davefairtex

Forum Replies Created

-

AuthorPosts

-

October 27, 2012 at 1:12 am in reply to: Japan Is Not A Good Example Of How Deflation Typically Plays Out #6160

davefairtex

Participantprofessor –

Not to scare the horses indeed.

If things go really badly south (meaning, if major institutions whose short-term repo instruments fill the money market funds go BK the way Lehman did) the fifty cents on the buck event could happen.

The funds are a bit smarter this time around – they’ve dropped euro banks from their dance cards, which I think will address the first wave of issues. But if I see tensions rising severely, you can bet my digital cash will run and hide in a short term treasury. Treasury Direct. Fewest middle men involved, and hopefully the last thing to get thrown under the bus. Its that or a demand deposit account.

Note that buying a short term treasury and stuffing it in your brokerage account will avoid losses from your money market fund breaking the buck, but it will NOT address the problem of the broker going under. Case: MF Global bankruptcy, where MFG customers who had physical gold bars (paying storage fees, no less!) became general creditors in the bankruptcy losing the same 20-something percent off their account balances as everyone else. Best to have a sturdy broker who doesn’t play funny games with hypothecating customer assets.

Note also the Treasury Direct purchase should probably occur a number of days prior to the emergency, or else the ACH transaction from your bank might not go through – or it might get reversed, etc. And some auctions only happen weekly, so…probably best not to cut things too fine.

Probably best to have a plan in place, with all the abilities to transfer assets tested ahead of time, understanding the delays involved.

Rules of Trading:

Rule #1: don’t panic!

Rule #2: when a panic is going to happen, make sure you panic first.October 25, 2012 at 6:27 pm in reply to: Japan Is Not A Good Example Of How Deflation Typically Plays Out #6150Participantbackwards –

I went through a phase where I had trouble sleeping too. The trick I finally learned is, the number of scenarios where it all goes bad overnight from a largely stable position (i.e. a “bolt from the blue”) are few. Likely, we’ll have some warning first.

Right now, believe it or not, things are more or less stable. Unsustainable, but stable.

In the meantime, just steadily work to increase your basic level of preparedness. Lower debt, have cash on hand, increase food & water reserves, basic physical fitness, that kind of thing.

I’m actually working on a sort of early warning system – just for my own peace of mind. The bits and pieces I’ve developed so far do help me to relax.

October 25, 2012 at 12:48 pm in reply to: Japan Is Not A Good Example Of How Deflation Typically Plays Out #6145Participantbackwards –

Savings middle men: anyone standing between you, and your savings. Another way to look at it is, anyone who could potentially say “no” to your demand to get your stored value. NO you can’t withdraw that much cash today. NO you can’t withdraw your savings for the next 60 days. NO our institution is closed today. Or this week. Or until further notice. NO, we’re going through bankruptcy and we’ll let you know in 2 years what share you receive as a general creditor. NO, we don’t actually have your allocated gold bars, even though we’ve been charging you storage fees for the past 10 years. NO, we’ve suspended withdrawls from your money market account due to our holdings in Lehman repos.

All actual cases. 1) normal bank policy on cash withdrawls. 2) standard savings account agreement. 3) bank holiday, 1933. 4) MF Global BK. 5) Morgan Stanley, 2007. 6) The Reserve, 2008.

If a major crisis happens in the financial system, your savings better not be stored by middle men – by anyone who could say NO to you.

TAE envisions that such a crisis is inevitable and must follow the credit bubble bust just like night follows day. Kind of like a law of financial physics.

October 24, 2012 at 10:01 pm in reply to: Japan Is Not A Good Example Of How Deflation Typically Plays Out #6128ParticipantJohn –

We are not the ones who should be making tight bets on the timing of trends, but rather building some kind of stable support for a rocky tumble ahead.

A fine attitude, and I’m completely supportive of that mind set.

If that’s the case, however, then we should also not AT THE SAME TIME be making unsupported claims that the market is currently in a topping process and undergoing a trend change, because that is getting into the business of making explicit market predictions.

Let’s say the market (given its tricky “fractal” nature) decides to rally after year end – after the fiscal cliff “can” gets kicked once again. What will people think of the statement “the market is undergoing a topping process” at that point? If the market makes a higher high, that’s not a topping process, that’s a breakout to new highs.

My main point is, why risk credibility on making an unsupported prediction on something that’s not core to your case anyway?

October 24, 2012 at 5:48 pm in reply to: Japan Is Not A Good Example Of How Deflation Typically Plays Out #6123Participantp01 –

The stopped clock phenomenon: “Even a stopped clock is right – twice per day.”

This refers to someone repeatedly making the same prediction, just like a stopped clock always says it’s 3pm. Wait long enough, and 3pm will in fact recur, and the clock will be correct. In the case of a market crash, if you predict one often enough, for long enough, you will be right because given enough time, the market will indeed crash.

October 24, 2012 at 12:54 pm in reply to: Japan Is Not A Good Example Of How Deflation Typically Plays Out #6121ParticipantOverall a good case, but I have two objections I’m going to make.

…people extrapolate the trend of the last three years forward, but fail to anticipate trend changes. We are in one. Many markets have topped already (gold, silver, commodities, oil etc), and the rolling top of the last year or so is about to claim the American stock market as well.

Some really smart traders I respect with 30 years of trading experience following these markets (and who called the bubble and the crash correctly too, I might add) do not have the hubris to make such declarative statements about what “is about” to claim the American stock market, selecting which markets have topped, etc. I’m just going to throw out there that incredibly smart though you may be, if history is any guide you will likely only be correct about your call on this particular top through luck, persistent top calls (the stopped-clock phenomenon), or by ignoring timeframe.

Viscount has enumerated the number of times you have successfully called the bottom of a particular market move – but as a contrary indicator. I know its quite impossible for me to make this sort of comment “with all due respect” but – I really do have a great deal of respect for both your intellect and your point of view about the forces in play today. Its just the market predictions made with such authority that impels me to comment.

I agree that the currency of a deflating nation strengthens. This is exactly why we have been writing about the value of the US dollar increasing, which it has done. The bottom came in a long time ago, and despite the set backs that are an integral part of a fractal market, the trend is up, and will be for some time.

Dollar increasing? Over what timeframe? A supporting chart for this assertion would be helpful. Since the peak in 2005 (92) its down, since 2009 (90) its down, since 2010 (89) its down, and its definitely off the 2012 high (85) as well – over the past 7 years, I could make a pretty good case for a series of 4 clear lower highs, which is not a bullish pattern at all.

Shorter term, USD is definitely off the lows of 2010 (72.5), but again, it is likely that a real trader would suggest that the dollar needs to bounce above at least the 2010 high before suggesting an actual trend change had occurred.

Why am I peeing in Stoneleigh’s wheaties this way? Have I no respect? Don’t I value all that good work she’s done?

Duh, of course I do.

But at this site, market predictions are sometimes made that have in fact often been wrong (and sometimes spectacularly so), and that has caused an unnecessarily loss of credibility in the underlying principles and market forces in play that this site has done such a good job in explaining. I’m trying to encourage a change in approach.

Now I’m going to play the “prediction game” based on the evidence I see. And I’m actually going to supply some evidence. It doesn’t mean I’ll be right. But I’d like to encourage people to use charts to back up their assertions, especially about the market, what it has done, and what they think it will or will not do.

Over the 10 year timeframe, the trend for the buck has been down. The buck hasn’t shown itself in 2012 to be as strong as it was in 2010 – I’d have expected it to perform better during the last eurozone crisis, which does itself seem to be getting progressively worse. USDX has just crossed its 200 MA to the downside again. My current sense is (60%) the dollar goes lower. And – as with any trend, it is your friend until it has been shown to change conclusively. It would have to break above 89 for me to change my mind. Currently: 79.93.

(I’m not a dollar bear – or bull. I’m just reporting on what I see; since I own dollars, I’d probably prefer it to go up, all else being equal.)

