Detroit Publishing Co Galveston Flood disaster cyclorama, Coney Island 1904

If there’s one thing that defines why we, and the world we live in, are doomed, it can be found – once more – in a recent spat of (leaked) reactions to the upcoming new IPCC report. We’ve come a long way since skeptics started budging in the way creationists demand equal time on the new Cosmos series – only more successful – and now we’re way past mere skepticism. Not only has it become totally acceptable to pooh pooh and hush hush climate change, we’ve arrived at the point where we go look for positive angles.

The first step in the new message is that things are not nearly as bad as we were once told, as is so craftfully put in words by the subtle change from ‘mitigation’ to ‘adaptation’. Throwing in the term ‘resilience’ further enforces the positive notion. As the Telegraph puts it:

Climate Change: The Debate Is About To Change Radically

The latest report from the UN’s Intergovernmental Panel on Climate Change (IPCC) is due out next week. If the leaked draft is reflected in the published report, it will constitute the formal moving on of the debate from the past, futile focus upon “mitigation” to a new debate about resilience and adaptation.

The new report will apparently tell us that the global GDP costs of an expected global average temperature increase of 2.5 degrees Celsius over the 21st century will be between 0.2% and 2%. To place that in context, the well-known Stern Review of 2006 estimated the costs as 5-20% of GDP. Stern estimates the costs of his recommended policies for mitigating climate change at 2% of GDP – and his estimates are widely regarded as relatively optimistic (others estimate mitigation costs as high as 10% of global GDP).

Achieving material mitigation, at a cost of 2% and more of global GDP, would require international co-ordination that we have known since the failure of the Copenhagen conference on climate change simply was not going to happen. Even if it did happen, and were conducted optimally, it would mitigate only a fraction of the total rise, and might create its own risks. And to add to all this, now we are told that the cost might be as low as 0.2% of GDP. At a 2.4% annual GDP growth rate, the global economy increases 0.2% every month.

See? We would be robbing ourselves by paying any further attention to Nicolas Stern, who just 8 years ago exaggerated the economical costs of climate change as much as 1000%. Has Stern now been found out to be a charlatan? Well, that too, and the science has greatly improved, through the addition of think tanks and scientists that know before they start researching that all dire warnings are just bogus anyway.

And no-one can seriously expect us to do anything drastic like shaking up the comfort we live in if the dollar cost is so low in comparison to the inconveniences we would have to suffer, can they?

So the mitigation deal has become this: Accept enormous inconvenience, placing authoritarian control into the hands of global agencies, at huge costs that in some cases exceed 17 times the benefits even on the Government’s own evaluation criteria, with a global cost of 2% of GDP at the low end and the risk that the cost will be vastly greater, and do all of this for an entire century, and then maybe – just maybe – we might save between one and ten months of global GDP growth. Can anyone seriously claim, with a straight face, that that should be regarded as an attractive deal or that the public is suffering from a psychological disorder if it resists mitigation policies?

But don’t let’s stop there; It’s not only that monetary costs are now claimed to be less than thought before, no, climate change should even be seen as offering opportunities:

Global warming poses risks, but also opportunities: IPCC

“Although it focuses on a whole analytical and sometimes depressing view of the challenges we face, it also looks at the opportunities we face,” said Christopher B. Field, the co-chair of the Intergovernmental Panel on Climate Change. “This can not only help us to deal with climate change but ultimately build a better world.”

This is of course just another way of saying: “how much money can we make from destroying the world we live in?” But that’s undoubtedly not how the IPCCs Mr Field would like you to see it. The IPCC long ago stopped being a serious research organization. Institutes and corporations who felt threatened in their ability to make money and hold on to power have successfully infiltrated it and demanded “equal airtime”.

And that’s a perfect reflection of the societal model we live in. Every single thing in our lives gets reduced to its dollar value. And if it’s too costly, sorry, but we must throw it out. Every plant, every river, every animal, every sunset and every human being only have a value insofar as it can be expressed in dollar terms.

Which is bad news for polar bears and lions and rhinos – and ultimately people, first in Africa, Asia, South America, then at home -, since they have value only as tourist attractions. And isn’t it much more convenient and cost effective to dump a few of each in a zoo somewhere so we can simply drive to go see them, instead of going on safari’s or Arctic cruises?

Nature is useless on its own; it only has a perceived value where we can stick a price tag on it. No matter that nature is where we come from and are an integral part of, and it never came with a bottom line until we invented one. Despite the fact that we have very little idea of how nature actually works. But then, that is the core of our tragedy, isn’t it? We manage to fool ourselves into believing that we are mighty smart. That’s a surefire way to get everything that really counts all wrong.

Our children and children’s children are going to find out that the only thing we really know about complex systems is that we don’t know much of anything about them. And that when risking to disturb them, the precautionary principle should always be the first thing on our minds.

Assigning dollar values to everything we see around us is a convenient simplification of things, and it guarantees that those who already have most dollars stay on top, but there’s nothing smart about it when you look at it in terms of complex systems or the precautionary principle.

But the worst part must be that it doesn’t make anyone any happier, either. And that we’re not capable of understanding that. We don’t know what makes us happy. We need other people to tell us what does. And there’s a lot of other people who see profit opportunities in that.

Anyway, this is why we’re doomed: if we don’t understand the consequences of our actions, then we just ignore them. Thinking that if we don’t understand them, how bad can they be? Since we are very smart, right? Thing is, if we were so smart, why do we feel the need to almost infinitely simplify our view of the planet’s almost infinitely complex system, by attaching price tags to everything? Either from a rational, scientific point of view, or from an emotional point of view, how does that make sense?

