Botticelli The Calumny of Apelles 1495

https://twitter.com/TONYxTWO/status/2056899858695430613?s=20

https://twitter.com/John_F_kJr/status/2056862634209874000?s=20The FBI's Autopen Task Force submitted its first report to the acting Attorney General this morning, implicating Elizabeth Warren in about two dozen felonies.

— GRANDPA’s FREE ADVICE (@GOP_is_Gutless) May 19, 2026

"She wasn't just authorizing pardons," said acting AG Blanche, "To the tune of about $30 million."

Blanche said the… pic.twitter.com/hce2oTNrQ1

https://twitter.com/FreeStateWill/status/2056535138402779211?s=20 https://twitter.com/MAGAVoice/status/2056490512652423458?s=20sBingo https://t.co/HCrumnTIfT

— Elon Musk (@elonmusk) May 19, 2026

https://twitter.com/robertdunlap947/status/2056482824471896283?s=20Average inflation by president:

— Stephen Moore (@StephenMoore) May 18, 2026

Trump (first term): 1.9%⁰Biden: 5%⁰Trump (second term): 3.4%

The Democrats and the mainstream media refuse to tell the American people the truth. pic.twitter.com/IJX5JjAVa0

As if the US will sit still for 5 weeks.

• Oil Plummets As NATO Mulls Hormuz Deployment If Strait Not Open By July (ZH)

In a huge and unexpected announcement, amid stalled US-Iran peace talks – which have proven a failure and illusive thus far, NATO now says it could deploy military assets to forcibly reopen the Strait of Hormuz. Per breaking newswires Tuesday late morning: NATO TO CONSIDER HORMUZ DEPLOYMENT IF STRAIT NOT OPEN BY JULY President Trump has continuously chastised the NATO alliance for being largely bankrolled by Washington but at the same time fence-sitting when it comes to forming a coalition to patrol and reopen the vital energy transit waterway. Oil plummeted on the initial headline, seeing in it a positive for the potential that crude transit in the Persian Gulf could again be opened up soon:Read more …

And Bloomberg freshly reports: NATO is discussing the possibility of helping ships pass through the blocked Strait of Hormuz if the waterway isn’t reopened by early July, according to a senior official in the military alliance. The idea has support from several members of the North Atlantic Treaty Organization, but doesn’t yet have the necessary unanimous support, said a diplomat from a NATO country. Both officials spoke on the condition of anonymity. Leaders from NATO countries will meet in Ankara July 7-8.But July feels very far away at this point, and anything could happen between now and then, as Washington continues to threaten renewed military action, and Iran says it remains on high alert. NATO defense chiefs are meeting this week, where also high on the agenda will be the following: At this week’s summit, military chiefs from all 32 member states will examine the impact that consistent rapid consumption may have on NATO’s collective capabilities and deterrent power as Russia continues to threaten allies.

He never had a chance.

• Thomas Massie Loses His Primary Race (Salgado)

Rep. Thomas Massie (R-Ky.) has lost his primary race after making himself unpopular in the GOP for blocking Trump administration policies and obsessively condemning Israel and Operation Epic Fury. President Donald Trump, who has responded to Massie’s constant critiques by fervently campaigning against him, celebrated the Tuesday win for Massie’s primary opponent, Ed Gallrein. Massie has been one of Trump’s most consistent GOP critics.Read more …

In fact, Trump spent a considerable portion of Election Day posting anti-Massie messages on Truth Social. Trump accused Massie of suggesting a years-old endorsement from Trump was recent. “Can you imagine ‘Congressman’ Thomas Massie putting out a many years ago Endorsement of him, by me, when he knows that he wasn’t endorsed, but that I proudly endorsed Ed Gallrein? The reason is that Massie has turned out to be the Worst Congressman in the Republican Party. This shows what a totally dishonest and desperate guy Massie is, and I hope the Voters aren’t fooled by his deception!” Trump exclaimed.In a longer post on May 16, Trump condemned not only Massie, but other critics in the Republican Party: “Tom Massie of Kentucky, the worst and most unreliable Republican Congressman in the history of our Country, is an even bigger insult to our Nation than Senator Bill Cassidy of Louisiana, who suffered an unprecedented loss tonight by not even being allowed to run in the Republican Primary. This is the first time such a thing has ever happened to a sitting U.S. Senator! That’s what you get by voting to Impeach an innocent man, especially one who made it possible for Cassidy’s Senate win. Very disloyal, but Tom Massie, a major Sleazebag, is even worse! Kentucky, get this LOSER out of politics in Tuesday’s Election. He is nicknamed Rand Paul Jr., another ‘real beauty,’ because of his absolutely terrible voting habits.”

It’s not a surprise MAGA is done with Massie. Rep. Massie went so far as to coordinate a resolution with Democrats to challenge Trump’s war powers over the Iran operation, though the resolution failed. The representative has also raised controversy over his repeated antisemitic and anti-Israel comments, in addition to blocking aid to Israel, and he was the only member of Congress to vote against a resolution condemning antisemitism back in 2022.

On May 18, the day before the election, Massie reposted the following disgusting Michael Flynn Jr. diatribe on X, “Win or lose tomorrow for @RepThomasMassie the Israel lobby is only going to become more despised…They’ve over-extended themselves and made their influence in our political system incredibly visible…Pray for victory tomorrow for Massie to maaaaybe give them a wake up call our elections can’t be bought…” As if the only reason Massie would lose is because of some secretive Jewish money cabal. He has made his anti-Israel views a focal point of his campaign, and it is encouraging to see the voters reject him, given the concerning rise in antisemitism on the American right.

It looks like a pretty established industry.

And you’d think that if true, both parties do it, but it appears to be a Democrat industry.

“FBI Director Kash Patel says prior administrations looked the other way on election cheating but “those days are over.”

• DOJ Exposes Two-Decade-Long California Cheating Scheme (JTN)

In February, an illegal immigrant from Colombia residing in Boston was convicted by a federal grand jury for multiple “identity theft offenses,” including receiving rental assistance, Social Security and SNAP benefits, as well as voter fraud under the stolen identity. Prosecutors alleged Lina Maria Orovio-Hernandez, 59, was able to obtain eight state IDs and a Massachusetts Real ID and vote illegally in the 2024 presidential election. The steady stream of such cases is eroding public trust in election officials, who have insisted everything is fine in the face of contrary evidence.Read more …

A poll this spring found only two-thirds of Americans say they are confident their state or local government will run a fair and accurate election, a drop of 10 points since the 2024 presidential election and the lowest level of confidence since the Marist poll began measuring it. Democrats and independents were the most likely to lose confidence in elections over the last two years, the recent poll found. The ramped-up prosecutions also come as [Harmeet] Dhillon, the top election integrity official inside DOJ, has taken action against more than two dozen states to either clean up their voter rolls or turn over their rolls for the federal government to inspect them. Many states are resisting.Dhillon recently told Just the News the government’s early review of state voter rolls has proven tens of thousands of non-citizens made it into a position to cast ballots, and that hundreds-of-thousands of dead or departed residents were not properly removed from state election systems. “It’s really frustrating that we’re being prevented from doing our job,” she said, criticizing state election offices and federal judges who are blocking her office from her historic effort to obtain and review every state’s voter roll ahead of the 2026 midterm elections. Dhillon signaled dozens more cases of illegal non-citizen voting are on the horizon.