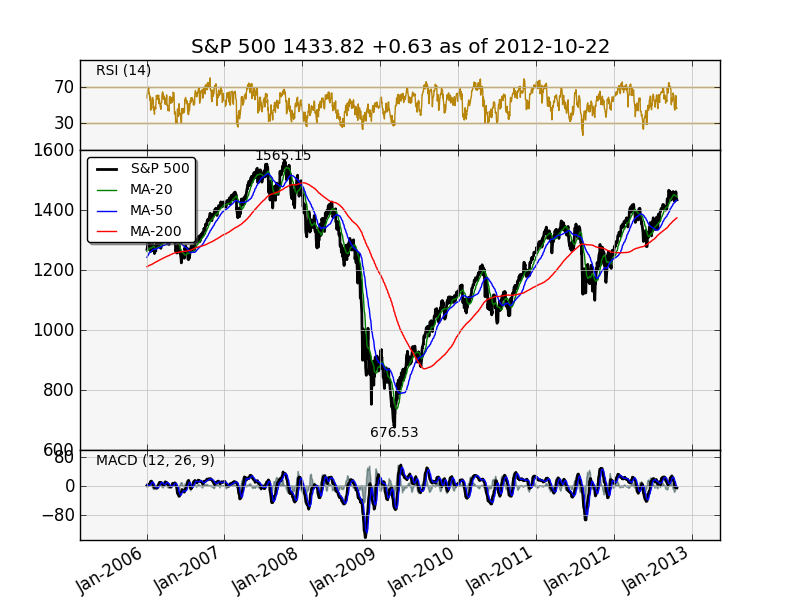

Has the US equity market started a topping phase? Not from what I see. Looking at this (long term) chart, do you? Remember, the trend is your friend until it (conclusively) changes. I’d phrase things by saying medium term downside risks have increased in the US equity market. Currently the trend indicators still signal up (the 50 MA is above the 200 MA) but we need to await market action before we draw a definitive conclusion. We might just track sideways for a while, and if “the fiscal cliff” is avoided, that combined with the January Effect might well (60%) pull us above our current cycle high. If responsible spending wins, likely we’ll see a selloff. Of course if europe collapses the US market goes down hard, maybe even very hard – but that’s not happening at the moment, at least according to my other indicators.

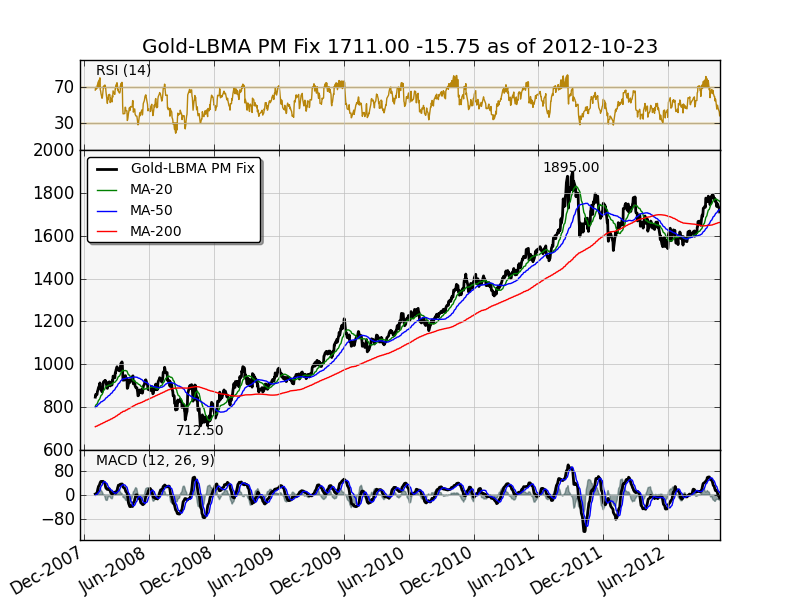

Gold broke out conclusively of its 18-month downtrend off the Sep 2011 high; the 50 MA crossed the 200 MA (that intermediate term trend change indicator again) and so with monthly QE a reality, my guess is PM still will have a bid (75%) and gold will likely break 1800 before it sees 1550 again.

I would have been singing a different tune back in July. The charts looked pretty bad for gold back then.

As always, my (hopefully evidence-based) market predictions are subject change as new data comes in.

Participantpipefit –

You’ve made a number of interesting points, but one I’d like to take issue with is your reference to a rising GAAP annual deficit.

Unlike a cash deficit, a GAAP deficit requires no bond auction to cover, and the government pays no interest rates on said deficit. Additionally, the GAAP deficit adds zero dollars to the economy of the moment, also unlike the cash deficit.

It reminds me of the Social Security Trust Fund. There’s no “there” there. Its completely notional. It represents a sum total of a future problem (or in the case of the Trust Fund, the sum total of future required additional borrowing by the Treasury from the very real bond market).

As such, if it doesn’t represent real dollars spent into the economy today, how can it possibly be inflationary, much less hyper-inflationary? Unlike deficit-spent dollars which definitely CAN be price-inflationary, especially in favorite sectors such as defense, education, and healthcare.

ParticipantHambone –

Not being in the RE industry I must rely on what others say. Most of my data comes from Mark Hanson.

The foreclosure pipeline requires some large number of months to completely execute; varies by state but its anywhere from 6 months to years. There was a foreclosure moratorium put in place last year (due to the wholesale fraud in foreclosure documentation finally being acknowledged), and I’m guessing that’s a big chunk of what is causing the dry-up in distressed property today.

I’d guess allowing the banks to keep REO around and rent it out contributes to this as well. Of course it also allows the banks to avoid recognizing losses too, which is always helpful if you are particularly focused on bank welfare.

For me, real estate will be “turned around” once interest rates return back to a more normal 6.5%, when the US government stops borrowing 10% of GDP every year, when the Fed stops monetizing the debt, and when Fannie & Freddie are no longer 90% of the mortgage market. Prior to this happening, what we’re seeing is just the result of stimulus and not sustainable.

I think that in some areas where rents exceed payments by a good margin, RE might be a decent buy. But – I’m cautious. What happens when rates go back to 6.5%? A 30% drop in home prices? How much fun would that be if you’ve put 20% down?

Do we imagine the Fed will be able to keep rates at 3.5% in perpetuity?

ParticipantGolden Oxen –

I have to say I liked many of those charts Ilargi posted, and the linkage with Japan makes sense to me since the situation is post Gold Standard and thus directly relevant. QE has an effect certainly, its just not the one many people imagine it is. Slowing money velocity – interesting stuff, worth watching. One cause of hyperinflation is rapidly increasing money velocity, and we’re seeing the opposite here.

Likewise, its totally clear to me that homeowners and small business are reducing their overall debt, for the first time – well ever, at least according to my Fed data. Reducing debt, in our money system, is deflationary whether accomplished via default or by paying it down. And they’ve been doing this since Q2 2008. And if you even bothered to glance at the data series, you’d see just how unprecedented this is.

The recent housing price bounce is (most likely) due to the massive reduction in interest rates; most homebuyers with mortgages buy with an eye only on monthly payments. As interest rates drop, payments decline, and they can get more home for the same payment. Mark Hanson calculated that over the past 12 months purchasing power went up by about 15%. All else being equal, that should have raised prices by that same amount. It didn’t. But the really amusing bit is, overall mortgage balances dropped over that same period. Deleveraging continued – a quite solid indicator for the deflationary trend! Rates at 3.5% didn’t bring buyers out of the woodwork. Do we imagine rates at 2.5% will magically do this?

Simply asserting Ilargi’s evidence is “mumbo jumbo” says to me that either you don’t understand the case being made, or that you don’t have a valid counter-argument.

Since you believe so strongly in Williams, why not find and post some compelling case (the stuff you call mumbo jumbo) that he has produced to explain the hyperinflation that is just waiting to burst forth – specifically how gobs of new money will be created without an influx of willing borrowers. Which do not seem to exist, and haven’t since 2008. Or why money velocity will suddenly increase. Which it hasn’t.

Certainly, trends can change, but we need to first have a clear understanding of the trend currently in place, and evidence (data series) that help to show us where we are and what the direction has been are quite valuable to furthering that understanding.

We can keep an eye on velocity and if that situation changes, then we might have to revisit. I really like having numbers that we can watch to see the evolution of thesis.

Sometimes I think that people with “faith” in an outcome feel no need to actually prove their case (or show their work). “Whatever it is you’re saying, why, it has to be wrong, because its import runs counter to my article of faith.” That might work among co-religionists or members of the choir, but it doesn’t play so well among people who prefer cases to be proven based on facts and evidence.

ParticipantTrivium –

So why the anti-semitic question?

