Fred Lyon Anne Lyon getting into her Riley on Nob Hill, San Francisco 1950s

When slow news becomes no news. I must have seen 100 different versions of the non-story of one of Trump’s not-so-bright sons meeting with a Russian lady, a story that’s supposed to prove what nothing else has yet proven, not even Bob Mueller, Russian meddling. Yeah, Russia spies, and it hacks, and so does everyone else. But that’s clearly not news, and you can’t make it so be endlessly repeating it. That Comey leaked classified information is apparently much less newsworthy. Only, it is not. It just serves the machine to a lesser degree. Be careful, America, or you’ll have no news sources left soon. Not a great prospect.

• Propaganda-ville (Robert Parry)

As much as the U.S. mainstream media wants people to believe that it is the Guardian of Truth, it is actually lost in a wilderness of propaganda and falsehoods, a dangerous land of delusion that is putting the future of humankind at risk as tension escalate with nuclear-armed Russia. This media problem has grown over recent decades as lucrative careerism has replaced responsible professionalism. Pack journalism has always been a threat to quality reporting but now it has evolved into a self-sustaining media lifestyle in which the old motto, “there’s safety in numbers,” is borne out by the fact that being horrendously wrong, such as on Iraq’s WMD, leads to almost no accountability because so many important colleagues were wrong as well.

Similarly, there has been no accountability after many mainstream journalists and commentators falsely stated as flat-fact that “all 17 U.S. intelligence agencies” concurred that Russia did “meddle” in last November’s U.S. election. For months, this claim has been the go-to put-down whenever anyone questions the groupthink of Russian venality perverting American democracy. Even the esteemed “Politifact” deemed the assertion “true.” But it was never true. It was at best a needled distortion of a claim by President Obama’s Director of National Intelligence James Clapper when he issued a statement last Oct. 7 alleging Russian meddling. Because Clapper was the chief of the U.S. Intelligence Community, his opinion morphed into a claim that it represented the consensus of all 17 intelligence agencies, a dishonest twist that Democratic presidential candidate Hillary Clinton began touting.

However, for people who understand how the U.S. Intelligence Community works, the claim of a 17-agencies consensus has a specific meaning, some form of a National Intelligence Estimate (or NIE) that seeks out judgments and dissents from the various agencies. But there was no NIE regarding alleged Russian meddling and there apparently wasn’t even a formal assessment from a subset of the agencies at the time of Clapper’s statement. President Obama did not order a publishable assessment until December – after the election – and it was not completed until Jan. 6, when a report from Clapper’s office presented the opinions of analysts from the Central Intelligence Agency, Federal Bureau of Investigation and the National Security Agency – three agencies (or four if you count the DNI’s office), not 17.

The report also contained no hard evidence of a Russian “hack” and amounted to a one-sided circumstantial case at best. However, by then, the U.S. mainstream media had embraced the “all-17-intelligence-agencies” refrain and anyone who disagreed, including President Trump, was treated as delusional. The argument went: “How can anyone question what all 17 intelligence agencies have confirmed as true?” It wasn’t until May 8 when then-former DNI Clapper belatedly set the record straight in sworn congressional testimony in which he explained that there were only three “contributing agencies” from which analysts were “hand-picked.”

Paul Craig Roberts lays it on. A bit much if you ask me, but then so is everything else.

• Trump Cannot Improve Relations With Russia (PCR)

On the same day that President Donald Trump said “it is time to move forward in working constructively with Russia,” and the day after he said “I had a tremendous meeting yesterday with President Putin,” the ignorant, stupid, Nikki Haley, who Trump appointed as US UN Ambassador, publicly contracted her president, forcefully stating: “we can’t trust Russia and we won’t ever trust Russia.” The ignorant stupid Haley is still in office, a perfect demonstration of Trump’s powerlessness. The ignorant stupid Haley has gone far beyond Obama’s crazed UN Ambassador, neocon Smantha Power in doing everything in her power to ruin the prospect of normal relations between the two major nuclear powers. Why does Nikki Haley work in favor of a confrontation between nuclear powers that would destroy all life on earth?

