Jack Delano Milk Woman Taking Over In Wartime, Bryn Mawr, Pa. June 1943

175,000 new jobs (we await revisions) and a rising unemployment rate (6.7%). Which was not due to people re-entering the labor force, as has been suggested, since the labor force participation rate remained stuck at 63%. This hasn’t been going anywhere for years now, it’s all stuck around 150,000 or so – the running to stand still level – , sometimes up, sometimes down, with lots of revisions. It should worry the pants off of America, but stock markets set new records on a regular basis instead.

Since the real economy is hardly budging at all, the “new profits” can only come from QE-esque money streams, and that, after 5 years now, is getting extremely worrisome. Janet Yellen may keep it up a while longer, but there’s so much inert volatility (aka volatile inertia) built in to the US economy by now that is has become inevitable that an infinitely small spark can set the whole thing on fire, let alone an escalating conflict like Crimea.

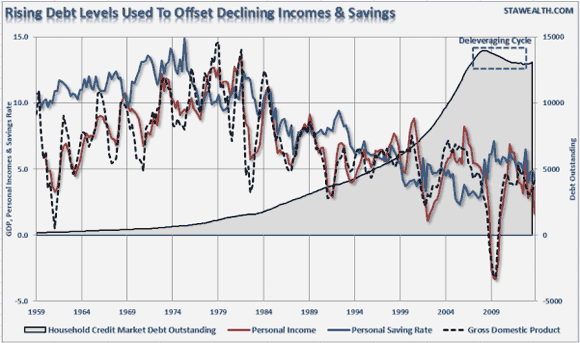

The US economy has no resilience left, it’s a severely overworked one trick pony that can’t, as should be organic and obvious, make up for losses in one field with gains in another, since all gains have come from one and the same source for years now. It’s an accident waiting to happen, and it has no defenses left against any such accident: they’ve been spent on various QEs, and used as a defense against truth finding, not crisis. How bad things are is illustrated in this graph I picked up at Zero Hedge:

Personal savings (yoy), personal income (yoy), GDP (yoy), everything is on a downward trend as, moreover, household debt levels have risen fast. Where on earth would GDP and incomes be without that debt? If you’re even a teeny weeny little faint of heart, you might not want to give that too much thought. And besides, there’s no shortage of good news, right? Like this from Bloomberg:

US Household Worth Climbs by $2.95 Trillion to Record $80.7 trillion

Net worth for households and non-profit groups rose by $2.95 trillion in the fourth quarter, or 3.8% from the previous three months, to a record $80.7 trillion,

• The value of financial assets, including stocks and pension fund holdings, held by American households increased by $2.52 trillion in the fourth quarter, according to today’s Fed report. The Standard & Poor’s 500 Index climbed 9.9% from Sept. 30 to Dec. 31, capping the best yearly gain since 1997.

• Household net worth was $11.8 trillion greater than its pre-recession peak of $68.8 trillion reached in the second quarter of 2007.

Does that look good or what? Well, it does, if you don’t read the last few paragraphs:

• Household debt increased at a 0.4% annualized rate last quarter, today’s Fed report showed. Mortgage borrowing dropped at a 1% pace. Other forms of consumer credit, including auto and student loans, increased at a 5.4% pace.

• For all of 2013, household debt climbed 0.9%, the biggest gain since 2007, even as Americans continued to pay down home loans. Mortgage borrowing fell 0.8%, the smallest drop since 2008, which marked the first year of the recession.

• Total non-financial debt increased at a 5.4% annual pace last quarter, the most in a year. Federal government obligations jumped by 11.6%, the biggest gain since the first three months of 2012.

Household worth rises at the same time that household debt does. Yes, sure. Federal debt up 11.6%, and the Fed still adds $65 billion a month.

We’re basking in the blinding light of a mirage that’s set to blow. One spark is all it will take. There are no firefighters left, and no water to extinguish the flames.

What could create that spark? Ukraine, obviously, people will panic the moment the first shot is fired. It’s not as if the US exudes confidence in the matter, but that is of minor importance, stocks would drown regardless.

Another possibility would be the housing market, and in general a continuation of rising interest rates in the real economy. As Michael Lombardi explains:

Why the U.S. Housing Market Recovery Will Falter This Year

• … from their peak in 2007 to their low in late 2011, U.S. home prices fell by about 30%. Since then, prices in the housing market have improved, but they are still down about 20% compared to 2007. Basically, home prices have recouped only one-third of their losses from the 2007 real estate crash.

• … the interest rate on the 30-year fixed mortgage tracked by Freddie Mac increased to 4.43% in January of this year from 3.41% in January of 2013.

• … mortgage rates have increased by 30% in one year’s time. With the Federal Reserve cutting back on its quantitative easing program, interest rates are expected to continue their path upwards in 2014.

• … The U.S. Mortgage Bankers Association reported last week that its index, which tracks mortgage activity (of both refinanced and new home purchases), fell 8.5% in the week ended February 21.

• … If there is one thing the housing market detests, it’s rising interest rates. Higher interest rates simply push would-be homebuyers away. And with rates expected to continue rising in 2014, I see the housing market rebound stagnating this year.

One spark to a defenseless system with far too few moving parts left and overflowing with volatility. The US economy is a sitting duck dead in the water.

• Why the U.S. Housing Market Recovery Will Falter This Year (Profit Confidential)

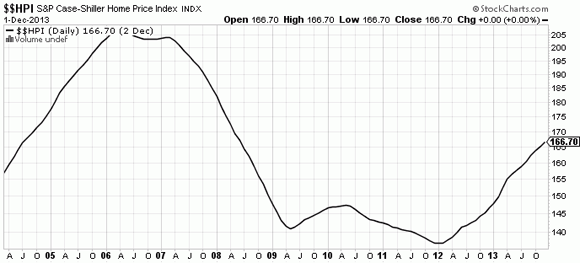

The chart below is of the S&P Case-Shiller Home Price Index, an index that tracks home prices in the U.S. housing market. As the chart shows, from their peak in 2007 to their low in late 2011, U.S. home prices fell by about 30%. Since then, prices in the housing market have improved, but they are still down about 20% compared to 2007. Basically, home prices have recouped only one-third of their losses from the 2007 real estate crash.