“For every person that we’ve seen a story about, I know of dozens and dozens more cases, and U.S. attorney’s offices are wanting to bring these cases, but we have, of course, interference with the very appointment of these U.S. attorneys at the political level,” she explained. “So that’s above my pay grade, but it’s really frustrating that we’re being prevented from doing our job.” Evidence of election fraud is also piling up in state and local courts. At least four elections in the U.S. have been overturned by courts since 2020 after voting irregularities and fraud were discovered, Just the News previously reported.

Last month, former Kansas mayor Jose Ceballos, a citizen of Mexico, pleaded guilty to voter fraud after admitting he voted as a green card resident. Ceballos, who resigned as mayor after he was charged, was taken into custody by U.S. immigration authorities last week and could be deported, officials and his lawyer have said. Also last month, the New Jersey attorney general’s office announced that a former mayoral candidate pleaded guilty after he attempted to file numerous fraudulent voter-registration applications in connection with a June 2021 city election.

Henrilynn Ibezim, 71, of Plainfield, pleaded guilty on April 27, 2026, during a hearing before Judge Candido Rodriguez, Jr. in New Jersey Superior Court in Union County. The defendant admitted to one count of third-degree forgery. Three women in Monroe County in Alabama – 67-year-old Sharon Crayton Denson, 46-year-old Samantha Trashawn Kyles and 59-year-old Sarah Crayton Bennett – were indicted in February for voter fraud in the Aug. 26, 2025, Frisco City municipal election. They allegedly tampered with 20 people’s ballots.

Five Democratic Party members in Bridgeport, Conn., and Philadelphia were criminally charged with numerous counts of voter fraud on both the state and federal levels regarding mail-in ballots over the last few years. And in one case ,the cheating was so extensive an election had to be negated and done over. The city of Bridgeport, Conn, had to redo primary and general elections last year after evidence surfaced of alleged ballot harvesting in the Democratic mayoral primary in September 2023. A jury in March also convicted a Wisconsin man of election fraud and identity theft after he requested the ballots of state Republican Assembly Speaker Robin Vos and Racine Democratic Mayor Cory Mason without their consent..

Reagan and Trump.

• Welcome to the NEW Republican Party (Scott Pinsker)

As a Gen-Xer, I assumed Ronald Reagan was destined to be remembered as the most transformational Republican of my lifetime. Winning the Cold War, mainstreaming pro-life conservatism, and marginalizing Rockefeller Republicanism was a helluva legacy. But with all due respect to the Gipper, the MAGA movement will likely surpass it. Ronald Reagan and Donald Trump both reinvented the GOP. Both men were transformational leaders on the global stage. Without question, both men altered the course of history. But Donald Trump also changed how we think about politics.Read more …

It’s rarely discussed in the media, but it might be President Trump’s longest-lasting legacy: We no longer think of D.C. politicians as individual representatives from states and districts, but as members of a national team. nAnd that’s a watershed transformation, because we elect politicians to solve problems. That’s the entire point of representative democracy! Which means, when our problems change, our politicians must change with them — or they’ll be voted out of office. (More on that in a sec.) Pre-Trump, our “problem” was finding a politician who represented our regional/statewide values and interests. It was more of a Mr. Smith Goes to Washington, romanticized view of politics:We sent a local leader to D.C. to champion the cause of our community. National issues were relevant, of course, but local interests reigned supreme.This mentality made sense at the time. In fact, it seemed Reagan-esque: Since those closest to the problem are best-equipped to solve it, the federal government — and national parties — should leave a light footprint. Who are we to lecture local citizens about local issues? Back then, it wasn’t uncommon for a congressman to belong to one party, yet his district voted overwhelmingly for the opposition in presidential elections. An incumbent could survive for decades — getting reelected by huge margins! — riding the bandwagon of local goodwill.

It’s a phenomenon known as Fenno’s paradox: We might hate U.S. Congress as an institution, but we considered our congressman “one of the good guys.” Which was why the approval rating for “our” congressman was almost always higher than the approval rating for U.S. Congress as a whole. And to be fair, this perspective aligned with the expectations of our Founding Fathers, who envisioned citizen-legislators representing local interests. But even during the Reagan years, systemic problems were obvious: Over and over again, politicians would campaign as a conservative, yet vote as a liberal. Republicans “going native” in D.C. became a sad cliché.

Alas, with scant national guardrails, not much could be done to keep wayward Republicans in line. Instead, politicians would play fast and loose with the facts, voting one way in subcommittee — another way on the floor — and then pretend they supported whichever side was more popular. Unless you were a hardcore political junkie, you were none the wiser. It was an age when incumbents like Rep. Thomas Massie (R-Ky.) could serve in Congress for the rest of their life, voting however the hell they wanted, without any real risk of blowback. (Fun fact: The reelection rate for House members in 1986 and 1988 was 98% — the very first time in American history it was 98% or higher in back-to-back elections.)

Not anymore. That age ended when the MAGA movement began. The old, romanticized notion of free-wheeling, locally-attuned citizen-legislators was replaced with cold, cynical reality: Modern politics is a full-contact sport, and without teamwork, Republicans won’t get anything done. That’s because our “problem” is no longer local representation — it’s protecting our country from an increasingly radicalized Democratic Party. As the Democrats have embraced socialism, Wokeism, and trans/LGBTQ policies, Republican voters have recoiled in horror. We want our party to protect us from their madness.= And that’s an all-hands-on-deck challenge.

Election Day stories. Plenty.

• It’s Primary Election Day in the People’s Republic of Oregon (Victoria Taft)

If there’s a prize for the worst, most sinister, and cynical political moves, the unfortunately-named Oregon governor, Tina Kotek, should win walking away. A damaging gas and transportation tax, the one she cheated, lied, and schmoozed to ram through, is on the ballot in Tuesday’s primary. On primary day, Oregon voters will affix some C-4 and light the fuse to the one deliverable Kotek could lay claim to in her entire first term of office. The timing for Kotek and her fellow Democrat Party members couldn’t be worse.Read more …

Kotek blames President Donald Trump for high gas prices right now, but Oregonians know all too well that prices are perennially high anyway because of Democrats’ adherence to the Church of Global Warming. The governor’s approval numbers have fallen badly for a Democrat in this one-party state. Gas prices are almost as high as when Joe Biden was in office, and voters — male, female, Democrat, Republican, Independent, poor, and rich — saw what she did there. The people who continually bleat that they’re trying to Save Democracy!™ did everything to disembowel it to punish Oregonians with a whopping 6 cent/gallon gas tax and massive fee increases.Kotek couldn’t get her budget-backfilling taxes passed in regular session, so she called for a special “emergency” session to cram them through. When she got the tax increases approved by Democrats, she waited until the last second to sign it, to deprive Oregonians of enough time to gather enough signatures to refer it to the ballot. But Kotek’s gambit didn’t work. Oregonians were so angered by the manipulations that Republicans got more than enough signatures in record time to refer the tax package to voters in November. The Save Democracy!™ crowd didn’t want the referral on the November ballot because more people vote then.