It has been a theme for quite some time that there is an international conspiracy of bankers, run by “the jews”, that dominate affairs of the world. This thinking culminated in the tragic actions in Nazi Germany. That’s why, since you espouse similar-sounding ideas and you use specific terminology that is also used by those same people, I asked the question.

Its great that you are focused on actions; to me that avoids the trap that advocates scapegoating a separate small group of people (who are “not-us”) that if they were only sent off to camps the world would be all better.

I think that focusing instead on the system of slavery and proposing changes is much more productive. One cannot expect success in an essentially moral enterprise if at the start one’s thinking is grossly immoral at the core.

I watched your corporation video and I felt it did have some pretty valid points – stuff I’ve been thinking in the back of my mind but had not solidified. I’m still sorting through the solutions in my mind. In some sense, one core problem with corporations is that not all stakeholders are represented in corporate governance. Nation, workers, and capital all need to have a voice in the entity that is an enterprise, since it is an organism that affects all three.

At the same time, the best work is done with teams, and private enterprise has an essential enthusiasm and creativity that if properly focused can really drive the search for solutions in a way that government cannot replicate, at least not long term. That’s because capitalism, if honestly implemented, ends up killing off poorly performing solutions on its own, which government (unfortunately) cannot seem to do.

It’s a pity we don’t have actual capitalism – right now we have crony capitalism, which ends up preserving those poorly performing solutions at taxpayer expense, which is of course the worst of both worlds.

ParticipantTrivium –

Thanks for clarifying whether or not you are anti-semitic. It seems clear that you are not. I’m glad that your remedy for The Money Power isn’t sending everyone of Jewish descent away to camps for them to be killed.

I’m all for replacing the system of debt based money and debt slavery with something better. I just have no interest in interacting with anyone suggesting any sort of sweeping group-oriented Final Solution style “remedy.”

ParticipantTrivium-

So I did a bit of research on what the code words “Money Power” mean and I’d like you to clarify something: do you believe as Henry Makow does, that The Money Power is basically Jewish in origin? Or does Money Power mean something different to you?

You’ve been coy about talking about this ever since I started reading your posts, and now I have a sense as to why that might be. Here’s your chance to clarify things so I don’t get an incorrect impression of your viewpoint.

ParticipantTrivium –

I already know how the debt/money system works, I’m surprised you didn’t pick that up from the few times I’ve mentioned it before. It makes me wonder if you actually read what I write. Good explanation though.

Sure its clear bankers benefit from the current system, and its also clear they are a powerful group these days. The Fed certainly works for the banks. And people in debt have big problems – in aggregate. But that combination of facts doesn’t necessarily add up to some eternal dark, ultrapowerful group of conspirators bent on owning everything and the total domination of mankind that you talk about.

The common thread in all of it is, I see you making a leap beyond the evidence which to me isn’t justified. And you have a level of certainty about it that (again to me) isn’t justified either.

Of course, I can’t prove this conspiracy doesn’t exist – that would be proving a negative.

However I’ll always be interested to read any new bits of evidence you unearth. I can always find new information interesting even if I don’t share the opinions of the presenter.

ParticipantTrivium –

So, why would they think the Euro benefits them when it is a debt backed currency that is engineered to bankrupt them? Using logic applied to the known data, we can reasonably surmise that the temporary ability to buy lots of stuff was really cool and they want to try and keep that party going and avoid the pain of going back to their own currency post Euro bubble relative to their own currency.

No. We cannot “reasonably surmise.” That’s just your guess, based on…your guess. One of many possible guesses that might be equally valid.

I believe you engage in this sort of thinking often. You make a lot of unsupported claims, ones that rely almost completely on you starting from the premise that a criminal conspiracy exists, and then you interpret the evidence (which might have alternative and equally valid interpretations) as support for this alleged conspiracy. They call this technique the Texas Sharpshooter Fallacy.

Let’s use Greece as an example. You surmised it was all about restarting party time. Another guess (just as valid, in my eyes) as to why Greeks might want to stay with the euro might be, the Greek people found the drachma to be a terrible currency where the government stole value from them egregiously through inflation, and those that have pensions or government jobs remember this, and really don’t want them inflated away.

Given the median age is 43, they likely remember the drachma quite well, their population pyramid sucks (they have a metric ton of old people there), and so they may well be focused much more on keeping what they have, and substantially less on re-igniting party time.

I’m not saying this is The Correct Explanation – I’m just trying to point out your claim of “reasonably surmising” is just your guess, and is one of many reasonable (and conflicting) guesses that can be made about the evidence. It’s definitely not the only reasonable choice.

I see this to be the case all throughout your reasoning about your criminal conspiracy. Interpretations – reasonable interpretations – that don’t support your starting theory of criminal conspiracy are simply dismissed.

These same criminals oversee Debt Money Tyranny – which is engineered to systematically asset strip society and subjugate them, which is pretty obvious in this chart:

A good example of the Texas Sharpshooter. You’re starting from the conclusion and working backward.

Here is an alternate interpretation. The credit money system evolved during a time of exponential growth. There was a NEED for an ever-growing amount of money in the system. This system worked pretty well during our exponential growth period throughout industrialization and our subsequent growth in energy resources. It just grew like topsy. The guys in charge tried to fix the bits that failed periodically as best as they could incrementally, and the ones in charge are trying to keep things working based on their 200 years of understanding on How Stuff Works in Credit Money Land. Now that energy resources aren’t growing exponentially anymore, Credit Money is encountering difficulties. Once energy resources start shrinking, Credit Money will likely fail pretty dramatically. But since such a resource constraint issue is not part of our history, they are quite reluctant to come to this conclusion. Generals always fight the last war – and in this case, the last 100 wars.

To me, that’s a perfectly valid interpretation of events, supported by the evidence I see. It doesn’t mean it is right, but it is supported by the evidence.

But ultimately I have to ask, why does it matter?

Credit Money will likely blow up because of its design, resource constraints, and circumstances. Its either run by evil people, or by people who are just trying to keep the machine going. Which it is doesn’t matter. The outcome is the same.

Unless of course you propose running some sort of campaign to uncover then root out these extant shadowy criminal group and bring them to justice, we’re both just observers in the grand play, and its likely more useful to focus not on blaming the shadowy set of characters (we have ALWAYS loved scapegoats) that may or may not exist, but rather on systemic effects and how they will end up affecting us.

By the way – I’m a big fan of the Z1. I look forward to reading it every release. Just know that its really just a survey conducted every couple of years with the interim data points being (likely) interpolations and/or guesses likely based on data the Fed gets from other places. But its the best data we’ve got.

ParticipantTrivium –

Hi Dave, has it ever occurred to you that the “mess we’re in” is precisely the objective of the social engineers?

Lots and lots of things have occurred to me over my lifetime. Certainly, that is one of them. Since I’m not in possession of the secret handshake, and I’ve not been invited to any of the the meetings, I can’t properly judge what is and what is not a precise objective of the social engineers – or if said group exists, or if said group is organized, uniform, etc. For those who are NOT in said group or have specific knowledge of actual events that have occurred at said meeting, assuming you have relatively complete knowledge of its motivations and inner workings seems … well lets just say that’s just not my style. I’m a data-driven guy.

For instance, I can speculate why the Greeks want to stay in the eurozone (and I definitely do speculate) but I don’t have the hubris to pretend that I really KNOW why this is the case. And honestly, it’s quite enough for me to know that they currently want to stay. Speculation is really for amusement purposes only. There’s data, and there’s speculation, and I know which is which.

To me, your assertions on all of these “social engineering” matters stray far outside any data I personally have, so I normally choose not to go there. As far as I know, you could be right, you could be wrong, you could be right about direction and wrong on intent – how could I possibly assess for myself what is correct since I have seen you present no actual information at all, just naked assertion. And to me, naked assertion does not constitute reliable data.

Clearly you are convinced of your position. I’m certainly not debating it with you – I can’t, because I have no information with which to do that. And that’s about all I can say on this subject.

ParticipantProfessor –

In Ireland, which was the original source of the discussion point, loans are full recourse, which is why I brought it all up.

Professor, I’d go with your “rule of law” thing if the rules and the laws were applied evenly. They aren’t. All the immense, widespread, egregious fraud engaged in by the lenders during the bubble along with the rest of the “smartest guys in the room” remains unprosecuted by our Rule of Law system. And yet we’re focused on getting that last nickel out of the borrower, lest sacred contract law be breeched.