Yes, the U.S. housing market has regained some lost ground, but it’s far from being back to where it was in 2007. And I’m very worried about the pace of the housing market recovery; I feel that the recovery is in jeopardy.

Chart courtesy of www.StockCharts.comConsider this: the interest rate on the 30-year fixed mortgage tracked by Freddie Mac increased to 4.43% in January of this year from 3.41% in January of 2013. (Source: Freddie Mac web site, last accessed February 26, 2014.) While there hasn’t been much mainstream media coverage on this, mortgage rates have increased by 30% in one year’s time. With the Federal Reserve cutting back on its quantitative easing program, interest rates are expected to continue their path upwards in 2014.

Higher interest rates are pushing would-be homebuyers away from the housing market. The U.S. Mortgage Bankers Association reported last week that its index, which tracks mortgage activity (of both refinanced and new home purchases), fell 8.5% in the week ended February 21. (Source: Reuters, February 26, 2014.)

And new homebuilders are seeing demand from homebuyers decline in the housing market as well. While presenting the company’s corporate earnings for the fiscal year 2014, the CEO of Toll Brothers, Inc. said, “As we have previously discussed, after very strong contract growth beginning in the fourth quarter of FY 2011 and running through the third quarter of FY 2013, demand has leveled more recently against some very strong prior year comparisons…” (Source: “Toll Brothers Reports FY 2014 1st Qtr Results,” Toll Brothers, Inc., February 25, 2014.)

Listen to those who know the U.S. housing market better. Robert Shiller, the co-creator of the S&P Case-Shiller Home Price Index, during an interview last week with CNBC said, “My instinct is that this momentum (in housing prices) will dissipate.” (Source: “Shiller: Signs housing is weakening,” CNBC, February 25, 2014.)

If there is one thing the housing market detests, it’s rising interest rates. Higher interest rates simply push would-be homebuyers away. And with rates expected to continue rising in 2014, I see the housing market rebound stagnating this year.

• US Household Worth Climbs by $2.95 Trillion to Record (Bloomberg)

Household wealth in the U.S. increased from October through December, as gains in stock portfolios and home prices boosted Americans’ finances. Net worth for households and non-profit groups rose by $2.95 trillion in the fourth quarter, or 3.8% from the previous three months, to a record $80.7 trillion, the Federal Reserve said today from Washington in its financial accounts report, previously known as the flow of funds survey.

More jobs, higher stock prices and improved home values have all helped consumers clean up their balance sheets in the years following the biggest recession since the Great Depression. Additional gains in the labor market and household wealth will be needed to give consumers the means to spend on goods and services, boosting economic growth. “The gains in wealth are cumulative and they’re likely to have, over time, a more positive effect on consumer spending,” said Sam Coffin, an economist at UBS Securities LLC in Stamford, Connecticut. Looking ahead, gains will be “a bit less rapid, but we do have continued improvement.”

The value of financial assets, including stocks and pension fund holdings, held by American households increased by $2.52 trillion in the fourth quarter, according to today’s Fed report. The Standard & Poor’s 500 Index climbed 9.9% from Sept. 30 to Dec. 31, capping the best yearly gain since 1997.

An improving housing market also boosted household wealth. The S&P/Case-Shiller national home-price index rose 11.3% in the fourth quarter from the same period in 2012, the biggest year-over-year advance since the first three months of 2006. Household real-estate assets climbed by $401.1 billion, the data show. Owners’ equity as a share of total household real-estate holdings increased to 51.7% last quarter from 50.6% in the previous three months.

Household net worth was $11.8 trillion greater than its pre-recession peak of $68.8 trillion reached in the second quarter of 2007. It was $77.7 trillion in the three months ended September.

The Fed is trying to preserve improvements in household net worth by maintaining an accommodative stance, even as it scales back its unprecedented stimulus program. Fed Chair Janet Yellen said the central bank intends to reduce asset purchases at a “measured” pace, in testimony before the Senate last week. She also said in response to a separate question that the bond-buying program is likely to end in the fall. At the same time, “if there’s a significant change in the outlook, certainly we would be open to reconsidering,” Yellen said.

Household debt increased at a 0.4% annualized rate last quarter, today’s Fed report showed. Mortgage borrowing dropped at a 1% pace. Other forms of consumer credit, including auto and student loans, increased at a 5.4% pace.

For all of 2013, household debt climbed 0.9%, the biggest gain since 2007, even as Americans continued to pay down home loans. Mortgage borrowing fell 0.8%, the smallest drop since 2008, which marked the first year of the recession.

Total non-financial debt increased at a 5.4% annual pace last quarter, the most in a year. Federal government obligations jumped by 11.6%, the biggest gain since the first three months of 2012. Business borrowing rose 7.1%. State and local government debt dropped at a 4.9% pace.

A view from Moscow.

• Why There Will Be War in Ukraine (Moscow Times)

The current crisis is not about Crimea. It is about the rights of Russian-speakers throughout Ukraine whom the Kremlin wants to protect from violence and discrimination. Russia does not want a military intervention in Crimea and does not want to take Crimea from Ukraine.

There is a political solution to this crisis. First, create a coalition government in Kiev composed of all parties, including those from the east and south of the country. The current government is dominated by anti-Russian extremists from western Ukraine.

Second, Ukraine needs to draft a democratic constitution that has guarantees for Ukraine’s Russian-speaking population that would grant official status to the Russian language and establish the principle of federalism.

Third, presidential and parliamentary elections must be held soon. Independent election observers must play an active role in ensuring that the elections are free and fair. There is a real danger that they will be manipulated by the neo-Nazi militants who de facto seized power in a coup.

If these democratic and peaceful solutions to the crisis in Ukraine are rejected by the opposition forces that have seized power in Kiev, I am afraid that Russia will have no other choice but to revert to military means. If the junta leaders want to avoid war, they need to adopt Moscow’s peaceful and democratic proposals and adhere to them.

