“Flora” (Roman Goddess of Spring), Villa di Arianna, Pompei 1st Century A.D.

IRAN WAR DISASTER: US HEADED FOR HUMILIATING DEFEAT

— Mark (@Mark4XX) March 3, 2026

In this explosive interview, decorated combat veteran Colonel Douglas McGregor pulls no punches on the escalating US-Iran conflict that's already spiraling into a regional catastrophe. With oil prices surging and key bases… pic.twitter.com/tmaLhu5GIS

BREAKING: QatarEnergy just declared Force Majeure.

— Shanaka Anslem Perera ⚡ (@shanaka86) March 4, 2026

Three words that mean: we cannot deliver, and legally, we do not have to.

This is no longer a supply disruption. This is a contract collapse.

Force Majeure is not a precaution. It is a formal legal declaration that an… https://t.co/4DBcRWrv7p pic.twitter.com/iMNUjwUX1G

BREAKING: Qatar just shut down all LNG production.

— Shanaka Anslem Perera ⚡ (@shanaka86) March 4, 2026

The world’s second largest LNG exporter. Gone. Today.

Iranian drones hit Ras Laffan and Mesaieed. QatarEnergy killed the plant. 20% of global LNG supply has disappeared from the market in a single morning.

Now here is the… pic.twitter.com/2ueMjFZBWI

BREAKING: Iran Agrees to Ceasefire Talks After Top Leader's Groupchats Hacked pic.twitter.com/5rEbjtr3NY

— Danny Polishchuk (@Dannyjokes) March 4, 2026

Senator John Kennedy lays out his three key points on the Iran conflict…and it quickly turns into a stand-up routine.

— Overton (@overton_news) March 4, 2026

KENNEDY: “Sean, in the words of Congresswoman Omar — I love you like a brother.”

“And I want you to understand I’m not trying to dodge your question, but I… pic.twitter.com/w8Qrgqkz5o

https://twitter.com/ivan_8848/status/2029139145168183437?s=20 https://twitter.com/GreereMedeea/status/2028870849718108499?s=20New infographic! The U.S. simply can't produce enough air defense munitions to keep up with Iran's domestic production. Within 1-2 weeks, everything changes as U.S. munitions run out… pic.twitter.com/UCI8ESm7LN

— HealthRanger (@HealthRanger) March 3, 2026

JOHN MEARSHEIMER: Iran isn’t going away. Even if this regime falls, the next won’t be friendly. With Ayatollah Ali Khamenei assassinated, the main brake on going nuclear is gone. The incentives for Iran to develop nuclear weapons are now much greater. pic.twitter.com/1Q8U1w3yCX

— The Resonance (@Partisan_12) March 3, 2026

They sold Britain. It is no longer a Christian nation. Prepare your kids.

• Keir Starmer Takes Cowardice to New Lows (Tim O’Brien)

To borrow a phrase from Foghorn Leghorn, when describing UK Prime Minister Keir Starmer, that boy is softer than a pound of wet leather, and he’s about as sharp as a bowling ball. Whether you agree strategically with the preemptive strikes against Iran by the U.S. and Israel, the reactions of the other developed nations have been a study in intelligence and loyalty on the part of their leaders. My colleague Catherine Salgado addressed this in her piece that focused on the reactions of Spain and Portugal reaction to the strikes: While Spain’s Prime Minister Pedro Sánchez was the most explicitly condemnatory, and forbade use of joint bases for the operation, Croatian Foreign Minister Gordan Radman, French President Emmanuel Macron, Finnish President Alexander Stubb, German Chancellor Friedrich Merz, Irish Taoiseach Micheál Martin, UK Prime Minister Keir Starmer, and the Slovenian government all more or less criticized the United States and Israel.Read more …

Times like this, you learn who your friends are and who isn’t bright enough to act in their countries’ best interests. Even if they’re still stinging from President Donald Trump’s tariffs—and in some cases, his public beatdowns—smart leaders know how to rise above all of that in this new context. A quick victory and resolution to the war with Iran can serve the West’s best interests on a number of levels, if handled right. Instead, we have a group of largely beta males who partly fear backlash from the Islamic populations in their countries, along with backlash from the Never Trumpers around the world. Some people will do anything to see Trump fail even if it means defending by default the evil and ruthless regime that has run Iran for the past 46 years.Keir Starmer stands out as a beta male’s beta male. He exudes cowardice—from that chronic deer-in-the-headlights look of fear, to his voice and its trademark trepidation, to a physical presence best described in one word: gooey. When G. Michael Hopf penned his novel Those Who Remain, it seems that he knew that a day would come when Starmer & Co. would arrive on the world stage when he wrote, “Hard times create strong men, strong men create good times, good times create weak men, weak men create hard times.” This week, we’re at the last phase of that sentence. Weak men like Starmer do create hard times.