What is wrong with Nikki Haley? Is she demented? Has she lost her mind, assuming she ever had one? How can President Trump normalize relations with Russia when every one of his appointees wants to worsen the relations to the point of nuclear war? How is President Trump going to improve relations with Russia when President Trump stands powerless in face of his dressing down by his UN Ambassador? Clearly, Trump is powerless, a mere cipher. Joining Nikki Haley was Trump’s Secretary of State, Rex Tillerson. Tillerson, allegedly a friend of Russia, is also working overtime to worsen relations between the two nuclear powers by publicly contradicting the President of the United States, thereby making it clear that Trump is barely even a cipher.

Tillerson, a disgrace, said that Putin’s refusal to admit that Putin elected Trump by interferring in the US election “stands as an obstacle to our ability to improve the relationship between the US and Russia and it needs to be addressed in terms of how we assure the American people that interference into our eletions will not occur by Russia or anyone else.” Trump’s incompetence is illustrated by his appointments. There is no one in “his” government that supports him. Everyone of them works to undermine him. And he sits there and Twitters. So, what is President Putin’s belief that an understanding can now be worked out with Washington worth? Not a plugged nickel. Trump has zero authority over “his” government. He can be contradicted at will by his own appointees. The President of the United States is a joke.

You can find him on Twitter, but nowhere else, not in the Oval Office making foreign or military policy. The president Twitters and thinks that that is policy. The Trump administration was destroyed when the weak Donald Trump allowed the neoconservatives to remove his National Security Advisor, General Flynn. Trump has never recovered. “His” administration is staffed with violent Russophobes. Wars can be the only outcome. We know two things about the alleged Russian inteferrance in the Trump/Hillary presidential election. One is that John Brennan, Obama’s CIA director, and Comey, Obama’s FBI director, implied repeatedly that Trump was elected by Russian interference in the election, but neither the CIA nor the FBI have provided any evidence whatsoever that any such interference occurred. Indeed, months into the case, the special prosecutor, the former FBI director, can produce no evidence.

The whole thing is a sham, but it is ongoing. There will be no end to it as it is designed to undermind President Trump with the people who elected him. The message is: “Trump is not for America. Trump is for Russia.”

Is Muelller going to investigate Comey soon?

• Comey’s Leaked Trump Memos Contained Classified Information (ZH)

Comey’s troubles started when he testified under oath last month that he considered the memos he prepared to be personal documents and that he shared at least one of them with a Columbia University lawyer friend. As Comey later disclosed, he asked that lawyer to leak information from one memo to the news media in hopes of increasing pressure to get a special prosecutor named in the Russia case after Comey was fired as FBI director. The Hill recounts that particular exchange with Senator Roy Blunt: “So you didn’t consider your memo or your sense of that conversation to be a government document?,” Sen. Roy Blunt (R-Mo.) asked Comey on June 8. “You considered it to be, somehow, your own personal document that you could share to the media as you wanted through a friend?”

“Correct,” Comey answered. “I understood this to be my recollection recorded of my conversation with the president. As a private citizen, I thought it important to get it out.” Comey insisted in his testimony he believed his personal memos were unclassified, though he hinted one or two documents he created might have been contained classified information. “I immediately prepared an unclassified memo of the conversation about Flynn and discussed the matter with FBI senior leadership,” he testified about the one memo he later leaked about former national security adviser Lt. Gen. Michael Flynn. Additionally, he added, “My view was that the content of those unclassified, memorialization of those conversations was my recollection recorded.”