Those currently in power in Kiev are carrying out a political strategy that is not so much pro-European as it is anti-Russian, as evidenced by the surprisingly heavy-handed tactics the U.S. and European Union have employed in Ukraine. In the end, a minority executed a violent coup that removed the democratically elected and legitimate president of Ukraine.

The Kremlin believes that the current Ukrainian leadership will manipulate the elections planned for May 25 to install a single leader or coalition government functioning much as former Georgian President Mikheil Saakashvili did in Tbilisi. A “Ukrainian Saakashvili” will unleash an even more repressive campaign of intimidation against Russian-speakers, one that over several years would stoke anti-Russia hysteria among the general population.

After that, Kiev may evict Russia’s Black Sea Fleet from Sevastopol and purge Crimea of any Russian influence. Ukraine could easily become a radicalized, anti-Russian state, at which point Kiev will fabricate a pretext to justify taking subversive action against Moscow. This looks especially likely considering that ruling coalition members from the neo-fascist Svoboda and Right Sector parties have already made territorial claims against Russia.

They could easily send their army of activists to Russia to join local separatists and foment rebellion in the North Caucasus and other unstable regions in Russia. In addition, Russia’s opposition movement will surely want to use the successful experience and technology of the Euromaidan protests and, with the help and financial support of the West, try to carry out their own revolution in Moscow. The goal: to remove President Vladimir Putin from power and install a puppet leadership that will sell Russia’s strategic interests out to the West in the same way former President Boris Yeltsin did in the 1990s.

The official census puts the Russian minority in Ukraine at 16% of the total population, although that number was falsified. The actual number is closer to 25%. Surveys indicate that 45% of the country’s population speak Russian at home, 45% speak Ukrainian and 10% speak both languages. In the most recent Gallup survey, when asked in which language they would like to be polled, 83% of respondents chose Russian. Taking into account the rural population in western and central Ukraine, about 75% of the people, probably speak Russian. Of that 75%, only about 10% are those in Kiev and a few other major cities who supported the protests. This means that only 35% of the population are attempting to impose its will on the remaining 65%, using a violent coup to achieve their goals.

Putin made the right decision: He did not wait for that attack and took preventative measures. Many in the West say the Kremlin’s reactions were paranoiac, but Germany’s Jews also thought the same of leaving the country in 1934. Most of them chose to believe they were safe and remained in Germany even after Hitler came to power. The infamous Kristallnacht took place five years later, one of the first early chapters in the “Final Solution.” Similarly, just four years remain until Russia’s presidential election in 2018, and there is a strong risk that subversive forces within and outside Russia will try to overthrow Putin, in part using their new foothold in Ukraine.

Will there be war in Ukraine? I am afraid so. After all, the extremists who seized power in Kiev want to see a bloodbath. Only fear for their own lives might stop them from inciting such a conflict. Russia is prepared to move its forces into southern and eastern Ukraine if repressive measures are used against the Russian-speaking population or if a military intervention occurs. Russia will not annex Crimea. It has enough territory already. At the same time, however, it will also not stand by passively while Russophobic and neo-Nazi gangs hold the people of Crimea, Kharkiv and Donetsk at their mercy.

And another one.

• Russia hits back at US ‘barefaced cynicism and double standards’ over Ukraine (RT)

The Russian Foreign Ministry has accused the US State Department of double standards and low-level propaganda after it published a list of President Vladimir Putin’s “false claims” about the events in Ukraine. “The State Department is trying to play on a shamelessly one-sided interpretation of the events,” ministry spokesperson Aleksandr Lukashevich said on Thursday. “Surely, Washington cannot admit that they were nurturing Maidan [protests], encouraging the violent overthrow of the legitimate government, and thus clearing the way for those who are now pretending to be a legitimate power in Kiev.”

On Wednesday, one day after the Russian president’s media conference on the events in Ukraine, the US State Department accused him of lying and published a “fact sheet” of Putin’s 10 “false claims” surrounding the crisis. Moscow said that it will not respond to such “low-level propaganda.” “We will only say, yet again, that we are dealing with unacceptable arrogance and a pretense of having a monopoly on the truth,” Lukashevich said in a statement posted on the Foreign Ministry’s website.

The United States has “no moral right” to lecture about observing international laws and respecting the sovereignty of other states, the diplomat added. “What about the bombing of former Yugoslavia or the invasion of Iraq over a fabricated cause?” Lukashevich pointed out. There have been quite a few examples of American military foreign interventions when there was no real threat to US security: Vietnam, Lebanon, the Dominican Republic, Grenada, Libya, and Panama.

“The Vietnam War claimed the lives of two million civilians, not to mention totally destroyed the country and polluted the environment,” the diplomat said. “On the pretext of providing security to Americans who simply happened to be in conflict zones, the US invaded Lebanon in 1958 and the Dominican Republic in 1965, attacked tiny Grenada in 1983, bombed Libya in 1986, and occupied Panama three years later.” “Still, they dare to blame Russia of ‘armed aggression’ when it stands up for its compatriots – who comprise the majority of Crimea’s population – in order to prevent ultra-nationalist forces from organizing yet another bloody Maidan.”

Apparently, Washington cannot adequately handle the development of events which are not in line with American templates, Moscow said. But this is no reason to shift the blame, the ministry concluded. The two nuclear powers have been involved in a bitter dispute over the Ukrainian crisis, with Washington giving its backing to the coup-appointed government. The US has repeatedly accused Russia of “invading” the Autonomous Republic of Crimea, ignoring the fact that an existing 1997 agreement between Russia and Ukraine allows Moscow to keep up to 25,000 Black Sea Fleet troops in the peninsula.

Following the violent uprising which resulted in the ouster of President Viktor Yanukovich,Crimean authorities denounced the coup-appointed government in Kiev and declared that all Ukrainian law enforcement and military deployed in the peninsula must take orders from them. The government of the republic – which comprises of mostly Russian speakers – asked Moscow to provide assistance to ensure peace and order in the region. Crimea is to decide in a March 16 referendum whether it wants to remain within Ukraine or join Russia.