• The US Is Now Spending 26% Of Available Tax Revenue To Pay Interest (Sovereign Man)

By the 19th century, the Ottoman Empire had become a has-been power whose glory days as the world’s superpower were well behind them. They had been supplanted the French, the British, and the Russian empires in all matters of economic, military, and diplomatic strength. Much of this was due to the Ottoman Empire’s massive debt burden. In 1868, the Ottoman government spent 17% of its entire tax revenue just to pay interest on the debt.

And they were well past the point of no return where they had to borrow money just to pay interest on the money they had already borrowed. The increased debt meant the interest payments also increased. And three years later in 1871, the government was spending 32% of its tax revenue just to pay interest. By 1877, the Ottoman government was spending 52% of its tax revenue just to pay interest. And at that point they were finished. They defaulted that year.

This is a common story throughout history. The French government saw a meteoric rise in their debt throughout the late 1700s. By 1788, on the eve of the French Revolution, they spent 62% of their tax revenue to pay interest on the debt. Charles I of Spain had so much debt that by 1559, interest payments exceeded ordinary revenue of the Habsburg monarchy. Spain defaulted four times on its debt before the end of the century.

It doesn’t take a rocket scientist to figure out that an unsustainable debt burden soundly tolls the death knell of a nation’s economy, and its government. Unfortunately, it can sometimes take a rocket scientist to figure out what the real numbers are; governments have a vested interest in not being transparent about their debts and interest payments.

[..] … total US interest payments in Fiscal Year 2013 were a whopping $415 billion, roughly 17% of total tax revenue. Just like the Ottoman Empire was at in 1868. Here’s the thing, though– it’s inappropriate to look at total tax revenue when we’re talking about making interest payments. The IRS collected $2.49 trillion in taxes last year (net of refunds). But of this amount, $891 billion was from payroll tax. According to FICA and the Social Security Act of 1935, however, this amount is tied directly to funding Social Security and Medicare. It is not to be used for interest payments.

Based on this data, the amount of tax revenue that the US government had available to pay for its operations was $1.599 trillion in FY2013. This means they actually spent approximately 26% of their available tax revenue just to pay interest last year… a much higher number than 17%. This is an unbelievable figure. The only thing more unbelievable is how masterfully they understate reality… and the level of deception they employ to conceal the truth.

Read more …

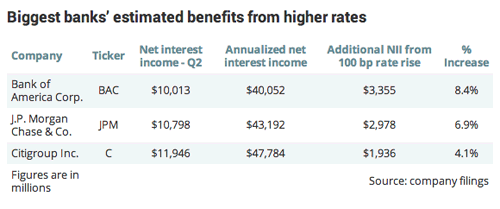

• You’re Still Giving the Big Banks a Handout (Bloomberg)

The largest U.S. banks and their lobbyists have been trying hard to counteract the growing impression that they present an unacceptable threat to the economy. In a new series of papers, the Federal Reserve Bank of New York offers some evidence that they probably won’t like. Critics of the big banks assert that repeated government bailouts have created a perverse incentive: The bigger and more systemically important a bank becomes, the more certain its creditors can be that they will get rescued in an emergency. Such too-big-to-fail status, the logic goes, allows banks to borrow more cheaply than they otherwise would — a taxpayer subsidy that encourages them to take the kind of risks that lead to disasters.

The contributions from the New York Fed economists support this narrative in two ways: They place a value on the big banks’ funding advantage, and they suggest that banks with government support do tend to take bigger risks. Looking at new bond issues from 1985 to 2009, New York Fed Vice President Joao Santos estimates that the largest banks paid 0.31%age point less when they issue A-rated debt than when their smaller peers did (after controlling for some idiosyncratic features of the bonds). He also found that the discount was significantly greater than what large companies enjoyed in other industries, undermining bank lobbyists’ argument that the funding advantage stems from the general benefits of size rather than from their too-big-to-fail status.

The study has some important blind spots. Its bond data go only through 2009, so it can’t show what, if anything, the 2010 Dodd-Frank financial-reform law may have done to reduce the taxpayer subsidy. Also, when grouping bonds by rating category, it ignores the rating uplift the largest banks receive thanks to the expectation of government support. This would have the effect of underestimating their funding advantage — a problem common among studies of the too-big-to-fail subsidy.

Perhaps more interesting is a separate paper in which Santos and two co-authors find that banks make more bad loans when they have a reasonable expectation of getting bailed out in a crisis. Specifically, the authors look at a special credit rating, issued by Fitch, that assesses the likelihood of government support. A one-notch increase in the rating — say, from A-minus to A — is associated with an 8% increase in a bank’s ratio of non-performing loans.

Read more …

• Hundreds Rush To Rural Chinese Banks After Solvency Rumours (Reuters)

Hundreds of people rushed on Tuesday to withdraw money from branches of two small Chinese banks after rumours spread about solvency at one of them, reflecting growing anxiety among investors as regulators signal greater tolerance for credit defaults. The case highlights the urgency of plans to put in place a deposit insurance system to protect investors against bank insolvency, as Chinese grow increasingly nervous about the impact of slowing economic growth on financial institutions. Regulators have said they will roll out deposit insurance as soon as possible, without giving a firm deadline.

Domestic media reported, and a local official confirmed, that ordinary depositors swarmed a branch of Jiangsu Sheyang Rural Commercial Bank in Yancheng in economically troubled Jiangsu province on Monday. The semi-official China News Service quoted the bank’s chairman, Zang Zhengzhi, as saying it would ensure payments to all the depositors. The report did not say how the rumour originated. Chen Dequn, a resident in Yandong, just outside Yancheng, said she saw a crowd of about 70 to 80 people gathering in a branch of Sheyang Rural Commercial Bank in her town on Tuesday. “At the moment there are about 70 or 80 people in there. Normally there’d only be about 10,” she told Reuters by telephone.