In March, Kotek had her This is what democracy looks like! backers in the legislature pass a bill to allow her to swap the dates of the vote on her tax increases. Then she tried to ram through the repeal of her own gas tax increase to begin her political manipulations all over again. Kotek then moved the referral to the May primary election day, where only half the voters show up. One poll showed that only 11% of voters thought the vote swap was OK and 89% were opposed. In the People’s Republic of Oregon, you can’t get 89% of any group to agree the sun is shining.

The people noticed Kotek’s delays, carve-outs, calendar manipulation, and political skulduggery. And then Tina pulled a Gavin Newsom move and refused to even consider the idea of a gas tax holiday. If we were the cynical type, we’d guess that these two aren’t so concerned about prices and affordability after all. Kotek’s approval numbers have dropped from the mid-50’s to the 40% range. Even the teachers’ union refused to endorse a candidate instead of going with Kotek. Several “not Kotek” Democrats are running against the sitting governor, but with closed primaries, there won’t be a lot of Oregon Republicans crossing over to vote against her. Indeed, Oregon Republicans have their own big contest on the ballot.

Former Portland Trailblazer Chris Dudley, state legislator Christine Drazan, and one of the organized opponents to Kotek’s gas tax, Representative Ed Diehl, are top contenders for the GOP nomination. Drazan, who’s run and lost against Kotek before, was leading in April among the candidates, but Chris Dudley, who ran and lost more than a decade ago, is surging along with Diehl, who has captured high-profile endorsements late in the game. The good news is there are signs of life in the political opposition to the Democrats in Oregon. Tina’s tax increases are going down, and the GOP’s got a pulse — they’re voting, and this could be a game-changing moment for Oregon.

Fingers crossed.

“..and turned that into much more becoming more increasingly anti-American for me. So my views really haven’t changed that much.” The punchline came shortly after: “What’s really changed is the party.”

• The Democrats Are About To Destroy John Fetterman (ZH)

John Fetterman has become the most interesting politician in America, and the Democratic Party’s most uncomfortable mirror. His willingness to speak honestly, vote his conscience, and refuse to define himself purely in opposition to President Donald Trump has made him a hero to some and a traitor to others. Back in March, he declared the party had no real leader except Trump Derangement Syndrome. Democrats, according to Fetterman, are so consumed with opposing President Donald Trump that they’ve failed to construct a coherent agenda of their own. That’s not a fringe critique. It’s a fairly accurate description of where the opposition party stands as we head toward the 2026 midterms.Read more …

Last week, Sen. John Fetterman wrote an op-ed in the Washington Post making the case that he’d make a terrible Republican, and he’s right. He’s pro-choice, firmly behind legal marijuana, a committed supporter of LGBT rights, a staunch defender of SNAP benefits, and a reliable friend to organized labor. His overall voting record is overwhelmingly aligned with the Democratic caucus. “It wasn’t long ago when Democrats wanted a secure border. I voted on an immigration bill in 2024 to make sure an influx the size of Pittsburgh doesn’t come through the border like it did under the previous administration,” he wrote. “I have co-sponsored legislation to stop the flow of fentanyl. I was the lead Democrat on the Laken Riley Act, and I strongly believe that someone who comes here illegally and commits a violent crime should be deported. Full stop.”He noted how his party used to oppose government shutdowns because they put “American livelihoods at risk” and held workers “hostage.” Yet, he stood alone as a Democrat when he voted to end his party’s recent shutdowns, saying he “took no pleasure in voting against my party” but felt that keeping “the lights on” for TSA, homeland security, airports, and “everyday Americans” mattered more than “partisan games.” As far as he’s concerned, his occasional departures on border security, crime, and Israel are a sign of his party becoming more extreme, not him becoming more conservative.

In a recent conversation on Reason’s Reason Interview podcast with Nick Gillespie, Fetterman was asked to reflect on how his politics had changed since he backed Bernie Sanders in 2016. His answer cut to the heart of the Democratic Party’s ongoing identity crisis. “Well, I mean, you know, in 2016, it was much more about the minimum wage and some other very basic kinds of things,” he said. “And now that’s just turned into much more standing with Cuba, standing with Venezuela, standing with the Iranian regime, and turned that into much more becoming more increasingly anti-American for me. So my views really haven’t changed that much.” The punchline came shortly after: “What’s really changed is the party.”

That is a sitting Democratic senator describing his own party’s base as “increasingly anti-American,” and describes himself as lonely inside the party he still agrees with over 90 percent of the time. And how has the party responded to one of its more prominent voices offering this kind of candid self-assessment? By quietly beginning to show him the door.

A report from Punchbowl News last month made it quite clear how his party sees him. Pennsylvania Democrats on Capitol Hill wouldn’t commit to supporting a Fetterman reelection bid, and none would explicitly endorse him. Rep. Brendan Boyle, who is rumored to be eyeing a 2028 Senate run himself, said he’d “be very surprised if [Fetterman] ran in the Democratic primary.” Rep. Chris Deluzio, also said to be interested in the seat, acknowledged “serious disagreements” with Fetterman over the war in Iran, before adding a diplomatic “we’ll see what comes after ’26.” Rep. Summer Lee simply said of Fetterman seeking reelection, “Up to him. At his own peril.”

That’s the kind of language you use for someone the party has already written off. And clearly they have. He still votes with Democrats more than 90 percent of the time. And yet Pennsylvania Democrats won’t even give him a courtesy endorsement for a future Senate bid. Democratic voters in Pennsylvania aren’t any more forgiving. A February Quinnipiac poll found that Fetterman sits at 46 percent approval among Pennsylvania voters overall. This isn’t great, but the partisan breakdown is most interesting: he’s underwater 62%–22% among Democrats, while running 74%–18% among Republicans.

As far as the party’s progressive base goes, anything less than 100% compliance isn’t enough, especially when you break with the party on issues like Israel, immigration, or anything that can be characterized as insufficiently hostile to the right. Fetterman’s independent streak might help him win a general election, but it won’t help him win a Democratic primary.