Austerity will take on gross forms.

• Pensions in Ukraine to be halved (RT)

The self-proclaimed government in Kiev is reportedly planning to cut pensions by 50% as part of unprecedented austerity measures to save Ukraine from default. With an “empty treasury”, reduction of payments might take place in March. According to the draft document obtained by Kommersant-Ukraine, social payments will be the first to be reduced.

“The Finance Ministry has prepared a plan for optimizing budget expenditures, which implies budget sequestration is to be in force before the end of March. For this purpose, in particular, it has been proposed to reduce capital costs, eliminate tax schemes and preferences and to cut social benefits, for example, 50% of pensions to working pensioners,” Kommersant-Ukraine reported.

Ukraine’s Ministry of Social Policy reported on December 1, 2013, that an average pension in Ukraine is $160. Right after the formation, the self-proclaimed government in Kiev announced that the “treasury is empty”. Ukraine’s new prime minister, Arseny Yatsenyuk, promised the government would do its best to avoid a default, adding that he expects an EU/IMF economic stabilization package soon. The plan has been formulated in record time, with the government’s strategy ratified in the Ukrainian parliament on February 27, and the document being sent for evaluation to the Ministry of Economic Development and Trade on March 3.

The European Commission offered Ukraine an 11 billion euro loan if Kiev agrees a deal with the IMF, European Commission President Jose Barroso announced on Wednesday. As a rule, help from financial organizations such as the IMF or the World Bank normally includes drastic austerity measures. Accepting IMF money will mean many sacrifices for Ukraine’s economy, which are likely to include increased gas bills, frozen government salaries, and all around budget cuts. The government in Kiev has already announced sequestration plans from $6.8 to $8.4 billion in 2014.

Moldova’s per capita GDP at $2000 per year is just over half of Ukraine’s dismal $3800.

• Russia Tries to Woo Back Moldova (Spiegel)

Moscow is now in the process of infiltrating the last pro-European republics in its sphere of influence. Moldova is especially important to the Russians: a country, smaller than the German state of Nordrhein-Westfalia, almost entirely surrounded by Ukraine except for a border it shares with Romania. The republic, which left the Soviet Union in 1991, only has three million inhabitants.

Until 2009, the communists led the country — but now a pro-European coalition is in power. Moldova long ago agreed on the text of an Association Agreement with the EU and it is supposed to be signed in August. This makes Moldova and Georgia the only ones of the six original former Soviet republics risking rapprochement with Europe.

But will it actually happen? The Kremlin is currently expending significant effort to loosen Europe’s grasp on Moldova — and using the Gagauz to do so. The Gagauz capital, Comrat, is a sleepy town in the south Moldavian steppe where the only language spoken aside from Gagauz is Russian and people watch Moscow’s Channel One.

The rest of Moldova has also changed its attitude towards Europe — only 44% of them are still in favor of integration into the EU, while, at the same time, the number of people in favor of entering the Customs Union with Russia has grown from 30 to 40%. Formuzal claims the Moldovan government has erected an “African democracy” in the country — claiming that it has tightened its control over ministries, courts and public prosecutors’ offices and is handing out money to party members and relatives, while the Gagauz minority receives nothing.

“We want our own state,” he says. “We want the same status as the Republic of Transnistria.” That strip of land, which separated from Moldova in 1992 in a civil war, has been kept alive by Russia ever since.

As predicted, China’s first default is here. Now it’s wait and see for the next ones.

• Chaori Can’t Make Full Payment in China’s First Onshore Default

Shanghai Chaori Solar Energy Science & Technology Co. became the first company to default in China after failing to pay full interest due today on onshore bonds. The maker of energy cells to convert sunlight into power is trying to sell some of its overseas solar plants to raise money to repay the debt, Vice President Liu Tielong said in an interview today at the company’s Shanghai headquarters. The company said on March 4 it will only be able to pay 4 million yuan ($653,990) of an 89.8 million yuan coupon due today on the notes.

Chaori Solar’s failure to pay makes it the first company to default in China’s onshore bond market, according to Guotai Junan Securities Co., the nation’s second-biggest brokerage. There haven’t been any defaults in the nation’s publicly traded domestic debt market since the central bank started regulating it in 1997, according to Moody’s Investors Service.

The yield on Chaori Solar’s bonds due 2017 was at 22% before trade was halted on July 8, exchange data show. Chaori Solar sold 1 billion yuan of five-year notes in March 2012 with a variable annual coupon starting at 8.98%, according to data compiled by Bloomberg. The notes were downgraded to CCC from BBB+ by Pengyuan Credit Rating Co. in May, Nomura Holdings Inc. said in a March 5 report.

This could be China’s “Bear Stearns moment,” strategists at Bank of America Corp. said earlier this week, and may prompt investors to reassess credit risks as they did after the troubled U.S. lender was sold to JPMorgan Chase & Co. in March of 2008. Six months later, Lehman Brothers Holdings Inc. collapsed in the biggest bankruptcy in U.S. history.

“This will likely be the first of many defaults, although I don’t think it’s going to cause a cascading effect in the bond market,” said Brian Coulton, a global emerging-market strategist in London at Legal & General Investment Management, which manages some 450 billion pounds ($753 billion) globally. “Short term, we’re likely to see higher bond yields but in the long term, this will create a better market for pricing credit risk.”

The yield on five-year AA- notes rose eight basis points to 7.77% on March 5, the most in almost four months. Yields rose a further five basis points to 7.82% yesterday. Ratings of AA- or below in China are equivalent to non-investment grades globally, according to Haitong Securities Co.

According to the 2012 prospectus for Chaori Solar’s notes, China Guangfa Bank Co.’s Shanghai branch and China Citic Bank Corp.’s Suzhou branch agreed to extend 800 million yuan in loans to Chaori Solar if the company faces a temporary cash squeeze. Chaori Solar also has $100 million of insurance against trade receivables to help meet repayments, according to the sale document.

