Lewis Wickes Hine Alma Croslen, 3, and mother. Both work at Barataria Canning, Biloxi, Miss. February 1911

Recent news, graphs and data confirm what we have long said would inevitably become clear: the entire global economy appears to have “functioned” through an orgy of refinancing, LBO and M&A lately. That is to say, zombie money has been enthusiastically slushed and re-slushed around to provide commissions, bonuses etc. to bankers and brokers, a process enabled by central bank and government policies in which large amounts of credit were thrown against the wall like so much Jello, hoping – but not demanding – that some would stick. Zero bound interest rates made this process all the more attractive, since it was crucial to lure mom and pop back in. But now, if our eyes don’t receive us, it is reaching its inherent limits. And that’s going to hurt something bad.

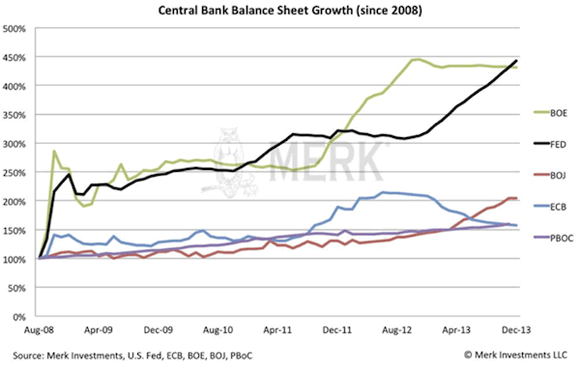

There has been such a flood of numbers in just the past week that it’s hard to choose, and to keep anything I would write on the topic from becoming an entire book. I’ll do my best. Let’s start with a few graphs that John Mauldin posted this weekend, which may seem a bit of a detour when US housing is the subject, but which are vital for understanding just that. First, from Merk, central bank balance sheets growth until January 1 2014. While most of you may be aware of the Fed Balance sheet growth, fewer might know what the Bank of England has been up to: a 200% growth in just one year, from mid-2011 to mid-2012. Note also that the Bank of Japan has been in the QE related game much longer than depicted by the graph’s timeline.

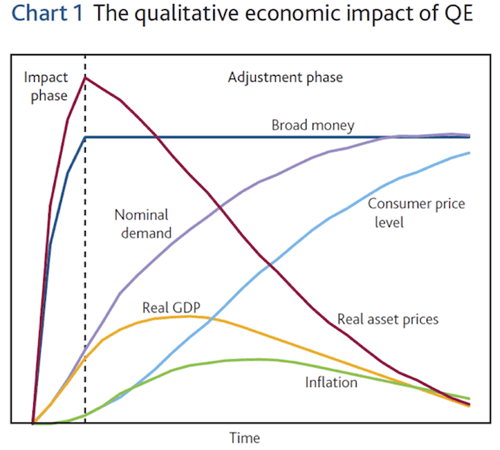

Then, a very interesting graph from the BOE, which dates back to 2011. Take a few real good looks. And realize that the ‘old lady of Threadneedle Street’ knew, as it undertook that 200% growth in its balance sheet, what, let’s put it mildly, the risks were. As an aside, it may be interesting to note how consumer price level and inflation run in opposite directions.

In the article he posted these graphs in, Mauldin says:

In 2011 the Bank of England gave us a paper outlining what they expected to be the consequences of quantitative easing. Note that in the chart below they predict exactly what we have seen. Real (inflation-adjusted) asset prices rise in the initial phase. Nominal demand rises slowly, and there is a lagging effect on real GDP. But note what happens when a central bank begins to flatten out its asset purchases or what is called “broad money” in the graph: real asset prices begin to fall rather precipitously, and consumer price levels rise. I must confess that I look at the graph and scratch my head and go, “I can understand why you might want the first phase, but what in the name of the wide, wide world of sports are you going to do for policy adjustment in the second phase?” Clearly the central bankers thought this QE thing was a good idea, but from my seat in the back of the plane it seems like they are expecting a rather bumpy ride at some point in the future.

