John Collier Grandfather Romero, 99 years old. Trampas, New Mexico 1943

It’s funny to see how fast the subprime car loan schemes are falling apart.

• August US Auto Sales Fall 4.2%; Carmakers Say Industry Has Peaked (R.)

U.S. auto sales fell 4.2% in August as some major automakers said a long-expected decline due to softer consumer demand had begun, possibly sparking a shift to juicer customer incentives and slower production. The top three sellers, General Motors, Ford and Toyota on Thursday reported declines of at least 5%. Of the seven top manufacturers by sales, only Fiat Chrysler reported a gain versus a year ago, when sales were restated to about 11,000 fewer than originally reported. Monthly spending on new cars and trucks is closely watched as the U.S. auto industry accounts for about one-fifth of U.S. retail sales. August sales, said Autodata, totaled 1.51 million vehicles, or 16.98 million vehicles at a seasonally adjusted annualized rate, versus a surprisingly strong 17.88 million vehicles in July.

Ford Chief Economist Bryan Bezold said sales had hit a plateau after steadily rising following the 2008-2009 recession. The auto industry outperformed the overall U.S. economy in those years largely due to pent-up demand that has now played out, he said. Wall Street has pressured automaker shares all year amid expectations of falling sales at some point. [..] Ford, whose sales tumbled 8.4%, said its U.S. inventory was at 81 days of supply versus 61 days a year earlier, suggesting Ford may have to cut production, increase profit-eroding incentives, or boost fleet sales.

“This watch is ticking because of high global debt and out-of-date monetary/fiscal policies that hurt rather than heal real economies.”

• Bill Gross Says Negative Interest Rates Are Nothing But Liabilities (MW)

Call bond-market veteran Bill Gross a “broken watch.” He doesn’t care. His gripe about negative interest rates and a flood of debt, which he considers a risk, not a fix, for a global economy that’s still limping out of the financial crisis, is challenged daily by resilient demand for the bonds he’s bearish on. But even if being “right” eventually is a hard sell right now, he’s not backing down, Gross said in his latest monthly commentary. “The problem with Cassandras, such as Gross and Jim Grant and Stanley Druckenmiller, among a host of others, is that we/they can be compared to a broken watch that is right twice a day but wrong for the other 1,438 minutes,” Gross wrote. “But believe me: This watch is ticking because of high global debt and out-of-date monetary/fiscal policies that hurt rather than heal real economies.”

Germany, Switzerland, France, Spain and Japan are among countries that have negative yields on government-issued debt. Their hope is that cheap, even free, borrowing raises inflation and revives asset prices that can filter through economies; they argue extreme policies have been needed. Gross and others have argued that rates, including those at the Federal Reserve, at near zero or below won’t create sustainable economic growth and actually undermine capitalism. The U.S. has not tipped rates quite as low as other central banks and the Federal Reserve weaned markets off its quantitative-easing program well ahead of its big-economy brethren. Still, Federal Reserve Chairwoman Janet Yellen said last week at the Fed’s Jackson Hole retreat that she wants her policy kit to include all tools, including further asset purchases if necessary.

Divergence with the rest of the world only complicates the debate over when and how aggressively the Fed should dial back accommodative policy. Was that enough to scare off most bond investors? Apparently not. Treasury yields logged their largest daily drop in nearly two months to kick off this week, taking back their Fed-spooked gain from hawkish comments at Jackson Hole. Yields, of course, fall when prices rise, and vice versa. At that mountain gathering, Fed second-in-command Stanley Fischer opened the door to more than one rate increase this year, depending on economic data. And Fischer himself said Fed Chairwoman Janet Yellen’s stance appears in line with that mind-set.

But Gross questions the long-term effects of the world’s unprecedented yield conditions and central banker reluctance to let them go. “Capitalism, almost commonsensically, cannot function well at the zero bound or with a minus sign as a yield,” wrote Gross, who manages the Janus Global Unconstrained Bond Fund, up just over 4% year to date. “$11 trillion of negative yielding bonds are not assets — they are liabilities. Factor that, Ms. Yellen, into your asset price objective.”