The prospectus, posted on the website of Shenyin & Wanguo Securities Co., also says investors in the notes can ask the entrusted bond manager, China Securities Co., to force Chaori Solar to make payments, and participate in any reorganization or insolvency proceedings. Chaori Solar must explain its situation in writing to the entrusted bond manager if it can’t make interest payments and if the default lasts longer than 30 days.

China Citic Bank won’t help Chaori Solar make any interest payment on its bonds because they weren’t guaranteed, the 21st Century Business Herald reported March 6 on its website, citing an unidentified person from the lender. An earlier liquidity support agreement between the bank and the company can’t be interpreted as a bond guarantee, the report said. A default would be a “wake-up call” and advance the growth of China’s bond market, Moody’s said in a report e-mailed today. It would also “signal regulators’ higher tolerance for corporate bond defaults amid financial market reforms, which is in line with the current central administration’s shift to adopt more market-oriented policies,” Moody’s said.

And it looks like there will be lots of next ones.

• Zombies Spreading Shows Chaori Default Just The Start (Bloomberg)

The number of Chinese companies with debt double equity has surged since the global financial crisis, suggesting the first onshore bond default won’t be the last.

Publicly traded non-financial companies with debt-to-equity ratios exceeding 200% have jumped 57% to 256 from 163 in 2007, according to data compiled by Bloomberg on 4,111 corporates. The yield on five-year AA- notes leapt 13 basis points in two days to 7.82% on March 6, the most in almost four months, after Shanghai Chaori Solar Energy Science & Technology Co. said it won’t be able to fully pay an 89.8 million yuan ($14.7 million) coupon due today on its March 2017 bonds. Chaori Vice President Liu Tielong said in an interview today the company still can’t make the payment.Some “zombie” companies in China that have cash shortages will fail as authorities end an overly loose monetary policy, Xia Bin, an adviser to the State Council and former central bank board member, said on Feb. 10. Chaori may become China’s “Bear Stearns moment,” prompting investors to reassess credit risks as they did after the U.S. securities firm was rescued in 2008, according to Bank of America Corp.

“After the first one, there may be more defaults,” said Zhang Yingjie, Beijing-based deputy general manager in the research department of China Chengxin International Credit Rating Co., Moody’s Investors Service’s joint venture in China. “The domestic economy is slowing, liquidity is tightening globally and more bonds are maturing this year with greater refinancing pressure, so there may be more defaults.”

Total debt of publicly traded non-financial companies in China and Hong Kong has surged to $1.98 trillion from $607 billion at the end of 2007. Some 63 companies have a debt-to-equity ratio exceeding 400%, compared to the average of 73%. In latest filings, 351 have negative ratios of earnings before interest, taxes, depreciation and amortization to interest expenses, while 409 have coverage of less than 1. Renewable energy, materials, household appliances and software companies dominate the rankings.

Premier Li Keqiang is trying to balance efforts to avoid sharper slowdowns in economic growth with steps to rein in debt. Expansion in gross domestic product is set to cool to a more than two-decade low of 7.5% this year from 7.7% in 2013, according to the median estimate in a Bloomberg survey.

Li told the National People’s Congress this week that China will develop a regulated regional borrowing mechanism, after local-government liabilities surged to 17.9 trillion yuan as of June 2013 from 10.7 trillion yuan at the end of 2010. Authorities have also started a cleanup of the $6 trillion shadow-banking industry and identified sectors of the economy in need of consolidation, including property. Default risks for trust products are under control, the official Xinhua News Agency reported today, citing central bank adviser Chen Yulu.

The government is signaling greater willingness to let borrowers be subjected to market discipline, according to Christopher Lee, head of corporate ratings for Greater China at Standard & Poor’s. “We expect more discrimination in terms of credit risk and more selective lending,” Hong Kong-based Lee said by phone yesterday. The Chinese government will allow any further defaults “in a selective and controlled basis as opposed to the Big Bang approach, which is not their style,” he added.

The BOE has a lot of explaining to do, as do the banks involved. Will this too be under the carpet soon?

• Two Senior City Traders Suspended In Forex Scandal (Telegraph)

The scandal surrounding alleged foreign exchange manipulation that has rocked the City intensified on Thursday after it emerged that two senior London-based dealers had been suspended as part of an investigation into the £3 trillion-a-day market. Robert de Groot, global head of spot trading at BNP Paribas, and Joe Landes, Bank of America Merrill Lynch’s head of spot trading for Europe, Middle East and Africa (EMEA), have been put on leave, according to reports.

The developments come a day after the Bank of England said it had suspended a member of staff over breaches of its “internal control processes”. Bank of England minutes released this week showed Mr de Groot attended several meetings held between Bank staff and leading foreign exchange dealers between 2005 and 2013. Minutes of one meeting held in May 2008 which Mr de Groot hosted while at Citibank showed there was “considerable discussion” on “issues around market fixings” linked to a foreign exchange benchmark.

Mr Landes relocated from New York to London in 2011 to become head of BoAML’s EMEA spot desk, and has been put on leave as the bank investigates allegations of currency manipulation, according to Reuters. The Wall Street Journal cited sources saying Mr de Groot had been suspended. No charges have been brought against either men.

Both US and UK regulators are investigating attempts by traders to manipulate foreign exchange markets. The investigations centre around how traders discussed their handling of deals before the crucial daily setting of a benchmark – known as WM – at 4pm each day. Mark Carney, the Governor of the Bank of England, will be quizzed by MPs next week about the central bank’s alleged involvement in the manipulation of the foreign exchange market.

• Bank Of England Was Warned Of Forex Fixing Problems As Early As 2006 (Independent)

The Governor of the Bank of England is set to face tough questioning from the Treasury Select Committee next week after it emerged last night that senior officials were warned about manipulation of the $6.3trn (£3.8trn) a day foreign exchange market as long ago as 2006. Details emerged as the Bank yesterday suspended an unnamed member of staff in connection with its inquiries into the affair and asked an oversight committee of the Court of Directors to investigate officials’ roles and behaviour.