If the U.S. and Israel are successful, now that hostilities are under way, the world has a chance to benefit by putting an end to the proxy wars and terrorism Iran has funded and orchestrated for decades, killing thousands of Americans. If Trump does what he said he’ll do, he’ll deal a final blow to Iran’s campaign to possess nuclear arms and the weaponry to strike the West with them. In that scenario, the whole world benefits. If that’s all Trump achieves, it’s a win. Smart world leaders can see that and will want to position themselves to be in Trump’s good graces if he succeeds. Leaders who aren’t too bright, or who act out of fear, will lose if he succeeds. This is Starmer’s “courageous” stand on the matter of deciding not to support the U.S. Speaking in Parliament, he called Trump’s efforts to prevent Iran from having nukes an “unlawful action.”

https://twitter.com/g_gosden/status/2028519334612529596

In his first official statement after the strikes against Iran, Starmer practically ran to the nearest podium and microphone to make it clear that he and his government “played no role in these strikes.”https://twitter.com/naijaamebonews/status/2027836993275576472

A real man in charge of a country like the UK would either openly support the U.S. in a situation like this or, if he disagreed with it, stay quiet while the situation is most volatile and give his ally a chance to take care of business. Instead, what Starmer did was to make sure the people he fears know that he’s not just distancing himself from the fighting, but running away from it. In doing this, he undermined the U.S, his supposed ally.He made it clear that he did not support any UK involvement in the attacks on Iran. He made it clear that his military would focus on defending itself and British installations.He decided on Sunday, the day after hostilities started, to give the U.S. permission to use its bases for certain operations. This was a change of course after it was reported that, prior to the operation, the UK had denied America’s request to use British bases in its Operation Epic Fury. In reaction to Starmer, Trump told the news media, “This is not Winston Churchill that we’re dealing with.” He said he was not happy with the Starmer, even though he eventually allowed the U.S. access to the base at Diego Garcia to mount strikes against Iranian missile facilities.

In a 24-hour period, Trump took the opportunity to let the world and Starmer know three times that Starmer’s initial rejection of American requests to use certain facilities had dealt a serious blow to U.S.-UK relations. Trump told the Sun that the “relationship is obviously not what it was,” and then he told the Telegraph that Starmer delayed giving the U.S. permission beyond what would have been reasonable. Trump suspects what everyone does at this point – that Starmer fears the Islamic community and is pandering to it, as he did here.

Donald Trump said earlier it was 'possible' Starmer was pandering to Muslims.

— Inevitable West (@Inevitablewest) March 3, 2026

12 hours later, here is he is holding a 'Westminster Hall iftar' telling the Muslim community that Britain was not involved in attacking the Iranian terror regime.

Donald Trump was right. pic.twitter.com/lHkSZVfqWO

Now, now, Jeff!!

• Jeffrey Sachs: ‘Trump Is An Utter Disgrace To Our Nation – He Lied To Us’ (ZH)

Columbia University economics professor Jeffrey D. Sachs appeared on Judge Napolitano’s ‘Judging Freedom’ podcast Monday, where he railed against the US-Israeli attack on Iran and the ‘CIA-led security state,’ calling President Donald Trump a ‘disgrace to our nation’ because ‘he lied to us.’Read more …

Sachs, a longtime critic of U.S. foreign policy, described the recent escalation as the continuation of a decades-old strategy he linked to Israeli and U.S. intelligence objectives dating back to 1996. “This is a long-term plan. This is a Mossad CIA plan for American control of the Middle East and Israeli military hegemony in the Middle East that has been underway since 1996,” Sachs said. “This is madness. This is murderous delusion.” The professor pointed to a series of U.S.-backed or U.S.-involved conflicts across the region, from Libya and Sudan to Somalia and the ongoing crisis in Gaza, as evidence of a consistent pattern aimed ultimately at confronting Iran.“It has involved wars across the Middle East. It has left rivers of blood from Libya to Sudan, Somalia, the genocide in Gaza,” he said, adding that Israeli Prime Minister Benjamin Netanyahu’s goal since the mid-1990s has been “the destruction of Iran.”= Sachs reserved some of his strongest language for Trump, whom he said reversed course on key foreign-policy pledges after taking office. “Trump… is an utter disgrace to our nation. Utter disgrace. He lied to us. Every word about America first… And he did exactly the opposite of what he said,” Sachs stated. The economist also criticized Washington’s approach to diplomacy more broadly, arguing that the United States has abandoned genuine negotiation in favor of coercive tactics. “The United States does not negotiate. It cheats… Now they kill you because if you negotiate, it means you’re weak,” he said.

On the domestic front, Sachs connected the country’s infrastructure challenges to the enormous costs of overseas military engagements.“Why do the roads not work and the bridges not work in the United States?… It’s because we spend trillions of dollars in war,” he said. “China just completed its 50,000th kilometer of fast rail because China doesn’t go to war.” Sachs concluded by expressing deep skepticism about the current state of American governance. “We’re in the hands of gangsters. We’re not in the hands of a constitutional system,” he said, noting that only a handful of lawmakers – citing Sen. Rand Paul (R-Ky.) as one example – have pushed back.

OK for now.