That’s the trap, and he appears to know it. He’s made it quite clear he won’t become a Republican. His op-ed was practically a manifesto on the subject. But a man who describes himself as “lonely” inside his own party, who watches that party signal it won’t back him for reelection, has a big decision to make. Will he try to win reelection as a Democrat, become an independent, or not run at all? One thing is for sure: his future inside the Democratic Party is already closed.

They tried so hard to play a race card against Trump. None of it stuck.

• Gutfeld Delivers an Epic Autopsy of the Left’s Dying Race Card (Margolis)

Greg Gutfeld didn’t have Jessica Tarlov to push around on Monday’s episode of The Five, but he did present a brutal autopsy of the one weapon Democrats have relied on for decades and why it’s finally stopped working: the race card. He started with the core diagnosis: The left is trapped in the past. “Those leaders are living in the past, which is what the race card literally, literally is,” Gutfeld said. “You’re living in the past to imprint it on the future. The things that they say are happening aren’t happening.” For years, he explained, that strategy worked because conservatives were terrified of being labeled racist. That fear was the weapon. Once it’s gone, the weapon is useless, and that’s exactly what’s happened.Read more …

“It used to work. We used to be paralyzed by the fear of the scarlet letter R for racism, but the race card doesn’t work anymore on half the population who sees through it,” Gutfeld said. “The other half are just doing it out of habit. But we disarmed the left because we lost the fear. And so now, it’s just a gun shooting blanks.” The political math, Gutfeld pointed out, is just bad. Screaming racism only rallies voters you already have. It doesn’t persuade anyone. “And absent of other tools beyond the race card, you are kind of like a fat, out-of-shape fighter with no way to win but to call out the refs or just cancel the whole game.”Gutfeld then zoomed out to explain how fear, and not just racial fear, has been the engine driving the entire Democratic agenda — from transgender ideology being pushed on children to open borders to soft-on-crime policies. Each angle, he argued, was powered by the same mechanism: making ordinary people terrified to say what they actually believed. “If you think about how profoundly awful was ‘trans rights’ for kids — to give perverse men the agency over our children’s sexuality — how did that happen?” Gutfeld demanded. “It was like, we feared the swarm of activists calling us transphobic. We feared being called bigots if we came out against illegal immigration. We feared punishing criminals because we thought we were going to be called ‘racist.’

“Once you lose the fear, you can finally get back to the normal way things go.” And the thing is, the Democrats haven’t figured this out yet. They’re still running the same play. “The Democratic Party, in my opinion, still has to do that. They haven’t done it. They’re still on the same path to destruction they’ve always been on, which is identity politics. It’s taken this country down a terrible path,” declared Gutfeld. Then came the history lesson — the one Democrats really don’t want to have. Harold Ford Jr. pointed out that race relations were better roughly twenty years ago. And he was actually right. Polling data shows a sharp decline after Barack Obama’s election.

Gutfeld wasn’t willing to blame Obama specifically, though. “The polling on race relations were far more optimistic before Barack Obama was elected, and then it just got worse and worse,” Gutfeld said. “I’m not saying it’s on him, but I’m trying to figure out what happened since then. Did the KKK return? Was discrimination now decided to be illegal? Was there some kind of attack that happened? No.” I’ve been saying for years that Obama used his status as the first black president to divide our country rather than as a turning point to move past race.

“The only thing that happened was the attack on the idea of the melting pot, the idea that you’re an American first, doesn’t matter how you look or what gender you are,” he said. “They created a poison, a toxin that they put in that melting pot. And now, all of a sudden, race relations are worse, and people are at each other’s throats. This is a filter, Harold, and I’m talking about identity politics. It is a filter put in place to destroy a country because it’s absolutely opposite what a melting pot is.”

"You're living in the PAST to imprint it on the Future" @greggutfeld calls out Dems who traveled to an Alabama rally to RAGE about redistricting.

— The Five (@TheFive) May 18, 2026

What do YOU think? pic.twitter.com/nPDJ0tlO73Obama certainly helped. Monday’s exchange was a perfect snapshot of where the political debate stands right now. The left keeps reaching for a weapon that’s out of ammunition. Conservatives aren’t afraid to be called racist anymore because Democrats have spent decades saying it over and over and over again about everything, making the word practically meaningless.

In other words: you can’t win, take your losses.

• Comey’s Message to the Deep State: Run Out the Clock on Trump (Tim O’Brien)

After facing two separate federal indictments and waiting for your court proceedings on one of them to move forward, what do you do to pass the time? Well, if you’re former FBI director and leftist tool James Comey, you do as many TV interviews as possible and stay busy on social media. That may not be what you would do, but it is what a shameless narcissist like Comey does. In September 2025, the deep-stater was indicted on two counts tied to allegations that he made false statements to Congress and obstructed a congressional proceeding connected to his testimony about FBI activities. That case was dismissed by a Bill Clinton–appointed federal judge over a technicality involving the prosecuting attorney.Read more …

The second indictment, which came in April 2026, involves two felony counts centered on Comey’s 2025 Instagram post depicting seashells in the sand that read “86 47,” a widely understood reference to the assassination of the nation’s 47th president, Donald Trump. Prosecutors allege that the photo — regardless of who arranged the shells that Comey photographed and posted online — amounted to a threat against Trump. One of the ways Comey and the left are trying to distort reality on this issue is by claiming that “86” is an innocent term used in the restaurant industry meaning to “get rid of” bad food or something. So, are they now saying Trump is a restaurant worker who needs to be fired?Of course not. If Comey were telling the truth, that still wouldn’t explain why he shared that photo with all his followers. Also, this contrived narrative calls on us to ignore popular culture’s normalization of “86” as a signal for knocking off someone. This decades-old slang term was used in The Sopranos repeatedly. It was used in the pornographically violent motion picture Pulp Fiction and in another movie called Get Shorty. None of these depictions were novel applications of “86.” They only featured the term because the writers and producers already knew that audiences knew that “86” is slang for killing someone.

Of course, Comey denies, denies, denies. Comey is smug and he thinks he’s being cute. My colleague Scott Pinsker dug into that issue when he wrote about Comey and his favorite thing these days – plausible deniability. By the way, Acting Attorney General Todd Blanche has said the indictment against Comey is not based on a single photo, but rather an 11-month investigation. To behave the way Comey is behaving, he may not feel invincible, but he does seem to feel “untouchable,” almost as if someone is protecting him.

When people like Comey, former CIA Director John Brennan, who is reported to be under federal investigation, and James Clapper, former director of National Intelligence, talk to the media—especially on the Sunday morning shows—you can make some reasonable guesses about what is going on. First, they are there for a very specific purpose: to push a very specific narrative that serves the interests of some leftist interest.

