NPC Ezra Meeker’s Wild West show rolls into town, Washington DC May 11 1925

“For these big banks, the fines that have been imposed amount to a parking ticket..”

• The Swiss Leaks (60 Minutes)

The largest and most damaging Swiss bank heist in history doesn’t involve stolen money but stolen computer files with more than 100,000 names tied to Swiss bank accounts at HSBC, the second largest commercial bank in the world. A 37-year-old computer security specialist named Hervé Falciani stole the huge cache of data in 2007 and gave it to the French government. It’s now being used to go after tax cheats all over the world. 60 Minutes, working with a group called the International Consortium of Investigative Journalists, obtained the leaked files.

They show the bank did business with a collection of international outlaws: tax dodgers, arms dealers and drug smugglers – offering a rare glimpse into the highly secretive world of Swiss banking. This is the stolen data that is shaking the Swiss banking world to its core. It contains names, nationalities, account information, deposit amounts – but most remarkable are these detailed notes revealing the private dealings between HSBC and its clients. Few people know more about money laundering and tax evasion by banks than Jack Blum. He’s a former U.S. Senate staff investigator. We asked him to analyze the files for us.

Jack Blum: Well, the amount of information here that has come public is extraordinary. Absolutely extraordinary. [..] If you read these notes, what you understand is the bank is trying to accommodate the secrecy needs of the client. And that’s the first concern.

Jailtime!

• HSBC Files: Swiss Bank Helped Clients Dodge Taxes And Hide Millions (Guardian)

HSBC’s Swiss banking arm helped wealthy customers dodge taxes and conceal millions of dollars of assets, doling out bundles of untraceable cash and advising clients on how to circumvent domestic tax authorities, according to a huge cache of leaked secret bank account files. The files – obtained through an international collaboration of news outlets, including the Guardian, the French daily Le Monde, BBC Panorama and the Washington-based International Consortium of Investigative Journalists – reveal that HSBC’s Swiss private bank:

• Routinely allowed clients to withdraw bricks of cash, often in foreign currencies of little use in Switzerland.

• Aggressively marketed schemes likely to enable wealthy clients to avoid European taxes.

• Colluded with some clients to conceal undeclared “black” accounts from their domestic tax authorities.

• Provided accounts to international criminals, corrupt businessmen and other high-risk individuals.The HSBC files, which cover the period 2005-2007, amount to the biggest banking leak in history, shedding light on some 30,000 accounts holding almost $120bn of assets. The revelations will amplify calls for crackdowns on offshore tax havens and stoke political arguments in the US, Britain and elsewhere in Europe where exchequers are seen to be fighting a losing battle against fleet-footed and wealthy individuals in the globalised world. Approached by the Guardian, HSBC, the world’s second largest bank, has now admitted wrongdoing by its Swiss subsidiary. “We acknowledge and are accountable for past compliance and control failures,” the bank said in a statement. The Swiss arm, the statement said, had not been fully integrated into HSBC after its purchase in 1999, allowing “significantly lower” standards of compliance and due diligence to persist.

The chance of Washington coming clean is zero.

• US Government Faces Pressure After Biggest Leak In Banking History (Guardian)

The US government will come under intense pressure this week to explain what action it took after receiving a massive cache of leaked data that revealed how the Swiss banking arm of HSBC, the world’s second-largest bank, helped wealthy customers conceal billions of dollars of assets. [..] .. the Swiss files, made public for the first time by the Guardian and other media, are likely to raise questions in Washington over whether there is evidence to prosecute HSBC or its executives in the US. Lawmakers are also expected to question the rigour of IRS investigations into undeclared assets hidden by US taxpayers in Geneva.

The IRS said it “remains committed to our priority efforts to stop offshore tax evasion wherever it occurs”, and pointed out it has collected more than $7bn from a program, introduced in 2009, that allows US taxpayers to voluntarily disclose previously undeclared offshore accounts. However the IRS declined to say how much it has retrieved in back taxes, interest and penalties as a result of investigations stemming from the leaked HSBC Swiss data. The IRS also declined to say how many US taxpayers have been investigated as a result of the leak, citing taxpayer privacy and the Tax Information Exchange Agreement (TIEA), a treaty that renders secret information shared between the US and France.

The DoJ said it “does not confirm or deny the existence of an investigation”. Senior Senate sources said government officials are likely to be questioned on Capitol Hill over what action was taken after the US received the leaked HSBC data almost five years ago. On Tuesday, Maryann Hunter, who is on the board of governors of the Federal Reserve, and has some responsibility for regulation of foreign banking organisations operating in the US, will give evidence to the Senate banking committee. Two days later, Geoffrey Graber, a deputy associate attorney general at the DoJ who oversees settlements with Wall Street banks, will appear before a House judiciary subcommittee. Both are expected to be questioned about the leak.

“The more our partners want austerity, the more the problem with the debt will get worse..“

• Greek Leader Tsipras Pledges to Press Ahead on Undoing Austerity Measures (WSJ)

Greece unveiled plans Sunday to undo several austerity measures that were a condition of its international bailout, ranging from tax cuts to increasing the minimum wage, putting the country firmly on a collision course with its European partners. In a speech to lawmakers, Prime Minister Alexis Tsipras reiterated that Greece would seek a bridge loan from its international creditors until June, refusing to accept an extension of its current bailout, as demanded by European partners. “We know very well that talks won’t be easy and that we are facing an uphill path but we believe in our abilities,” he said, presenting his newly-elected government’s policy statement to lawmakers. “The more our partners want austerity, the more the problem with the debt will get worse,“ he said.

