Detroit Publishing Co. Excursion steamers Tashmoo and Idlewild at wharf, Detroit 1901

This is one of those days where I wonder what I’m going to say about this one. It’s all too convoluted six ways to Sunday. Yeah, Mario Draghi delivered for markets and investors, and stocks rise a bit more. Like they’re not high enough yet, setting records in . One thing he didn’t do is commit to asset backed securities purchases, and so that is now what markets will be demanding from him next time around. Who cares anymore that ABS were the main conduit to blew up the same markets in 2008? Investors are happy, and Jack and Jill are ignorant. The Great QE Bubble lives to see another day. Yay!

The ECB has lowered its refinancing rate to 0.15%, its marginal rate to 0.4% and the deposit rate to -0.1%. Negative interest sounds like a big deal, but there are hardly any bank deposits left with the ECB, so despite the giamt novelty made out of it, this is just a paper measure. They took all these “bold steps” ostensibly because Draghi et al find inflation rates too low. But how would lowering interest rates fix that? Wouldn’t it be better to raise them, wouldn’t that be more inflationary (in the inflation equals rising prices sense)? It seems obvious it would, but that would kill the housing sector, among other things, and we want to keep people tied in to their mortgages, don’t we?

Still, at least raising rates would have been surprising, and volatility would have gone up, which is just what central bankers say they want – even if they don’t say out loud they badly need it -. Maybe the disparity between the Fed and BoE, who threaten to raise rates, and the ECB that lowers them, will lift the VIX. But that’s not certain by any means.

The newly announced $640 billion LTRO channel for business loans sounds nice, but interest rates are already very low, so they were not the reason businesses didn’t borrow. The real reason is in all likelihood hidden in the demand side of the real economy. Which, simple as it may be, is very poorly understood in economics. The ECB’s decisions are all based around economists’ extreme -and extremely wrong – focus on demand, which manifests itself in terms like aggregate demand and pent-up demand (of course the magical option is increased demand).

What they are (seemingly?) incapable of getting into their heads is that demand is not some sort of constant – let alone constantly growing – metric. That, like for instance this past winter when Americans were forced to spend far more than usual on heating and healthcare costs, there was no pent-up demand left come spring, because people were maxed out (they had spent their “demand”). For economists, when sales numbers have been low(er) than expected/desired during a certain period of time, that must mean more sales are just around the corner. Something went wrong, so you repair it. There is no risk that it can’t be repaired. That’s about as close to religion as one can possibly shirk without coming out on the other side of it.

The entire interest rate circus happens because the overriding “philosophy” amongst economists and politicians is that banks are more important than people. the idea is that if banks are doing well, that will automatically trickle up/down to the people. But why wouldn’t the opposite be true? If policies were aimed at making sure people as as well off and – economically – protected as they can be, wouldn’t that trickle down/up to banks? If stocks are up, then the economy must be good. If banks make solid profits, the economy must be good. And people are nowhere in sight, they’re an afterthought as best.

In the eyes of Draghi and Yellen and all the clowns who think like they do, our economies exist of banks and investors, not of you and me. But we are 70% or so of those economies, even if we can’t keep up with the demand they tell us their theories tell them we should be exhibiting. As societies, we clearly don’t have our priorities in order; we instead let others set them for us, but they’re not ours. The sooner we acknowledge this, the more damage to the lives and well-being of our children and grandchildren we can prevent from being unloaded upon them.

But we need to start doing that like about now. We need to realize that there is very little left that is being decided for us that actually benefits us, and that there are a million things being concocted that are only dragging us down ever further. Mario Draghi and Janet Yellen and Washington and Brussels are not trying to make this world a better or happier place for us, but for their banker friends. That is what I take away from Draghi’s performance today, from the whole financial world circus around it, and most of all from the silence in the real world as that circus put on its show. Will we really only react when we have nothing left at all? It’s starting to look that way. And you won’t have anyone to blame anyone but yourself.

• ECB Cuts Refi Rate To 0.15%, Deposit Rate To -0.1% (FT)

The European Central Bank has cut interest rates to a fresh record low, lowering one of its benchmark rates below zero in a radical move that policy makers hope will help the currency bloc stave off the threat of deflation. The ECB cut its main refinancing rate to 0.15 per cent, from 0.25 per cent, and its deposit rate from zero to -0.10 per cent, becoming the first major central bank to venture into negative territory. Neither the Federal Reserve, the Bank of Japan nor the Bank of England, have tried the measure, which the ECB hopes will lift inflation by weakening the euro and spurring lending in the bloc’s more unsettled periphery.

