A few days ago, former Reagan Budget Director and -apparently- permabear (aka perennial bear) David Stockman did an interview (see below) with Stuart Varney at Fox -a permabull?!-, who started off with ‘the stock rally goes on’ despite a London terror attack and the North Korea missile situation. His first statement to Stockman was something in the vein of “if I had listened to you at any time after the past 2-3 years, I’d have lost a fortune..” Stockman shot back with (paraphrased): “if you’d have listened to me in 2000, 2004, you’d have dodged a bullet”, and at some point later “get out of bonds, get out of stocks, it’s a dangerous casino.” Familiar territory for most of you.

I happen to think Stockman is right, and if anything, he doesn’t go far enough, strong enough. What that makes me I don’t know, what’s deeper and longer than perennial or perma? But it’s Varney’s assumption that he would have lost a fortune that triggered me this time around. Because it’s an assumption built on an assumption, and pretty soon it’s assumptions all the way down.

First, that fortune is not real, unless and until he sells the stocks and bonds he made it with. If he has, that would indicate that he doesn’t believe in the market anymore, which is not very likely for a permabull to do. So Varney probably still has his paper ‘fortune’. I’m using him as an example, of course, of all the permabulls and others who hold such paper.

Presumably, they often also think they have made a fortune, and presumably they also think that means they are smart. But that begs a question: how can it be smart to put one’s money into paper that is ‘worth’ what it is today ONLY because the world’s central banks have been handed the power to save the ailing banks that own them with many trillions of freshly printed QE? And no, there can be no doubt of that.

And there are plenty other data that tell the story. The world’s central banks have blown giant bubbles all over the place. That’s where the bulls’ “fortunes” come from. They are bubble fortunes. It has nothing to do with being smart. And of course, as I’ve said many times before, there are no investors left to begin with, because you can’t be an investor if there are no functioning markets, and for a market to function you need price discovery.

Which is exactly what central banks have killed. No-one has one iota of a clue what anything is really worth, what the difference between ‘price’ and ‘value’ is. Stockman at one point suggests people should hold on to Microsoft, but does he really believe that Bill Gates will remain standing when everyone around him crashes? That tech stocks are immune to the impending crash for some reason? If true, that would seem to indicate that tech stocks represent real value while -virtually- no others do. Hard to believe.

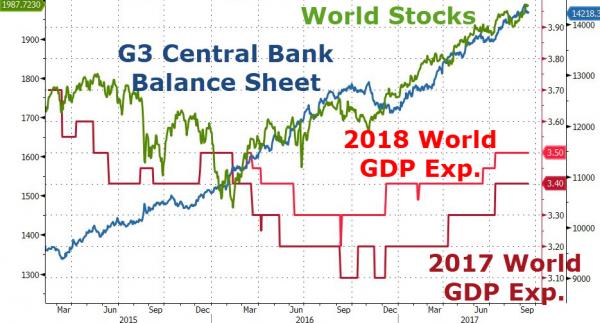

Please allow me to insert a graph. This one is from Tyler Durden the other day, and it paints a clear picture as much as it raises a big question. It suggests that until December 2016 the S&P and the ‘real economy’ were in lockstep. I think not. But one thing’s for sure: ever since January, i.e. the Trump presidency, the gaping gap between the two has grown so fast it’s almost funny.

Not that I would for one moment wish to blame Trump for that; he’s merely caught up in a wave much larger than an election or a White House residency. What is happening to the US -and global- economy goes back decades, not months. Which makes the graph puzzling, too, obviously. Just ask the new-fangled platoons of waiters and greeters with multiple jobs in America. And/or the 50-60-70% who can’t afford a $500 emergency bill, the 97 million who live paycheck to paycheck.. America’s already crashing, it’s just a matter of waiting for the markets to catch up with America’s reality. That’s what price discovery is about. Here’s another, similar, graph. Note: I don’t really want to go and find the best graphs, we’ve posted and re-posted so many of them it would feel like an insult to everyone involved.

But I digress. This was to be about Stuart Varney and the platoons and legions of permabulls out there. As I said, many of them, make that most, will feel they’ve made their fortune because they’re smart. Even if riding a Yellen and Draghi and Abenomics wave has zilch to do with intelligence. But there’s another side to that supposed smartness. And Stockman is on to it.

The large majority of people who think they got rich because they’re smart will also lose their ‘fortunes’ because they think they’re smart. It is inevitable, it’s a mathematical certainty. And not only because the central banks are discussing various forms of tapering. It’s a certainty because those who think they’re smart will hold on to their ‘assets’ too long. Because the markets will become much less liquid. Because the doors through which people will have to pass to escape the fire are too narrow to let them all though at the same time.