Among the changes announced by Mr. Tsipras are raising the taxable income threshold; gradually increasing the minimum wage, starting next year; and dropping a recently introduced property tax. He also promised the retirement age wouldn’t be changed. These changes are aimed at providing the country with a growth push, he added, after the economy contracted by about a quarter in the last five years and unemployment shot up to more than 25%. It is not clear, however, where the savings will come from in order to pay for these changes, given that Mr. Tsipras promises that the country will avoid creating fresh budget deficits. Greece’s current €240 billion rescue runs out at the end of the month, and the government has warned it could run out of money in weeks unless it can gain access to additional funds.

The Greek government also has said that it wants to change the terms of its funding agreement, which require the new leftist government to adhere to austerity measures agreed to by its predecessors. But Greece’s partners in the European Union—led by Germany—have insisted that promises made by the previous Greek government have to be kept if Athens wants to receive further assistance. Eurozone officials have asked Greece to come up with a specific funding plan by Wednesday, when finance ministers, meeting in Brussels, will try to move closer to a deal on the paralyzed bailout program. A day later, Mr. Tsipras will sit down for his first talks with German Chancellor Angela Merkel at a European summit in Brussels.

The oracle comes clean with his last breath.

• Greenspan Predicts Greece Exit From Euro Inevitable (BBC)

The former head of the US central bank, Alan Greenspan, has predicted that Greece will have to leave the eurozone. He told the BBC he could not see who would be willing to put up more loans to bolster Greece’s struggling economy. Greece wants to re-negotiate its bailout, but Mr Greenspan said “I don’t think it will be resolved without Greece leaving the eurozone”. Earlier, UK Chancellor George Osborne said a Greek exit would cause “deep ructions” for Britain. Mr Greenspan, chairman of the Federal Reserve from 1987 to 2006, said: “I believe [Greece] will eventually leave. I don’t think it helps them or the rest of the eurozone – it is just a matter of time before everyone recognises that parting is the best strategy.

“The problem is that there there is no way that I can conceive of the euro of continuing, unless and until all of the members of eurozone become politically integrated – actually even just fiscally integrated won’t do it.” Following the election in Greece of the anti-austerity Syriza party, Greek ministers have been touring European capitals trying to drum up support for a re-negotiation of its bailout terms. However, there appears little willingness in Berlin, or at the European Central Bank, to alter the terms of its €240bn rescue by the EU, ECB and IMF. “The [bailout] conditions with Greece were generous, beyond all measure,” German Finance Minister Wolfgang Schaeuble said last week. He saw no justification for relaxing them further. Mr Greenspan said: “All the cards are being held by members of the eurozone.”

He also warned that trying to hold the 19-nation euro bloc together “is putting strain on everybody”. He said as well as Greece leaving the eurozone, there was a real risk of a “much bigger break-up” with other southern European countries forced out. Alan Greenspan has long been a critic of the European single currency. Now, the 88-year-old former chairman of the US Federal Reserve has repeated a claim that nothing short of full political union – a United States of Europe – can save the euro from extinction. Given that few (if any) of the current 19 sovereign governments which make up the eurozone would choose to create such an entity at this time, that means – for Greenspan at least – the euro is doomed. Before all that, though, he foresees Greece quitting the single currency, but the euro surviving intact. Grexit, he says, is more manageable now than it would have been when Greece got its first EU bailout in 2010.

“The euro is fragile, it’s like building a castle of cards, if you take out the Greek card the others will collapse.”

• Greek Finance Minister Says Euro Will Collapse If Greece Exits (Reuters)

– If Greece is forced out of the euro zone, other countries will inevitably follow and the currency bloc will collapse, Greek Finance Minister Yanis Varoufakis said on Sunday, in comments which drew a rebuke from Italy. Greece’s new leftist government is trying to re-negotiate its debt repayments and has begun to roll back austerity policies agreed with its international creditors. In an interview with Italian state television network RAI, Varoufakis said Greece’s debt problems must be solved as part of a rejection of austerity policies for the euro zone as a whole. He called for a massive “new deal” investment program funded by the European Investment Bank.

“The euro is fragile, it’s like building a castle of cards, if you take out the Greek card the others will collapse.” Varoufakis said according to an Italian transcript of the interview released by RAI ahead of broadcast. The euro zone faces a risk of fragmentation and “de-construction” unless it faces up to the fact that Greece, and not only Greece, is unable to pay back its debt under the current terms, Varoufakis said. “I would warn anyone who is considering strategically amputating Greece from Europe because this is very dangerous,” he said. “Who will be next after us? Portugal? What will happen when Italy discovers it is impossible to remain inside the straitjacket of austerity?”

Varoufakis and his Prime Minister Alexis Tsipras received friendly words but no support for debt re-negotiation from their Italian counterparts when they visited Rome last week. But Varoufakis said things were different behind the scenes. “Italian officials, I can’t tell you from which big institution, approached me to tell me they backed us but they can’t tell the truth because Italy also risks bankruptcy and they are afraid of the reaction from Germany,” he said. “Let’s face it, Italy’s debt situation is unsustainable,” he added, a comment that drew a sharp response from Italian Economy Minister Pier Carlo Padoan, who said in a tweet that Italy’s debt was “solid and sustainable.”