Both decisions were widely forecast following hints from policy makers that, after more than six months of standing firm, the ECB would take concrete steps in June. A lower-than-expected figure for May inflation, which at 0.5 per cent is well below the central bank’s target of just under 2 per cent, had cemented expectations that the governing council would act. Analysts also expect Mario Draghi, ECB president, to announce measures to ease borrowing constraints on the currency bloc’s smaller businesses at the post-meeting press conference, to begin at 1.30pm GMT.

• ECB Throws Cash At Sluggish Euro Zone Economy (Reuters)

The European Central Bank said on Thursday it will offer banks a targeted long-term refinancing operation (LTRO) to persuade them to lend, was preparing to purchase asset-backed securities in future and will discontinue sterilising previous bond purchases. The decision came after the ECB had cut its main interest rate to 0.15% and imposed negative interest rates on banks’ overnight deposit. The measures are designed to offer the euro zone economy stimulus, but stop short of the large-scale effect the ECB could unleash with a big plan of quantitative easing (QE) – money printing to buy assets. “In pursuing our price stability mandate today we decided on a combination of measures to provide additional monetary policy accommodation and to support lending to the real economy,” ECB President Mario Draghi told a news conference.

Ambrose doesn’t quite get it yet, but he does provide the data. Good on him.

• The Nagging Fear That QE Itself May Be Causing Deflation (AEP)

The way we are going, the whole world will end up with zero interest rates or some variant of quantitative easing before long. Such is the overwhelming power of deflation in countries with burst credit bubbles. Such too is the implication of a global savings rate that has spiralled to an all-time high of 25pc of GDP, starving the world of demand. The European Central Bank looks poised to cut the discount rate below zero on Thursday, becoming the first of the monetary superpowers to venture into these uncharted waters. Banks will be charged to park money in Frankfurt. More than €800bn of money market funds will sink below the water line, so the funds will go elsewhere. The chief purpose is to drive down the euro, an attempt to pass the toxic parcel of incipient deflation to somebody else.

The ECB is expected to map out future purchases of asset-back securities, “unsterilised” and intended to steer stimulus with surgical precision towards small businesses in what amounts to light QE This is not yet the €1 trillion blitz already modelled and sitting in the ECB’s contingency drawer. Germany’s DIW institute is calling for €60bn of bond purchases each month, equal to 0.7pc of total EMU sovereign debt, and roughly in line with moves by the US Federal Reserve. Such radical action will have to wait. In China the new talk is “targeted monetary easing”, with the first hints of outright asset purchases. Railways bonds have been cited, and local government debt. The authorities are casting around for ways to keep the economy afloat while at the same gently deflating a property boom that has pushed total credit from $9 trillion to $25 trillion in five years. [..]

The Bank for International Settlements says the world is suffering from addiction to stimulus. “The result is expansionary in the short run but contractionary over the longer term. As policy-makers respond asymmetrically over successive financial cycles, hardly tightening or even easing during booms and easing aggressively and persistently during busts, they run out of ammunition and entrench instability. Low rates, paradoxically, validate themselves,” it said. Claudio Borio, the BIS’s chief economist, says this refusal to let the business cycle run its course and to purge bad debts is corrosive. The habit of turning on the liquidity spigot at the first hint of trouble leads to “time inconsistency”. It steals growth and prosperity from the future, and pulls the interest rate structure far below its (Wicksellian) natural rate. “The risk is that the global economy may be in a deceptively stable disequilibrium,” he said.

It doesn’t hold up in theory either.

• Why Central Bank Stimulus Cannot Bring Economic Recovery (Mises Inst.)

Central bank credit expansion is the best example of the Keynesian disregard for the inevitable consequences of violating Say’s Law. Money certificates are cheap to produce. Book entry credit is manufactured at the click of a computer mouse and is, therefore, essentially costless. So, receivers of new money get something for nothing. The consequence of this violation of Say’s Law is capital malinvestment, the opposite of the central bank’s goal of economic stimulus. Central bank economists make the crucial error of confusing GDP spending frenzy with sustainable economic activity. They are measuring capital consumption, not production.

The credit expansion causes capital consumption in two ways. Some of the increased credit made available to banks will be lent to businesses that could never turn a profit regardless of the level of interest rates. This is old-fashioned entrepreneurial error on the part of both bankers and borrowers. There is always a modicum of such losses, due to market uncertainty and the impossibility to foresee with precision the future condition of the market. But the bubble frenzy fools both bankers and overly optimistic entrepreneurs into believing that a new economic paradigm has arrived. They are fooled by the phony market conditions, so bold entrepreneurs and go-go bankers replace their more cautious predecessors. The longer the bubble lasts, the more of these unwise projects we get.