I think the key line in that is: “what [..] are you going to do for policy adjustment in the second phase?“, because there doesn’t seem to be any policy available to stop the “second phase”. And that is essential when it comes to US housing (and many other asset classes in the global economy).

Mauldin continues to quote an interview from Finanz und Wirtschaft with William White, the former chief economist of the BIS:

… the fundamental problem we are still facing is excessive debt. Not excessive public debt, mind you, but excessive debt in the private and public sectors. To resolve that, you need restructurings and write-offs. That’s government policy, not central bank policy. Central banks can’t rescue insolvent institutions. All around the western world, and I include Japan, governments have resolutely failed to see that they bear the responsibility to deal with the underlying problems. With the ultraloose monetary policy, governments have no incentive to act. But if we don’t deal with this now, we will be in worse shape than before.

But wouldn’t large-scale debt write-offs hurt the banking sector again? Absolutely. But you see, we have a lot of zombie companies and banks out there. That’s a particular worry in Europe, where the banking sector is just a continuous story of denial, denial and denial. With interest rates so low, banks just keep ever-greening everything, pretending all the money is still there. But the more you do that, the more you keep the zombies alive, they pull down the healthy parts of the economy. When you have made bad investments, and the money is gone, it’s much better to write it off and get 50% than to pretend it’s still there and end up getting nothing.

Do you see outright bubbles in financial markets?

Yes, I do. Investors try to attribute the rising stock markets to good fundamentals. But I don’t buy that. People are caught up in the momentum of all the liquidity that is provided by the central banks. This is a liquidity-driven thing, not based on fundamentals.So are we mostly seeing what the Fed has been doing since 1987 – provide liquidity and pump markets up again? Absolutely. We just saw the last chapter of that long history. This is the last of a whole series of bubbles that have been blown. In the past, monetary policy has always succeeded in pulling up the economy. But each time, the Fed had to act more vigorously to achieve its results. So, logically, at a certain point, it won’t work anymore. Then we’ll be in big trouble. And we will have wasted many years in which we could have been following better policies that would have maintained growth in much more sustainable ways.

The BIS knew, the BOE knew, and there can be no doubt the Fed did too. Obviously, the key line here, “at a certain point, it won’t work anymore”, is essentially the same as Mauldin’s “what [..] are you going to do for policy adjustment in the second phase?“ Any bubble that ever has been blown, or will be, must pop. Or, as Mises put it: ““There is no means of avoiding the final collapse of a boom brought about by credit expansion.”

And at that point we can move on to US housing. First, the withdrawal of LBO funds like Blackrock from the housing market is a major issue. “The nation’s largest landlord” has slowed its purchases from $100 million to $10 million, as Jeffrey Snider writes for Alhambra:

The Q1 Housing Rollover Is Deep And Wide—And A Stinging Rebuke To Monetary Central Planning

In the middle of last week, the Census Bureau estimated that permits to build new single-family homes declined on a year-over-year basis for the second consecutive month. That s the first time we have seen anything like that since the middle of 2011, just before this latest surge in housing began. This week, the National Association of Realtors (NAR) reported another significant decline in existing home sales. After falling 5.1% Y/Y in January (snow, we are told), home sales decreased 7.1% in February (some snow, we are told) and then 7.5% in March (getting ready for next winter?). If that wasn’t enough, the Census Bureau reported on Wednesday that new home sales dropped by a rather stark 12.2% Y/Y, also in March.

Across the state of housing-related finance, there was little surprise to see quarterly bank reports for the first quarter show heavy, massive declines in mortgage finance. Originations at Wells Fargo (-67%), JP Morgan Chase (-68%) and Bank of America (-63%) were a cumulative $185 billion in the first quarter of 2013, but a mere $61.9 billion in this latest quarter. Most of that conclusive cessation of mortgage lending is attributable to refinancing, but more than a fair amount was once lent on the basis of home purchasing intentions.

