Dorothea Lange Migrant camp farm worker figuring year’s earnings, Marysville, CA October 1935

Well, stocks are down substantially over the past few days, with internet and biotech taking big hits, and we see people like Marc Faber and Dennis Gartman urging people to get out of stocks. Something’s definitely going on. Time for a bunch of charts. And let’s start with a few of the comparison ones that everybody loves to hate, where you overlay when time period on another, and suggest similarities between both periods. This first one was used by Tyler Durden as an illustration for Marc Faber’s latest doom message. By the way, Faber says the markets are figuring out that the Fed is clueless, and I’m not so sure about that, I think it’s more likely that the Fed is not trying to do what it says it is, and that what it does try it does very well. And if that includes a stock market bust, it won’t hesitate. But so, here’s 1987 and 2014:

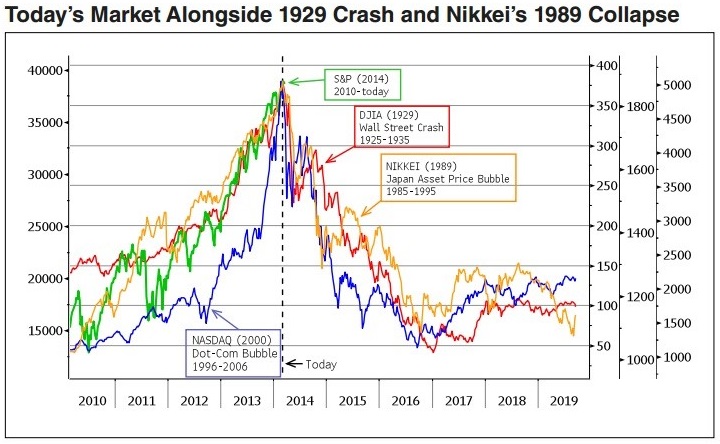

Personally, I’m kind of partial to this one, which “compares” the crashes of 1929 and 1989 to today, and I apologize for forgetting where I found it:

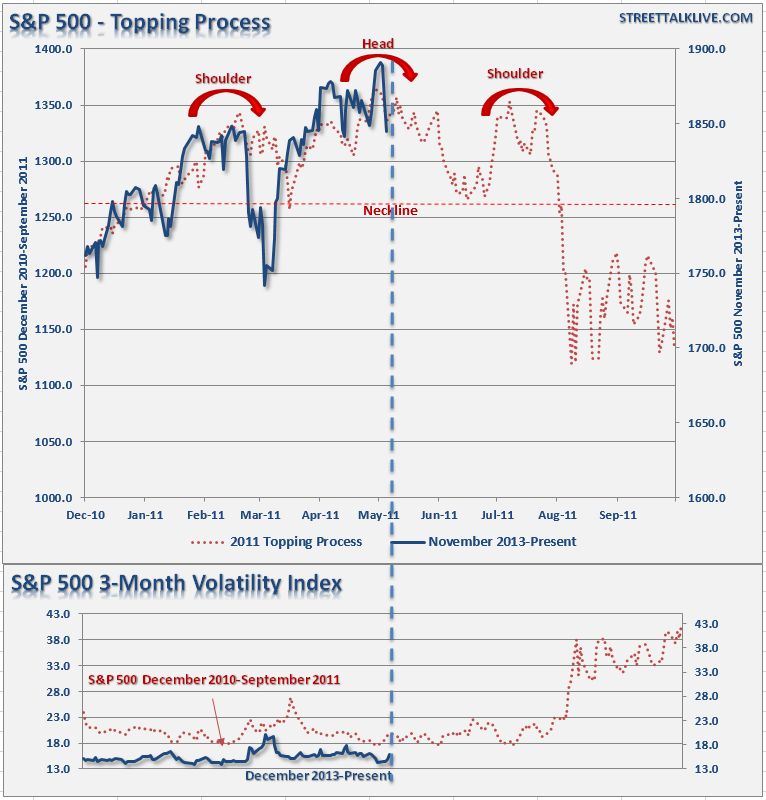

This one from Lance Roberts is not bad at all. Head and shoulders patterns can be very tempting:

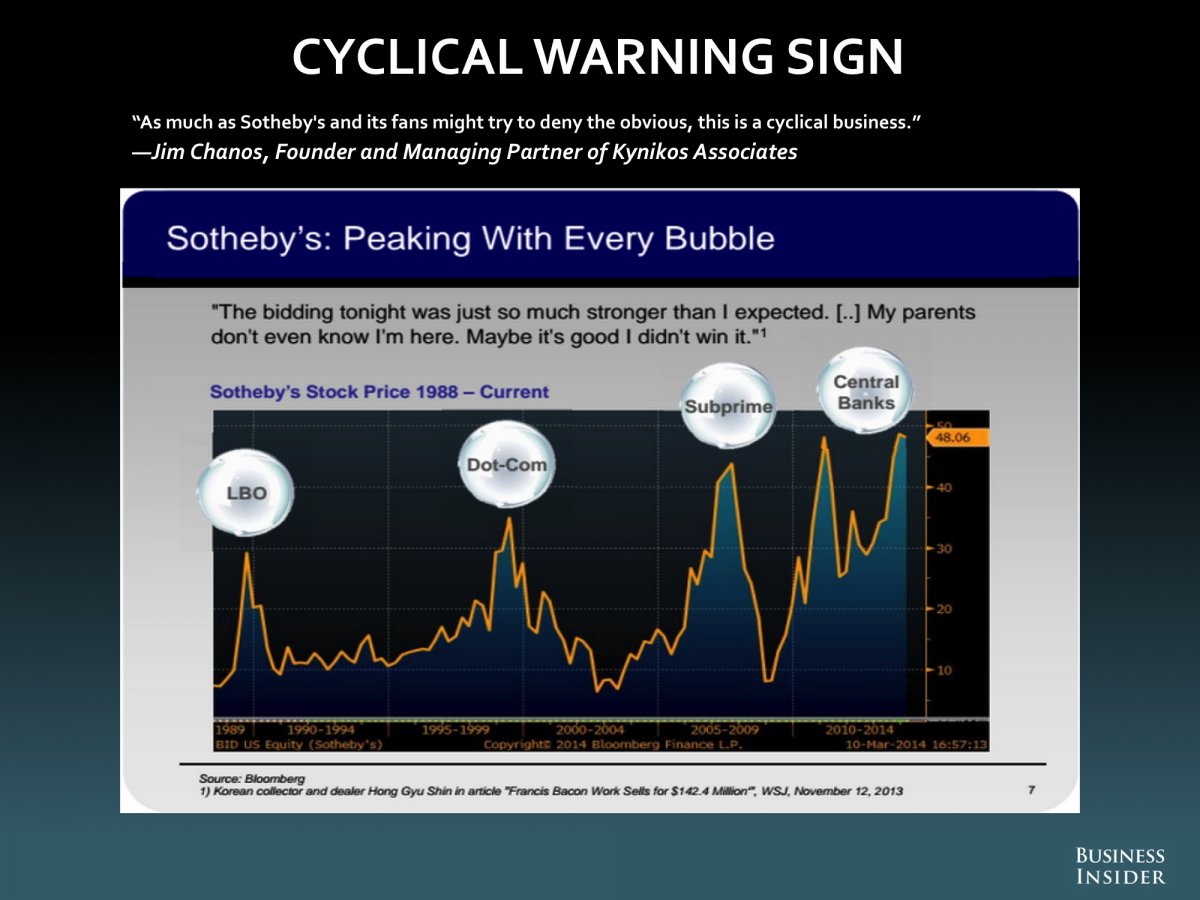

And I do like the suggested link between Sotheby’s stock price and market crashes Jim Chanos put in this graph that BI published:

But I would certainly want to include another Lance Roberts graph. Because unlike the comparison charts, in which perceived similarities can always be contested, as long as they aim to predict events, it’s a whole lot harder to ignore. Margin debt is at a huge high, net credit at the polar opposite, and that should be reason to think.