Fortunes built on central banks largesses are virtual. You have to sell your assets to make them real. But the same mechanics that blew the bubbles in housing, stocks, bonds et al also keep people from selling them. Until it’s too late. It may seem easier to sell stocks and bonds than homes, and it is, but in a crash it’s harder than one might think. And prices can come down very rapidly in very little time.

So perhaps the right way to look at this is to tell yourself you were not smart at all when you made that fortune, but now you’re going to smarten up. There will be a few people who do that, but only a few. Most will feel confident that they can see the crash coming in time to get out. Because they’re smart enough. After all, they just made a fortune, right?

It’s not just individuals. Pension funds have been accumulating huge portfolios in ever riskier ‘assets’. Which of them will be able to react fast enough if things start unraveling? And for the lucky few that will, what are they going to buy with the money? Bonds, stocks? Gold perhaps? Crypto? Everyone at once?

Don’t let’s forget that one of the main characteristics -and its consequences- of the everything bubble the central banks granted us is far too often overlooked: leverage. Low interest rates have made borrowing stupidly cheap, and so everyone has borrowed. As soon as things start crashing, there will be margin calls, lines of credit will be withdrawn, people and institutions will have to panic sell (everything including crypto) just to try to stay somewhat afloat, it’s all very predictable and we’ve seen it all before.

But yes, you’re right. The rally continues. And we can’t know what will trigger the downfall, nor can we pinpoint the timing. Still, it should be enough to know that it’s coming. Alas, for many it is not. They’re blinded by the light. But even that light is not real. It’s entirely virtual.

Austria won’t give fresh capital to Heta Asset Resolution making the “bad bank” of failed Hypo Alpe-Adria-Bank the first case under new European Union rules imposing losses on bank bondholders. Austria cut off support for Heta, which has already cost Austrian taxpayers about €5.5 billion in aid, after Heta notified the government it may need as much as €7.6 billion euros on top of that, the Finance Ministry said in a statement on Sunday. The Finanzmarktaufsicht regulator put Heta into resolution and ordered an immediate debt moratorium. “The decision was triggered by information from Heta’s management about the first results of an asset review,” the ministry said.

“Because of that dramatic change of the asset evaluation, the ministry together with the entire government decided not to invest any more tax money into Heta.” Heta’s predecessor Hypo Alpe was nationalized in 2009 after it was close to collapse because of bad loans in the western Balkans and shareholders led by Bayerische Landesbank walked away from the bank. Its rescue and wind-down has been complicated by a string of court cases and by the fact that a large part of its debt is guaranteed by the Carinthia province, a former owner of the bank. The FMA is taking over the wind-down of Heta, which kept around €18 billion of Hypo’s assets when it was set up last year.

While it works out a resolution plan it won’t repay Heta’s liabilities under an Austrian law that came into force Jan. 1 to implement the EU Bank Recovery and Resolution Directive, the authority said in a statement. The immediate debt moratorium means €950 million of bonds due March 6 and March 20 won’t be repaid. It affects €9.8 billion in outstanding bonds, supplementary capital and Schuldschein loans, €1.24 billion debt to Pfandbriefbank, a bank that handles bond issues for Austrian provinvial banks, as well as loans from BayernLB, according to the FMA’s decree published on its website.

The latest episode of Greece’s debt crisis has revived doubts about the long-term survival of the euro, nowhere more so than in London, Europe’s main financial center and a hotbed of Euroskepticism. The heightened risk of a Greek default and/or exit comes just as there are signs that the euro zone is turning the corner after seven years of financial and economic crisis and that its perilous internal imbalances may be starting to diminish. To skeptics, the election of a radical leftist-led government in Athens committed to tearing up Greece’s bailout looks like the start of an unraveling of the 19-nation currency area, with southern countries rebelling against austerity while EU paymaster Germany rebels against further aid.

A last-ditch deal to extend Greece’s bailout for four months after much kicking and screaming between Athens and Berlin did little to ease fears that the euro zone’s weakest link may end up defaulting on its official European creditors. U.S. economist Milton Friedman’s aphorism – “What is unsustainable will not be sustained” – is cited frequently by those who believe market forces will eventually overwhelm the political will that holds the euro together. Countries that share a single currency cannot devalue when their economies lose competitiveness, as occurred in southern Europe in the first decade of the euro’s existence. There is no mechanism for large fiscal transfers between member states.

So the only option has been a wrenching “internal devaluation” by countries on the periphery of the euro area, involving real wage, pension and public spending cuts and mass unemployment that has caused deep social distress. Austerity has fueled radical forces of political protest and may be running out of democratic road – not just in Greece – but none of the alternative ways out of the euro zone’s economic divergence dilemma looks remotely plausible. “The history of the gold standard tells us that an asymmetric adjustment process involving internal devaluation in debtor countries, with no corresponding inflation in the core, is unlikely to be economically or politically sustainable,” economic historians Kevin O’Rourke and Alan Taylor wrote in the Journal of Economic Perspectives in 2013. “What is desirable for the euro zone may not be feasible.”