Total MBS issuance in June 2013 was $185.5 billion, but the latest figures for March show a 53% decline to only $87.2 billion. Institutional buying of property, as you might surmise from that last sentence, has attained more than whispers of dramatic retrenchment, becoming further and actual anecdotes. In California, the largest REO-to-rent firms, those with direct access to QE’s primary magnanimity , have scaled back purchase activity by as much as 70% in recent months. Blackstone, now the nation’s largest landlord, has condensed its purchase pace in California by as much as 90%; 70% overall from last year’s peak pace of more than $100 million per week.

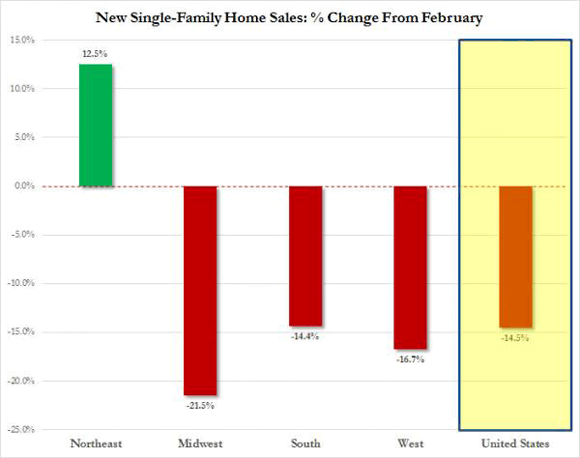

Blackstone is an all-cash buyer, no mortgages involved. So when we see that mortgages, too, are plunging, that’s a double whammy. Moreover, new home sales were reported to have plummeted 14.5% in March (13.3% YoY), to an eight month low, and refinancing is MIA. All in all, US housing looks to be in, say, a bit of a pickle. And with it everyone who’s taken on debt to purchase a house. The Wall Street Journal:

Demand for Home Loans Plunges: Mortgages at 14-Year Low

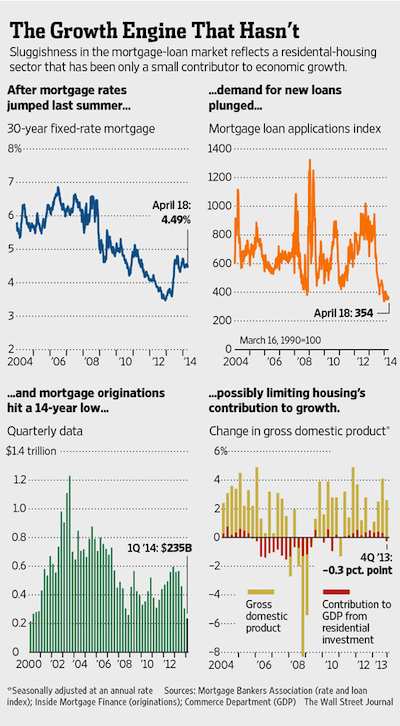

Mortgage lending declined to the lowest level in 14 years in the first quarter as homeowners pulled back sharply from refinancing and house hunters showed little appetite for new loans, the latest sign of how rising interest rates have dented the housing recovery.

Lenders originated $235 billion in mortgage loans during the January-March quarter, down 58% from the same period a year ago and down 23% from the fourth quarter of 2013, according to industry newsletter Inside Mortgage Finance. The decline shows how the mortgage market is experiencing its largest shift in more than a decade as an era of generally falling interest rates that began in 2000 appears to have run its course. [..] The decline in mortgage lending last quarter stemmed almost entirely from the slide in refinancing. [..] Applications for purchase mortgages last week ran nearly 18% below the level of a year ago, even as the average loan amount on new applications hit a record of $280,500 [..]

While mortgage rates are still low by historical standards, they’re less useful to traditional buyers because home prices have risen swiftly, offsetting any benefit that low rates provide to reduce housing costs. As a result, “housing is becoming a less effective transmission belt for the Fed” to boost the economy, [Stan Humphries, chief economist at Zillow] said. The rise in mortgage rates has also slammed refinancing, which fell 75% during the first quarter from the year-earlier period, according to Inside Mortgage Finance.