It also released the minutes of a series of meetings between its market experts and traders at upmarket City restaurants such as Smiths that reveal concerns about “attempts to move the market around popular fixing times” – when reference exchange rates are determined. This, they note, was causing “fixing business” to “becoming increasingly fraught”.

The chair of the Treasury Select Committee, Andrew Tyrie, last night criticised the Bank of England for its tardy response to explosive claims that it knew about manipulation of the market. “There is a strong case that the non-executives in the Bank should have taken the initiative on this from the moment the need for external assistance was considered,” said Mr Tyrie. “Yet this issue does not appear to have been raised with Court or the Oversight Committee – the nearest the Bank has to a board – until December. Indeed, it appears to have taken the suspension of a Bank employee for the Oversight Committee to be fully engaged.”

The Governor, Mark Carney, and other senior officials including the Bank’s director of markets, Paul Fisher, will face questions on the subject before the committee next week. The suspension of one of the Bank’s own employees is likely to feed suspicions that within the central bank there was, at least, concerns over the integrity of the foreign exchange market. Last December the Bank ordered an internal review into allegations that its officials “condoned or were informed of manipulation in the foreign exchange market or the sharing of confidential client information”.

Traders have alleged that the Bank was told they regularly exchanged information on the size of their clients’ orders before fixing exchange rates. They say they were told by Bank officials that there was nothing inappropriate in doing this. As well as involving the Court of Directors, the Bank has commissioned the law firm Travers Smith to prepare a report which will be made public.

The Bank stressed that it has not taken any decision to discipline any member of staff, and emphasised that it is working closely with the Financial Conduct Authority. “This extensive review of documents, emails and other records has to date found no evidence that Bank of England staff colluded in any way in manipulating the foreign exchange market or in sharing confidential client information,” it said. It added that it had already examined 15,000 emails, 21,000 Bloomberg and Reuters chat-room records and more than 40 hours of telephone recordings.

Stock shocks. Name for a band?

• City Heavyweights Warn Of Stock Shocks Ahead (Independent)

Two veterans of the stock market reported record results today but both warned investors to stand by for shocks. Lord Rothschild, whose RIT Capital Partners looks after £2.1 billion of his family’s and other long-term investors’ money, said: “With the world recovery still fragile and reliant to a large extent on policy support, it is not hard to envisage markets having to deal with shocks in the coming year.”

Michael Dobson, chief executive of Schroders, which manages £263 billion for institutional and retail investors, said he expects equities to return between 6% and 8% this year after a stonking run last year. “We don’t expect as strong an equity market as in 2013. There is still macro uncertainty around Ukraine, Syria, China and Japan and the continued [reining in] of quantitative easing. But equities remain our preferred asset class and there are even signs that emerging markets may have been sold off too much.”

Schroders reported a 41% profit rise to £508 million, reflecting its takeover of Cazenove Capital and a US fixed-income fund manager last year, as well as a big leap in performance fees. These hit £80 million, with 68% of its funds outperforming their benchmarks or rivals. Assets under management increased by just over £50 billion, with net inflows of £9.4 billion coming almost equally from institutions and intermediaries. The dividend for the year has been hiked by 35% to 58p a share, which was well above analysts’ forecasts. The shares jumped by 150p, or 6%, to an all-time high of 2740p.

Shares in RIT Capital Partners also rose sharply, gaining 17p to 1305p. The investment fund’s net asset value rose 193p a share to 1384p last year and produced a return of 18.6%. Rothschild said: “As market conditions have become more volatile, I am increasingly satisfied with the progress which your company made … Our 2013 performance combined appropriate levels of caution with a significant participation in stock market increases. We did not forsake our focus on long-term growth and for this our shareholders have rewarded us with their loyalty.”

He said that last year the fund had moved into US and Japanese equities, which turned out to be two of the strongest-performing markets. It also traded out and in of sterling successfully as the pound weakened then strengthened last year. The only poor area of performance was its exposure to gold and goldminers.

Pre-cooked, and no sharp edges.

• European Banks Stressed by Approaching Stress Tests (Spiegel)

In Spain, the number of real-estate loans in default is growing as the crisis continues. In Italy, corporate loans are suffering the same fate amid economic doldrums. Even worse, the balance sheets of many Italian banks are loaded with Italian sovereign bonds, a situation which makes them vulnerable should the debt crisis flare up again.

German banks, on the other hand, are struggling with billions of loans to the shipping industry. With commercial shipping in its sixth year of crisis, large numbers of defaults are looming. One former high-ranking bank manager who focused on shipping says that banks should already have written off up to a third of the money they have tied up in the industry. But Nord/LB, to take one example, has only cleared 10% of its holdings from its balance sheet. Commerzbank has refused to say how much of its €14 billion shipping portfolio it has written off.

Even Deutsche Bank, Germany’s biggest financial institution, could have trouble passing the stress test, say KBW analysts. The Frankfurt-based bank has a particularly large number of complex securities whose prices are determined by modeling. The ECB intends to take a closer look at the practice.

Yet the regulators may run into trouble. Not only does Deutsche Bank have some €40 billion worth of such securities on their books, but they use several thousand different models to calculate their value. It is “illusory to think you can look at all of them,” one supervisor admits. It will likely only be possible to analyze a few such models at random. Time, after all, is short. The ECB has committed to completing the balance sheet checks in the next three months. The second phase — that of determining how much capital each bank will need to withstand specific crisis scenarios — is to begin in May.

Further complicating the effort is the fact that, while the first phase may already have begun, Nouy is still establishing her team. Of the 1,000 employees that she will eventually have, only a few hundred have started work, and many of those are only on loan from national oversight agencies. Four new directors general were named as recently as January. “They first have to figure out how their printers work,” one banker complained.

The ECB has thus delegated much of the evaluation to auditors hired by national institutions. They have only recently begun their work — a situation akin to a team of paramedics beginning open-heart procedure before the doctors arrived. And the banks affected have had little time to prepare. “We still don’t have a schedule for the test, no documentation,” said one bank employee shortly before the auditors arrived.