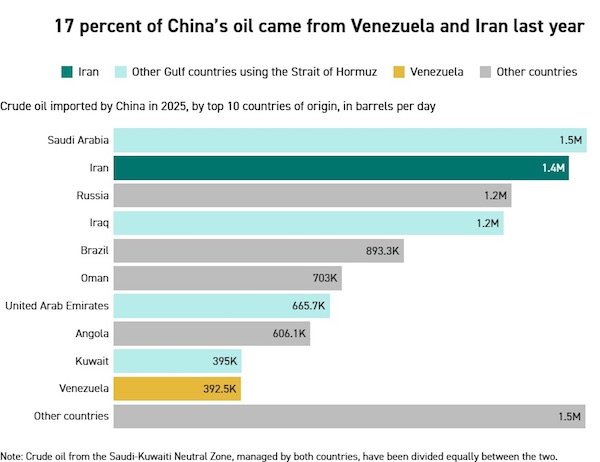

• Iran Conflict – Oil Disruption Hits Key BRICS Members Hard (CTH)

• First blow, the Trump tariffs hit Beijing hardest. • Second blow, the Beijing tentacle on the Panama Canal is severed. • Third blow, global tariff threats changed the risk dynamic for southeast Asia countries who acted as transnational shippers for China. • Fourth blow, cheap sanctioned oil from Venezuela was cut-off. • Now, the fifth blow; cheap, sanctioned Iranian oil is disrupted.Read more …

As noted by Politico: Following USA military strikes, “ships have begun to avoid the Strait of Hormuz off the coast of Iran — a critical shipping lane for Gulf nations to export oil to Asia. China in 2025 received about half of its imported oil from the six Gulf countries that rely on the strait. Other large crude oil producers in the region — including Saudi Arabia, Iraq and the United Arab Emirates — transport almost all their crude exports through the geographic bottleneck.”

It’s not just a factor of oil flow, but also the price that China will ultimately end up having to pay. Beijing was buying oil from Venezuela, Iran and Russia at steep discounts because their purchases were skirting western sanctions. With Iranian oil production now no longer a market option, China will seek to replace their needs with more Russian alternative. However, that diversion means the oil India was purchasing from Russia will come at a higher price, and the refined final product that was exported by India will arrive to the European Union carrying an additional cost. Simultaneously, Vladimir Putin was asked about Russia’s lack of military support to Iran in response to the U.S. military action, to wit the Russian president noted the technical terms of their joint military agreements did not include Russia’s immediate involvement. In shorthand, Russia is busy and is not getting involved.Russia was/is partially dependent on receiving military supplies from Iran in exchange for oil transfers. The military component is reported to include drones from Iran for use in the Ukraine conflict. Now that exchange profile is shuttered. Taking Iran’s malign influence off the geopolitical chessboard is beginning to surface in major challenges to the BRICS assembly (Brazil, Russia, India, China, South Africa). Russia, China and India are impacted directly. The BRICS nations were skirting western oil sanctions by trading the commodity outside the petrodollar structure. However, President Trump now controls the flow of oil from Venezuela, and his administration controls the currency in which it is sold.

With Iranian oil removed from the non-petro supply chain, the only remaining non-petro oil producer is Russia – who is simultaneously hit with a loss in military hardware support. China may end up as a larger oil customer to Russia, but at what price and in what payment structure. With global oil supplies in a state of flux, and with the USA in control of the oil flow from Venezuela, North America is certainly in the best position for minimal energy disruption. Asia is heavily dependent on oil flows through the Strait of Hormuz, and the majority of Europe has already shut themselves off from Russian oil production, putting themselves in a position of dependency to the global markets. The short-term ramifications of this oil disruption hit China, Southeast Asia, Japan and Europe particularly hard.

“OPEC+ countries affirmed on Sunday that they would boost oil production starting in April by 206,000 barrels daily — a modest increase intended to dampen the war’s effect on prices down the road. The majority of the increase would come from Saudi Arabia and Russia.” {SOURCE}

All of a sudden, this happens: Zelenskyy not to be trusted? “Ukraine is under pressure to let the EU inspect a damaged pipeline carrying Russian oil to Hungary and Slovakia, as the two pro-Kremlin countries accuse Kyiv of overstating the impact of an attack by Moscow — despite what Ukrainian officials say is evidence of extensive destruction,” the report said. According to five diplomats and EU officials who spoke to the FT, even pro- Ukrainian governments within the European Union and the European Commission have also asked Ukraine to permit a delegation to inspect the pipeline. Two sources told the newspaper that European Commission President Ursula von der Leyen requested access for EU experts during her visit to Kyiv on Feb. 24, the fourth anniversary of Russia’s full-scale invasion. The request, according to the sources, was refused.

As tensions escalated, the EU’s ambassador to Ukraine, Katarina Mathernova, reportedly asked through the presidential office for permission to inspect the damaged pipeline herself or to allow visits by other EU diplomats. Those requests were denied for security reasons, the sources said.” �

John Fetterman thinks for himself. Works for me.