The mortgage industry has grown steadily since the early 1980s and particularly since the early 2000s from repeated refinancing binges. The share of refinancing, which made up more than 40% of all mortgage lending since 2000, fell to 47% of all mortgage lending in the first quarter, compared with 78% a year earlier. “The real question for 2014 and later is how low the refinance share is going to go,” said Guy Cecala, publisher of Inside Mortgage Finance. When mortgage rates jumped nearly two percentage points in 1994, refinancing fell to 11% that June, from 63% the prior October. [..]

Lenders not only face a more competitive environment with lending demand dropping, but they must also focus more heavily on loans to buy homes, which are more time intensive than loans to refinance. “Margins and profitability will be tremendously difficult this year for mortgage companies,” said Anthony Hsieh, chief executive of loanDepot.com, a closely-held mortgage bank based in Foothill Ranch, Calif. [..] In Nevada and Florida, more than 80% of condos have sold without a mortgage since 2009, according to data from CoreLogic Inc. [..] Some economists say a bigger problem facing the economy is consumers that are too weak. Too many can’t borrow because they have high levels of debt, damaged credit from the recession or insufficient incomes to become home buyers, and looser credit standards aren’t likely to easily address those challenges.

[..] … two developments allowed the mortgage industry to keep production humming even after rates began to rise. First came the expansion of the subprime market from 2004 to 2006. Lenders relaxed standards, triggering a boom in so-called cash-out refinancing in which rising home prices and aggressive lenders enabled borrowers to take out larger loans on their homes. Then in late 2008, the Fed embarked on the first of its bond purchases, known as “quantitative easing,” which brought rates back to their 2003 lows and later, below those levels to their lowest in nearly 60 years.

The latest boom was also fueled by a revamped government initiative that made it easier for more homeowners to refinance even if they were underwater, or owed more than their homes were worth. Now, the industry is poised for a shakeout that could flush out lenders that can’t survive on smaller margins. “This change is much more structural and will be longer lasting,” said David Stevens, chief executive of the Mortgage Bankers Association. “It’s a classic supply-and-demand scenario. We have an excess supply of lenders and a lack of demand.”

Not that lenders will give up so easily. The Guardian sees more trickery in the near future.

Banks Return To Risky Business: Lax Standards And Subprime Loans

Homeowners aren’t refinancing any more, and new home sales hit their lowest levels in eight months in March. The result? Double digit dips in mortgage lending, already buffeted by an uptick in long-term interest rates. Fixed-income trading is in the doldrums, too. That leaves new mortgage lending at a 14-year low. [..] It’s going to get tougher for the banks to make their earnings look better than they really are. If all these falling profits are the banks’ problem, their solution to the problem could end up being worse.

That’s because whenever growth falters, profit-hungry banks have a history of taking on more risk: risk they can’t afford, that they don’t understand or that they can’t manage. They relax lending standards (remember no-doc loans and the subprime lending debacle?) or underwriting standards (the junk bond and leveraged buyout boom of the late 1980s; and during the dot.com bubble). Allegations of mis-selling of products, ranging from annuities to complex derivatives, multiply like rabbits left unattended.

But former Director of the Office of Management and Budget under Reagan, David Stockman, is not so sure trickery will do the job this time.

That Was Quick! How The Fed Ravaged The Main Street Housing Market, Again

In less than two years more than 400,000 busted mortgages were scooped up by LBO funds on the theory that single family suburban housing had become a new “asset class”—-and that the “buy-to-rent” investment models put together by spreadsheet jockeys was the next Big Thing. There was even going to be a new version of the Wall Street slice-and-dice machine—this time in the form of securitized rental payment streams rather than mortgage payments. That way renters in Scottsdale AZ could send their rent checks to Wall Street where they would be forwarded in pieces to the proverbial Norwegian fishing village retirement fund.

But the grand scheme didn’t attain lift-off—other than to drastically and suddenly inflate housing prices in the default-ridden lower-end of the bombed-out sub-prime housing markets. In some areas, prices exploded upwards by 25-50% in less than two years, but that wasn’t evidence of healing and recovery as was so loudly brayed by Wall Street and Fed economists. It was just fast-ignition hot money piling into another momentum trade.