Officials at another small bank, Rural Commercial Bank of Huanghai, said they had faced similar rushes by depositors, triggered by rumours of insolvency at Sheyang. “We will be holding an emergency meeting tonight,” an official at the bank’s administration office told Reuters, but declined to comment further. Why Yancheng investors suddenly lost confidence in the security of their bank deposits is not clear, given that the Sheyang bank is subject to formal reserve requirements, loan-to-deposit ratios and other rules to ensure it keeps sufficient cash on hand to meet demand. Bank failures in China are virtually unknown, as Chinese banks are considered to operate under an implicit guarantee from the government.

Finally, money market interest rates have eased since February, and traders say liquidity in the interbank market – where banks like Sheyang can tap short-term funds to meet depositor demand – remains relatively relaxed. “It’s true that these rumours exist, but actually (the bank going bankrupt) is impossible. It’s a completely different situation from the problem with the cooperatives,” said Zhang Chaoyang, an official at the propaganda department of the Communist Party committee in Tinghu district, where the bank branch is located. Zhang was referring to an incident that rattled depositors in Yancheng in January, when some rural cooperatives – which are not subject to the supervision of the bank regulator – ran out of cash and locked their doors.

Read more …

• High Debt, Slow Sales Loom Over Chinese Property Firms (SCMP)

All eyes are now on a few Chinese real estate developers particularly vulnerable to slow sales and tight credit, as mainland China’s property market enters a new downturn. On the watch list are Hopson Development, Renhe Commercial, Glorious Property and Coastal Greenland, all suffering from either weak sales or high debt ratios, according to global ratings agencies. These companies are scheduled to announce annual results Thursday or Friday.

Glorious Property issued a profit warning last week, saying that lower gross profit margin, provision for impairment losses on some unsold units and smaller gains in the fair value of investment properties would result in “a significant decrease” in net profit for last year. At the end of June, Glorious Property (36%) and Hopson (42.8%) had the lowest ratio of cash versus short-term debt among all mainland Chinese developers rated by Moody’s.

Adding to their cash strain is the extra caution being exercised by domestic banks when lending to developers after the collapse of a small private property firm in Ningbo and the first onshore debt default by a solar energy firm earlier this month that shattered the long-held belief that Beijing would always bail out struggling firms. “In this environment, we believe financiers and investors will become more selective and favour borrowers with relatively strong credit quality, thereby further pressuring the liquidity of financially weak developers,” said Franco Leung, a property analyst at Moody’s Investors Service.

Both Leung and Matthew Kong from Standard & Poor’s ruled out the possibility of any short-term systemic risk, while expecting bigger developers to become even stronger. “The key lies in developers’ sales execution this year,” Kong said. “But bankruptcies are less likely, as they can opt to sell assets to peers and quit the market.” Shou Bainian, chief executive of Greentown China, said on Monday: “If their assets are good, there is still hope (of survival).” “But if their assets are not so good, neither is their reputation – then it will become more difficult.”

Read more …

• China Poised To Ramp Up Its Stimulus Policies (SMH)

Signs that China’s economy is coming off the boil are fuelling speculation that the country’s government will step in with new stimulus measures and could even cut official interest rates. But any stimulus measures are expected to stop short of the massive economic “pump priming” undertaken by the country in 2008-09, when the central government announced a four trillion yuan package.

“Can growth stabilise without a major change of policy stance? We believe it cannot, as tight labour market conditions suggest that potential growth has already dropped to around 7% or below,” analysts at Japanese broker Nomura said in a note. “From a cyclical perspective the cumulative policy tightening since mid-2013 will likely damage investment momentum in coming quarters unless the policy stance loosens.”

While the Chinese government has sought to pursue its long-term policy of reforming the country’s economy and shifting it away from investment-led growth, Nomura said it could turn back to its short-term goals if, as expected, the growth target for this year is not reached. China set a growth target of 7.5% this year, the same level of economic expansion it had targeted over the past two years. Economists have said that recent data, such as a weakening in manufacturing activity, meant that the government would have loosen fiscal and monetary policies if it wants to met its GDP target.

“When short-term objectives are challenged, the government usually shifts its focus toward promoting growth. We have witnessed this ‘two-step forward, one-step back’ style of policy swings in the past,” the analysts wrote. The latest reading of manufacturing activity, from HSBC’s March preliminary survey, showed that the sector had shrunk for the third-straight month. It also followed a fall in exports and weaker industrial output figures. Some economists have also revised down their outlook for Chinese growth.

Policy levers that the central government looks most likely to pull include cuts to banks’ reserve requirement ratio (RRR) to boost growth amid high overall financing costs. Nomura’s analysts are tipping RRR cuts of 50 basis points in the second-quarter of this year, and further easing of 50 basis points in the third-quarter. The supply of credit through bank loans and total social financing is also expected to rise, while the likelihood of interest rate cuts is increasing, the analysts wrote.

Economists said the recent weakening of the yuan, while seen as being part of the People’s Bank of China’s attempts to punish speculators betting on the continued rise of the renminbi, could also provide some relief to local exporters. At the same time, the weakening of the currency, which analysts believe was through the central bank’s intervention in foreign exchange markets, has lowered domestic interest rates and made funding cheaper for borrowers.

Read more …

• Morgan Stanley Dismisses Talk of China Minsky Moment (Bloomberg)

Morgan Stanley is sticking to its buy recommendation on Chinese stocks, saying concern that there’ll be a “significant market disruption” in the world’s second-largest economy is overstated. China’s consumption and services are bigger than officially reported, giving the economy more room to cope with slowing productivity growth, the Morgan Stanley analysts said. The government’s reforms and its “formidable” financial resources will help policy makers transform the economy without triggering a debt crisis, the analysts wrote in a report in which they kept their overweight calls on both Chinese and Russian equities.