“The Fed is out of control,” exclaims David Stockman – perhaps best known for architecting Reagan’s economic turnaround known as ‘Morning in America’ – adding that “people don’t want to hear the reality and the truth that we’re facing.” The following discussion, with Harry Dent, outlines their perspectives on the looming collapse of free market prosperity and the desctruction of American wealth as policymakers “take our economy in a direction that is dangerous, that is not sustainable, and is likely to fully undermine everything that’s been built up and created by the American people over decades and decades.” The Fed, Stockman concludes, “is a rogue institution,” and their actions have led us to “one of the scariest moments in our history… it’s a festering time-bomb and we’re not sure when it will explode.”[..]

David Stockman: People don’t want to hear the reality and the truth that we’re facing. But I think there is an enormous appetite out in the country to get a different perspective than what you have from the media day in and day out, so I say the fed is out of control. Its balance sheet is exploded. It’s printing money like never before. Zero interest rates for 70 months have basically destroyed the pricing function in the financial markets. I said that as a result of this, Wall Street has become a huge casino which basically rewards gamblers, but it is not functioning as a capital raising, capital allocating instrument, which really is what the financial markets should do in a free market system. I warned about the size of the federal debt.

I’m an old budget director from the Reagan days. We had a trillion dollar national debt, a 3 trillion economy when I started. Today, it’s 18 trillion. Eighteen fold gain in the last 35 years versus maybe a fourfold gain in the economy. So all of these trends are taking our economy in a direction that is dangerous, that is not sustainable, and is likely to fully undermine everything that’s been built up and created by the American people over decades and decades. So people don’t want to hear the warning. They don’t want to hear the truth in the establishment, in Wall Street, in Washington, but I think out in the country they must.

Last week we noted that with the start of Q€ just around the corner, the ECB finds itself in a rather absurd situation. In what we called the ultimate easy money paradox (or the ultimate Keynesian boondoggle), Mario Draghi and crew are doomed to trip over their own policies as they (literally) attempt to monetize twice the net supply of eurozone fixed income this year. The problem is two-fold: 1) the central bank’s adventures in NIRP-dom mean anyone willing to sell their EGBs would face the truly silly prospect of sending the proceeds right back where they came from, except at a cost of 20 bps (negative deposit facility rate), and 2) because the central bank’s easy money policies have compressed credit spreads, sellers who wanted to reinvest the cash they would theoretically receive for their EGBs would have to do so at ridiculously low rates, a scenario that would compound QE’s already negative effect on NIM for banks and would be absolutely untenable for insurers.

So what we have “is one deflation-fighting policy stymying another [and] the central bank’s previous efforts to drive down rates thwarting its current plans to … drive down rates.” Now, courtesy of Citi’s Matt King, it’s our distinct pleasure to present yet another wonderfully ridiculous paradox inadvertently created by central banks who apparently aren’t capable of understanding when they’re just pushing on a string: manufactured deflation or, more poignantly, just what the doctor did not order. Here’s Citi:

It’s that linkage between investment (or the lack of it) and all the stimulus which we find so disturbing. If the first $5tn of global QE, which saw corporate bond yields in both $ and € fall to all-time lows, didn’t prompt a wave of investment, what do we think a sixth trillion is going to do? Another client put it more strongly still. “By lowering the cost of borrowing, QE has lowered the risk of default. This has led to overcapacity (see highly leveraged shale companies). Overcapacity leads to deflation. With QE, are central banks manufacturing what they are trying to defeat?”

Ultimately, the question is whether the ceaseless printing of money is actually creating any demand, and for King, the answer is pretty clearly “no”: “QE, and stimulus generally, is supposed to create new demand, improving capacity utilization, not reducing it. But … it feels ever more as though central bank easing is just shifting demand from one place to another, not augmenting it.”

Some central banks have cut interest rates into negative territory in an effort to eke out some economic growth, but the step could spur unintended, counterproductive outcomes. “Negative rates could backfire,” Francesco Garzarelli, co-head of macro markets research at Goldman Sachs, said in a note Friday. “At least some segments of the population could feel poorer, and less secure,” he said. “Rather than lifting consumption and borrowing, ultra-loose monetary policy could perversely lead to an increase in precautionary savings and a slower economic recovery.” In an effort to ward off potential deflation and bolster nearly flat-lined economic growth, some central banks – including the ECB, the Swiss National Bank and central banks in Sweden and Denmark – have cut rates into negative territory.