So yes, I favor as part of bankruptcy law a cramdown provision where as a part of a general personal bankruptcy the principal on home loans get written down to fair market value. Its not a freebee for the borrower, but it is a realistic way for the debt burden to be adjusted to something sustainable without having to go through the costs of foreclosure, which ends up costing everyone involved more money.

As for you being repeatedly victimized by bankruptcy scammers, it would seem to me that doing business with (and/or extending credit to) a serial bankruptcy declarer is a – how do I say this politely – a risky practice. You might consider avoiding doing business with such people in the future.

Just some free business advice. 🙂

ParticipantViscount –

I can agree with the psychological research you bring up, it seems to be a basic part of human nature.

That’s no doubt in play here – you could also summarize that as “a euro in the hand is worth a fistful of drachma of uncertain value in the future.” Better the devil you know than the even bigger devil you remember from the past!

But I think there’s more here as well.

Greeks really don’t trust their government. They believe their country is the most corrupt country in the eurozone. Of course the Spanish think this about Spain, Italians think this about Italy, but it turns out the Greeks are the ones who are right based on yet another survey I found. When asked who is to blame for the problems, overwhelmingly the Greek government is identified (87%) – banks are a distant second (39%).

So my interpretation is, Greeks see the euro as an important check against their own government’s corruption and penchant for mismanagement. Not the ECB, not Brussels, not Germany – the Euro.

Should we keep the Euro or return to our old currency?

Greece: 71%

France: 69%

Germany: 66%

Spain: 60%

Italy: 52%ParticipantProfessor-

Bankruptcy is a form of principal forgiveness. It comes with a price – no ability to obtain a loan for a period of time. Other forms include principal writedowns to current market value – and there are a lot of ways to skin that particular cat that allows the holder of the mortgage to participate in the potential upside if and when the house is sold for a profit.

Anything that skips the whole foreclose & sell cycle (which is a guaranteed loss for everyone involved, except for the folks picking up the pieces on the other side) would seem to be a whole lot more efficient from a systemic point of view, too.

Honestly, the smartest guys in the room were the people making the loan, in every one of these home mortgage situations. They should have known better, period.

Nations can default, companies can default – why not homeowners? Christianity teaches forgiveness, and allegedly some vast majority of the people in these countries are Christian, yet why is it so difficult when it applies to borrowers?

Its true that “some people” are more comfortable with debtors prisons; its the ultimate form of spanking for those who reneg on their obligations. An excellent deterrent to such behavior.

Personally, I’m not in debt, so I don’t have a dog in the hunt, but until big chunks of principal forgiveness (in whatever form) takes place, we’re not getting out of this mess we’re in.

ParticipantA possible example of “missing the important bits” from Mish today. In his post he talked about the protests against Merkel in Greece and what it signified.

Looking at poll data, its easy to see why these protests occurred. When asked, “do you have a favorable opinion of Germany”, only 21% of Greeks said yes. The rest of the zone polled: Italy had a score of 67%, and they were the lowest. France was highest (higher even than GERMANY) at 84%. The French really respect the Germans.

But the Greeks don’t like Germany (79%). They don’t like the crisis handling skills of Merkel (86%) Sarkozy (83%) Cameron (84%) or their own leader (68%). They don’t like the ECB (80%). They don’t like EU budgetary oversight (75%), and they blame their own government (90%) for their current troubles. Talk about some cognitive dissonance!

But they love the euro (71%) and they REALLY love bailouts (91%). Highest reported values in this particular poll for both categories.

Amazing.

Do you think there will be a revolution in Greece to support leaving the zone? Not if these numbers stand. If you were Greek, and you loved the euro AND bailouts, why on earth would you support revolution? Protest against the hated Merkel: sure, its an easy sell. But perhaps we shouldn’t over-interpret what the implications of these protests really are.

I’m not an advocate for a position, its just the conclusions I’ve drawn from the data I’ve seen. If you look at the same data and draw a different conclusion, I’d be interested to hear it.

And of course if things change on the ground, I reserve the right to change my conclusion.

Raw data:

https://www.pewglobal.org/2012/05/29/chapter-2-views-of-european-unity/

ParticipantIt has taken me a few weeks, but I’ve completed a first pass analysis of the different countries in MENA that have either staged revolutions or are engaged in civil wars, etc, and compared them with the current Greek situation. My top-line thought is, unless something major changes its not gonna happen in Greece – based on it not happening in other MENA nations that had either higher incomes, less corruption, more social spending, and a few other euro-specific factors I think are also critical.

[table]

[tr]

[td][/td]

[td]GREECE[/td]

[td]”Revolting” MENA[/td]

[/tr]

[tr]

[td]Avg age[/td]

[td]43[/td]

[td]22[/td]

[/tr]

[tr]

[td]Per Capita GDP[/td]

[td]28,000[/td]

[td]3,200[/td]

[/tr]

[tr]

[td]Democracy+Corruption Index[/td]

[td]48[/td]

[td]121[/td]

[/tr]

[tr]

[td]Social Spending as %Govt Spending[/td]

[td]32%[/td]

[td]17% (approx)[/td]

[/tr]

[/table]Last point. A poll was conducted in March 2012. While only 17% of Greeks reported “my situation is good” (74% of Germans thought so), only 23% of Greeks said they wanted to leave the Euro. They were angry about a whole laundry list of other things about the eurozone (Germany, the ECB, economic control from Brussels, on and on) but on that one key issue – leaving the eurozone – they overwhelmingly wanted to stay. More than ANY other country polled, they wanted to stay.

I think that last detail is critical. Unless that last bit changes, it will be a bunch of relatively well off middle-aged men (compared to people in MENA anyway) sitting around in their cafes and complaining over coffee about the dreadful decrease in social spending, while in MENA it will be a horde of really poor (and immortal-feeling) 20 year old boys getting guns and shooting people because they really don’t have enough money to buy food, so they’ve got nothing to lose.

Situation is similar in Spain; avg age 41, per capita GDP 31k, social spending about 30% of govt spending, and a pretty flat GINI coefficient of 32. (US is 45, right up there with China at 48).

Old people don’t revolt, especially if what they REALLY want to do is to stay in the eurozone.

Of course, this could always change. Best to watch polling numbers for the “leave the euro” parties and see how things transpire.

ParticipantWow, Irish finally get principal relief, AND bankruptcy. That’s really good news for them, well mostly anyway.

Back of the envelope calculation: the Irish Bad Bank owns about 70B (face value) in mortgage notes of a total of 120B in total Irish mortgage debt. Now with Principal Relief, who pays for this? That would be the Irish taxpayers, at least for 59% of it.

Now I’m a big fan of principal relief, don’t get me wrong. Its just – amusing to see that it only happened long after most of the mortgage debts were transferred to the bad bank.

What ever happened to creditors taking losses?

ParticipantTrivium –

The concept behind your diagram was pretty well explained by a video I saw called Money as Debt. I had to watch it twice to completely get it. Debt being unpayable by design, interest rates controlling expansion and contraction, fractional reserve lending (and no-reserve lending, like we have now), creation of money, and so on.

I think the presentation of this material needs to be dynamic, not static. Additionally, there’s too much assumed knowledge in your diagram; basically I think when people learn, they can only absorb one new concept at a time.

And the vast majority of people think they already know how things work, and they’re wrong, and its a hard thing (and it takes repeated presentations from different angles) to get that worldview to change.

In other words, you likely can’t compress the effect of a 1-hour video into a one page diagram, no matter how often you revise it!

Simply getting people to see that a bank charter allows a bank to create money from thin air upon the act of someone signing a loan document – people just tune it out because they don’t believe it can be true. “That can’t possibly be happening.”

Here’s an exercise for you. List the new concepts you are trying to get across in that diagram. Then imagine a person has to have the new concept explained in a clear and explicit way, with a set of expected questions answered. My guess is you’d come up with at least 5 new concepts you are presenting, that would likely require 5 diagrams. Or maybe one diagram, with a zoom-in of each subsection with an explanation. Like a comic book.

Think political cartoons. The old-style cartoons had a million people talking. Then, the first guy to come up with a cartoon with one, laser-like point, changed the whole paradigm. Everyone got it. Now nobody does the old cartoons, simply because people don’t get them.