The economy’s slowdown and rising debt levels pushed the Hang Seng China Enterprise Index (HSCEI), which tracks Chinese firms listed in Hong Kong, into a bear market on March 20. While Morgan Stanley’s analysts said that debate is mounting about whether China is approaching a “Minsky moment,” a term used to explain an asset collapse following the exhaustion of credit expansion, they said they remain bullish. “The apparent deterioration in productivity and diminishing returns to leverage are not as severe as the consensus thinks when one takes into account true activity” in the consumer and service sectors of the economy, Morgan Stanley analysts led by Jonathan Garner wrote in the note.

Read more …

• China Finds The Credit Habit Hard To Kick (Satyajit Das)

China has had a 35-year addiction to cheap credit. The 2007/2008 global financial crisis and the resulting rare synchronous recessions in the developed world exposed China’s economy, especially its export sectors, to a large external demand shock – slowing growth. The recovery has been driven by a significant expansion in credit (known as TSF – total social financing). Post-crisis, new lending by Chinese banks has been consistently about 30% or more of GDP. About 90% of this lending was directed towards investment in building, plant, machinery and infrastructure, especially by state-owned enterprises.

According to the World Bank, almost all of China’s growth since 2008 has come from “government-influenced expenditure”. This expansion led to a rapid increase in the level of debt. Most estimates now put Chinese government (including local government), corporate and household debt at about 200-250% of GDP, up from about 140-150% in 2008. According to a 2013 report by China’s National Audit Office, Chinese government debt, including local government debt, is about 55% of GDP –about $5 trillion (£3 trillion) – an increase of about 60% from 2010.

But the official Chinese government debt figure may not be complete, as it may exclude debts from local governments and central departments outside the finance ministry. If these items are included, China’s government debt including contingent liabilities would be higher, perhaps 90% of GDP. There has been a parallel increase in private sector debt. Corporate debt has increased sharply, approaching 150% of GDP. Traditionally considered compulsive savers, Chinese households have increased borrowing levels from about 20-30% to 40-50% of GDP. Inflation has driven increases in household borrowing, with sharply higher home prices requiring greater borrowings and devaluation of purchasing power encouraging debt-fuelled consumption.

China’s overall debt is high, especially when benchmarked against comparable emerging markets. Many Asian emerging markets had lower debt and higher per capita GDP before the Asian monetary crisis of 1997/1998. The rapid rate of increase in debt is also seriously concerning. An increase in debt of about 30% of GDP in five or less years is regarded as problematic. Several economies – Japan in the late 1980s, South Korea in the 1990s, not to mention the US and UK in the early 2000s – experienced similar rapid growth rates in credit, resulting in serious financial crises.

Another measure is the credit gap – the difference between increases in private sector credit growth and economic output. Research studies have found that 33 countries with credit gaps experienced a subsequent rapid slowdown in growth, typically by at least 50%. In China, the credit gap since 2008 is over 70% of GDP. Chinese credit intensity (the amount of debt needed to create additional economic activity) has increased. China now needs about $3-$5 to generate $1 of additional economic growth, although some economists put it even higher, at $6-$8. This is an increase from the $1-$2 needed for each dollar of growth 8 to 10 years ago.

Read more …

• Hong Kong’s Soaring Bank Exposure to China Sparks Credit Concerns (Reuters)

In just a few years, Hong Kong banks have ramped up lending to China from near zero to $430 billion, fueling concerns about their credit exposure to the mainland at a time when sliding economic growth and defaults are making investors nervous. Even a modest increase in non-performing loans would have a significant impact on Hong Kong bank profits, suggesting the sector will be a sensitive indicator of China’s debt markets in the year ahead.

A landmark domestic bond default earlier this month and headlines of bankruptcies – highlighted last week by Zhejiang Xingrun Real Estate Co – have underscored concerns that an unprecedented surge in company debt in China is now showing signs of unraveling. “The quality of these loans extended by Hong Kong banks to Chinese companies has not been tested,” said Mirza Baig, head of foreign exchange and interest rate strategy at BNP Paribas in Singapore. “That is a concern in the backdrop of the rapid rise in exposure.”

Foreign bank claims on China hit $1 trillion last year, up from nearly zero 10 years ago, Bank of International Settlements data shows. The biggest portion of that is provided by Hong Kong, according to analyst estimates of the BIS data. The $430 billion in loans outstanding represents 165% of Hong Kong’s GDP, figures in Hong Kong Monetary Authority (HKMA) reports show.

Data from the HKMA, the city’s de-facto central bank, showed a similar astonishing rise. By the end of 2013, Hong Kong banks’ net claims on China as a percentage of their total loan book was nearing 40 percent, compared with zero in 2010. The rival financial center of Singapore has ramped up its China loans as well, but its exposure is the equivalent of 15% of its GDP, figures from its monetary authority show.

Local banks in both these centers have taken over lending that foreign banks once dominated, drawn by cheap funding rates following the global financial crisis, a voracious appetite from Chinese borrowers and healthy growth in the world’s second-biggest economy.

Read more …

• Bank of Japan Decision on Extra Easing Possible in May (Bloomberg)

The Bank of Japan could decide as soon as mid-May whether further stimulus is needed to keep inflation on track for its 2% target after a sales-tax bump next month, an adviser to Prime Minister Shinzo Abe said. “If the BOJ judges that the economy has fallen off its projected path, it will act appropriately and flexibly, and further easing is possible,” Etsuro Honda said in an interview at the Prime Minister’s Office in Tokyo yesterday. “I believe the BOJ will act if it sees changes in price expectations.”