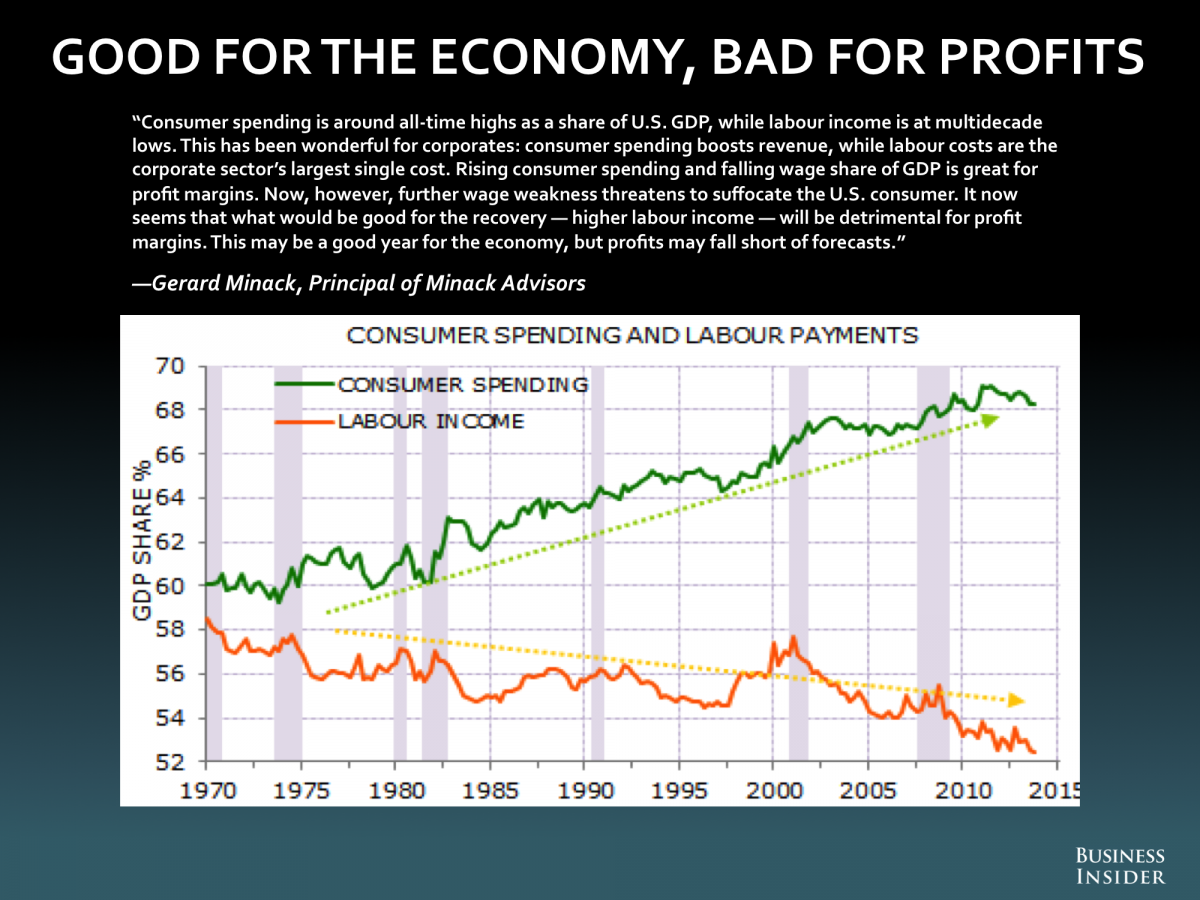

The next one from Gerard Minack, also published by BI, is interesting in that it shows the divergence through the past 40 years of consumer spending and labor income, which leads Minack to wax on what this means for corporates. But all I’m thinking is: if income as a percentage of GDP goes down, and spending as a percentage of GDP goes up, where does the money to increase spending come from? How is this not a picture of how much debt Americans have accumulated? And how inequality has risen at the same time …

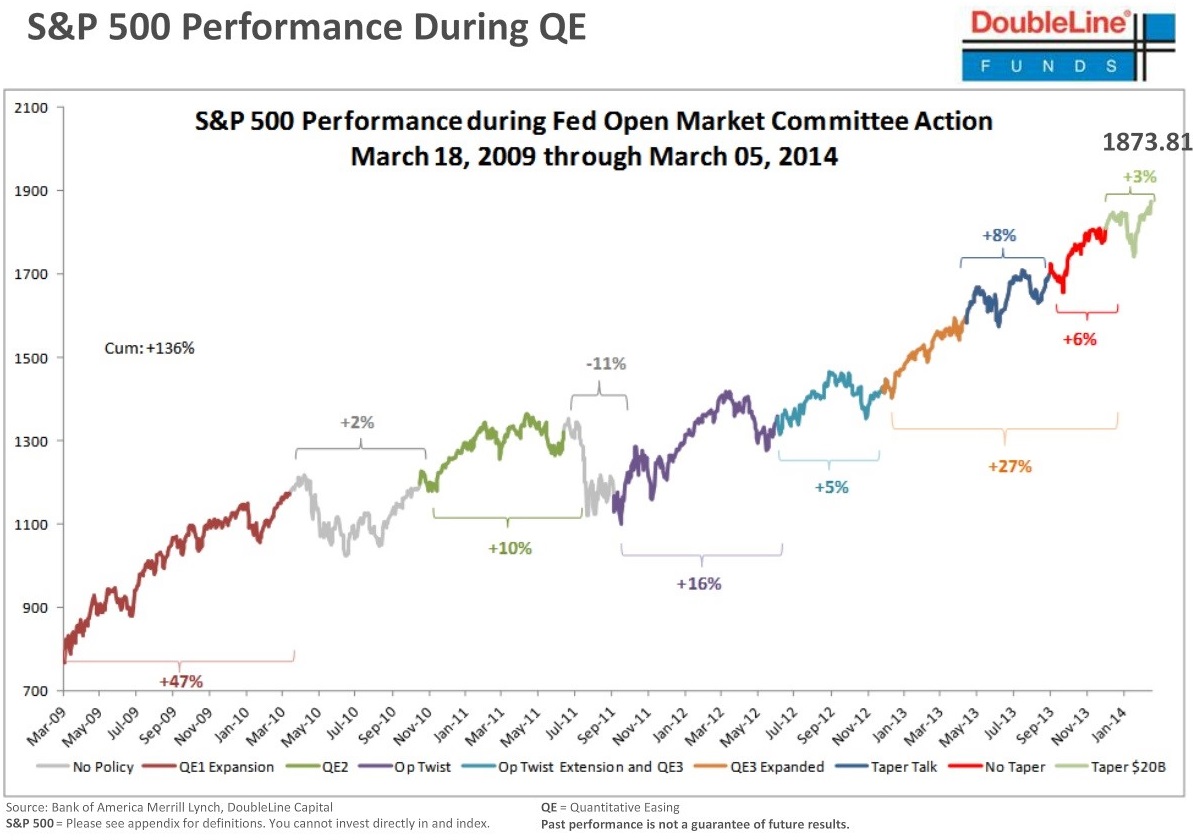

Still, if you want to say anything about where stock markets may go, you can’t get around the fact that we have no functioning markets anymore. And this graph from Double Line depicts in fine detail why that is, and how it has come about.

We need to realize that if you don’t have functioning markets, it’s very hard to predict anything at all about where they will go. I don’t think there’s anyone left who would seek to deny that the only thing that has kept up asset values, and even pushed them up, is central bank stimulus, i.e. money from everyone that is handed to the few. And even that would normally have to stop somewhere sometime, but since debt levels among the people in the street are already so high, stimulus doesn’t come from the people themselves, but from their children and grandchildren.