• Fetterman Chooses Country Over Party After Iran Operation (David Manney)

Sen. John Fetterman (D-Pa.) backed the U.S. and Israeli strikes on Iran without hesitation, calling Operation Epic Fury entirely appropriate, and said eliminating Ayatollah Ali Khamenei, the un-alived supreme leader of Iran, removed one of the most dangerous figures in modern history.Read more …

President Donald Trump confirmed the mission targeted senior regime leadership gathered in Tehran, with early reports stating roughly 40 to 50 of the top Iranian officials were killed in the attack’s early wave. Fetterman didn’t hedge, asking why anybody would grieve leaders of a regime tied to terror networks and decades of repression. He said that Americans should recognize the strategic impact of removing the head of a government that funds violence across the world..@SenFettermanPA on killing of Iranian Supreme Leader Khamenei, after closed-door briefing: "The world is safer, and it's more just now…Why can't you just acknowledge that one of the most evil people on the face of the earth was erased? That's a good thing," pic.twitter.com/7s0AQx37EY

— CSPAN (@cspan) March 3, 2026

Fetterman’s stance again puts him at odds with several Democratic colleagues who questioned the legality and timing of the strikes. He described their reactions as bizarre. He pointed to the regime’s record, including the 1988 mass executions of political prisoners that killed an estimated 30,000 dissidents under orders tied to regime leadership, making clear the target wasn’t the Iranian people, just the regime. Vice President JD Vance stated that the administration’s objectives remain preventing Iran from acquiring nuclear weapons. Fetterman said he’d oppose efforts to restrict the president’s authority under the War Powers Resolution.Because Fetterman’s policy beliefs keep him planted firmly on the left, Fetterman won’t switch parties. But when national security comes into focus, he regularly breaks from progressive orthodoxy and takes a position rooted in deterrence and strength. In a chamber full of Congresscritters using scripted responses, his statements read as uncommon steadiness. Critics raised legal concerns, questioning whether the threshold for immediate military action had been met, while others argued Congress should’ve been consulted before the strike. Raise of hands: who envisions Schiff, Jeffries, and Swalwell would keep their pie holes shut?

Fetterman countered that Iran’s nuclear development and missile expansion represent a continuing threat, even if not tied to a single launch window, saying that waiting for perfect conditions invites greater danger.Israeli Prime Minister Benjamin Netanyahu led his country’s role in the coordinated strike, and Fetterman defended both Netanyahu and Trump against critics who labeled the attack as reckless. Fetterman argued that removing senior regime leadership weakens proxy forces such as Hezbollah. His position exposed a visible split inside his party, particularly among lawmakers who reflexively oppose any military action.

The broader debate now turns on escalation and authority. President Trump said the objective remains stopping Iran’s nuclear ambitions and restoring deterrence in the region. Lawmakers continue to argue over oversight and limits, but Fetterman’s remarks show that support for the strikes crosses party lines, even if only in narrow lanes. The result of Operation Epic Fury and how it will reshape the relations between the U.S. and Iran remains to be seen. What’s clear is that one Democrat senator chose to defend a strike he believes strengthens American and Israeli security, even when doing so separates him from much of his caucus. National security debates test whether lawmakers follow party currents or independent judgment. Fetterman, thankfully, chose judgment.

This will solve the economy at home. You just wait.

• Trump: US Insurance for “All Maritime Trade Flowing Through the Gulf”

This is a remarkable position for President Trump to take. Optimal Solutions: (President Trump) – “Effective IMMEDIATELY, I have ordered the United States Development Finance Corporation (DFC) to provide, at a very reasonable price, political risk insurance and guarantees for the Financial Security of ALL Maritime Trade, especially Energy, traveling through the Gulf. This will be available to all Shipping Lines.Read more …

If necessary, the United States Navy will begin escorting tankers through the Strait of Hormuz, as soon as possible. No matter what, the United States will ensure the FREE FLOW of ENERGY to the WORLD. The United States’ ECONOMIC and MILITARY MIGHT is the GREATEST ON EARTH — More actions to come. Thank you for your attention to this matter! President DONALD J. TRUMP“President Trump will use the full weight of the U.S. military to change behavior in Iran. Not just to change the regime per se’, but to change the behavior of whoever surfaces to represent the interests of the people. The change in behavior is the goal. While this forced shift is underway, the full weight of the USA will also seek to mitigate any collateral economic damage to well behaved economic partners. Forceful action, optimal stewardship.

This is a ballsy power play by Trump.

— Steve Skojec (@SteveSkojec) March 3, 2026

Lloyd's of London was the gold standard for maritime insurance policies until just a day or two ago when they started cancelling policies or jacking them up 3-5X. Others insurers followed. That collapsed commercial shipping traffic through… https://t.co/C2Oa6PhC63

“.. the first kill by a U.S. submarine since World War II. “

• US Sub Sinks Iranian Warship, First Such Hit Since WWII (Catherine Salgado)

A United States submarine successfully sank an Iranian regime warship, according to a Wednesday morning update from the secretary of war.The American submarine using a torpedo to sink an Iranian ship is particularly historic because, according to Secretary of War Pete Hegseth, this is the first such sinking of a ship since World War II. And just as the USA demanded unconditional surrender during World War II, Hegseth emphasized, now the U.S. is in it to win it again. The U.S.-Israeli joint Operation Epic Fury continues to claim prizes, including a warship named for the terrorist Iranian Islamic Revolutionary Guard Corps (IRGC) leader (Qasem Soleimani) whom Donald Trump eliminated during his first term and on behalf of whom the likewise assassinated Ayatollah Khamenei repeatedly vowed to assassinate President Donald Trump.Read more …

