to buy asset-backed securities.

A lot.

• A Look At Just How Much China’s Housing Downturn Could Hurt GDP (WSJ)

Just how much will a downturn in China’s property market hurt the economy? A new analysis by analysts at Japanese bank Nomura sheds some light. China’s property market won’t recover any time soon, say the analysts, who figure the downturn will shave the country’s GDP growth by 1.4 percentage points in 2014 and 0.6 percentage points in 2015 if there are no drastic changes to policy. In the worst-case scenario , GDP growth could plunge by 4 percentage points. There is no easy way out: the property market correction will be long-lasting if orderly, or very painful if sudden, Nomura analysts Changchun Hua, Wendy Chen and Rob Subbaraman say in a report. The analysts came up with three scenarios. If government policy continues at its current pace—piecemeal targeted easing—GDP growth will drop by 1.4 percentage points this year because property takes a big bite out of industries like steel, construction, chemicals and transport.

If the government eases monetary policy by lifting credit curbs, cutting banks’ reserve requirement ratios and interest rates, and rolling out large stimulus packages, the impact on GDP would be smaller this year and next, shaving growth by 1.1 percentage points in 2014 and 0.3 percentage points in 2015. But in the longer term, it could be worse than continuing current policy because debt levels would be pushed higher and the oversupply situation would worsen, the analysts say. “This is a risky strategy as it could eventually lead to an even sharper correction in the sector, and indeed in the wider economy, ahead.” The third scenario is if the government does nothing and a housing crash ensues. In that case, GDP growth could fall 4 percentage points, the investment firm said. In any case, the downturn could last between two to four years.

“This is not a minor correction,” they said. “This property market downturn is different to those China has experienced in the past. Previous downturns were largely driven by tighter policies while this one appears more naturally driven by market forces.” The last two property market corrections in China occurred in 2007-08 and in 2011-12. (China, where the private housing market only started in 1998, has a shorter property cycle than more mature markets such as the U.S. and Japan.) Those downturns were triggered by policy tightening aimed at reining in property investment, but the market turned around quickly because policymakers changed their minds and loosened the curbs to counter effects of the global financial crisis in 2009 and slowing domestic growth in 2012. This time, the market isn’t likely to behave like a yo-yo. The country is currently plagued by an oversupply problem, especially in so-called third- and fourth-tier cities, and barring a significant crash, the correction will likely be long-lasting, the Nomura analysts said.

• Pimco May Suffer Over $250 Billion In Outflows: Deutsche (CNBC)

Estimates of how much investors are likely to pull from Pimco following the departure of star manager Bill Gross are swirling, with Deutsche Bank now expecting around $266 billion in outflows or a fall in assets equivalent to 20% over the next two years.

The firm has named Daniel Ivascyn as chief investment officer and Gross’s successor while Scott Mather, Mark Kiesel and Mihir Worah will take on Gross’s flagship $221 billion Total Return fund after his shock exit on Friday. Chief executive of Pimco Doug Hodge has said Gross’s former fund “does not define Pimco,” but analyst estimates of outflows are racking up. Deutsche Bank research argued that each €100 billion in outflows is equivalent to around 9% of third party assets under management (AUM), which reduces Pimco’s parent company Allianz’s earnings by around 2%.The bank also cut its price target on the insurer to €135 from €140, but maintained a hold position on the stock. Bernstein Research expects asset outflows between 10 and 30% and sees a “good deal” of Pimco clients switching to Janus Capital Group – where Gross has taken up a post managing a recently launched unconstrained bond fund and similar strategies. “We estimate that a drop in AUM of 10% would have a minor impact on Allianz fair value of 2%, while a 30% drop in AUM would hit the stock by around 13% according to our fundamental valuation mode,” analysts led by Thomas Seidl said.

• Hong Kong Protesters Stockpile Supplies, Prepare For Long Haul (Reuters)

Tens of thousands of pro-democracy protesters extended a blockade of Hong Kong streets on Tuesday, stockpiling supplies and erecting makeshift barricades ahead of what some fear may be a push by police to clear the roads before Chinese National Day. Riot police shot pepper spray and tear gas at protesters at the weekend but withdrew on Monday to ease tension as the ranks of demonstrators swelled. Protesters spent the night sleeping or holding vigil unharassed on normally busy roads in the global financial hub. Rumors have rippled through crowds of protesters that police could be preparing to move in again on the eve of Wednesday’s anniversary of the Communist Party’s foundation of the People’s Republic of China in 1949. “Many powerful people from the mainland will come to Hong Kong. The Hong Kong government won’t want them to see this, so the police must do something,” Sui-ying Cheng, 18, a freshman at Hong Kong University’s School of Professional and Continuing Education, said of the National Day holiday.