While Honda, 59, said he’s become more confident the economy will withstand the higher levy as inflation expectations take root and price gains accelerate, the first indications of the extent of the blow will appear in May. Honda said he sees “considerable” room for the BOJ to boost the pace it buys exchange-traded funds should it deem more stimulus is needed. The economy is forecast to contract an annualized 3.5% in the three months from April, when the sales levy will rise to 8% from 5%. Abe is lifting the tax in an effort to rein in the world’s biggest debt burden, even as he tries to end 15 years of deflation with fiscal and monetary stimulus and steps to boost private-sector growth.

Read more …

• Bundesbank Opens The Door To QE Blitz (AEP)

The last bastion is tumbling. Even the venerable Bundesbank is edging crablike towards quantitative easing. It seems that tumbling inflation in Germany itself has at last shaken the monetary priesthood out of its ideological certainties. Or put another way, the Pfennig has dropped that euroland is just one Chinese shock away from a deflation trap, an outcome that would play havoc with the debt dynamics of southern Europe, render the euro unworkable, and ultimately inflict massive damage on Germany.

Bundesbank chief Jens Weidmann was not exactly panting for QE in comments to Market News published this morning, it has to be said, but the tone marks a clear shift in policy. “The unconventional measures under consideration are largely uncharted territory. This means that we need a discussion about their effectiveness and also about their costs and sideeffects”, he said. “This does not mean that a QE programme is generally out of the question. But we have to ensure that the prohibition of monetary financing is respected”.

At least we can put to rest the bogus argument that EU Treaty law (Article 123) prohibits QE by the European Central Bank. This claim was always a smokescreen. Bond purchases are what used to be known as open market operations, a tool of central banks dating back into the mist of monetary history. Purchasing bonds across the board (not just the bonds of insolvent states) is a plain vanilla liquidity management tool.

Mr Weidmann says he prefers negative interest rates as the first resort. This is an admission that the ECB is alarmed by the strength of the euro as it hovers near the pain barrier of $1.40, since negative rates are a sure-fire way to drive down the currency. “If you wanted to counter the consequences of a strong appreciation of the euro for the inflation outlook, negative rates would, however, appear to be a more appropriate measure than others”, he said. Quite so.

Read more …

• ECB Bank Stress Tests Hit Legal Blind Spot (BusinessWeek)

The European Central Bank will soon find out how hard it can be to keep a secret. The ECB’s plan to keep its health check on euro-area lenders under wraps until the completion of a stress test in October could be undermined by national rules requiring disclosure far sooner. Domestic regulators may order banks to tap the market immediately if an Asset Quality Review ending in July shows they need more capital, according to law firms including Clifford Chance LLP.

The risk is that market volatility could rise if multiple announcements cast doubt on the ECB’s control of a process designed to clean up balance sheets. Officials from the 128 lenders in the appraisal are meeting supervisory staff in Frankfurt today for an update on the Comprehensive Assessment, which includes both the AQR and the stress test. The ECB has said the exam will be more credible than previous efforts to restore trust to the financial system.

“This is the biggest blind spot in the ECB’s program,” said Nicolas Veron, a fellow at the Bruegel institute in Brussels and the Peterson Institute for International Economics in Washington. “The banks are still subject to national law, and it’s not clear to me that the ECB had fully integrated this into their planning for the Comprehensive Assessment. They don’t seem to have a very clear stance.” The ECB has said the AQR and stress test are related stages in a single exercise and there will be no partial reporting of results before the process finishes in October. The central bank will become the euro area’s bank supervisor on Nov. 4.

Read more …

• Mirage of the ‘new economy’ (Caixin)

The current Internet boom, centered around social networking, e-commerce and online gaming, has not produced a significant productivity boost for the economy and likely will not in the future. The boom is mostly about redistributing existing demand from offline to online. As most hot businesses have gained market share with cheap financing and without profit, it is doubtful that the demand re-slicing is entirely due to a more efficient channel of distribution. Cheap financing, i.e., a liquidity bubble, may have been the main engine for the Internet boom.

The bubble may not inflict much damage on its own because the amount of financing is small relative to the overall size of investment in the global economy. The danger to China is that it offers false hope that it can revive the economy. The false hope becomes an excuse not to implement painful structural reforms. If one envisions a rising tide to lift the economy ahead, where is the incentive to reform?

How a product is sold is insignificant compared to the product itself. Steve Jobs had the iPhone to sell. Whether the phones are sold online or through posh Apple stores is not important. A sustainable economy is based on businesses that make better products at lower costs over time. An economy full of colorful middlemen and no unique or high-value products cannot go far.

China’s only path forward is to increase efficiency on the supply side and shift the savings to the household sector as an increase in real purchasing power. This requires major reductions in government and state-owned enterprise spending, and boosting competition by eliminating government-approved market access. A necessary condition is for the high-yield debt bubble to burst.

Read more …

• Brazil at risk of recession as S&P downgrades debt to near junk (AEP)

Brazil’s sovereign debt is one step away from junk after Standard & Poor’s downgraded Latin America’s powerhouse economy, prompting a furious reaction from the Brazilian treasury. The rating agency cut Brazil’s debt one notch to BBB-, citing “fiscal slippage”, bad economic management, and one-off tricks that flattered the public accounts. It warned of a widening trade deficit and weak growth for years to come.

Marcelo Carvalho from BNP Paribas said the former darling of the BRICs quartet is staring “down the barrel of a recession”, a viewed echoed on Tuesday by Mark Mobius from Templeton Emerging Markets. The economy escaped recession with a rebound in the fourth quarter but has relapsed this year as punitive borrowing costs exact their toll. Carlyle Group had to inject $67m this month into its Urbplan real estate venture as unsold malls and commercial projects build up in the major cities. Rental prices fell 15% in Sao Paulo last year.

Marcelo Ribera from the hedge fund Pentagono Asset Management in Brazil said the country’s “decade-long bubble” has burst, warning that the real is likely to fall by 40% against the dollar as the excesses are purged from the system. Brazil, Russia, and Turkey are each on the brink of recession after tightening monetary policy to defend their currencies. All three neglected reforms during the boom years and now face much harsher global conditions as the US Federal Reserve turns off the spigot of dollar liquidity.