All the other factors which were supposed to get better according to the spreadsheet models, however, didn’t track their appointed paths. In the real world the cost of rehabbing the foreclosures purchased in bulk on the courthouse steps ended up higher; vacancy rates fell more slowly than modeled; renter churn was greater; maintenance costs were higher; rents rose more slowly; and the Norwegian fishing villages were not quite so eager to buy the latest product from Wall Street’s meth labs.

Add to all the above, the 130 basis point surge in the home mortgage yields in recent months, and suddenly a whistle blew on the buy-to-rent stampede. It stopped nearly dead in the water during the past four months, and now there is growing evidence that Wall Street landlords may be trying to liquidate their hastily acquired properties [..] The fact is, Wall Street’s financial models didn’t work—even if the LBO shops were able to carry their surging property inventories on cheap, Fed-enabled bank lines. Instead, prices fired-up too rapidly while all the operating variables of the rental models came out of the gates too tepidly. [..] the next phase should be even more combustible than the flash boom. Namely, if housing prices head south again, the LBO funds will be forced to liquidate their inventories—-and they won’t be deliberate about it.

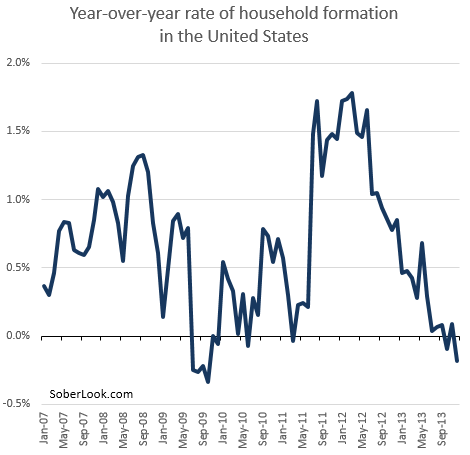

Lance Roberts at STA drives home the importance of the stunning decline in US household formation. When middle aged people return home to live with their parents, something’s going spectacularly wrong. And when young people can’t find jobs that pay enough to afford the simplest homes, they sit and wait and don’t start families. This is dramatic for reasons far superior to mere financial issues; it greatly changes the entire composition and fabric of society.

Schadenfreude: Economists “Stunned” By Housing Fade

The slowdown in housing is not due to the “weather.” It began prior to the onset of the recent winter blasts. Nor will reduced distressed sales, delinquencies, negative equity or rising inventories salvage the predictions. These are all indicators “OF” the housing market, but not what “DRIVES” the housing market. The real answer to the slowdown in housing is not so difficult to comprehend [..] The housing market is driven by what happens at the margins. At any given point, there are a finite number of people wanting to “buy” a home and those that have a “for sale” sign in their yard. As with all markets, changes in the housing market are driven by the “supply/demand” equation. There is notably five important points that should be considered.

[..] Incremental increases in interest rates have a direct effect on a buyer’s “willingness” and “ability” to make certain monthly payments. Since, the majority of American’s are already primarily living paycheck-to-paycheck, any increase in the monthly payment may change both affordability and qualification for a loan. Since individuals are “backward looking,” increases in interest rates may put a hold on activity as they “hope” that the payment, mortgage rate or home price they just missed out on will be available again soon. While individuals will eventually adjust upward, it will take some time for them to become “convinced” that a change has permanently occurred.

Many of the homes that have been purchased to date were by “all cash” buyers and institutions for conversions to rental properties. Now, with “price-to-rent” ratios reaching levels of low profitability – the demand for that activity is decreasing. As I stated last year: “We are likely witnessing the beginning of that slowdown.” Furthermore, with institutions now moving to liquidate their rental investments either through direct sale or IPO – the increase in supply without an increasing pool of available and willing buyers could intensify downward pressure. [..] As discussed by Walter Kurtz recently:

“The biggest issue, however, remains household formation. As of the end of last year, for example, the number of American households was not growing at all. This is likely due to record low marriage rates as well as a slew of other factors (lack of employment, wage growth, etc.). Whatever the reason, household formation needs to stabilize before we see stronger results in the US housing market.”