“We are not scared. We will stay here tonight. Tonight is the most important,” she said. The protesters, mostly students, are demanding full democracy and have called on the city’s leader, Leung Chun-ying, to step down after Beijing ruled a month ago it would vet candidates wishing to run for Hong Kong’s leadership in 2017. While Leung has said Beijing would not back down in the face of protests it has branded illegal, he also said Hong Kong police would be able to maintain security without help from People’s Liberation Army (PLA) troops from the mainland. “When a problem arises in Hong Kong, our police force should be able to solve it. We don’t need to ask to deploy the PLA,” Leung told reporters at a briefing on Tuesday. There was a growing sense that the protests could come to a head later on Tuesday before the National Day celebrations.

No.

• Will Hong Kong Spark An Asian Spring? (CNBC)

Thousands of protesters campaigned for full democracy in Hong Kong over the weekend, raising the question: Could unrest spread to mainland China. “Today is a very important moment for Beijing and for the Hong Kong government because if they don’t control the streets of Hong Kong today they could see this thing start to mushroom,” Gordon Chang, author of ‘The Coming Collapse of China’ told CNBC on Monday. “Beijing has a lot at stake here as this is something that could spread…political scientists call it the ‘demonstration effect,'” he said. “We’re starting to see that now in China.” Netizens across China shared images from the protests and expressed their views via social media, but authorities quickly deleted posts and shut down websites, in line with China’s history of censorship.

Popular photo sharing website Instagram was blocked after photos and videos from the Hong Kong protests were posted, according to numerous reports. Meanwhile, the phrase “Occupy Central” was blocked on Weibo – the hugely popular micro-blogging site in China – on Sunday. Ripples of discontent have begun to show in Taiwan and Macau. In Taiwan, a state that is essentially autonomous, student leaders occupied the lobby of Hong Kong’s representative office on Monday in a show of support for democracy protesters, according to local media. Meanwhile, in Macau – another “special administrative region” like Hong Kong, a referendum conducted last month during the official election of its chief executive, showed a striking disparity between the election result and public opinion.

Obama step in?!

• US Judge Holds Argentina in Contempt of Court in Bond Payment Case (NY Times)

For more than a year, Judge Thomas P. Griesa of Federal District Court in Manhattan has warned that Argentina would suffer repercussions if it defied his orders regarding payments to bondholders. On Monday, the judge put some teeth behind those warnings, ruling the nation in contempt of court. He stopped short of issuing sanctions, however, saying he would make a decision on them in the future. Speaking firmly, Judge Griesa indicated that the Republic of Argentina had gone a step too far in seeking to sidestep his injunction that forbids the government from paying only the bondholders it chooses. “What has happened is the Republic, in various ways, has sought to avoid, to not attend to, almost to ignore this basic part of its financial obligations,” Judge Griesa said on Monday. The ruling was another dramatic turn in a legal battle that has pitted President Cristina Fernández de Kirchner of Argentina against a group of hedge funds that are seeking more than $1.5 billion in payments on bonds that defaulted in 2001.In a separate move that could increase the tension, the Argentine government sent a letter to Secretary of State John F. Kerry on Monday morning before the hearing, seeking to enlist his support and calling the actions by Judge Griesa “excessive judicial harassment,” according to the embassy in Washington. “A declaration of contempt would result in an unprecedented escalation in the conflict,” the letter, signed by the Argentine ambassador to the United States, said. “We are in uncharted waters,” said Arturo C. Porzecanski, economist in residence at American University’s School of International Service. “This makes official the fact that Argentina has been a rogue debtor for many many years and has been in contempt of many many judgments.”

And they’re right.

• Argentina Says US Judge Contempt Order ‘Violates International Law’ (BAH)

The Foreign Ministry has asserted that New York district judge Thomas Griesa’s contempt ruling against Argentina is in clear breach of international law, adding that the decision had no practical ramifications against the nation and only served to aid the vulture fund campaign. The government department, headed by Foreign minister Héctor Timerman, stated this evening that Griesa’s ruling “is in violation of international law, the United Nations Charter and the Organisation of American States charter,” in a press statement.