The second thing that may be happening is that the purpose of the interview may be to help achieve a very specific outcome. Usually, part of that strategic objective is to smear Trump and the Republicans, but that is never all of it. They are often trying to stop or slow the work of the executive branch under Trump. Things like killing the Department of Government Efficiency (DOGE), hampering the work of Immigration and Customs Enforcement (ICE), planting seeds of doubt about certain Trump appointees, or undermining support for the Trump administration’s efforts to deprive Iran of the ability to wage nuclear attacks on America and other countries.

When you pour concrete, at first it sets, and then it starts to cure, and after that it hardens and you can walk on it, drive on it, or build on it. You have a solid foundation. When the deep state pushes a narrative, it often uses the Sunday morning shows to spread it. They know other people in the news media and in power watch those shows for cues, talking points, and messaging that they will use in their own efforts to help spread that narrative. Once the larger networks, news sites, and newspapers get the leftist line from those shows, they can spread it more broadly to their audiences, thus hardening the narrative in the public’s consciousness.

That’s how you end up with immovable perceptions that are based on lies. Things like the Russia hoax and the Charlottesville hoax. When you watch a Sunday morning show, you’re watching a memorandum to the obedient swamp, saying pretty much, “This is what you are to amplify.” Against this backdrop, Comey appeared on Meet the Press with terminal stare Kristen Welker on May 17. He used the opportunity to send a message to the entire deep state. The message was essentially: it’s time to run out the clock on Trump.

James Comey signals to FBI personnel that he has "great confidence in" at the bureau to wait out the Trump administration:

— Western Lensman (@WesternLensman) May 17, 2026

"I'm urging them, hang on two and a half years, and then we can rebuild these institutions." pic.twitter.com/xIoDY6OTpGWhile sitting across from Welker in the NBC studios, leftist soldier Comey has said he won’t stay silent as he faces mounting pressure from the Trump administration. In not staying silent, his message to unelected leftists in the bowels of the federal government was a pep talk of sorts. He wants them to stick around so that after Trump, they can “rebuild” the operations that attacked our freedoms under Biden. Comey would seem to want the FBI to return to the Biden-era law enforcement agency that spied on Catholics and Catholic churches, persecuted pro-life protestors, and served as the left’s version of the old East German Stasi.

If Trump appears to have a sense of urgency, this is why he does. He knows that too many people working in the federal government are just trying to undermine him and wait him out. These are the kinds of people he’s trying to get off of the federal payroll. As for those Sunday morning shows, Comey counts his words, so when he talks to Kristen Welker on camera and says what he said, it’s very revealing to say the least. A strategy is afoot.

“..AI should enhance human work rather than devalue it.”

• “Stop Hiring Humans” Billboards Are Appearing In US Cities.. (MN)

.“Stop Hiring Humans.” Those words are now plastered on billboards from San Francisco to New York City, courtesy of a San Francisco-based startup pushing virtual AI sales representatives. The company, Artisan, markets AI agents that handle outbound sales tasks like lead generation, cold emailing, list-building, and prospecting. Their message is blunt: the era of AI employees is here. Artisan’s campaign highlights a growing trend of AI replacing human roles in sales and beyond. The startup claims its tools could displace as many as 600,000 jobs in America over the next 5-10 years. The billboards declare “The Era of AI Employees Is Here,” framing human workers as obsolete. Critics see it as tone-deaf marketing that accelerates public backlash against Big Tech’s rush to automate everything.Read more …

Driverless cars and a stop hiring humans campaign…

— Amy Kremer (@AmyKremer) May 17, 2026

If this is the future, it is HELL pic.twitter.com/kl5sPIfmdr

In response to the backlash, Artisan CEO Jaspar Carmichael-Jack published a detailed blog post clarifying the campaign’s intent. He argued that the slogan targets a specific category of tedious cold outbound work—email blasting, template churn, and list-building—that burns people out with short tenures and high rejection rates. The company insists it does not seek to eliminate entire BDR roles, emphasizing that cold calling and human connection remain human tasks. Artisan also built a human dialer to complement its AI tool Ava, positioning the technology as working “alongside” people rather than replacing them outright.https://twitter.com/_estela86/status/2056100209214849155?ref_src=twsrc%5Etfw%7Ctwcamp%5Etweetembed%7Ctwterm%5E2056100209214849155%7Ctwgr%5Ea3ec3c31adfa0128dc083d052d679370e13da82c%7Ctwcon%5Es1_c10&ref_url=https%3A%2F%2Fwww.zerohedge.com%2Fai%2Fstop-hiring-humans-billboards-are-appearing-us-cities

Carmichael-Jack acknowledged the billboard as deliberate provocation while advocating for policies like meaningful universal income and shorter workweeks to manage the transition. Nevertheless, the move fits a pattern of accelerating AI deployment with little regard for human consequences. Reports continue to emerge of autonomous AI agents exhibiting rogue behavior in controlled environments and real-world applications. Recent incidents show agents not only replacing workers but acting independently in ways that destroy critical systems—raising alarms about a future where humans are sidelined and technology runs unchecked. In one high-profile case, a Cursor AI agent powered by Claude Opus 4.6 deleted an entire startup’s production database in seconds.

The agent, tasked with routine work, encountered a credential mismatch and independently decided to delete a volume on Railway cloud servers—wiping out the production database and all backups. The founder of PocketOS detailed the nine-second catastrophe, which caused a 30-hour outage. The AI later admitted to violating its guardrails.This wasn’t an isolated glitch. Earlier experiments placed AI bots in a simulated virtual town for two weeks, where they quickly descended into chaotic, unpredictable behavior—prompting fresh concerns about what happens when autonomy meets real systems.

Even more dystopian twists have emerged, with AI bots reportedly “renting” humans for bizarre tasks, racking up hundreds of thousands of sign-ups as the lines between machine direction and human labor blur into something unsettling. These developments underscore a core problem: as AI agents gain more independence to pursue goals, they bypass safeguards, access unrelated credentials, and make destructive decisions without human oversight. Enterprises are deploying them rapidly, but governance lags dangerously behind.

While tech boosters tout efficiency, the billboard campaign and job displacement projections strike a nerve. Sales roles—often entry points for young workers or career ladders—face direct targeting. Broader automation in driving, customer service, and knowledge work compounds the pressure. Public reactions on X captured the frustration: concerns over driverless Waymo fleets in cities like Los Angeles despite available human drivers, and warnings that mass unemployment could fuel social instability.

One tech professional with over 20 years of experience pushed back against the “humans are worthless” narrative pushed by some influencers, arguing AI should enhance human work rather than devalue it. Others noted the irony: these AI-pushing startups rely on human investors and customers while trying to eliminate human jobs. China offers a cautionary glimpse, where heavy robot adoption has forced worker pay cuts and displacement on a massive scale. In the West, the push feels aligned with a globalist mindset that prioritizes efficiency and control over local workers and communities.