Another chunk of increased credit goes to businesses that could make a profit if there really were sufficient resources available for the completion of what now appears to be profitable long term projects. These are projects for which the cost of borrowing is a major factor in the entrepreneur’s forecasts. Driving down the interest rate encourages even the most cautious entrepreneurs and bankers to re-evaluate these shelved projects. Many years will transpire before these projects are completed, so an accurate forecast of future costs is critical. These cost estimates assume that enough real capital is available and that sufficient resources exist to prevent costs from rising over the years. But such is not the case. Austrian business cycle theory explains that absent an increase in real savings that frees resources for their long term projects, costs will rise and reveal these projects to be unprofitable.

Snow! Ice!

• US Q1 Productivity Misses; Plunges By Most In 6 Years (Zero Hedge)

Nonfarm productivity in the frost-bitten US in Q1 plunged at its fastest pace since Q1 2008. The 3.2% drop is considerably bigger than the 3% expected but was accompanied (oddly) by a rise in employee hours (so despite the catastrophic weather, everyone was going to work and working more) but producing less. Unit labor costs soared 5.7% – the most since Q4 2012.

From the report:

Nonfarm business sector labor productivity decreased at a 3.2% annual rate during the first quarter of 2014, the U.S. Bureau of Labor Statistics reported today, as hours increased 2.2% and output decreased 1.1%. (All quarterly% changes in this release are seasonally adjusted annual rates.) The decrease in productivity was the largest since the first quarter of 2008 (-3.9%). From the first quarter of 2013 to the first quarter of 2014, productivity increased 1.0% as output and hours worked rose 2.8% and 1.7%, respectively. Labor productivity, or output per hour, is calculated by dividing an index of real output by an index of hours worked of all persons, including employees, proprietors, and unpaid family workers. The measures released today are based on more recent source data than were available for the preliminary report.

In the first quarter of 2014, nonfarm business productivity fell 3.2%, a greater decline than was reported in the preliminary estimate. The revised figure reflects a 1.4%age point downward revision to output and a 0.2%age point upward revision to hours. Unit labor costs were revised up due to the downward revision to productivity, and grew 5.7% in the first quarter of 2014. In the manufacturing sector, productivity growth in the first quarter was revised up to 3.8%, due to an upward revision to output and a downward revision to hours worked. Unit labor costs declined 0.4%, rather than increasing 0.1% as previously reported.

And notably: 1.8% increase in hours worked in a quarter in which, supposedly, nobody could get to work. Huh???

On and on we go …

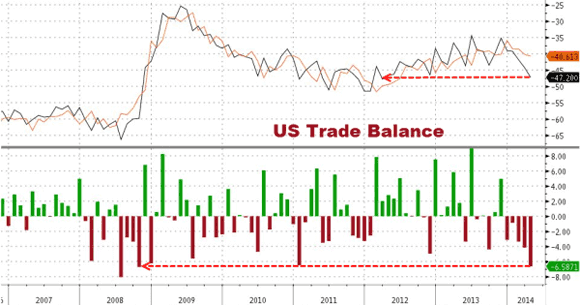

• What Q2 GDP Rebound? US Trade Deficit Soars To 2 Year High (Zero Hedge)

The US trade balance collapsed in April dashing hopes for the exuberant hockey-stock rebound in Q2 GDP. This is the biggest trade deficit since April 2012 and the biggest miss from expectations since October 2008. The last 2 months have seen the biggest slide in the deficit in a year as trade gaps with the European Union and South Korea reach records and the deficit with China surged by $7billion to $28 billion. Impots of capital goods, autos, and consumer goods all set records. And Q2 GDP downgrades in 3…2…1…

The details: The U.S. monthly international trade deficit increased in April 2014 according to the U.S. Bureau of Economic Analysis and the U.S. Census Bureau. The deficit increased from $44.2 billion in March (revised) to $47.2 billion in April as exports decreased and imports increased. The previously published March deficit was $40.4 billion. The goods deficit increased $3.3 billion from March to $65.8 billion in April; the services surplus increased $0.2 billion from March to $18.6 billion in April.

Yeah, blame the people for your failures, why not?