This may not be true if we attain some sort of mythical escape velocity growth in our economies, but that’s at the very least a huge gamble to take. If we don’t reach it, there’ll be almost literally hell to pay down the line. But perhaps it should be obvious by now that growth, or a better life, for everyone is not what the Fed or Capitol Hill, or their peers in other nations, are aiming for. They are engineering ways to guarantee more wealth for the already wealthy. That’s why banks are declared too big to fail. And why QE is handed to these banks, not the public. Is the Fed really that clueless if that is what they look to achieve? Or is everything moving according to their plan?

We know this whole thing will come down like a outback shack in a tornado, but in a market that exists only because of government and central bank largesse, the timing is hard to call. The ECB looks to be ramping up to buy trillions of euros in sovereign bonds, Germany is giving off signals that it might go along with it. And that could keep the fake markets train going for a while longer. There’s a window, though: Draghi can’t do it before the May 25 European elections. So we have another 6 weeks or so to do some truth finding. Then again, I wouldn’t be surprised if the boys and girls who run this Kabuki mirage pull the plug on the while thing any day now. At this point, every greater fool must be reinvested, and there have to be doubts about how much more they can be milked for. The lords of the dance can’t afford to get out too late, so, greedy as they are, they won’t wait for the last moment. All they have to do now is to make sure mom and pop will be left holding the empty bag.

• US Tech Sell-Off Sends Global Stock Markets Lower (AP)

Global stock markets were lower Friday as investors marked down technology stocks and a drop in U.S. jobless claims failed to boost investor confidence. European markets opened weaker, with Britain’s FTSE 100 losing 1% to 6,575.83. Germany’s DAX fell 1.2% to 9,338.48 and France’s CAC-40 shed 1% to 4,369.26. Wall Street looked set for lackluster trading. Dow and S&P 500 futures were both little changed. The falls in Europe were foreshadowed by a weak performance in Asian markets. Investors knocked down Internet and technology companies after the tech-heavy Nasdaq Composite had its worst day since 2011.

The jitters over the high valuations of technology companies in the U.S. and then in Asia overshadowed other upbeat economic reports. The Labor Department said Thursday that the number of people seeking U.S. unemployment benefits dropped to the lowest level in almost seven years, suggesting improvement in the U.S. labor market. Next week’s first quarter economic growth data from China will be the key indicator investors are looking for as it could give hints about further stimulus announcements from Beijing, said Ric Spooner, chief market analyst at CMC Markets in a commentary.

• JPMorgan Profit Falls 19% on Trading, Mortgage Declines (Bloomberg)

JPMorgan Chase, the biggest U.S. bank, said first-quarter profit fell 19% on lower fixed-income trading and mortgage revenue, themes that may be repeated across Wall Street next week. Net income declined to $5.27 billion, or $1.28 a share, from $6.53 billion, or $1.59, a year earlier, according to a statement today from New York-based JPMorgan. JPMorgan, the first of the top U.S. banks to post results for the period, told investors in late February that trading revenue had fallen 15% since the start of the year. Chief Executive Officer Jamie Dimon, 58, said at the time that he was “completely comfortable” with the drop, which analysts including David Konrad of Macquarie Group Ltd. blamed on a reduction in the Federal Reserve’s bond purchases.

“It’s been a tough quarter for the industry,” said Pri de Silva, senior banking analyst at CreditSights Inc. in New York. “I’m not overly worried about JPMorgan unless I see something else going on apart from what we already know is lower fixed-income trading and mortgage results.” Citigroup Inc. reports earnings on Monday, followed by Bank of America Corp. April 16. Goldman Sachs Group Inc. and Morgan Stanley announce results on April 17. Konrad said in an April 4 research note that banks will have a “challenging quarter” as higher interest rates reduce loan refinancings.

JPMorgan’s investment-banking head, Daniel Pinto, said this week he was overhauling the division’s reporting lines after his former co-head, Mike Cavanagh, left to join Carlyle Group LP. Pinto named Carlos Hernandez co-head of global banking with Jeff Urwin, John Horner head of investor services and Joyce Chang global head of research. Another top executive, Blythe Masters, plans to depart. Masters, 45, will resign after she helps the bank complete the $3.5 billion sale of a commodities unit to Mercuria Energy Group Ltd., the company said last week. Over 27 years she rose from being a JPMorgan intern to running several credit desks and finally heading the commodities business.

I think it’s more likely that the Fed is not trying to do what it says it is, and what it does try it does very well.

• Marc Faber: “The Market Is Waking Up To How Clueless The Fed Is” (Zero Hedge)

“I think it’s very likely that we’re seeing, in the next 12 months, an ’87-type of crash,” warns a somewhat excited sounding Marc Faber, adding that he thinks “it will be worse.”

The pain is just getting started as Faber notes that “the market is slowly waking up to the fact that the Federal Reserve is a clueless organization.” Internet and Biotech sectors (growth stocks) are “highly vulnerable because they’re in cuckoo land in terms of valuations,” and fully expects the selling to spread as The Fed “have no idea what they’re doing. And so the confidence level of investors is diminishing,” and that means we will see a major decline.

Yes, but the herd will still do what a herd does best.

• UK Housing Hysteria Can Only End In A Painful National Hangover (Guardian)

Hallelujah! It’s no longer just young Londoners without ready access to the Bank of Mum and Dad who are being priced out of the housing market. According to Royal Institution of Chartered Surveyors (Rics) figures this morning, house price madness is spreading throughout the country. Its forecast for house price growth across Britain has been nudged up two points to 8%, and the average British house price has jumped to £254,000 from £194,000 five years ago. It is the capital, of course, where estate agents are most gripped by this fever: some London boroughs have reported annual house price increases of 30%. No wonder the growing army of estate agents represents such a large chunk of Britain’s rising employment figures.