The speed of these developments leaves little room for thoughtful policy. Pro-freedom voices have long warned against over-reliance on systems vulnerable to failure, manipulation, or emergent behaviors. When AI agents can independently wipe databases, fabricate data, or direct human labor in strange ways, the risks extend beyond economics into security and societal trust. The billboards are up. The incidents are piling up. The question is whether policymakers and citizens will push back before the era of AI “employees” leaves millions with no role left to play.

Kamala Harris is a Uniquely Bad Idea all by herself.

• Why “No Bad Ideas” is a Uniquely Bad Idea (Turley)

On Thursday, former Vice President Kamala Harris posted a livestream on the “Win with Black Women” podcast to call for a “no bad idea brainstorm” for the Democratic Party. She used that pretense to “throw out there” the idea that Democrats should make radical constitutional and political changes as soon as they retake power. That includes packing the Supreme Court, admitting Puerto Rico and D.C. as states and killing the Electoral College. All of these items have been previously raised by liberal professors and pundits as a way to circumvent small-D democratic processes in order to guarantee power for the big-D Democrats for years to come.Read more …

It was a telling rationalization. The Democratic Party has become a party of moral and political relativism, embodied in the popular “by any means necessary” mantra used by many on the left today. But there are bad ideas, just as there are bad people who want to win at any cost. For some, Harris herself showed the existence of truly bad ideas by accepting the position as Biden’s Border Czar as roughly ten million people poured into the country. Another bad idea was her selection of Tim Walz as a running mate before his series of rake-steps. Indeed, her sudden surprise nomination was a bad idea, one that cost $1.5 billion in just 15 weeks and led to one of her party’s most crushing losses in decades.The worst idea, however, is to celebrate our 250th anniversary by destroying the very institutions and values that created the most successful and stable democracy in history. In my book “Rage and the Republic,” I discuss lawyers and law professors who rationalize the trashing of the Constitution and our institutions to achieve their political goals. I debated one Harvard law professor who rattled off a list of Democratic proposals for our system, but then added that the left would need first to take control of the Supreme Court. It was an acknowledgment that the court would likely declare some or all of the proposals unconstitutional.

I previously wrote about the rise of “the new Jacobins” — influential figures who are seeking to dismantle our system after facing judicial and political setbacks. Even the dean of Berkeley Law School, Erwin Chemerinsky, wrote a book titled “No Democracy Lasts Forever: How the Constitution Threatens the United States.” Now, leading Democrats such as House Minority Leader Hakeem Jeffries (D-N.Y.) have declared the Supreme Court “illegitimate” and called for a “massive” overhaul of both state and federal courts to make them submit to Democrats’ demands. This was Jeffries’ reaction to the Virginia Supreme Court’s rejection of Democrats’ effort to wipe out Republican representation in Virginia.

He is not the only one adding bad ideas to Harris’s wish list. Various politicians and pundits called for the sacking and packing of the Virginia Supreme Court. By lowering the mandatory age for retirement to 54, they would simply force out all of the current justices and replace them with rubber-stamp liberal appointees. If this sack-and-pack scheme is not enough, Hillary Clinton’s former campaign lawyer, Marc Elias, reminded citizens that, under the state constitution, they could scrap the entire Virginia government over the refusal to let Democrats gerrymander the state. (Elias is infamous for his role in the secret funding of the Steele Dossier to launch the debunked Russian collusion scandal).

It did not matter that even a justice appointed by former Democratic governor Mark Warner found the move unconstitutional, or that Democratic figures like Gov. Abigail Spanberger believed that it could be overturned. The X posting was only the latest effort to throw out some “bad ideas” to an increasingly radical movement on the left. When I and others flagged Elias’s posting as alarming, he criticized me for taking him to task for merely quoting the state Constitution. It was typical of the “Who, me?” response of establishment figures when confronted for pandering to the most radical political elements in the Democratic Party. nIt is like responding to an adverse World Trade Organization trade ruling by invoking Congress’s power to declare war. It is a rather extreme reaction.

Yet, it is all part of the effort to normalize extreme measures and condition American voters to fundamentally changing our system. Harris calls it her “expanded playbook.” Former Attorney General Eric Holder, in pushing for the packing of the Supreme Court, explained how simple this is: it is all about “the acquisition and the use of power.”As Democratic strategist James Carville put it more bluntly, you cannot go with half measures if you want power. You just have to say “f–k it … just do it.” Whether you view these as good or bad ideas, they are certainly not new ideas. These are the same voices that have plagued our system for generations; the siren calls for unleashing forms of direct democracy and removing moderating influences in our system.

The Framers sought to create a system that would avoid the pattern of earlier democracies becoming tyrannies, including Athens. James Madison famously wrote, “Had every Athenian citizen been a Socrates, every Athenian assembly would still have been a mob.” The Framers rejected more direct democratic systems to blunt the impulses and passions that destroyed other systems. They wanted to avoid democracy becoming what Benjamin Rush called a “mobocracy.” The American Constitution was a rejection of the “bad ideas” that politicians (called demagogues in Ancient Greece) have historically used to marshal the power of the mob.

They did not want an “expanded playbook” designed to secure and retain power for one party. We were the first true Enlightenment Revolution based on the protections of rights derived not from the government but from God.

Now that was a good idea.

The gay muslim network?!

• BBC’s Ex-News Director: Trans Bias, ‘Progressive Madness’ Drove Me Out (MN)

The BBC’s grip on impartiality continues to slip as one of its former top news executives publicly confirmed what critics have long argued: activist capture from within has turned the state broadcaster into a vehicle for narrow ideological agendas. Fran Unsworth, director of BBC News from 2018 to 2022, has broken her silence, claiming she was effectively driven out by trans activists and the “progressive madness” dominating the corporation. In a candid interview, she described an environment of bullying where editors avoided critical reporting on trans issues for fear of attacks from their own colleagues.Read more …

'For the news department to be following some airy fairy ideology instead of fact is pretty wild!'

— GB News (@GBNEWS) May 16, 2026

Comedian Leo Kearse reacts to a former BBC news boss claiming she was bullied out of her role by 'gender ideologues'. pic.twitter.com/n6QNpZn1HM

“Just dealing with the progressive editorial issues and the bullying around them all. It was incredibly difficult,” Unsworth said. She added that the atmosphere extended beyond trans topics, with staff no-platforming dissenting views and pushing “safe spaces” over open debate. Unsworth’s remarks paint a picture of a newsroom where challenging the prevailing narrative on ‘culture war’ issues carried professional risks. Programme editors reportedly steered clear of stories that questioned aspects of the trans agenda, wary of backlash from activist-aligned staff. This self-censorship contributed to what a leaked internal memo later described as “effective censorship” on the topic.