A big chunk of the government bond market has gone negative: JPMorgan estimated that in January, around $3.6 trillion worth of developed market government bonds—or 16% of its Global Bond Index—was at a negative yield. That’s something that can spur new problems, Goldman said, noting concerns that pension funds and insurance companies may struggle to meet guaranteed payouts. “Today’s very low or even negative fixed income yields often are not large enough to match future liabilities,” Goldman said, noting insurance companies are generally assuming forward rates will be positive and above current rates. If low or negative yields persist, making guaranteed products work will become increasingly difficult, it said. In addition, if banks’ profitability takes a hit from negative rates, it could actually discourage bank lending, hurting efforts to revive economic activity, Goldman said.

There’s also the risk of asset bubbles forming, Garzarelli said, adding the risk is especially high for “high duration” assets such as technology stocks and high-dividend-paying stocks, which already have “eye-watering” valuations. Others also believe ZYNY, or zero-yield to negative-yield, may not follow the theoretical playbook in the real economy. “Traditional economic theory suggests that low interest rates will encourage households to borrow more, both to acquire housing and also to favor present consumption over future consumption,” Michala Marcussen at SocGen said in a note dated Sunday. But in practice, it may not work as households are already relatively highly indebted, labor markets remain fragile and regulations have become more demanding, she said. “Indeed, households may even opt to save more to compensate for low yields, and all the more so in ageing populations,” Marcussen said.

Ironically, Ukrainians are spending like crazy just so they have things, and not a rapidly falling currency, in their hands. The Greeks do the opposite: they spend even less.

The agreement between the Greek government and its lenders, which was sanctioned by the Eurogroup last Tuesday, appears to be more of a respite and less of a sea change in the relationship between the two sides. The apparent confidence gap is bound to aggravate economic conditions and undermine talks on debt relief unless it is bridged fast. Refraining from adversarial statements is the least they can do at this point, especially some ministers. According to the latest revision of gross domestic product data, based on seasonally adjusted figures, the Greek economy shrank by a revised 0.4% in the last quarter of 2014 compared to the previous quarter as opposed to a 0.2% drop in the flash estimate. This brought the real GDP growth rate to 0.75% for the whole year, still better than earlier forecasts, ranging between 0.4 and 0.6%.

Political uncertainty appears to have taken its toll as households and businesses cut back on spending. Unfortunately, businessmen and others think this trend has continued in the first months of 2015. If they are right, real GDP will dip again in the first quarter of this year, compared to the last one in 2014. This will make it unlikely to reach the budget goal of 2.9% annual growth in 2015. Moreover, international investment banks and others are downgrading this year’s economic growth forecasts, ranging between 0.6 and 2%. With the consumer price index continuing to decline, the prospects for an end to deflation do not look promising at this point. In the 12-month period from February 2014 to January 2015, average prices as measured by the CPI decreased by 1.4% year-on-year.

Even if deflation settles closer to a 1% average decline, nominal GDP is likely to be little changed and may even shrink, assuming real economic activity disappoints. This is not a good omen for the sustainability of the Greek public debt, bankers and others point out. This is even more the case if one thinks the country’s official creditors will accept the government’s arguments and economic reality, lowering the target of the primary budget surplus to 1.5% of GDP for 2015. Readers are reminded that the surplus target has been set at 3% of GDP in the program for this year and 4.5% next year. The country is projected to pay about 6 billion euros, or more than 3% of GDP, in interest payments to its creditors in 2015. In other words, interest payments will exceed the likely primary budget surplus, adding to the public debt stock.

German finance minister Wolfgang Schaeuble has softened his hard-line attitude towards Greece, saying its new Left-wing Syriza government needs “a bit of time” but appears to be able to work towards resolving its debt crisis. “The new Greek government has strong public support,” Mr Schaeuble told German newspaper Bild am Sonntag. “I am confident that it will put in place the necessary measures, set up a more efficient tax system and in the end honour its commitments. You have to give a little bit of time to a newly elected government,” he told the Sunday paper. “To govern is to face reality.” Mr Schaeuble added that his Greek counterpart, Yanis Varoufakis, despite their policy clashes, had “behaved most properly with me” and had “the right to as much respect as everyone else”.

It was an abrupt change in tone for Mr Schaeuble, who has repeatedly exchanged jibes with Mr Varoufakis since the Greek election in January brought in an anti-austerity government. Ahead of Friday’s crucial parliamentary vote in Germany, where MPs voted overwhelmingly to extend Greece’s existing financial aid programme until June, Mr Schaeuble had warned that Greece would not receive “a single euro” until it meets the pledges of its existing €240bn bail-out programme. “If the Greeks violate the agreements, then they have become obsolete,” a visibly angry Mr Schaeuble said at a meeting on Friday to persuade German MPs to support the deal ahead of the parliamentary vote. “Mr Varoufakis had not done anything to make our lives easier,” he added. After German MPs voted for the four-month bail-out extension, which Mr Schaeuble insisted was not a new finance deal for the troubled country, Greece pledged to implement reforms and savings.