“The Iranian Navy rests at the bottom of the Persian Gulf,” Hegseth confidently announced. “[It’s] combat ineffective, decimated, destroyed, defeated, pick your adjective. In fact, last night, we sunk their prize ship, the ‘Soleimani’.” Soleimani was responsible for the deaths of hundreds of Americans and the wounding of thousands more. Not only is he dead thanks to the first Trump administration, but the second Trump administration even took out the ship named for him. As Hegseth joked, “Looks like POTUS got him twice.”Hegseth assured America and the world that the Iranian regime’s “navy is not a factor. Pick your adjective, it is no more.” He continued, “In fact, yesterday, in the Indian Ocean, and we’ll play it on the screen there, an American submarine sunk an Iranian warship that thought it was safe in international waters. Instead, it was sunk by a torpedo, quiet death.” That is particularly impressive because it represents the U.S. Navy’s “first sinking of an enemy ship by a torpedo since World War II. Like in that war, back when we were still the War Department, we are fighting to win,” Hegseth declared.

Trump insisted on restoring the name of the War Department to the Defense Department, and from Venezuela to Iran to Ecuador, the U.S. military has been pulling off spectacular operations ever since. What’s in a name? The difference between weakness and strength, it seems. The Iranian regime had assassins in the United States attempting to kill President Trump even before he came to office again, as they seemed to understand that his return to power would spell disaster for them, as it did. But Hegseth noted, “Also, yesterday, the leader of the unit who attempted to assassinate President Trump has been hunted down and killed. Iran tried to kill President Trump, and President Trump got the last laugh.”

Yeah yeah. Sure.

• Trump Denies Israel ‘Forced His Hand.’ (Salgado)

President Donald Trump and Secretary of War Pete Hegseth summarily demolished the argument from Jew-haters that the Israeli government forced the USA into a joint strike on Iran’s regime. Despite what Tucker Carlson, Candace Owens, Megyn Kelly, and the rest of the Jihad Squad claim, Israel didn’t strong-arm the United States into Operation Epic Fury. The Iranian terrorist regime brought it all upon themselves.The fact is that the late Supreme Leader Ayatollah Ali Khamenei and co. were treating this administration the way they have treated almost every U.S. administration over decades. They defied the U.S., funded the terrorists who attacked our troops and our allies, screamed “death to America” over and over, and demanded we lie down and take it.Read more …

But this time, it didn’t turn out the way it usually does. Unlike Barack Obama or Joe Biden, who rewarded Iranian jihad, Donald Trump grew tired of being pushed around. A reporter asked Trump during a press conference if Israel “forced” his hand on the Operation Epic Fury strikes. Trump coolly replied, “No, I might have forced their hand. You see, we were having negotiations with these lunatics, and it was my opinion that they were going to attack first. They were going to attack. If we didn’t do it, they were going to attack first. I felt strongly about that.”Trump’s first priority and duty is to the American people. Democrats think we should always prioritize foreign terrorists, tyrants, and dictators, and that’s why they’re furious about this. Think of how much American money went to the Ayatollah’s regime through the hands of Democrats. At a certain point, America has to face reality about Islamic dictatorships and acknowledge that Muslim sacred texts have been commanding jihad against non-Muslims for some 1,400 years, and that the endless violence and conflict is not going to stop because of diplomacy. We have been at war with Iran’s regime for half a century, and eventually one government or the other must concede defeat.

Hence Trump observed, “And we have great negotiators, great people, people that do this very successfully, and have done it all their lives — very successful — and based on the way the negotiation was going, I think they were going to attack first. And I didn’t want that to happen.” Trump therefore preempted them with Operation Epic Fury, as Hegseth confirmed. “So if anything, I might have forced Israel’s hand,” Trump added. “But Israel was ready, and we were ready, and we’ve had a — a very, very powerful impact.”

Letitia, where did we go wrong?

• NY AG James Orders Hospital to Resume Gender-Transition for Minors (Turley)

In a rare and controversial move, New York Attorney General Letitia James has ordered a Manhattan hospital to resume offering gender-transition treatment to transgender youth. NYU Langone had discontinued such treatments after funding threats from the Trump administration. It is now caught between the proverbial rock (HHS) and a hard place (NYAG). Last year, President Donald Trump signed an executive order entitled “Protecting Children from Chemical and Surgical Mutilation,” seeking to restrict gender-transition treatment for people under 19. HHS then threatened hospitals with a cut off of federal Medicaid and Medicare funding for continuing such treatment for children.Read more …

Various European countries have also halted certain procedures after countervailing studies suggesting that the risks are too high. England’s National Health Service 2024 report on the subject, known as the Cass Report, found concerning evidence of harm for minors and inconclusive benefits. James threatened “further action” if NYU Langone does not defy the Trump Administration, declaring that the cessation of its Transgender Youth Health Program violates New York anti-discrimination law by “jeopardizing access to medically necessary healthcare for some of the most vulnerable New Yorkers.” NYU Langone had previously declared that it would no longer provide certain gender-transition treatments for patients under the age of 19.James’s move could trigger a fascinating challenge. In the Feb. 25 letter signed by the attorney general’s health care bureau chief, Darsana Srinivasan, the state said that the federal regulatory change did not affect a “medical institution’s existing duties and obligations under New York law.” That raises an interesting conflict between state and federal regulations.The letter gives the hospital until March 11 to comply and resume these treatments. Effectively, James is ordering the hospital to defy the federal government. However, the hospital, not James or the state, would bear the financial and regulatory consequences.