The language class I’m currently taking is a case in point. When I learn a new word, it is really useful to hear that new word used in a sentence – hopefully more than one sentence to really hammer it in. But if you try and speed things up by having 2 new words in one sentence, more often than not I get confused and things take longer overall and they work less well. And at 3 new words, my brain shuts off and simply refuses to work!

One new concept per diagram.

ParticipantJohn –

I’m looking more at what will be globally accepted after debt based fiat currencies are retired, as I think they must be in a shrinking-resource-constrained world. No more exponential growth economic model…

I don’t see gold as a short-term holding for profit, but more as a strategic asset for individuals, and the basis for international trade deals across the ages.

I think it will be that again, in a powered-down world, but that is a view to the indefinite future, after the dollar hegemony ends.I can definitely imagine the world you describe, and the question of what sort of currency will function properly for flat-to-shrinking resources & populations is a really good one. It simply can’t be debt-based money.

Certainly as a basis for international trade deals in such a world, gold makes sense and has a lot of historical momentum behind it. And if it has international trade utility that means it will definitely retain value. I’d say: argument nicely put. I’m not convinced it is our only possible future – but it feels to me like it has a decent chance of occurring.

My next question you already anticipated – it is one of timeframe. As you say, the “indefinite future” might be a while from now, possibly even decades. The end of dollar hegemony probably also implies the end of US military hegemony as well. Hard for me to imagine today – but we did see the Soviet Union collapse extremely rapidly back in 1989, so its not without precedent, and it might happen more rapidly than one might expect.

ParticipantJohn –

Perhaps I should go read more about that period. Banks can certainly cause depressions if they are allowed to collude and raise rates.

Where there is a bona fide gold standard (as in from 1800-1972) with an explicit linkage of currency to a particular weight of gold, gold performs just like cash. Since cash does well during deflation, so will gold.

It is less clear how well gold will do during deflation with no gold standard in place. We’re in uncharted waters now, we have no historical guide, and so I perceive the risk as higher. Certainly during recent deflationary episodes (late 2008, late 2011) gold did not respond so well.

ParticipantTrivium –

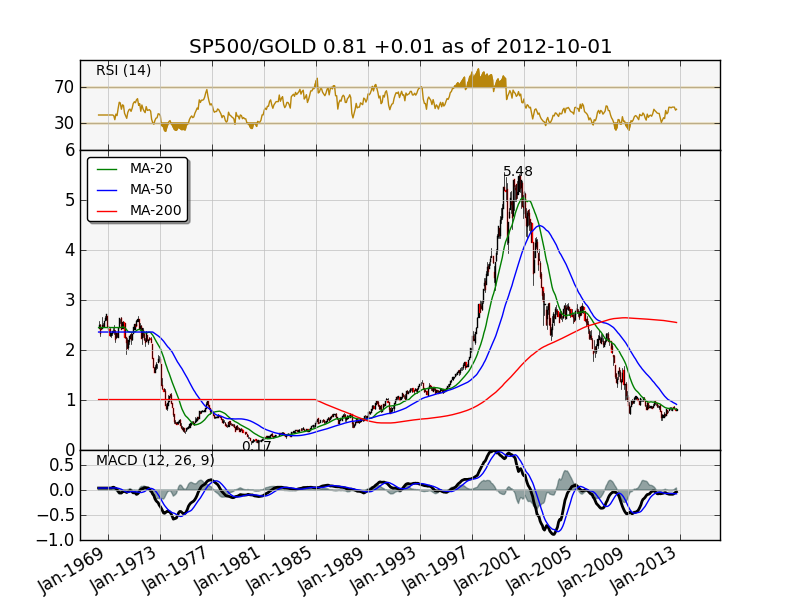

In looking at the longer term SP500/GOLD chart, I’m not entirely certain I’d call it a “low risk trade.” Its true that the trend is your friend right up until it changes, but just eyeing the chart, the low risk period would have been in 2001 after the price moved strongly through the 50 month moving average. Hindsight of course is always 20/20 but you can use moving averages to help you spot major trend changes when they occur. (Its unfortunate I was completely asleep during this period of history!)

In a narrower timeframe, its true that in 2007-2009 gold held up much better than SP500, and maybe that’s the period you’re focusing on more. I’d have to agree with that, and also that there is some risk of not being paid for one side of the trade if things go particularly poorly. However if things proceed as they did last time (i.e. with the SP500 gradually moving down over a period of months, as opposed to a 1987 one-day event) you could periodically take money off the table as events unfold.

Participant

ParticipantJohn –

During the period of the 1800s, gold was convertible (variously) at a rate of 1.6g and 1.5g per dollar. That rate held until 1933. That’s why gold did well during all those depressions – price fixing by the Treasury, plain and simple. If you brought the Treasury 100 tons of gold, they’d hand you a wagonload of dollar bills. Why not, printing bills is cheap, and mining gold is darned difficult. Of course it meant that gold discoveries caused inflation, but that’s the price you pay for a commodity-based monetary standard.

Had the US Treasury decided to declare donut convertibility at $1 per donut, they would have performed quite well during depressions too.

ParticipantGold in deflations –

During the 1930s deflation, gold did well because it was linked by the Gold Standard to the value of the USD. In the depression, cash was king; bonds could default, deposits could vanish, but one ounce of gold was linked by – fiat – to be about $20. Take your ounce to the Treasury, and they’d give you $20 in cash. Cash and gold were interchangeable, by law.

In 1933, the law was changed; now your ounce of gold got you $35. Gold kept its purchasing power, while the dollar was cut by 40%. Gold holders were winners. A gold mine was literally a license to print money. That’s why people think “gold does well during deflations” – last time around it did, courtesy of the Gold Standard and the US Treasury.

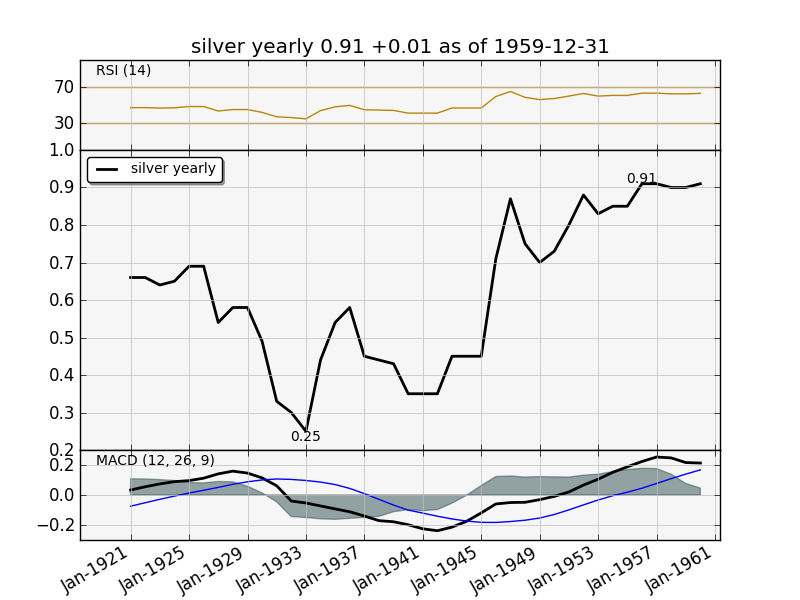

Other items that did not have such laws mandating their direct convertibility to cash were very volatile. Silver started the depression at about $0.60/oz, and then dropped to $0.25/ounce in 1932, bouncing back to $0.60/ounce immediately after reflation of 1933, only to drop again to $0.35/oz in 1939. By 1945 it was up to $0.70/oz. Did silver “do well” during deflation. I don’t think so. A strong stomach was required. Cash would have been a better bet, unless you were tough enough to hold for 16 years or clever enough to buy at the valleys at $0.25/oz.

Could this be a model for how gold performs during another deflation; this time with no mandate from the Treasury to buy gold at a price certain, might not gold perform much as silver did?

My opinion based on watching both markets operate for several years is that gold will maintain its value better than silver did – but not as well as cash during an initial deflationary downdraft. If you are nimble and have some spare cash you can buy gold after it tanks, but it will likely be a bit of a wild ride.

I think gold will do quite well in the inevitable reflation that follows the downdraft.