That’s when the problems escalated, because according to The Hill – which for the first time disclosed that the total number of memos linked to Comey’s nine conversations with Trump – when the seven memos Comey wrote regarding his nine conversations with Trump about Russia earlier this year were shown to Congress in recent days, the FBI claimed all were, in fact, deemed to be government documents. Oops. As The Hill reveals, four, or more than half, of the seven memos had markings making clear they contained information classified at the “secret” or “confidential” level, according to officials directly familiar with the matter. This is a major problem for Comey because FBI policy forbids any agent from releasing classified information or any information from ongoing investigations or sensitive operations without prior written permission, and mandates that all records created during official duties are considered to be government property.

“Unauthorized disclosure, misuse, or negligent handling of information contained in the files, electronic or paper, of the FBI or which I may acquire as an employee of the FBI could impair national security, place human life in jeopardy, result in the denial of due process, prevent the FBI from effectively discharging its responsibilities, or violate federal law,” states the agreement all FBI agents sign. FBI policy further adds that “all information acquired by me in connection with my official duties with the FBI and all official material to which I have access remain the property of the United States of America” and that an agent “will not reveal, by any means, any information or material from or related to FBI files or any other information acquired by virtue of my official employment to any unauthorized recipient without prior official written authorization by the FBI.”

“..Not since Herbert C. Hoover has there been a more perfect scapegoat for an economic depression of the Fed’s making.”

• Tales from the FOMC Underground (PT)

“What should we do?” began Yellen. “A decade of easy monetary policies has turned financial markets into a Las Vegas casino while the economy’s lazed around like my smelly house cats. What the heck was Bernanke thinking?” “Hell, Janet,” remarked New York Fed President William Dudley. “He wasn’t thinking. He soiled his pantaloons and then he soiled them again.” “So now we must clean up his stinky pile while he promotes his revisionist courage to act shtick. The reality is we must orchestrate a take-down of financial markets, and we must do it by year’s end.” “Well, gawd damn Bill!” barked St. Louis Fed President James Bullard. “With the exception of Neel, the $700 billion dollar bailout boy, don’t you think we all know that?”

“Hey, now!” interjected Minneapolis Fed President Neel Kashkari. “Don’t blame me. I was just carrying out Hank Paulson’s will, right Bill? Saving our boys’ bacon back at Goldman so they could continue doing god’s work.” “Besides Fish, it was you all who lined up behind Bernanke and tickled the poodle with his crazy QE experiment while I was busy chopping wood at Donner Pass and getting my fanny spanked in the California Governor’s race by retread Jerry Moonbeam Brown, of all people.” “Fair enough,” continued Bullard. “The point is, taking down the stock market will cause an extreme upset to the economy’s applecart. The mobs will come after us with torches and pitchforks.” “You see, the real trick is to do the dirty deed then disappear behind a fog of confusion. That’s what Greenspan would do. How can we pull that off?”

After a moment of silent contemplation, and a licked finger held up to the cool political winds drafting across the country… “Eureka! We can pin it on President Donald J. Trump!” exclaimed Chicago Fed President Charles Evans. “Could our good fortune be any better? Not since Herbert C. Hoover has there been a more perfect scapegoat for an economic depression of the Fed’s making.” “Hear, hear!” approved Yellen. “Damn the economy,” they bellowed in harmony… minus Kashkari. “This one’s on Trump!” “Bill, one last thing,” closed Yellen. “After the meeting, remember to give the public that shake n’ bake you dreamed up about crashing unemployment. We have to give off an air of being data dependent.” “That misdirection should twist them up until NFL football starts. Shortly after that, our work will be done…” “…and by the New Year, Congress and Joe public will be begging us to rescue the economy from the Fed’s… I mean… Trump’s disastrous economic program.”

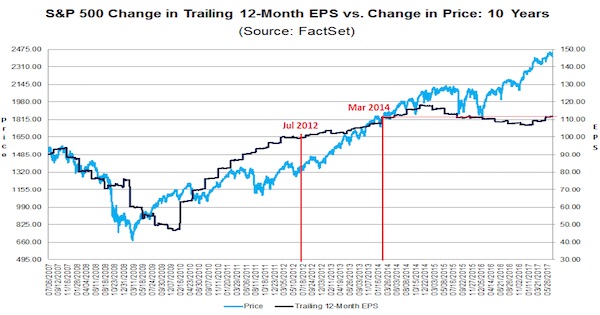

Earnings vs S&P. Something will give.