Pretty ugly.

• If Greece Exits, Here Is What Happens – Redux (Zero Hedge)

Now that the possibility of a Greek exit from the euro is back to being topic #1 of discussion, just as it was back in the summer of 2012 and the fall of 2011, and investors are propagandized by groundless speculation posited by journalists who have never used excel in their lives and are merely paid mouthpieces of bigger bank interests, it is time to rewind to a step by step analysis of precisely what will happen in the moments before Greece announces the EMU exit, how the transition from pre- to post- occurs, and the aftermath of what said transition would entail, courtesy of one of the smarter minds out there at the time (before his transition to a more status quo supportive tone), Citi’s Willem Buiter, who pontificated precisely on this topic previously. Three words: “not unequivocally good.” From Willem Buiter (2012): What happens when Greece exits from the euro area?

Were Greece to be forced out of the euro area (say by the ECB refusing to continue lending to Greek banks through the regular channels at the Eurosystem and stopping Greece’s access to enhanced credit support (ELA) at the Greek central bank), there would be no reason for Greece not to repudiate completely all sovereign debt held by the private sector and by the ECB. Domestic political pressures might even drive the government of the day to repudiate the loans it had received from the Greek Loan Facility and from the EFSF, despite it having been issued under English law.

Only the IMF would be likely to continue to be exempt from a default on its exposure, because a newly ex-euro area Greece would need all the friends it could get – outside the EU. In the case of a confrontation-driven Greek exit from the euro area, we would therefore expect to see around a 90% NPV cut in its sovereign debt, with 100% NPV losses on all debt issued under Greek law, including the debt held, directly or directly, by the ECB/Eurosystem. We would also expect 100% NPV losses on the loans by the Greek Loan Facility and the EFSF to the Greek sovereign.

Everyone is, of course.

• UK Is Readying Contingency Plans for Possible Greek Eurozone Exit (WSJ)

The U.K. government is stepping up contingency planning to prepare for a possible Greek exit from the eurozone and the market instability such a move would create, U.K. Treasury chief George Osborne said on Sunday. The U.K. government has said the standoff between Greece’s new antiausterity government and the eurozone is increasing the risks to the global and U.K. economy. “That’s why I’m going tomorrow to the G-20 [Group of 20] to encourage our partners to resolve this crisis. It’s why we’re stepping up the contingency planning here at home,” Mr. Osborne told the BBC in an interview. “We have got to make sure we don’t, at this critical time when Britain is also facing a critical choice, add to the instability abroad with instability at home.”

Mr. Osborne is on Monday heading to Istanbul for talks with other finance officials from the G-20. Alan Greenspan , former chairman of the U.S. Federal Reserve, said in a separate interview that he believed Greece would eventually leave the eurozone. He told the BBC he couldn’t see who would be willing to put up more loans to bolster the country’s struggling economy. “I believe [Greece] will eventually leave. I don’t think it helps them or the rest of the eurozone—it is just a matter of time before everyone recognizes that parting is the best strategy,” he was quoted as saying by the BBC.

Ahead of the U.K. general election in May, Prime Minister David Cameron and Mr. Osborne have used the Greek situation to argue their case for a continuation of the government’s austerity plans. Mr. Osborne noted that Greece had chosen to stay in the eurozone and had worked hard to do so. “If Greece left the euro that would create real instability in financials markets in Europe,” he said. “That’s why we have got to avoid this crisis getting out of control, which is why we have got to make sure we have an international effort to resolve the standoff and here in Britain we step up our contingency planning to prepare for whatever is thrown at us.”

“In the 1920s, according to a prominent German economic historian, Germany was “like Greece on steroids.”

• Historically Speaking Germany A Bigger Deadbeat Than Greece (Joe Schlesinger)

In its attempt to bust the austerity shackles that lenders have imposed, Greece’s new leftist government is finding a particularly unsympathetic ear in Germany, the EU’s paymaster, which says it is done writing off Greek debt. That warning from German Chancellor Angela Merkel and others is overwhelmingly backed by a German public outraged by the contrast between Greece’s spendthrift ways, with its penchant for treating tax bills as junk mail, and their own obsession with a tight hold on the purse strings, both personal and as a country. What the Germans are conveniently ignoring is their own record as one of history’s biggest deadbeats. In the 1920s, according to a prominent German economic historian, Germany was “like Greece on steroids.”

Albrecht Ritschl, a professor at the London School of economics and adviser to Germany, says that Germany’s current prosperity was built on borrowed — mostly American — money, much of it written off. It all started in 1918 when Germany lost the First World War. In the peace settlement that followed, the victors exacted payment of 269 billion marks or 96,000 tonnes of gold. Mirroring the Greeks’ current sentiments regarding debt repayment and forced austerity, Germans after WWI saw the reparations as a national humiliation and rejected the validity of that Versailles Treaty. They did pay, though. But they made their payment by printing ever more money, which led to the kind of hyperinflation where money was carried around in suitcases. By 1923, one U.S. dollar was worth billions of marks. In Berlin, a streetcar ticket cost 15 billion marks.