A side note; physical gold in hand will likely do much better than bank deposits or bonds if the system really locks up. Then again so will FRNs, at least until the reflation.

ParticipantViscount –

Hmm. Let me take your points case by case.

I find Nigel Frange and the EuroSkeptic’s perscription naive. He suggests:

Greece should leave the Euro devalue and fight her way back to competitiveness. And what would be the response among Euro-zone neighbors to a dramatic devaluation? I’d imagine: trade barriers.Nigel Farage’s position has the virtue of being backed up by historical experience. Nations unable to print during the 1930s (due to being on the gold standard) suffered up until they defaulted and devalued. Nigel is using his understanding of history when he makes that case.

I would suggest that the globalized economy would ensure that money would flood to a place where stuff is now cheap: Greek real estate, Greek agricultural products, Greek labor. A 60% off sale looks mighty attractive. And even if the neighbors do get upset, the eurozone isn’t the only source for funds in the world. It would take a worldwide tariff agreement to seal off Greece. I don’t see that happening. Heck, the Chinese elites would probably flood in and buy cheap Greek vacation homes if nobody else would.

Is it possible Greek society will be able to handle the “internal devaluation” plus default that is going on now – the other route to the same place? My guess is no, based on the trending strength of their Nazi party.

In Ireland, I’d say it probably will hold together. Different country, different dynamics.

The gradual dissolution of the nation state through globalization is one of humanity’s greatest achievements.

I’d say its more due to surplus energy than an achievement of humanity. Declining surplus energy means de facto declining globalization, simply because of physics. Shipping products made elsewhere will be gradually less interesting as shipping costs take an increasing share of the benefits of off-shoring.

Likewise, the high degree of inter-connectedness of world trade was thought by many elites prior to 1914 that it would make war between the major powers unthinkable. That assumption ended badly, as we know.

The creation of the ICBM tipped with nuclear warheads rendered the nation state obsolete.

I don’t share that assertion. We’ve had missiles since 1960, and the US nation state is alive and well.

Historically, national associations form and stick because of shared culture and language. Major cultural differences will end up dividing peoples along those same fault lines in times of trouble. Corruption levels in Germany vs Greece along with language and other cultural differences will likely rip the two apart eventually. Heck, the US had an incredibly vicious Civil War and the two sides had far more in common than the Germans and the Greeks.

The expanding eurozone and the progression toward global digital currency and world government is the only route to lasting peace

If you are in the business of assessing conditions and trying to determine the likelihood of possible outcomes, its dangerous (in terms of your accuracy) to be rooting too strongly for any particular outcome.

In other words, wishing won’t make it so.

ParticipantViscount –

Agree with you on what happened in the Netherlands. They toyed with the idea for a while, but found it not to their liking and rejected it.

Lets use this as chance to examine what group the Netherlands belongs to. Is it core, or periphery? As I look at my big picture spreadsheet, I see the economic conditions in the Netherlands is actually not bad:

Netherlands:

* Unemployment: 6.5%

* Inflation: 2.3%

* Debt/GDP: 65%

* Deficit/GDP: 4.7%

* 10 year bond: 1.78%Contrast with Spain:

* Unemployment: 24.5%

* Inflation: 3.5%

* Debt/GDP: 69%

* Deficit/GDP: 8.5%

* 10 year bond: 5.7%To me, that says Netherlands is core, not periphery, even though the deficit is a bit iffy.

Certainly it does suggest to me that core countries’ populations are not yet ready to insist on a eurozone exit. What are the factors driving a core nation to exit? I’d say: pocketbook issues, as everywhere.

Either that could come from inflation due to too much money printing, or from cutbacks in social programs due to the need to fund transfers (bailouts) of the periphery.

But what drives the people in the Core is not indicative of what drives the people in the Periphery. The people in the Core are making decisions based on avoiding inflation and the disagreeable concept of having to sacrifice for others, while the people in the Periphery are making decisions based on increasing poverty and desperation. It seems like a very different calculus to me.

I think we should be watching both groups simultaneously, but with an eye on different metrics.

ParticipantA couple more thoughts.

While German culture tends to encourage rule-following, politicians tend to be a breed apart. I didn’t mean to suggest (inadvertently) that Merkel herself tends to follow rules. I think she’s pretty similar to all the rest of them, actually. But she is constrained by her own culture’s expectations of her more so than, say, the men in charge of Italy and/or Greece.

Also, this money printing doesn’t come for free. Over time a larger and larger share of government spending will go to interest payments, crowding out spending that normally would have gone to defense, infrastructure, medical care, education, social safety nets, and pensions. Austerity is all about imposing those costs immediately and specifically rather than hiding them in a “deficit”.

How sustainable is that? I think that depends on the social cohesion of the country. It might well work in Ireland. I’m not so sure about Spain. I don’t think it will work for much longer in Greece. The 20% support for the Greek Nazi Party is my evidence for that. The NSDAP had 33% of the vote in 1932. Perhaps that’s the metric we can use. The only shred of good news is, if Greece does go Nazi, at least she’s not the dominant economy in Central Europe.

The financial wizardry will likely work. The social aspect? I am less confident.

In some real sense those of us who follow markets have been looking only at “market risk” of various parts of the eurozone equation, while largely ignoring political risk. Since 1945 political risk has been gradually removed from the calculus over time. It has been a steady march of democracy and freedom. You can get on a train in southern spain and travel throughout a dozen nations without once showing your passport. Now that’s freedom. Sure other countries can go batshit crazy, but not in the modern eurozone – a european version of American Exceptionalism.

I think that’s the Black Swan here. They’ll seal up the deal financially, but social cohesion will fail eventually in the periphery, and we’ll end up with an increasing number of nutty (read: totalitarian) governments in what used to be a peaceful democratic europe. Will the eurozone governments go along with that just to keep the dream alive?

It might be educational to read through the NSDAP official positions on economic policy dated 1932. An executive summary:

https://www.calvin.edu/academic/cas/gpa/sofortprogramm.htm

* nationalization of the banking industry

* self-sufficient/local production of agricultural products

* debt jubilee for various hard-hit sectors of the economy

* currency controls (the death penalty for failure to comply)

* government job creation programs – a RIGHT to have a job

* strict control ensuring no trade imbalances

* international debt renegotiationHere’s two quotes I think might resonate today:

Finance capital attacks the middle class from above, since 100 million mark loans exist for the huge concerns to finance dubious enterprises, but middle class craftsmen, businessmen, and retailers can receive only small loans at unbearable rates of interest.

and also

As a result of the state support since July 1931, through which the Reich covered 1 1/2 billion marks of foolish speculation on the part of the big banks with tax money, more than half of the German credit bank system is already in the hands of the Reich.

We therefore demand that the banking system and the money and capital systems be nationalized, just as the railroad and postal systems were fifty years ago…”

And perhaps we thought 33% of the German people were simply idiots for voting in Hitler? I think a good chunk of the blame lies in the people that came before – those who kowtowed too hard and for too long to the banking establishment.

If I were still doing political science, there’s a lot of good material for a paper I could write on this subject: a case study comparing the conditions fostering the rise of totalitarianism in the 1930s with the economic trends in the modern-day european periphery.

ParticipantI’m thinking the system actually has the financial issues under control at the moment. It’s all about money printing. Here’s how it works:

Insolvent Spanish banks are buying Spanish government bonds using money created from thin air – sovereign bonds have zero risk weighting. Spanish regulators ignore bank insolvency issues. As a result of all the buying, Spanish bond yields have gone down.

In fact, across all the PIIGS nations bond yields have dropped. Ireland’s 10Y bonds are 4.8% (down from 10%), Portugal’s 10Y bonds are at 8% (down from 14%) and Italy is at 5%.

And the ECB hasn’t had to buy one single bond to make this work. The trick was getting the local banks to step up to the plate and do their part. As a result of this success, this past week money has moved from the safe haven countries to the PIIGS, reinforcing the action.

Its too soon to tell how sustainable this whole plan is. All the participants of the system know what is going on. It would seem that the Germans have agreed to let this occur because the debts haven’t been transferred outside the country, but money printing is still definitely happening since all the bond-buying is happening through the standard bank money creation mechanism.