[..] The current decline in housing is not a “weather related” anomaly but a function of “real” affordability. I say “real” affordability, because buying a house is not just about the price, but the ability for a family to qualify for and pay the mortgage. Unfortunately, despite the ever ebullient hopes of mainstream analysis, the core requirements of rising wage growth, full-time employment, loan qualification and the ability to save a downpayment keeps home ownership elusive for many. That is unlikely to change anytime soon.

David Stockman again:

It Didn’t Snow In San Jose: The Q1 Housing And GDP Rollover Is Not Due To Weather

In truth, the US economy is freighted down by peak debt and is incapable of the kind of conventional credit-fueled rebound cycle that the Fed has orchestrated in the past. As should be evident by now, our national LBO is over. With $59 trillion of public and private credit market debt, the US leverage ratio stands at 3.5X national income – massively above the 1.5X leverage ratio that was compatible with healthy, stable economic conditions before 1980. The two extra turns of leverage laid on the economy over the past 35 years is exactly what blocks the ‘escape velocity’ that Keynesian economists and Wall Street stock peddlers continuously espy just around the bend.

[..] ]Economic growth hewed to the flat line notwithstanding the massive money printing by the Fed because after a three decade-long party, the American economy has way too much debt; has generated way too little real savings and investment in productive assets; and has accumulated wage and cost levels which are way too high to be competitive in today s world economy. Yet now we are in month 58 of this recovery cycle compared to an average expansion of 53 months during the 10 post-war business cycles. That is, on a calendar basis this so-called recovery is already on borrowed time. But actually the true condition is much worse because now there are headwinds coming from nearly every direction on the economic compass.

On the international scene, Abenomics is failing catastrophically in Japan. The Chinese house of cards is becoming more shaky by the week. The EM economies, which boomed on cheap capital inflows owing to financial repression by the DM central banks and as the supply base for the Chinese building spree, are heading for devastating financial crises and recessions. And in Europe Draghi’s complete con job is self-evidently not sustainable. In fact, the still faltering EU economies outside of Germany are only one slip-of-the-tongue away from a drastic sell-off of their ridiculously mis-priced government bond markets, and therefore a renewed round of fiscal and financial crisis.

So the US economy can not export its way into escape velocity . Indeed, it actually stands squarely in harm’s way as the two-decade long central bank fueled global investment boom and financial bubble stumbles into the brutal correction and deflation that is just now getting underway. Likewise, the domestic headwinds are already evident in the stunning roll-over in the housing market during the last several months. Now that the flash boom in housing prices is over owing to the hasty retreat of the big LBO funds from the short-lived buy-to-rent market, the underlying weakness of organic demand has become starkly evident.

Sales are now down significantly from year ago levels in major markets all across the country, and, as the following list makes clear, it was not the weather that did it. Instead, it was 130 basis points of interest rate normalization -and that is just the beginning. The salient fact of the matter is that the decades long era of refi madness is over. During the first quarter, gross mortgage originations totaled just $235 billion, the lowest rate in 14 years. Stated differently, the mortgage issuance run rate is now about $1 trillion on an annualized basis -a level that represents just 30% of the normal volume since the mid-1990s.

And the stalled-out housing finance engine is not unique. It’s just the leading edge illustration of what happens when credit-fueled rebounds no longer happen. Indeed, the crash of Q1 mortgage finance volumes shown below demonstrates that the very notion of escape velocity , or what in truth is really a euphemism for a credit fueled growth surge, is an obsolete relic of a bygone era. [..] … this time is different. The debt party is over. The era of financial retrenchment and living within our means has begun.