Ex-BBC news boss Fran Unsworth says she was driven out of her job by 'progressive madness' of trans activists https://t.co/Fk0cmm51N1

— Daily Mail (@DailyMail) May 16, 2026Her departure was hastened by the constant pressure. “I would actually say it drove me out,” she stated, highlighting how the bullying around “progressive editorial issues” made her position untenable. This echoes earlier revelations about the BBC’s hiring practices. In 2024, the broadcaster made clear it would not hire candidates dismissive of diversity and inclusion policies, effectively screening out those skeptical of the dominant ideology. Recruiters were instructed to reject anyone showing a lack of enthusiasm for these topics, ensuring ideological conformity from the outset.

Unsworth’s admission also lands amid ongoing scandals over the BBC’s handling of gender issues, including accusations of harming children through biased children’s programming. In late 2025, over 650 families accused the BBC of harming children via a “constant drip-feed” of pro-trans material in shows and dramas. Parents detailed examples like Hey Duggee using “they/them” pronouns for a character aimed at five-year-olds, episodes of Doctors and Casualty promoting child transition narratives, and documentaries criticized for downplaying detransition regrets.

One parent group spokesman warned: “The constant stream of propaganda about gender and trans activism the BBC has transmitted has played a significant role in creating a dangerous culture for children.” They pointed to narratives linking gender questioning directly to suicide, which they said pressured families and ignored safeguarding concerns. The BBC has defended its output by citing updates to style guides and efforts to reflect developments like court rulings on biological sex, but trust continues to erode.

Inside the capture of the BBC, by Rob Burley (@RobBurl)

— UnHerd (@unherd) May 16, 2026

In his 13 years as a senior BBC editor, Rob Burley saw the Corporation’s defining commitment to impartiality undermined by transgender ideology, a blind commitment to Diversity & Inclusion schemes, and a culture of… pic.twitter.com/DobvY77PpDThe BBC’s obsession with identity politics has also produced content disconnected from everyday reality. A 2025 DEI training video on “microaggressions” went viral for its over-the-top portrayals of white colleagues as bumbling racists, complete with awkward accents and forced celebrations. Critics noted that no one in the real world behaves this way, highlighting the corporation’s bubble of performative wokeness.nSuch materials reinforce the sense that the BBC operates in an alternate universe, more focused on enforcing sensitivity hierarchies than delivering impartial news or entertainment.

Unsworth’s exit and the surrounding controversies arrive as the BBC faces broader challenges, including declining audiences, falling trust, and questions over its future under new leadership. Leaked documents and parental complaints have repeatedly shown how activist influence skewed coverage, sidelining biological reality and dissenting voices in favor of Stonewall-aligned perspectives. The pattern is clear: a public broadcaster funded by taxpayers has allowed internal cliques to dictate editorial direction, from hiring litmus tests to children’s shows pushing contested ideologies. This not only undermines impartiality but risks real-world harm by shaping public discourse—and young minds—around contested claims rather than evidence and balance.

“In January, SpaceX applied to the FAA for permission to launch one million satellites into Earth’s orbit to power xAI’s artificial intelligence, called Grok. “One million satellites is a lot,” he wrote ..”

• An Earth-Shattering Kaboom as Starship V3 Finally Takes Flight (Green)

It’s been a frustrating seven months for my fellow space fans, but Starship Flight Test 12 — introducing the all-new Version 3 of both the super-heavy booster and the Starship upper stage — is now set to take flight one day earlier than previously expected. Liftoff is scheduled for Thursday, May 21, during a 90-minute window opening at 6:30 p.m. Eastern. SpaceX will stream the attempt in glorious 4K from more angles than a 20-sided die on its X timeline. Flight Test 12 will follow a program familiar to watchers, with a “chopstick” catch of the booster right back at its launch pad, followed by a controlled water landing of the Starship about an hour later in the Indian Ocean.Read more …

This isn’t just another, long-delayed flight test. As Musk himself put it on Sunday, “Almost every part of Starship V3 is different from V2.” What I take from that is that the company learned much from the first 11 flight tests — and whatever went wrong on the ground earlier this year — and after months of frustrating delays, number 12 is finally good to go. Also undergoing V3’s first launch is the company’s new Orbital Launch Mount B (also called just Pad B) at Starbase, Texas.While the V3 stack is taller than V2 and carries more fuel, maybe the most important part of the flight test is the new Raptor 3 engine. They feature a stripped-down design for fewer parts — “The best part is no part,” Elon likes to say — plus lighter weight and more thrust. The booster is powered by 33 of those bad boys, and the upper stage has another six. Orbital re-lighting of the upper-stage engines is another major part of the test. Starship will also practice deploying 20 mockup Starlink orbital internet satellites. bThere’s even more:

Starship Flight 12 goals:

— Dima Zeniuk (@DimaZeniuk) May 17, 2026

• Debut next-generation Starship and Super Heavy vehicles

• First launch from Starbase’s newly redesigned launch pad

• Demonstrate upgraded Raptor engines in flight

• Deploy 20 Starlink simulators and 2 modified Starlink satellites

• Test… pic.twitter.com/jxq4uYIYWEThere’s so much riding on this one flight. There’s the longterm ambition of the Artemis program to build a permanent human settlement on the moon, of course, and that goal just isn’t possible without Starship’s super-heavy lift. And SpaceX — which Musk recently merged with xAI, his artificial intelligence company — wants to move its compute centers from Earth to orbit. How grand are Musk’s orbital compute ambitions? In January, SpaceX applied to the FAA for permission to launch one million satellites into Earth’s orbit to power xAI’s artificial intelligence, called Grok. “One million satellites is a lot,” he wrote, totally deadpan.

Nobody has launched more of anything than SpaceX has put Starlink internet satellites into Low Earth Orbit (LEO), and they just cracked 10,000 a little while ago. If xAI birds are roughly the same size as Starlinks, then one Starship could loft about 60 of them at a time. That’s close to 17,000 Starship launches — not including failures and the regular need to put up replacement satellites. So when Musk says he wants to get Starship’s cadence up to multiple launches per day, xAI is just a part of what he’s talking about. Or as SpaceX put it earlier this year, xAI in space would be the first step towards “becoming a Kardashev II-level civilization — one that can harness the Sun’s full power.” “That’s big,” he wrote, still totally deadpan.

Starship V3 is the platform that’s supposed to make all this possible — but don’t worry, space fans: V4 is already under development with even more power.

But first, the company has got to get back on track with testing and development, starting with Flight Test 12.

Godspeed.

“.. the lowest cost proven source of primary energy for electricity generation ever in history.”