• President Of Eurogroup Issues ‘Self-Fulfilling’ Deflation Warning (CNBC)

President of the Eurogroup, Jeroen Dijsselbloem, warned on Thursday that deflation fears plaguing the euro zone could become a “self fulfilling prophecy” as investors grow increasingly wary. Dijsselbloem, the head of the group euro zone finance ministers and Dutch finance minister, said the European Central Bank had “grounds to act” at an interest rate decision meeting on Thursday as inflation is off moving in the wrong direction. Euro zone inflation fell unexpectedly to 0.5% last month, intensifying pressure on Mario Draghi, President of the European Central Bank, to act against the rising threat of deflation. “The ECB have a mandate, they have to make sure that in the mid-term the inflation stays close to the 2% target — it is not going in that direction, so there seems to be grounds to act.

We will wait for today and see what they do within their mandate,” the Eurogroup chief told CNBC. The euro zone’s inflation reading is well below the ECB’s target of just under 2 per cent and on a par with March, when it hit its lowest level since autumn 2009. He warned that the market is expecting too much from just one meeting and the euro zone deflation issue cannot be tackled by ECB intervention alone. “If you listen to some of the expectations that some of the commentators have shown in the last couple of days, they will probably be disappointed anyway because no way can you deliver such big results in such short time,” he said.

Lemme guess: not the poorest.

• Who Wins If Europe Moves To Quantitative Easing? (SMH)

Investors will be closely watching the European Central Bank’s monthly interest rate decision later tonight But this meeting will be anything but normal, with ECB president Mario Draghi widely tipped to launch quantitative easing measures, pumping more liquidity into the eurozone to help fight the threat of deflation So if the ECB follows the US, how will this affect global asset markets French bank Societe Generale has a few thoughts, including how Australian investors might benefit. If the ECB adopts a quantitative easing policy and enters a negative deposit rate scenario, high carry trade currencies that react positively to risk appetite, like the Aussie, are expected to react strongly. Societe Generale global head of research Patrick Legland says the euro against the Aussie and Norwegian Krone are key pairs to benefit, given Australia and Norway are the only two G10 economies where the inflation rate is at least at their respective central banks’ targets.

Commodities is expected to be the asset class least sensitive to ECB quantitative easing because it is driven by the strength of US growth, Mr Legland said. But there is still expected to be some movement, given the divergence between 10 and two year US and euro rate spreads, which are rising and declining respectively. Mr Legland said as eurozone rates drop relative the US, making the US dollar stronger, it made commodities more expensive, since they are mostly priced mostly in US dollars. “This seems to have the greatest impact on gold as its increase is significantly lower than the other commodities in this environment”. Mr Legland says emerging market investors are focused mainly on the US monetary policy outlook, particularly the risk of early Fed rate hike.

But “bold” ECB easing is likely to trigger a “major risk sentiment boost” for high yielding assets in emerging markets. “The positive impact is likely to be felt across all global emerging markets,” he said. “An ECB move will reinforce the bullish environment for emerging market fixed income. “Our top picks … include Romania, South Africa and Mexico.” If the ECB was to buy government bonds directly this would cause government credit default risk to disappear and reassure markets, Mr Legland said. “We believe eurozone periphery country spreads will continue to tighten, pushing domestic equity markets and overall eurozone bank valuations higher.” Mr Legland said QE could also end volatility in eurozone equities. “Whether the ECB purchases [asset-backed securities] or government bonds, it will increase its balance sheet and print money. This would partly reduce the current risk premium on European equities which is due to deflationist fears.”

Not even susprising anymore. But still dark.

• ZIRP Unmasked: Zero Growth In Private Labor Hours Since 1998 (Stockman)

Every now and again the apparatchiks who dutifully tend Washington’s statistical sausage factories accidently let loose a damning picture of what actually goes on inside. In that vein the BLS has just published the equivalent of a smoking gun. Namely, a study showing that in 2013—the year of 32% stock returns—the business sector of the US economy generated no more labor hours than it did way back in Bill Clinton’s blue dress period (1998) yet purportedly produced 42% more output in real terms:

“…workers in the U.S. business sector worked virtually the same number of hours in 2013 as they had in 1998 – approximately 194 billion labor hours.1 What this means is that there was ultimately no growth at all in the number of hours worked over this 15-year period….. it is perhaps even more striking that American businesses still managed to produce 42% – or $3.5 trillio – more output in 2013 than they had in 1998, even after adjusting for inflation.