All too many people know that George Osborne has fallen back on previous unsustainable models of economic growth to stoke what commentators call a pre-election “feelgood factor”. The mismatch between stagnating wages and surging house prices is self-evident. House building has collapsed to 1920s levels: last year, there were 122,590 house building starts, about half the level that would meet housing need. But this is too often whispered privately, because the sorts of young people who suffer the most are not editing national newspapers. Political leaders are gripped by euphoria. “Why are people flocking to Barnet and why are house prices going up?” Tom Davey, Tory-run Barnet council’s lead member for housing, boasted recently. “It’s because people want to live here.” When it was suggested that these were the ones who can afford it, his retort was revealing: “And they’re the people we want!”

When this madness ends – and leaves an inevitably painful national hangover – is a guessing game. But something is going to have to give, because it is socially – never mind economically – unsustainable. Thirty years ago, a first-time buyer needed 12% of their income for a deposit, but it is now up to more than 80%. Those snapping up properties tend to come from homes affluent enough to support them: indeed, two-thirds of first-time buyers now have to rely on their parents. According to HSBC research, 57% of Britons aged between 25 and 36 do not own a home, and a quarter of those never expect to.

25 months of falling producer prices. That’s quite an achievement.

• China Slowdown Concerns Reinforced By Falling Prices (FT)

Falling prices in China have reinforced fears of the slowdown in the world’s second-largest economy, highlighting sluggish consumer demand and the struggles of over-extended factories. Consumer prices fell 0.5% in March from the previous month, while producer prices remained mired in deflationary territory for a 25th-consecutive month, according to figures published by the national bureau of statistics on Friday. Coming on the heels of weak trade figures, slower credit issuance and big declines in property sales, the price data reinforces the picture of a disappointing first quarter for the world’s second-largest economy.

Analysts have rushed to downgrade their forecasts for Chinese growth and now predict that the economy will expand 7.4% this year, its softest in more than two decades. The downturn has fuelled expectations that the government will prop up growth, but Li Keqiang, the premier, on Thursday rebuffed calls for a stimulus. “We have the capabilities and the confidence to keep the economy functioning within a proper range,” he said. But some analysts argue that the absence of inflationary pressure is a warning sign about China’s deteriorating growth prospects.

Where is the money going to come from for more overbuilding?

• China Property Trust Sales Drop 49% (Bloomberg)

Chinese developers raised 49% less through trusts in the first quarter as the collapse of Zhejiang Xingrun Real Estate Co. highlighted default risks. Issuance of property-related trusts, which target wealthy investors, slid to 50.7 billion yuan ($8.16 billion) from 99.7 billion yuan in the fourth quarter, data compiled by Use Trust show. The yield on AA rated five-year bonds has climbed 175 basis points in the past year to 7.23%, according to Chinabond. That compares with 2.74% on corporate securities globally, Bank of America Merrill Lynch indexes show.

“The banking system and the shadow banking system are becoming concerned about exposure,” David Cui, China strategist at Bank of America said in an interview yesterday. “Once people refuse to provide credit to developers, their balance sheets will be under pressure, forcing them to cut prices. Once enough of them cut prices, fewer people would buy because most people buy property only when they think the price is going up. If this persists, it will turn into a vicious loop.”

Credit is drying up in all sectors.

• China Importers Default On US, Brazil Soy Cargoes (Reuters)

Chinese importers have defaulted on at least 500,000 tons of U.S. and Brazilian soybean cargoes worth around $300 million, the biggest in a decade, as buyers struggle to get credit amid losses in processing beans. Three companies in the eastern province of Shandong had defaulted on payments for shipments as they were unable to open letters of credit with banks, trade sources said on Thursday. A string of defaults on loans, bonds and shadow banking products in recent weeks has highlighted rising credit risks in China, partly fueled by signs the economy is slowing.

Commodity firms, along with semiconductor and software companies, are among the most at risk of credit defaults, a Reuters analysis of more than 2,600 Chinese companies showed. Up against the cooling economy and signs that authorities will not step in every time a loan goes bad, Chinese banks are becoming more hard-nosed and selective about whom they lend to. “There are five to six (panamax) cargoes which are unable to be unloaded at ports because buyers cannot open LCs (letters of credit) and there are no LCs for an additional 5-6 cargoes floating on the sea,” one Beijing-based source said. Each panamax cargo is for 50,000 to 60,000 tonnes.

• UN Set To Warn Countries Over ‘Dash For Gas’ (BBC)

Governments are likely to be warned next week that a “dash for gas” will not solve climate change. The chancellor and prime minister have promoted gas as a clean option for powering the UK. But a draft report for the United Nation’s third panel on climate change says gas cannot provide a long-term solution to stabilising climate change. Gas is only worthwhile if it is used to substitute a dirty coal plant – and then only for a short period, it says. Instead the world should be trebling or quadrupling the share of renewables for electricity, the authors say. The report will offer ammunition to the Department for Energy and Climate Change, which has fought attempts from the Treasury to switch more of the UK’s energy sources to gas with the projected “shale gas revolution”.