The nickname for the IMF in the markets is “It’s mostly fiscal”, reflecting the IMF’s view that when a country gets into trouble, the manifestation is a huge government budget deficit. And the cure involves spending cuts and higher taxes. That is exactly what happened in Greece. But there was a difference. In most cases, the traditional IMF medicine counter-balances fiscal tightening with a devaluation of the exchange rate. The idea is that as the fiscal tightening squeezes domestic demand and threatens to cause higher unemployment, then a more competitive currency encourages net exports. Essentially, exports fill the hole left by the retreating government But this was not possible in the Greek case because the country does not have its own currency – because it joined the euro.

The only way of compensating for this absence was to allow domestic deflation of prices to produce an “internal devaluation”. What a laugh! We learned in the 1930s that this does not work. Deflation is extremely slow and painful and, even if it succeeded in improving competitiveness, it would worsen the debt ratio because it reduces the money value of GDP (the denominator of the ratio). The result is that Greece is on the road to misery, with no obvious escape. Why don’t the Germans understand the logic of this argument? They tend to look at matters with regard to debt – and economic policy more generally – moralistically. The Greek public sector has been wasteful in the extreme and Greek taxpayers have treated paying tax as near-voluntary. Accordingly, they have had it coming to them.

When they reform themselves, then the economy will bounce back. I am speechless at this attitude. Yes, the Greek public sector has been appallingly wasteful and making it less so is an important part of boosting Greece’s sustainable growth rate. But the current priority is not that, but boosting Greece’s actual growth rate now – and that is all about demand. There is no such thing as a free spending cut. Even tax evaders and under-employed public servants go shopping. Why do the IMF and the other lenders persevere with this destructive path? The answer is IMP: “It’s mostly political.” That is to say, it is driven by the overriding will to keep the euro on the road. By now you should know my answer. Greece should come out of the euro and allow its new currency to depreciate sharply, perhaps by 30pc to 40pc.

A first eurogroup meeting to start the process broke up in acrimony. Mr Dijsselbloem tried again five days later but the ensuing bust-up proved even more spectacular: Mr Varoufakis marched out of the session accusing the Dutchman of reneging on a deal Athens had struck with Pierre Moscovici, the European Commission s economic chief. Mr Dijsselbloem blames the commission, which has typically been more lenient towards Greece than its other creditors, saying its intervention had short-circuited proper procedure and that he had been kept in the dark. The Greeks then thought they had an agreement, Mr Dijsselbloem said. I was not involved in that, and that s not very smart.

If you want to get an agreement with the eurogoup, it would help to inform me of what you re trying to do. Instead, Mr Dijsselbloem issued his own, far tougher proposal, which quickly leaked to the press. He put his head in his hands to mimic his reaction upon learning of the leak, presumably orchestrated by Mr Varoufakis. I know in politics it’s all about the frame and who gets to frame first, he said. But if you’re in such a delicate process, trying to rebuild trust, trying to get a process going, to then .. walk into the press room and say: Oh, these guys can’t be trusted, look what they re trying to push down our throats. That was just not very helpful.

A third and final eurogroup session was held the day after Athens finally sent its request for an extension, and Mr Dijsselbloem changed strategy. The key players in the debate were all present: the three institutions that monitor Greece s bailout (the commission, the European Central Bank and the International Monetary Fund) along with the Greeks and the Germans, to put it quite bluntly , Mr Dijsselbloem said. Each was brought in for pre-meeting negotiations. But instead of dealing with Mr Varoufakis, Mr Dijsselbloem spoke only to Mr Tsipras over the phone. I didn’t see Varoufakis at all that morning, he said. I didn’t speak to him. I said to Tsipras, this had to be it. And I think after 15 minutes he called me back, and there was one more word we managed to change. And that was it.

Greece’s anti-austerity government has denied that it sees Europe through the prism of “hostile and friendly countries” as the Spanish prime minister Mariano Rajoy hit back at accusations that Spain and Portugal had deliberately tried to topple the new leftist-led administration. The war of words erupted when Greek premier Alexis Tsipras attacked the sabotage tactics that had, he said, been employed by Lisbon and Madrid in an effort to scupper the chances of a successful end to the negotiations over the eurozone’s extension of the Greek bailout programme. He accused the Iberian partners of deliberately taking a hard line in the talks because they feared the rise of radical forces in their own countries.