Brazil’s authorities rejected S&P’s claims as completely “unfounded”, insisting that the country has a primary budget surplus of 1.9% of GDP, “one of the highest in the world”. The downgrade is a harsh blow for President Dilma Rousseff as she prepares to host the World Cup and braces for elections this year, though the government is unlikely to change policy. S&P said Brazil has yet to feel the full impact of a 350 basis point rise in interest rates. Yields are now an eye-watering 13%, or 7% in real terms. This has sucked in a rush of foreign money but at a high economic cost.

Brazil has come down to earth with a thud after the glory days of the commodity boom, when the economy seemed near take-off as the top supplier of iron ore and grains for China. It became a textbook case of the “Dutch disease”, suffering from an overvalued currency that “hollowed out” core industry. Industrial output is barely higher today than in 2008, a picture more like Italy than an Asian tiger.

Neil Shearing from Capital Economics said private sector credit has soared by over 40 percentage points of GDP in a decade, the third most extreme case after China and Thailand. This sort of increase is often the precursor for banking crises in emerging markets. “The lessons from history are ominous. The fall-out tends to be especially painful when lending is funded by borrowing from overseas and denominated in foreign currencies”, he said. “This is a particularly toxic combination since, when the bubble bursts, investors tend to pull the plug, exchange rates collapse and the local currency cost of servicing debt jumps. This in turn causes default rates to soar and the economic downturn to deepen.”

Read more …

• Ukraine Only Has Enough Gasoline For A Month (Zero Hedge)

Nothing to see here, move along. While it appears the Russians are willing to pay the price of modest sanctions from the west to ‘liberate’ their fellow countrymen, the fallout from further tension with Ukraine could “boomerang” once again on the divided nation. As RBC Ukraine reports, the Minister of Energy and Coal Industry Yuriy Prodan said at a press conference today that “oil reserves will last for 28-29 days” in Ukraine. After that, the negotiation begins as Ukraine already owes billions for previously delivered gas – as Ukraine’s storage levels more than halved in the last 3 months.

Via RBC Ukraine,

Stocks of petroleum products in Ukraine will last for 28-29 days, said at today’s press conference, the Minister of Energy and Coal Industry Yuriy Prodan. “Speaking on the situation with oil, then ensure there is quite stable. Today oil reserves will last for 28-29 days,” – he said, the ” RBC-Ukraine . ”

At the same time, the Minister noted the significant risk reduction in the supply and rising gas prices. As of March 25, 2014 in Ukrainian underground gas storage facilities located 7 billion cubic meters of gas. “Up there can be about 2 billion is not the quantity that scares experts, it would be possible to hold only a week. It all depends on what kind of regime will be whether we can take about 20 million cubic meters. Meters of gas to reverse and so on “- said Prodan.

According to the company “Ukrtransgaz” abnormally warm winter 2013 2014 has reduced gas extraction from underground storage by an average of 37% compared to the same period last year: it was 60 million cubic meters per day. In late December 2013. occupied at the time the post of Minister of Energy and Coal Industry of Edward Stawicki reported that Ukrainian gas reserves in underground storage is 16.5 billion cubic meters.

We suspect any further military intervention will only crimp this supply even faster.

Read more …

• Lithuania Pleads For US Gas Exports To Counter Russia (BBC)

Lithuania’s energy minister has called on the US Senate to speed up the export of natural gas to Europe. Jaroslav Neverovic said that Lithuania was being forced to pay a “political price” for being entirely dependent on Russian gas supplies. The crisis in Ukraine has led to calls for the US to ease its current restrictions on gas exports. Some analysts have suggested that doing so would help challenge Russia’s dominance in the sector.

In his statement to a US Senate committee, Mr Neverovic urged members to do everything within their power to release natural gas resources “into the world market”. “A law enacted in your country some 75 years ago denies us access to your abundant and affordably priced energy resources,” he said. The energy minister said customers in Lithuania were having to pay 30% more for natural gas than other European nations, because they were “beholden to a monopolistic supplier.” “This is not just unfair,” said Mr Neverovic. “This is abuse of monopolist position.”

The crisis in Ukraine has seen the US and European Union impose sanctions targeting members of the Russian political elite. They have had their European and US assets frozen, and travel bans have been put in place to restrict their movements. However, some analysts have argued that these moves are symbolic and any sanctions would only work if they impacted the wider Russian economy.

Read more …

• Milk Row Threatens To Sour Greece’s Latest Bailout Deal (Reuters)

Greece’s government risks another rebellion over bailout terms this week after milk producers lobbied against a move to free up prices as part of efforts to make the economy more competitive. The country’s international lenders want it to ditch rules, such as limiting the shelf life of fresh milk to five days, that effectively deter importers. But Greek dairy producers and lawmakers representing farming constituencies are fighting the move to call milk up to 11 days old ‘fresh’ – the latest in a long line of last-minute disruptions to Greece’s bailout reviews with the European Union and International Monetary Fund.

Six lawmakers from within the ruling coalition – three from Prime Minister Antonis Samaras’s New Democracy party and three from the Socialist PASOK – have opposed the proposal that will be submitted to parliament on Friday as part of an omnibus reform bill that Greece must pass to secure bailout aid. If they vote against it, Samaras and PASOK leader Evangelos Venizelos could be forced to expel them, further reducing the government’s slim majority of just 153 seats in the 300-seat assembly.