The key pressure point that I’d pick are the Spanish bank “rescues”. Everyone knows about all the bad mortgages from the bubble, and yet the banks are required co-conspirators for money printing. Choreographing this dance will be quite a trick.

First, spanish government bond yields have to be hammered down prior to a rescue, or else the price of the rescues go up due to losses on – spanish government bonds. So the banks about-to-be-rescued need to stuff themselves full of bonds which will raise the prices of those bonds. I think that part is happening now, and going relatively well, especially if the hedge funds and others desperate for yield pile on once they see a trend change.

But once the banks start being rescued – with public money, maybe even funded by the banks-about-to-be-rescued – how will that play domestically, given all the austerity being employed by the government? Austerity is required – it is a quid pro quo for the Germans to look the other way. (Culturally, Germans tend to follow rules, while cultures in other countries are “more flexible”; that culture of rule-following is the source for the credibility of the euro itself)

So we have a delicate negotiation; Rajoy is trying to minimize the amount of austerity he’ll have to inflict in order for the banks to be (cosmetically) rescued and for the bond-buying program to remain in place. And my guess is, the banks won’t be “rescued” all at once, otherwise there will be nobody left to support the buying of Spanish government bonds.

Like I said at the start, I think they have the financial bits dialed in, but the wildcard will be people and their tolerance for austerity once they see the price tag of the bank bailout.

My guess: the bank bailouts will happen slowly, it will have a final price tag greatly exceeding current estimates, and it will be paid for by money printing executed by the local banks buying sovereign debt.

Can the financial bits continue? As long as Germany puts up with it, I think it can. But it requires local banks to be willing co-conspirators, the regulators to look the other way, and most importantly every euro printed dilutes the savings of German taxpayers, so we get austerity, and that delicate dance of “how much punishment must be borne to allow the money printing to continue.”

October 4, 2012 at 7:44 pm in reply to: Will The Collapse Of Spain Put Romney In The White House? #5862Participantwilliam –

I think that yours is a well-reasoned point of view. I’m inclined to agree. I’ve certainly never gone down the bilderberg rabbit hole before, but were I to do so, I think yours would be a reasonable methodology. Just my two cents. 🙂

October 2, 2012 at 9:15 am in reply to: Will The Collapse Of Spain Put Romney In The White House? #5843ParticipantMy guess is, a solid majority of those voters in the swing counties that effectively decide the US presidential election could not accurately locate Spain, Portugal, Greece, and Ireland on a map. If Greece fell into the Aegean Sea, the swing state voters would definitely watch it on CNN but I don’t think it would affect who they’d select as President, unless the catastrophe directly affected them, AND there was a credible linkage between the sinking of Greece and the Obama administration.

For US electoral politics, europe is one big ho-hum “not my problem” unless there’s the prospect of the US actually having to send troops somewhere.

I believe Obama engineered his successful election run last year in Aug/Sep when he successfully got the banks to declare a moratorium on processing foreclosures, and at the same time got long mortgage rates dropped 150 basis points. These two things created a modest bounce in home prices in summer 2012, and this matters far more to US voters than some random midsized country having problems across the sea.

The rest of the win has been all about the simple avoidance of calamity; no disorderly eurozone exits causing turbulence in the US financial system, etc.

I heard a rumor that the eurozone politicians don’t particularly want Romney to win, so they’re cooperating also. Not sure how accurate that is, but it would seem to fit with the actions being taken on the ground. At the very least, its not contradicted by said actions. As I said, its a rumor.

So will Spain’s collapse put Romney in the White House? I put the chances of Spain collapsing in the next 30 days at less than 5% (Spain seems able to fund itself right now according to bond market yields) and even if Spain did collapse, I don’t see any such collapse resulting in specific economic effects on US voters in the time remaining prior to the election.

So barring some major Obama blunder, I see Romney losing regardless of what happens in Spain – and I don’t think anything will happen in Spain for the next 30 days anyway.

September 28, 2012 at 8:58 pm in reply to: There's Only One Way Forward For Europe, And This Isn’t It #5825ParticipantIlargi –

People follow stock markets. In the sense that if the markets are doing fairly well, they think everything else must be doing fairly well too (like their own lives). And that’s all they do. But you can’t gauge European reality through looking at stock markets.

I have to ask, who is “people” here?

Ok, that was a rhetorical question. I fully realize that the use of the word “people” in the phrase “People follow stock markets” is similar to the phrase “some people say” used heavily at Fox News:

https://www.youtube.com/watch?v=NYA9ufivbDw

As mentioned in the video, its a pretty useful way for someone to state one’s own opinion without actually saying its just an opinion. It can also facilitate constructing a strawman argument which is then promptly destroyed.

Let me try one of my own: “People think that I’m the coolest guy ever.”

I have to say, I like it!

September 27, 2012 at 12:20 am in reply to: You're Dreaming If You Think The Euro Crisis Is Resolved #5806ParticipantIlargi –

As for graphs on civil unrest: don’t count on it. It must be a year or so since I first said the only thing that’s certain is chaos, and I think that still stands upright very much. And chaos in graphs doesn’t work very well. Unless your samples are huge, like in the Hadron Collider or something, but that doesn’t tell you anything about what will happen if and when the first Spanish demonstrator is killed by a police bullet.

I found an intriguing study that suggested a linkage between high food prices and civil unrest in the MENA area. They had a chart I was particularly enamored of…naturally. Here is a link to the study, updated as of September 2012.

https://necsi.edu/research/social/foodprices/briefing/

Combining this concept and focusing on the nations whose populations spend a relatively larger proportion of their household budgets on food (i.e. the poor ones) and then sort by unemployment rate and it might actually end up being predictive.

I think its quite possible that “random” yet significant acts really aren’t random at all. People get shot all the time, apparently at random. But why is it sometimes the whole society decides to rise up in response to one particular guy being shot in one particular place?

I’m asserting that the whole society doesn’t suddenly become unhappy just because something bad happens to one guy – the one guy provides a catalyst for an already-unhappy society to decide they’ve had enough.

Detecting that high level of latent societal unhappiness should be visible in charts. It may be that some societies avoided revolution because no catalyst occurred, but I think it would be interesting to check back through recent history and see if we can plot revolutions vs food difficulties.

It is said that every society is nine missed meals away from complete chaos. I can relate to that. After missing 9 straight meals during my desert survival class, I was plenty cranky…and I still had a surprising amount of energy to do something about it, too.

September 26, 2012 at 11:52 am in reply to: You're Dreaming If You Think The Euro Crisis Is Resolved #5801Participantprofessor –

The “resistance” and “support” levels in charts are all about fear and greed – in fact most of chart art (which I believe at varying degrees of enthusiasm) is basically all about people’s desire to either get in, or get out, at a given price point. Resistance points are generally about a bunch of people who have been holding on (at a loss) getting back to break-even, and feeling that desire to bail out without loss. Likewise support is about people who missed a good entry point before and are now seeing it come around again having vowed they’d buy “if that price ever got back to X again.” All these things are innately human reactions – fear of loss, or of missing out – and if you can read the charts, you can see them in action. They don’t always work, like anything I suppose, but it can tilt the odds a bit in your favor now and then. The tendency of things to move in cycles can also be seen on a chart too, sometimes at least.

If you have any suggestions on how to chart sentiment of the players in the game, crowd perceptions, etc, and you have sources for said data, just post your thoughts and I’ll run off and see what I can come up with. Even if I have to hand-enter the information, I’m game if the prize is potentially worthwhile. Although if its a time series already in FRED, that’s always nice. 🙂

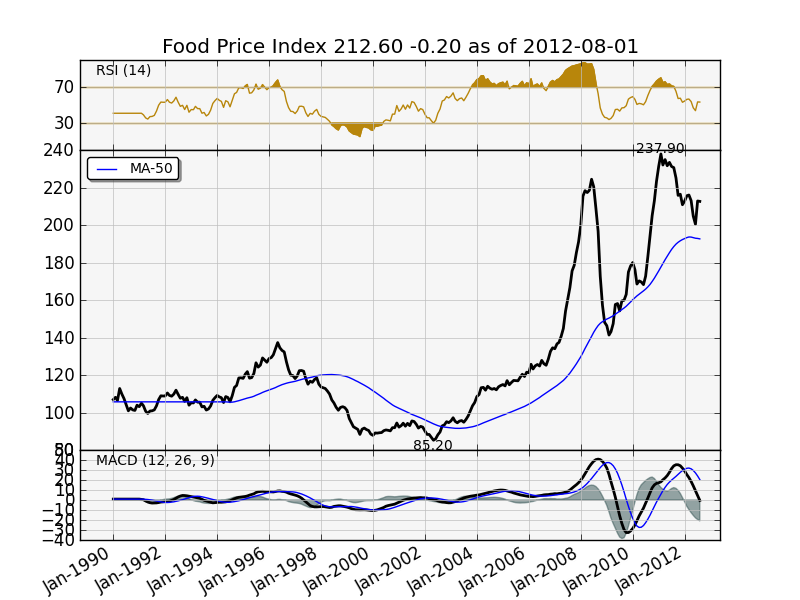

Right now I’m musing on FPO’s “food price index” and how to merge that with household food expense percentages and unemployment rates to see where the touchpoints might be. Usually my problem is lack of meaningful data though, not lack of ideas to play with.