The collapse of the German economy led to the demise of the country’s Weimar Republic democracy and the rise of Adolf Hitler, who promptly stopped the payments once he came to power. It is often said that the debacle of the Versailles settlement thus led directly to Second World War. But once that war was over, with Germany having lost again, the lesson of Versailles was finally heeded. Instead of punishing the Germans, the victorious Western allies decided to help them get back on their feet again. Not all Germans, of course, because by that time the country was divided between the Soviet satrapy of Communist East Germany and the budding democracy of West Germany. The Cold War was on, and the allies wanted to make sure that Western Europe didn’t succumb to Joseph Stalin, as it had a decade earlier to Hitler and his collaborators. The problem, though, was that Western Europe lay in ruins and its people were starving. There was only one possible rescuer — the U.S.[..]

In 1947, the U.S. Congress voted $13 billion in aid to the Europeans, a massive sum at the time. The Germans got $1.45 billion of that money. They were also allowed to put off paying, and indeed never did fully repay the money they already owed to other Europeans as well as the Americans. [..] As for the money they owed, in 2010 the Germans made a last payment of €69.9 million to settle all their debts from both wars. That settlement, though, was more symbolic than real as the original debt was repeatedly reduced over the decades.

“..nor does she want to be the politician responsible for rolling back more than half a century of closer European integration.”

• A Greece Debt Deal Is By All Means Not Impossible (Guardian)

Tsipras is not going to get everything he wants. He might only get a fraction of what he wants. But he will get something. Why? Because this is Europe, where horse-trading and deal-making is the natural order of things. Because the Greek people have spoken by voting for Syriza. Because there is an acceptance that the country has suffered grievously in the past five years. But, above all, because sending Tsipras off with a flea in his ear would mean risking Greece leaving the eurozone. And nobody wants that: not Juncker, not Mario Draghi, not Angela Merkel. The German chancellor may not be prepared to offer Tsipras much, but nor does she want to be the politician responsible for rolling back more than half a century of closer European integration.

A deal will be done despite what appeared to be a hardening of positions in the second half of last week. The mood darkened after the European Central Bank said it would no longer accept Greek bonds as collateral for lending to Greek banks. That was seen as an aggressive act, since it means the Greek central bank will have to provide its own emergency assistance at a higher interest rate. And even that source of funding could be ended by the ECB if it thought there was no prospect of a deal between Athens and its eurozone partners. Were this to happen, it would precipitate a financial crisis. Greece’s banks would become insolvent very quickly, leaving Tsipras with the choice of either abject surrender or exit from the euro, followed by debt default and devaluation.

It is, though, unlikely to get to this point. Indeed, there are some commentators – such as the US prizewinning economist Paul Krugman – who believe that far from being a crude act of belligerence this was actually another one of Draghi’s subtle ploys, designed to make it clear to Merkel just how close the eurozone was to losing one of its 19 members. By refusing to be provoked by the ECB move, Tsipras and his finance minister, Yanis Varoufakis, pitched their response just about right. That said, any concessions to Greece will be limited. That was clear in the two days I spent in Brussels last week talking to officials and politicians. Valdis Dombrovskis, commissioner for the euro and social dialogue, said: “We are respecting the democratic choice of the Greek people. The European commission is willing to engage with Greece. The basis of the negotiations is that all sides stick with their own commitments.”

Merkel has largely morphed into a tool.

• War and Default in Europe Pose Merkel’s Biggest Challenge (Bloomberg)

After almost a decade as German chancellor, Angela Merkel faces a moment of truth as a resurgent Russia and fed-up Greeks challenge her blueprint for Europe’s future. As bloodshed in eastern Ukraine escalates and the new Greek government rejects austerity championed by Merkel, her deliberate leadership style may be reaching the limit of its effectiveness. With Europe’s post-Cold War order and its unifying currency at stake, the weight of global and domestic expectations is pushing Merkel out of her comfort zone and into two direct confrontations. Both adversaries and allies have repeatedly underestimated Merkel’s determination as she rose from obscurity in an East German lab to become the world’s most powerful woman.

“It underscores how much Germany is really the pivotal power in Europe and Angela Merkel is the pivotal leader,” Daniel Hamilton, head of the Center for Transatlantic Relations at the Paul H. Nitze School of Advanced International Studies in Washington, said in an interview. “Much of it has to do with Germany’s success, but much of it also has to do with default by other powers. It’s not like she or Germany aspires to this role.” Merkel’s status as Europe’s go-to leader will be on display when President Barack Obama hosts her at the White House on Monday. In the run-up, she’s resisting pressure by U.S. politicians to send arms to Ukraine’s government. The biggest risk for Merkel is if either crisis spiraled out of control. At that point, she would have failed to address “German concern about stability,” Hamilton said.

While Merkel, 60, doesn’t deliver grand visions of European unity and reconciliation like her mentor Helmut Kohl, she has a practical set of values that are now under threat. For the 19-nation currency bloc, her goal is to make economies from Greece to Ireland more like her export-driven powerhouse. She says changes are vital to adapt to globalization and Europe’s aging populations. Even so, bailouts she backed have spawned a challenge by the anti-euro Alternative for Germany party that limits her leeway for cutting another deal with Greece.

They all start to admit their failures, but still insist Greece pay for them.