“All of these instruments establish that the United States of America as a state is the only entity responsible for the actions of any of its organisms, such as the recent decision from its judicial branch,” the missive fired, hours after the judge’s ruling was made public.“Judge Griesa’s decision has no practical effect, expect for providing new elements for the vulture funds to use in their slanderous political and media campaign against Argentina.” The Ministry strongly criticised the magistrate, who despite finding Argentina in contempt declined to immediately impose financial penalties of up to 50,000 dollars a day, as requested by plaintiffs NML Capital in the ongoing sovereign debt conflict in New York. “Griesa boasts the sad record of being the first judge to hold a sovereign state in contempt for paying a debt, after failing in his efforts to obstruct Argentina’s foreign debt restructuring,” the statement said. “The Argentina government reaffirms its decision to keep exercising its defence of national sovereignty, and requesting that the United States accepts the International Court of Justice’s juridisction in order to solve this controversy between the two countries.”

Word.

• Europe’s Real Crisis Will Be Political With Spain as Ground Zero (Phoenix)

Spain’s Mariano Rajoy is back with yet another display of why he should never have been allowed to take office in the first place. For those who need a quick primer, here’s a quick highlight reel of Rajoy’s more notable accomplishments:

1) Helped facilitate biggest housing bubble in Spanish history, a bubble so large that the US’s looks like a molehill in comparison

2) Took bribes and kickbacks from developers in helping to create said bubble (more on this later).

3) Claimed Spain would never need a bailout, then demanded a €100 billion bailout one weekend before flying off to watch a soccer match.

4) Raided Spain’s social security fund, investing 90% of its assets in Spanish bonds… which were on the verge of default a mere six months before.

5) Got caught with dirty money he received from property developers and stated the following, “…everything that has been said about me and my colleagues in the party is untrue, except for some things that have been published by some media outlets,”

Now Rajoy is dealing with the problem of Catalonia (a region in Spain) wanting independence. Catalonians are proposing putting the matter to a vote, much as Scotland recently did regarding its own move to potentially break away from the UK. Rajoy, never one to miss the opportunity to embarrass himself, has called the decision to vote for independence “profoundly anti-democratic.” Bear in mind, this is the same “leader” who likes to proclaim that Spain is in a recovery… while Spain’s unemployment is roughly 24% and youth unemployment is above 50%. At some point, the markets will call BS on Spain’s dreams of recovery and the bond markets will rebel. When this happens the whole fraud will come unraveled. However it might take a full-scale political crisis before this happens. And by the look of things we’re not far from one. We’re back in trouble whenever Spain takes out the long-term trendline for its 10-year bond yields.

Democracy?

• Spain Court Blocks Catalonia Vote as Standoff Escalates (Bloomberg)

Spain’s Constitutional Court temporarily blocked Catalan government plans to hold a vote on independence, raising the stakes in the central government’s standoff with the regional administration in Barcelona. Catalan president Artur Mas signed a decree on Sept. 27 calling for a Nov. 9 ballot as a non-binding consultation on independence for the region of about 7.5 million people in northeastern Spain. Spanish Prime Minister Mariano Rajoy denounced the vote as unconstitutional and said yesterday that his government had filed a lawsuit to block it. The suit was admitted for consideration, effectively blocking the Catalan decree and vote until the court makes a further ruling on the government’s legal action, a Madrid-based official at the court said last night by phone.

“It’s false that the right to vote can be assigned unilaterally to one region about a matter that affects all Spaniards,” Rajoy told reporters at the government palace in Madrid. “It’s profoundly anti-democratic.” Less than two weeks after Scotland voted against independence from the U.K. after 307 years of union, Mas and Rajoy are at loggerheads over whether the Spanish region can stick with its plan to vote on independence following the court’s blocking of the vote. Unlike in Scotland, polls suggest a majority of Catalans would support independence. “The Constitutional Court met at supersonic speed,” Mas said yesterday during a televised presentation of the steps to be taken on the proposed transition of Catalonia. “We hope the members of the Constitutional Court keep in mind that they should be a referee for everyone, not for one side only.”

Mass graves uncovered. No mention in the west.

• Russia Investigates ‘Kiev Sponsored Genocide’ In East Ukraine (Reuters)

Russia opened a criminal case Monday into what it called Kiev’s genocide of Russian-speaking residents in eastern Ukraine in a move that could increase tensions during a strained ceasefire in the region. An official statement said Russian-speaking citizens were targeted by Kiev forces using heavy weapons to kill over 2,500 people in the “Luhansk and Donetsk people’s republics,” the breakaway regions in the east. The investigation could ratchet up tensions between the post-Soviet neighbors weeks after Kiev and pro-Russian rebels agreed on a ceasefire earlier this month that has been marred by daily skirmishes and artillery shelling. “The Investigative Committee opened has opened a criminal case into the genocide of the Russian-speaking population of Ukraine’s southeast,” said the statement by the Investigative Committee of the Russian Federation, a law enforcement body that answers only to President Vladimir Putin.