Nevertheless, the ECB’s aims are ambitious. Auditors have identified 15 risky credit portfolios at each bank for evaluation. Thousands of loans and securities at each institution are to be examined, a number of checks that is four to five times greater than for average year-end statements. Everything is to be questioned: whether the risks have been adequately calculated, what collateral has been established, their most recent appraised value. “The effort is enormous,” says one banker.

Even the Telegraph gets nervous.

• UK House Price Growth ‘Approaching Madness’ (Telegraph)

The speed UK property prices are rising at is “approaching madness”, analysts have warned, after data showed house prices jumped 2.4% in February, the biggest monthly increase in five years. The rise, revealed in the latest Halifax House Price Index, outstripped analysts’ expectations of a 0.7% rise, renewing fears of a house price bubble. House prices advanced 7.9% on an year-on-year basis, the figures showed, taking the average price across the UK to £179,872 and marking the strongest annual uplift since October 2007.

Oliver Atkinson, director at urbansalesandlettings.co.uk, said in parts of Britain “the momentum is approaching madness, as price rises continue to accelerate”. Stephen Noakes, mortgages director for Halifax, said the improving economy, falling unemployment, growing consumer confidence and low interest rates are all boosting the market.

The surprisingly strong data led to renewed calls for Government to cool policies it put in place to support the housing market. “Cuts to the Help to Buy scheme would send a stronger message that the authorities are willing to take action to cool an overheating market,” said Matthew Pointon, property economist at Capital Economics. Average house values remain 10% below their 2007 peak and Mr Noakes said factors such as wage rises failing to keep up with inflation are expected to “constrain” property prices.

Oh man, this is not going to stop.

• Pay rises while profits slide at the City’s banking giants (Independent)

Banks headed into another storm of controversy over wages last night as it emerged that Standard Chartered had quietly increased its total pay pot despite a sharp slide in profits, while Barclays, whose profits also fell, admitted 481 employees earned more than £1m last year. Eight of the Barclays executives earned more than £5m.

Lloyds and Barclays, meanwhile, said they were paying their chief executives almost £1m each in shares in 2014 to compensate them for the EU-imposed bonus cap. The two banks also onfirmed they would be seeking shareholder approval to pay bonuses of two-times salary.

Total staff pay at Standard Chartered rose in 2013, despite an 11% slide in profits, an analysis of the bank’s accounts by The Independent has revealed. The Asia-focused bank confirmed yesterday that its profits declined last year for the first time in a decade, slipping to $6bn (£3.75bn), down from $6.9bn in 2012, after suffering heavy write-downs in its South Korean operations. Stressing that pay is linked to performance, Standard Chartered chief executive Peter Sands said the bonus pool for staff would be slashed 15% to $1.21bn to reflect the “tough” year. Mr Sands’ own bonus would be cut by 21% to $2.5m (£1.6m).

But staff pay across the bank actually increased by 2.1% on 2012, casting doubt on the claim that pay is tracking performance. Wages and salaries including bonuses rose from $4.87bn to $4.9bn. The number of bank staff in 2013 rose to 88,257, up from 87,569 in 2012. This implies average pay per employee rose from $55,693 to $56,449. Aggregate “salaries, allowances and benefits in kind” of senior directors rose to $25m (up from $21m in 2012). This offset a $3m fall in bonuses (which came down from $10m in 2012 to $7m).

A spokesman said inflation in the Far East, where Standard Chartered employs many of its workers, pushed up the overall pay bill and stressed bonus figures included in the report also included previous years’ awards that vested in 2013. Standard Chartered intends to follow HSBC with a share-based allowance scheme to boost fixed pay of top employees despite the EU’s incoming cap limiting bonuses to 200% of salary. Mr Sands said this was necessary to retain talent and stop losing staff to rival banks.

By unveiling a cut in bonuses yesterday, Standard Chartered had hoped to distinguish itself from Barclays, which has come under intense criticism for increasing the bonus pot of its investment bankers for 2013 by 13%, despite a 37% fall in the unit’s profits. Barclays’ annual report yesterday also showed that chief executive Antony Jenkins was awarded £4.4m worth of shares as part of his “2013-15 long-term incentive plan” last March.

Nice starting point, but I’m not sure about the conclusions.

• Not even climate change will kill off capitalism (Guardian)

Arguably the single most important mistake the revolutionary movements of the 60s and 70s made was to overlook the resilience of capitalism. The idea – catastrophism, as it is often called – that the system was going to crumble under the pressure of its own contradictions, that the bourgeoisie produces its own “gravediggers” (as Marx and Engels put it in the Communist Manifesto) has been disproved. When the rate of profit started showing signs of decline in the first half of the 70s, the redistributive policies implemented after the second world war were terminated and the neoliberal revolution was launched.

This resilience of capitalism has little to do with the dominant classes being particularly clever or far-sighted. In fact, they can keep on making mistakes – yet capitalism still thrives. Why?

Capitalism has created a world of great complexity since its birth. Yet at its core, it is based on a set of simple mechanisms that can easily adapt to adversity. This is a kind of “generative grammar” in Noam Chomsky’s sense: a finite set of rules can generate an infinity of outcomes. The context today is very different from that of the 60s and 70s. The global left, however, is in danger of committing the same error of underestimating capitalism all over again. Catastrophism, this time, takes the form of investing faith in a new object: climate change, and more generally the ecological crisis.

There is a worryingly widespread belief in leftwing circles that capitalism will not survive the environmental crisis. The system, so the story goes, has reached its absolute limits: without natural resources – oil among them – it can’t function, and these resources are fast depleting; the growing number of ecological disasters will increase the cost of maintaining infrastructures to unsustainable levels; and the impact of a changing climate on food prices will induce riots that will make societies ungovernable.

The beauty of catastrophism, today as in the past, is that if the system is to crumble under the weight of its own contradictions, the weakness of the left ceases to be a problem. The end of capitalism takes the form of suicide rather than murder. So the absence of a murderer – that is, an organised revolutionary movement – doesn’t really matter any more.