Well, that makes us feel much better…

• Goldman: The Fed Might Have a New, Big Idea (BBG)

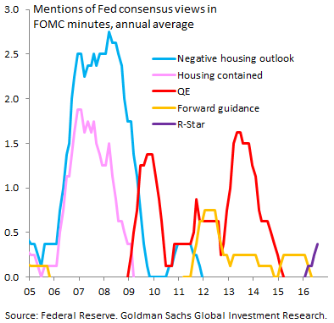

The Death Star is a fictional space station popularized by the Star Wars franchise. The r-star (r*) is the natural rate of interest that sometimes crops up in economics texts. It also might be the Federal Reserve’s newest, biggest idea, according to strategists at Goldman Sachs. The notion that the natural or neutral rate of interest has been stuck at ultra-low levels might help the U.S. central bank square a dilemma between hiking interest rates and strengthening the U.S. dollar, they said.

“For the FOMC, this is a genuine conundrum, because it means that too hawkish a message could send the Dollar sky-rocketing, a deflationary shock that would also weigh on growth, thereby – in a way – undermining the very rationale for shifting hawkish in the first place,” write Goldman strategists led by Robin Brooks. “To deal with this conundrum, the framework that many at the Fed seem to be converging around is that ‘r-star’ is low, so that the degree of monetary policy accommodation is only moderate, despite policy rates being so low.” Such a stance could allow the central bank to justify keeping benchmark interest rates lower for longer. While the strategists don’t judge the notion on its merits, they do compare it to some previous big ideas that have been discussed at the central bank in recent years.

Among these is the concept that the effects of the U.S. housing crisis would not be material – a theme that dominated in the two years before the 2008 financial crisis (and shown in the pink line below). That idea soon gave rise to concerns that the bursting of the housing bubble would have a negative impact on the U.S. economy (shown in blue). Subsequently, policymakers’ collective imaginations were captured by the notion that quantitative easing would prove positive for economic growth (in red), while the notion that forward guidance (in yellow) is a useful policy tool soon gained in popularity.

Yeah, dismantle itself.

• BOJ Must ‘Do Something Meaningful,’ Former Official Says (BBG)

The Bank of Japan should abandon the monetary base target that’s driving its unsustainable bond purchases while pursuing a negative-rate loan program to help companies and consumers, said a former BOJ executive director. “The BOJ can’t get out of this struggle as long it has this cursed monetary base target,” Hideo Hayakawa, who retired from the central bank in 2013, said in an interview on Thursday. “Once they drop it, they can take a variety of other easing measures.” Hayakawa, 61, contends that there is no evidence that the monetary base target championed by Governor Haruhiko Kuroda is effective in spurring inflation. It should be dropped, and bond purchases scaled back and managed via a range rather than aiming for a specific number, he said.

“As long as they make it very clear that their goal is to keep a lid on bond yields, and the yields stay low, they can gradually lower the range of bond purchases,” said Hayakawa, who also served as the central bank’s chief economist. At the same time, he said Kuroda ought to avoid taking a deeper dive on the existing negative interest rate charged on some funds commercial banks park at the BOJ. It should simultaneously take rates on its lending facilities from zero into negative territory, which would effectively pay some borrowers who take out loans. People familiar with talks at the BOJ said in April that the central bank may consider minus rates on the Stimulating Bank Lending Facility.

Can it still get crazier than this?

• Is the ECB Buying Bonds From Itself? (WSJ)

The European Central Bank may be buying bonds from itself as it runs out of debt to sate its massive quantitative easing program. That’s according to economists at Jefferies. The ECB’s bond-buying program has been running for nearly 18 months, and investors and analysts have often asked whether the central bank is running out of debt to buy. Now, the ECB may be indirectly buying bonds from itself, according to Marchel Alexandrovich and David Owen at Jefferies, in a research note published Thursday. But here’s how Jefferies thinks it may work. The ECB’s QE program is implemented through several national central banks, like Germany’s Bundesbank and Spain’s Banco de Espana. National central banks buy bonds according to rules set by the ECB.

The problem is that these constraints narrow the stock of debt the banks can buy from. These rules prevent the purchase of too much debt from any one country and stop central banks from buying debt with steeply negative yields. Portuguese and Irish debt, for instance, is now becoming scarce. But the national central banks also sell sovereign bonds. They sometimes reduce their holdings as a part of their reserve management activities, which aim to ensure that banks, state institutions and other organizations “manage their euro-denominated reserve assets comprehensively, efficiently, and in a safe, confidential and reliable environment,” according to the ECB’s website. That means, for example, that while the German Bundesbank bought €209 billion in sovereign bonds between March and July, they also sold off €43 billion of such debt, according to Jefferies.