“Unidentified representatives of Ukraine’s senior political and military leadership, National Guard and the Right Sector [nationalist organization] gave orders aimed at the intentional annihilation of the Russian-speaking citizens,” the statement said. The statement cited violations of the 1948 U.N. convention on genocide and other “international legal acts” to describe the reported violence, including the destruction of 500 houses and public infrastructure buildings since fighting erupted in April. Russia has long blamed Kiev for violence against civilians in the east, as the West has accused Moscow of sending weapons and troops to help pro-Russian rebels fighting Kiev’s forces. A recent U.N. report put the death toll at 2,593 people on both sides and accused pro-Russian separatists of a wide array of human rights abuses, including murder, abductions and torture.

“Carter said 200-300 girls are sold into sexual slavery every month in his home state Georgia.”

Happy birthday, Mr. President.

• Jimmy Carter, Turning 90, Says Slavery Is Worse Now Than In 1700s (CNBC)

Human slavery is not just a major issue in developing countries, but is a serious problem in the U.S. and is more prolific now than during the 18th and 19th century, former President Jimmy Carter has told Tania Bryer, host of “CNBC Meets.” Carter said 200-300 girls are sold into sexual slavery every month in his home state Georgia, and many living in advanced economies are completely unaware of the abuse happening to young women close to home. Referring to facts in his most recent book, “A Call to Action, Women, Religion, Violence and Power,” Carter describes the abuse of women around the world as “the worst, unaddressed issue that the world faces today.” “And those of us in the more advanced countries don’t know much about horrible abuse of girls whose genitals are mutilated when they’re very young, children who are killed because a girl is raped by strangers and her family kills her to protect their own nation’s honor.

These kinds of things go on in the more remote parts of the world as far as we’re concerned,” the Democratic former president said. “But even in the United States, human slavery now is greater than it ever was during the 18th or 19th century. In Atlanta, Georgia, we have between 200-300 girls sold into sexual slavery every month,” he added. Before moving into politics, Carter was in the Navy and worked on the family’s farm. He served as the 39th president from 1977 to 1981 and was awarded the Nobel Peace Prize in 2002 for his efforts in finding peaceful solutions to international conflicts and his work in human rights. Carter, who is turning 90 on Wednesday, and wife Rosalynn still travel the world doing work for The Carter Center, his human rights and health care charity, which he set up after leaving the White House.

Export land model.

• Saudi Arabia Poised To Tip Into Deficit (CNBC)

Saudi Arabia risks falling into a budget deficit next year and may have to tap its reserves, the International Monetary Fund (IMF) has warned. One sign that Saudi Arabia is in danger of dipping into deficit is its “break-even oil price” – the price oil would need to be for the country to balance its budget. The IMF, in its annual consultation paper released Wednesday, notes that Saudi Arabia’s break-even price has risen to $89 a barrel in 2013 from $78 a barrel in 2012. It would be the first time since 2010 that the Middle East’s largest economy records a deficit for its government finances. Apart from domestic expenditures such as ambitious infrastructure outlays, pressure on government finances is also coming from substantial aid pledges to countries across the Arab World.

“This expenditure path and lower oil revenues lead to an overall fiscal deficit in 2015, which is expected to deteriorate further to almost 7.5% of (gross domestic product) GDP by 2019,” the fund said in the 54-page dossier. But while Saudi officials have shrugged off suggestions spending needed to be reined in, experts diverge on projections. “According to our model, we will see a fiscal deficit in 2016 as government maintains high spending while a gradual decline in oil prices will push revenues downward,” Fahad Alturki, Head of Research at Riyadh-based Jadwa Investment, told CNBC. “We also factor in lower oil production as many of the oil outages that we see today are expected to resume production”.

Something tells me taxpayers will chip in.

• North Sea Oil Costs Threaten $1.6 Trillion Investment Needed (Bloomberg)

North Sea oil operators’ surging costs risk scaring away the more than 1 trillion pounds ($1.6 trillion) of investment needed to meet their production goals, according to industry lobby Oil & Gas U.K. The country needs that investment if it hopes to recover the equivalent of more than 20 billion barrels of oil, the group said today in a statement. Unit operating costs are about 60% higher than as recently as 2011, it said. “The U.K. has to compete for each and every pound of that investment,” Malcolm Webb, chief executive officer of the industry group, said today in the statement. “If the current trend of rising cost continues, the U.K. Continental Shelf will cease to provide a healthy return on investment.”