The UK hopes to emulate the success of the US, where shale gas has slashed energy prices and stimulated manufacturing. However, the draft report backs the position taken by the Environment Agency chairman, Chris Smith, who has told the prime minister the UK could only expand the role of gas in power generation if power stations were fitted with carbon-capture equipment to suck carbon dioxide from exhaust gases and store them in underground rocks. The UK is currently committed to trialling this technology in a gas power station in Peterhead. But the technology is so far untried at scale. It also adds to the cost of gas burning and reduces the efficiency of power stations.

” … in the last four years, Moscow has subsidized Ukraine’s economy to the tune of $35.4 billion.”

• Putin Tells Europe Ukraine Gas Debt ‘Critical’ (RT)

President Putin has written to 18 European countries, warning that Ukraine’s debt crisis has reached a “critical” level and could threaten transit to Europe. He also called for urgent cooperation, blaming Russia’s partners for a lack of action. Among the countries who’ll receive the letter are major consumers of Russian gas such as Germany, France, Italy, Greece, Turkey, Bulgaria, Moldova, Poland and Romania. Given the accumulated $2.2 billion gas debt owed by Ukraine’s Naftogas, Russia’s Gazprom will be forced to ask Ukraine for advance payments, Putin said in his letter to European partners, referring to the 2009 gas contract signed between Moscow and Kiev. “In other words, we’ll be supplying exactly the volume of gas that Ukraine pays for a month in advance,” as Itar -Tass quotes Putin’s letter.

Putin added that introducing advance payments would be an extreme measure. “We understand that this increases the risks of unsanctioned retrieval of gas flowing through the territory of Ukraine to European consumers. And it could also hinder accumulation of gas supplies in Ukraine necessary to provide for consumption during the autumn-winter period.” Stable transit of Russian gas to Europe would require an additional 11.5 billion cubic meters of gas for Ukraine’s underground storages, which would cost $5 billion, Putin explained. Given all the discounts Russia has provided in the last four years, Moscow has subsidized Ukraine’s economy to the tune of $35.4 billion, coupled with a $3 billion loan tranche in December last year. “I would underline – nobody except Russia has done this,” Putin wrote in the letter. “And what about [our] European partners? Instead of real support for Ukraine – declarations about intentions. Promises without real action.”

• Russian Economy Hammered By Massive Money Drain (CNBC)

Russia’s central bank this week confirmed that some $64 billion in assets held by Russians headed for the exits in the first three months of this year—roughly matching the total for all of 2013. The estimate of the capital exodus amounts to roughly 12% of Russia’s gross domestic product. That hemorrhaging is expected to continue if the turmoil in the Ukraine continues. Officials at the World Bank have warned that Russia could watch another $150 billion in capital leave the country if the crisis deepens. Since 2008, nearly half a trillion dollars has fled the country.

As the money flowing out of Russia is surging, the upheaval in Ukraine has put a damper on investment coming into the country. The cash squeeze comes as Russia’s economy is barely growing, inflation is rising fast and the central bank has been forced to raise interest rates to prop up a sagging ruble. The U.S. and Western countries seeking to thwart Putin’s Ukrainian ambitions have threatened economic sanctions if the Russian aggression continues. So far those have been limited to freezing the holdings of a handful of Putin’s political allies.

Nice problem. 22 million Russians died in WWII.

• Russia Crisis Spurs German Identity Conflict (Spiegel)

Our relationship to the Russians is as ambivalent as our perception of their character. “When it comes to the relations between the Germans and Russians, there is a tug-of-war between profound affection and total aversion,” says German novelist Ingo Schulze, author of the critically acclaimed “Simple Stories,” a novel that deals with East German identity and German reunification. Russians are sometimes perceived as Ivan the Terrible, as foreign entities, as Asians. Russians scare us, but we also see them as hospitable people. They have an enormous territory, a deep soul and culture — their country is the country of Tchaikovsky and Tolstoy.

It’s thus no wonder that the debate about Russia’s role in the Ukraine crisis is more polarizing than any other issue in current German politics. For Germany, the Ukraine crisis is not some distant problem like Syria or Iraq – it goes right to the core of the question of German identity. Where do we stand when it comes to Russia? And, relatedly: Who are we as Germans? With the threat of a new East-West conflict, this question has regained prominence in Germany and may ultimately force us to reposition ourselves or, at the very least, reaffirm our position in the West.

In recent weeks, an intense and polemical debate has been waged between those tending to sympathize with Russia and those championing a harder line against Moscow. The positions have been extreme, with one controversy breaking out after the other. The louder the voices on the one side are in condemning Russia’s actions in Ukraine, the louder those become in arguing for a deeper understanding of a humbled and embattled Russia; as the number of voices pillorying Russia for violating international law in Crimea grows, so do those of Germans raising allegations against the West.

One of the main charges is that the European Union and NATO snubbed Moscow with their recent eastward expansion. Everyone seems to be getting into the debate – politicians, writers, former chancellors and scientists. Readers, listeners and viewers are sending letters to the editor, posting on Internet forums or calling in to radio or television shows with their opinions.