Because why would they invest in liabilities?

• Bond Buyers Leave Europe to the ECB, Head to US (WSJ)

The ECB recently started buying corporate bonds to boost the eurozone economy. One of the big beneficiaries so far: U.S. credit markets. Faced with dwindling returns in Europe, a growing number of investors are selling their corporate bonds to the ECB and heading across the Atlantic where yields are higher and they aren’t so vulnerable to changes in expectations around central bank buying habits. The extra yield investors demand to hold corporate bonds over safe government debt—or credit spread—has declined more rapidly in Europe than the U.S. since the ECB announced its buying plans in March. But that trend has reversed in recent weeks, with U.S. credit markets outperforming the eurozone in August, according to Bloomberg Barclays bond indexes.

That comes as investors have sold European corporate bonds and shifted funds into the U.S. as they fan out in search of returns. Net inflows into U.S. corporate bond funds have outpaced inflows to similar European funds by almost $2 billion since the start of the ECB’s program in early June, according to the latest available data from EPFR Global. As a result, borrowing costs for large U.S. companies have remained near record lows even as expectations have mounted that the Federal Reserve will soon resume raising interest rates. Mark Kiesel at PIMCO said he had been buying euro and sterling corporate bonds in anticipation of the ECB and, more recently, the Bank of England entering these markets. Now, he’s selling and moving more into U.S. credit markets.

Modern colonialism.

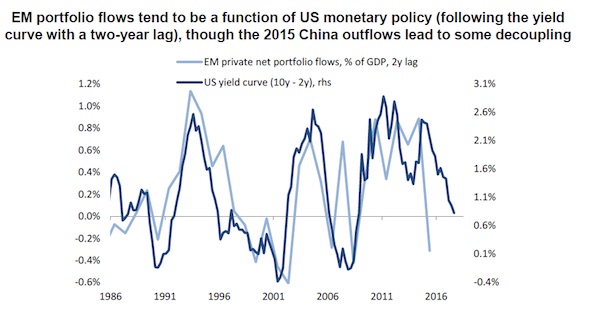

• The Fed Poses a Big Risk to the Emerging Market Inflow Party (BBG)

Battle-hardened emerging-market investors have seen this movie before: A U.S. Federal Reserve interest-rate hike triggers a jump in nominal local rates in emerging markets, especially those with fixed or semi-fixed exchange rate regimes. Hot money flows out of developing nations, across FX, equity and fixed-income markets. Local currencies weaken against the dollar. And the ensuing jump in the cost of dollar liquidity, and declining portfolio flows, spark fears over the debt-servicing capacity of emerging-market borrowers. In short, the boom-and-bust capital-flow cycles in emerging markets over the past three-decades have roughly followed this script.

Fast-forward to September 2016: markets are raising their bets that the Fed will hike rates this year – raising fears the post-Brexit-vote inflow party in emerging markets might ease, while international financial conditions, more generally, might tighten. Now, analysts say that the outlook for EM asset classes hinges on how the U.S. yield curve reprices in the coming months. In short, the shape of the Treasury yield curve and the level of long-term U.S. real rates, in particular – rather than the absolute level of U.S. short-end rates – will be crucial in driving capital flows into emerging markets, analysts say. Sebastian Raedler, equity strategist at Deutsche Bank, is one analyst who urges caution, citing EMs’ dependence on U.S. monetary policy.

EM portfolio flows tend to follow developments in the U.S. yield curve with a two-year lag, he says, suggesting financial conditions could tighten significantly in emerging markets if the Fed becomes notably more hawkish. “It’s very clearly the case that low U.S. rates are historically a push factor for foreign capital flows into emerging markets,” Raedler says. “The best scenario to support continued inflows into emerging markets is that financial conditions remain benign. But, thinking about the 30-year history, investors tend to love EM the most when the party in U.S. monetary policy — low rates — is in full swing.”

I’m waiting for the next domino to fall. Only then will people recognize what’s going on.

• Hanjin Shipping Bankruptcy Causes Turmoil In Global Sea Freight (G.)