Striking indeed! The most important thing we know about those 194 billion labor hours is that the mix of labor supplied to the US economy deteriorated drastically during that 15 year period owing to the sharp decline of the goods producing economy in the US and its replacement by the low productivity HES Complex (health, education and social services). So the implication of the BLS study is that business sector productivity soared—at about 2.4% annually over the period— even as factory materials handlers were replaced by bedpan handlers in the labor mix. Needless to say, to smell a skunk in that woodpile does not take a lot of sniffing.

Here is the reason. The BLS claim that real business sector output grew by 42% during the period, and therefore that private productivity grew by leaps and bounds, is based on an arithmetical derivative, not a direct measure of output. Stated differently, what the GDP accounts measure directly is spending by households, business and government—a metric which is then “deflated” by patently low-balled guesstimates about the inflation rate. Subtract from that figure for “real GDP” actual government consumption and investment spending (plus a small amount for household sector output) and, presto, you get a fiction called “business sector output”. According to the BEA’s official publication of the NIPA accounts, that figure was $8.4 trillion in 1998 and just shy of $12 trillion in 2013.

That still means 3 out of 10 do.

• 7 In 10 Americans Believe The Crisis Is Not Over (Zero Hedge)

For all the talk about a recovery, pundits, especially those who peddle expensive newsletters, continue to forget one key distinction of the New Normal: there are those for whom the recovery has never been stronger, well under 10% of the population, i.e., the already wealthy whose net worth is allocated in financial assets. And then there is everyone else, that vast majority of Americans, who not only have not benefited by the Fed’s relentless balance sheet expansion and accompanying asset reflation but whose incomes just posted the first decline in real terms since 2012. It is this latter segment that should be concerned by a recent survey conducted by the MacArthur Foundation titled “How Housing Matters”.

According to the survey during the past three years, over half of all U.S. adults (52%) have had to make at least one sacrifice in order to cover their rent or mortgage. Such sacrifices included getting an additional job, deferring saving for retirement, cutting back on health care and healthy foods, running up credit card debt, or moving to a less safe neighborhood or one with worse schools. More disturbing, the survey also found that while there are some indicators that the American public’s views about the housing crisis are shifting toward the positive, large proportions of the public are not feeling the relief: seven in 10 (70%) believe we are still in the middle of the crisis or that the worst is yet to come. And no, it is not just the high school graduates who are desperate: a whopping 60% of college grads agree: the worst is yet to come (perhaps after looking at their student loan balances).

As MarketWatch reports, “although mortgage rates are still quite low, down payments, poor credit and tighter lending standards remain three of the biggest hurdles for buying a home, especially among young people, Blomquist says. “The slow jobs recovery for young adults has made it harder for them to save and to get a mortgage.” Some 84% of young people are delaying major life decisions due to the poor economy, according to a 2013 survey by Generation Opportunity, a nonprofit think tank based in Arlington, Va.” What’s more, at least 15% of American homeowners (or residents of 78 counties across the country) were living in housing markets where the monthly mortgage payment on a median-priced home requires more than 30% of the monthly median household income — long considered the maximum for rent/mortgage repayments.

Housing costs above that threshold are “unaffordable by historic standards,” says Daren Blomquist, vice president at real estate data firm RealtyTrac. In New York county/Manhattan, mortgage payments represent 77% of the median income and in San Francisco County represents 70%. As a result of a broken economy and lack of good job opportunities the “American dream” is now on its last legs: more than half of Americans, or 54%, believe that buying a home has become less appealing than it once was while some 43% of respondents have indicated that it is no longer the case that owning a home is “an excellent long-term investment and one of the best ways for people to build wealth and assets.” Even as seven in 10 renters (70%) aspire to owning a home, high proportions (58%) believe that “renters can be just as successful as owners at achieving the American Dream.”

BNP Paribas looks set to become a major roadblock in US-France relations.

• Dimon’s Raise Haunts BNP Paribas as US Weighs $10 Billion Fine (Bloomberg)

When JPMorgan Chase’s Jamie Dimon got a 74% raise in January, U.S. Attorney Preet Bharara fumed. He had forced the bank just weeks before to pay $1.7 billion for enabling Bernard Madoff’s Ponzi scheme. And yet Dimon was being rewarded. Now, five months later, Bharara’s frustration is directed at another bank. In the next few weeks, BNP Paribas could face criminal charges and a fine of up to $10 billion for doing business in sanctioned countries such as Iran and Sudan. That penalty would far exceed the fines incurred by six other banks that escaped criminal charges for similar offenses since President Barack Obama took office in 2009 — and would be the largest-ever criminal penalty in the U.S.