• Obama Joins the Greek Chorus (Ashoka Mody)

US President Barack Obama’s recent call to ease the austerity imposed on Greece is remarkable – and not only for his endorsement of the newly elected Greek government’s negotiating position in the face of its official creditors. Obama’s comments represent a break with the long-standing tradition of official American silence on European monetary affairs. While scholars in the United States have frequently denounced the policies of Europe’s monetary union, their government has looked the other way. Those who criticize the euro or how it is managed have long run the risk of being dismissed as Anglo-Saxons or, worse, anti-Europeans. British Prime Minister Margaret Thatcher accurately foresaw the folly of a European monetary union. Gordon Brown, as British Chancellor of the Exchequer, followed in Thatcher’s footsteps.

When his staff presented carefully researched reasons for not joining the euro, many Europeans sneered. And that is why Obama’s statement was such a breath of fresh air. It came a day after German Chancellor Angela Merkel said that Greece should not expect more debt relief and must maintain austerity. Meanwhile, after days of not-so-veiled threats, the European Central Bank is on the verge of cutting funding to Greek banks. The guardians of financial stability are amplifying a destabilizing bank run. Obama’s breach of Europe’s intellectual insularity is all the more remarkable because even the IMF has acquiesced in German-imposed orthodoxy. As IMF Managing Director Christine Lagarde told the Irish Times: “A debt is a debt, and it is a contract. Defaulting, restructuring, changing the terms has consequences.”

The Fund stood by in the 1990s, when the eurozone misadventure was concocted. In 2002, the director of the IMF’s European Department described the fiscal rules that institutionalized the culture of persistent austerity as a “sound framework.” And, in May 2010, the IMF endorsed the European authorities’ decision not to impose losses on Greece’s private creditors – a move that was reversed only after unprecedented fiscal belt-tightening sent the Greek economy into a tailspin. The delays and errors in managing the Greek crisis started early. In July 2010, Lagarde, who was France’s finance minister at the time, recognized the damage incurred by those initial delays, “If we had been able to address [Greece’s debt] right from the start, say in February, I think we would have been able to prevent it from snowballing the way that it did.”

The US, too, is at risk.

• Bernie Sanders Asks Janet Yellen to Explain Her Apparent Inaction on Greece (NC)

Senator Bernie Sanders issued a letter over the weekend asking Janet Yellen to “make it clear to the leadership of the European Central Bank that the United States and the Federal Reserve object to actions that affect our national interest and risk U.S. and global financial stability through the unnecessary and counterproductive implementation of deflationary policies.” The full letter is embedded below. Also note that Senator Sanders wrote Christine Lagarde at the IMF on January 28, two days after Syriza’s victory, expressing his concern about the humanitarian costs and political risks of continuing to pursue failed austerity policies. If you are a Vermont voter, please e-mail him and thank him for taking this stand. And the rest of you who are moved to help, please write Hillary Clinton’s office and ask why, as the Democratic party Presidential nominee-in-waiting, why she is silent on this important topic.

Greece 2.

• In The Eternal City, The Euro Remains The Eternal Problem (Guardian)

You see, for decades, the Italian economy trundled along quite nicely, with a strong industrial sector, a great name for design, and the ability to devalue the lira from time to time, when wages got out of control and international competitiveness suffered. That is to say, for all its “structural rigidities” and “Italian practices”, the economy performed reasonably well. In recent decades, it has been hit by a succession of blows, not least the financial crisis – which struck after great strides had been made in reducing the budget deficit – and the economic straitjacket of the eurozone. Membership of the single currency not only removes the freedom to devalue against, for example, Germany: it also subjects Italy to the kind of fiscal sadism against which the Greeks have just revolted.

The many “rigidities” of Italy’s economy are highlighted in the film Girlfriend in a Coma, made by Annalisa Piras and former Economist editor Bill Emmott, described by Le Monde as “a desperate love letter to Italy”. Well, the Italians are having another go. One reform which might not be too popular with Pessina is yet another attempt to crack down on tax avoidance – generally considered something of a national sport. They are trying to speed up the justice system as part of an effort to stimulate more inward investment, and – especially important for so many of the young, who are effectively excluded from the labour market – the Renzi administration aims to reduce the imbalance in labour contracts between those with a “job for life” and those desperate to get a job.

Meanwhile, rays of hope as the sun was setting in Venice last Saturday were: first, although Italy cannot devalue against Germany, the entire eurozone may gain some relief from both the ECB QE programme – boosting money and credit – and the devaluation of the euro. Then there is the potential boost to spending from the lower oil price.Nevertheless, macroeconomic policy in the eurozone remains far too restrictive. I think we are talking of alleviation of the Italian economy’s problems, rather than a cure.

In your dreams: “Appropriate tax relief or state guarantees on assets backed by bad debts would smooth the way for the creation of a private market in non-performing loans..”

• Italy Lenders Seen Cleansing Books Amid Bad-Bank Plans (Bloomberg)

Italian banks, under pressure to bring their balance sheets in line with the ECB’s health check, will probably set aside billions more for loan losses in the fourth quarter as the government considers a national plan for offloading their troubled assets. Banca Monte dei Paschi the weakest performer in the 130-bank review, is likely to almost triple its loan-loss provisions to €3.2 billion, according to the average of six analyst estimates compiled by Bloomberg for Italy’s third-biggest bank. In total, the top five banks may set aside about €8 billion, estimates show.