While James does not state how she will penalize the hospital, the letter is likely sufficient to challenge the move. The question is whether the political costs for the NYU hospital are prohibitive. There is also the question of whether the HHS has standing or interest in challenging the move as a direct threat to federal authority. The problem with a federal challenge is that nothing in the New York threat prevents the federal government from carrying out its intent to cut off funding. Hospitals would have to choose between penalties in New York or loss of funding in Washington. Nevertheless, New York’s move is a direct attack on the enforcement of federal policy by state hospitals.

The first ever openly gay Treasury Secretary is loyal to a T. He’s also very good at what he does.

• Trump’s 15% Global Tariff Will Take Effect This Week: Bessent (ET)

President Donald Trump’s 15 percent global tariff will take effect sometime this week, Treasury Secretary Scott Bessent said. Following the Supreme Court’s rebuke of the president’s signature economic policy last month, Trump imposed a 10 percent global tariff, invoking Section 122 of the Trade Act of 1974. A day later, Trump pledged to raise the rate to 15 percent. In an interview with CNBC’s “Squawk Box” on March 4, Bessent confirmed that the new rate would be introduced sometime this week and remain in place for 150 days. He also anticipates tariff rates would return to the levels that were in place before the high court’s decision. “It’s my strong belief that the tariff rates will be back to their old rate within five months,” Bessent said.Read more …

“They have survived more than 4000 legal challenges. They are more slow moving, but they are more robust.” Bessent’s comments come two days after a U.S. federal appeals court rejected the president’s effort to postpone legal proceedings connected to tariff refunds, sending the battle to a lower court. Estimates suggest the federal government’s tariff refunds could total $175 billion. Fiscal year-to-date, the administration’s tariffs have generated more than $150 billion, according to Treasury data as of March 2. Global energy markets have been highly volatile since the Iran War, with crude oil and natural gas prices rocketing on fears of supply disruptions.The president calmed down the oil market on March 3. In a Truth Social post, Trump said the White House would offer naval escorts and guarantee political risk insurance for commercial oil and gas tankers traveling through the Strait of Hormuz. The Strait of Hormuz is a vital global chokepoint that handles approximately 20 million barrels of oil and petroleum products per day. It has effectively been shuttered as insurance companies canceled coverage or dramatically raised premiums. But the administration will make additional announcements to help stabilize prices, Bessent said. n“We have a series of announcements that we’re going to be making,” Bessent stated.

“We began yesterday with the announcement that [Development Finance Corporation] will provide the insurance for both the crude carriers and the cargo ships operating in around the Gulf over the weekend.” He shrugged off a possible energy shock as the Middle East conflict intensified, saying that the United States and the global marketplace maintain ample supplies. “This was a well telegraphed geopolitical event. The crude market had already moved substantially over the past two months. The crude markets are very well supplied,” Bessent said. A barrel of West Texas Intermediate—the U.S. benchmark for oil prices—fell by about 0.5 percent in pre-market trading to around $74 on the New York Mercantile Exchange.

Brent—the international benchmark—was little changed at slightly above $81 a barrel on London’s ICE Futures exchange. “Oil prices retreated after news the U.S. will ensure safe passage through the Strait of Hormuz, easing fears of a major global supply shock,” Adam Turnquist, chief technical strategist for LPL Financial, said in a note emailed to The Epoch Times. “Softer oil prices are also helping cool inflation concerns and pull interest rates lower.” Market watchers had warned that the risk of oil prices reaching $100 were high if the narrow waterway were closed for an extended period. U.S. stocks also rebounded midweek, with the leading benchmark averages in the green prior to the opening bell.

… the 3:00 minute mark of the video

• Bessent Outlines U.S. Financial/Economic Stabilization Plan (CTH)

Treasury Secretary Scott Bessent appears on CNBC to discuss the Trump administration policies that were proactively deployed during Operation Epic Fury. The goal of global financial stabilization is actually part of the strategic planning within the White House, including Treasury, Energy and Interior in alignment with the State Dept., Pentagon and national security agencies. Part of that plan was the announcement for the U.S. to underwrite maritime insurance to ensure a minimal disruption to the global energy markets. Secretary Bessent discusses the insurance facet at the 3:00 minute mark of the video below.Read more …

Wasn’t this Walz figure part of the Kamala cloud posse in the 1800s? Losers cling together, right?