• Stock Market Tsunami Siren Goes Off (WS)

Everyone who’s watching the stock market has their own reasons for their endless optimism, their doom-and-gloom visions, their bouts of anxiety that come with trying to sit on the fence until the very last moment, or their blasé attitude that nothing can go wrong because the Fed has their back. But there are some factors that are like a tsunami siren that should send inhabitants scrambling to higher ground. Since July 2012 – so over the past five years – the trailing 12-month earnings per share of all the companies in the S&P 500 index rose just 12% in total. Or just over 2% per year on average. Or barely at the rate of inflation – nothing more. These are not earnings under the Generally Accepted Accounting Principles (GAAP) but “adjusted earnings” as reported by companies to make their earnings look better.

Not all companies report “adjusted earnings.” Some just stick to GAAP earnings and live with the consequences. But many others also report “adjusted earnings,” and that’s what Wall Street propagates. “Adjusted earnings” are earnings with the bad stuff adjusted out of them, at the will of management. They generally display earnings in the most favorable light – hence significantly higher earnings than under GAAP. This is the most optimistic earnings number. It’s the number that data provider FactSet uses for its analyses, and these adjusted earnings seen in the most favorable light grew only a little over 2% per year on average for the S&P 500 companies over the past five years, or 12% in total. Yet, over the same period, the S&P 500 Index itself soared 80%.

And these adjusted earnings are now back where they’d been on March 2014, with no growth whatsoever. Total stagnation, even for adjusted earnings. And yet, over the same three-plus years, the S&P 500 index has soared 33%. This chart shows those adjusted earnings per share for all S&P 500 companies (black line) and the S&P 500 index (blue line). I marked July 2012 and March 2014:

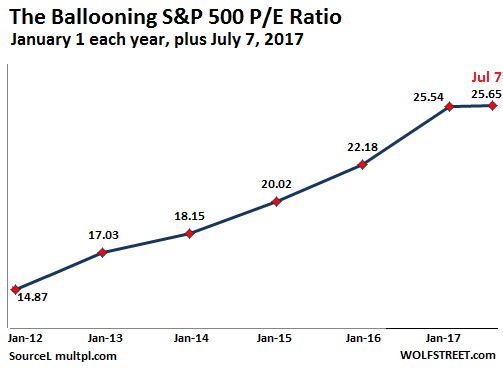

Given that there has been zero earnings growth over the past three years, even under the most optimistic “adjusted earnings” scenario, and only about 2% per year on average over the past five years, the S&P 500 companies are not high-growth companies. On average, they’re stagnating companies with stagnating earnings. And the price-earnings ratio for stagnating companies should be low. In 2012 it was around 15.5. Now, as of July 7, it is nearly 26. In other words, earnings didn’t expand. The only thing that expanded was the multiple of those earnings to the share prices – the P/E ratio. Such periods of multiple expansion are common. They’re part of the stock market’s boom and bust cycle. And they’re invariably followed by periods of multiple contraction. How long can this period of multiple expansion go on? That’s what everyone wants to know. Projections include “forever.” But “forever” doesn’t exist in the stock market. The next segment of the cycle is a multiple contraction.

The incessant call far a return to normal. There’s no such thing. The economy never recovered.