[..] Hanjin’s banks decided to end financial support for the shipper this week and many of its vessels were denied entry to ports or left unable to dock as container lashing providers worried they would not be paid. This included the port of Busan, South Korea’s largest. The Korea International Trade Association said on Thursday that about 10 Hanjin vessels in China have been either seized or were expected to seized by charterers, port authorities or other parties. That adds to one other ship seized in Singapore by a creditor earlier in the week. The collapse comes at a time of high seasonal demand for the shipping industry ahead of the year-end holidays. In the US, at the ports of Los Angeles and Long Beach, the nation’s busiest port complex, three Hanjin container ships, ranging from about 700 feet to 1,100 feet long, were either sitting offshore or anchored away from terminals on Thursday.

A fourth vessel that was supposed to leave Long Beach on Thursday morning remained anchored inside the breakwater. The National Retail Federation, the world’s largest retail trade association, wrote to the US secretary of commerce, Penny Pritzker, and the Federal Maritime Commission chairman, Mario Cordero, on Thursday, urging them to work with the South Korean government, ports and others to prevent disruption. Hanjin represents nearly 8% of the trans-Pacific trade volume for the US market and the bankruptcy was having “a ripple effect throughout the global supply chain” that could cause significant harm to both consumers and the US economy, the association wrote.

[..] Other shipping lines were moving to take over some of the Hanjin traffic but at a price, with vessels already are operating at high capacity because of the season. The price of shipping a 40ft container from China to the US jumped by up to 50% in a single day, said Nerijus Poskus, director of pricing and procurement for Flexport, a licensed freight forwarder and customs broker based in San Francisco, who predicted the higher prices would last a month or two. The price from China to west coast ports rose from $1,100 per container to as much as $1,700 on Thursday, while the cost from China to the East Coast jumped from $1,700 to $2,400, he said.

There is no one answer here. Applying tax laws retroactively is thin ice. But so is allowing companies to pay 0.005% in taxes

• Don’t Criticize Europeans For Standing Up To Apple – Thank Them (Robert Reich)

For years, Washington lawmakers on both sides of the aisle have attacked big corporations for avoiding taxes by parking their profits overseas. Last week the European Union did something about it. The EU’s executive commission ordered Ireland to collect $14.5 billion in back taxes from Apple. But rather than congratulate Europe for standing up to Apple, official Washington is outraged. Republican House Speaker Paul Ryan calls it an “awful” decision. Democratic Senator Charles Schumer, who’s likely to become Senate majority leader next year, says it’s “a cheap money grab by the European Commission.” Republican Orrin Hatch, chairman of the Senate Finance Committee, accuses Europe of “targeting” American businesses. Democratic Senator Ron Wyden says it “undermines our tax treaties and paints a target on American firms in the eyes of foreign governments.”

P-l-e-a-s-e. These are taxes America should have required Apple to pay to the U.S. Treasury. But we didn’t – because Ryan, Schumer, Hatch, Wyden and other inhabitants of Capitol Hill haven’t been able to agree on how to close the loophole that has allowed Apple, and many other global American corporations, to avoid paying the corporate income taxes they owe. Let’s be clear. The products Apple sells abroad are designed and developed in the United States. So the foreign royalties Apple collects on them logically should be treated as corporate income to Apple here in America. But Apple and other Big Tech corporations like Google and Amazon – along with much of Big Pharma, and even Starbucks – have avoided paying hundreds of billions of dollars in taxes on their worldwide earnings because they don’t really sell things like cars or refrigerators or television sets that they make here and ship abroad.

[..] over the last decade alone Apple has amassed a stunning $231.5 billion cash pile abroad, subjected to little or no taxes. This hasn’t stopped Apple from richly rewarding its American shareholders with fat dividends and stock buybacks that raise share prices. But rather than use its overseas cash to fund these, Apple has taken on billions of dollars of additional debt. It’s a scam, at the expense of American taxpayers. Add in the worldwide sales of America’s Big Tech, Big Pharma and Big Franchise operations, and the scam is sizable. Over €2 trillion of U.S. corporate profits are now parked abroad – all of it escaping the U.S. corporate income tax. To make up the difference, you and I and millions of other Americans have to pay more in income taxes and payroll taxes to finance the U.S. government.

Meanwhile, the opinions are fun to read.

• Apple Boss Tim Cook Should Stop Whinging And Pay Up (Ind.)