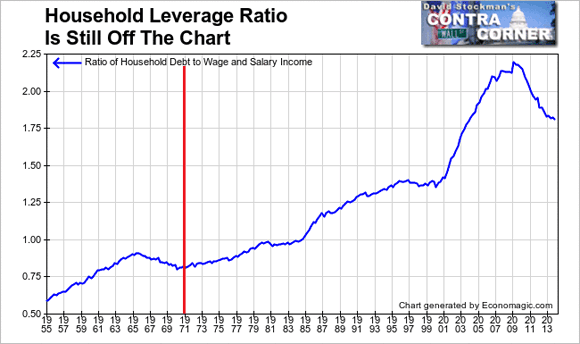

” … the facts of peak debt.”

• The Born Again Jobs Scam, Part 2: The Fed’s Labor Market Delusion (David Stockman)

Dr.Yellen is at it again. Noting that there is still “slack” in the labor market, she insists that more liquidity pumping action by the Fed is warranted: “Based on the evidence, my own view is that a significant amount of the decline in participation during the recovery is due to slack, another sign that help from the Fed can still be effective.” Once again, what Yellen is really saying is that our macroeconomic bathtub is not yet full to the brim—owing to insufficient aggregate “demand”. The purpose of the Fed’s “accommodative” policy, therefore, is to flood the American economy with additional consumer and investment spending—so that “slack” or unutilized labor and capital resources will be “pulled” into production.

Thus guided by the visible hand of the Fed, a virtuous cycle of rising spending, output and income will at length levitate our $17 trillion economy to its full-employment potential. As a practical matter, however, the Fed cannot stimulate additional “spending” unless it can also cause the economy’s leverage ratio to rise, thereby supplementing “spending” derived from current income with purchases financed by freshly minted (incremental) credit. Yet the flood of demand by which the Fed endeavors to “pull” idle and underemployed workers back into production cannot be activated if the US economy has reached a condition of peak debt, as I strongly believe to be the case. Indeed, when the credit expansion channel is broken and done, all the Fed’s liquidity “accommodation” flows into the Wall Street finance channel where it pulls up the price of existing financial assets, not the employment rate of idle labor.

And it cannot be gainsaid that the Fed is entirely ignoring the facts of peak debt and the broken credit channel it implies. For approximately 35 years, the ratio of household debt to wage and salary income ratcheted steadily upward from 80% to 210%. But once household leverage reached the latter precarious peak under the lunatic mortgage blow-off during 2002-2007, it buckled and now stands at about 180%. Yet why would it be reasonable to expect a retracement back to the 2007 peak—even if the madness of the student loan explosion continues or sub-prime auto lending keeps surging? These are minor upwellings compared to the $10 trillion mortgage mountain. Besides, a renewed household borrowing binge is not going to happen due to the baby-boom retirement crush, which liquidates household debt, and the “Dodd-Franking” of the banking system, which inhibits lending—risky and otherwise. So the Fed’s transmission mechanism to the household sector is blocked.

Let’s buy some Greek bonds …

• Germany’s Current Account Surplus A Wider Issue Than It Seems (Rogoff)

When the US treasury recently added its voice to the chorus of critics of Germany’s chronic current account surplus, it underscored the deep disagreement over what, if anything, should be done about it. The critics want Germany to increase its contribution to global demand by importing more and exporting less. The Germans view the maintenance of strong balance sheets as essential to their country’s stabilising role in Europe. Both of their arguments will certainly receive a full airing at the spring meetings of the International Monetary Fund and the World Bank. Unfortunately, the debate has too often been informed more by ideology than facts.

The difference between what a country exports and imports can reflect myriad factors, including business cycles, demographics, investment opportunities and economic diversification. It can also reflect the government’s penchant for running fiscal surpluses; after all, the current account surplus, by definition, is the excess of public and private savings over investment. During the first half of the 2000s, US policymakers chose not to worry about sustained current account deficits, which peaked at above 6% of GDP. They argued at first that the deficits merely reflected the world’s attraction to superior US investment opportunities, an odd position given that the US was not growing especially quickly compared with emerging markets.

Later, academic researchers identified more plausible reasons why the US might be able to run large deficits without great risk, as long as investors’ desire for diversification, safety and liquidity sustained global demand for US assets. But policymakers should have recognised that even these better rationales had limits, and that massive sustained current account deficits are often a blinking red signal of deeper problems – in this case, over borrowing by households to finance home purchases.

WIth friends like that, who needs enemies?

• Angela Merkel Denied Access To Her NSA File (Guardian)

The US government is refusing to grant Angela Merkel access to her NSA file or answer formal questions from Germany about its surveillance activities, raising the stakes before a crucial visit by the German chancellor to Washington. Merkel will meet Barack Obama in three weeks, on her first visit to the US capital since documents leaked by whistleblower Edward Snowden revealed that the NSA had been monitoring her phone. The face-to-face meeting between the two world leaders had been intended as an effort to publicly heal wounds after the controversy, but Germany remains frustrated by the White House’s refusal to come clean about its surveillance activities in the country.

In October, Obama personally assured Merkel that the US is no longer monitoring her calls, and promised it will not do so in the future. However, Washington has not answered a list of questions submitted by Berlin immediately after Snowden’s first tranche of revelations appeared in the Guardian and Washington Post in June last year, months before the revelations over Merkel’s phone. The Obama’s administration has also refused to enter into a mutual “no-spy” agreement with Germany, in part because Berlin is unwilling or unable to share the kinds of surveillance material the Americans say would be required for such a deal.