• America Is Struggling With Economic Rot (BBG)

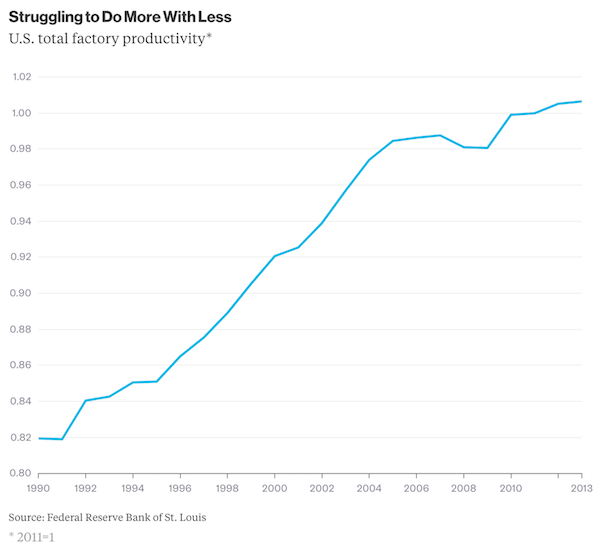

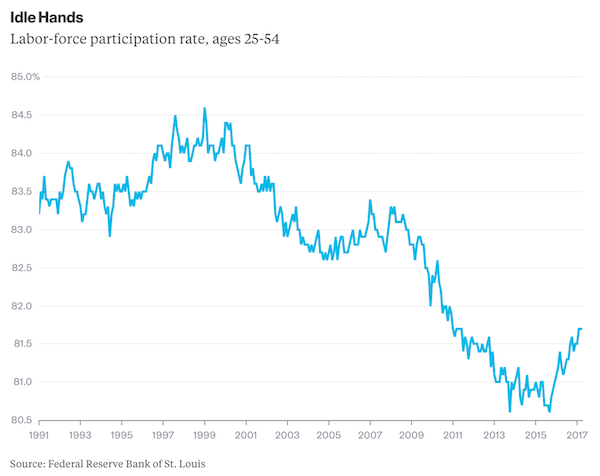

The Great Recession, and the financial crisis that preceded it, were such enormous and terrible events that they occupied most of our economic thinking for a decade. But now that the smoke has cleared and the economy has returned to a semblance of normality, we’re starting to think more about long-term trends. And evidence is mounting that the Great Recession may have drawn attention away from a slow rot that has been eating the U.S. economy since the turn of the century. Some of the top macroeconomists in the business have a new paper that reaches this conclusion. In “The Disappointing Recovery of Output after 2009,” John G. Fernald, Robert E. Hall, James H. Stock and Mark W. Watson break down the declines in growth and employment into a structural, long-term component and a short-term part related to the crash.

That’s an inherently hard thing to do, since there’s no universally accepted theory of how recessions work. But Fernald et al. use two accounting methods, and find basically the same thing – although the recession hurt the economy a lot, it happened to coincide with two trends that were slowly eroding the U.S.’s fundamentals. Those two trends are slowing productivity and reduced labor-force participation. Slow productivity growth is hardly news – Bloomberg View recently ran a whole series of articles about the phenomenon. This unhappy trend appears to have begun three years before the financial crisis:

As for labor-force participation, this has been falling since the turn of the century, though the last two years have seen a small uptick:

Both of these trends might have been exacerbated by the Great Recession. That economic disaster caused businesses to stop investing, which may have deprived them of the technology needed to increase productivity. Workers thrown out of employment by the recession might have seen their skills, connections and work ethic degrade, preventing them from going back to work even after the economy recovered.

His advise: call a snap election.

• May Appeals To Corbyn For Help In Coming Up With New Ideas (Ind.)

Theresa May is to insist she has the right vision for Britain and an “unshakeable sense of purpose” to build a fairer nation as she launches a fightback after her General Election gamble backfired. The Prime Minister will acknowledge that the loss of her Commons majority means she will have to adopt a different approach to government, signalling she is prepared to “debate and discuss” ideas with her opponents. But amid rumours of unrest within Tory ranks about her position, Ms May will insist her commitment is “undimmed” almost 12 months after entering Number 10 as Prime Minister. Her comments in a speech on Tuesday will be viewed as an attempt to relaunch her premiership after the humiliation of the election result and the need to strike a deal with the Democratic Unionist Party to prop up her administration in the Commons.