Having been handed a €13bn bill for back taxes – it is not a fine as some would have you believe – Apple boss Tim Cook has gone on the offensive. The under fire tech giant’s chief executive chose Ireland’s state broadcaster RTE as the venue for a broadside against the European Commission in the wake of its ruling that the tax deal arranged between Apple and Ireland amounted to illegal state aid. What he said was, well, hard for me to read without inflicting damage on my, erm, Apple Mac. So read on at your own computer’s risk: “When you’re accused of doing something that is so foreign to your values, it brings out an outrage in you, and that’s how we feel. Apple has always been about doing the right thing.”

Oh Mr Cook. It’s not you who should be feeling outraged. It’s us. Even if you think that what the EC did was pushing it, this is is still a company that has cynically gamed the international tax system with the aim of depriving nation states from whose citizens Apple makes its living, the tax they are due. Taking advantage of loopholes, employing accountants to manipulate the rules; Apple’s defenders might call that pragmatic. But it’s hard to see how anyone not in the business of creating propaganda for Apple could describe its behaviour as “doing the right thing”. Mr Cook, it appears, has no shame. “Total political crap,” he ranted. “Maddening.”

What’s maddening is the way multinational companies like Apple utilise their resources to avoid paying their share at a time of austerity. What’s maddening is the way tax authorities bring the hammer down on individual citizens for making honest mistakes while shrugging their shoulders when it comes to policing wealthy corporations. As for “political crap”? This is a man who has hosted fundraisers for Hilary Clinton. If that’s not political crap, I’d really like to know what is.

Victoria Nuland is still around. In fact, under a potential Hillary presidency, she’s set to acquire a whole lot more power (Secretary of State?). That’s very scary.

• US Imposes Sanctions On ‘Putin’s Bridge’ To Crimea (R.)

Companies building a multi-billion dollar bridge to link the Russian mainland with annexed Crimea, a project close to the heart President Vladimir Putin, were targeted by the United States in an updated sanctions blacklist on Thursday. The U.S. Department of the Treasury added dozens of people and companies to the list, first introduced after Russia annexed the Crimean peninsula from Ukraine in 2014 and expanded over its support for separatist rebels in the east of the country. As well as multiple subsidiaries of Russian gas giant Gazprom and 11 Crimean officials, the Treasury named seven companies directly involved in the construction of the 19 km (11.8 miles) road-and-rail connection across the Kerch Strait, dubbed “Putin’s bridge” by some Russians.

Chief among those were SGM-Most, a subsidiary of lead contractor Stroygazmontazh which is already under U.S. sanctions, and sub-contractor Mostotrest, one of Russia’s biggest bridge builders. “Treasury stands with our partners in condemning Russia’s violation of international law, and we will continue to sanction those who threaten Ukraine’s peace, security and sovereignty,” said John Smith, acting director of the Treasury’s Office of Foreign Assets Control, which levies sanctions.

The Russian Foreign Ministry was not immediately available for comment, but Moscow has previously said sanctions levied over its actions in Ukraine undermine efforts to resolve the conflict. Set to be the longest dual-purpose span in Europe when completed, the Kremlin sees its 212-billion rouble ($3.2 billion) bridge as vital to integrating Crimea into Russia, both symbolically and as an economic lifeline for the region. Putin has called the undertaking an historic mission.

Note: all of the Hillary campaign’s allegations about Russia hacking the DNC remain wholly unsubstantiated. That’s some flimsy ground to stand on, if that’s all you got. Innuendo can’t carry you all the way.

• Putin Says DNC Hack Was a Public Service, Russia Didn’t Do It (BBG)

Vladimir Putin said the hacking of thousands of Democratic National Committee emails and documents was a service to the public, but denied U.S. accusations that Russia’s government had anything to do with it. “Listen, does it even matter who hacked this data?’’ Putin said in an interview at the Pacific port city of Vladivostok on Thursday. “The important thing is the content that was given to the public.’’ U.S. officials blame hackers working for the Russian government for the attacks on DNC servers earlier this year that resulted in WikiLeaks publishing about 20,000 private emails just before Hillary Clinton’s nominating convention in July.

The documents showed attempts by party officials to undermine her chief Democratic rival, Bernie Sanders, and led to the resignation of the head of the DNC, Representative Debbie Wasserman Schultz of Florida. Putin, in power since 2000 and facing re-election in 18 months, and Clinton have had an acrimonious relationship since her failed attempt to “reset” relations as secretary of state in 2009. Putin in 2011 blamed her personally for stoking the biggest protests of his rule by sending an activation “signal” to “some actors” inside Russia. Clinton has compared his annexation of Crimea in 2014 to actions taken by Adolf Hitler before World War II.