The potential severity in BNP’s case stems in part from Bharara’s determination to punish banks that have repeatedly evaded harsher penalties by warning that a wave of unforeseen consequences could result, the egregiousness of BNP’s conduct and the bank’s apparently slow response to the U.S. investigation during its early stages, according to two people familiar with the matter. The case has strained relations between the U.S. and France, with French President Francois Hollande set to confront Obama today at a Paris dinner over what he says is a threat to his country’s financial system. This story, the result of interviews with more than two dozen people with knowledge of the BNP investigation, illustrates how France’s largest bank became the target of the U.S. in its effort to show that large financial institutions shouldn’t expect special treatment under the law. It also describes a previously unreported letter that shows prosecutors’ dissatisfaction with the bank’s cooperation.

• BNP Paribas Hit By Downgrade Warning From Standard & Poor’s (Guardian)

France’s biggest bank, BNP Paribas, has been threatened with a downgrade to its credit rating as it braces for a potential $10bn (£6bn) fine from US regulators for busting sanctions. The warning by the Standard & Poor’s agency came amid fresh estimates of the regulatory costs facing the European banking industry, which could leave a $104bn bill for a catalogue of errors ranging from tax evasion and mis-sold financial products to manipulation of financial markets. Analysts at Credit Suisse doubled their estimates for the costs of the scandals which have gripped the industry since the financial crisis.

Upping their estimate to $104bn from $58bn, the Credit Suisse analysts forecast that litigation facing Royal Bank of Scotland could further delay the government selling off its 83% stake. US authorities accuse BNP Parisbas of breaking sanctions on Sudan, Iran and Syria over a seven-year period to 2009. S&P said that the potential settlement with the US had forced it to consider a potential downgrade to BNP’s A plus rating and place the bank on “credit watch negative”, until the outcome of the discussions with the US authorities is known. The situation facing BNP is causing concern in France where it has emerged that president François Hollande had written to Barack Obama in April to complain the fine would be disproportionate. The pair are due to meet in Paris over dinner where Hollande will raise the situation in person with the US president, according to the Reuters news agency.

What an insane record. When’s the last time GDP actually beat expectations?

• The History Of Consensus Expectations For US GDP (Zero Hedge)

Same Stuff, Different Year. How many more of these annual disappointments does it take before the world gets the joke…

3 articles on the mysteious missing 100,000 tons of copper and aluminum that could have far reaching repercussions in commodities and financing markets. As if it’s not nuts enough to use metals as collateral for more metals, what if they were never even there? And how widespread is this?

• Chinese Port Stops Metal Shipments Due To Missing Inventory Probe (Reuters)

China’s northeastern port of Qingdao has halted shipments of aluminium and copper due to an investigation by authorities, causing concern among bankers and trade houses financing the metals, trading and warehousing sources said on Monday. “We were told we can’t ship any material out while they do this investigation,” a source at a trading house said. The port of Qingdao is China’s third-largest foreign trade port and the world’s seventh-largest port, trading with 700 ports in more than 180 countries, according to its website. “Banks are worried about their exposure,” one warehousing source in Singapore said. “There is a scramble for people to head down there at the minute and make sure that their metal that they think is covered by a warehouse receipt actually exists,” he said.

Metal imports have been partly driven in China as a means to raise finance, where traders can pledge metal as collateral to obtain better terms. In some cases the same shipment can be pledged to more than one bank, fuelling hot money inflows and spurring a clampdown by Chinese authorities. “It appears there is a discrepancy in metal that should be there and metal that is actually there,” said another source at a warehouse company with operations at the port. “We hear the discrepancy is 80,000 tonnes of aluminium and 20,000 tonnes of copper, but we hear that the volumes will actually be higher. It’s either missing or it was never there – there have been triple issuing of documentation,” he said.

Beijing last year set new rules to curb currency speculation amid signs that hot money inflows helped push the yuan to a series of record highs. The rules required banks to tighten the management of their foreign exchange lending and types of clients that are able to access those loans. “It’s such a massive port I would think virtually everybody has exposure,” the trading source said. “Once the investigation is over, it could be bearish for metals. I think that a lot of Western banks will try to offload material and try not to deal with Chinese merchants,” the trading source added.

TEXT

• China Commodity Financing Probe Could Lead To Heavy Losses (CNBC)

A more severe crackdown on the use of commodities as collateral to finance deals in China could lead to heavy losses across the asset class, analysts warn. “The profitability of the [commodity financing] schemes is being eroded, and the authorities are stepping up efforts to curb some forms of shadow banking,” said Caroline Bain, senior commodities economist at Capital Economics in a note. In typical commodity financing deals Chinese companies obtain a letter of credit, use it to import a commodity – copper for instance – sell that commodity in the local market or deploy it as collateral and use that money to invest in higher yielding assets before paying back the original loan. The practice isn’t new but recently came into focus following reports that such deals accounted for one third of China’s money supply growth in 2013.