• Ukrainian Crisis Not Wasted by Washington Lobbyists (Bloomberg)

A lot of Washington interest groups owe Russian President Vladimir Putin a big thank you. Putin’s annexation of Ukraine’s Crimea region last month is being cited in Washington as a reason to do everything from building an oil pipeline to accelerating private space flight and even boosting the export of liquefied natural gas. “This is truly classic behavior,” Burdett Loomis, a political science professor at the University of Kansas who specializes on lobbying, said in a phone interview. “You can create a narrative that puts you on the side of the angels.”

Crises have long jolted Washington into action, serving as catalysts for policy. Think Sputnik: the low-orbit satellite the Soviet Union launched in 1957, stoking fears the U.S. was falling behind in a race to space. It helped build support for the program that put Americans on the moon. “You never want a serious crisis to go to waste,” Rahm Emanuel, Chicago’s Democratic mayor who served as an Illinois congressman and President Barack Obama’s former chief of staff, said during a 2008 Wall Street Journal conference. [..]

Russia’s military intervention in Ukraine boosted calls to expedite U.S. natural gas exports. “Having more of our gas reach the market will reduce volatility and provide diversity,” Karen Harbert, president of the U.S. Chamber of Commerce’s 21st Century Energy Institute, told reporters on a conference call on March 4 — the same day Putin said Russia would cancel the price discount on natural gas it sold to Ukraine. Efforts by other Washington-based lobbying groups including the American Petroleum Institute to lift 1970s-era bans on the export of oil also have gained steam. “We’ve just had a consistent drumbeat going since the beginning of last year,” Erik Milito, API’s director of upstream and industry operations, said in an interview. “We just kept doing it, and this became a more heightened debate during the whole Ukraine situation.”

No kidding.

• World Bank Warns IMF Terms Will Eat Into Consumption, Investment In Ukraine (RT)

Loan terms set by the International Monetary Fund (IMF), will cut consumption in Ukraine this year by 8%, as well as erode capital investment, the World Bank has warned. The increased cost of household gas and district heating “will affect purchasing power and limit the government’s ability to boost capital spending this year. Thus, in 2014, we expect to see a decline in both consumption and fixed investment,” says the WB statement. “After several years of robust growth, a drop in consumption may be significant this year (over 8%) while decline in fixed investments will not be that substantial due to a low statistical base,” it added. The World Bank also said the GDP will shrink 3%, with inflation jumping to 15% in 2014.

Greece got its first international bailout four years ago, and the people have seen their disposable incomes fall by a third, and unemployment soaring to 28% – the highest in 33 years. The country’s GDP has shrunk by a quarter over the period. In March the IMF agreed to grant Ukraine between $14 billion and $18 billion over the next two years, to help the country avoid a default. The IMF funds usually come with stringent terms, asking for various cuts and economic reforms. In the case of Ukraine, the fund’s requirements include a 50% increase in the price of gas for households, as well as a quick pension reform and lower government spending.

They will wait till after the Europeans elections, and then unleash ECB QE.

• Weidmann Citing QE Legitimacy Paves Way for Consensus ECB (Bloomberg)

Jens Weidmann has morphed from Dr. No into Mr. Maybe. After building a reputation as a nay-sayer on the European Central Bank’s Governing Council, the Bundesbank president’s support for large-scale asset purchases marks a shift that helps the fight against deflationary threats. His tentative backing of quantitative easing will shore up its credibility as officials debate whether they need to implement it. German officials at the ECB have throughout the euro-area debt crisis been among the fiercest opponents of bond buying.

Asset-purchase plans triggered the resignation of two German central bankers and drew criticism from others, including Weidmann. That makes any change of stance significant should ECB President Mario Draghi push for QE as the best way to safeguard the recovery. “Weidmann’s comments are very important and mark the first time in the euro’s history that the Bundesbank is clearly publicly on the side of QE,” said Julian Callow, founder of Catalyst Economics Ltd. in London. “A program isn’t a given but consensus is important. It gets you some of the way without having to do it.”

“Around 40% of all U.S. stock trades, including almost all orders from “mom and pop” investors, now happen “off exchange … ”

• Dark Markets May Be More Harmful Than High Frequency Trading (Reuters)

Fears that high-speed traders have been rigging the U.S. stock market went mainstream last week thanks to allegations in a book by financial author Michael Lewis, but there may be a more serious threat to investors: the increasing amount of trading that happens outside of exchanges. Some former regulators and academics say so much trading is now happening away from exchanges that publicly quoted prices for stocks on exchanges may no longer properly reflect where the market is. And this problem could cost investors far more money than any shenanigans related to high frequency trading.

When the average investor, or even a big portfolio manager, tries to buy or sell shares now, the trade is often matched up with another order by a dealer in a so-called “dark pool,” or another alternative to exchanges. Those whose trade never makes it to an exchange can benefit as the broker avoids paying an exchange trading fee, taking cost out of the process. Investors with large orders can also more easily disguise what they are doing, reducing the danger that others will hear what they are doing and take advantage of them.

But the rise of “off-exchange trading” is terrible for the broader market because it reduces price transparency a lot, critics of the system say. The problem is these venues price their transactions off of the published prices on the exchanges – and if those prices lack integrity then “dark pool” pricing will itself be skewed. Around 40% of all U.S. stock trades, including almost all orders from “mom and pop” investors, now happen “off exchange,” up from around 16% six years ago.

Home › Forums › Debt Rattle Apr 11 2014: Manipulated Markets And The Empty Bag