The nation’s lenders are saddled with a record €181 billion of nonperforming loans that are hindering their ability to expand lending and holding back the country’s recovery from its third recession in six years. More than two years after the balance-sheet clean-up started, the government is considering creating a bad bank to accelerate disposals of problematic assets. Government support would help generate economic growth, Bank of Italy Governor Ignazio Visco said Saturday. “Appropriate tax relief or state guarantees on assets backed by bad debts would smooth the way for the creation of a private market in non-performing loans,” he said in a speech in Milan.

“A bad bank vehicle combined with structural reforms would be a key tool to improve Italian bank profitability,” analysts at Morgan Stanley including Francesca Tondi wrote in a report Friday. Fabrizio Bernardi, an analyst at Fidentiis Equities, said banks with a lower-than-average asset quality profile would benefit the most from a bad bank. All five banks are scheduled to publish fourth-quarter earnings this week. Leading the pack, UniCredit and Intesa Sanpaolo will probably set aside about €3 billion between them. Both banks posted full-year losses in 2013 after writing down billions of non-performing loans. Banco Popolare, the country’s fifth-biggest lender, may post €1.27 billion in provisions, according to the surveys.

Boo hoo hoo.

• US Banks Say Soaring Dollar Puts Them at Disadvantage (WSJ)

The strengthening U.S. dollar is rippling through the financial system in unexpected ways, revealing what bankers say is a hidden flaw in a Federal Reserve proposal to increase capital cushions at the nation’s largest banks. Big U.S. banks say that, under the rule proposed in December, the recent steep rise in the dollar’s value would force some U.S. firms to hold billions of dollars more in capital than foreign competitors, including weaker European banks, because of how the Fed plans to calculate a so-called surcharge levied on the eight most systemically important U.S. banks. The Fed rule is aimed at forcing big banks to add extra layers of financing to protect against losses.

The banks believe it would wind up penalizing U.S. banks if the dollar remains strong against the euro, as many economists expect, because the high exchange rate makes their dollar-denominated assets and operations look larger relative to their European peers. Officials from banks including Citigroup, Goldman Sachs, Bank of America and Morgan Stanley met privately with Fed officials in January to discuss the threat and other concerns about the rule, according to people who attended. The banks plan to file an official comment letter later this month detailing those concerns and seeking changes to how the proposal calculates the extra capital required. The currency’s potential impact on big U.S. banks is the latest example of how a strengthening dollar is affecting the U.S. economy.

The strong dollar is hitting the profits and sales of a wide swath of corporate America, including firms that expanded overseas aggressively, like consumer-products giant Procter & Gamble and pharmaceuticals company Pfizer, but are now finding that sales abroad are suffering or not keeping up with dollar-based costs. The impact has weighed on U.S. stocks and raised worries about the health of the U.S. economy. U.S. banks say the currency volatility exposes underlying problems with the Fed’s proposal, which is aimed at forcing banks to shrink by putting a price on bigness but ties their capital requirements in part to forces beyond their control. Banks have already expressed concern that the Fed’s surcharge proposal is tougher than what European regulators are expected to require.

In dollar terms.

• Global Economy Will Shrink By $2.3 Trillion In 2015 (Zero Hedge)

Via BofAML: The $2.3 Trillion Global GDP Write-Off

Global nominal GDP is likely to contract by about $2.3tn in 2015, a consequence of the USD strengthening. It will be the sixth time since 1980 that global nominal GDP contracts in dollar terms and the second biggest contraction since 2009. This change will have far reaching implications across markets, principally for commodity prices. The world is going to be about $2.37tn smaller in 2015 than what we thought when we prepared our Year Ahead forecasts. This is not insignificant, as it represents 3.2% of last year’s estimated global GDP. For perspective, that would be as if an economy of the size between Brazil’s and the UK’s would have just disappeared.

In our calculation, we include the US, the Euro area, Japan, the UK, Australia, Canada and all the emerging markets we cover. Together they totaled $70.9tn last year, or 91% of the world output as measured by the IMF. The change is mostly attributed to the stronger USD. We barely changed our real growth forecasts from the time of the Year Ahead publication. In fact, we expect global real growth to accelerate to 3.5% in 2015 from 3.3% in 2014. The number of goods and services produced will increase at a faster rate; it is just that most of them are going to be produced in countries where the currency has weakened against the USD, and will continue to weaken, according to our forecast.

“The dilemma for the People’s Bank of China is how to keep liquidity flowing without prompting more outflows.”

• Trouble For China As Money Flows Out (MarketWatch)

China’s reserve requirement cut last week failed to provide much of a lift as it was more about replacing hot money outflows than adding new money. It also helped to bring into focus the central bank’s tricky position: In an environment of capital outflows how do you fine-tune policy so that both a credit crunch and currency crunch are avoided? Without signs the economy is regaining momentum, investors should watch out for unexpected policy moves — such as meaningful currency depreciation or new measures to trap capital inside its borders. Concerns will be compounded by terrible trade figures released at the weekend, with exports unexpectedly down 3.3% in January from a year earlier and imports falling almost 20%.

After running the reserve-reduction numbers, analysts poured cold water on last week’s half-percentage-point cut, as it merely tops up liquidity after recent outflows. Fitch Ratings calculates the 570 billion yuan ($91.4 billion) freed up almost equals exactly the 575 billion yuan in net capital outflows in 2014. The dilemma for the People’s Bank of China (PBOC) is how to keep liquidity flowing without prompting more outflows. If it loosens aggressively during a period of capital outflows and dollar strength, this could just help facilitate capital flight. Expectations of a weakening yuan would also have the same effect.