“We found opposing us an axis of powers … led by the governments of Spain and Portugal which, for obvious political reasons, attempted to lead the entire negotiations to the brink,” Tsipras told party members on Saturday. “Their plan was, and is, to wear down, topple or bring our government to unconditional surrender before our work begins to bear fruit and before the Greek example affects other countries… And mainly before the elections in Spain.” Rajoy responded angrily on Sunday, saying that Spain had stood by Greece in solidarity by contributing to the debt-stricken country’s €240bn bailout. “We are not responsible for the frustration generated by the radical Greek left that promised the Greeks something it couldn’t deliver on,” he said.

Aides close to Tsipras insisted that Athens had little desire to “seek enemies abroad,” but the leftist leader had a duty to disclose the details of last month’s dramatic negotiations with creditors to keep the bankrupt country afloat. “Prime minister Alexis Tsipras was obliged to relate in detail to the Greek people the hard negotiations at the crucial eurogroup that led to the agreement,” said the insiders. “The attitude [shown by] governments towards the deal isn’t a secret – after all such views had become publicly known from the first moment, which is only right.”

Catalonia is preparing its own tax system, and creating a network of foreign missions as it prepares for a snap regional vote on independence. Recently Spain’s top court ruled that the region’s symbolic referendum vote in November was unconstitutional. Nationalist leaders in the northeastern region have urged a snap local vote on the issue of independence on September 27, AFP reported. Catalan president Artur Mas and his government are reportedly working on tax, diplomacy, and social security restructuring in case Catalonia becomes an independent state. The focus is on taxation as the Catalan authorities now collect only 5% of the taxes raised in the region.

Last November, Catalan president Artur Mas organized a symbolic vote on independence, with 80% voting in favor. However, the turnout was only 40%. Catalonia has 7.5 million residents (16% of Spain’s population), and represents some 20% of the country’s GDP. Alone, the region could collect €100 billion in taxes yearly, much more than Catalonia would need if it becomes independent, said Joan Iglesias, a former Spanish tax inspector, who is now behind the Catalan tax reform. “Everyone knows that Catalonia would be viable economically. It is the most economically productive territory in Spain,” Iglesias told AFP. Apart from the tax reform, Catalonia would need to establish its own central bank, upgrade computer systems and employ more civil servants.

Also, the region says it needs to open more foreign offices. Currently, Catalonia is represented in the UK, France, Germany, the US, Belgium and has recently set up missions in Austria and Italy. In February, Mas set up a commission responsible for carrying out the tasks essential for an independent state. Plus, he ordered a study into the steps Catalonia needs to take to make sure the services like telecommunications would function in case of secession. However, “work is advancing too slowly,” Catalan lawmaker with the separatist Esquerra Republicana de Catalunya (ERC) party, Lluis Salvador, told AFP. “We need to streamline our efforts so we arrive at the elections in September at a much more advanced state.”

Greek funding and quantitative easing in Europe, an expected rate cut in Australia and the buoyant U.S. labor market are set to be the focus of an economic week dominated by a host of central bank meetings. Greece may have secured an extension of its bailout last week, but it remains reliant on emergency funding.The European Central Bank’s Governing Council convenes in Cyprus on Thursday and may take a decision on whether to accept Greek government bonds as collateral for its direct ECB funding, which it stopped doing at the start of February.If the ECB does not – and it most likely will not – it could be forced to prolong the provision of Emergency Liquidity Assistance (ELA) to the Greek central bank.

“The Greek question will be a hot topic,” said ING Chief Eurozone Economist Peter Vanden Houte. “(Greek Finance Minister Yanis) Varoufakis has been saying the country is counting on the ECB for finances over the next few months.”ECB President Mario Draghi is also expected to provide further details on the bank’s €1 trillion government bond buying program, which begins in March. He may face questions about the program’s ability to reach its target, such as how the ECB intends to convince domestic banks to sell their government debt, with the prospect of then parking the money with the ECB at a negative interest rate. The ECB will also release new economic forecasts. Chief Economist Peter Praet said last week that it was likely to revise upward its expectations for growth in the euro zone, with low oil prices and a weak euro helping.

A leading member of German Chancellor Angela Merkel’s conservative allies in Bavaria has criticised the European Commission’s decision to give France two extra years to cut its deficit, a letter seen by Reuters shows. On Wednesday Brussels said it would give France until 2017 to bring its deficit below the EU limit of 3% of GDP, sparing Paris a fine and giving it a new grace period after it missed a second deadline to put its finances in order. The decision has been condemned by some euro zone policymakers, who said it undermines the credibility of EU budget rules which were tightened in recent years to prevent overspending and a future sovereign debt crisis. Gerda Hasselfeldt, head of the Christian Social Union (CSU) parliamentary group, wrote to European Commission President Jean-Claude Juncker in a letter dated Feb. 27 to say that the timing of Brussels’ decision left a “bad aftertaste”.