The bill – which will pave for the way for up to 10 billion euros ($14 billion) of aid – is expected to pass after last-minute wrangling, but the row has highlighted how powerfullobbies can undermine the country’s bailout lifeline. “You don’t need to be an expert to understand that extending the shelf life is aimed at allowing milk from abroad to be labelled as fresh,” PASOK lawmaker Mihalis Kassis told Greek radio at the weekend. “If that’s a prerequisite by the (EU/IMF) troika then we deserve what we get.”

Read more …

• U.S. Farmers Mark Spring by Planting GMO Corn Banned in China (Bloomberg)

Archer-Daniels-Midland Co. and Bunge Ltd. , two of the world’s largest grain traders, are facing a new obstacle in their quest to expand corn exports to China – U.S. farmers. Six months after China began rejecting shipments of a genetically modified corn, Bunge says it won’t take deliveries of the variety developed by Switzerland’s Syngenta AG. ADM will test the corn and may reject it as well. Even so, farmers will soon begin planting it this spring, more interested in its high yield for the domestic market than for exports.

Exporters and farmers going in two different directions on GMO corn underscores a new set of challenges faced by international agricultural commodity traders. Even as demand continues to grow in line with the global population, China and other countries have been slower than the U.S. to approve new types of crops amid concerns about food safety and threats to biodiversity from genetically modified organisms, or GMOs. China’s curbs on some modified corn threaten to block millions of tons of imports and in so doing cut into the profits of international trading houses.

“It’s a significant issue for major North American traders,” said Andrew Russell, a New York-based analyst for Macquarie Group who recommends buying ADM and Bunge shares. “Anything that puts Chinese growth potential at risk is a significant issue.” Traders rerouting shipments originally destined for China to other markets may lose $30 to $50 a ton, said Tim Burrack, an Iowa corn and soybean farmer who’s also the former chairman of the U.S. Grains Council’s trade committee.

China may also be motivated by wanting to protect domestic corn prices after a record harvest, said Burrack, 62. “When China needs corn imports, they will ramp up the approval process.” White Plains, New York-based Bunge isn’t buying the Syngenta GMO corn, an insect-repelling variety called Agrisure Viptera, or another modified variety from the Swiss company called Agrisure Duracade. ADM, the world’s largest corn processor, said in a Feb. 21 statement it won’t accept Duracade until the GMO is approved by China and other major importers. And the company remains uncommitted to Viptera.

Read more …

• The Priciest Baseball Park in the Whole Atlantic Ocean (Bloomberg)

Something odd happens to the neighborhood around Marlins Park, Miami’s new $650 million baseball stadium, when you overlay 21st-century sea-level rise projections. It sinks below the waterline. It’s a shame. The park has a retractable, cloud-white roof to shield players and spectators from the summer sun. It recycles, sips energy and water, and is plugged into public transit. It has 27 flood gates, and was built one foot higher than floods are supposed to reach in once-in-500-year storms. The total, publicly financed package, with debt servicing, could cost Miami $2.4 billion by 2049.

If the Atlantic inches in as projected, eventually it might not matter how many flood gates there are. Oceans are swelling as they absorb heat, and ice sheets in Greenland and Antarctica have been melting faster since the early 1990s. Sea-level rise estimates for later this century have been revised upward, to a global average of a foot and a half to three feet by 2100, without aggressive carbon-cutting, according to the Intergovernmental Panel on Climate Change.

South Florida is a national leader in understanding the changing world. But politics and even policy change much more quickly than bureaucracy. That makes Marlins Park a symbol for cities in transition, a future relic from a time when the people who could build really cool things worked more or less independently from the people who monitored how fast the seas were rising.

The same potential problem exists wherever cities are laying down infrastructure expected to last into the second half of the century. Boston’s “Big Dig” highway project, a generation in the making, wasn’t driven by late 21st-century storm surge considerations. Oil and gas platforms in the Gulf of Mexico have never been built with permanent sea-level rise in mind. Another newish baseball stadium, Nationals Park, stands yards from Washington’s Anacostia River. Marlins Park checked enough LEED boxes to make it “the most sustainable stadium in Major League Baseball,” according to the team’s website.

Green building standards became common before a city’s ability to bounce back from large-scale shocks, or resilience, surfaced as a popular idea. The U.S. Green Building Council (USGBC) developed its widely used LEED building practices to promote efficiency in the use of energy, water and materials, and other practices related to construction, safety and maintenance; not necessarily to help people live through some of the charms that might await us in a hotter world — extreme heat, stronger storms and encroaching seas, to name three.

Read more …

• IPCC Report Downplays Economic Impacts Of Climate Change (SMH)

An upcoming United Nations report on climate change has been altered after the expert review stage, with changes added that downplay the economic impacts of a warming planet, according to one of the reviewers. Bob Ward, an expert reviewer for the Intergovernmental Panel on Climate Change, also said alterations to the economics chapter of the draft report sent to governments included an assessment of a paper by the chapter’s own convening lead author Richard Tol that contained at least one error.

An added section also included a line likely to be hotly contested if it survives a final review by IPCC delegates gathered this week in Yokohama, Japan, to approve the Working Group II report: “Estimates agree on the size of the impact (small relative to economic growth) but disagree on the sign.” Mr Ward said disagreement over whether the sign of climate change’s economic impact is positive or negative “is patently not supported by the evidence presented”.

Of the data assessed, only one study out of about 18 suggests there would be a significant positive impact on gross domestic product from global warming, Mr Ward told the IPCC in an email seen by Fairfax Media. Earlier analysis of economic costs by one of the assessed papers – by Professor Tol – also “excluded a long list of important impacts, including those relating to recreation, tourism, extreme weather, fisheries, construction, transport, energy supply and morbidity,” said Mr Ward, who is also a policy director at the London School of Economics.