Commodity financing drives hot money inflows which can negatively affect the economy, creating a credit boom and driving inflation, while eventual outflows could lead to sharp asset price deflation. The resulting buildup of large unofficial commodities stockpiles in China makes markets look artificially tight. Unofficial copper stocks, for instance, could be as high as 700,000 tonnes, according to Capital Economics. “A disorderly unwinding of the deals could lead to sharply lower prices as stocks are offloaded to the market,” Bain said. Chinese authorities took action in May, with the China Banking Regulatory Commission warning banks to tighten controls on letters of credit for iron ore imports.

TEXT

• China Qingdao Port Metals Inventory Probe Fuels Worries (Reuters)

Worries over a probe into commodity stockpile financing at China’s Qingdao port appeared to deepen on Wednesday as Standard Bank and a part-owned unit of Louis Dreyfus warned of potential losses and copper prices fell further. The inquiry, first reported by Reuters and other media earlier this week, has revived concerns about the impact of China’s deepening credit crisis on its metal imports, much of which piles up in warehouses to be used as collateral. London copper prices have fallen 2% in two days. Responding to queries about the probe at Qingdao, which has not been officially confirmed, South Africa-based Standard Bank said it was “working with local authorities” to investigate potential irregularities at China’s third-largest port, a major source for metal and iron ore imports. “Standard Bank Group is not yet in a position to quantify any potential loss arising from these circumstances,” the bank, whose Standard Bank Plc subsidiary conducts commodities trading, said in a statement.

Singapore-based logistics provider GKE Corporation warned shareholders that it was “assessing the potential impact” of the investigation on its GKE Metal Logistics unit, a joint-venture 51% owned by global commodities merchant Louis Dreyfus. They are the first companies to publicly discuss the issue since the inquiry came to light on Monday, when Reuters reported the port in northeastern China had halted shipments of copper and aluminum as it launched an investigation into metal stockpiles used for collateral on loans. According to traders and warehousing sources, port authorities at Qingdao’s Dagang wharfs have been examining whether there had been multiple issuing of receipts for single cargoes of metal tied to a trading company and linked companies. The tumult has revived concerns that first surfaced in March, when China’s first domestic bond default fueled fears of further financing woes and triggered one of copper’s steepest drops in years, with prices tumbling 8% in three days.

Actually, a link to an RT section on Snowden and the NSA. The quoted article is the first in the section.

• One Year Ago, Total Surveillance Was A Conspiracy Theory (RT)

A year has passed since Edward Snowden started telling us what really was going on in the world. Since that date, various holders of power have been struggling – without success – to reclaim the control of the narrative, the control of the news flow. But in the age of the net, the power of narrative rests squarely with the many, rather than with the elite. People have become aware of mass surveillance, even if they haven’t become aware of its full consequences yet. But the story is out. The proverbial cat isn’t just out of the bag, but has left the entire city and is halfway across the continent. This hasn’t prevented an ivory tower establishment from playing “no see, no hear, no speak” monkey games, pretending Snowden does not exist and that people don’t already know what we know.

Carl Bildt, the Swedish Minister of Foreign Affairs, has been one of the strongest proponents of NSA-style mass surveillance and trying to “control” the net – completely ignoring the fact that this necessarily means controlling (effectively eliminating) free speech. He’s even gone on record stating that mass surveillance doesn’t violate human rights because it is covert: as if security services don’t violate people when doing so doesn’t leave traces. Bildt’s favorite alibi conference has been the Stockholm Internet Forum, which is supposed to be about net liberty and development in general. He has been inviting freedom activists from all over the world to show himself in their presence, trying to polish his image as pro-freedom and pro-liberty. However, his actions say the opposite: He has been negotiating spy deals with the United States at the same time. This year, the arrangers of the Stockholm Internet Forum suggested – naturally and obviously – Glenn Greenwald, Edward Snowden, and similar activists like Jacob Appelbaum as speakers. However, this did not sit well with Bildt. His Department of Foreign Affairs unceremoniously blacklisted them from speaking at the Stockholm Internet Forum, as reported by Cicero..

Quite a movement.