Hasselfeldt wrote: “Right now, at a time when we’re facing big challenges in our responsibility for the European Union and the euro zone and when we’re working on the principle of solidarity in return for solidity, it’s extremely important not to allow any exceptions.” She said the euro zone was vehemently urging Athens to stick to rules set by the Eurogroup of euro zone finance ministers despite significant domestic resistance, and that while she did not want to compare Greece with France, “stringent action” was the only way to ensure Europe and the euro zone remain credible. “We should not create the dangerous impression that we want to apply double standards,” Hasselfeldt said, adding that the same rules needed to apply to all countries whatever their size.

Dutch church bells that for centuries have tolled to warn of floods across the low-lying countryside are sounding the alarm for a new threat: earthquakes linked to Europe’s largest natural gas field. “Money can buy a lot of things, but a building like this cannot be replaced,” said Jur Bekooy, a civil engineer with the Groningen Old Churches Association, pointing to cracks in the ceiling and walls of the 13th-century Maria Church in the village of Westerwijtwerd. Long ignored, voices like Bekooy’s are being heard as elections loom this month and following a damning report from the independent Dutch Safety Board. It accused the government and the field’s operators, Shell and Exxon Mobil, of ignoring the threat of earthquakes linked to the massive Groningen gas field for years.

There are now questions about the future exploitation of the field that lies under the northern province of Groningen, with implications that reach well beyond its significance for Dutch state coffers. Lessons from Groningen, which lies far from any natural fault line, feed into a debate over the threat posed by hydraulic fracturing in the United States, China, Britain and elsewhere. The world’s 10th largest gas field, Groningen is expected to supply the bulk of the Netherlands’ annual gas needs of 20-30 billion cubic meters (bcm) until the mid-2020s. The Dutch also have contracts to sell 40-60 bcm annually to buyers in Germany, Britain, Italy, Belgium and France. In all, Groningen and a few smaller Dutch fields supply 15% of Europe’s gas consumption, providing one alternative to Russian supply. When Economic Affairs Minister Henk Kamp recently ordered production at Groningen cut by 16%, gas prices jumped across Western Europe.

Groningen has been in continuous production since 1963. As far back as 1993 small quakes were definitively linked to its output. But in the late 2000s, they suddenly became more frequent and stronger. With government finances under pressure from the 2008 financial crisis, production at Groningen had been ramped up from around 30 bcm in 2007 to more than 50 bcm by 2010. The money generated helped the Dutch cushion the blow of austerity policies championed by the Cabinet. As Prime Minister Mark Rutte publicly pressed southern European governments to bring their spending under control, Dutch government gas revenues of €15 billion by 2013 were about the size of the national deficit.

Without gas, the deficit that year would have doubled from 2.5% to 5%, violating eurozone budget rules. But on Aug. 16, 2012, an earthquake with its epicenter under the town of Huizinge marked the beginning of the end for aggressive output from Groningen. It registered 3.6 on the Richter scale, larger than any predicted by engineers at NAM, the joint venture field operator between Shell and Exxon. “Until the Huizinge earthquake, we had 1,100 damage claims in 20 years,” said NAM spokesman Sander van Rootselaar. “After the quake we had more than 30,000.” Earthquakes caused by gas production are usually small, unless they happen near a fault line and can trigger a larger natural quake. But in Groningen they occur close to the surface, damaging stone and brick buildings never designed to withstand shaking. Of the 50 churches located above the field, some 40 have been affected, said Bekooy.

Ukrainians are seeing signs the economy is cracking under the weight of war and the risk of default. While restaurants and cafes are bustling and shelves are full in Kiev, a city of 3 million, a recession stretching into a second year is igniting angst about the return of the disarray unleashed by the Soviet Union’s collapse in 1991. Especially outside the capital, that era of food shortages, hyperinflation and mass unemployment doesn’t seem so far away.= “My business is about to close and there are many more like it,” said Valentyna Lozova, a 65-year-old accountant in Kiev. “Salaries aren’t rising, inflation is galloping and the hryvnia’s in freefall. I’m afraid of the future.”

It’s becoming harder for Ukrainians, mindful of the thousands who’ve died in a 11-month insurgency near the nation’s border with Russia, to put a brave face on their economic woes. With much of the country’s industrial base in ruins and a looming debt restructuring, the effect may be felt for years. The economy is set to plunge 12% in 2014-15 and the inflation rate jumped to 28.5% in January, the world’s second-highest behind Venezuela. As the economy deteriorated, the hryvnia has sunk 70% in the past year, the most in the world, sparking panic in some towns. “I see people every day in supermarkets buying sacks of flour and cereals as prices grow,” said Iryna Lebiga, a 31-year-old mother of three who’s struggling to find a buyer for her unprofitable sheep farm in Poltava, a 350-kilometer (220-mile) drive east of Kiev. “People don’t have money. Someone approached us last year but my husband thought he offered too little. Now, nobody offers even half of that.”