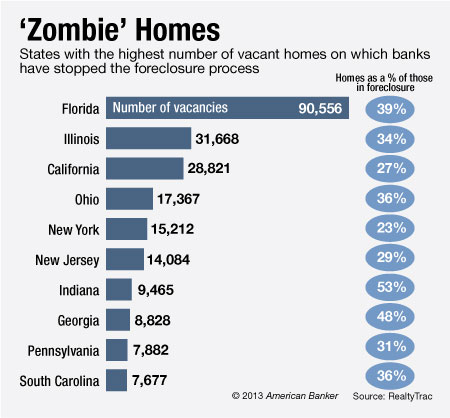

And as if all those bad sales numbers are not misery enough, there’s yet another factor, that few have acknowledged, but Kate Berry at American Banker does notice: zombie foreclosures, which have gone up about tenfold in the past 4 years.

Banks Halting Foreclosures to Avoid Upkeep (American Banker)

Banks are walking away from thousands of vacant properties after starting and then refusing to complete the foreclosure process because they do not want to pay for maintaining the homes. The result: hundreds of thousands of homes are being withheld from the market, raising questions about whether the recent run-up in housing prices is artificial. Meanwhile, former homeowners that have already left the property with the belief they lost the home to foreclosure are ending up on the hook for the unpaid debt, taxes and repairs. [..]

Bank “walkaways” used to be extremely rare, but they have ballooned in the past year or so, resulting in a large number of homes stuck in foreclosure, sometimes for years. More than 300,000, or 35%, of the roughly 1 million homes currently in the process of foreclosure are vacant and the servicer has not taken title to the home, according to new data from RealtyTrac, the Irvine, Calif., data firm. In 2010, the Government Accountability Office estimated the number of abandoned foreclosures to be between 14,500 to 34,600 homes. “We call them zombie foreclosures,” says Daren Blomquist, vice president at RealtyTrac…

That was 8 articles I quoted from. And I could quote 8 more. But the general drift should be clear by now, I think and hope. The US housing sector has hit a major snag, and it’s hard to see what would lift it up again. I called this piece US Housing Is Down For The Count, not US Housing Is Down For The Count, because there may still be some silly Fed move that can hide the truth a little longer, though it gets harder to see what that would be. And much more importantly, I find, is for us all to wonder whether such a move would be good thing in an economy, and a housing sector, that has become so dependent on and addicted to easy Fed money that asset prices across the board have become so distorted it’s no longer possible to do any genuine price discovery, even if that is supposed to be a main pillar of our economic system.

Fed policy over the past two decades (or make that at least since the day Greenspan came in) has taken away a large part of what the American people had ‘amassed’ in wealth. That wealth has now been transferred to the financial sector, while the already much poorer people can expect the bill to land on their doormats for all the additional debt ‘amassed’ by the government and the Fed. And that leads me, again, to question ideas like for instance this one from John Mauldin:

” … there is reason to believe that there have been major policy mistakes made by central banks – and will be more of them – that will lead to dislocations in the markets – all types of markets.”

I wonder: why would anyone use the term ‘mistakes’ in this context? Why are people so averse to even considering that perhaps this is not a long series of mistakes, but instead, a deliberate policy? After all, it’s Mauldin himself who comes up with the 2011 BOE graph that proves to us that central banks were acutely aware, at least as long ago as that, of the risks involved in QE policies. Yet, one full year after that graph was published, and there’s no way the Fed heads didn’t see it when it did, that same Fed started expanding its balance sheet by another 50%. In what universe is that called a mistake?

Mind you, in the graph broad money is kept at a stable level, after it’s been highly elevated through QE. Need you ask what might happen when that too is brought down to more “historically normal” levels? When it comes to US housing, what deserves attention is the insane drop in asset prices, but also falling GDP and rising consumer prices. The last two will combine to make buying property much less affordable to much more people. Even as prices come down. I’m 100% with Stockman on this one: The debt party is over. The era of financial retrenchment and living within our means has begun.

And even if Janet Yellen pulls one last rabbit from her hair, that’s just delay of execution. But don’t think you’ll hear about that from her, or your trusted media, or your favorite politician. The carefully scripted recovery story is not yet about to fade; indeed, the efforts to make you believe it will surge at the same rate as the federal debt and the Fed balance sheet have. Until, to quote one of my quotes, “at a certain point, it won’t work anymore”.

Home › Forums › US Housing Is Down For The Count