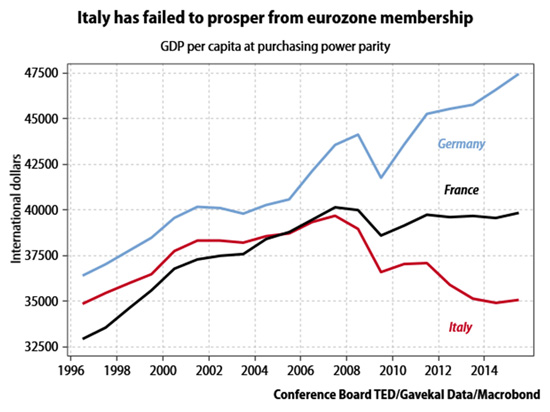

No doubt about it. The euro makes no more sense for Italy than it does for Greece.

• The Italian Referendum Could Result In The Death Of The Euro (Andrews/Capacci)

Prime ministers come and go in Italy—four since the financial crisis—but precious little seems to change. The latest incumbent, Matteo Renzi, has pursued structural reform more energetically than his predecessors. But for all the progress he has made, he might as well have been wading through molasses. Now, in a bid to secure a popular mandate for his restructuring program, Renzi has bet his premiership on a referendum over badly-needed constitutional reforms. It is a high stakes gamble. If Renzi wins the vote, which is due in either October or November, his proposed measures will streamline Italy’s legislative process, breaking the parliamentary gridlock which has crippled successive governments, and opening the way to far-reaching economic reforms.

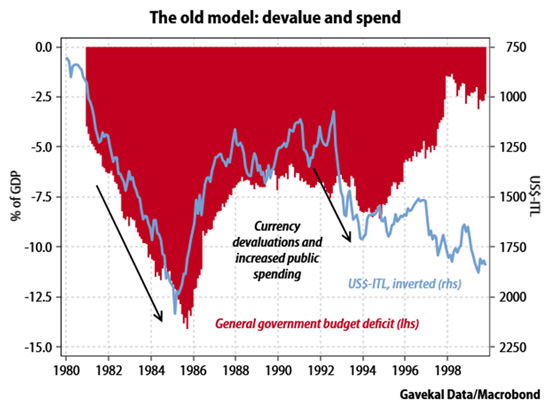

If he loses, Renzi has promised to step down—a pledge that has turned the referendum into a popular vote of confidence in the unelected prime minister, his Europhile policies, and—by extension—Italy’s membership of the eurozone itself. As a result, a “no” vote in October will not just precipitate the fall of Renzi’s government; it could throw Italy’s long-term membership of the eurozone into doubt, plunging the single currency area once again into crisis. Italy’s fundamental problem is that it’s stuck in a policy no man’s land. Its old economic model, in place for much of the last three decades of the 20th century, relied on a combination of currency devaluation to maintain international competitiveness together with fiscal spending to support the poorer regions of the country’s south.

Signing up to the euro put an end to all that, preventing devaluations and prohibiting budget deficits at 10% of gross domestic product. However, the design of Italy’s bicameral parliamentary system, in which the upper and lower house—the Senate and the Chamber of Deputies—wield equal legislative power, made it almost impossible for any government to push through the structural reforms necessary for Italy to compete and prosper within the eurozone. The result has not just been depressed growth and relative impoverishment, but an outright decline in living standards as Italy’s real GDP per capita has slumped to a 20-year low.

Problem is, the refugees don’t want to say in France.

• France Vows To Dismantle ‘Jungle’ Refugee Camp In Calais (G.)

France is to gradually dismantle the “Jungle” refugee camp in Calais, the interior minister, Bernard Cazeneuve, has vowed. Cazeneuve told regional newspaper the Nord Littoral he would press ahead with the closure of the camp “with the greatest determination”, dismantling the site in stages, clearing the former wasteland where record numbers of refugees and migrants are sleeping rough in dire sanitary conditions as many hope to reach Britain. He said France would create accommodation for thousands elsewhere in the country “to unblock Calais”.