Ms May will return to her core message from when she succeeded David Cameron: a “commitment to greater fairness” and tackling “injustice and vested interests” in recognition that the EU referendum result was a “profound call for change across our country”. She will say: “Though the result of last month’s General Election was not what I wanted, those defining beliefs remain, my commitment to change in Britain is undimmed; my belief in the potential of the British people and what we can achieve together as a nation remains steadfast; and the determination I have to get to grips with the challenges posed by a changing world never more sure. “I am convinced that the path that I set out in that first speech outside Number 10 and upon which we have set ourselves as a Government remains the right one.

“It will lead to the stronger, fairer Britain that we need.” The fragile nature of Ms May’s position in the Commons will not stop her being “bold”, she will insist. “I think this country needs a Government that is prepared to take the bold action necessary to secure a better future for Britain and we are determined to be that Government. “In everything we do, we will act with an unshakeable sense of purpose to build the better, fairer Britain which we all want to see.”

Hard to believe.

• US-Russian Ceasefire Deal Holding In Southwest Syria (R.)

A U.S.-Russian brokered ceasefire for southwest Syria held through the day, a monitor and rebels said on Sunday, in the first peacemaking effort of the war by the U.S. government under President Donald Trump. The United States, Russia and Jordan reached the “de-escalation agreement,” which appeared to give Trump a diplomatic achievement at his first meeting with Russian President Vladimir Putin at the G20 summit in Germany this week. The Syrian Observatory for Human Rights, a Britain-based war monitor, said “calm prevailed” in the southwest since the truce began at noon (0900 GMT) on Sunday despite minor violations. Combatants briefly exchanged fire in Deraa province and in Quneitra around midnight, but this “did not threaten the ceasefire,” said Observatory Director Rami Abdulrahman.

Major Issam al Rayes, spokesman of the Southern Front coalition of Western-backed rebel groups, said “a cautious calm” continued into the evening. “The situation is relatively calm,” Suhaib al-Ruhail, a spokesman for the Alwiyat al-Furqan faction in Quneitra, said earlier. Another rebel official, in Deraa city, said there had been no significant fighting. It was quiet on the main Manshiya front near the border with Jordan, which he said had been the site of some of the heaviest army bombing in recent weeks. “Syrian ceasefire seems to be holding … Good!” Trump tweeted on Sunday. A Syrian official indicated that Damascus approved of the ceasefire deal, describing the government’s silence over it as a “sign of satisfaction.” “We welcome any step that would cease the fire and pave the way for peaceful solutions,” the government official told Reuters.

Majestic animal. But 1,300 years is a big gap.

• The Lynx Could Return To UK Within Months After 1,300-Year Absence (Ind.)

The Eurasian lynx could be stalking through British woodlands within months after plans were submitted to reintroduce the species, absent from Britain for about 1,300 years. Campaigners have applied for a licence to import six of the wildcats, which were hunted to extinction in the UK, and release them in Northumberland’s Kielder Forest. The Lynx Trust said the animals, which can grow to 1.3m in length, “belong” in Britain and there was a “moral obligation” to bring them back. The cats’ return would also generate millions of pounds for rural communities by attracting tourists, according to the group. But the proposal has met with opposition from sheep farmers, who claim their livestock would be put at risk.

The scheme would initially involve six lynx, four females and two males, being imported from Sweden and fitted with GPS tracking collars for a five-year trial. The trust applied to Natural England for permission to release the cats after it carried out an 11-month consultation. No date has been set for the proposed reintroduction but they cats could return to the UK by the end of 2017 if the plans are approved. The trust said in a statement: “In many other countries Eurasian lynx reintroduction has proven exceptionally low-conflict and wonderfully beneficial for the local communities that live alongside them, and we do sincerely hope that these cats, which thrived here for millions of years, do have the opportunity to prove they can still fit into both our ecology, and alongside local communities like those across the Kielder region.”