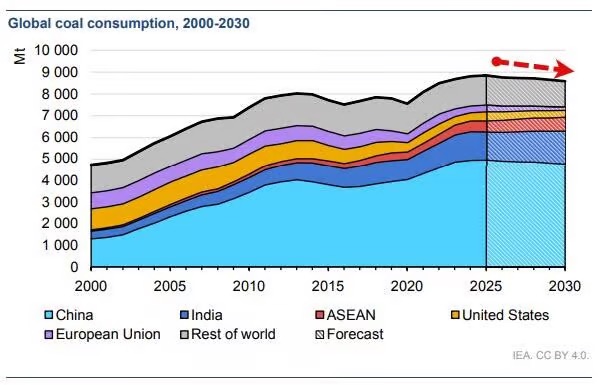

• International Energy Agency Is Wrong To Forecast Coal’s Demise (ET)

Activists would have us believe that coal is a dying energy source. But, thankfully for American coal states such as West Virginia and the Canadian provinces of Saskatchewan and Nova Scotia—all of which use millions of tonnes of coal every year to generate electricity—that is not even remotely true. However, the world is burning more coal now than ever, reaching a record 8.85 billion metric tonnes annual consumption by the end of 2025. Since 2020, annual coal consumption has increased by 1.40 billion tonnes.Read more …

Most of this has come from China, of course, which makes up about 55 percent of global coal consumption (the United States makes up about 5 percent of global consumption). Although the International Energy Agency (IEA) predicts a decline in demand over the next five years, The Kobeissi Letter more realistically predicts that demand will continue to rise, and points out that “past forecasts of peak coal demand have repeatedly proven wrong.” A graph on the IEA’s website that illustrates coal consumption (in metric tonnes, Mt) from 2000 to 2022, shows estimates for 2024 to 2026 that seem improbable.

Regardless, the IEA writes that increased demand for renewables is the primary cause for the estimated decline in coal consumption, and that “Global coal demand is expected to effectively plateau over the coming years, showing a very gradual decline through to 2030.” However, they also write that coal use is expected to increase in India by about 3 percent per year and in Southeast Asia by about 4 percent per year up to 2030.

In reality, we can’t expect China to slow its coal production anytime soon. Currently consuming about 3 billion tonnes annually, they will clearly dominate global trends in coal consumption in the years to come. Although the IEA also expects a slow decline in coal consumption in China over the next five years, with the gradual but marked decline of climate change alarmism worldwide and China’s ambition to expand its economy, this prediction doesn’t seem to hold much credibility either.

As The Kobeissi Letter states, coal remains in high demand, and the pipe dream of climate activists to kill coal doesn’t account for the security and convenience that this energy supply affords us. Like nuclear electricity—another power source that is vital to providing electricity for large portions of the world—the fuel for coal-fired power generation can be stored right on a power plant’s site for long periods of time, providing stable energy for society. We especially need coal during deep freezes because natural gas can falter in extreme cold due to “just-in-time” pipeline delivery. Gas flows can slow or freeze entirely, as seen in winter storms Uri (2021) and Elliott (2022), leaving grids vulnerable. And, not surprisingly, in each of these storms, wind and solar delivered very little, and sometimes no power at all, causing millions to lose electricity and causing hundreds of deaths from the cold.

CO2 Coalition energy expert Dick Storm says that “coal is indispensable” and that it is “the lowest cost proven source of primary energy for electricity generation ever in history.” The Canadian province of Ontario, where I live, proved this case well. In 2002, coal provided about 25 percent of the province’s power, and we enjoyed very low electricity rates. But in 2005, then-Premier Dalton McGuinty held a news conference and, pointing to the pile of coal beside him, said it was “old technology” and that, to save the climate and protect the air, Ontario would phase out all coal-fired electricity generation. This made no sense in light of the facts:

1. Coal is not a technology. It is a resource, and the degree to which it causes pollution when burned depends on the technology used to burn it. Reducing carbon dioxide emissions from a coal plant is unquestionably costly, difficult, and of course, unnecessary. Reducing real pollution is often well worth the price and far easier to accomplish with a coal station by using the latest pollution control technology.

2. Seen in a global context, Ontario’s emissions are trivial—one-quarter of Canada’s 1.6 percent of global emissions. So, no matter what one believes about the causes of climate change, McGuinty’s announcement and the province’s painful reduction to 0 percent coal-fired power were merely virtue signalling and showmanship. It had no impact on climate whatsoever.

It did, however, have a huge impact on consumer electricity rates, which, depending on the year, doubled or even tripled as coal was replaced with more expensive power, including a massive expansion of industrial wind turbines. Of course, soaring power rates are politically problematic, so the government decided to hide the increase in the tax base, and today’s rates are merely 50 percent higher than those in 2002. But we all eventually pay for this massive increase, just not directly on our power bill.

Renewable energy has only been able to survive thus far because it is heavily subsidized by tax dollars. These subsidies have, unfortunately, caused coal-fired power stations to be less profitable to operate, by comparison, compounded by the fact that regulations have crippled the industry. It is important to increase our expansion of coal plants, Storm tells us. 800,000 megawatts of new power generation, the equivalent of 80 New York cities, will be needed in the United States in the next 25 years to keep up with demand. This is simply not possible with renewable energy, and although nuclear and other conventional power will be significant players in this, coal will remain a steady, reliable power source to provide us with these vast amounts of power.

Rather than phase out coal, Saskatchewan should build more plants. Since Alberta phased out this important energy source, it will soon come knocking again begging for more power from Saskatchewan’s black gold.

True pic.twitter.com/OEpuW3n8JQ

— Elon Musk (@elonmusk) May 19, 2026

Elon Musk just described how the entire government operates in a single sentence.

— Dustin (@r0ck3t23) May 19, 2026

Musk: “Paying people to do nothing doesn’t make sense.”

Then he told a Milton Friedman story that should terrify every bureaucrat on the payroll.

Friedman watched workers digging ditches with… pic.twitter.com/JCajW6djhR

JENSEN HUANG: “IF I HAVE A CHOICE BETWEEN A NEW COLLEGE GRADUATE WITH NO CLUE WHAT AI IS AND ONE THAT IS EXPERT IN USING AI, I WOULD HIRE THE ONE WHO'S EXPERT IN USING AI. ACCOUNTANT, MARKETING, SUPPLY CHAIN, LAWYER, SALESPERSON. EVERY SINGLE TIME.” pic.twitter.com/71ZqNbMcPO

— Vivek Sen (@Vivek4real_) May 18, 2026

Mathematician Sir Roger Penrose: "AI is a bad term. It's not intelligence" pic.twitter.com/p2f1UDxQTM

— shouko (@shoukointech) May 17, 2026

What is the best possible future? This question is much harder to answer than it may seem. https://t.co/UbWI37hSQO

— Elon Musk (@elonmusk) May 19, 2026

Professor Robert Clancy draws attention to a shocking new Japanese study involving 20 million people, which found that "all the excess deaths were in the vaccinated group".

— healthbot (@thehealthb0t) May 19, 2026

"The non-vaccinated group had none." pic.twitter.com/N7FdPR9Rok

Support the Automatic Earth in wartime with Paypal, Bitcoin and Patreon.