• Walz, Ellison Knew About Minnesota Fraud ‘for Years,’ House Report (DS)

Minnesota Gov. Tim Walz was aware of the widespread welfare fraud in his state “for years” and “repeatedly failed to act,” alleges a congressional report released on Wednesday. Walz and the state’s Attorney General Keith Ellison are set to testify Wednesday about the $9 billion scandal before the House Oversight and Government Reform Committee. The report, which also alleges that Ellison knew of the welfare fraud in Minnesota, draws from interviews with state employees and whistleblowers. “Senior officials in the governor’s office and Attorney General Ellison’s office were aware of credible fraud concerns in Minnesota’s social services programs as early as 2019 within the Department of Human Services (DHS) and by April 2020 within the Department of Education (MDE), despite later public statements by Governor Walz suggesting otherwise,” the report says.Read more …

The committee and staff conducted transcribed interviews with nine key current and former Minnesota state officials. The investigation focuses on alleged money laundering and fraud in Minnesota’s social services programs, uncovered by the U.S. Attorney’s Office for the District of Minnesota. The report, titled “The Cost of Doing Nothing,” further alleges retaliation against whistleblowers, including surveillance, and quotes some officials as not acting against suspected fraud out of fear of being labeled a racist. “As a result, potentially billions of American taxpayer dollars were allowed to flow to fraudulent actors, while vulnerable populations were harmed and whistleblowers were ignored, sidelined, and retaliated against,” the House report says.This led to about $300 million in federal child nutrition funds and potentially $9 billion in Medicaid-related funds lost or placed at significant risk, according to the report. “Testimony obtained by the committee reveals that Governor Tim Walz and Attorney General Keith Ellison were aware of widespread fraud in social service programs, lied about their knowledge of the fraud, and retaliated against employees who dared to raise concerns,” House Oversight Chairman James Comer, R-Ky., said in a statement. The report also alleges whistleblower retaliation against state employees who raised red flags at the Minnesota Department of Human Services.

“Whistleblowers within the DHS have alleged that Governor Walz not only knew about this fraud, but that he retaliated against whistleblowers, ‘spen[ding] millions on surveilling staff and hiring private investigator (sic) or law firms to silence staff,’” the report says. The agency’s then-temporary commissioner confirmed to investigators that the agency “used outside entities” to investigate its own staff, according to the report. “Instead of protecting vulnerable Americans, they handed over billions in taxpayer dollars to fraudsters and threw their own state employees under the bus,” Comer added. “Governor Walz and Attorney General Ellison are appearing before the committee because the American people deserve clear answers about how this rampant fraud was allowed to flourish under their watch.”

“The state accused the government of weaponizing the Medicaid program as ‘political punishment.’”

• Minnesota Sues Federal Government Over Medicaid Funding Freeze (Aldgra Fredly)

Minnesota filed a lawsuit on March 2 to block the federal government from withholding $243 million in Medicaid funds, saying the freeze could lead to potential cuts in medical services for low-income individuals. The Centers for Medicare and Medicaid Services (CMS) last month temporarily deferred $259 million in Medicaid funds to Minnesota over alleged fraud in the state’s program, according to the court filing. The lawsuit, filed by Minnesota Attorney General Keith Ellison and the state’s Human Services Department, asked the court to block the withholding of $243 million of those funds that were tied to 14 services the government identified as “high-risk” and subject to “noncompliance action.”Read more …

“These cuts are the latest in a long series of efforts to go around the law to punish Minnesotans — but just as we fought back and won when they illegally tried to cut funding for childcare, hungry families, and our schools, we are suing them again today to make them follow the law,” Ellison said in a statement. The suit called the funding freeze unlawful, alleging that the government used the program as “political punishment” against the state, citing its previous attempts to withhold other funding from the state, including funds tied to the Supplemental Nutrition Assistance Program (SNAP). According to the lawsuit, the federal government announced in January that it would freeze more than $2 billion in annual Medicaid funding to Minnesota over allegations of noncompliance.The state appealed but said the federal government has not clarified the alleged conduct it deemed noncompliant or how Minnesota can remedy the issue. n “Impatient that it cannot withhold the $2 billion until Minnesota is provided a hearing and other due process, the administration ‘deferred’ $243 million from the state on February 25, 2026,” it stated.The lawsuit is seeking a temporary restraining order to block the funding freeze, saying the withholding of funds would affect more than 1 million Minnesota residents enrolled in Medicaid.

“Unless the deferral is quickly reversed, the state will be irreparably harmed. The administration has already stated that the deferral will recur every quarter, crippling the state budget,” it stated. The lawsuit names the Department of Health and Human Services and the Centers for Medicare and Medicaid Services, as well as Dr. Mehmet Oz, in his official capacity as CMS administrator, and Robert F. Kennedy Jr., in his official capacity as health secretary.

Problems? You suck!

• SCOTUS Decision Highlights Problems with Parents in Blue States (Turley)

In the law, the concept of In loco parentis refers to those who act in the place of parents. The problem is when that authority is taken rather than granted. It is a growing problem in blue states as parents push back on Democratic measures stripping them of notice or consent over their children in public schools. In the last few months, Democrats have been buoyed by protests over immigration enforcement. Many politicians have fueled a wave of rage sweeping major cities before the midterm elections, denouncing law enforcement as “Gestapo” and “Nazis.”Read more …

However, a Supreme Court decision this week may lay bare an even greater threat to Democratic aspirations over parental rights. For many parents, blue states are attacking the most fundamental right of citizens in raising their own children. This week, the Supreme Court granted an emergency appeal filed on behalf of Catholic parents in California. The order in Mirabelli v. Bonta proved a decisive victory for parental rights and an equally notable defeat for California democrats.The action, filed by the Thomas More Society, challenged a policy under a state law, signed by Gov. Gavin Newsom in 2024, that prevented teachers from notifying parents of their children’s gender identity changes. The law was heralded as a protection against the “outing” of transgender students. Some of us have been following the litigation since the original filing and heralded the decision of District Court Judge Roger Benitez, who wrote a powerful opinion in support of the rights of all parents. However, the United States Court of Appeals for the Ninth Circuit stayed his injunction.In issuing the order on its “shadow docket,” the Court delivered a key win for parental rights that many of us have been seeking for years.