September 26, 2012 at 7:44 am in reply to: You're Dreaming If You Think The Euro Crisis Is Resolved #5799Participant

September 26, 2012 at 7:44 am in reply to: You're Dreaming If You Think The Euro Crisis Is Resolved #5799Participantprofessor, skip –

Charts are really not about showing us the future (at least not to my mind anyway) they simply show us the range things have been in during the past, as well as the current trend.

“Well first things got THIS bad, and then something changed, and then they got THIS good…and now they’re ticking along in this particular direction, and have been for this amount of time…”

It is also interesting to me when the charts show us when things are worse now than they have been before – like right before Draghi’s “I’ll do anything” speech.

So how much higher could gold get, theoretically? Higher, I think, maybe by a factor of four or so, all else remaining generally equal.

And it could go a whole lot lower too, of course. But its the range that is interesting to me. Range, and the current trend.

Last point about charts. I’ve been thinking about how to come up with some sort of unrest indicator. Perhaps a news scanner, or something based on unemployment, social spending, and the level of support for the eurozone in country. I agree with the professor that civil unrest, increasing euroskepticism, the threat of civil war, and possible military coups are an increasing danger as time passes, and having a chart for the forces that act to bring such things about might prove interesting. It is foolish to imagine that any chart could actually predict such things of course, but seeing if things are getting better or worse and by how much might prove enlightening. But clearly I’m a chart guy, and so I’m predisposed to think that way.

Synchro –

I think the Fed does have political limits on money printing, in spite of what we hear now from their current policy. If commodity inflation picks up (housing certainly won’t) the Fed may well be thrown under the bus by politicians eager to blame some organization other than themselves for the consumer’s higher prices for stuff.

To me, the true test will occur when the eurozone gets resolved one way or the other. Then we will see how the US deficit and bond issues will get resolved – i.e. without the benefit of safe haven flows boosting treasury sales.

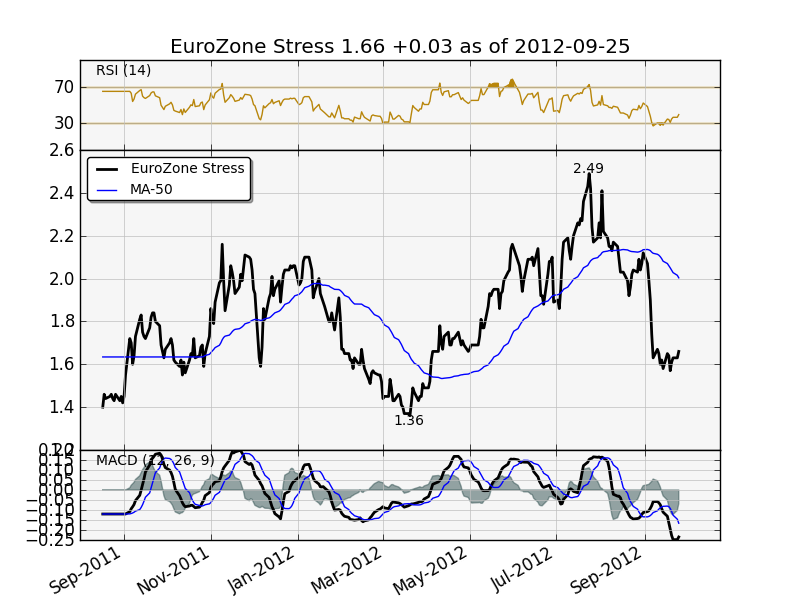

September 26, 2012 at 1:15 am in reply to: You're Dreaming If You Think The Euro Crisis Is Resolved #5790ParticipantHere’s my newly-minted eurozone stress chart. It is based on interest rate differentials on 10 year bond debt, and the difference in yield between “safe haven” debt (Germany), the debt of the PIGS, and the ostensible “average” yield of eurozone debt. Ideally, the value of 0 would be the best possible – where German debt yields the same as Greek debt.

My sense is, more likely than not (60/40) we’ve seen the bulk of the happy reaction to the most recent intervention. The fact that SPX seems to have fallen off a bit even in the face of QE3 lends a bit of support to this thesis for me.

Next step: inserting event labels onto the chart so we can see how the various interventions affected the eurozone bond market.

September 25, 2012 at 10:16 pm in reply to: You're Dreaming If You Think The Euro Crisis Is Resolved #5781ParticipantWhat, Martenson has done a 180? Whaddaya know?

Chris Martenson makes an effort to base his viewpoint based on evidence (as he sees it), and that he reserves the right to change his mind as new evidence arises and situations change.

His current assessment on the inflation/deflation outcome is 90%/10%. From what I can tell, the biggest differentiator in the TAE vs Martenson perspective boils down to the Fed + Treasury’s ability to monetize & deficit-spend.

So far, Martenson sees few real impediments to Fed monetizing Treasury deficit spending. I know for sure TAE does not agree with this.

September 25, 2012 at 7:42 pm in reply to: You're Dreaming If You Think The Euro Crisis Is Resolved #5774ParticipantSkip –

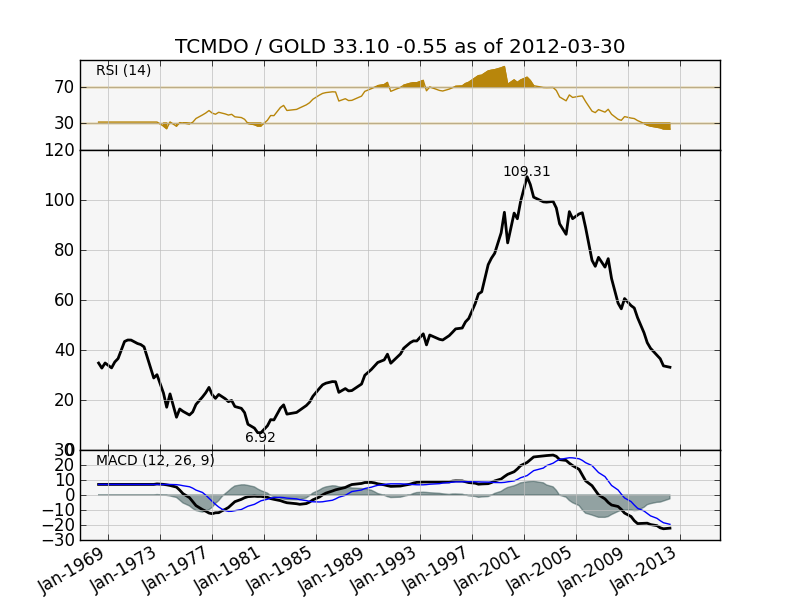

Gold is most definitely looking expensive from the standpoint of your chart right now. But check out this chart:

This odd chart is the US total credit market debt owed divided by the price of gold. With a bit of (hopefully forgivable) hand-waving, we could approximate this to be the following:

TCMDO – claims on real wealth (Billions of $ US; as of apr-2012=$55T)

GOLD – real wealth ($ US per ounce, on apr-2012=$1660)We can see this bottomed out at a ratio of 6.92 back in 1981. Its got a ways to go before it hits that point again. But it certainly has made a brisk move already.

I think this chart is interesting because it pretty neatly shows the interrelationship between gold and credit from the standpoint of the major moves in recent times – and it also puts the current move in the perspective of history.

Then again it could be total bollocks. Let me know what you think!

-

AuthorPosts