Here, the consensus remains that authorities will be resolute in defending the loosely pegged exchange rate, with Bank of America saying it expects the PBOC will stabilize the rate in order to stem capital flight. Keeping the currency stable is widely viewed as a key policy objective of Beijing as it seeks to elevate the yuan to a means of settlement for international trade and even as a reserve currency. What’s more, Chinese corporations hold a sizeable amount of foreign-currency debt. However, analysts warn that pressure is building on the exchange rate. TD Securities estimates monetary conditions in China are the tightest in a decade, with a real effective exchange rate at 15-year highs and growth in credit at decade lows. January’s decline in exports will put the yuan’s level under renewed scrutiny.

“We suggest you take a look at a chart of Chinese retail margin debt, but not just right before bedtime. It looks something like the U.S. figures heading for 1929.”

• Citi Fears 23% Downside Correction in Chinese Stocks (Zero Hedge)

The Chinese stock market is “looking prercarious” according to Citi FX Technicals’ team. A bearish outside day on the Shanghai Composite could represent just the first of a series of technical patterns that suggest a potential 23% correction… as 100s of thousands of newly minted margin’d retail equity ‘investors’ find out the hard what a tap on the shoulder feels like. As Paul Singer warned, “take a look at a chart of Chinese retail margin debt, but not just right before bedtime. It looks something like the U.S. figures heading for 1929.” Via Citi FX,

• The Shanghai Composite Index posted a bearish outside day in today’s trading

• This suggests a return to the recent low from January 14th at 3,095. A breach of that level would confirm a double top that would target a decline to 2,785

• Such a move would break through the 55dMA for the first time since July 2014 (on a closing basis).

• Given the stretched moving average dynamic a breach of the 55dMA would leave the way open for a move to the 2,415 – 2,445 range, where the 200dMA converges with support from the February 2013 high

Everything’s fine…

Perhaps – more fundamentally speaking – Elliott’s Paul Singer sums it up best… “A universal belief underlying global financial markets is that the Chinese government has complete control over its economy and financial system. We cannot know whether the corruption, bad loans, see-through projects, and internal dynamics of the Chinese system are bad, very bad, or headed for a crack-up, but any set of developments that challenge the widespread assumption of complete Chinese control over its destiny would be a very large shock to global markets.

We suggest you take a look at a chart of Chinese retail margin debt, but not just right before bedtime. It looks something like the U.S. figures heading for 1929. But there is no way for outsiders to know the net of the balance of forces, and whether the negatives are overwhelmed by the Chinese economic growth juggernaut. To paraphrase Senator Everett Dirksen: A trillion dollars of margin debt, a couple of trillion dollars of sour loans, a trillion dollars of wasted capital projects, and pretty soon you are talking about real money.”

“Although consumers are better off than they’ve been in years, they sure haven’t acted like it.” That’s because they’re only better off in accounting models.

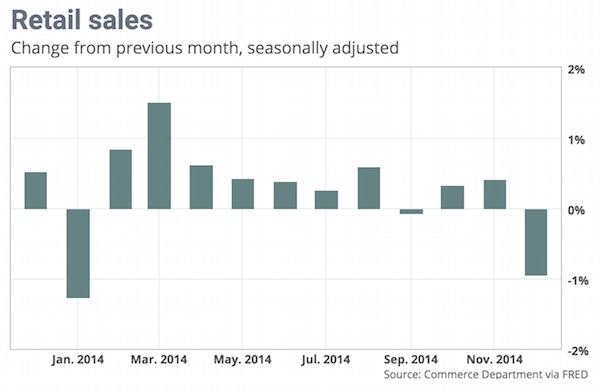

• Will US Consumers Ever Go On Spending Spree? (MarketWatch)

There are more jobs now, for more money, than any time since the recession ended in mid-2009. Gas prices are at a six-year low, while the stock market is near near an all-time high. The question is whether Americans will spend that newfound wealth. So far, the answer has been no. The pace of consumer spending continues to disappoint even though unemployment has tumbled below 6% and U.S. added 3.1 million jobs in 2014 — the biggest gain since 1999. Although consumers are better off than they’ve been in years, they sure haven’t acted like it. Americans are still saving more and shopping frugally. Just look at what’s happened in the past few months. The savings rate rose in December to 4.9% to mark the highest level since midsummer, government data showed.

At the same time, both retail sales and consumer spending fell sharply. There’s a big asterisk to that last factoid: in both cases the negative readings reflected lower prices, namely at the gas pump. Even so, inflation-adjusted consumer spending fell slightly in December. Which again raises the question heading into Thursday’s report on retail sales. When will consumers start to spend that extra cash — and pump up the U.S. economy? Retailers seem to expect it will happen soon, as they’ve added 113,000 new positions over the last three months. Traders are expecting the headline figure again to decline in January, reflecting the lower revenue coming in for gas stations. Auto sales also will be lower, according to what the auto companies themselves have reported.

“..the US deflation threat is every bit as immediate as that in the eurozone.”