• ‘Don’t Ask For Privacy, Take It Back’: Anti-NSA #ResetTheNet Campaign (RT)

Internet activists and rights groups have launched a massive online campaign against mass government surveillance, urging users and websites to use encryption. The campaign’s inspiration – NSA whistleblower Snowden – has called to join ResetTheNet. A year to the day since the first revelations of the US National Security Agency’s (NSA) warrantless and huge-scale web surveillance were published in the media, the international June-5 campaign for data encryption kicked off. Hundreds of websites and organizations, including Reddit, Imgur, Mozilla, Greenpeace and Amnesty International are promoting the campaign with a splash screen, which everyone can install on their pages by adding a script.

Meanwhile, thousands of social network users are readying to bombard Twitter, Facebook and Tumbrl with a giant ‘Thunderclap.’ More than 9 million of people are within the reach of the action, and it is hoped some will spread the word further. Initiated by Fight for the Future, the campaign does not simply aim to raise awareness of the encryption means necessary for secure communication online – it actually provides a detailed list of tips and software for both mobile and desktop operating systems. The listed tools and services do not promise 100% immunity against NSA snooping – but they are said to be able to make mass state surveillance difficult and economically not viable. US internet giant Google, which initially refrained from joining the campaign, has been added to the list of participants, with a note saying that the company will be “releasing email encryption tools and data, and supporting real surveillance reform.”

This land is our land to drill, not yours to protect!

• N.Y.’s Local Fracking Bans Spur Debate Before Top Court (Bloomberg)

New York’s cities and towns shouldn’t be able to block hydraulic fracturing within their borders because such prohibitions are trumped by state law, opponents of the bans told the state’s highest court. Lawyers defending such measures enacted by the upstate towns of Dryden and Middlefield argued to the Court of Appeals in Albany today that local governments are within their rights to bar fracking, which uses chemically treated water to free gas trapped in rock. If pro-fracking forces prevail, they will still face a six-year-old statewide moratorium instituted in 2008. Governor Andrew Cuomo, who inherited the ban, may decide by next year whether to lift it. If the court rules for the towns, the lifting of the state ban may instead leave a patchwork of municipalities across the nation’s third-largest state by population that allow or block the drilling method.

Fracking in states from North Dakota to Pennsylvania has helped push U.S. natural gas production to new highs in each of the past seven years, according to the U.S. Energy Information Administration, while the practice has come under increasing scrutiny from environmental advocates. Parts of New York sit above the Marcellus Shale, a rock formation that the Energy Information Administration estimates may hold enough natural gas to meet U.S. consumption for almost six years. The state barred fracking in 2008 while studying the environmental effects of the process, which is allowed in more than 30 states. Since then, more than 75 New York towns have banned fracking, while more than 40 have passed resolutions stating they support it or are open to it, according to Karen Edelstein, an Ithaca consultant affiliated with FracTracker Alliance, which analyzes the effects of oil and gas drilling.

How crazy would you like it?

• Scientists Warn Against China’s Plan To Flatten Over 700 Mountains (Guardian)

Scientists have criticised China’s bulldozing of hundreds of mountains to provide more building land for cities. In a paper published in journal Nature this week, three Chinese academics say plan to remove over 700 mountains and shovel debris into valleys to create 250 sq km of flat land has not been sufficiently considered “environmentally, technically or economically.” Li Peiyue, Qian Hui and Wu Jianhua, all from the School of Environmental Science and Engineering at Chang’an University, China, write: “There has been too little modelling of the costs and benefits of land creation. Inexperience and technical problems delay projects and add costs, and the environment impacts are not being thoroughly considered.” One of the largest projects began in April 2012 in Yan’an in the Shaanxi province, where the aim was to double the city’s area by creating an additional 78.5 sq km of land.

Local officials expect the project to generate billions of yuan from the sale or lease of the new land and spare agriculture land elsewhere in the country, which otherwise may have been used for development. Soil erosion increases the sediment content of local water sources. In Shiyan, Hubein province, pounding hills into valleys caused landslides, flooding and altered water courses. This had serious implication for the city as it lies close to the headwaters of the South-North Water Transfer project, an endeavour to divert river waters along channels to Beijing. In Langzhou, Gansu province, work was temporarily halted because of air pollution levels caused by dirt from the excavation. No one had thought to damp the soil to stop it flying in the wind. Mountain top removal has been performed before, especially in the strip mines of the eastern United States, but nothing has been performed on the scale of the Chinese earthworks.

Home › Forums › Debt Rattle June 5 2014: You Won’t Have Anyone To Blame But Yourself