But the left would be better off learning from its past mistakes. Capitalism might well be capable not only of adapting to climate change but of profiting from it. One hears that the capitalist system is confronted with a double crisis: an economic one that started in 2008, and an ecological one, rendering the situation doubly perilous. But one crisis can sometimes serve to solve another.

Capitalism is responding to the challenge of the ecological crisis with two of its favourite weapons: financialisation and militarisation. In times of crisis, for instance, markets will require simultaneously that wages be cut and that people keep consuming. Opening the flow of credit allows the reconciliation of these two contradictory injunctions – at least until the next financial crisis.

As Costas Lapavitsas has recently shown, finance has penetrated every nook and cranny of our everyday lives: housing, health, education, even nature. Carbon markets, weather or biodiversity derivatives, catastrophe bonds, among others, belong to a new variety of “environmental finance” products. Each one has its own specific way of functioning, but their overall purpose is to alleviate or spread the rising costs of climate change and the super-exploitation of the environment.

For instance, catastrophe bonds – or “cat bonds” – are not linked to future investment, as traditional government or private bonds are, but to the possible occurrence of a catastrophe, say, an earthquake in Japan, or the continuing floods in the UK, whose cost to the insurance industry is estimated at about £3bn. A government issues a “cat bond” to gather funds. In return, it pays an attractive interest rate to the investors. If a catastrophe occurs, the government keeps the money to rebuild infrastructures or compensate victims. If it doesn’t, the investors eventually get their money back (and they keep the interest).

With the growing number of natural disasters due to climate change, the sums spent by governments on catastrophe management have risen to unprecedented levels. In some regions, this has put public budgets in jeopardy. The financialisation of catastrophe insurance is supposed to keep budgets balanced. It remains to be seen if this is a sustainable response to the threat. But, from the point of view of the system, it may well be.

With financialisation comes the second capitalist response to the ecological crisis: militarisation. Since the second half of the last decade, all major armies of the world have published detailed reports on the military consequences of climate change. Among the different sectors of the ruling classes, the military is the one that takes the environmental crisis most seriously – the environment is a crucial parameter in war-making. Clausewitz’s On War, the greatest military treatise ever written, explains the importance of the “terrain”. So whether and to what extent environmental parameters start changing matters greatly to the military.

A report published in the US in 2007, titled National Security and the Threat of Climate Change – created by, among others, 11 three- and four-star admirals and generals – defines climate change as a “threat multiplier” that will intensify existing menaces. For instance, by further weakening “failed states” it will make it easier for terrorists to find refuge on their territory. Or by provoking climate migration, it will destabilise the regions where the migrants arrive and exacerbate ethnic conflicts. The US army, the report concludes, should adapt its tactics and equipment to a changing environment.

Like financialisation, militarisation is about reducing risk and creating a physical and social environment favourable to capitalist accumulation. They are a kind of “antibody” that the system secretes when a menace looms. This doesn’t necessarily take the form of shocks of the sort described by Naomi Klein in her book The Shock Doctrine: it is a more gradual process that slowly takes hold of every aspect of social life.

Nothing in the system’s logic will make it go away. A world of environmental desolation and conflict will work for capitalism, as long as the conditions for investment and profit are guaranteed. And, for this, good old finance and the military are ready to serve. Building a revolutionary movement that will put a stop to this insane logic is therefore not optional. Because, if the system can survive, it doesn’t mean that lives worth living will.

Berman’s an old school oil man and skeptic. Good read.

• Art Berman: Shale Is Not A Revolution, It’s A Retirement Party (Oilprice.com)

On the gas side, all shale gas plays except the Marcellus are in decline or flat. The growth of US supply rests solely on the Marcellus and it is unlikely that its growth can continue at present rates. On the oil side, the Bakken has a considerable commercial area that is perhaps only one-third developed so we see Bakken production continuing for several years before peaking. The Eagle Ford also has significant commercial area but is showing signs that production may be flattening. Nevertheless, we see 5 or so more years of continuing Eagle Ford production activity before peaking. The EIA has is about right for the liquids plays–slower increases until later in the decade, and then decline.

The idea that Texas shales will produce one-third of global oil supply is preposterous. The Eagle Ford and the Bakken comprise 80% of all the US liquids growth. The Permian basin has notable oil reserves left but mostly from very small accumulations and low-rate wells. EOG CEO Bill Thomas said the same thing about 10 days ago on EOG’s earnings call. There have been some truly outrageous claims made by some executives about the Permian basin in recent months that I suspect have their general counsels looking for a defibrillator.

Recently, the CEO of a major oil company told The Houston Chronicle that the shale revolution is only in the “first inning of a nine-inning game”. I guess he must have lost track of the score while waiting in line for hot dogs because production growth in U.S. shale gas plays excluding the Marcellus is approaching zero; growth in the Bakken and Eagle Ford has fallen from 33% in mid-2011 to 7% in late 2013.

Oil companies have to make a big deal about shale plays because that is all that is left in the world. Let’s face it: these are truly awful reservoir rocks and that is why we waited until all more attractive opportunities were exhausted before developing them. It is completely unreasonable to expect better performance from bad reservoirs than from better reservoirs.

The majors have shown that they cannot replace reserves. They talk about return on capital employed (ROCE) these days instead of reserve replacement and production growth because there is nothing to talk about there. Shale plays are part of the ROCE story – shale wells can be drilled and brought on production fairly quickly and this masks or smoothes out the non-productive capital languishing in big projects around the world like Kashagan and Gorgon, which are going sideways whilst eating up billions of dollars.

This article addresses just one of the many issues discussed in Nicole Foss’ new video presentation, Facing the Future, co-presented with Laurence Boomert and available from the Automatic Earth Store. Get your copy now, be much better prepared for 2014, and support The Automatic Earth in the process!

Home › Forums › Debt Rattle Mar 7 2014: The US Economy’s Volatile Inertia