• Albert Edwards: Core Inflation In The US And Europe Are The Same (Zero Hedge)

.. one thing the SocGen strategist revealed which most certainly was not widespread public knowledge is that if one uses the inflation-measurement methodology of Europe, then not only is core CPI in the US below that of “deflationary” Europe, but is in fact negative! The US deflationary predicament, which is hiding between the lines, is why Edwards maintains his “view that the market is far too convinced that the US is in the spring of its economic recovery, whereas I believe we could well be in the autumn. What matters though is not my view, but the overconfidence of investors together with the very rich equity valuations.” The catalyst would be investor realization “that, despite the US having recently been the single engine of global growth, the US deflation threat is every bit as immediate as that in the eurozone.” Edwards explains:

The US CPI shelter component is made up of rent (7% of total CPI) and owner-occupier equivalent rent (OER, a massive 24% of the CPI). Now, when we exclude food and energy from the CPI we often hear people complain that we shouldn’t as food and energy are real expenditures that cannot be avoided. In contrast, the OER is a totally made-up number which no homeowner actually pays! OER is meant to measure the implied rent they incur by living in their home rather than renting it out – economists debate its inclusion in the CPI.

Typically OER mirrors actual rents which tend to lag house price inflation, which rose strongly in 2013 but is now slowing sharply. Hence OER inflation will probably slow too this year, revealing the underlying deflation threat. But whatever the whys and wherefores, the bottom line is simple – OER is not part of the eurozone CPI and to compare like-with-like we should exclude it. If we do, the yoy rate of core US CPI inflation is the same as in the eurozone.

But, perhaps more significantly, the 6m change in core US CPI inflation (using the eurozone definition) is actually already negative, unlike the eurozone series. Who then do you think has the bigger deflation problem ? the US or the eurozone? Which sadly means that not only all those “whopping” job gains of the past 3 months will be promptly “seasonally-adjusted” away during the next major revision opportunity, but that all the talk of a rate hike at a time when the US has a worse deflation problem than the Eurozone, will quickly and quietly disappear.

“..the thinktank’s annual “Going for Growth” report..” Oh boy..

• OECD: Changes Must Cut Inequality, Not Just Boost Economic Growth (Guardian)

Politicians must focus on policies that ensure stronger economic growth goes hand in hand with fairer distribution of the gains if they are to stem rising inequality, a leading economic thinktank has said. Analysing the effects of pro-growth policies on inequality, the Paris-based Organisation for Economic Co-operation and Development (OECD) has identified widening gaps in wealth distribution in many rich nations, with the the poorest hardest hit. The OECD urges governments to prioritise policies that help reduce inequality while also boosting growth, such as more education for low-skilled workers and measures to get more women into work.

The recommendations, part of the thinktank’s annual “Going for Growth” report, are being unveiled in Istanbul on the first day of the G20 finance ministers’ meeting. The OECD suggestion that some pro-growth policies have widened inequality will further fuel the heated debate over how countries can best restore sustainable economic growth six years after the global financial crisis. “The financial crisis and continued subdued recovery have resulted in lower growth potential for most advanced countries, while many emerging-market economies are facing a slowdown,” says the report. “In the near term, policy challenges include persistently high unemployment, slowing productivity, high public-sector budget deficit and debt, as well as remaining fragilities in the financial sector.

The crisis has also increased social distress, as lower-income households were hit hard, with young people suffering the most severe income losses and facing increasing poverty risk.” The report comes as Greece’s new leftwing government faces off with its international creditors and argues that relentless cuts under the terms of its bailout package have stifled the economy and caused widespread hardship. The OECD report highlights large increases in income inequality and poverty in Greece, alongside other countries hit hardest by the crisis: Iceland, Ireland and Spain.

Understatement of the year; “Treasuries are “becoming detached from U.S. economic fundamentals..”

• US Locks In Cheap Financing (Bloomberg)

Uncle Sam is going long. As the insatiable demand for Treasuries pushes down yields, the U.S. has locked in low-cost financing for years to come by issuing more long-term debt. The average maturity of Treasuries is now poised to reach an all-time high this year. The shift is saving money for American taxpayers – but it’s also made Treasuries more perilous for bond investors as the strength of the U.S. economy bolsters the Federal Reserve’s case for raising interest rates. Holders stand to lose about $570 billion if yields rise by a%age point, data compiled by Bloomberg show. In 2009, it was $170 billion. Treasuries are “becoming detached from U.S. economic fundamentals,” said William Irving at Fidelity Investments, which oversees about $2 trillion. “I don’t think it’s a great time to buy.”\

Long-term Treasuries have been some of the best investments around in the past year as oil tumbled, deflation emerged in Europe and a global slowdown threatened to drag on the U.S. recovery. The 30-year bond, the longest maturity security issued by the Treasury, returned 29%, double that for U.S. equities. The rally accelerated in 2015, pushing down yields to a record-low 2.22% on Jan. 30. A year ago, yields were closer to 4%. The demand for long bonds helped the Obama administration trim the nation’s short-term borrowing, which ballooned as U.S. ran trillion-dollar deficits to restore demand after the credit crisis. Treasuries due three years or less make up 48% of the market for U.S. debt, versus 58% six years ago.

The share of bills, due in one year or less, is approaching the least since the 1950s. That’s given the U.S. more time to repay its obligations. The average maturity has reached 68.7 months, or two months short of its high in 2001. With the U.S. budget deficit falling to a six-year low, the government is in better shape to finance its record debt burden when interest rates do rise.

Home › Forums › Debt Rattle February 9 2015