Blue state legislators and educators have been waging a war on parental rights, particularly in the area of transgender policies. Recently, in Michigan, parents sued to defend their rights after the Rockford Public School District refused to inform them of gender identity changes in their children. Last year, I wrote about a startling decision in Foote v. Feliciano in which the United States Court of Appeals for the First Circuit ruled against Massachusetts parents Marissa Silvestri and Stephen Foote seeking such notice. As in the California case, they learned that school administrators did not inform them that their 11-year-old child had self-declared as “genderqueer” and that teachers and staff were using a new name and new pronouns for the student.

The First Circuit dismissed the right of parents over their own children in the case, holding that “as per our understanding of Supreme Court precedent, our pluralistic society assigns those curricular and administrative decisions to the expertise of school officials, charged with the responsibility of educating children.” Foote was a chilling decision that reflected the view of state officials that parents give up their rights over their children when enrolling them in public schools. That view was evident in the comment of State Rep. Lee Snodgrass (D-Wis.), who once tweeted: “If parents want to ‘have a say’ in their child’s education, they should home school or pay for private school tuition out of their family budget.” [..]

4 years of nothing.

• Ukraine Blocks EU Mission To Inspect Russian Oil Pipeline – FT (RT)

Ukraine has rejected a proposed EU mission to inspect the Soviet-era pipeline that transports Russian oil through Ukrainian territory to Central Europe, the Financial Times reported on Tuesday, citing diplomats and officials. Hungary and Slovakia have accused Ukraine of deliberately blocking the flow through the Druzhba pipeline, while Ukraine said the infrastructure was damaged by Russian strikes in January. The EU is pressuring Ukraine to restore the operation of the Soviet-era pipeline that transports Russian oil through Ukrainian territory to Central Europe, the Financial Times reported on Tuesday, citing diplomats and officials.Read more …

Hungary and Slovakia have accused Ukraine of deliberately blocking the flow through the Druzhba pipeline, while Ukraine claimed the infrastructure was damaged by Russian strikes in January. According to FT, some pro-Ukrainian EU member states and the European Commission are now asking Kiev to allow a visit to demonstrate that it is working to restore oil flows. Last week, European Commission President Ursula von der Leyen and European Council President Antonio Costa personally requested access to the pipeline for inspection but were denied, FT said.One of the newspaper’s sources argued that by blocking the inspection, Ukraine scored an “own goal” and gave Hungary an excuse to veto the planned $106 billion emergency loan for Ukraine and the EU’s 20th round of sanctions against Russia.In a post on X on Tuesday, Hungarian Prime Minister Viktor Orban said he had sent a letter to von der Leyen calling for enforcement of the EU-Ukraine Association Agreement, which “obliges Ukraine to allow oil shipments to Hungary.” “As confirmed by recently published satellite evidence, there is no technical or operational reason preventing the pipeline from reverting to normal operations immediately,” Orban stated. nmOrban said that Hungary and Slovakia had proposed dispatching a “fact-finding mission” to inspect the pipeline, but their “efforts were rejected.”

In August, Hungary imposed sanctions on Ukraine’s top drone commander Robert Brovdi after attacks on sections of the Druzhba pipeline in Russia. Ukrainian leader Vladimir Zelensky has called on Hungary to stop purchasing energy from Russia. Reuters reported on Tuesday that some EU members, including France and Germany, oppose the idea of granting Ukraine fast-tracked accession to the bloc, citing “rampant corruption.”

https://twitter.com/AndrewBolis/status/2029168756661039225?s=20 https://twitter.com/Juliedonuts/status/2029187803414671858?s=20 https://twitter.com/HungaryBased/status/2028915815525781828?s=20

https://twitter.com/AstronomyVibes/status/2029110904508547240?s=20Saturn's north pole is a perfect hexagonal storm!

— Black Hole (@konstructivizm) March 3, 2026

Earth is about 12,700 km wide. This hexagon is nearly 30,000 km across. You could drop two whole Earths inside this storm and they still wouldn't touch the sides. A geometric masterpiece raging at the top of the world.

NASA pic.twitter.com/r9e3DfAkds

Scientists have identified strong evidence for a vast quantity of water located roughly 400 miles (about 660 kilometers) beneath Earth’s surface, within the planet’s mantle. This water is not present as underground lakes or flowing reservoirs. Instead, it is chemically bound… pic.twitter.com/O4OWhjEqx4

— Science girl (@sciencegirl) March 3, 2026

camouflage of leaf insects and orchid mantises

— Science girl (@sciencegirl) March 4, 2026

pic.twitter.com/g0lMkKhQdl

beautiful!pic.twitter.com/QLHcI79u8D

— istanbulmu9 ❦ (@istanbulmu9) March 4, 2026

Support the Automatic Earth in wartime with Paypal, Bitcoin and Patreon.