Even in Kiev, some people were spooked into stocking up on staples after the central bank banned foreign-currency trading for one day last week and the hryvnia’s street price plunged. The Silpo supermarket chain rearranged delivery to its outlets to keep up with growing demand, its press office said in an e-mail. While the recession isn’t yet as deep as the last one in 2009, this contraction is longer-lasting and Ukraine entered it after two years of almost zero-growth. The scale of the malaise risks triggering disquiet among some Ukrainians who helped unseat their Russian-backed leader last year with the hope of rebuilding the nation, according to Citibank in Moscow.

Uruguay’s president, Jose “Pepe” Mujica, a former guerrilla who lives on a farm and gives most of his salary to charity, is stepping down after five years in office, ending his term as one of the world’s most popular leaders ever. Mujica, 79, is leaving office with a 65% approval rating. He is constitutionally prohibited from serving consecutive terms. “I became president filled with idealism, but then reality hit,” Mujica said in an interview with a local newspaper earlier this week, according to AFP. Some call him “the world’s poorest president.” Others the “president every other country would like to have.” But Mujica says “there’s still so much to do” and hopes that the next government, led by Tabare Vazquez (who was elected president for a second time last November) will be “better than mine and will have greater success.”

Mujica said he succeeded in putting Uruguay on the world map. He managed to turn the cattle-ranching country, home to 3,4 million people, into an energy-exporting nation, Brazil being Uruguay’s top export market (followed by China, Argentina, Venezuela and the US.) Uruguay’s $55 billion economy has grown an average 5.7% annually since 2005, according to the World Bank. Uruguay has maintained its decreasing trend in public debt-to-GDP ratio – from 100% in 2003 to 60% by 2014. It has also managed to decrease the cost of its debt, and reduce dollarization – from 80% in 2002 to 50% in 2014. “We’ve had positive years for equality. Ten years ago, about 39% of Uruguayans lived below the poverty line; we’ve brought that down to under 11% and we’ve reduced extreme poverty from 5% to only 0.5%,” Mujica told the Guardian in November.

After Latin America’s anti-drug war proved a failure, the South American country became the first in the world to fully legalize marijuana, with Mujica arguing that drug trafficking is in fact more dangerous than marijuana itself. One of the most progressive leaders in Latin America. Muijica also legalized abortion and same-sex marriage and agreed to take in detainees once held at the notorious Guantanamo Bay. Six former US detainees, who were never charged with a crime, came to Uruguay in December as refugees. The six included four Syrians, a Palestinian and a Tunisian. Although they were cleared for release back in 2009, the US was not able to discharge them until the Uruguayan President offered to receive them. Mujica, a former leftist Tupamaro guerrilla leader, spent 13 years in jail during the years of Uruguay’s military dictatorship. He survived torture and endless months of solitary confinement. Majica said he never regretted his time in jail, which he believes helped shape his character.

Millions of Chinese, riveted and outraged, watched a 104-minute documentary video over the weekend that begins with a slight woman in jeans and a white blouse walking on to a stage dimly lit in blue. As an audience looks on somberly, the woman, Chai Jing, displays a graph of brown-red peaks with occasional troughs. “This was the PM 2.5 curve for Beijing in January 2013, when there were 25 days of smog in that one month,” explains Ms. Chai, a former Chinese television reporter, referring to a widely used gauge of air pollution. Back then, she says, she paid little attention to the smog engulfing much of China and affecting 600 million people, even as her work took her to places where the air was acrid with fumes and dust.

“But,” Ms. Chai says with a pause, “when I returned to Beijing, I learned that I was pregnant.” She has said her concerns about what the filthy air would mean for her infant daughter’s health prompted her to produce the documentary, “Under the Dome.” It was published online Saturday, and swiftly inspired an unusually passionate eruption of public and mass media discussion. The newly appointed minister of environmental protection even likened the documentary to “Silent Spring,” Rachel Carson’s landmark exposé of chemical pollution. “I’d never felt afraid of pollution before, and never wore a mask no matter where,” Ms. Chai, 39, says in the video. “But when you carry a life in you, what she breathes, eats and drinks are all your responsibility, and then you feel the fear.”

By early Monday morning, “Under the Dome” had been played more than 20 million times on Youku, a popular video-sharing site, and it was also being viewed widely on other sites. Tens of thousands of viewers posted comments about the video, many of them parents who identified with Ms. Chai’s concern for her daughter. Some praised her for forthrightly condemning the industrial interests, energy conglomerates and bureaucratic hurdles that she says have obstructed stronger action against pollution. Others lamented that she was able to do so only after leaving her job with the state-run China Central Television.