French authorities have made repeated efforts to shut down the camp, which the state was responsible for creating in April 2015 when authorities evicted migrants and refugees from squats and outdoor camps across the Calais area and concentrated them into one patch of wasteland without shelter. Less than six months ago, the authorities demolished a large area of the southern part of the camp, saying the aim was to radically reduce numbers. But this month the number of people in the camp reached an all-time high of almost 10,000 people, aid organisations estimate. The French authorities put the official number of people in the camp at almost 7,000. Authorities have said over the past year more than 5,000 asylum seekers have left the northern French town for 161 special centres set up around France.

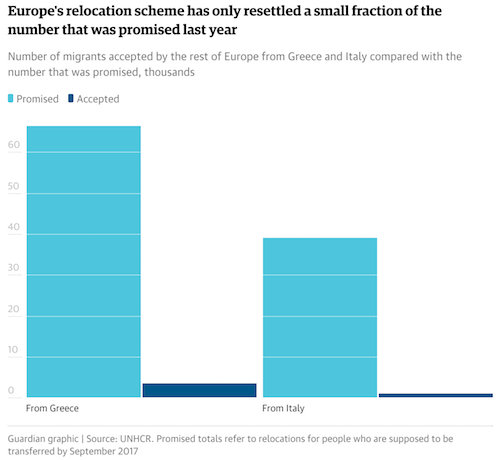

Beware the numbers. The relocation scheme has been one big EU failure, one among far too many.

• Greece On Edge, As Turkish Coup Prompts Surge In New Arrivals (Omaira Gill)

After dropping for several months, the numbers of refugees pouring through Greece have started to increase again in recent weeks. When an EU-Turkey deal was hacked out in March 2016, it was hailed by EU governments as a success. The massive numbers that had transited through Greece in 2015 and early 2016 quickly whittled down to almost nothing. But people have not stopped coming, and the failed coup in Turkey on 15 July seems to have had consequences. The EU-Turkey deal came into effect on 20 March 2016. In February, UNHCR data showed 55,222 arrivals in Greece. This had fallen to 26,623 in March and 3,419 in April. The numbers for May and June were more or less steady at 1,465 and 1,489, respectively. But in July, the pattern began to change.

There were 1,855 arrivals recorded for the month of July. This could be written off as part of the settling down period for the deal, until the numbers are broken down and matched with events which took place that month. On 15 July, an attempted putsch took place in Turkey. The number of arrivals from 1 July to 14 July came to 560. But that number jumped to 1,295 for the period 15 July to 31 July – an increase of 131%. Taking a step further back, between 15 June and 14 July, 1,438 arrivals were registered in Greece. But from 15 July to 14 August, the number was 2,675, representing an 86% increase in arrivals. In the face of this data, it is hard to ignore Turkey’s current instability as a driving factor behind refugee flows. Between 1 and 28 August, the latest available date for arrivals by the UNHCR, 2,810 refugees and migrants arrived on Greek shores.

We will be judged on this.

• The Death Of Alan Kurdi: One Year On, Compassion Towards Refugees Fades (G.)

Sitting in a refugee camp in northern Greece, Mohammad Mohammad, a Syrian taxi driver, holds up a picture of three-year-old Alan Kurdi. It is nearly a year since the same photograph of the dead toddler sparked a wave of outrage across Europe, and heightened calls for the west to do more for refugees. Twelve months later, Mohammad uses it to highlight how little has changed. Alan may have died at sea, he says, “but really there is no difference between him and the thousands of children now dying [metaphorically] here in Greece”. Tens of thousands have been stranded in squalid conditions in Greece since March, when Balkan leaders shut their borders. “It is,” says Mohammad, “a human disaster.” A year ago, Alan’s tragic death seemed to have shifted the political discourse on refugees.

European leaders appeared to have been shocked into forming more compassionate policies, while previously hostile media outlets took a more conciliatory tone. Two days after Alan’s death, Germany agreed to admit thousands of refugees who had been stranded in Hungary. The move encouraged the leaders of central and eastern Europe to create a humanitarian corridor from northern Greece to southern Bavaria, while Canada promised to resettle 25,000 Syrians. In the UK David Cameron agreed to accept 4,000 refugees a year until 2020. It was less than the number landing each day on the Greek islands at that point, but far more than Cameron had previously dared to offer. He was cheered on by the Sun, whose opinion pages had previously described migrants as cockroaches, but now mounted a front-page campaign in Kurdi’s name: “For Aylan [sic]”.