Professor Tol, who is a professor at University of Sussex in the UK, said Mr Ward’s complaints were reviewed “and found that most of them were unfounded”. One typo was identified and a dropped minus sign was re-instated. “Both errors have been corrected,” Professor Tol said. In a paper published last year, Professor Tol stated that “the impact of a century of climate change is roughly equivalent to a year’s growth in the global economy,” and that “carbon dioxide emissions are probably a negative externality”.

Professor Tol is a member of the academic advisory council for The Global Warming Policy Foundation, a climate change sceptic think tank founded by the UK’s Lord Lawson. The council also includes prominent Australian sceptics Bob Carter and Ian Plimer, according to its website. Unless resolved in the final week, a row over the contents of UN report may cast a cloud over some of its major findings, which include the prospect of widespread social dislocation of climate change and big impacts for eco-systems such as Australia’s Great Barrier Reef.

Read more …

• Climate Change: The Debate Is About To Change Radically (Telegraph)

The latest report from the UN’s Intergovernmental Panel on Climate Change (IPCC) is due out next week. If the leaked draft is reflected in the published report, it will constitute the formal moving on of the debate from the past, futile focus upon “mitigation” to a new debate about resilience and adaptation.

The new report will apparently tell us that the global GDP costs of an expected global average temperature increase of 2.5 degrees Celsius over the 21st century will be between 0.2 and 2%. To place that in context, the well-known Stern Review of 2006 estimated the costs as 5-20% of GDP. Stern estimates the costs of his recommended policies for mitigating climate change at 2% of GDP – and his estimates are widely regarded as relatively optimistic (others estimate mitigation costs as high as 10% of global GDP).

Achieving material mitigation, at a cost of 2% and more of global GDP, would require international co-ordination that we have known since the failure of the Copenhagen conference on climate change simply was not going to happen. Even if it did happen, and were conducted optimally, it would mitigate only a fraction of the total rise, and might create its own risks. And to add to all this, now we are told that the cost might be as low as 0.2% of GDP. At a 2.4% annual GDP growth rate, the global economy increases 0.2% every month.

So the mitigation deal has become this: Accept enormous inconvenience, placing authoritarian control into the hands of global agencies, at huge costs that in some cases exceed 17 times the benefits even on the Government’s own evaluation criteria, with a global cost of 2% of GDP at the low end and the risk that the cost will be vastly greater, and do all of this for an entire century, and then maybe – just maybe – we might save between one and ten months of global GDP growth. Can anyone seriously claim, with a straight face, that that should be regarded as an attractive deal or that the public is suffering from a psychological disorder if it resists mitigation policies?

The 2014 Budget recognised reality, with the Government now introducing special measures to keep energy prices low for energy intensive firms – abandoning what little pretence remained that it was attempting to prevent climate change by limiting energy use so as to limit CO2 emissions. The new IPCC report – though it remains as robust as ever in saying that there will be climate change and its effects will be material (points that relatively few mitigation policy sceptics deny) – has a marked change of focus from the 2007 report.

Whereas previously the IPCC emphasised the effects climate change could have if not prevented, now the focus has moved on to how to make economies and societies resilient and to adapt to warming now considered inevitable. Climate exceptionalism – the notion that climate change is a challenge of a different order from, say, recessions or social inclusion or female education or many other important global policy goals – is to be down played. Instead, the new report emphasised that adapting to climate change is one of many challenges that policymakers will face but should have its proper place alongside other policies.

Quite so. It has been known since the late 1970s that there would be material warming during the 21st century and we will need to adapt to it. At present, though, in the UK we still carry the legacy of a panoply of enormously expensive but futile policies that were designed to be pieces of a global effort to mitigate that is just not going to happen. Our first step in adapting to climate change should be to accept that we aren’t going to mitigate it. We’re going to have to adapt. That doesn’t mean there might not be the odd mitigation-type policy, around the edges, that is cheap and feasible and worthwhile. But it does mean that the grandiloquent schemes for preventing climate change should go. Their day is done. Even the IPCC – albeit implicitly – sees that now.

Read more …

• Global warming poses risks, but also opportunities: IPCC (AP)

Along with the enormous risks global warming poses for humanity are opportunities to improve public health and build a better world, scientists gathered in Yokohama for a climate change conference said Tuesday. The hundreds of scientists from 100 countries meeting in this Japanese port city are putting finishing touches on a massive report emphasizing the gravity of the threat the changing climate poses for communities from the polar regions to the tropics.

“Although it focuses on a whole analytical and sometimes depressing view of the challenges we face, it also looks at the opportunities we face,” said Christopher B. Field, the co-chair of the Intergovernmental Panel on Climate Change. “This can not only help us to deal with climate change but ultimately build a better world.”

Japan’s awareness of the severity of climate change has been driven home by record temperatures of over 40 C , and in Yokohama, by unusually heavy snows this winter, said the environment minister, Nobuteru Ishihara.

Japan plans to release an adaptation plan of its own by the summer of 2015 that would focus on a more “eco-friendly lifestyle,” he said. That includes improvements in energy efficiency ahead of the 2020 Tokyo Olympic games.

“We aim to take full environmental consideration so that the Tokyo Games will be the ‘environmental Olympics,’” Ishihara said.

Japan is struggling to rein in its own emissions of greenhouse gases after it shut down its nuclear plants following the disaster in Fukushima after the March 2011 earthquake and tsunami. Increased burning of natural gas, coal and oil to compensate for lost generating capacity have undone much of the progress the country had made in cutting carbon emissions.

While each region faces its own mix of challenges, research conducted by thousands of scientists around the world underscores the need for urgent measures, J. Lengoasa, deputy head of the World Meteorological Organization, said in a recorded message to Tuesday’s meeting.

He said countries in Africa already spend $7 billion to $15 billion a year on climate adaptation. “Time is running out. We must take action,” he said. “It is our obligation and our duty to inform the world of the prospects and risks that lie ahead.”

Read more …