Energy resources were central to the debate over Scottish independence, with those supporting a split claiming almost all the oil as the nation’s own. Oil companies were among those who said before the Sept. 18 referendum that keeping Britain’s 307-year-old union was good for the industry because of the stability and certainty it provided. A review by Ian Wood, former head of engineering company John Wood Group Plc (WG/), this year estimated there were 12 billion to 24 billion barrels yet to be extracted from the North Sea. Production has dropped 40% in the past three years as fields mature, according to the February report. “We need a lighter tax burden, a simpler and more predictable system of field allowances and fiscal support for exploration,” said Michael Tholen, director of economics at Oil and Gas U.K. The government is expected to announce the results of its fiscal review in December.

How low are we going to take this?

• Earth Lost 50% Of Its Wildlife In The Past 40 Years (Guardian)

The number of wild animals on Earth has halved in the past 40 years, according to a new analysis. Creatures across land, rivers and the seas are being decimated as humans kill them for food in unsustainable numbers, while polluting or destroying their habitats, the research by scientists at WWF and the Zoological Society of London found. “If half the animals died in London zoo next week it would be front page news,” said Professor Ken Norris, ZSL’s director of science. “But that is happening in the great outdoors. This damage is not inevitable but a consequence of the way we choose to live.” He said nature, which provides food and clean water and air, was essential for human wellbeing. “We have lost one half of the animal population and knowing this is driven by human consumption, this is clearly a call to arms and we must act now,” said Mike Barratt, director of science and policy at WWF. He said more of the Earth must be protected from development and deforestation, while food and energy had to be produced sustainably.

The steep decline of animal, fish and bird numbers was calculated by analysing 10,000 different populations, covering 3,000 species in total. This data was then, for the first time, used to create a representative “Living Planet Index” (LPI), reflecting the state of all 45,000 known vertebrates. “We have all heard of the FTSE 100 index, but we have missed the ultimate indicator, the falling trend of species and ecosystems in the world,” said Professor Jonathan Baillie, ZSL’s director of conservation. “If we get [our response] right, we will have a safe and sustainable way of life for the future,” he said. If not, he added, the overuse of resources would ultimately lead to conflicts. He said the LPI was an extremely robust indicator and had been adopted by UN’s internationally-agreed Convention on Biological Diversity as key insight into biodiversity.

A second index in the new Living Planet report calculates humanity’s “ecological footprint”, ie the scale at which it is using up natural resources. Currently, the global population is cutting down trees faster than they regrow, catching fish faster than the oceans can restock, pumping water from rivers and aquifers faster than rainfall can replenish them and emitting more climate-warming carbon dioxide than oceans and forests can absorb. The report concludes that today’s average global rate of consumption would need 1.5 planet Earths to sustain it. But four planets would be required to sustain US levels of consumption, or 2.5 Earths to match UK consumption levels.

Useless stats.

• Affordable Global Housing Will Cost $11 Trillion (Bloomberg)

Replacing the world’s substandard housing and building affordable alternatives to meet future global demand would cost as much as $11 trillion, according to initial findings in a McKinsey & Co. report. The shortage of decent accommodation means as many as 1.6 billion people from London to Shanghai may be forced to choose between shelter or necessities such as health care, food and education, data disclosed at the 2014 CityLab Conference in Los Angeles show. McKinsey will release the full report in October. The global consulting company says governments should release parcels of land at below-market prices, put housing developments near transportation and unlock idle property hoarded by speculators and investors. The report noted that China fines owners 20% of the land price if property is undeveloped after a year and has the right to subsequently confiscate it.

“Cities struggle with the dual challenges of housing their poorest citizens and providing housing at a reasonable cost,” said the paper, whose lead author, Jonathan Woetzel, is a Shanghai-based director of McKinsey Global Institute, the company’s research unit. About 330 million households — about 1.2 billion people — now struggle with substandard housing, a number that may increase to 440 million in 11 years, McKinsey forecasts. Acceptable housing is within an hour’s commute of work and has basic services including flush toilets and running water, the report says. What the authors call the affordable-housing gap now stands at about $650 billion a year, or 1% of global gross domestic product. The baseline for their calculation is housing payments that exceed 30% of household income in 2,400 cities around the globe.